Presentation Budget 2014-1 2014-155

185

Presentation Budget 2014-15 Community College District 535 1600 East Golf Road, Des Plaines, Illinois esentation Budget Presentation Budget esentation Budget 5 1 - 4 1 0 2 esentation Budget Presentation Budget esentation Budget 5 1 4 1 0 2 1600 East Golf Road, Des Plaines, Illinois Community College District 535 1600 East Golf Road, Des Plaines, Illinois Community College District 535

Transcript of Presentation Budget 2014-1 2014-155

Presentation Budget 2014-15

Community College District 535

1600 East Golf Road, Des Plaines, Illinois

esentation Budget Pr esentation Budget esentation Budget 51-4102 esentation Budget Pr esentation Budget esentation Budget 514102

1600 East Golf Road, Des Plaines, Illinois

Community College District 535

1600 East Golf Road, Des Plaines, Illinois

Community College District 535

Annual Budget for the

Fiscal Year Ended June 30, 2015

Board of Trustees Community College District No. 535

County of Cook 1600 East Golf Road, Des Plaines, Illinois 60016

www.oakton.edu

To the Board of Trustees:

With great pleasure, I present to you and to the residents of District 535 the Annual Budget for the fiscal year ending June 30, 2015. This document sets forth the College’s financial plan for operations during the coming year. Successfully serving students and their learning objectives form the core of Oakton’s mission. We are committed to equipping our students for work and continued learning in a world where change remains the only

constant. Our success is measured in the lives we change.

In developing the budget for fiscal year 2015, we have carefully considered revenues from the State of Illinois and evaluated our tax rates on district residents and businesses. For this academic and budget year, tuition was increased to $103.25 per credit hour, an increase of 8.30%. Oakton’s per credit hour tuition and property tax rates continue to be among the lowest in the State of Illinois. We have examined expenditures closely and have prepared this budget mindful of the need to equip, support, and enhance the programs and services that form the core of our mission. Oakton continues as a participant in “Achieving the Dream.” This national network comprised of over 200 colleges has a common goal to increase community college student persistence and degree attainment. Key components of the fiscal year 2015 budget directed towards student success include investments in new programs for Workforce Development, Nano Technology and Diesel Technology. Ongoing classroom enhancements include Lecture Capture Stations on both campuses allowing faculty to record high quality video, audio and podcast resources for student use outside the classroom. Additionally, expanded orientation, student to student mentoring, financial literacy training and many other student programs provide tools for students to achieve their certificate, degree or transfer objectives. This budget contains $16 million of expenditures for the Facilities Master Plan. In October 2014, a new integrated student services center will open at the Des Plaines campus. The opening of the new LEED-certified Science and Health Careers Center in January 2015 will feature sophisticated labs, flexible and light-filled classrooms, enhanced technology, and abundant lab preparation and storage space. As approved by the Board of Trustees in December 2010, these capital improvements will be funded through a combination of net asset balances and a College’s Series 2014 Limited Tax Bonds.

Oakton Community College is equally committed to responsible financial stewardship. We are proud of maintaining one of the lowest tax and tuition rates in the State of Illinois and even more proud of the quality education we provide to some 36,000 credit and non-credit students each year. We are grateful for the communities who support us, the communities we serve. Oakton is, indeed, the community’s college. Margaret B. Lee, Ph.D. President and Professor of English

iii

-10

40

90

140

190

FY 06

FY 07

FY 08

FY 09

FY 10

FY 11

FY 12

FY 13

FY 14

FY 15

Master Plan

Debt Repayment

Ongoing Operations

(000,000) Total Budgeted Expenditures (000,000)

Total Budgeted Expenditures

To: President Lee, Members of the Board of Trustees, and Citizens of Oakton Community College, District No. 535: SUMMARY Oakton Community College, Community College District 535’s Annual Budget for Fiscal Year 2014-2015 was presented to and approved by the Board of Trustees on June 24, 2014. Several significant factors guided the development of this year’s budget including:

• Multiple initiatives in the areas of graduation rates, assessment, and student success, • Execution of the 2012-2017 Connecting What Matters strategic plan, • Ongoing implementation of the current five-year Facilities Master Plan, • Ongoing uncertainty about funding to be received from the state of Illinois as well as

proposals to shift responsibility for current state-funded retirement contributions to local governments such as community colleges,

• External economic impacts including property tax uncertainties and limitations and low rates of return on investments, and

• Declining student enrollment trends throughout the country and at Oakton. All Funds The budget contains a total of $144,947,905 in revenues (a decrease of 1.8%) and $166,544,495 in expenditures (a decrease of 10.5%). Projected expenditures exceed revenues by $21,596,590, largely attributable to funding of Capital Improvement projects

arising from the Facilities Master Plan, budgeted costs of the Liability, Protection and Settlement Fund exceeding anticipated revenues and interfund transfers, and budgeted costs of ALLiance, Athletics, Bookstore and Early Childhood Education Lab School Auxiliary Fund

operating costs exceeding anticipated revenues. As discussed in detail in the Capital Expenditures section, execution of the College’s Facilities Master Plan project is underway. Master Plan projects totaling $16,895,000 have been included in the FY2015 budget. While carrying out the Master Plan components, the College has committed to maintaining its physical space and infrastructure. In FY2015, key capital projects include remaining construction of the Science and Health Careers (SHC) Building and Enrollment Center at Des Plaines Campus, building automation at both

Vice President for 1600 East Golf Road Business and Finance Des Plaines, Illinois 60016 847.635.1876 Fax 847.635.1764

iv

campuses, parking lot improvements, remodeling of vacated space and relocation of administrative offices displaced by the Enrollment Center, and a lavatory remodeling project. Budget monies have also been designated for projects in the aftermath of flooding-related seepage experienced in April 2013. A plan to upgrade the generator system and evaluate the underground drainage will enhance the ability to withstand future flooding events. These planned projects drive the budgeted deficits in each of the Education Fund, Operations and Maintenance Fund and the Operations and Maintenance (Restricted) Fund. A transfer of $4,850,000 from the Education Fund is budgeted to the Operations and Maintenance (Restricted) Fund in support of Master Plan and other projects. In conjunction with the FY2015 budgeting process, fewer property tax revenues were directed towards the Audit and the Liability, Protection and Settlement Funds. This chosen alignment of the FY2013 tax levy and corresponding revenues results in a deliberate reduction of the Audit and the Liability, Protection and Settlement Fund balances. Budgeted expenditures exceed revenues in the Operations and Maintenance (Restricted) Fund by $17,564,510. With a transfer of $4,850,000 from the Education Fund, a total budgeted deficit of $12,714,510, will result in the Operations and Maintenance (Restricted) Fund. Lastly, budgeted expenditures significantly exceed revenues for certain Auxiliary Fund programs contributing to the overall budgeted $5.1 million excess of expenditures over revenues. Support of athletic programs is a significant commitment on the part of the College. Historical data reports that combined mentoring/athletic programs lead to a greater degree of student success – particularly for economically disadvantaged students. Also within the Auxiliary Fund, the Alliance for Lifelong Learning (“ALLiance”) provides significant services to the community for a variety of continuing education programs including GED programs and adult courses for Literacy and English as a Second Language. Despite uncertainties about state funding in FY2015, ALLiance will endeavor to serve an equivalent number of students as prior years. The Bookstore and Early Childhood Education (ECE) Centers are budgeted to incur deficits as student textbook buying shifts to both the internet and rental programs and required staffing required in the ECE operations challenge financial results in periods of varying enrollment. Budgeted total personnel costs (salaries and benefits) for the institution, which represent 54% of budgeted expenditures, increased by 3.3% (compared with an 11% increase budgeted for FY 2014 and 5.4% decrease for FY 2013). The FY2015 overall increase is a combination of multiple factors including the addition of new Staff positions focused on Student Success and Maintenance for the new Science and Health Careers (SHC) Building. Salaries are also expected to rise in conjunction with contractual obligations. The budget reflects an overall increase in employee benefit costs of 6.6% from the FY2014 budget. Beginning January 1, 2014, as a result of the negotiation of the Adjunct Faculty union contract, approximately 70 Affiliated Adjunct Faculty members became eligible to participate in the College’s medical insurance programs in conjunction with the Affordable Care Act. FY2015 will experience an entire year of these additional healthcare costs. In addition, this increase is largely attributable to increases in contributions made by the State of Illinois on behalf of Oakton employees. Contributions made by the State of Illinois relating to the State University Retirement Systems (“SURS”) and College Insurance Plan (“CIP”) on behalf of the College’s employees are recognized, but never received, by the College as revenues and expenses in the Restricted Purposes Fund. In FY2014, such actual contributions were $14.9 million (as compared to $19.7 million budgeted) and in FY2013,

