Preparation Tax Burden from the Source of Revenue.

36

Preparation Tax Burden from the Source of Revenue

-

Upload

bryce-newman -

Category

Documents

-

view

223 -

download

0

Transcript of Preparation Tax Burden from the Source of Revenue.

Preparation

Tax Burden from the Source of Revenue

Formula under Labor Law (Art.158,358)

TI (taxable income)=TR-Deductions

PIT = (TR- Deductions-Pension-Min.Salary)*0.1PIT = (TI-0.1*TI-18,660)*0.1

Social Tax = (TR-Deductions-Pension)*0.11Social Tax = (TI-0.1*TI)*0.11

Tax Burden = PIT + Social Tax

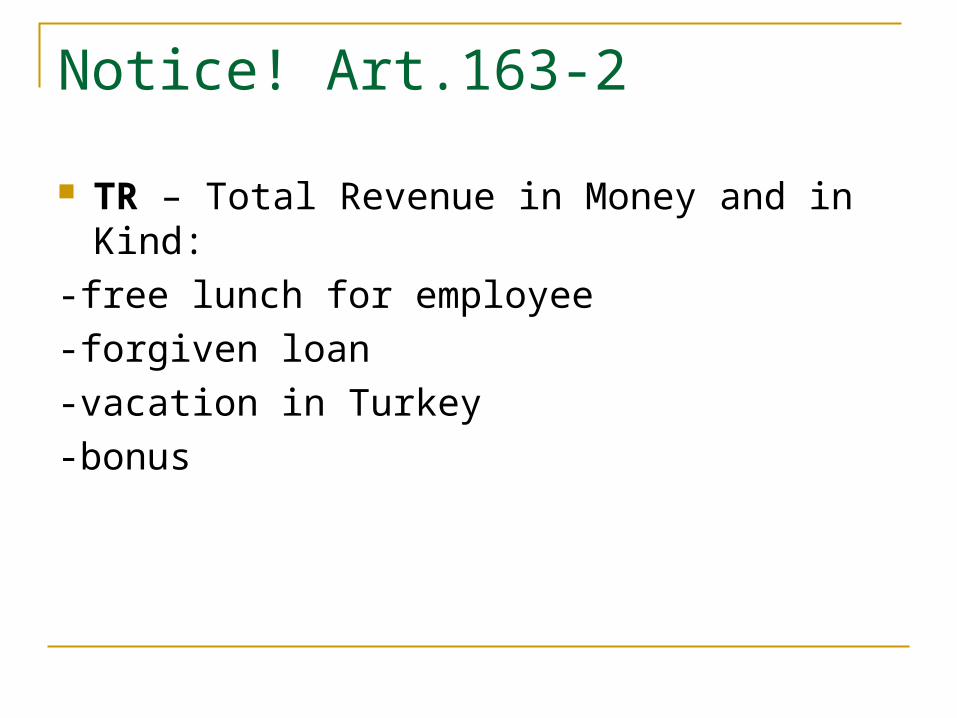

Notice! Art.163-2

TR – Total Revenue in Money and in Kind:

-free lunch for employee

-forgiven loan

-vacation in Turkey

-bonus

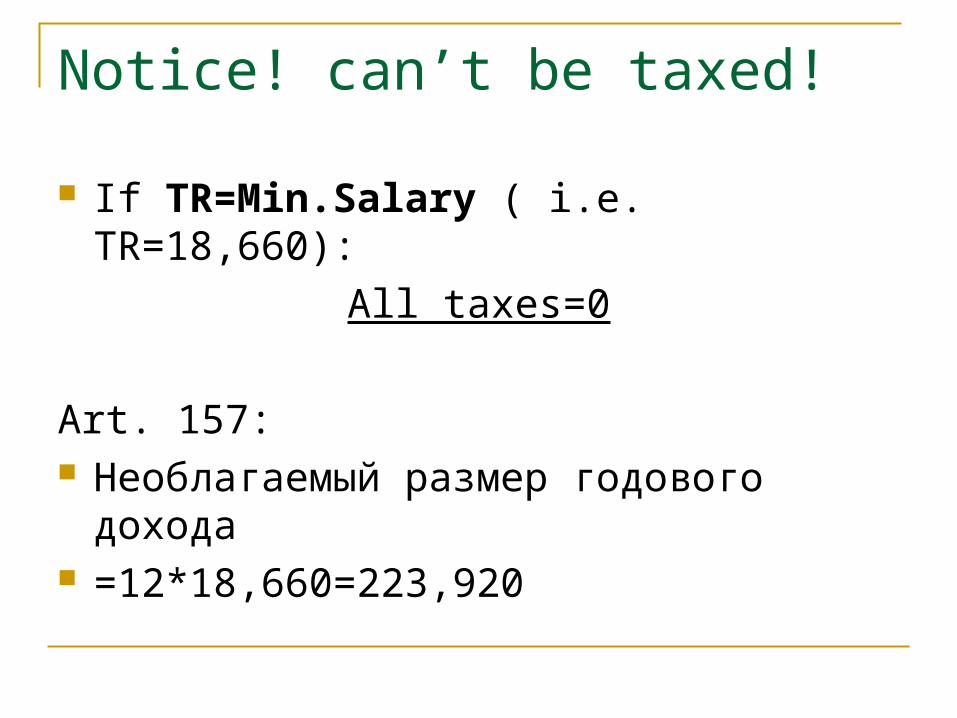

Notice! can’t be taxed!

If TR=Min.Salary ( i.e. TR=18,660):

All taxes=0

Art. 157: Необлагаемый размер годового дохода =12*18,660=223,920

Notice! Art.22-1,St.on Pension

Pension = TI*0.1

BUT if income ≥ 1,399, 500 KZT:

