Presentation Composed By: J ames W ang, L inda Y u, M ichael T ao, T ony L iu April 20, 2007.

11

Presentation Composed By: James Wang, Linda Yu, Michael Tao, Tony April 20, 2007

-

date post

20-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Presentation Composed By: J ames W ang, L inda Y u, M ichael T ao, T ony L iu April 20, 2007.

Presentation Composed By:James Wang, Linda Yu, Michael Tao, Tony Liu April 20, 2007

Please do not click on the screen at this moment

Online Video Growth

Viewing Habits

Age Groups

Males Online

Capturing the Market

Online Video Growth

Viewing Habits

Age Groups

Males Online

Capturing the Market

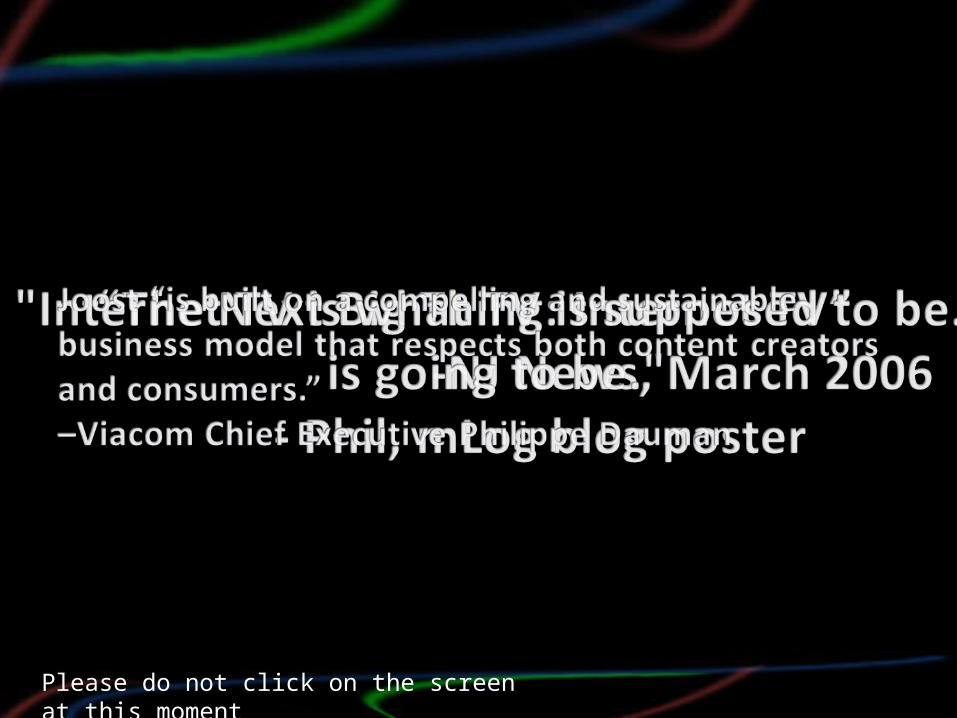

Data Analysis:Online video is growing rapidly as a share of total online advertising spending.

Joost will consequently benefit from this trend.

Data Analysis:Online video is reducing the time people spend on watching traditional television.

Similarly, Joost will cut heavily into TV’s market share.

Data Analysis:The largest viewer demographic for online videos is the age group 16 to 34.

Joost is expected to draw its viewers primarily from this demographic.

Data Analysis:This demographic is one of the most influential for online based services.

Additionally, this is the preferred market of television advertisers.

Data Analysis:The convergence of these factors creates an opportunity in the market which did not exist before.

Joost is uniquely situated to capitalize upon this opening.

