Prepared For Financial Goal Plan Jim and Anne Sample ...

76

Financial Goal Plan Prepared by: Baird Advisor Financial Advisor Private Wealth Management Prepared For Prepared on January 29, 2019 Jim and Anne Sample

Transcript of Prepared For Financial Goal Plan Jim and Anne Sample ...

Financial Goal Plan

Prepared by:

Baird AdvisorFinancial AdvisorPrivate Wealth Management

Prepared For

Prepared on January 29, 2019

Jim and Anne Sample

Table Of Contents

IMPORTANT DISCLOSURE INFORMATION 1 - 7

Summary of Goals and Resources

Personal Information and Summary of Financial Goals 8 - 9

Worksheet Detail - Health Care Expense Schedule 10 - 13

Net Worth Summary - All Resources 14

Net Worth Detail - All Resources 15 - 16

Resources Summary 17 - 18

Tax and Inflation Assumptions 19

Model Portfolio Table 20

Worksheet Detail - Allocation Comparison 21 - 22

Employer Stock Plans

Stock Options 23 - 24

Stock Options Summary 25 - 28

Restricted Stock Summary 29 - 30

Results

What If Worksheet 31 - 38

Worksheet Detail - Social Security Analysis 39 - 40

Worksheet Detail - Special Asset Test 41

Worksheet Detail - Inside the Numbers Final Result 42

Worksheet Detail - Combined Details 43 - 46

Worksheet Detail - Retirement Distribution Cash Flow Chart 47 - 55

Risk Management

Life Insurance Needs Analysis 56

Disability Needs Analysis - Jim 57 - 59

Long-Term Care Needs Analysis - Jim 60

Estate Analysis

Estate Analysis Results Combined Summary 61

Estate Analysis Results Flowchart 62 - 63

Star Track

Star Track 64

Glossary 65 - 68

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 1 of 68

The return assumptions in MoneyGuidePro are not reflective of any specific product, and donot include any fees or expenses that may be incurred by investing in specific products. Theactual returns of a specific product may be more or less than the returns used inMoneyGuidePro. It is not possible to directly invest in an index. Financial forecasts, rates ofreturn, risk, inflation, and other assumptions may be used as the basis for illustrations. Theyshould not be considered a guarantee of future performance or a guarantee of achievingoverall financial objectives. Past performance is not a guarantee or a predictor of futureresults of either the indices or any particular investment.

IMPORTANT: The projections or other information generated by MoneyGuidePro regardingthe likelihood of various investment outcomes are hypothetical in nature, do not reflectactual investment results, and are not guarantees of future results.

MoneyGuidePro results may vary with each use and over time.

In consideration for the receipt of this financial report or plan (the “Report” or “Plan”),each recipient (“you”), hereby understands, acknowledges, and agrees as follows:

Important Information about Baird’s Obligations To You When Providing FinancialPlans and Financial Planning Services

Robert W. Baird & Co. Incorporated (“Baird”) offers financial plans and financial planningservices to clients in two ways: (1) as a brokerage service, provided in Baird’s capacity asbroker-dealer; and (2) as an investment advisory service, provided in Baird’s capacity asinvestment advisor under the Investment Advisers Act of 1940, as amended (the “AdvisersAct”). There are important differences between brokerage services and investment advisoryservices and Baird’s obligations to clients when it provides those services. Some of thosedifferences are described below. More specific information about those services, and thedifferences between them, is available on Baird’s website at http://www.rwbaird.com/about-baird/disclosures.aspx.

Whether Baird provides financial planning services as broker-dealer or investment advisordepends upon whether or not a client has entered into a written financial planningagreement with Baird. If a client does not enter into a written financial planning agreementwith Baird, then Baird acts as broker-dealer when providing those services. If a client entersinto a written financial planning agreement with Baird, then Baird acts as investmentadvisor when providing those services.

Brokerage Services—Financial Planning Services Provided without a Written FinancialPlanning Agreement

If you have not entered into a written financial planning agreement with Baird for the Planand related financial planning services, you should understand that Baird and your BairdFinancial Advisor do not provide investment advisory services to you or act as a fiduciary toyou under the Advisers Act. Rather, Baird is providing the Plan and related financialplanning services to you in its capacity as a broker-dealer, and Baird’s provision of the Planand financial planning services to you are solely incidental to the brokerage services itprovides to you. In providing services to you as a broker-dealer, Baird must have areasonable basis for believing the recommendations made to you are suitable. Once thePlan is delivered to you, the financial planning services provided to you will be deemed tobe completed, and Baird and your Baird Financial Advisor will have no obligation to updatethe Plan, implement the Plan or monitor the investments in your accounts.

If you would like more information about investment advisory financial planning services, orif you would like to enter into a written financial planning agreement with Baird for thoseservices, please contact your Baird Financial Advisor. You should note that Baird generallycharges a separate financial planning fee for investment advisory financial planning services.

Investment Advisory Services—Financial Planning Services Provided under a WrittenFinancial Planning Agreement

If Baird is providing the Plan and related financial planning services to you under a writtenfinancial planning agreement, Baird acts as a fiduciary to you under the Advisers Act andsuch services constitute investment advisory services subject to the Advisers Act. Thespecific terms and conditions related to the Plan and financial planning services provided toyou will be contained in your written financial planning agreement. Additional importantinformation about Baird, Baird’s Financial Planning Department and your Baird FinancialAdvisor and the advisory services they provide in connection with the Plan is contained inBaird’ Form ADV Part 2A Financial Planning Services Brochure and the Form ADV Part 2BBrochure Supplements for the Financial Planning Department and your Baird FinancialAdvisor (collectively, the “Brochure Documents”). Unless your written financial planningagreement with Baird otherwise provides, the advisory services provided by Baird and yourBaird Financial Advisor to you are limited to advice or recommendations incorporated intothe Plan delivered to you and advice or recommendations made to you, if any, during ameeting relating to the contents of the Plan. Unless Baird has otherwise agreed in writing,the financial planning services provided to you and Baird’s investment advisory relationshipwith you will be deemed to be completed when the Plan is delivered to you, and Baird andyour Baird Financial Advisor will have no obligation to update the Plan, implement the Planor monitor the investments in your accounts. You should refer to your written financialplanning agreement and the Brochure Documents for more specific information.

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 2 of 68

Date of Plan

The information contained in the Plan is provided as of the date shown on the cover pageto the Plan. Baird and its Financial Advisors do not undertake to update the Plan or theinformation contained therein unless they specifically agree to do so in writing. However,Baird reserves the right to amend the Plan should additional information or evidencebecome available. Account values that are shown in the Plan are based on values providedas of a specific date. Actual account values will change on an ongoing basis, and they maybe substantially different from that shown in the Plan.

Use of Third Party Software

The Plan was prepared using MoneyGuidePro Software. While Baird believes thatMoneyGuidePro Software is reliable, Baird makes no representation or guarantee that thecalculations made by the software or the information contained in the Plan are accurate.

Legal and Tax Advice

Baird and its representatives do not provide legal or tax advice to clients. You are stronglyurged to consult with your legal and tax professionals prior to taking any action based uponthe information contained in the Report.

Not an Official Statement of Assets, Debt or Income

The Plan is provided to you for informational purposes only and is not intended, in anymanner, to be an official account statement or an official statement of your assets, debt orincome.

Baird’s Reliance upon Information Provided by You

Baird and your Baird Financial Advisor have prepared the Plan for you using the informationthat you have provided. You are solely responsible for providing information to Baird andyour Baird Financial Advisor reasonably requested by them in order to provide the servicesselected by you and for ensuring the information in this Plan is true and complete. Inproviding the services and preparing the Plan, Baird and your Baird Financial Advisor haveassumed that you have provided true and complete responses to the information requestedby them. Baird and your Baird Financial Advisor have relied upon this information withoutindependent verification. You are responsible for promptly informing your Baird FinancialAdvisor of any inaccuracies or changes in any information you provide. Neither Baird noryour Baird Financial Advisor is responsible for any errors in the Plan or any adverseconsequence arising out of the failure by you to provide true and complete information orto promptly inform your Baird Financial Advisor of any such inaccuracies or changes.

Forward-Looking Projections and Certain Hypothetical Assumptions

The Report contains forward-looking projections that are based upon certain hypotheticalassumptions about future events. Some of these hypothetical assumptions include, withoutlimitation, hypothetical assumptions about future: rates of inflation, interest rates, rates ofreturn, levels of asset appreciation, dividend rates, growth rates, your income andexpenditure amounts, taxes, tax rates, tax filing status, liquidations and divisions ofproperty, and support payments, as applicable. If you would like information about theassumptions made in connection with the preparation of the Report, you should contactyour Baird Financial Advisor. Forward-looking projections illustrate the effects of usingassumptions and should be used only as an aid for planning and decision making. Youshould not interpret forward-looking projections as an indication or guarantee of what willhappen in the future. Baird and its representatives do not make any promise or guaranteethat forward-looking projections or hypothetical assumptions will be realized in the future.You should note that any hypothetical assumption about future events made in the Reportmay not occur as is assumed by the Report. The forward-looking projections contained inthe Report could be materially impacted to the extent actual future events differ from thehypothetical assumptions made in the Report. You are, therefore, cautioned against undulyrelying upon the forward-looking projections contained in the Report.