Pension = 139,950 KZT

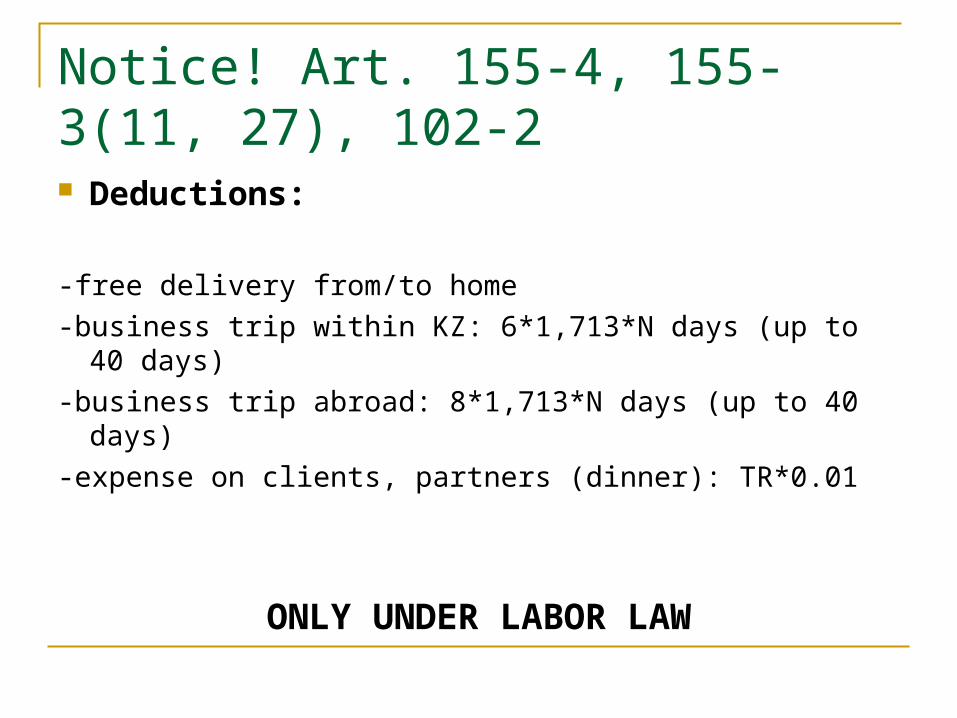

Notice! Art. 155-4, 155-3(11, 27), 102-2 Deductions:

-free delivery from/to home

-business trip within KZ: 6*1,713*N days (up to 40 days)

-business trip abroad: 8*1,713*N days (up to 40 days)

-expense on clients, partners (dinner): TR*0.01

ONLY UNDER LABOR LAW

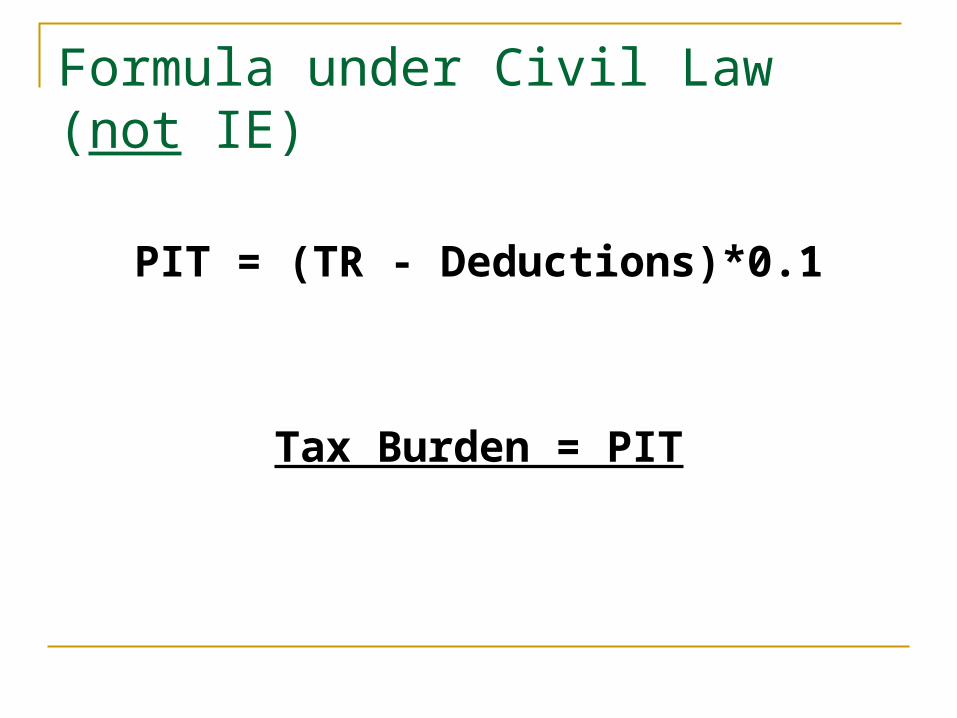

Formula under Civil Law (not IE)

PIT = (TR - Deductions)*0.1

Tax Burden = PIT

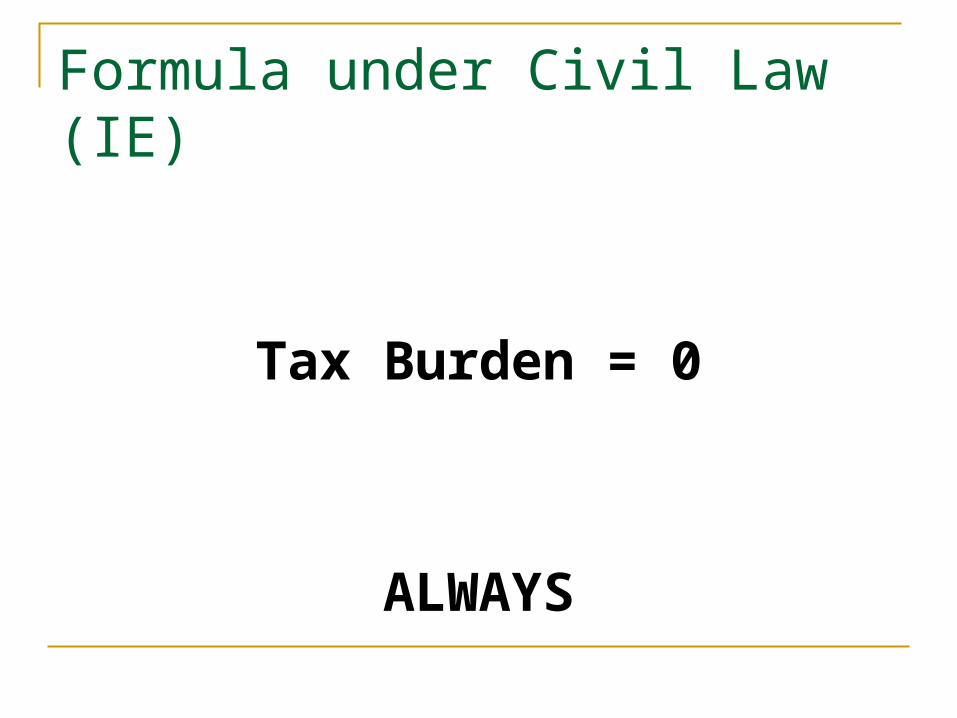

Formula under Civil Law (IE)