v

such contributions were $16.5 million (as compared to $12.0 million budgeted). The State does not provide information to participating organizations about the amount of contributions made on behalf of employees until approximately two months following the end of the applicable fiscal year. Contributions have varied significantly over the last several years and Oakton has been unable to closely estimate such amounts for budgeting purposes due to the lack of available information. For FY2015, Oakton budgeted $22.0 million – an increase of 11.7% as compared to the FY2014 budgeted amount. It is important to note that such amounts have no cash flow impact to the College. Budgeted expenditures for both contractual services and conferences and meetings have increased 8.4% and .8%, respectively. Budgeted expenditures for general materials and supplies have increased .6%. As compared to FY2014, greater contractual services have been budgeted in the Education, Operations and Maintenance, and Operations and Maintenance (Restricted) Funds. Contractual services increases in the Operations and Maintenance Fund is due to increased building and grounds maintenance services for FY2015. In the Education Fund, the increase in contractual services is primarily attributable to an increase in personnel recruiting costs due to the retirement of President Margaret Lee. Greater contractual service spending in the Operations and Maintenance (Restricted) Fund is budgeted for services related to the slab remediation of the SHC Building discussed below. In fiscal year 2015, student success initiatives and participation in “Achieving the Dream” will continue. Expenditures for these programs are expected to remain at amounts similar to FY2014, for conferences and meetings, travel, and employee training. “Achieving the Dream” is a national network comprised of over 200 colleges and state policy teams with a common goal to increase community college student persistence and degree attainment. Oakton was accepted into the Achieving the Dream program during FY2013. The principles that focus colleges on student success include: 1) a student-centered vision, 2) equity & excellence, and 3) evidence-based decision-making. These increased expenditures, including membership fees for Achieving the Dream, are budgeted in the Education Fund. Custodial equipment and supplies for the SHC Building represent the increased general materials and supplies budget in the Operations and Maintenance Fund. An increase of $83,800 for will provide for various tools and equipment for maintenance and repair of the SHC and other Des Plaines Campus buildings. Monies budgeted for the SHC Building also includes furniture for public spaces and administrative offices. The Auxiliary Enterprise Fund contains budgeted monies for significant new IT equipment including replacement of the 10 year old Bookstore point of sale system (budgeted in FY2014 but not purchased). Additionally, the College is continuing a Document Imaging project, initiated in FY2014, expanded mobile applications for students and lecture capture systems for Nursing and other curriculums. Utility charges are budgeted to decrease 2.4% after a budgeted increase of 7.4% in FY2014. In FY2014, the College applied for and was awarded energy-savings related grant for the SHC building. The expected savings from significant recent upgrades to more efficient Central Plant equipment and Building Automation Systems on both campuses will be partially offset by market rate fluctuations and issuance of delivery charges. Based on these investments, energy costs are not expected to increase as the new building is brought on line for the Spring semester of FY2015.

vi

Expenditures for capital outlay have decreased by 58.6%, reflected by the planned completion of various Master Plan projects during FY2015. In FY2015, $1.2 million is budgeted for renovation of the softball fields which includes: re-grading, installation of drainage and underground sprinklers systems, reconstruction of the infields and outfields, and rebuilding of the field dugouts and backstops. Also, renovation of the athletic locker rooms is planned for the new fiscal year. In FY2015, the repayment of $14.5 million of Debt Certificates, Series 2014 is budgeted. Additionally, ongoing principal and interest payments on the 2014 Debt Certificates and the 2011 and 2014 Limited Bonds are budgeted for FY2015. As described more fully in the Capital Expenditures portion of this document, in addition to Master Plan projects, a variety of IT equipment, replacement vehicles and upgrading the generator system for the Des Plaines campus are part of the FY2015 Capital Outlay budget. Other expense, which is primarily comprised of financial aid, is budgeted to decrease 7.7% to $13.7 million. This compares to a .35% increase between the budgets for fiscal years 2013 and 2014. Changes in the economic climate, decreasing amounts available from State of Illinois programs and changes in Pell grant guidelines are expected to keep financial aid levels moderately lower. These monies are provided by the State and Federal government and distributed by Oakton; there is no net cash impact to Oakton and students who successfully complete their classes do not need to repay these awards. Presidential Search With the impending retirement of President Margaret B. Lee after 30 years of exemplary service, Oakton’s Board of Trustees has launched a national search for a new president. After a survey and meetings with stakeholders across the college community, a College-wide committee will begin the search process with the goal of selecting a candidate by the end of April 2015. Budgeted expenditures for personnel recruitment have been increased in FY2015 by $100,000 for selection process costs. Operating Funds The Operating Funds, which are those funds used for the primary instruction and general support functions of the College, show revenues of $72,144,940 and expenditures of $69,327,940 for the fiscal year, plus fund transfers of $4,850,000 to the Operations and Maintenance Fund (Restricted), $946,000 (net) to the Auxiliary Enterprises Fund, $510,000 to the Liability/Settlement Fund, $100,000 to the Restricted Purposes Fund, $940,000 to the Social Security/Medicare Fund, and $29,000 from the Working Cash Fund. This leaves a net, planned deficit for the Operating Funds of $4.5 million; thus revenues plus interfund transfers in less expenditures plus interfund transfers out are projected to decrease fund balance by approximately $4.5 million for this fiscal year, as compared to a projected net planned deficit of $7.1 million for the Operating Fund budget in FY 2014. Greater than budgeted collections of property taxes and state credit hour reimbursement funding combined with an decrease in expenditures that was less than amounts budgeted contributed to a FY 2014 operating net surplus of $1.3 million in contrast to the $7.1 million deficit budgeted. (These amounts exclude depreciation which is not budgeted. Refer to the “Finance and Accounting” section of this document for additional information.) The $4.5 million budgeted deficit for FY2015 is primarily comprised of the contribution being transferred from the Operating Funds to the Operations and Maintenance (Restricted) Fund. As outlined in the Capital Expenditures section of this document and as further discussed in the Finance and Accounting section, the College’s Board of Trustees has established policy with respect to the amount and appropriate use of Net Assets within the budget. The Board has approved the

vii

investment of $20 million of Operating Fund Net Position in the current Five-Year Facilities Master Plan. The FY2015 contribution of $4.5 million represents the third installment of that investment for the fiscal years 2013 through 2016. Transfers from the Operating Funds and their purpose are summarized in the following table. At the same time, the FY2015 budget includes the transfer of $288,000 in royalty proceeds associated with a lease of airwaves owned by the College (“ITFS Lease”) into the Operating Funds. These monies are designated to support instructional programs.