You and your tax and legal professionals should carefully review the Report andconsider the hypothetical assumptions made before making any decision or takingany action based upon the Report.

Asset, Debt, Income and Expense Information

If the Plan contains assets over which Baird has custody, Baird generally relies upon thirdparty sources, such as third party pricing services, when valuing those assets. In someinstances, such as when Baird is unable to obtain a price for an asset from a pricing service,Baird may obtain a price from its trading desk or it may elect to not price the asset.Obtaining a price from its trading desk may present a conflict of interest. In some cases,Baird obtains prices from the issuers or sponsors of investment products. This frequentlyoccurs with respect to the valuation of alternative investment products. Baird does notconduct a review of valuation information provided by third party pricing services, issuers,or sponsors, and it does not verify or guarantee the accuracy of such information. Valuationdata for investments, particularly alternative investment products, may not be provided toBaird in a timely manner, resulting in valuations that are not current.

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 3 of 68

The Plan contains assets that are not custodied with Baird. Those assets have beenincluded in the Plan at your request and have been valued based solely upon theinformation that you or your agents have provided to your Baird FinancialAdvisor(s). Likewise, all debt, income and expense information included in thePlan has been included in the Plan at your request based solely upon theinformation that you or your agents have provided to your Baird FinancialAdvisor(s). The Plan is useful only if all asset, debt, income and expenseinformation contained in the Plan is accurate. Therefore, you and your tax andlegal professionals should carefully review the Plan and verify the accuracy of allasset, debt, income and expense information before making any decision or takingany action based upon the Plan. Baird and its Financial Advisors do not verify orguarantee the existence of assets that are not under Baird’s custody or theaccuracy of any information provided by you or your agents. Neither Baird nor itsFinancial Advisors are responsible for any adverse consequence arising out ofinformation provided by you or your agents.

The values shown in the Plan could be materially different from prices obtained from othersources. This is especially true for certain types of assets that may be difficult to value, suchas real property, automobiles, jewelry, art, antiques, coins, or other similar assets orcollectibles. Values used in the Plan may vary from prices received in actual transactions andare not firm bids, offers or guarantees of any type with respect to the value of assets, andthe values shown in the Plan may be greater than or less than the amount you wouldreceive if the assets were actually sold.

Characterization and Division of Property; Support Payments

Any characterization of property in the Report as marital property or separate property andany proposed division of property contained in the Report is based solely upon informationprovided by you or your agents. Any proposed division of property contained in the Reportare for settlement and discussion purposes only (i.e., to reflect a proposed settlement offer,possible property division scenarios, etc.). It is not a recommendation of what should bedone. In addition, support calculations contained in the Report are shown for settlementand discussion purposes only. It is not a recommendation of what should be done. You andyour legal professionals should carefully review any such property characterization ordivision or support payments to ensure that they are accurate.

Information that you provided about your assets, financial goals, and personal situation arekey assumptions for the calculations and projections in this Report. Please review theReport sections titled "Personal Information and Summary of Financial Goals", "CurrentPortfolio Allocation", and "Tax and Inflation Options" to verify the accuracy of theseassumptions. If any of the assumptions are incorrect, you should notify your financialadvisor. Even small changes in assumptions can have a substantial impact on the resultsshown in this Report. The information provided by you should be reviewed periodically andupdated when either the information or your circumstances change.

Information Provided by You

MoneyGuidePro Assumptions and Limitations

All asset and net worth information included in this Report was provided by you or yourdesignated agents, and is not a substitute for the information contained in the officialaccount statements provided to you by custodians. The current asset data and valuescontained in those account statements should be used to update the asset informationincluded in this Report, as necessary.

Assumptions and Limitations

MoneyGuidePro offers several methods of calculating results, each of which provides oneoutcome from a wide range of possible outcomes. All results in this Report are hypotheticalin nature, do not reflect actual investment results, and are not guarantees of future results.All results use simplifying assumptions that do not completely or accurately reflect yourspecific circumstances. No Plan or Report has the ability to accurately predict the future. Asinvestment returns, inflation, taxes, and other economic conditions vary from theMoneyGuidePro assumptions, your actual results will vary (perhaps significantly) from thosepresented in this Report.

All MoneyGuidePro calculations use asset class returns, not returns of actual investments.The projected return assumptions used in this Report are estimates based on average annualreturns for each asset class. The portfolio returns are calculated by weighting individualreturn assumptions for each asset class according to your portfolio allocation. The portfolioreturns may have been modified by including adjustments to the total return and theinflation rate. The portfolio returns assume reinvestment of interest and dividends at netasset value without taxes, and also assume that the portfolio has been rebalanced to reflectthe initial recommendation. No portfolio rebalancing costs, including taxes, if applicable,are deducted from the portfolio value. No portfolio allocation eliminates risk or guaranteesinvestment results.

MoneyGuidePro does not provide recommendations for any products or securities.

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 4 of 68

Asset Class NameProjected Return

AssumptionProjected Standard

Deviation

Large Cap Core 7.20% 15.00%

Large Cap Growth 6.70% 16.90%

Large Cap Value 7.30% 14.40%

Mid Cap Core 8.90% 16.50%

Mid Cap Growth 8.60% 20.00%

Mid Cap Value 9.20% 15.60%

Small Cap Core 9.40% 19.30%

Small Cap Growth 9.30% 22.40%

Small Cap Value 9.50% 17.30%

International Equity 7.70% 17.20%

Emerging Markets Equity 9.90% 22.10%

Broad Equity 7.60% 15.20%

Commodities 2.10% 14.60%

REITs 12.20% 18.30%

Global REITs 10.10% 17.60%

Short Term Taxable 1.70% 2.70%

Intermediate Term Taxable 2.30% 4.10%

Long Term Taxable 4.20% 8.60%

Short Term Tax-Exempt 2.15% 3.00%

Short Term Tax-Exempt(Tax-Free)

1.40% 3.00%

Intermediate Term Tax-Exempt 2.92% 3.80%

Intermediate Term Tax-Exempt(Tax-Free)

1.90% 3.80%

Long-Term Tax-Exempt 4.77% 7.10%

Long-Term Tax-Exempt(Tax-Free)

3.10% 7.10%

High Yield Fixed Income 6.30% 8.50%

Global Fixed Income 3.20% 5.40%

Broad Fixed Income 3.20% 5.30%

Asset Class NameProjected Return

AssumptionProjected Standard

Deviation

Cash 0.70% 1.10%

Hedge Funds 6.70% 8.50%

Managed Futures 4.40% 6.40%

Private Equity 13.40% 23.50%

Alternatives - Other 5.80% 7.40%

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 5 of 68

Risks Inherent in Investing

Investing in fixed income securities involves interest rate risk, credit risk, and inflation risk.Interest rate risk is the possibility that bond prices will decrease because of an interest rateincrease. When interest rates rise, bond prices and the values of fixed income securities fall.When interest rates fall, bond prices and the values of fixed income securities rise. Creditrisk is the risk that a company will not be able to pay its debts, including the interest on itsbonds. Inflation risk is the possibility that the interest paid on an investment in bonds willbe lower than the inflation rate, decreasing purchasing power.

Cash alternatives typically include money market securities and U.S. treasury bills. Investingin such cash alternatives involves inflation risk. In addition, investments in money marketsecurities may involve credit risk and a risk of principal loss. Because money marketsecurities are neither insured nor guaranteed by the Federal Deposit Insurance Corporationor any other government agency, there is no guarantee the value of your investment will bemaintained at $1.00 per share, and your shares, when sold, may be worth more or less thanwhat you originally paid for them. U.S. Treasury bills are subject to market risk if sold priorto maturity. Market risk is the possibility that the value, when sold, might be less than thepurchase price.

Investing in stock securities involves volatility risk, market risk, business risk, and industryrisk. The prices of most stocks fluctuate. Volatility risk is the chance that the value of a stockwill fall. Market risk is chance that the prices of all stocks will fall due to conditions in theeconomic environment. Business risk is the chance that a specific company’s stock will fallbecause of issues affecting it. Industry risk is the chance that a set of factors particular to anindustry group will adversely affect stock prices within the industry. (See “Asset Class –Stocks” in the Glossary section of this Important Disclosure Information for a summary ofthe relative potential volatility of different types of stocks.)

International investing involves additional risks including, but not limited to, changes incurrency exchange rates, differences in accounting and taxation policies, and political oreconomic instabilities that can increase or decrease returns.