Joost Background

About the Product

Benefit Analysis

Business Model

Joost Background

About the Product

Benefit Analysis

Business Model

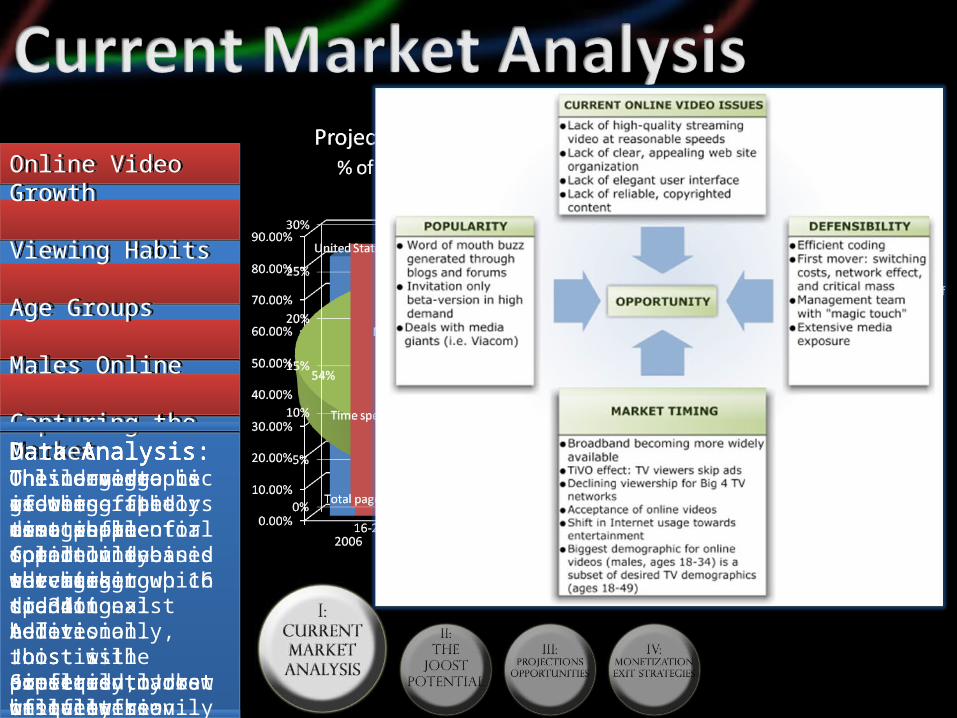

What is it?Free TV provided through the internet. It relies on partnerships with content distributors to provide programming. Additionally, it seamlessly incorporates internet features such as instant messaging and news feeds into the product.

The company, founded by Niklas Zennstrom and Janus Friis in early 2006, currently has 80 employees.

The next stepCurrently in Beta-version and only available by invitation. Expected to be widely available in the second quarter of this year.

Further improvements to online video sharing: -High quality video: Peer-to-peer sharing of files provides a network for sharing videos. This system eliminates up to one third of the bandwidth needed to download content.

-Ease of navigation: Channels organized both in list form and by category.

-Elegant design: Web applications integrated in an unimposing way.

-High quality, reliable content: Professional programming (i.e. MTV, National Geographic, BET, Comedy Central, etc.) provided by TV networks eliminates copyright issues.

Analysis:Joost takes advantage of the interactions between the parties exhibited to formulate a strong base for revenue growth.

