PRESENT AND FUTURE OF ARGENTINE MINING · PRESENT AND FUTURE OF ARGENTINE MINING. REGIONALLY...

24

PACHON – SAN JUAN XXIII Reunión Plenaria del Comité Mixto Empresario Argentino – Japonés Diciembre 5, 2014 PRESENT AND FUTURE OF ARGENTINE MINING

Transcript of PRESENT AND FUTURE OF ARGENTINE MINING · PRESENT AND FUTURE OF ARGENTINE MINING. REGIONALLY...

PACHON – SAN JUANXXIII Reunión Plenaria del ComitéMixto Empresario Argentino – Japonés

Diciembre 5, 2014

PRESENT AND FUTURE OF ARGENTINE MINING

REGIONALLY UNBALANCED

RAIL NETWORK

AND POPULATION

DENSITY

Jujuy, Salta, Catamarca,

Tucuman and Sgo. del Estero

Corrientes, Chaco, Misiones

and Formosa

Mendoza, S. Luis, La Rioja

and S. Juan

Chubut, R. Negro, La Pampa,

Sta. Cruz, Neuquén and T. del

Fuego

Buenos Aires.

37%

15%

14%

11%

3%

Córdoba, Sta. Fé and E. Ríos

20%

Production Value

USD 510,000,000

Export Value

USD 30,000,000

Argentine

Mining

PAMPAS REGION

• 20% Territorial area

covered

• 75% National GDP

• 83% Industrial

Manufacturing Exports

(MOI)

• 81% Agricultural

Manufacturing Exports

(MOA)

• 55% Primary

Products Exports

• 65% Total Population

• 67% Economically

Active Population

(PEA)

• 57% Mining

Production Value

1990

Countries with Potential Geological Mining Favorable

Source: Mining Journal

01 CHINA

02 PERU

03 FILIPINAS

04 BRASIL

05 CHILE

06 ARGENTINA

07 MEXICO

08 BOLIVIA

09 VENEZUELA

10 BIRMANIA

11 INDONESIA

12 RUSIA

13 ZAIRE

14 COLOMBIA

15 TAILANDIA

16 ECUADOR

Prospection

ARGENTINA Initial Exploration

Advanced Exploration

CHILE Project Feasibility

PERU (prospectives reserves )

BRASIL Construction

MEXICO Operation / Production

Mining Business Stages

Main Exploration AreasMINING GEOLOGIC MAP

AREA 6

AR

EA

5

AR

EA

4A

RE

A 3

AREA 1

MAIN EXPLORATION AREAS

Area 1: Santa Cruz

Area 2: Río Negro and Chubut

Area 3: Neuquén and Mendoza

Area 4: Mendoza, San Juan and

La Rioja

Area 5: La Rioja and Catamarca

Area 6: Catamarca, Salta and Jujuy

Main Exploration Areas

Iron

Sn - W - Be - Li - NbPrincipal districts

Copper

Gold

Polymetallic

Lead - Zinc

JUJUY 9.600 km2 > 30.000 km2SALTA 5.000 km2 > 65.000 km2CATAMARCA 12.000 km2 > 75.000 km2LA RIOJA 13.450 km2 > 50.000 km2SAN JUAN 32.600 km2 > 60.000 km2CORDOBA 3.400 km2 > 40.000 km2MENDOZA 56.000 km2 > 75.000 km2SAN LUIS 2.200 km2 > 25.000 km2NEUQUEN 17.000 km2 > 50.000 km2RIO NEGRO 7.000 km2 > 70.000 km2CHUBUT 8.000 km2 > 75.000 km2SANTA CRUZ 15.070 km2 > 75.000 km2T. DEL FUEGO 1.600 km2 > 10.000 km2OTHER ... > 50.000 km2