Report Is a Snapshot and Does Not Provide Legal, Tax, or Accounting Advice

This Report provides a snapshot of your current financial position and can help you to focuson your financial resources and goals, and to create a plan of action. Because the resultsare calculated over many years, small changes can create large differences in future results.You should use this Report to help you focus on the factors that are most important to you.This Report does not provide legal, tax, or accounting advice. Before making decisions withlegal, tax, or accounting ramifications, you should consult appropriate professionals foradvice that is specific to your situation.

MoneyGuidePro Methodology

MoneyGuidePro offers several methods of calculating results, each of which provides oneoutcome from a wide range of possible outcomes. The methods used are: “AverageReturns,” “Historical Test,” “Bad Timing,” “Class Sensitivity,” and “Monte CarloSimulations.” When using historical returns, the methodologies available are AverageReturns, Historical Test, Bad Timing, and Monte Carlo Simulations. When using projectedreturns, the methodologies available are Average Returns, Bad Timing, Class Sensitivity, andMonte Carlo Simulations.

Results Using Average Returns

The Results Using Average Returns are calculated using one average return for yourpre-retirement period and one average return for your post-retirement period. AverageReturns are a simplifying assumption. In the real world, investment returns can (and oftendo) vary widely from year to year and vary widely from a long-term average return.

Results Using Historical Test

The Results Using Historical Test are calculated by using the actual historical returns andinflation rates, in sequence, from a starting year to the present, and assumes that youwould receive those returns and inflation rates, in sequence, from this year through the endof your Plan. If the historical sequence is shorter than your Plan, the average return for thehistorical period is used for the balance of the Plan. The historical returns used are those ofthe broad-based asset class indices listed in this Important Disclosure Information.

Results with Bad Timing

Results with Bad Timing are calculated by using low returns in one or two years, andaverage returns for all remaining years of the Plan. For most Plans, the worst time for lowreturns is when you begin taking substantial withdrawals from your portfolio. The Resultswith Bad Timing assume that you earn a low return in the year(s) you select and then anAdjusted Average Return in all other years. This Adjusted Average Return is calculated sothat the average return of the Results with Bad Timing is equal to the return(s) used incalculating the Results Using Average Returns. This allows you to compare two results withthe same overall average return, where one (the Results with Bad Timing) has low returns inone or two years.

When using historical returns, the default for one year of low returns is the lowest annualreturn in the historical period you are using, and the default for two years of low returns isthe lowest two-year sequence of returns in the historical period. When using projectedreturns, the default for the first year of low returns is two standard deviations less than theaverage return, and the default for the second year is one standard deviation less than theaverage return.

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 6 of 68

Results Using Class Sensitivity

The Results Using Class Sensitivity are calculated by using different return assumptions forone or more asset classes during the years you select. These results show how your Planwould be affected if the annual returns for one or more asset classes were different thanthe average returns for a specified period in your Plan.

Results Using Monte Carlo Simulations

Monte Carlo simulations are used to show how variations in rates of return each year canaffect your results. A Monte Carlo simulation calculates the results of your Plan by runningit many times, each time using a different sequence of returns. Some sequences of returnswill give you better results, and some will give you worse results. These multiple trialsprovide a range of possible results, some successful (you would have met all your goals) andsome unsuccessful (you would not have met all your goals). The percentage of trials thatwere successful is the probability that your Plan, with all its underlying assumptions, couldbe successful. In MoneyGuidePro, this is the Probability of Success. Analogously, thepercentage of trials that were unsuccessful is the Probability of Failure. The Results UsingMonte Carlo Simulations indicate the likelihood that an event may occur as well as thelikelihood that it may not occur. In analyzing this information, please note that the analysisdoes not take into account actual market conditions, which may severely affect theoutcome of your goals over the long-term.

MoneyGuidePro Presentation of Results

The Results Using Average Returns, Historical Test, Bad Timing, and Class Sensitivity displaythe results using an “Estimated % of Goal Funded” and a “Safety Margin.”

Estimated % of Goal Funded

For each Goal, the “Estimated % of Goal Funded” is the sum of the assets used to fund theGoal divided by the sum of the Goal’s expenses. All values are in current dollars. A result of100% or more does not guarantee that you will reach a Goal, nor does a result under100% guarantee that you will not. Rather, this information is meant to identify possibleshortfalls in this Plan, and is not a guarantee that a certain percentage of your Goals will befunded. The percentage reflects a projection of the total cost of the Goal that was actuallyfunded based upon all the assumptions that are included in this Plan, and assumes that youexecute all aspects of the Plan as you have indicated.

Safety Margin

The Safety Margin is the estimated value of your assets at the end of this Plan, based on allthe assumptions included in this Report. Only you can determine if that Safety Margin issufficient for your needs.

Bear Market Loss and Bear Market Test

The Bear Market Loss shows how a portfolio would have been impacted during the worstbear market since the Great Depression. Depending on the composition of the portfolio,the worst bear market is either the "Great Recession" or the "Bond Bear Market."

The Great Recession, from November 2007 through February 2009, was the worst bearmarket for stocks since the Great Depression. In MoneyGuidePro, the Great RecessionReturn is the rate of return, during the Great Recession, for a portfolio comprised of cash,bonds, stocks, and alternatives, with an asset mix equivalent to the portfolio referenced.

The Bond Bear Market, from July 1979 through February 1980, was the worst bear marketfor bonds since the Great Depression. In MoneyGuidePro, the Bond Bear Market Return isthe rate of return, for the Bond Bear Market period, for a portfolio comprised of cash,bonds, stocks, and alternatives, with an asset mix equivalent to the portfolio referenced.

The Bear Market Loss shows: 1) either the Great Recession Return or the Bond Bear MarketReturn, whichever is lower, and 2) the potential loss, if you had been invested in thiscash-bond-stock-alternative portfolio during the period with the lower return. In general,most portfolios with a stock allocation of 20% or more have a lower Great RecessionReturn, and most portfolios with a combined cash and bond allocation of 80% or morehave a lower Bond Bear Market Return.

The Bear Market Test, included in the Stress Tests, examines the impact on your Plan resultsif an identical Great Recession or Bond Bear Market, whichever would be worse, occurredthis year. The Bear Market Test shows the likelihood that you could fund your Needs,Wants and Wishes after experiencing such an event.

Regardless of whether you are using historical or projected returns for all otherMoneyGuidePro results, the Bear Market Loss and Bear Market Test use returns calculatedfrom historical indices. If you are using historical returns, the indices in the Bear Market Lossand the Bear Market Test may be different from indices used in other calculations. Theseresults are calculated using only four asset classes – Cash, Bonds, Stocks, and Alternatives.The indices and the resulting returns for the Great Recession and the Bond Bear Market are:

IMPORTANT DISCLOSURE INFORMATION

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 7 of 68

Because the Bear Market Loss and Bear Market Test use the returns from asset class indicesrather than the returns of actual investments, they do not represent the performance forany specific portfolio, and are not a guarantee of minimum or maximum levels of losses orgains for any portfolio. The actual performance of your portfolio may differ substantiallyfrom those shown in the Great Recession Return, the Bond Bear Market Return, the BearMarket Loss, and the Bear Market Test.

Asset Class Index Great RecessionReturn

11/2007 – 02/2009

Bond Bear MarketReturn

07/1979 – 02/1980

Cash Ibbotson U.S. 30-dayTreasury Bills

2.31% 7.08%

Bond Ibbotson Intermediate-TermGovernment Bonds – TotalReturn

15.61% -8.89%

Stock S&P 500 - Total Return -50.95% 14.61%

Alternative HFRI FOF: Diversified*S&P GSCI Commodity - TotalReturn**

-19.87%N/A

N/A23.21%

*Hedge Fund Research Indices Fund of Funds

**S&P GSCI was formerly the Goldman Sachs Commodity Index

MoneyGuidePro Risk Assessment

The MoneyGuidePro Risk Assessment highlights some – but not all – of the trade-offs youmight consider when deciding how to invest your money. This approach does not provide acomprehensive, psychometrically-based, or scientifically-validated profile of your risktolerance, loss tolerance, or risk capacity, and is provided for informational purposes only.

Based on your specific circumstances, you must decide the appropriate balance betweenpotential risks and potential returns. MoneyGuidePro does not and cannot adequatelyunderstand or assess the appropriate risk/return balance for you. MoneyGuidePro requiresyou to select a risk score. Once selected, three important pieces of information are availableto help you determine the appropriateness of your score: an appropriate portfolio for yourscore, the impact of a Bear Market Loss (either the Great Recession or the Bond BearMarket, whichever is lower) on this portfolio, and a compare button to show how yourscore compares to the risk score of others in your age group.