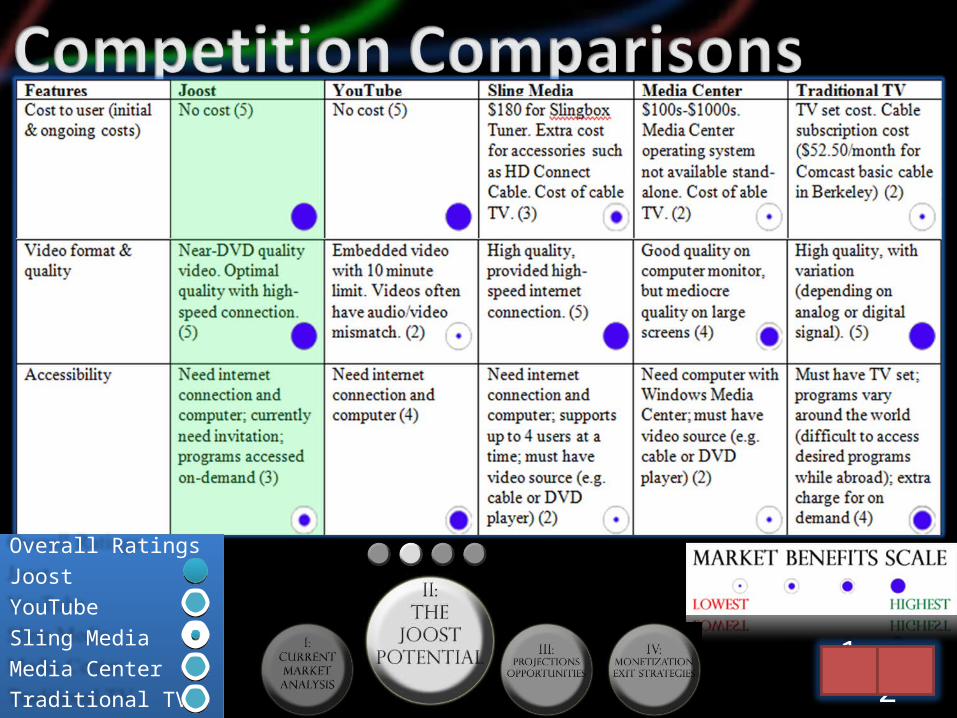

Overall Ratings

Joost

YouTube

Sling Media

Media Center

Traditional TV1 2

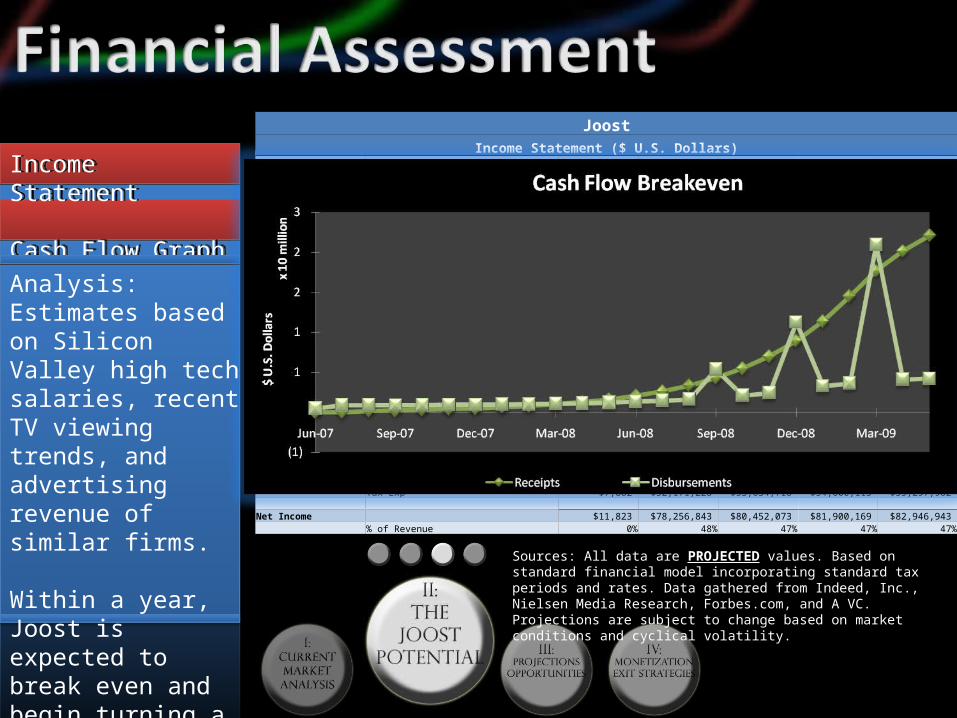

Income Statement

Cash Flow Graph

Income Statement

Cash Flow Graph

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Revenue

Joost $11,700,636 $164,717,797 $169,461,997 $172,828,060 $175,438,981

Product Two $0 $0 $0 $0 $0

Product Three $0 $0 $0 $0 $0

Services $0 $0 $0 $0 $0

Total Revenue $11,700,636 $164,717,797 $169,461,997 $172,828,060 $175,438,981

Cost of Goods Sold $759,700 $794,325 $785,881 $824,055 $864,138

Gross Margin $10,940,936 $163,923,472 $168,676,115 $172,004,004 $174,574,843

% of Revenue 94% 100% 100% 100% 100%

JoostIncome Statement ($ U.S. Dollars)

Operating Costs Engineering $5,848,411 $6,120,672 $6,406,545 $6,706,713 $7,021,888 % of Revenue 50% 4% 4% 4% 4%Marketing/Sales $3,541,757 $22,746,761 $23,421,538 $23,928,135 $24,344,632 % of Revenue 30% 14% 14% 14% 14%Administration $1,531,063 $4,627,968 $4,761,243 $4,868,874 $4,963,419 % of Revenue 13% 3% 3% 3% 3%

Total Operating Expenses $10,921,231 $33,495,401 $34,589,326 $35,503,722 $36,329,938 % of Revenue 93% 20% 20% 21% 21%

Income Before Int & Taxes $19,705 $130,428,071 $134,086,789 $136,500,282 $138,244,904 % of Revenue 0% 79% 79% 79% 79%

Income Before Taxes $19,705 $130,428,071 $134,086,789 $136,500,282 $138,244,904

Tax Exp $7,882 $52,171,228 $53,634,716 $54,600,113 $55,297,962

Net Income $11,823 $78,256,843 $80,452,073 $81,900,169 $82,946,943 % of Revenue 0% 48% 47% 47% 47%

Analysis:Estimates based on Silicon Valley high tech salaries, recent TV viewing trends, and advertising revenue of similar firms.

Within a year, Joost is expected to break even and begin turning a profit.