Tax Burden = 0

ALWAYS

EASY CASES

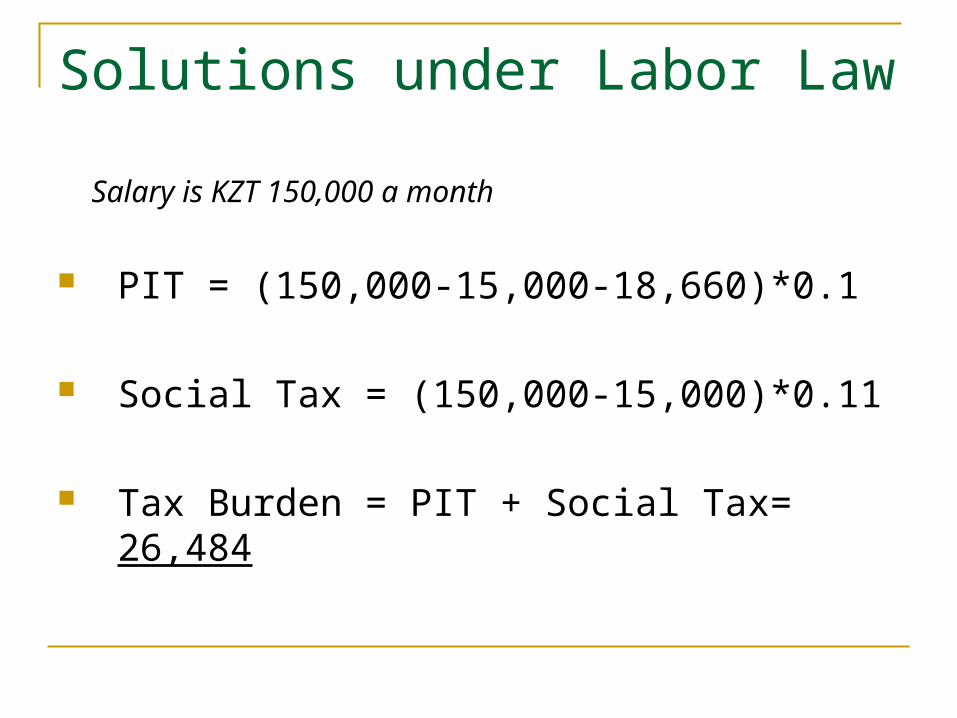

Solutions under Labor Law

Salary is KZT 150,000 a month

PIT = (150,000-15,000-18,660)*0.1

Social Tax = (150,000-15,000)*0.11

Tax Burden = PIT + Social Tax= 26,484

Solutions under Civil Law (not IE)