Inter Fund Transfers FY14 Budget

FY14 Actual FY15 Budget

Auxiliary Enterprises Fund: ALLiance for Lifelong Learning $222,000 222,000 $304,000 Information Technology 912,000 912,000 930,000 Royalties from Airwave Lease (850,000) (850,000) (288,000) Operations and Maintenance (Restricted) Fund:

Remodeling and Infrastructure Projects Master Plan Projects

350,000

6,800,000

350,000

6,800,000

350,000

4,500,000 Liability/Settlement Fund: Tort 400,000 400,000 510,000 FICA/Medicare-Medicaid 780,000 780,000 940,000 Restricted Purposes Fund: Return of Unspent Strategic Initiative

Monies

(460,000)

(460,000)

Student Scholarships 100,000 100,000 100,000 Working Cash Fund: Interest Allocation

(32,000) -

(32,000) -

(29,000)

Net Operating Funds Transfers

$8,222,000

$8,222,000

$7,317,000

Annually, the Education Fund contributes monies towards funding the operations of the Alliance for Lifelong Learning. Additional transfers to the Auxiliary Enterprises Fund represent funding for the student and financial information technology systems. The transfers to the Operations and Maintenance (Restricted) Fund reflects the College’s commitment towards utilizing Net Position to partially fund the Master Plan and the ongoing utilization of net position for remodeling/infrastructure projects that are outside of the Master Plan. The College is evaluating the method it uses to fund liability, workers compensation and unemployment insurances along with employer payments of FICA and Medicare/Medicaid. Rather than levying taxes specifically for such obligations, FY2015 costs have been budgeted to be paid from transfers out of the Operating Funds. In fiscal year 2011, Oakton implemented an increase in tuition of $5 per credit hour. In conjunction with this increase, it was agreed that fifty cents of this increase (estimated to total $100,000 for the year) would be given to the Student Government Association to assist students with financial need. This practice continues in FY2015.

viii

The financial plan predicts total Operating Fund revenues will increase by 3.9%, in contrast to a 2.3% increase in the last budget. Among the Chicago collar county community colleges, Oakton’s combined tuition and credit hour fee rate is the lowest for FY2015. In February 2014, Oakton’s Board of Trustees approved a tuition increase for FY2015 and 2016. With the adoption of tuition increases for these years, Oakton will continue to be almost 23% lower than the current State-wide and peer group maximum tuition/fee rates. For FY2015, this represents a $9.71 increase to the previous rate of $95.34. Overall tuition and fees are projected to be comparable to FY2014 considering the impact of a tuition rate increase, and volume decreases anticipated for both tuition and fees. Overall tuition and fee are projected to increase by $1.1 million compared to FY2013, despite the elimination of the graduation fee. The graduation fee was eliminated to encourage a greater number of students to complete an Associate Degree or Certificate prior to transferring to a four-year college. A small ($18,000) increase has been assumed in credit hour funding collected from the state. The increase is not attributable to an increase in reimbursable credit hours, but rather to variation in the mix of credit hours and the rates at which the different types of courses are reimbursed. Due to uncertainties about the receipt of such funding, Oakton has continued to establish a reserve for potentially uncollectible state funding approximating 25% of amounts due. It should be noted that Oakton has established such reserves in preceding years, but did ultimately collect 100% of the College’s credit hour funding grant for FY2012 through 2014. Oakton’s budgeted credit hour grant funding has been nearly level at $5.6 to $5.3 million the last three years in contrast to rising costs during that period. (Of this total credit hour grant funding, in FY2015, $3.3 million is attributed to the Operating Funds and the remainder to the Auxiliary Enterprises Fund.) Property taxes are budgeted to increase $1.6 million from FY2014, consistent with the rate of inflation and statutory limitations on such increases. Local government revenues (property taxes and chargebacks) account for more than 63% of all Operating Fund revenues in this budget, the exact percentage budgeted in FY2014, and a reflection of steady enrollment trends and the corresponding impact on tuition and fees. State funding remains relatively consistent at 5.1% of budgeted operating fund revenues in FY 2015, compared to 5.2% for both FY2013 and FY2014. Other sources of revenue, including investment income, are expected to increase by 12% due to interest rates on those invested assets and the planned transfer of $4.5 million of Operating Fund net position to the Operations and Maintenance (Restricted) Fund for use in the Facilities Master Plan. Operating Funds budgeted expenditures are budgeted to increase by 1.5% or approximately $1.03 million, as compared to a FY2014 increase of 3.0% and the .17% increase for FY 2013. While the overall increase is modest, it is comprised of fluctuations in a variety of line items. Contractual salary increases along with the authorization of additional Staff positions account for the bulk of the increase. Salary expense is budgeted to increase approximately $180,000 (or .4%) in FY2015. Employee benefit costs for medical insurance plans and

Revenues

Operating Funds

Local Government 63.41%

Other Sources 0.72%

State Government

5.10%

Student Tuition and Fees 30.77%

ix

Expenditures

All Other 6.39%

Salaries and Benefits 78.73%

Contractual Services 8.28%

General Materials and Supplies

6.60%

Operating Funds Operating Funds

retirement benefits are budgeted to decrease 1.3% in FY15. The decrease arose due to a lower demand for benefits as a result of the Faculty and Staff retirements in 2014. This decrease is somewhat offset by the budgeted participation of Affiliated Adjunct faculty in the health insurance plan effective January 1, 2014. As should be expected in a service organization, the majority of the expenditures are for salaries (69.4%) and benefits (9.4%). Of the non-personnel categories contractual services (8.3%) and general materials and supplies (6.6%) constitute the other major expenditure areas. These categories are budgeted

to increase (6.5% and 5.4%, respectively) in FY15, this follows an increase of 6.0% for contractual services and an increase of 13.4% in materials and supplies between the fiscal year 2013 and 2014 budgets. The contractual services change is largely attributable to an increase in building and grounds maintenance and instructional contracts for the Fire Science program. Increased material and supply budgets are largely attributable to equipping the new SHC Building. Net Position The total net position for the College’s budgeted funds is $108.3 million at June 30, 2014 based on preliminary year end data. (Inclusive of all funds and account groups, the total net position is $168.4 million at June 30, 2014.) It is budgeted to decline $21.6 million or 19.1% by June 30, 2015. Two funds are budgeted to experience a reduction in fund balance of more than 10% during FY2015. The decrease of 32.5% budgeted for the Auxiliary Fund reflects a conscious intent to utilize a portion of monies that were accumulated during positive economic times to fund operations and initiatives, and provide improvements to specified athletic facilities. As discussed earlier, the reduction of the Education and the Operations and Maintenance Fund Net Position is equivalent to the contribution being transferred to the Operations and Maintenance (Restricted) Fund plus the projected net cost of Affiliated Adjunct participation in the College’s medical insurance plan effective January 1, 2014. The Board has approved the investment of $20 million of Operating Fund Net Position in the current Five-Year Facilities Master Plan; the FY2015 contribution of $4.5 million represents the third installment of that investment. Historical experience indicates a reasonable possibility that cost savings and supplemental revenues may decrease the amount of budgeted net position reductions. In either case, these net position reductions are not anticipated to alter Oakton’s overall strong financial standing or Aaa general obligation bond rating. The Auxiliary Enterprises Fund begins the fiscal year with a net position of $15.8 million. For FY2015, a portion of this net position (via a budgeted contingency) may be utilized to continue operating Adult Education and Literacy programs of the Alliance for Lifelong Learning in the event that State funding cuts occur. If budgeted expenditures are fully realized, the net position of the Auxiliary Enterprises fund would decline to $10.7 million. Net position of the Auxiliary Enterprise Fund will also be reduced by budgeted expenditures

x

20 35 50 65 80 95

110 125 140

2005

2007

2009

2011

2013

2015

(Excl. Inv. in Plant)

NET POSITION (000,000)

in excess of revenues for the ALLiance, ECE Lab Schools, and Athletics. In preparing the budget, ALLiance anticipated revenues will decrease as a result of both reduced tuition from enrollment trends and reduced state funding. As enrollment has declined and state funding has been subject to greater question, ALLiance has closely monitored staffing and other expense levels achieving small contributions to net position despite budgeted deficits. However, certain fixed costs remain and, facing potential cuts in State funding for Adult Education and Literacy programs, some costs historically paid by grants were budgeted in contingency for the Auxiliary Fund (reported as part of “Other Operations” within this fund) based upon the College’s commitment to offer these programs. As noted above, utilizing Auxiliary Fund monies to support the cost of Athletic programs is a key component of Oakton’s commitment to Student Success based upon historical evidence that mentoring/athletic programs lead to a greater degree of student success. The Early Childhood Education Lab Schools on Oakton’s Des Plaines and Ray Hartstein campuses have historically incurred expenses in excess of revenues however; the programs provide a valuable teaching tool for the Early Childhood Education degree program. Required staff, Oakton student and child classroom ratios are components of the net expense structure. The Restricted Purposes Fund is used to account for grant and other monies that have

restrictions regarding their use. Generally, the Restricted Purposes Fund is budgeted to have a net revenue, expense and interfund transfer result of zero. For many years, the Restricted Purposes Fund has carried a net position that appears to have originated primarily from indirect cost allocations associated with certain grants and interest on idle monies. At June 30, 2015, the Restricted Purposes Fund is budgeted to have a net position of $109,000.