Sources: All data are PROJECTED values. Based on standard financial model incorporating standard tax periods and rates. Data gathered from Indeed, Inc., Nielsen Media Research, Forbes.com, and A VC. Projections are subject to change based on market conditions and cyclical volatility.

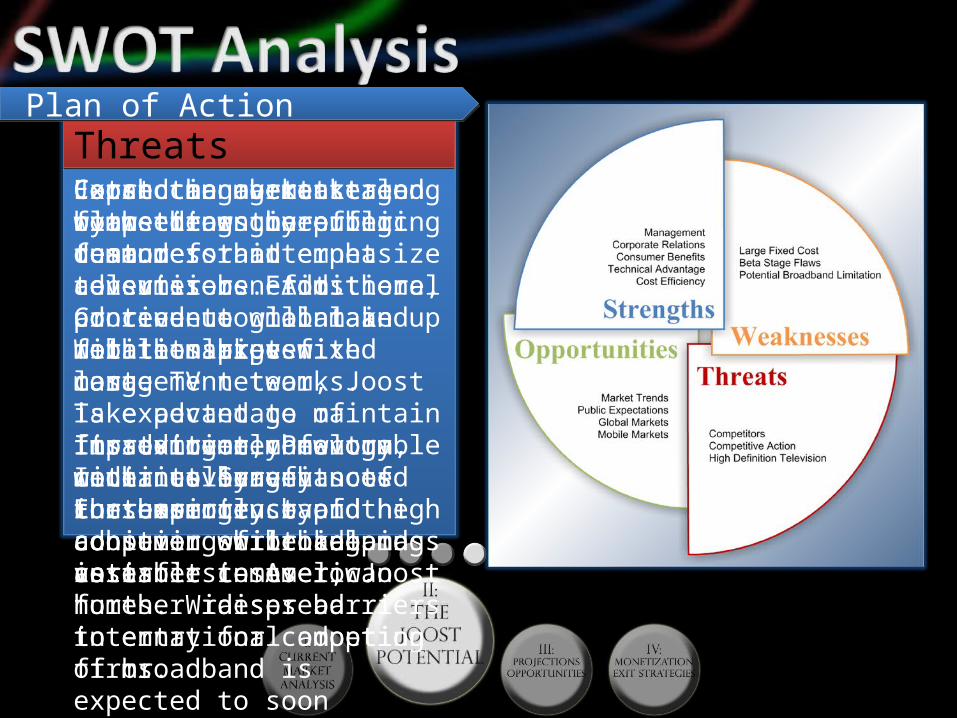

StrengthStrengthOpportunitiesOpportunitiesWeaknessesWeaknessesThreatsThreatsJoost can overtake competitors by offering features that emphasize consumer benefits.

With its proven management team, Joost is expected to maintain its extremely favorable media coverage. Furthermore, by achieving critical mass as a first-mover, Joost further raises barriers to entry for competing firms.

Correcting beta stage flaws draws more customers and advertisers. Additional ad revenue will make up for the large fixed cost.

In addition, Pew Internet Survey noted increasingly rapid adoption of broadband internet in American homes. Widespread international adoption of broadband is expected to soon follow.

Catch the market trend by meeting the public demand for internet television. From there, proceed to global and mobile markets.

Take advantage of first-mover momentum, with its benefits of consumer trust and high consumer switching costs.

Expand management along with the engineering team.

Continue to maintain relationships with large TV networks.

Improving technology continually enhances the experience of the consumer while keeping variable costs low.