MoneyGuidePro uses your risk score to select a risk-based portfolio on the Portfolio Tablepage. This risk-based portfolio selection is provided for informational purposes only, andyou should consider it to be a starting point for conversations with your advisor. It is yourresponsibility to select the Target Portfolio you want MoneyGuidePro to use. The selectionof your Target Portfolio, and other investment decisions, should be made by you, afterdiscussions with your advisor and, if needed, other financial and/or legal professionals.

Summary of Goals and Resources

Personal Information and Summary of Financial Goals

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 8 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Jim and Anne Sample

Needs

Retirement - Living Expense10

Jim (2021)Anne (2021)Both Retired (2021-2050)Anne Alone Retired (2051-2051)

6665$425,000$365,000Base Inflation Rate (3.00%)

Health Care10

Both Medicare (2021-2050)Anne Alone Medicare (2051)

$17,177$9,921Base Inflation Rate plus 2.00% (5.00%)

Wants

College - Daughter7

4 years starting in 2021Attending College - Private (4 years)

$50,900Base Inflation Rate plus 2.00% (5.00%)

New Vehicle7

In 2017Recurring every 5 years for a total of 8 times

$40,000No Inflation

Vacation Home5

In 2020 $1,000,000Base Inflation Rate (3.00%)

Personal Information and Summary of Financial Goals

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 9 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Jim and Anne Sample

Wishes

Charitable Gifts3

In 2016Recurring every year until end of plan

$25,000No Inflation

Annual Exclusion Gifts to Brian3

In 2016Recurring every year until end of plan

$14,000Base Inflation Rate (3.00%)

Personal Information

Jim

Male - born 08/29/1955, age 63

Anne

Female - born 05/27/1956, age 62

Married, US Citizens living in WI

Employed - $400,000

Employed - $200,000

• This section lists the Personal and Financial Goal information you provided, which willbe used to create your Report. It is important that it is accurate and complete.

Participant Name Date of Birth Age Relationship

Brian 05/27/1973 45 Child

Emma 01/01/2003 16 Child

Charity Charity

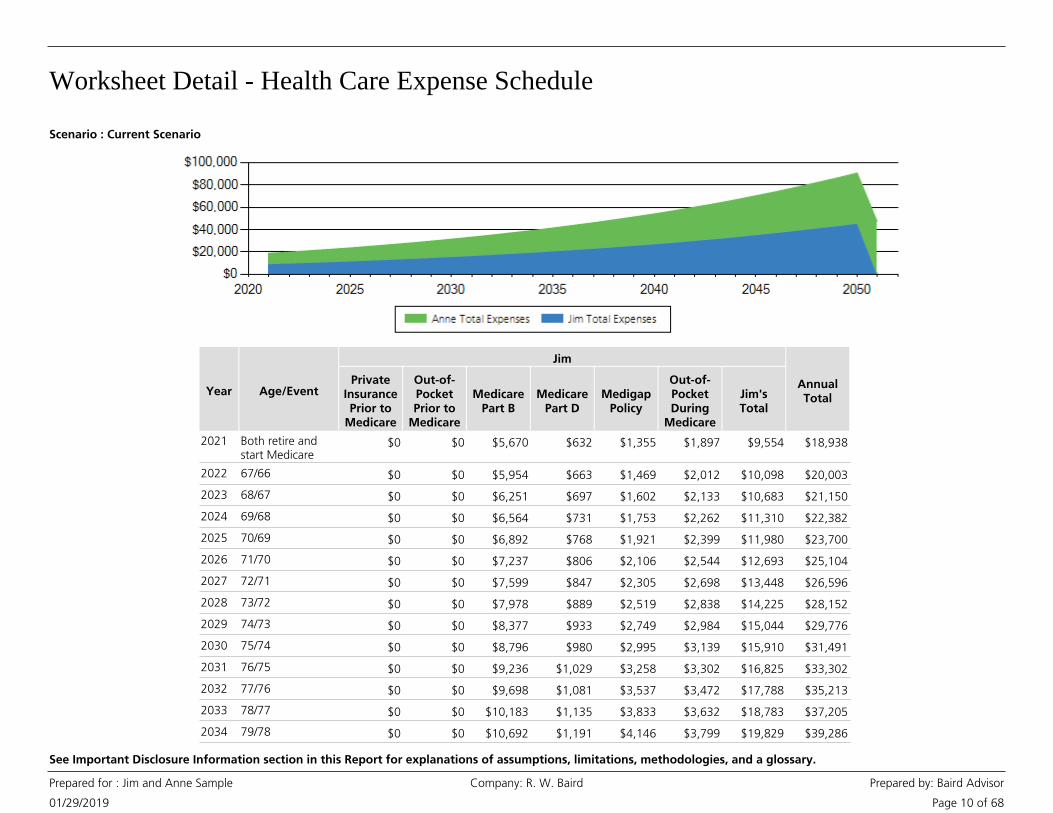

Worksheet Detail - Health Care Expense Schedule

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 10 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Year Age/EventPrivate

InsurancePrior to

Medicare

Out-of-PocketPrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-PocketDuring

Medicare

Jim'sTotal

Jim

AnnualTotal

2021 Both retire andstart Medicare

$0 $0 $5,670 $632 $1,355 $1,897 $9,554 $18,938

2022 67/66 $0 $0 $5,954 $663 $1,469 $2,012 $10,098 $20,003

2023 68/67 $0 $0 $6,251 $697 $1,602 $2,133 $10,683 $21,150

2024 69/68 $0 $0 $6,564 $731 $1,753 $2,262 $11,310 $22,382

2025 70/69 $0 $0 $6,892 $768 $1,921 $2,399 $11,980 $23,700

2026 71/70 $0 $0 $7,237 $806 $2,106 $2,544 $12,693 $25,104

2027 72/71 $0 $0 $7,599 $847 $2,305 $2,698 $13,448 $26,596

2028 73/72 $0 $0 $7,978 $889 $2,519 $2,838 $14,225 $28,152

2029 74/73 $0 $0 $8,377 $933 $2,749 $2,984 $15,044 $29,776

2030 75/74 $0 $0 $8,796 $980 $2,995 $3,139 $15,910 $31,491

2031 76/75 $0 $0 $9,236 $1,029 $3,258 $3,302 $16,825 $33,302

2032 77/76 $0 $0 $9,698 $1,081 $3,537 $3,472 $17,788 $35,213

2033 78/77 $0 $0 $10,183 $1,135 $3,833 $3,632 $18,783 $37,205

2034 79/78 $0 $0 $10,692 $1,191 $4,146 $3,799 $19,829 $39,286

Scenario : Current Scenario

Worksheet Detail - Health Care Expense Schedule

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 11 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Year Age/EventPrivate

InsurancePrior to

Medicare

Out-of-PocketPrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-PocketDuring

Medicare

Jim'sTotal

Jim

AnnualTotal

2035 80/79 $0 $0 $11,227 $1,251 $4,481 $3,974 $20,932 $41,478

2036 81/80 $0 $0 $11,788 $1,313 $4,836 $4,157 $22,095 $43,788

2037 82/81 $0 $0 $12,377 $1,379 $5,213 $4,349 $23,318 $46,221

2038 83/82 $0 $0 $12,996 $1,448 $5,613 $4,516 $24,572 $48,748

2039 84/83 $0 $0 $13,646 $1,521 $6,037 $4,689 $25,893 $51,362

2040 85/84 $0 $0 $14,328 $1,597 $6,493 $4,870 $27,287 $54,118

2041 86/85 $0 $0 $15,045 $1,676 $6,982 $5,057 $28,760 $57,028

2042 87/86 $0 $0 $15,797 $1,760 $7,503 $5,252 $30,311 $60,098

2043 88/87 $0 $0 $16,587 $1,848 $8,049 $5,454 $31,938 $63,325

2044 89/88 $0 $0 $17,416 $1,941 $8,610 $5,664 $33,630 $66,694

2045 90/89 $0 $0 $18,287 $2,038 $9,174 $5,947 $35,445 $70,254

2046 91/90 $0 $0 $19,201 $2,140 $9,744 $6,244 $37,329 $74,019

2047 92/91 $0 $0 $20,161 $2,247 $10,326 $6,556 $39,290 $77,931

2048 93/92 $0 $0 $21,169 $2,359 $10,923 $6,884 $41,336 $82,008

2049 94/93 $0 $0 $22,228 $2,477 $11,528 $7,229 $43,461 $86,253

2050 Jim's plan ends $0 $0 $23,339 $2,601 $12,133 $7,590 $45,663 $90,655

2051 Anne's plan ends $0 $0 $0 $0 $0 $0 $0 $47,272

$709,431Total Lifetime Cost ofHealth Care

Year Age/EventPrivate

InsurancePrior to

Medicare

Out-of-PocketPrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-PocketDuring

Medicare

Anne'sTotal

Anne

AnnualTotal

2021 Both retire andstart Medicare

$0 $0 $5,670 $632 $1,321 $1,761 $9,384 $18,938

Scenario : Current Scenario

Worksheet Detail - Health Care Expense Schedule

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 12 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Scenario : Current Scenario