Budgeted revenues of the Audit Fund and of the Liability, Protection and Settlement Fund exceed anticipated expenditures and interfund transfers. In conjunction with the FY2015 budgeting process, fewer property tax revenues were directed towards these Funds. Revenues that were previously levied for these funds will support student success and related initiatives in the Education Fund. This chosen alignment of the FY2014 and FY2015 tax levies and corresponding revenues results in a deliberate reduction of the Audit Fund and Liability, Protection and Settlement Fund net positions. The main component of the College’s Master Plan is the construction of a new $42 million, state of the art Science and Health Careers (SHC) Building. Construction of the SHC Building began in calendar year 2012 with build-out of all three floors being substantially completed by the end of January 2014. In November 2013 it was discovered that the first floor’s concrete slab-on-grade on the west side of the building (an area of approximately 8,300 square feet of the building’s total square footage of approximately 93,000) had begun to settle resulting in numerous cracks and uneven surfaces. As a result, final build-out of Division 1 offices as well as the outfitting of equipment and installation of furniture throughout the building, were put on hold.

xi

Relative Salaries

Administrator 6..83%

Student 2.78%

Staff 31.75%

Faculty 58.64%

(Operating Funds)

The projected cost of the remediation plan, scheduled for completion in late November 2014, is currently $4.1 million. The College has agreed to initially fund the costs of the remediation work without waiving any claims and has reserved its rights to pursue such claims against all potentially responsible entities for recovery of those costs. All parties have agreed to this process. By virtue of its excellent financial position and more than adequate reserves, the College is well positioned to manage cash flow for the remediation work. Salaries and Employees For fiscal year 2015 the College has added four new full time staff positions and three new part-time staff positions. Within the Administrator group, two positions were modified – one was upgraded to administrator and one was increased from part-time to full-time. One new position will provide HVAC maintenance for the new SHC Building. The number of authorized Full Time Faculty positions remains consistent. In the last several years there have been a significant number of Full Time Faculty retirements and 17 more are scheduled through August of 2017. Consistent with prior years, part-time faculty counts will vary in accordance with enrollment levels. The contractual agreement with the College’s part-time faculty was approved by the Board of Trustees in September 2013 and extends through August 2017 with an average annual salary increase of 3.2%. The current Full-Time faculty agreement extends to August 2016 and includes an annual salary increase of 3.04% in year one, 2.98% in year two and 2.95% in year three. Depending on the CPI-U, the increase in year four will be at least 2.6% but will not exceed 3.9%. Faculty at the top step will receive 1.25% raises for years 1-3. Their increase in year 4 may be up to 3% depending on economic conditions. The contract contains retirement-related incentives to those who declare their intent under specified guidelines. The current contract with Public Safety Officers extends to June 2016 and included a significant equity adjustment in the first year followed by an average annual salary increase of 2.75% over the remaining three years. The current contract with the Classified Staff extends to December 2016 and includes an annual salary increase of 3.04 in year one, 2.98% in year two, and 2.95% in years three and four. As the College continually examines its future needs through budget staffing requests and ongoing administrative review, a few positions may remain unfilled and there may be shifting of approved positions as the institution continues to refine its structure to meet the needs of the students and other operational necessities.

xii

210

220

230

240

250

FY 05

FY 06

FY 07

FY 08

FY 09

FY 10

FY 11

FY 12

FY 13

FY 14

Enrollment Trend Credit Hours

FY 06 FY 08 FY 10 FY 12 FY 14

Baccalaureate

Occupational

Relative Credit Hour Trends

Values adjusted for comparative purposes

Enrollment and Credit Hours Total institutional enrollment for Fiscal Year 2014 was 213,443 credit hours. These hours

represent a 4.3% decrease from 223,072 in 2013 and comparing to 227,393 in 2012 and 232,788 in 2011. In comparing the institutional credit hours for FY2014 and FY2013, it is also important to consider the composition of credit hours between Oakton credit related hours and ALLiance continuing education hours. Oakton credit-related hours in FY2014 of 180,626 declined 4.6% as compared with FY2013 credit-related hours of 189,405; this change is generally consistent what the experience of other area community colleges. A decrease in credit hours

occurred for ALLiance whose hours fluctuated to 32,817 in FY2014 from 33,667 hours in FY2013. ALLiance credit hours are predominantly restricted hours that are not eligible for reimbursement through state funding. It was assumed that Oakton enrollment would decline by approximately 4,000 credit hours (or 2%) in FY2015. Initial data is reflecting a 1.3% decrease in credit hours from the Fall Semester 2014 to Fall 2013. These fluctuations are being felt by other Chicago area community colleges as well. For FY2015, ALLiance does not expect enrollment to significantly increase. In several of the recent years, significant credit hour growth occurred consistent with negative changes in the economy. Consistent with other community colleges, Oakton anticipated this would level off with economic improvements. Additionally, there is anecdotal evidence that recent/potential community college students who have experienced longer term unemployment may be fully focused on job search efforts and choosing not to invest limited financial resources on continued education at this point in time. Economic factors, such as recent lay-offs by some major companies, should also be considered as the employees upgrade skills and look for training for career changes. It is likely that, for some students, the significant price differential between four-year college tuition and fees and those of the community college is a deciding factor in their college of choice. In the current economic environment, a more consistent level of enrollment is expected. Given the historical and comparative relative economic stability of the district, dramatic enrollment fluctuations are not anticipated. For the period 2008 through 2014, the relative relationship between baccalaureate course enrollment (77% of total enrollment) and vocational course enrollment at 23% has also remained steady. In baccalaureate offerings, computer science and engineering have experienced more growth than any other program – at least a 40% increase in credit hours

xiii

between fiscal years 2009 and 2014. Global business studies, modern languages, historical policy studies, and music experienced declines greater the 20% in that same period. Among vocational programs real estate and architecture/ construction management programs decreased significantly and those programs have been dropped. While fire science, paralegal studies and automobile technology courses have shown a substantial increase, electronics technology, early childhood education, and mechanical design have declined. Oakton continually reviews and refines its educational offerings to more closely meet the needs of the district residents and local businesses and continues its efforts to improve its enrollment posture through recruitment, partnerships and expanded marketing approaches. The College continues to carefully manage resources through financial control, investment in capital projects providing long-term benefit to the College’s student population, and reduction of expenditures where possible without affecting the quality and viability of the educational programs. The College’s financial goal of maintaining a healthy fiscal position through development of new and additional resources and through the wise allocation and use of available resources in support of the educational goals and mission of the College remains unchanged and was affirmed by the Aaa bond rating received from Moody’s in both August 2011 and August 2014. Overall, we believe that Oakton Community College presents an extremely vibrant educational and financial picture, in spite of the current state and federal grant funding questions. The College is confident it will be able to wisely manage our available resources and support our mission in the future. Budgetary Performance The following comments address certain variations between budgeted amounts and preliminary actual amounts for FY2014. Comparison of these figures is an indication of the assumptions and accuracy with which the budget was prepared and monitored. Amounts presented for the 2014 budget are not adjusted for subsequent budget transfers. Overall revenues were 10.6% under budget. Collections of property taxes and personal property replacement taxes were 9.0% less than budgeted amounts. Revenues from state government sources varied negatively from budget by more than 13% due to variances experienced with revenues reported for SURS contributions made by the State on behalf of Oakton employees that were $4.8 million less than budgeted. These deficits are also explained by other state grants and financial aid budgeted for but not ultimately received. Primarily due to unrealized grants, Federal government revenues were 33% (or $4.7 million) less than budgeted. Student tuition and fee revenues were approximately $209,000 (or 0.9%) less than budgeted. The revenue from other sources, primarily interest revenue and unrealized gains/losses on investments, was less than expected by 7.0%. Declining bookstore sales also contributed to this budget variance. For all funds, expenditures were greater than revenues by $4,559,741 and under budget by $49.5 million, or 26.6%. The largest components of this variance occurred in Salaries, Employee Benefits, General Materials and Supplies, Fixed Charges, Capital Outlay, and Other. Salary expenditures budgeted for $57,714,444 compared to actual expense of $53,519,637. These fluctuations are attributable to full-time faculty retirements and salaries that were compensated by grants, capital improvement projects that progressed at a quicker pace than expected in FY2013, and staff positions that were unfilled or delayed prior to