Salary is KZT 150,000 a month

PIT = 150,000*0.1

Tax Burden = PIT = 15,000

Solutions under Labor Law

Salary is KZT 2,300,000 a month

PIT=(2,300,000-139,950-18,660)*0.1

Social Tax=(2,300,000-139,950)*0.11

Tax Burden=PIT + Social Tax= 451,744.5

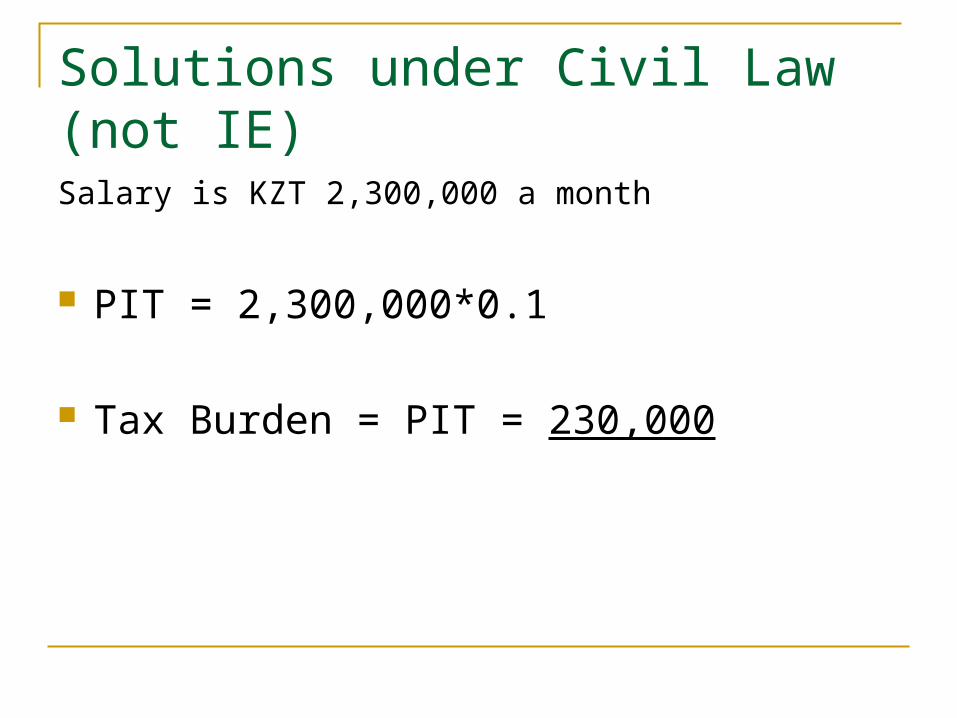

Solutions under Civil Law (not IE)Salary is KZT 2,300,000 a month

PIT = 2,300,000*0.1

Tax Burden = PIT = 230,000

INTERESTING CASES

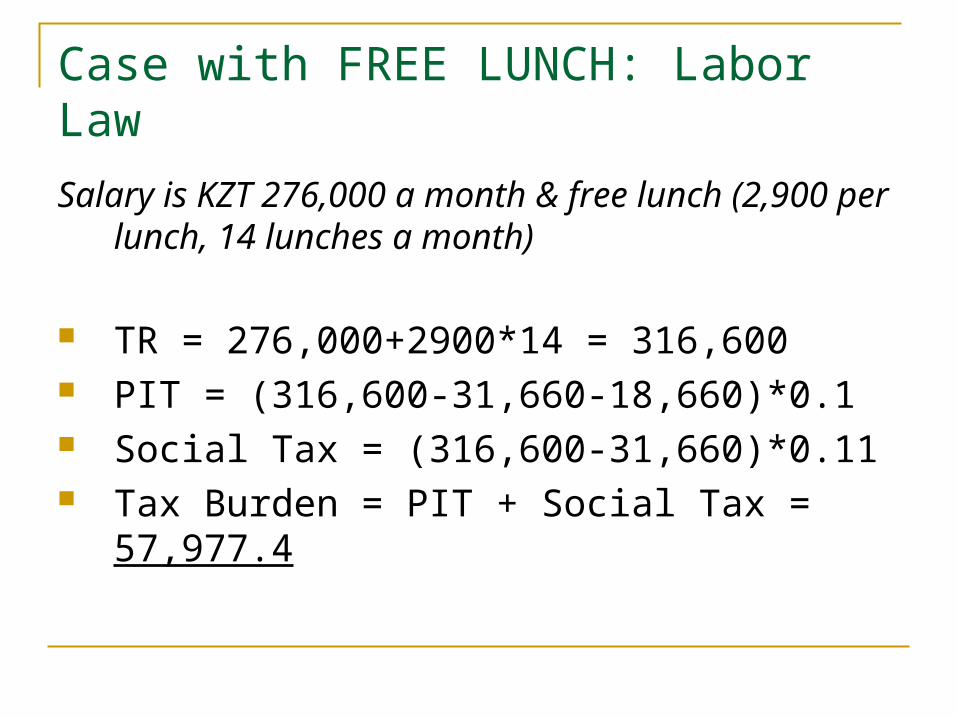

Case with FREE LUNCH: Labor Law

Salary is KZT 276,000 a month & free lunch (2,900 per lunch, 14 lunches a month)

TR = 276,000+2900*14 = 316,600 PIT = (316,600-31,660-18,660)*0.1 Social Tax = (316,600-31,660)*0.11 Tax Burden = PIT + Social Tax = 57,977.4

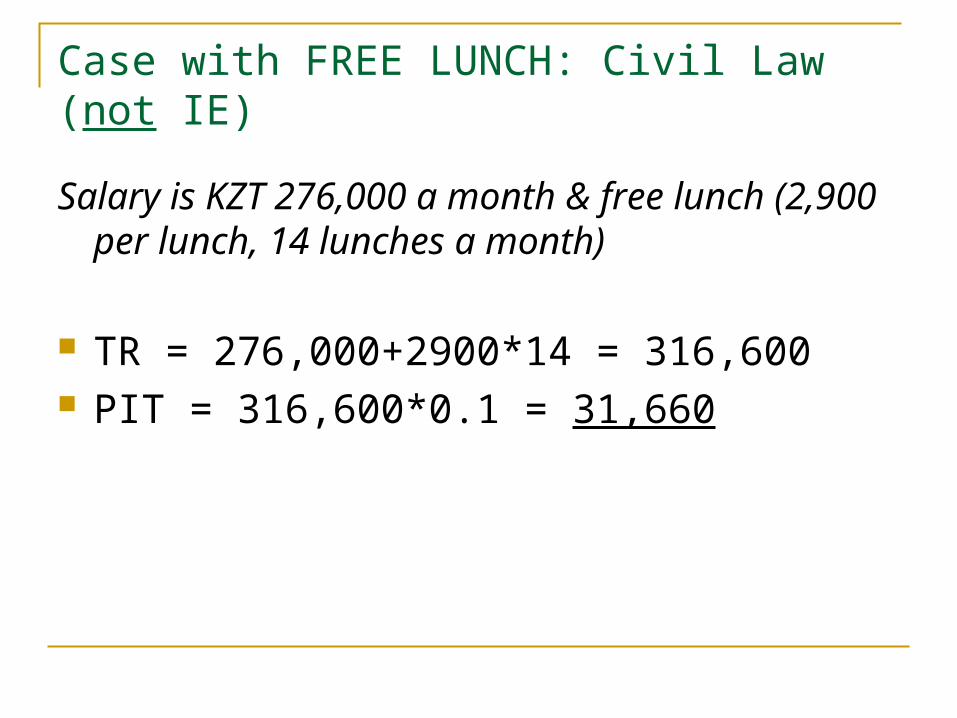

Case with FREE LUNCH: Civil Law (not IE)

Salary is KZT 276,000 a month & free lunch (2,900 per lunch, 14 lunches a month)

TR = 276,000+2900*14 = 316,600 PIT = 316,600*0.1 = 31,660

Case with FREE DELIVERY: Labor Law

Salary is KZT 347,000 a month & free delivery from work to home (cost of the delivery is 900 per day, 23 days).

TR = 347,000+900*23=367,700 TI=367,700-900*23=347,000 PIT = (347,000-34,700-18,660)*0.1 Social Tax = (347,000-34,700)*0.11 Tax Burden=63,717

Case with FREE DELIVERY: Civil Law (not IE)

Salary is KZT 347,000 a month & free delivery from work to home (cost of the delivery is 900 per day, 23 days).

TR = 347,000+900*23=367,700 PIT=367,700*0.1=36,770

Case with BONUS: Labor Law

Salary is KZT 1,700,000 a month & bonus 344,000

TR = 1,700,000+344,000=2,044,000 PIT = (2,044,000-139,950-18,660)*0.1 Social Tax = (2,044,000-139,950)*0.11 Tax Burden = 397,984.5