Year Age/EventPrivate

InsurancePrior to

Medicare

Out-of-PocketPrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-PocketDuring

Medicare

Anne'sTotal

Anne

AnnualTotal

start Medicare $0 $0 $5,670 $632 $1,321 $1,761 $9,384 $18,938

2022 67/66 $0 $0 $5,954 $663 $1,422 $1,866 $9,905 $20,003

2023 68/67 $0 $0 $6,251 $697 $1,542 $1,977 $10,467 $21,150

2024 69/68 $0 $0 $6,564 $731 $1,682 $2,094 $11,071 $22,382

2025 70/69 $0 $0 $6,892 $768 $1,840 $2,219 $11,719 $23,700

2026 71/70 $0 $0 $7,237 $806 $2,017 $2,351 $12,411 $25,104

2027 72/71 $0 $0 $7,599 $847 $2,211 $2,491 $13,147 $26,596

2028 73/72 $0 $0 $7,978 $889 $2,421 $2,639 $13,927 $28,152

2029 74/73 $0 $0 $8,377 $933 $2,645 $2,775 $14,731 $29,776

2030 75/74 $0 $0 $8,796 $980 $2,887 $2,918 $15,580 $31,491

2031 76/75 $0 $0 $9,236 $1,029 $3,145 $3,068 $16,478 $33,302

2032 77/76 $0 $0 $9,698 $1,081 $3,421 $3,225 $17,424 $35,213

2033 78/77 $0 $0 $10,183 $1,135 $3,714 $3,391 $18,423 $37,205

2034 79/78 $0 $0 $10,692 $1,191 $4,024 $3,549 $19,457 $39,286

2035 80/79 $0 $0 $11,227 $1,251 $4,354 $3,714 $20,546 $41,478

2036 81/80 $0 $0 $11,788 $1,313 $4,705 $3,887 $21,693 $43,788

2037 82/81 $0 $0 $12,377 $1,379 $5,078 $4,068 $22,902 $46,221

2038 83/82 $0 $0 $12,996 $1,448 $5,474 $4,258 $24,176 $48,748

2039 84/83 $0 $0 $13,646 $1,521 $5,893 $4,410 $25,469 $51,362

2040 85/84 $0 $0 $14,328 $1,597 $6,339 $4,567 $26,831 $54,118

2041 86/85 $0 $0 $15,045 $1,676 $6,818 $4,730 $28,269 $57,028

2042 87/86 $0 $0 $15,797 $1,760 $7,331 $4,899 $29,787 $60,098

2043 88/87 $0 $0 $16,587 $1,848 $7,878 $5,074 $31,387 $63,325

2044 89/88 $0 $0 $17,416 $1,941 $8,452 $5,256 $33,064 $66,694

Worksheet Detail - Health Care Expense Schedule

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 13 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Year Age/EventPrivate

InsurancePrior to

Medicare

Out-of-PocketPrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-PocketDuring

Medicare

Anne'sTotal

Anne

AnnualTotal

2045 90/89 $0 $0 $18,287 $2,038 $9,040 $5,444 $34,809 $70,254

2046 91/90 $0 $0 $19,201 $2,140 $9,633 $5,717 $36,690 $74,019

2047 92/91 $0 $0 $20,161 $2,247 $10,231 $6,003 $38,641 $77,931

2048 93/92 $0 $0 $21,169 $2,359 $10,842 $6,303 $40,673 $82,008

2049 94/93 $0 $0 $22,228 $2,477 $11,470 $6,618 $42,792 $86,253

2050 Jim's plan ends $0 $0 $23,339 $2,601 $12,104 $6,949 $44,992 $90,655

2051 Anne's plan ends $0 $0 $24,506 $2,731 $12,740 $7,296 $47,272 $47,272

$744,119Total Lifetime Cost ofHealth Care

• Program assumptions:

• The scenario assumes that client and co-client will each use a combination of Medicare PartA (Hospital Insurance), Part B (Medical Insurance), Part D (Prescription Drug Insurance),Medigap insurance , and Out-of Pocket expenses. Alternatively, Medicare Advantage may beselected instead of Medigap and a Part D plan. The program uses initial default values thatmay have been adjusted based on your preferences and information provided by you.

Notes

• The scenario assumes that client and co-client each qualify to receive Medicare Part A at nocharge and therefore it is not reflected in the Health Care Expense schedule.

• Medicare and Medigap costs begin at the later of age 65, your retirement age, or thecurrent year.

• All costs are in future dollars.

• Costs associated with Long Term Care needs are not addressed by this goal. A separate LTCgoal can be created.

• General Information regarding Medicare:

• Part B premiums are uniform nationally and are increased for those with a higher ModifiedAdjusted Gross Income.

• Part D coverage is optional. Premiums are increased for those with a higher ModifiedAdjusted Gross Income, differ from state to state, and vary based on the specific plan andlevel of benefit selected.

• Medigap coverage is optional and policies (Plans A-N) are issued by private insurers.

• Clients may incur out-of-pocket healthcare expenses, for costs not covered by Medicarebenefits and Medigap insurance.

• If clients retire before age 65, they may choose to purchase private health insurance or toself-insure. Costs and coverage for private health insurance varies greatly.

Scenario : Current Scenario

Net Worth Summary - All Resources

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 14 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

This is your Net Worth Summary as of 01/29/2019. Your Net Worth is the difference between what you own (your Assets) and what youowe (your Liabilities). To get an accurate Net Worth statement, make certain all of your Assets and Liabilities are entered.

+ $12,549,700Other Assets

Investment Assets $9,254,297

Total Liabilities $150,000

Net Worth $21,653,997

$21,803,997Total Assets

-

Description Total

Investment Assets

Employer Retirement Plans $2,850,000

Individual Retirement Accounts $799,297

Annuities & Tax-Deferred Products $130,000

Taxable and/or Tax-Free Accounts $5,475,000

Total Investment Assets: $9,254,297

Other Assets

Home and Personal Assets $1,750,000

Business and Property $10,000,000

Pension and Deferred Compensation $500,000

Cash Value Life $250,000

Stock Options $49,700

Total Other Assets: $12,549,700

Liabilities

Personal Real Estate Loan: $150,000

Total Liabilities: $150,000

Net Worth: $21,653,997

Net Worth Detail - All Resources

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 15 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

This is your Net Worth Detail as of 01/29/2019. Your Net Worth is the difference between what you own (your Assets) and what you owe(your Liabilities). To get an accurate Net Worth statement, make certain all of your Assets and Liabilities are entered.

Description TotalJointAnneJim

Investment Assets

Employer Retirement Plans

401(k) $0

Jim's 401(k) $2,850,000$2,850,000

Individual Retirement Accounts

Anne's Baird IRA $480,000$480,000

Jim's Baird IRA $319,297$319,297

Annuities & Tax-Deferred Products

Variable Annuity with GMWB $130,000$130,000

Taxable and/or Tax-Free Accounts

Jim's Baird Account $1,500,000$1,500,000

Jim's Investment Account $3,000,000$3,000,000

Joint Cash & Bank Accounts $300,000$300,000

Joint Mutual Fund Account $675,000$675,000

Total Investment Assets: $9,254,297$7,799,297 $480,000 $975,000

Other Assets

Home and Personal Assets

AIG 10-Year Fixed Annuity $100,000$100,000

Home $650,000$650,000

Lake Home $1,000,000$1,000,000

Business and Property

Business $10,000,000$10,000,000

Pension and Deferred Compensation

Deferred Compensation $500,000$500,000

Net Worth Detail - All Resources

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 16 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Description TotalJointAnneJim

Other Assets

Cash Value Life

Second to Die Policy $250,000$250,000

Stock Options

APPLE INC $49,700$49,700

Total Other Assets: $12,549,700$10,799,700 $0 $1,750,000

Liabilities

Personal Real Estate Loan:

Mortgage $150,000$150,000

Total Liabilities: $150,000$0 $0 $150,000

Net Worth: $21,653,997

Resources Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 17 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Description Owner Current Value

Investment Assets

Additions Assign to Goal

Manually Entered

Jim401(k) Fund All Goals

AnneAnne's Baird IRA $480,000 Fund All Goals

JimJim's 401(k) $2,850,000 $25,000 Fund All Goals

JimJim's Baird Account $1,500,000 Fund All Goals

JimJim's Baird IRA $319,297 Fund All Goals

JimJim's Investment Account $3,000,000 $50,000 Fund All Goals

Joint SurvivorshipJoint Cash & Bank Accounts $300,000 Fund All Goals

Joint SurvivorshipJoint Mutual Fund Account $675,000 Fund All Goals

JimVariable Annuity with GMWB $130,000 Fund All Goals

$9,254,297Total Investment Assets :

Description Owner Scenario Year Assign to Goal

Stock Options

Amount

- See the Stock Options Summary for Scenario Detail.