xiv

filling. Employee benefit expenditures were $25,624,925 as compared to budgeted amounts of $29,083,833. The favorable variance is mostly due to the over estimation of contributions to SURS from the State of Illinois during FY 2014. Expenditures for Capital Outlay were $27,309,313 as compared to $44,796,380 budgeted. This fluctuation has two primary components: $4.4 million was not incurred due to the speed of construction experienced towards the end of FY2013 and an unspent amount of $2.1 million caused by unrealized grants. Actual Operating Funds revenues were greater than budgeted by 2.50%. A negative variance in other sources (primarily interest income and fair market value adjustments) was offset by greater than budgeted property tax and personal property replacement tax collections in the Operating Funds. Additionally, all credit hour grant revenues from the State have been recognized as compared to the 75% reserve that Oakton had established in its budget for possible nonpayment; subsequent to year end, Oakton received the remaining payments due. Operating fund expenditures were less than budgeted by 9.7%. The largest savings was in salaries due to a combination of full time faculty retirements, salaries that were compensated by grants, ongoing efforts to optimize classes, unspent sign interpreter monies and staff positions that were unfilled or delayed prior to filling. Additionally, substantially all Contingency monies budgeted were not utilized.

Operations and Maintenance Fund (Restricted) expenditures were significantly less ($26,611,486) than planned ($46,157,849). This fluctuation is primarily attributable to the timing of expenditures related to the Five Year Master Plan. Major site and construction work was completed for the SHC Building; however, due to the cracks and uneven surfaces discovered in the concrete slab-on-grade and resulting remediation, a portion of remaining construction was delayed. Due to this delay in completion of the SHC Building a major portion of capital funds were unspent. In addition, expenditures budgeted in FY2014 for other projects were not incurred due to the speed of construction towards the end of FY2013. However, some of the unplanned surplus in the O&M Restricted Fund was offset due the majority of work for the Des Plaines campus Enrollment Center postponed during FY2013 and, therefore incurred during FY2014. Spending occurred for various other Master Plan projects including the relocation of the Northwest Municipal Conference, the last phase of Classroom Remodeling, a portion of the HVAC and Building Automation Systems Improvements, Phone upgrades, and nearly half of the Parking Lot improvements. Also, no work occurred in FY2014 for Lavatory Upgrades (re-budgeted for $500,000 in FY2015). Auxiliary Enterprises Fund expenditures were less than planned by 16.7%, due primarily to significant savings in Capital Outlay, Salaries and Contingency. The positive variance in Capital Outlay is attributable to IT – primarily from unspent monies and items that were ultimately charged to General Materials and Supplies as the purchases did not meet Oakton’s capitalization policy. Salaries varied from budget due to unfilled vacancies in IT, ALLiance and Athletics. Both the Bookstore and ALLiance carefully managed salary expense relative to decreases in revenue. Additionally, substantially all Contingency monies budgeted were not utilized. Other Information The Government Finance Officers Association of the United States and Canada (GFOA) presented a Distinguished Budget Presentation Award to Oakton Community College,

xv

Illinois for the Annual Budget beginning July 1, 2013. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, as an operations guide, as a financial plan, and as a communications device. This award is valid for a period of one year only. We believe our current budget continues to conform to program requirements, and we are submitting it to GFOA to determine its eligibility for another award. Oakton Community College also received the Certificate of Achievement for Excellence in Financial Reporting and the Award for Outstanding Achievement in Popular Finance Reporting for the fiscal year ended June 30, 2013. Miscellaneous Everyone is strongly encouraged to read the Introduction section of this budget presentation. It contains additional significant information on the goals, policies and processes which helped to define and shape this year’s budget and includes important supplementary information which will be of interest to the reader. Although for the purposes of publication organization it is a separate section, the information that the Introduction section contains may be considered an extension of this addendum. We have chosen to place the material in that section in order to be able to develop the information in greater detail and breadth. Robert J. Nowak Vice President for Business and Finance

xvi

The Government Finance Officers Association Of the United States and Canada (GFOA)

Presented a

Distinguished Budget Presentation

Award

to

Oakton Community College, Illinois

for its Annual Budget for the fiscal year beginning July 1, 2013

In order to receive this award, a governmental unit must publish

a budget document that meets program criteria as a policy document, as an operations guide,

as a financial plan, and as a communications device.

This award is valid for a period of one year only. We believe our current budget

continues to conform to program requirements, and we are submitting it to GFOA

to determine its eligibility for another award.

xvii

SECTION PAGE

Letter from the President iAddendum to the President's Letter iiiDistinguished Budget Award xviTable of Contents xviii

Introduction Section

Chart of Organization - Community College District No. 535 2Listing of Principal Officials 3Our Vision, Mission and Values 5Goals and Objectives 16Capital Expenditures 22Finance and Accounting 30Budget Process 46Notes on Preparation and Conventions 53

Budget Section

Comparison of Budgeted Fund Revenue and Expenditure Relationships 55Comparison of Revenues and Expenditures - All Funds 56Summary of Revenues and Expenditures - All Fund Groups 58Chart of Organization - President 60Chart of Organization - Academic Affairs 61Chart of Organization - Information Technology 63Chart of Organization - Student Affairs 64Chart of Organization - Business and Finance 65

xviii

OAKTON COMMUNITY COLLEGE Community College District No. 535

Annual Budget Fiscal Year 2015 Table of Contents

Comparison of Revenues and Expenditures - Operating Funds 67Comparison of Revenues and Expenditures - Education Fund 68Comparison of Revenues and Expenditures

Operations and Maintenance Fund 69Comparison of Revenues and Expenditures - Auxiliary Enterprise Fund 70Comparison of Revenues and Expenditures

Auxiliary Enterprise Fund by Program 72Comparison of Revenues and Expenditures

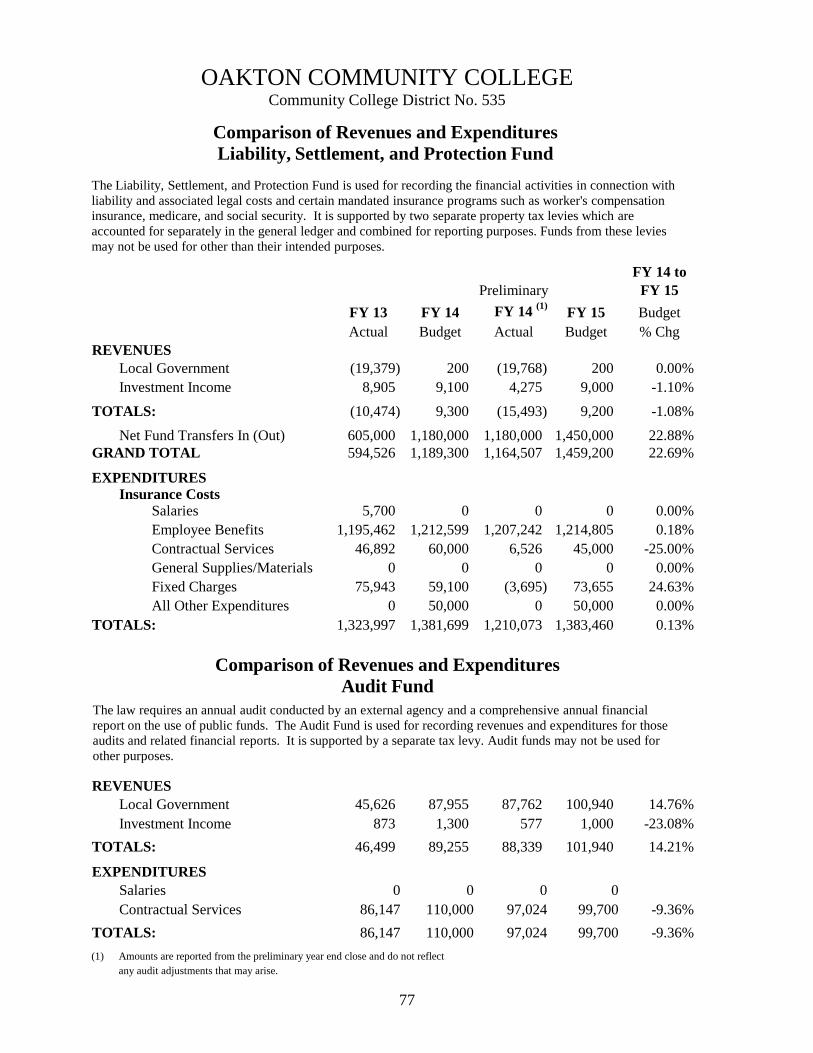

Bond and Interest Fund 76Comparison of Revenues and Expenditures

Liability, Protection, and Settlement Fund 77Comparison of Revenues and Expenditures