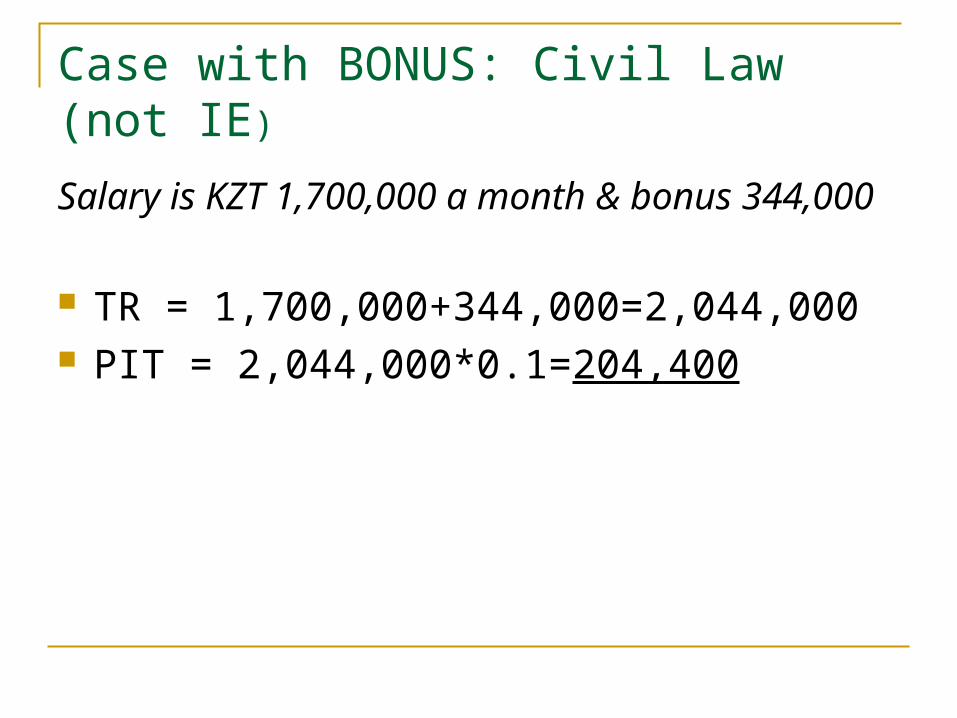

Case with BONUS: Civil Law (not IE)

Salary is KZT 1,700,000 a month & bonus 344,000

TR = 1,700,000+344,000=2,044,000 PIT = 2,044,000*0.1=204,400

Case with BUSINESS TRIP: Labor Law

Salary is KZT 575,000 a month & business trip within KZ (19 nights, hotel 21,000 a night, food 3,500 a day)

TR=575,000+19*21,000+19*3,500=1,040,500 Deductions=6*1713*19=195,282 TI=1,040,500-195,282=845,218 PIT=(845,218-84,521.8-18,660)*0.1 Social Tax =(845,218-84,521.8)*0.11 Tax Burden =157,880.282

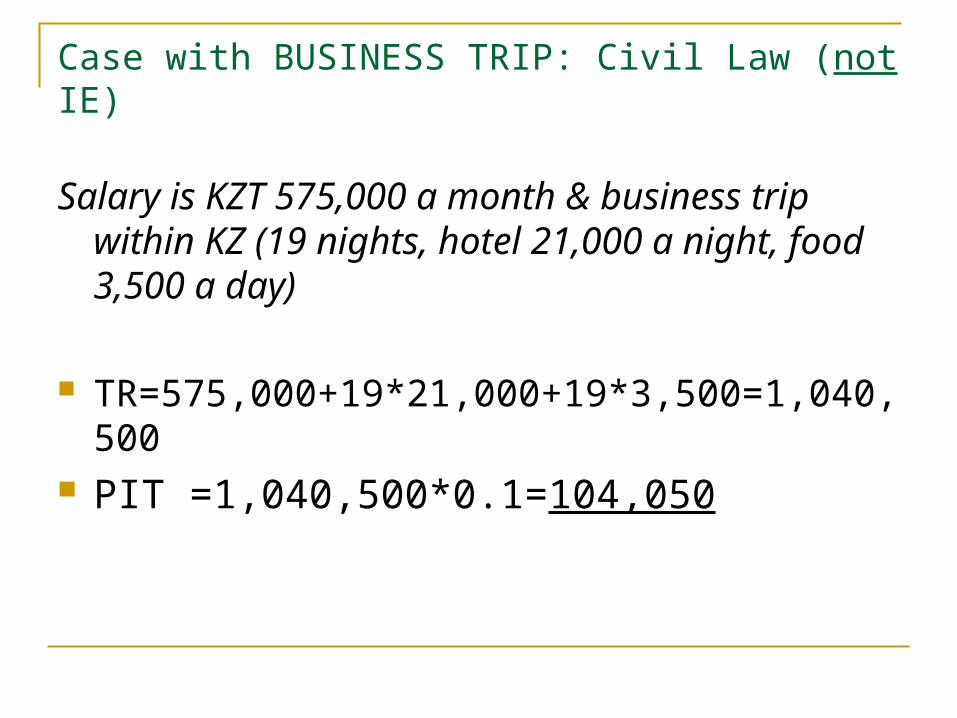

Case with BUSINESS TRIP: Civil Law (not IE)

Salary is KZT 575,000 a month & business trip within KZ (19 nights, hotel 21,000 a night, food 3,500 a day)

TR=575,000+19*21,000+19*3,500=1,040,500 PIT =1,040,500*0.1=104,050

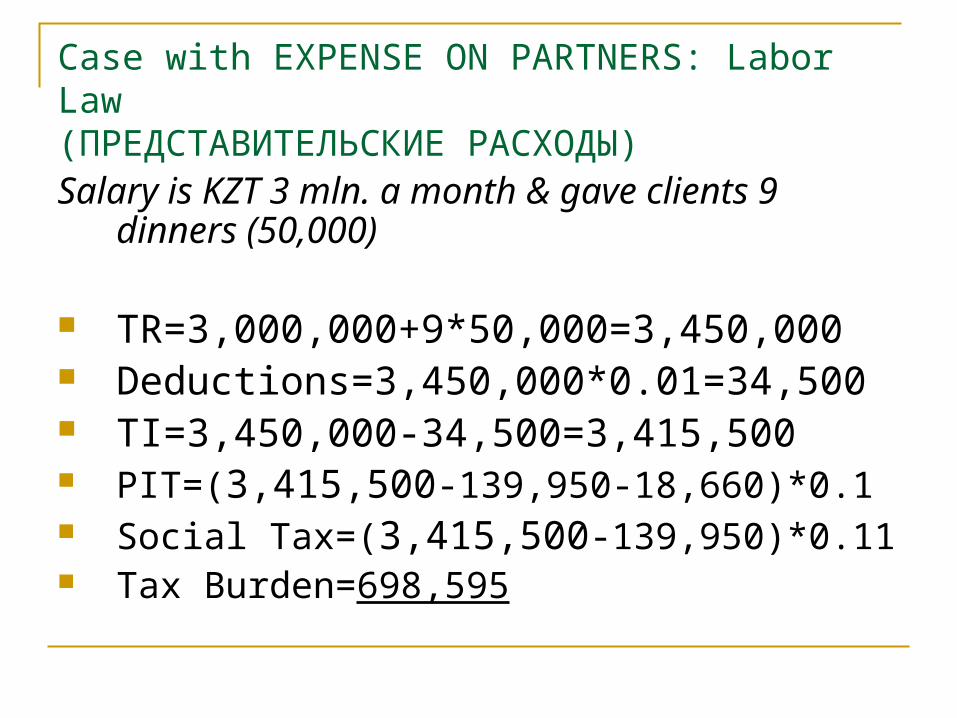

Case with EXPENSE ON PARTNERS: Labor Law(ПРЕДСТАВИТЕЛЬСКИЕ РАСХОДЫ)Salary is KZT 3 mln. a month & gave clients 9

dinners (50,000)