PROVINCESCOVERAGE OF

EXPLORATION

MOST POTENTIAL

MINING AREAS

TOTAL 183.000 km2 > 750.000 km2

PROSPECTED AREAS

MINIMUM FREE

ARES: 75%

MINING POTENTIAL

China -

Japón

Australia

Canadá

USA

Mexico

Peru

Chile

Mining Investment Flow

Argentina

Brasil

Inglaterra

10%

Rest of Asia

8%

USA

6%

Rest of Europa

and Asia

9%

Canada

49%

Australia 12%

América Latina

6 %

Companies with Exploratory Activities in Argentine

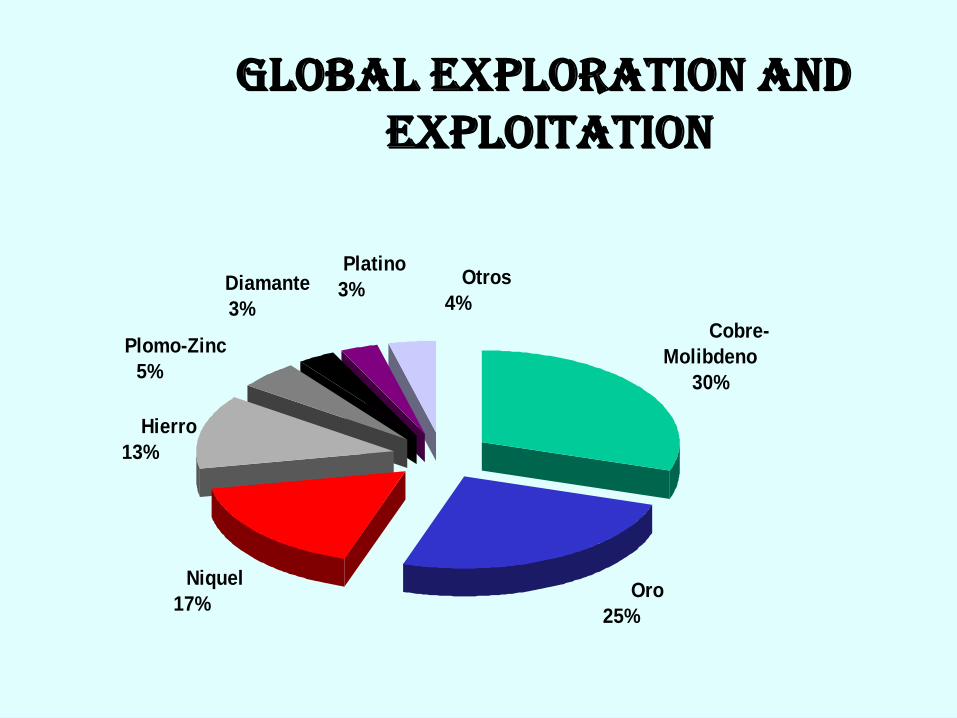

Cobre-

Molibdeno

30%

Niquel

17% Oro

25%

Hierro

13%

Otros

4% Diamante

3%

Plomo-Zinc

5%

Platino

3%

Global Exploration and Exploitation

MINING INTEGRATIONARGENTINA – CHILE

Mining Integration Treaty Argentina - Chile

• PROMOTE THE EXPLORATION AND EXPLOITATION OF MINING RESOURCES ALREADY EXISTING IN SCOORDILLERA AREAS

• FACILITATE ACTIVITIES IN THE AREA AND PEOPLE AND GOODS FRONTIER TRANSIT

• PERMITS THE USEGE OF ALL CLASS OF NATURALRESOURCES AND INFRASTRUCTURE

• PROVIDES A COORDINATION FRAME OF EACH STATE TAXING ORDER

• PROMOTE THE EXCHANGE OF IMPORTANT INFORMATION IN RELATION TO MAIN ENVIRONMENTAL EFFECTS WHICH MINING BUSINESS COULD CAUSE