Manually Entered

APPLE INC (AAPL) Jim 2019 $49,700

Description Owner Current Value Future Value Assign to Goal

Other Assets

Manually Entered

Business Jim $10,000,000 $10,000,000 Fund All Goals

Home Joint Survivorship $650,000 Not Funding Goals

Lake Home Joint Survivorship $1,000,000 Not Funding Goals

Deferred Compensation Jim $500,000 $140,376 for 5 years Fund All Goals

Second to Die Policy Jim $250,000 Not Funding Goals

AIG 10-Year Fixed Annuity Joint Survivorship $100,000 $130,000 Fund All Goals

$12,500,000Total of Other Assets :

Resources Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 18 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Annual Premium Cash ValueDescription Owner BeneficiaryInsured Death Benefit Premium Paid

Insurance Policies

Manually Entered

Cash Value Life Insurance Policies Summary (included in Assets)

$15,000 $250,000Second to Die Policy Whole Life

Jim Co-Client of Insured- 100%

Second to Die $5,000,000 Until Insured Dies

Insurance Policies Summary (not included in Assets)

Term Policy Term Life

Anne Co-Client of Insured- 100%

Anne $100,000 Until Policy Terminates

$5,100,000Total Death Benefit of All Policies :

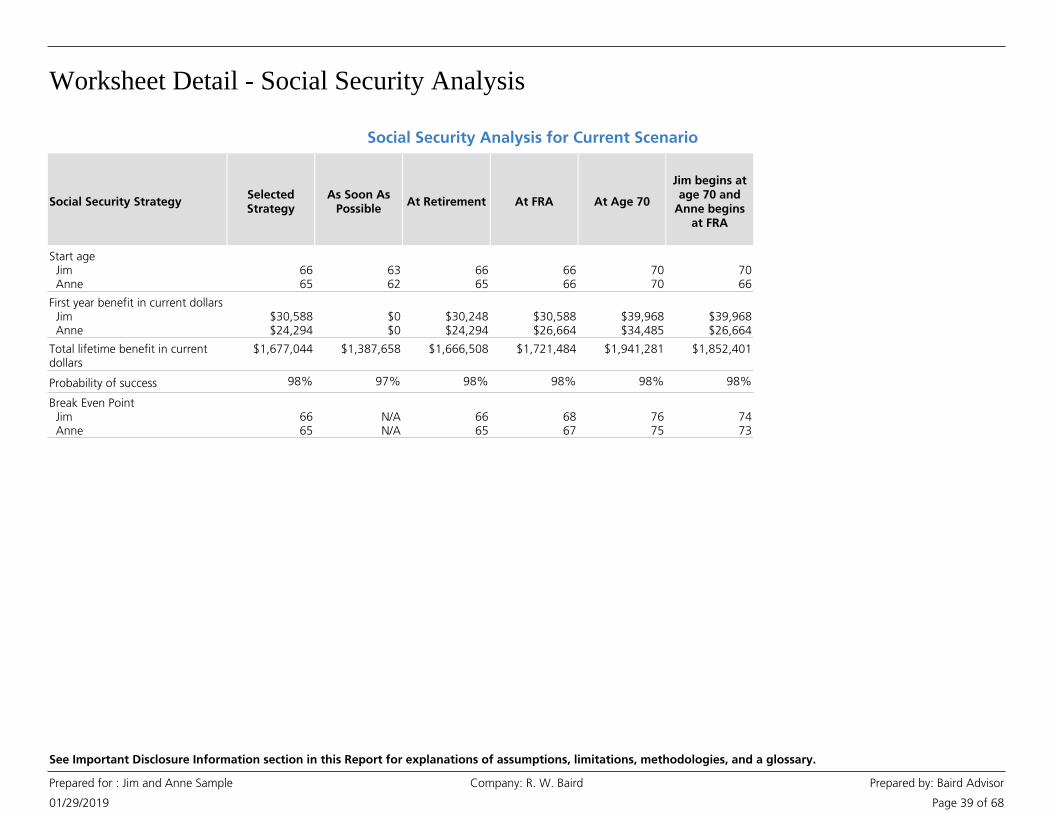

Social Security

Description Value Assign to Goal

Social Security Jim will file a normal application at age 66 Years, 2 Months.He will receive $30,588 in retirement benefits at age 66.

Fund All Goals

Social Security Anne will file a normal application at age 65.She will receive $24,294 in retirement benefits at age 65.

Fund All Goals

Retirement Income

Description Value Assign to GoalOwner Inflate?

Pension Jim $155,000 from Jim'sRetirement to End of Jim'sPlan

Fund All GoalsNo

Pension Anne $4,000 from Anne'sRetirement to End of Anne'sPlan

Fund All GoalsNo

Type Outstanding BalanceDescription Owner

Liabilities

Interest Rate Monthly Payment

Manually Entered

Total Amount Mortgage $150,000Joint $1,000

$150,000Total Outstanding Balance :

Tax and Inflation Assumptions

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 19 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Base Inflation Rate

Inflation rate : 3.00%

Social Security Inflation rate : 2.00%

Tax Assumption Inflation rate : 3.00%

Tax Rates : 35.00%

Federal

7.65%

State

0.00%

Local

Marginal Tax Rates Before Retirement

Untaxed Gain on Taxable Earnings - Before Retirement

What portion of your Annual Taxable InvestmentEarnings will not be taxed until withdrawn?

0.00%

What portion of your Taxable Investment Earningswill be taxed at the LTCG rate?

20.00%

Long Term Capital Gains rate : 20.00%

Long Term Capital Gains (LTCG) - Before Retirement

Tax Rates During Retirement

Local rate : 0.00%

Deduction estimate : Use standard deductions

Let the Program calculate taxes each year

0.00%

Untaxed Gain on Taxable Earnings - During Retirement

What portion of your Annual Taxable InvestmentEarnings will not be taxed until withdrawn?

Long Term Capital Gains (LTCG) - During Retirement

What portion of your Taxable Investment Earningswill be taxed at the LTCG rate?

20.00%

Long Term Capital Gains rate : Use Program estimate

Taxation of Social Security

What portion of Social Security will be taxed? 85.00%

Tax Penalty

Include penalties in Plan? : Yes

Treat Tax-Free Assets as Tax-Free

Tax Free Earnings - Options

Model Portfolio Table

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 20 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

The Risk-Based Portfolio was selected from this list of Portfolios, based upon the risk assessment. The Risk Band is comprised of theportfolio(s) that could be appropriate for you, based upon the Risk-Based Portfolio indicated. The Target Portfolio was selected by you.Refer to the Standard Deviation column in the chart below to compare the relative risk of your Current Portfolio to the Target Portfolio.

Portfolios Name Cash Bond Stock Alternative UnclassifiedProjected

ReturnStandardDeviation

Capital Preservation 20% 80% 0% 0% 0% 1.80% 2.76%

Conservative Income 15% 65% 20% 0% 0% 2.91% 3.70%

Income with Growth 10% 50% 40% 0% 0% 4.40% 6.81%

Current 8% 35% 57% 0% 0% 5.07% 9.41%

Growth with Income 5% 35% 60% 0% 0% 5.62% 9.89%

Capital Growth 3% 17% 80% 0% 0% 6.73% 12.94%

All Growth 3% 0% 97% 0% 0% 7.63% 15.57%

Risk Band Current Risk-Based Target

Return vs. Risk Graph

This graph shows the relationship of return and risk for each Portfolio in the chart above.

When deciding how to invest your money, you must determine the amount of risk you arewilling to assume to pursue a desired return. The Return versus Risk Graph reflects a set ofportfolios that assume a low relative level of risk for each level of return, or conversely anoptimal return for the degree of investment risk taken. The graph also shows the position ofthe Risk Band, Target, Risk-Based, and Custom Portfolios. The positioning of these portfoliosillustrates how their respective risks and returns compare to each other as well as theoptimized level of risk and return represented by the Portfolios.

Worksheet Detail - Allocation Comparison

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 21 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Current Portfolio

These charts compare your Current Portfolio with the Composite Portfolio you selected and show changes associated with investmentstrategies (if applicable) and allocation changes you should consider.