Audit Fund 77Comparison of Revenues and Expenditures - Restricted Purposes Fund 78Comparison of Revenues and Expenditures

Operations and Maintenance Fund (Restricted) 79Comparison of Capital Expenditures 80

Statistics Section

History of Actual Revenues and Expenditures - Operating Funds 83Comparison of Audited Operating Revenues by Source 85Comparison of Audited Operating Expenditures by Object 86Comparison of Audited Operating Expenditures by Function 87Comparison of Full-time Faculty Assignments 88Comparison of Instructional Faculty and Administrators 90Comparison of Classified Staff Assignments 92Comparison of Classified Staff 93Comparison of Total Reimbursable Credit Hours

by Instructional Categories 94Total and Reimbursable Credit Hours by Instructional/Funding Category 96History of ICCB Credit Hour Grant Rates by Instructional Category 98Enrollment Statistical Data 100Comparison of Student Enrollment Information

Fall Term Student Headcount 102History of Academic Awards 103History of Tuition and Fee Charges 104History of Financial Aid to Students 105Comparison of Property Tax Rates and Tuition and Fee Rates 106Ten Year History of Tax Rates and Assessed Valuations 108

xix

Typical History of Property Tax Rates - Overlapping Governments 109Comparison of Facilities and Use - Square Footage Data 110History and Comparison of Utility Costs 112

Appendix Section

Description of Functional Areas and Programs 114Degrees and Certificates Awarded by the College 134Agenda Item 12/12-8 consisting of:

Adoption of Resolution Setting Forth Tax Levies for 2012 136Certificate of Tax Levy filed with the County Clerk 138Certificate of Compliance with Truth in Taxation 139

Agenda Item 6/13 - 8b Resolution to Adopt FY14 Annual Budget 140(Legal Budget omitted)

Land Use Summary 143Neighboring Community College Districts Map 144District 535 and Surrounding Area Map 145Des Plaines Campus Map 146Ray Hartstein Campus Map 147Glossary 148Acknowledgements 160

xx

INTRODUCTION SECTION

2

VICE PRESIDENT FOR

ACADEMIC AFFAIRS

ASSOCIATE VICE PRESIDENT

FOR CONTINUING

EDUCATION, TRAINING & WORKFORCE DEVELOPMENT

VICE PRESIDENT FOR

BUSINESS AND

FINANCE

VICE PRESIDENT FOR

TECHNOLOGY AND DATA ANALYTICS

ASSISTANT VICE PRESIDENT

FOR OFFICE OF ACCESS,

EQUITY & DIVERSITY

EXECUTIVE DIRECTOR

FOR HUMAN RESOURCES

EXECUTIVE DIRECTOR OF COLLEGE

ADVANCEMENT VICE PRESIDENT

FOR STUDENT AFFAIRS

3

OAKTON COMMUNITY COLLEGE Community College District No. 535

Listing of Principal Officials

Members of the Board of Trustees (with term expiration)

Mr. William Stafford - 2015

Chairman, Board of Trustees

Ms. Patricia N. Harada - 2017 Vice Chairman, Board of Trustees

Ms. Ann E. Tennes - 2019

Secretary, Board of Trustees

Ms. Theresa Bashiri-Remetio - 2015 Member, Board of Trustees

Dr. Joan W. DiLeonardi - 2019

Member, Board of Trustees

Mr. Kyle Frank - 2019 Member, Board of Trustees

Mr. Jody Wadhwa - 2017

Member, Board of Trustees

Mr. Daniel J. Alferes - 2015 Student Member, Board of Trustees

Emeritus Members of the Board of Trustees

Mrs. Joan B. Hall

Mr. Ray Hartstein

4

OAKTON COMMUNITY COLLEGE Community College District No. 535

Listing of Principal Officials (Continued)

Principal Administration Officials

Dr. Margaret B. Lee President

Dr. Michael Anthony

Assistant Vice President for Access, Equity and Diversity

Dr. Michael Carr Assistant Vice President for Academic Affairs

Dr. Thomas Hamel

Vice President for Academic Affairs

Dr. Merrill Irving Associate Vice President for Continuing

Education, Training and Workforce Development

Ms. Bonnie Lucas Vice President for Technology and Data Analytics

Ms. Mum Martens

Executive Director for Human Resources

Mr. Robert Nowak Vice President for Business and Finance

Dr. Joianne Smith

Vice President for Student Affairs

5

OAKTON COMMUNITY COLLEGE Community College District No. 535

Our Vision, Mission and Values

Oakton’s vision, mission and values are based on long-standing and fundamental principles guiding the College’s work and the relationships among all those who work and study at Oakton, as well as members of the community and professional colleagues throughout the nation. The vision, mission and values were formally ratified by the Board of Trustees on October 20, 1998. They were reaffirmed by the Board on October 15, 2002. WE ARE THE COMMUNITY’S COLLEGE We are dedicated, first, to excellence in teaching and learning. We challenge our students to experience the hard work and satisfaction of

learning that leads to intellectual growth and we support them academically, emotionally and socially.

We encourage them to entertain and question ideas, think critically, solve problems, and engage with other cultures, with one another, and with us.

We expect our students to assume responsibility for their own learning, to exercise leadership and to apply ethical principles in their academic, work, and personal lives.

We demand from ourselves and our students tolerance, fairness, responsibility, compassion and integrity.

WE ARE A COMMUNITY OF LEARNERS We provide education and training for and throughout a lifetime. We seek to improve and expand the services we offer in support of the people in

the communities we serve. We promote a caring community of staff and faculty members, students,

administrators, and trustees who, in keeping with our values, work together to fulfill our mission.

WE ARE A CHANGING COMMUNITY We recognize that change is inevitable and that education must be for the future. We respond to change informed by our values and our responsibility to our

students and our communities. We challenge our students to be capable global citizens, guided by knowledge and

ethical principles, who will shape the future.

6

History Founded in 1969, Oakton Community College opened its doors to 832 students in fall 1970. The “campus” consisted of four factory buildings at the intersection of Nagle Avenue and Oakton Street in Morton Grove. Search for a new site began almost immediately, but four years elapsed before the College purchased 170 acres of land between the Des Plaines River and a county forest preserve on the far western edge of the district. Site development began in 1975, and the first students walked through the doors of the new building for summer school classes in June 1980. Major additions were completed in 1983 and 1995. Also in 1980, the College leased, and subsequently purchased, Niles East High School in Skokie, in the eastern part of the district. The College eventually demolished the high school and opened a brand new facility in 1995. In 2006, the Ray Hartstein Campus (RHC) in Skokie opened the Art, Science, and Technology Pavilion. In 2012 the College broke ground for a new Science and Health Careers (SHC) Building on the Des Plaines campus. The first classes are scheduled in the SHC Building for the Spring 2015 Semester. Extensive remodeling will take place in spaces vacated on the Des Plaines campus as programs move to the new building.

Educational Programs and Services In accordance with the Illinois Community College Act, Oakton provides, at a minimum, the following educational programs and services: Baccalaureate and general education for students planning to transfer to four-year

colleges and/or to earn an associate degree in the liberal arts, science, engineering, or fine arts.

Occupational education to provide students with career training suitable for obtaining

employment or enhancing occupational skills.