CH

ILE

BUENOS

AIRESLA PAMPA

RIO

NEGRO

CHUBUT

SANTA CRUZ

NE

UQ

UE

N

ME

ND

OZ

A

SAN

LUIS

SAN

JUAN

CO

RD

OB

A

LA

RIOJA

SA

NT

A F

E

EN

TR

E

RIO

S

SANTIAGO

DEL

ESTERO

TUCU -

MAN

SALTA

JUJUY

CHACO

ESTIMATED

ENLARGEMENT

AREA

Profile Concept

Cu

Cu/Mo

Au

CHILE ARGENTINA

Pacific Ocean

5.500 m

3.000 m

0 m

Bajo de la AlumbreraAgua Rica

Cu, Au, Mo

Pascua Lama

Au

Au : Gold

Cu: Copper

Mo : Molybdenum

References

R ío Turbio

SURVEYING -GEOLOGICAL

Pachón

Taca Taca

Pelambres

Cu/Mo

Escondida

URUGUAY

BRASIL

1

2

3

4

5

6

7

8

9

AREAS OF COMMON MININGINTEREST ETWEEN

ARGENTINE and CHILE

LEGEND1- Iron/ Lithium: El Laco /Atacama – Salta/Jujuy/Catamarca

2- Copper: La Escondida – Taca Taca

3- Gold: Faja de Maricunga- Valle Ancho

4- Gold: Faja de El Indio. Pascua-Lama/ Los Helados /

Filo del Sol – José María

5- Copper: Pelambres – Pachón

6- Copper: Faja Cuprífera Elisa

7- Pollimetalics: Grupo Monte S. Lorenzo

8- Pollimetalics: Aldea Beleiro

9- Coal: Río Turbio

Integration Paths

URUGUAY

Bajo la Alumbrera

Cerro Vanguardia

El Pachón

Salar del Hombre Muerto

Agua Rica

Pirquitas

RESULTS

ARGENTINE

MINING

Cerro Negro

Río Colorado

Veladero

Salar Olaroz

Sierra Grande

ADEQUACY OF THE MINING CODE 1993- 1996

LAW Nº 24.498

MINING UPDATE Removal of archaic institutions of the Mining Code (MC)

Promotion of technical innovation

Deregulation of nuclear mining

LAW Nº 24.585

ENVIRONMENTAL PROTECTION Provincial enforcement authority

Balance between mining production and environment

Environmental presenvation. Information/approval

Prior to the commencement of the activity.

COMPLEMENTARY LAWSLAW Nº 24.196 /25.161/ 25.429

MINING INVESTMENTS Fiscal Stability

International price of equipments

Promotion of Risk investments

Pithead value

LAW Nº 24.224

MINING REORGANIZATION Geological mapping

Institutionaliation of the Federal Mining Council Advisory Board

(COFEMIN )

Mining tax reorganization

LAW Nº 24.228

FEDERAL MINING AGREEMENT Unification of administrative proceedings

Large scale exploration allowed

Tax Elimination

LAW Nº 24.402

VAT FINANCING Capital Goods Purchase

Infrastructure Works

Advanced Repayment

LAW 24.466

NATIONAL BANK OF GEOLOGICAL

INFORMATION It centralises the Public Geological information of the Country

at the Mining Secretary.

LAW Nº 24.523

NATIONAL MINING TRADE SYSTEM Creation of a user-provider system for minerals trading under the

unit of the National Mining Secretariat.

LAW 24.695

NATIONAL BANK OF MINING INFORMATION Human Resources and equipment information bank at the

Mining Secretariat

LAW 24.227

BICAMERAL COMMISSION Commission made up for 4 Senators and 4 Representatives

4 7

MINING EXPLORATIONFOREIGN COMPANIES

0

200000

400000

600000

800000

1000000

1200000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

67

0.0

00

17

00

0

20

00

0

EVOLUTION OF DRILLED METERS IN THE EXPLORING MINING ACTIVITY SINCE 1992 - 2013

73

00

0

11

0.0

00

15

0.0

00

18

1.0

00

24

0.0

00

23

5.0

00

23

0.0

00

16

5.0

00

13

5.0

00

15

6.0

00

25

0.0

00

41

0.0

00

47

8.5

00 6

00

.00

0

1.0

50

.000

98

5.0

00

32

0.0

0045

0.4

72

73

0.0

00

BUENOS AIRES:

1- PLANTA DE PELLETIZACION (Dolomita en pellets)

2- PLANTA LAMALI (Cemento)

CATAMARCA:

3- SALAR DEL HOMBRE MUERTO (Cloruro y carbonato de litio)

4- BAJO DE LA ALUMBRERA (Concentrado de cobre, bullión dorado)

5- AGUA RICA (Cu – Mo)

CHUBUT:

6- PORFIDOS VARIAS EMPRESAS

7- NAVIDAD (Ag- Pb)

8- CORDON DE ESQUEL (Au – Ag)

CORDOBA:

9- PLANTA MINETTI (Cemento)

JUJUY:

10- MINA AGUILAR (zinc, Plata, concentrado de plomo)

11- LOMA BLANCA (Boratos naturales)

12- PIRQUITAS (Sn- Ag)

LA PAMPA:

13- PLANTA DURLOCK (Placas de yeso – cartón)

MENDOZA:

14- YESOS KNAUF (Placas de yeso – cartón)