Composite PortfolioGrowth with IncomeProjected Returns

5.07% Total Return 5.61%

3.00% Base Inflation Rate 3.00%

2.07% Real Return 2.61%

9.41% Standard Deviation 9.86%

Bear Market Returns

-24% Great Recession -25%

6% Bond Bear Market 6%

Asset Class % of Total Composite AmountCurrent Amount % of Total

Portfolio Comparison with Allocation Changes

Increase / Decrease

Large Cap Core 0% $020%$1,859,136 -$1,859,136

Large Cap Growth 15% $1,349,41821%$1,937,808 -$588,390

Large Cap Value 15% $1,349,4181%$48,960 $1,300,458

Mid Cap Core 10% $899,6120%$34,587 $865,025

Small Cap Core 4% $359,8452%$150,000 $209,845

Small Cap Growth 0% $06%$600,000 -$600,000

International Equity 14% $1,259,4577%$603,585 $655,872

Emerging Markets Equity 2% $179,9220%$9,650 $170,273

Broad Equity 1% $64,0871%$65,000 -$913

Commodities 0% $00%$9,434 -$9,434

Short Term Taxable 10% $899,61215%$1,415,452 -$515,840

Intermediate Term Taxable 20% $1,799,2252%$180,895 $1,618,330

Short Term Tax-Exempt 0% $012%$1,125,000 -$1,125,000

Intermediate Term Tax-Exempt 0% $02%$225,000 -$225,000

Scenario : Baird Model

Worksheet Detail - Allocation Comparison

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 22 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Asset Class % of Total Composite AmountCurrent Amount % of Total

Portfolio Comparison with Allocation Changes

Increase / Decrease

High Yield Fixed Income 5% $449,8062%$155,214 $294,592

Global Fixed Income 0% $00%$5,214 -$5,214

Broad Fixed Income 1% $64,0871%$92,629 -$28,542

Cash 5% $449,8068%$736,732 -$286,926

$9,254,297 $9,124,297 -$130,000

Changes to the Investable Assets Target ValueCurrent Value

Total Investment Portfolio $9,124,297$9,124,297

Effect of Investment Strategies

Current GMWB Investment Strategies $130,000$130,000

$9,254,297Total Investment Assets$9,254,297

Scenario : Baird Model

Employer Stock Plans

Stock Options

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 23 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

- Beginning in the exercise start year, vested options thatequal or exceed the minimum percentage gain are exercised. After the exercise start year,remaining options are exercised in the year they expire if they are in-the-money by anyamount.

- Currently vested options that are in-the-money by any amountare exercised now; all remaining options are lost.

- Currently vested options that equal or exceed the minimumpercentage gain are exercised now. Remaining options are either exercised in the first yearthey are both vested and exceed the minimum percentage gain or are exercised in the yearthey expire if they are in-the-money by any amount.

- Currently vested options that equal or exceed the minimumpercentage gain are exercised now. All remaining options are exercised in the year theyexpire if they are in-the-money by any amount.

- Beginning in the exercise start year, vested options that equalor exceed the minimum percentage gain are exercised. After the exercise start year,remaining options are either exercised in the first year they are both vested and exceed theminimum percentage gain or are exercised in the year they expire if they are in-the-moneyby any amount.

- One advantage of an ISO is that no regular income tax isrecognized upon exercising the option. In addition, if the acquired stock is held for twoyears from the date of grant and one year from the date of exercise, favorable long-termcapital gains rates will apply to all of the appreciation (between the strike price and saleprice) upon the subsequent sale of the stock. The sale of any shares prior to satisfyingeither of these holding period requirements will be treated as a "disqualifying disposition".If the acquired stock is not held for one year from exercise, the bargain element (thedifference between the value of the stock on exercise and the strike price, also referred toas "spread") is treated as ordinary income and any post-exercise gain is short-term capitalgain. If the stock is held for one year from exercise but not two years from grant, thebargain element (or spread) is ordinary income and any post-exercise gain is long-termcapital gain.

Introduction to Your Stock Options Although the exercise of an ISO is generally not a taxable event for regular tax purposes,the difference between the strike price and the stock price on the date of exercise isconsidered a preference item for federal, and possibly state, alternative minimum tax(AMT) purposes. Depending on the circumstances, the exercise of ISOs can cause ataxpayer to be subject to the AMT and incur a higher tax liability even though shares havenot yet been sold and gains have yet to be realized.

Stock Options Scenarios

Available Timing Methods

• Now - All Vested Only

This section of your report summarizes your Stock Option plan and calculates your currentoption equity value for all fully vested shares. It also calculates an estimate of the potentialfuture option equity values, that may be available to help fund your goals each year basedupon the assumptions you have made.

We believe this information is an important step in a financial goal plan. We look forwardto helping you make informed decisions regarding your stock option strategy.

This Report is for your information only and does not constitute the solicitation to purchaseor sell any specific security.

General Discussion

Your stock options can be a significant component of your financial portfolio. Stock optionscan give you the opportunity to benefit from the potential appreciation in your company'sstock. As with any other investments, there are certain risks associated with stock optionswhich you should take into consideration. Therefore, it is critical that you are familiar withyour stock options, how they function, and the financial implications they may have on youroverall portfolio. Stock options provide employees with the right to buy company stock at aspecified price, known as the strike price, within a certain period of time. A company cangrant two types of stock options - incentive stock options (ISOs) and non-qualified stockoptions (NQOs).

Incentive Stock Options (ISOs)

Nonqualified Stock Options (NQOs) - Unlike ISOs, the spread on NQOs is immediatelyrecognized as compensation income upon exercise, for regular tax purposes, and istherefore subject to federal, and possibly state income tax, as well as Medicare and FICAtax. If the stock is held after exercise, any subsequent appreciation is treated as capitalgain (long-term, if held for more than one year) when the stock is sold.

The future potential after-tax option equity cash flows illustrated in this analysis, for eachexercise scenario, were calculated based on selecting one or more Timing Methods andcertain assumptions described below:

All scenarios assume a cashless exercise strategy.

• Now and As Vested

• Now and At Expiration

• Start Year and As Vested

• Start Year and At Expiration

- Options are exercised in the year they expire if they are in-the-money byany amount.

• At Expiration

Stock Options

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 24 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

- The projected return for the asset class categoryselected, unless otherwise indicated by you. If a Stock Option Plan with Scenarios is treatedas a Special Asset, the return assumption for this stock includes three growth rates --labeled Low, Expected and High returns. The Program default for all three returns is theprojected return for the asset class category selected, and can be changed by you. Thisapproach can help illustrate financial risk not otherwise reflected in the Plan results.

Other Assumptions

• Return assumption for this Stock

- A year in which it is assumed that vesting ends prematurely.All remaining unvested options are lost.

- The minimum percentage gain in the stock priceabove the exercise price that is required before exercising options. Applying this minimumdefers the exercise of options with only relatively small spread between the stock price andthe option price.

• Minimum percentage gain to exercise

• Vesting Termination Year

- A year in which it is expected that you will begin to exercise vestedoptions, if different than the current year.

• Exercise Start Year

- If it is indicated that ISO shares are not to be "Held for OneYear", then it is assumed that the ISO shares are disqualified and a Regular Tax Rate isapplied. If it is indicated that ISO shares are to be "Held for One Year", it is assumed thatthose shares will have been held for at least two years from the date of grant and over oneyear from the date of exercise, thus qualifying for long-term capital gains treatment and theLong-Term Tax Rate is applied.

• Hold ISO for One Year

General Assumptions

• The Long-Term Tax Rate is the estimated tax rate applied to the potential option equity onany ISO shares sold that were held for more than one year after exercise (as well as twoyears from date of grant). This rate should be the total estimate for all applicable taxes,including Federal, State, and Local Income taxes.

• The possible impact of the Alternative Minimum Tax (AMT) is not reflected in anycalculations. Since the exercise of ISOs can have substantial AMT consequences, you shouldconsult with your personal tax advisor.

• The Regular Tax Rate is the estimated tax rate applied to the potential option equity on allNQOs exercised and sold and on any ISO shares sold that were not held for one year. Thisrate should be the total estimate for all applicable taxes, including Federal, State, and LocalIncome taxes. Unless included in this rate, Medicare and FICA taxes are not appliedseparately to NQO equity.

• The after-tax calculations within the Option Equity Schedule and Price Sensitivity Analysisassume that all ISOs are disqualified and the Regular Tax Rate is applied. In addition, theVesting Schedule does not calculate whether ISO grants meet the $100,000 limitation.

• Exercise costs for NQOs and ISOs have not been considered nor have any dividends thatmight have been received from ISOs that are exercised and held for one year.

• Grants expected to be received in the future are not represented in this Stock OptionSummary.

Cash Receipt Schedule

The future potential after-tax option equity cash flows illustrated in this analysis, for eachCash Receipt Schedule, are the amounts you entered, based on your own calculations.

Assumptions

• The Current Value should represent the current value of all vested stock options in thisStock Option Plan.

• The Value if the Owner dies today should represent the value to be paid by the StockOption Plan if the owner dies today.

• The Cash Receipts Table shows expected after-tax amounts for one or more years in thefuture, based on your own calculations and as entered by you.

• If a Stock Option Plan with a Cash Receipt Schedule is treated as a Special Asset, the CashReceipts Table shows the Low, Expected, and High after-tax amounts for each year in thefuture, based on your own calculation and as entered by you. This approach can helpillustrate financial risk not otherwise reflected in the Plan results.