TR=3,000,000+9*50,000=3,450,000 Deductions=3,450,000*0.01=34,500 TI=3,450,000-34,500=3,415,500 PIT=(3,415,500-139,950-18,660)*0.1 Social Tax=(3,415,500-139,950)*0.11 Tax Burden=698,595

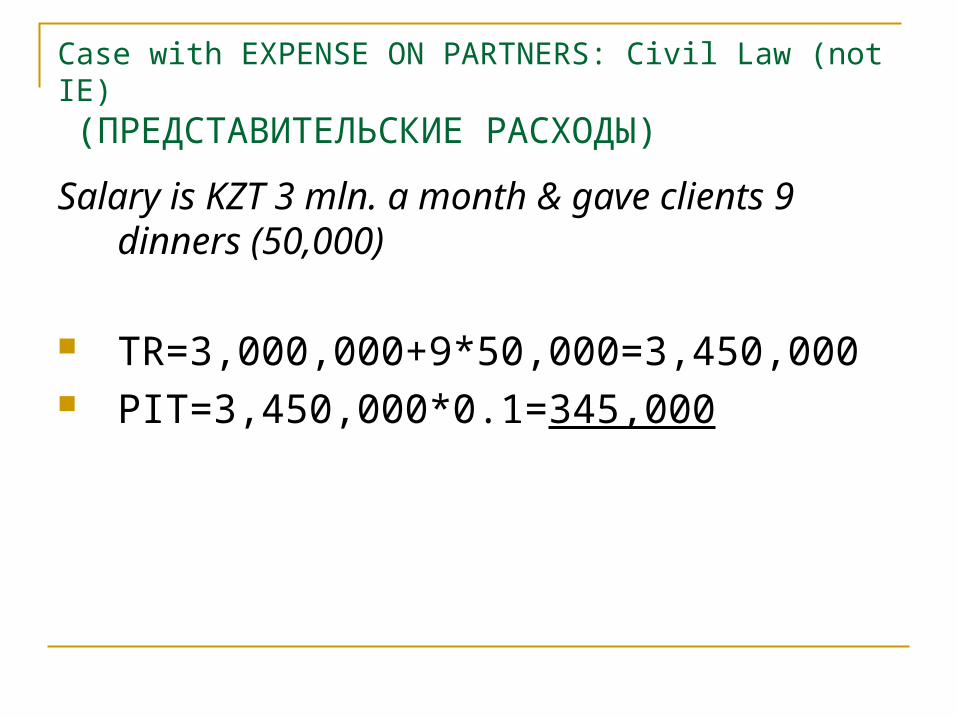

Case with EXPENSE ON PARTNERS: Civil Law (not IE) (ПРЕДСТАВИТЕЛЬСКИЕ РАСХОДЫ)

Salary is KZT 3 mln. a month & gave clients 9 dinners (50,000)

TR=3,000,000+9*50,000=3,450,000 PIT=3,450,000*0.1=345,000

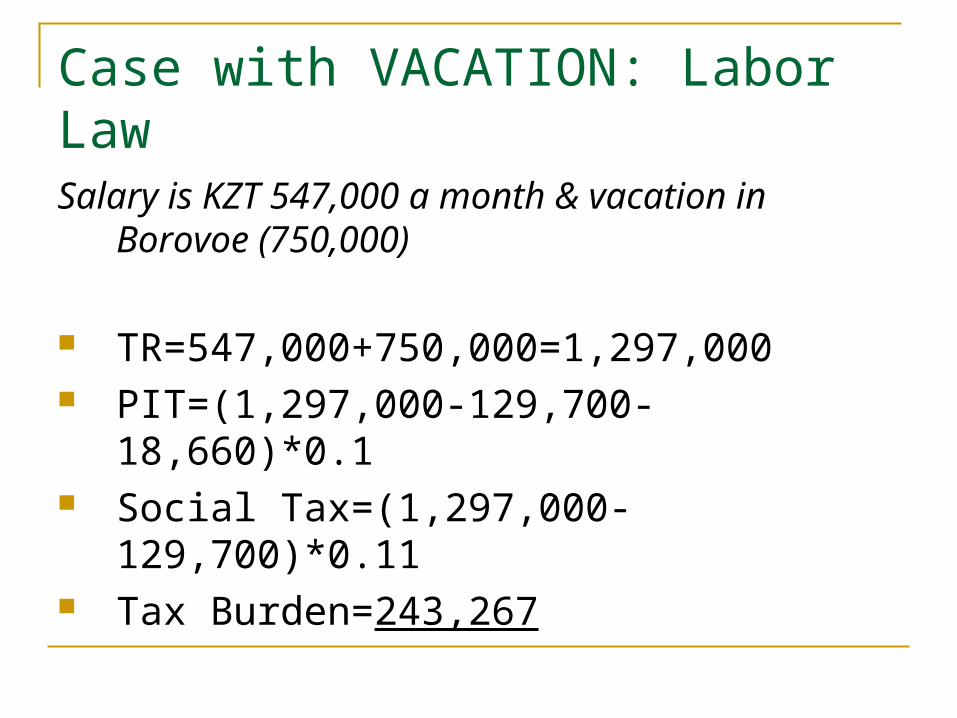

Case with VACATION: Labor LawSalary is KZT 547,000 a month & vacation in

Borovoe (750,000)

TR=547,000+750,000=1,297,000 PIT=(1,297,000-129,700-18,660)*0.1 Social Tax=(1,297,000-129,700)*0.11 Tax Burden=243,267