15- SAN JORGE (Cu –Au)

16- POTASIO RIO COLORADO (K)

17- DON SIXTO (Au)

NEUQUEN:

18- ANDACOLLO (Au – Ag)

RIO NEGRO:

19- SIERRA GRANDE (hierro)

20- CALCATREU (Au – Ag)

SALTA:

21- BORATOS VARIAS EMPRESAS

22- SALAR DE RINCON (Li – K)

23- LINDERO (Cu- Au)

SAN JUAN:

24- PLANTAS DE CAL

25- VELADERO (Au)

26- PASCUA LAMA (Au)

27- GUALCAMAYO (Au)

28- PACHON (Cu – Mo)

29- CASPOSO (Au – Ag)

SANTA CRUZ:

30- CERRO VANGUARDIA (Bullión dorado)

31- CERRO MORO (Au- Ag)

32- CERRO NEGRO (Au – Ag)

33– SAN JOSE – HUEVOS VERDES (Ag)

34- VIRGINIA – SANTA RITA (Ag- Au)

35- MANANTIAL ESPEJO (Au)

URUGUAY

BRASIL

10

3

4

24

929

13

6

30

21

Producción

11

12

527

25

28

12

8

18

Factibilizado

26

35

14

16

32

19

PROJECTS IN PRODUCTION AND FEASIBLE23

15

17

7

20

3134

22

• SCENERY 1992

PRODUCTION GROSS VALUE:

u$s 434 millions

EXPORTS: u$s 16 millions

FOREIGN ENTERPRISES: 4

SURFACE TO EXPLORE: In government

hands (Unmoved) 70.000 Km2

ANNUAL AVERAGE OF

EXPLORATION DRILLINGS 70-92:

Private: 7.000 meters

Government: 25.000 meters

• SCENERY 2013

PRODUCTION GROSS VALUE:

u$s 4.924 millions

EXPORTS :

u$s 4.084 millions

FOREIGN ENTERPRISES: 157

SURFACE TO EXPLORE: Concessions

Private 183.000 km2

ANNUAL AVERAGED DRILLINGS

EXPLORATION YEAR 2013

PRIVATE: 320.000 meters

Main Indicators of Mining Sector Years 1992 – 2013

SCENARIO OF INVESTMENTS WITH STATE POLICY 2015 – 2025

Minera Alumbrera - Catamarca

1- Companies with mining prospects under development (*) 157

A- Foreign (85%) 133

B- Domestic (15%) public and private 24

2- Mining Prospects under development 435

A- Prospection 46,2 %

B- Initial Exploration 36,25 %

C- Medium-Advanced Exploration 8,0 %

D- Prefeasibility/ Feasibility 5,75 %

E- Development / Production 3,8 %

3- Argentine geological-mining potential 750.000 km2

A- Mining Properties ( prospection-exploration ) 183.000 km2

B- Total drillings made during 2013 (exploration ) 320.000 m

C- Total investments (USD) during 2013 (exploration) 106 million

(*) Only exploration companies, taking into account that there are another 50 junior

foreign (brokers).

ARGENTINE MININGCURRENT SITUATION

The potential investments considered for t his decade are product of the development status

of existing mining projects, which should be technically feasible in full in 2017 at the latest.

The investment decision shall depend on:

1- The macro-political, macroeconomic and sectoral conditions to be established by future

Argentine Authorities.

2- The resolution of interprovincial conflicts that are currently shaping the provincial

paralysis and the under development of previously considered mining projects.

3- The global market conditions, commodity prices, war conflicts, country constraints and

regional hegemony.

4- Corporate decision (credibity, priorities, availabity of fiunds, etc.).

POTENTIAL INVESTMENTS IN MINING 2015 -2025

POTENTIAL INVESTMENTS IN MINING 2015 -2025

Metal Mining Exploration USD 4,000 million

(mainly foreign companies)

Metal and Non metal Mining Exploration USD 60,694 million

(mainly foreign companies)

Traditional Non Metal Mining Exploration USD 1,200 million

(foreign and domestic S&MEs) _____________

Total Investment (2015-2025) USD 65,894 million

Total Estimated Value of Production / Year USD 10,978 million

which would increase as from 2025

THANK YOU VERY MUCH

COMITÉ MIXTO EMPRESARIO ARGENTINO – JAPONÉS