General or developmental studies for students requiring additional preparation before they can begin college-level education.

Continuing education for residents, employers, and employees of the community

desiring classes without having to enroll in formal college-level courses.

Public service activities to meet specialized needs of the community; such activities may include workshops, seminars, and customized employee training programs offered on or off campus.

Student services, such as counseling and advisement, testing, and tutoring.

7

About Oakton

Oakton’s external environment is shaped by trends and characteristics of residents, businesses, educational institutions, public agencies and governments, other organizations and the economy. The external environment provides the setting within which the College develops and offers programs and services that respond to student, employer, and community needs. The external environment also affects resources available to the College. To learn about the external environment, Oakton holds numerous conversations with local, state, and national leaders; convenes meetings with employers; reviews public and professional literature; and analyzes data and information about the area, the state, and the global economy. Based on the above studies, the College identifies these important characteristics: Geographic Location Oakton Community College includes Maine, Evanston, New Trier, Niles, and Northfield Townships and serves an estimated population of approximately 440,000 living in the communities of Des Plaines, Evanston, Glencoe, Glenview, Golf, Kenilworth, Lincolnwood, Morton Grove, Niles, Northbrook, Northfield, Park Ridge, Skokie, Wilmette, and Winnetka. The College also serves one square mile of Wheeling township and small portions of Norwood and Leyden townships. With campuses in Des Plaines and Skokie, Oakton also offers continuing education classes at locations throughout the district and distance learning courses via the Internet and interactive television. Both campuses are conveniently located, close to major roadways leading into Chicago as well as to all parts of the Chicago metropolitan area, Wisconsin, and Indiana. Students also have access to public transportation including Metra commuter trains and Pace bus routes. The College's educational neighbors include College of Lake County to the north, William Rainey Harper College to the west, and Triton College and City Colleges of Chicago to the south. Population Stable in terms of size, the College’s district population is not expected to change significantly. However, the area is becoming increasingly diverse with respect to ethnicity, race, nation of origin, culture, religion, educational background, English language competency, and household composition (for example, single-parent families and multiple generation households). For the most part, district residents are well-educated and upper middle class. For example, 51 percent of adults age 25 and above have a college degree, compared to 30 percent statewide and 27 percent nationally. According to the 2010 U.S. Census the estimated 2008 median household income in Oakton’s district was $83,100 compared to $56,853 statewide and $53,046 nationally.

8

The population is white (72 percent), Asian (14 percent), Hispanic/Latino (8 percent), Black or African-American (5 percent), and all other groups including two or more races (1 percent). The decade from 2000 to 2010 saw an increase in Asian, Hispanic/Latino, and ‘other’ or ‘two or more races’ residents. Education K-12 public school systems are strong, and Oakton’s feeder high school students are the most recruited college-bound students in the country. As many as 97 percent of high school graduates pursue postsecondary education. The district also contains a number of private and parochial schools that offer all levels of education through high school. K-12 officials report an increasing number of students with special needs, including students with physical, emotional, and/or learning disabilities. The number of school-age children is stable, and schools do not anticipate significant growth. Shifting national perceptions about higher education as a private good to benefit individuals, rather than a public good to benefit society, play out in reduced public financing of higher education and greater reliance on student tuition and fees. Oakton’s good fortune to have a strong tax base buffers the College from the most dramatic effects of reduced state funding, but concerns remain that the state may change its funding formula, threatening the ability of colleges in districts like Oakton’s to benefit from robust local tax bases. An additional concern centers on the taxpayers, who, faced with reduced home values and increased property taxes, may resist supporting public institutions as taxes rise and as assessed valuations fall due to the tax cap “guaranty.” This “guaranty” allows the College to levy at the previous year’s amount plus 5% or inflation (whichever is lower) regardless of (any) decline in assessed valuation. Explicit state and national mandates call for more college graduates. Shortly after the presidential election in 2008, the Obama administration set a goal for five million more degrees/certificates by 2020 as compared to 2010. The State of Illinois has set a goal that 60 percent of Illinois adults will have a college degree or certificate by 2025, compared to the current 43 percent. Technology continues to evolve and expand, with what seems to be a never-ending array of new applications, equipment, and uses. Colleges and universities approach technology from multiple directions: as a tool to enhance learning and teaching; as the subject of study; and as a means to improve efficiency and effectiveness in managing the organization and delivering services to multiple constituencies. Online education has exploded in the number of colleges and universities offering distance learning courses and the number of students taking them. At the same time, social media has transformed the way people communicate for personal, educational, and professional reasons. Business and Industry Employers indicate the need for employees who not only have technical skills, but also the ability to communicate, work in teams, think critically, solve problems, and demonstrate responsibility. A new development focused on nanotechnology and

9

biotechnology recently opened in the Illinois Science and Technology Park, providing the College opportunities for partnerships with the Village of Skokie, North Suburban Educational Region for Vocational Education and Forest City Enterprises, the major developer associated with nanotechnology in the country. The economic base and labor markets within Oakton’s district comprise a diverse array of businesses, industries, and service providers. At the same time, the financial turmoil during the recent years has led to increased home foreclosures, high unemployment, and economic uncertainty for many district residents. Identifying jobs for which to retrain workers, with confidence they will be able to obtain employment remains challenging. Fields in which job opportunities exist, such as manufacturing, appear not to be aligned with the interests of district residents. The Area With the area’s largely developed geographical base, minimum potential exists for added housing. Recently, many communities have again witnessed older housing being demolished and replaced with new single family or multiple family residences. This “teardown” activity had slowed significantly as the economy shrank and housing prices declined. The district’s local public governments, as well as library and park districts, have traditions of high-quality service and relative autonomy. An increasing number of schools, organizations, and commercial vendors are offering education and training to residents and employees through distance education, in traditional classroom settings, and at the workplace. More than 50 postsecondary institutions lie within easy driving distance of Oakton with many others offering online classes to district residents. Financial Base The assessed value of taxable property in Oakton’s district is $18.9 billion. This reflects a decline from assessed values of $21.6 billion in tax levy year 2012 and a high of $28.5 billion in tax levy year 2009. The Property Tax Extension Limitation Law (PTELL) limits the increase in property tax extensions to five percent, or the percent increase in the national Consumer Price Index (CPI) for the prior year, whichever is less. Adjustments are made for annexations, mergers, disconnections, new construction, and increases approved by taxpayer referendum. Oakton’s district houses more than 25,000 businesses of all sizes. The labor market includes substantial numbers of employees in service, financial, health care, and related occupations at all levels. Economic Modeling Specialists, Inc, a national labor market research company, estimates Oakton’s district has more than 400,000 full-and part-time jobs. Until the last couple of years, unemployment has been low. Illinois is experiencing serious financial issues, and support for higher education remains problematic. Oakton’s revenue from the state continues to be uncertain as to both the amount and reliability of state funding for higher education, including the availability of the Illinois MAP (Monetary Award Program) grant for student financial assistance. Given

10

its significant deficit, Illinois’ financial health undoubtedly will not improve substantially over the next several years. The fiscal situation at the federal level also is creating uncertainties regarding grant funding for special programs such as those supported through the National Science Foundation and the Department of Education. Additionally, grant applications and requirements for reports on grants received are becoming more complex and time consuming. Students are graduating from college with high debt and poor job prospects, prompting prospective students to begin questioning the value of postsecondary education. Doubts about qualifying for student financial assistance; e.g., the federal Pell grant and the Illinois MAP grant, place additional financial pressure on students and their families. At the same time, state agencies, legislators, accreditation agencies, the federal government, and the public demand more accountability from schools at all levels, including colleges and universities. Employees More than 50 full-time faculty and 65 staff retired in the period 2010-2014. New faculty and staff will provide fresh ideas and build on Oakton’s history of employee engagement and institutional loyalty. Thinking more creatively, the College now recruits more broadly for employee replacements, especially for full-time faculty, and includes provisions for seeking full-time faculty from adjuncts/part-time faculty. Accreditation Oakton Community College is accredited by The Higher Learning Commission of the North Central Association of Colleges and Schools (230 South LaSalle Street, Suite 7-500, Chicago, IL 60604; 312.263.0456; www.ncahlc.org). The College is recognized by the Illinois Community College Board and is a member of the American Association of Community Colleges, as well as numerous professional organizations.