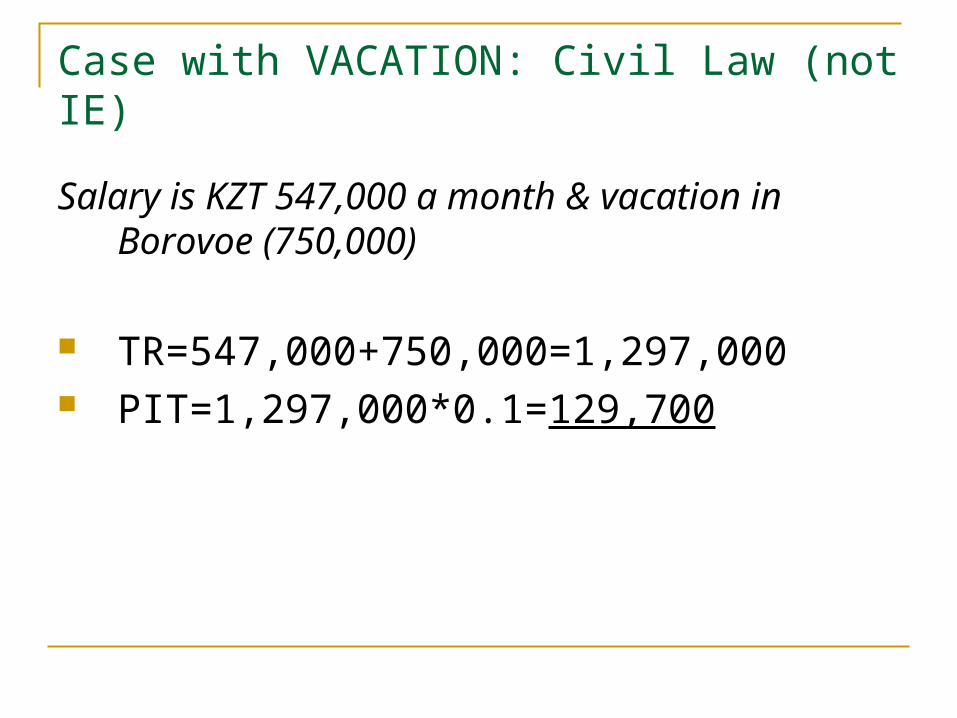

Case with VACATION: Civil Law (not IE)

Salary is KZT 547,000 a month & vacation in Borovoe (750,000)

TR=547,000+750,000=1,297,000 PIT=1,297,000*0.1=129,700

Case with FORGIVEN LOAN: Labor Law

Salary is KZT 570,000 a month & forgave the loan from the company in the amount of 300,000.

TR=570,000+300,000=870,000 PIT=(870,000-87,000-18,660)*0.1 Social Tax=(870,000-87,000)*0.11 Tax Burden=162,564

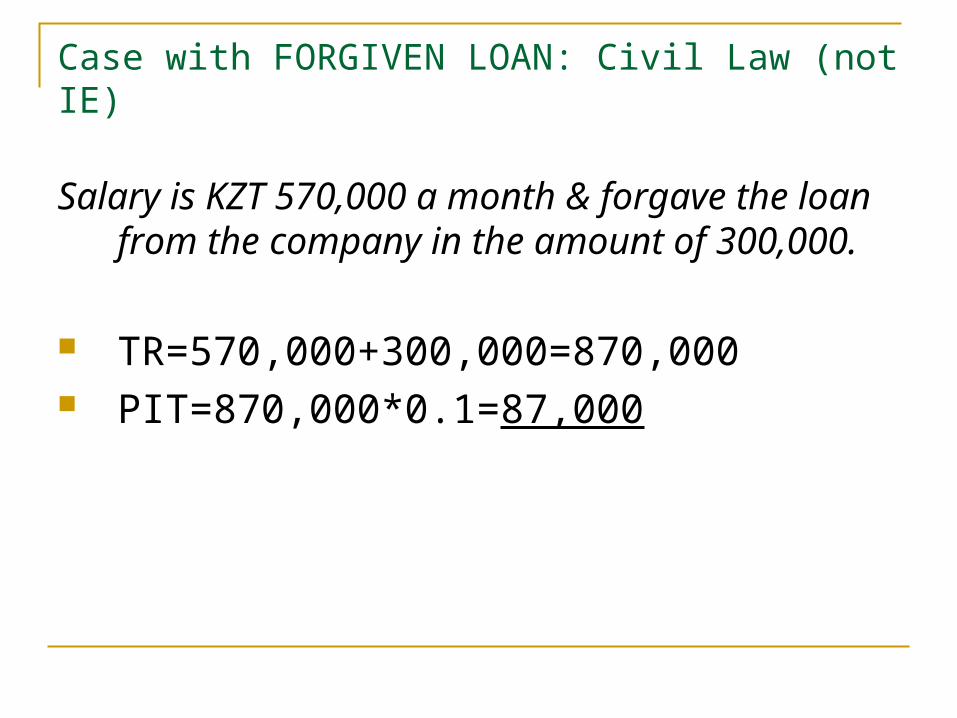

Case with FORGIVEN LOAN: Civil Law (not IE)

Salary is KZT 570,000 a month & forgave the loan from the company in the amount of 300,000.

TR=570,000+300,000=870,000 PIT=870,000*0.1=87,000

INCREASE IN VALUE

ПРИРОСТ СТОИМОСТИ

Art.155-3(19-22)