Plan of Action

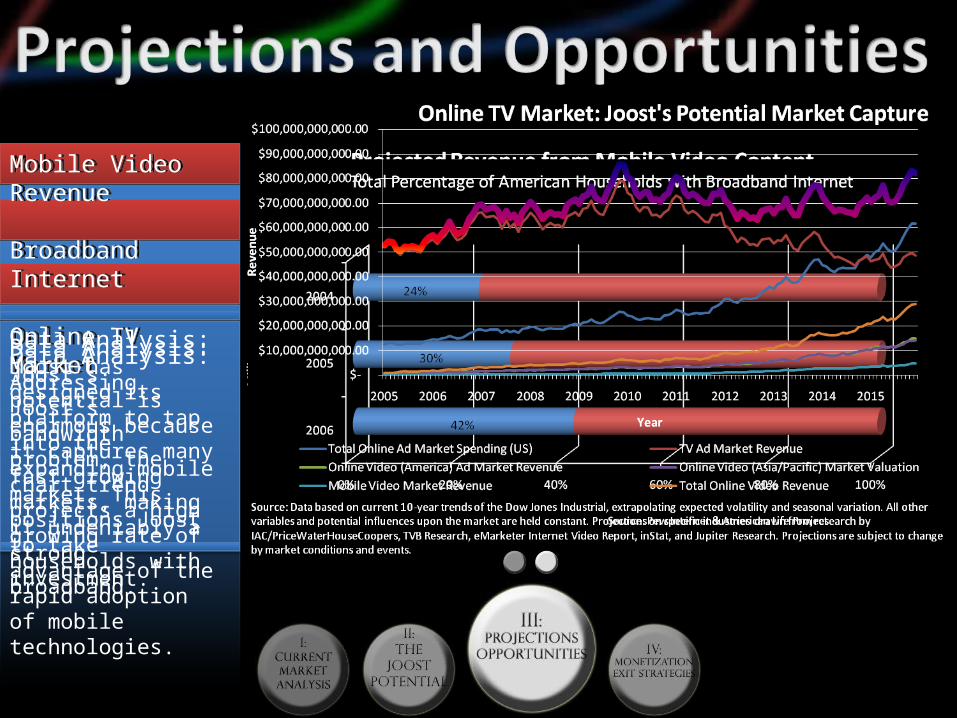

Mobile Video Revenue

Broadband Internet

Online TV Market

Mobile Video Revenue

Broadband Internet

Online TV Market

Data Analysis:Joost has designed its platform to tap into the expanding mobile market. This positions Joost to take advantage of the rapid adoption of mobile technologies.

Data Analysis:Addressing Joost’s bandwidth problem, the chart trend projects a high growing rate of households with broadband.

Data Analysis:Joost’s potential is enormous because it captures many fast growing markets, making it undeniably a strong investment.

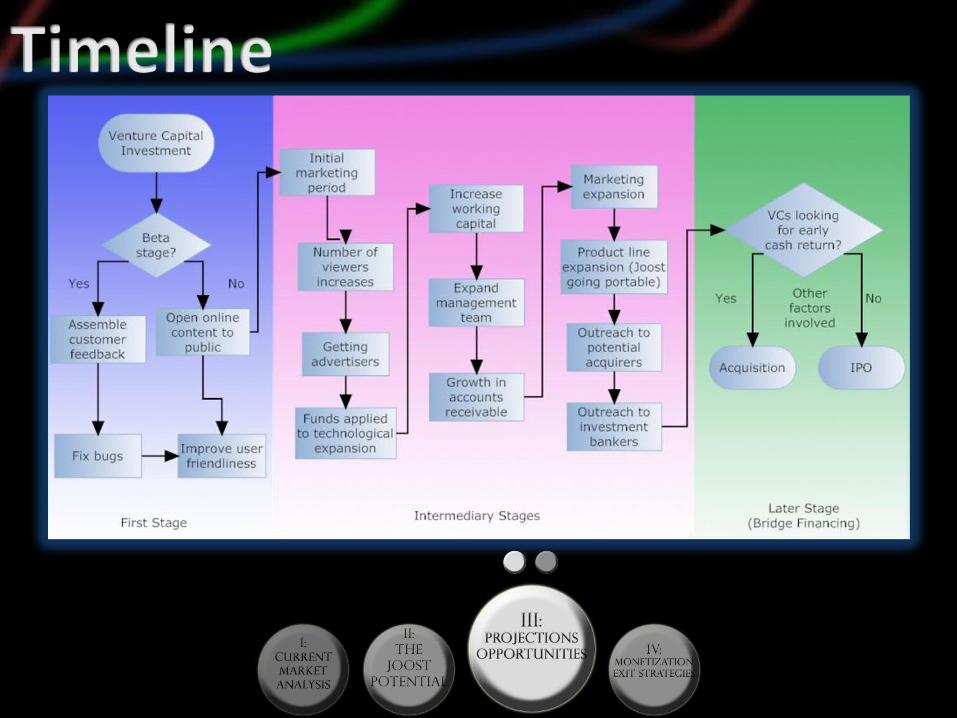

Return liquidity/cash likely through acquisition rather than IPO

The strength of Joost’s platform is enough to take Joost to IPO as a standalone company

However, the current market environment makes it difficult to IPO companies. Additionally, Joost’s product characteristics make it complementary to the business strategies of major corporations moving in the direction of online TV.

Thus, it is likely that Joost would be acquired by large companies seeking to expand their capability, such as Google (which announced its intentions recently) and Microsoft (Media Center), which are the most likely acquirers.

Furthermore, the history of the founders’ past acquired companies makes it likely that corporations will have confidence in the strength of Joost, making it an appealing acquisition target.