Facilities and Services One College, Four Campuses As noted above, Oakton Community College maintains physical campuses in Des Plaines and Skokie. Occupying 193 total acres, the College’s properties include 25 acres of lake and drainage, 30 acres of athletic fields, 29 acres of parking lots, a two-acre prairie restoration area with the balance occupied by buildings.

11

Oakton’s scenic Des Plaines campus at 1600 East Golf Road, surrounded by woodlands and prairie, includes a 410,000 square foot main building and a 7,300 square foot grounds maintenance building. The main building will also house the new Enrollment Center which integrates student services for admission, advising and counseling, financial aid, and registration and records functions in one convenient location. At approximately 13,800 square feet, the enrollment center also incorporates all functions now scattered across the Des Plaines building into a facility that is modeled after the successful design implemented at the RHC. The College houses 61 classrooms, 64 labs, 285 offices, and a 9,500 square foot gymnasium. Other facilities include a Performing Arts Center, with a 285-seat theater; the Koehnline Museum of Art; an Early Childhood Demonstration Center; and a Fitness Center. (See Capital Expenditures for additional information about the Science Health Center) Currently, a new Science and Health Careers Center is under construction on the Des Plaines campus which will meet contemporary and emerging science and health career educational standards, and will house the College’s anatomy and physiology, biology, chemistry, earth science, medical laboratory technology, nursing, physics, and physical therapy assistant programs. The Center broke ground in April 2012. Located on the northeast side of the existing campus, 93,000-square-foot facility will feature sophisticated labs; flexible, light-filled classrooms; enhanced technology; and abundant lab preparation and storage space. The building is scheduled for completion in November 2014 and classes are scheduled for Spring 2015. The RHC in Skokie, situated on 21 acres at 7701 North Lincoln Avenue, is home to 34 classrooms, 34 labs, and 86 offices. In 2006, the College constructed the Art, Science, and Technology Pavilion which houses Oakton’s programs in art and graphic design, computer networking and systems, computer technology and information systems, electronics, engineering, and manufacturing. The Pavilion’s architect, Ross Barney, earned a “citation of merit” in the Distinguished Building category from the Chicago chapter of the American Institute of Architects. A $75,000 Illinois Clean Energy Fuel Foundation grant enabled the firm to incorporate numerous energy efficient features into the Pavilion design, including building materials that reduce heat transfer; occupancy sensors for lighting and temperature control; low flow technologies to reduce water consumption; and bamboo flooring and other sustainable materials. With rapidly changing technologies putting a new emphasis on alternative course delivery, Oakton offers an “electronic” campus, with distance learning and online education. The College has been at the forefront of this digital revolution, developing a wide variety of quality, innovative, online courses to serve the needs of an increasingly diverse student body. Nearly all general education requirements for the Associate in Arts or Associate in Science degrees can be completed entirely through online courses at Oakton. In the Fall 2013 semester, 9% of students took courses exclusively online and 13% of students took a combination of on-campus and online courses.

12

The College also provides a “neighborhood” campus represented by the Continuing Education, Training, and Workforce Development programs delivered through the Alliance for Lifelong Learning and the Business Institute. Historically an Illinois leader in adult and continuing education, Oakton’s noncredit program serves more than 38,000 people annually, with 19,600 in noncredit courses and workshops and at least 8,700 more in community service offerings. Through a unique partnership with all but one of the local high school districts and other community groups, the Alliance for Lifelong Learning currently offers courses at more than 150 locations. Educational Services Approximately 53,000 students enroll in Oakton’s credit and noncredit courses each year, including both courses approved by the Illinois Community College Board (ICCB) and personal interest courses that do not require state approval. Of the enrolled students, more than 15,000 take Oakton credit courses annually, with fall term enrollments of more than 10,300. Many other individuals connect with Oakton by attending an array of special programs, athletic competitions, and cultural events, or by participating in the activities sponsored by outside groups that lease Oakton’s facilities. Students enroll at the College for a variety of reasons. Forty-five percent of Oakton’s students register in transfer programs, while 35 percent pursue career and technical education (CTE) programs, and 20 percent remain undecided. However, students are not always clear about the distinction between transfer and CTE programs, particularly in fields such as business. For example, a student who wants to earn a baccalaureate degree in marketing may indicate a marketing major at Oakton, though the College’s marketing program falls into the CTE domain, and the A.A.S. does not transfer to baccalaureate colleges of business. (It is important to note the courses taken by this student do transfer to baccalaureate colleges of business.) Dedication to quality and innovation characterizes the entire scope of Oakton’s credit course offerings and programs. The College’s 21 baccalaureate departments offer associate degrees in liberal arts (A.A.), science (A.S.), engineering (A.S.E.), art or music (A.F.A.) and education (A.A.T.). In addition, more than 100 certificates are available through 36 career programs. Oakton participates in the Illinois Articulation Initiative (IAI), an agreement among Illinois public and private colleges and universities to identify freshman and sophomore level courses in a number of majors and honor a general education core curriculum. To facilitate ease of transfer for interested students, Oakton has negotiated articulation, 2+2, and dual admission agreements with more than 20 four-year colleges and universities. A substantial number of students enter Oakton unprepared for college. Many may lack knowledge about how to navigate higher education or be unable to overcome the economic challenge to pay for their education. Others need additional academic skills to succeed in college-level courses. For example, 30 percent of recent high school graduates place into developmental writing, and 66 percent place into developmental math, including intermediate algebra. These figures comport with those found at

13

community colleges across the nation. In Fall 2013 Oakton joined Achieving the Dream, a national initiative to improve student success, especially the success of minority and low-income students. The associate’s degree appears to be less appealing than a bachelor’s degree, as evidenced by the significant number of students who transfer prior to earning the associate’s degree and the large cadre of students who take CTE courses but do not complete a degree or certificate. Moreover, except in selected fields such as health care careers, students can enter the labor market without earning an official credential. More students from other countries enroll with different cultural and family expectations and a lack of understanding about higher education in the United States. They experience cross-pressures to assimilate, and at the same time, honor the culture with which they identify. A substantial number of Oakton students enroll part time, and even full-time students often take less than 15 credit hours per semester, thereby extending the time to earn a degree well beyond two years after entry. Student Services The College also provides other services to insure that students enjoy a successful, well-rounded, and supportive college experience. College initiatives to improve student success are underway (e.g., the reorganization of developmental mathematics known as RoadMATH; expanded orientation for new full-time, traditional-aged students; and recommendations for a variety of support services from the Student Success Working Group). Preliminary data about the success of the new initiatives show much promise. Achieving the Dream initiatives will expand and refine the Student Success Working Group projects. The Learning Center helps students who want to develop, improve, and refine their learning skills. The Center offers tutoring in a multitude of subject areas, as well as workshops focused on grammar, writing mechanics, and research papers. Staff place special emphasis on helping English as a Second Language students through tutoring, conversation groups, and workshops and provide assistance with academic counseling, financial aid, and registration. Students also may take College 108, a success seminar that enhances academic skills, interpersonal adjustment, cultural understanding, and career awareness. All students must take assessment tests in English, mathematics, and certain other subject areas. The College is witnessing increased numbers of students with documented disabilities (physical, emotional, learning), and they and their families have differing expectations for Oakton to serve them. These requests range from sign language interpreters, to more time for test taking, to classroom note taking and other services.

14

Other services also foster student development, including special programs for adults and older returning students. Career Services provides information about work-study, internships, apprenticeship programs, government jobs, volunteer opportunities, and current employment opportunities within the greater Chicago area. Career Services also manages all student employees. Counselors and Academic Advising offer professionally trained staff who help students with education and career planning as well as those with issues that might interfere with personal and academic growth. Also available are a robust range of student activities such as clubs and organizations, intercollegiate and intramural athletics, and student government, which represents student interests to the administration, faculty, and Board of Trustees. An elected student represents the Student Government Association by serving as an advisory-voting member of the Board of Trustees. The Office of Student Life also supports social and entertainment events for the campus and the College community.