• The possible impact of the Alternative Minimum Tax (AMT) and any other cost and taxesassociated with exercising Stock Options are not reflected in any calculations, unless itsimpact was taken into account, by you, when entering the cash receipt amounts.

Stock Options Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 25 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

APPLE INC (AAPL)

Owner : Jim

Options

Granted :

Exercised :

Outstanding Options

Vested :

Not Vested :

2,000

0

2,000

0

Regular Tax Rate : 50.0%

Long-Term Tax Rate : 23.8%

Assumptions

Option Equity After Tax : $24,850

Market Price* :

Options Vest at Death :

$109.85 on 04/15/2016

No

Asset Class : Large Cap Core

* Security prices included in the stock option analysis are based on the market price that you entered for the date referenced and are included onlybecause the system requires it for analysis purposes. This Report is for your information only and does not constitute the solicitation to purchase orsell any specific security and you should not rely on the information presented when making an investment or liquidation decision. We make nowarranty with respect to any security price and do not guarantee that the price listed will be available to you should you choose to exercise youroptions. The actual price available to you should you choose to exercise your options may be more or less than indicated on the report.

Special Asset : No

Vesting Schedule

The Vesting Schedule below is a summary showing the percentage of each option grant that becomes exercisable over time according to theinformation you have provided.

Name % Vested by Year

1 2 3 4 5 6 7 8 9 10

3-Year Vest 33% 33% 34% 0% 0% 0% 0% 0% 0% 0%

Stock Options Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 26 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Option Equity Schedule

The Option Equity Schedule below shows a summary of your stock option grants and calculates the pre-tax and after-tax option equity value for allvested stock options based on the current market price. These values are calculated using the information you provided for each grant, your taxrate assumption and the current market price of the stock as indicated by you. If your plan includes ISOs, the After Tax Option Equity value assumesthat all ISOs are immediately disqualified and the regular tax rate is applied. This Report does not constitute the solicitation to purchase or sell anyspecific security.

Name Date Price Type ExpirationDate

Granted Exercised Vested Not Vested Pre-Tax Tax at 50.0%

Grant

VestingSchedule

Options Outstanding Options

After Tax

Option Equity - Vested OnlyMarket Price $109.85

2013 Grant 03/01/2013 $70.00 NQO 03/01/2023 3-Year Vest 1,000 0 1,000 0 $39,850 $19,925 $19,925

2015 Grant 03/01/2015 $100.00 NQO 03/01/2025 3-Year Vest 1,000 0 1,000 0 $9,850 $4,925 $4,925

2,000 0Total : 2,000 0 $49,700 $24,850 $24,850

Price Sensitivity Analysis

The Price Sensitivity Analysis shows a summary of your stock option grants and calculates the potential after-tax option equity values for all vestedstock options based on the current market price as indicated by you as well as a variety of higher and lower assumed prices. Understanding theimpact of potential stock price changes on the after-tax option equity value of particular grants can play an important role in determining optionexercise strategies. If your plan includes ISOs, the After Tax Option Equity value assumes that all ISOs are immediately disqualified and the regulartax rate is applied.

Name Date Price Type ExpirationDate

-25%$82.39

-15%$93.37

Market*$109.85

+15%$126.33

Grant

VestedOptions

+25%$137.31

Option Equity Sensitivity - After Tax for Vested Options Only

2013 Grant 03/01/2013 $70.00 NQO 03/01/2023 1,000 $6,194 $11,686 $19,925 $28,164 $33,656

2015 Grant 03/01/2015 $100.00 NQO 03/01/2025 1,000 $0 $0 $4,925 $13,164 $18,656

$6,194 $11,686 $24,850 $41,328 $52,313Total :

Change In Value: -$18,656 -$13,164 $0 $16,478 $27,463

* Security prices included in the stock option analysis are based on the market price that you entered for the date referenced and are included onlybecause the system requires it for analysis purposes. This Report is for your information only and does not constitute the solicitation to purchase orsell any specific security and you should not rely on the information presented when making an investment or liquidation decision. We make nowarranty with respect to any security price and do not guarantee that the price listed will be available to you should you choose to exercise youroptions. The actual price available to you should you choose to exercise your options may be more or less than indicated on the report.

Stock Options Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 27 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Full Vesting Schedule

The Full Vesting Schedule illustrates the amount of stock options that are currently vested and calculates any additional amounts that vest in futureyears based on the applicable Vesting Schedule.

Name Date Price Type ExpirationDate

2019 2020 2021 2022

Grant

VestingSchedule

2023

Options Vesting Each Year

CurrentlyVested

Beyond

2013 Grant 03/01/2013 $70.00 NQO 03/01/2023 3-Year Vest 0 0 0 0 01,000 0

2015 Grant 03/01/2015 $100.00 NQO 03/01/2025 3-Year Vest 0 0 0 0 01,000 0

0 0 0 0 02,000 0Total :

Stock Options Scenarios

The Stock Options Scenarios show a summary of your stock option grants and, for each scenario, the timing method(s) and other assumptionsoutlined in the Stock Options Introduction that will be used to calculate future potential after-tax option equity as summarized in the Cash FlowSchedule.

Name Date Price Type ExpirationDate

Timing HoldISO?

Timing HoldISO?

Grant

VestingSchedule

Timing

Scenario 1

Vested Not Vested

Outstanding Options

HoldISO?

Scenario 2 Scenario 3

2013 Grant 03/01/2013 $70.00 NQO 03/01/2023 3-Year Vest Now And AsVested

N/A Now And AtExpiration

N/A At Expiration1,000 0 N/A

2015 Grant 03/01/2015 $100.00 NQO 03/01/2025 3-Year Vest Now And AsVested

N/A Now And AtExpiration

N/A At Expiration1,000 0 N/A

2,000 0Total :

7.40%7.40%7.40%Return assumption for this stock :

Accelerated Expiration Year : 2025 2025 2025

Minimum percentage gain to exercise : 8.00% 8.00%

Exercise Start Year : 2015 2015 2015

Stock Options Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 28 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Cash Flow Schedule

The Cash Flow Schedule below shows the future potential after-tax option equity value for each scenario indicated, on a year-by-year basis. Theseare only estimates based on current information and not guarantees that you will obtain a specific value or tax benefit upon exercise of the StockOptions. This Report does not constitute the solicitation to purchase or sell any specific security.

Year Assign to Goals Scenario 1 - Option Equity (after-tax) Scenario 2 - Option Equity (after-tax) Scenario 3 - Option Equity (after-tax)

2019 Fund All Goals $24,850$24,850

2020 Fund All Goals

2021 Fund All Goals

2022 Fund All Goals

2023 Fund All Goals $38,078

2024 Fund All Goals

2025 Fund All Goals $34,294

2026 Fund All Goals

$24,850 $24,850 $72,372Total :

Important Note on Alternative Minimum Tax (AMT): If your plan includes ISOs, the possible impact of AMT is not reflected in these calculations.Since the exercise of ISOs can have substantial AMT consequences, you should consult with your personal tax advisor. Also, the possible impact ofthe value of ISOs becoming first exercisable during a single year and exceeding the $100,000 limitation, causing the excess ISOs to be disqualified, isnot reflected in these calculations.

Restricted Stock Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 29 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

APPLE INC (AAPL)

JimOwner :

Granted :

Not Vested :

1,000

0

Regular Tax Rate : 50.0%

AssumptionsShares

Market Price* :

Shares Vest at Death :

$109.85 on 04/15/2016

No

Asset Class : Large Cap Core

* Security prices included in the restricted stock analysis are based on the market price that you entered for the date referenced and are includedonly because the system requires it for analysis purposes. This Report is for your information only and does not constitute the solicitation topurchase or sell any specific security and you should not rely on the information presented when making an investment or liquidation decision. Wemake no warranty with respect to any security price and do not guarantee that the price listed will be available to you should you choose to sellyour shares. The actual price available to you should you choose to sell your shares may be more or less than indicated on the report.

Special Asset : No

Vesting Schedule

The Vesting Schedule below is a summary showing the percentage of each grant that becomes vested over time according to the information youhave provided.

Name % Vested by Year

1 2 3 4 5 6 7 8 9 10

Year ofGrant

5-Year Vest 20% 20% 20% 20% 20% 0% 0% 0% 0% 0%0%

The Full Vesting Schedule below illustrates the shares of restricted stock granted and the shares vesting in each year.

Full Vesting Schedule

Name Date 2019 2020 2021 2022

Grant

VestingSchedule

2023

Shares Vesting Each Year

BeyondVestedSharesGranted

2014 Grant 01/01/2014 5-Year Vest 0 0 0 0 01,000 01000

0 0 0 0 01,000 0Total :

Restricted Stock Summary

01/29/2019

Prepared for : Jim and Anne Sample Company: R. W. Baird Prepared by: Baird Advisor

Page 30 of 68

See Important Disclosure Information section in this Report for explanations of assumptions, limitations, methodologies, and a glossary.

Restricted Stock Scenarios