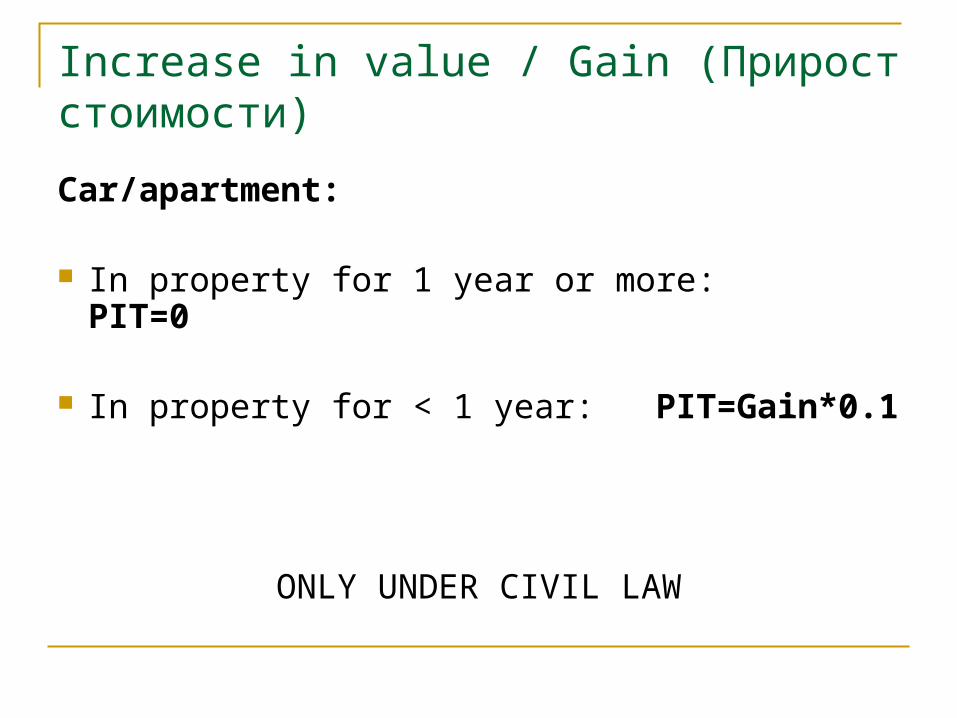

Increase in value / Gain (Прирост стоимости)

Car/apartment:

In property for 1 year or more: PIT=0

In property for < 1 year: PIT=Gain*0.1

ONLY UNDER CIVIL LAW

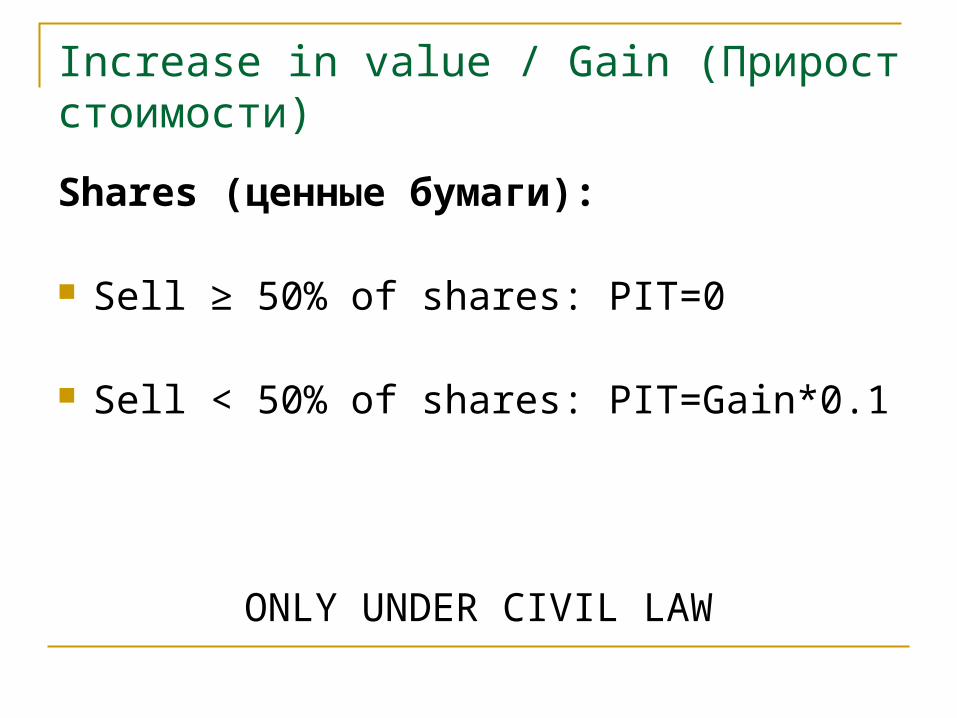

Increase in value / Gain (Прирост стоимости)

Shares (ценные бумаги):

Sell ≥ 50% of shares: PIT=0

Sell < 50% of shares: PIT=Gain*0.1

ONLY UNDER CIVIL LAW

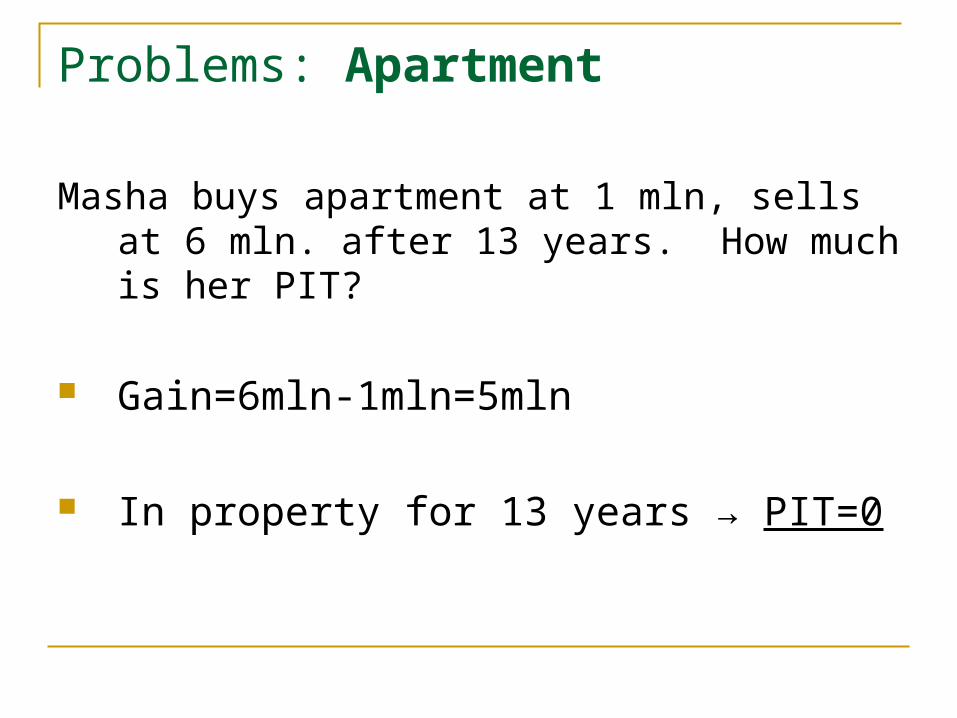

Problems: Apartment

Masha buys apartment at 1 mln, sells at 6 mln. after 13 years. How much is her PIT?

Gain=6mln-1mln=5mln

In property for 13 years → PIT=0

Problems: Car

Masha buys a car at 2 mln, sells at 4 mln. after 3 years. How much is her PIT?

Gain=4mln-2mln=2mln

In property for 3 years → PIT=0

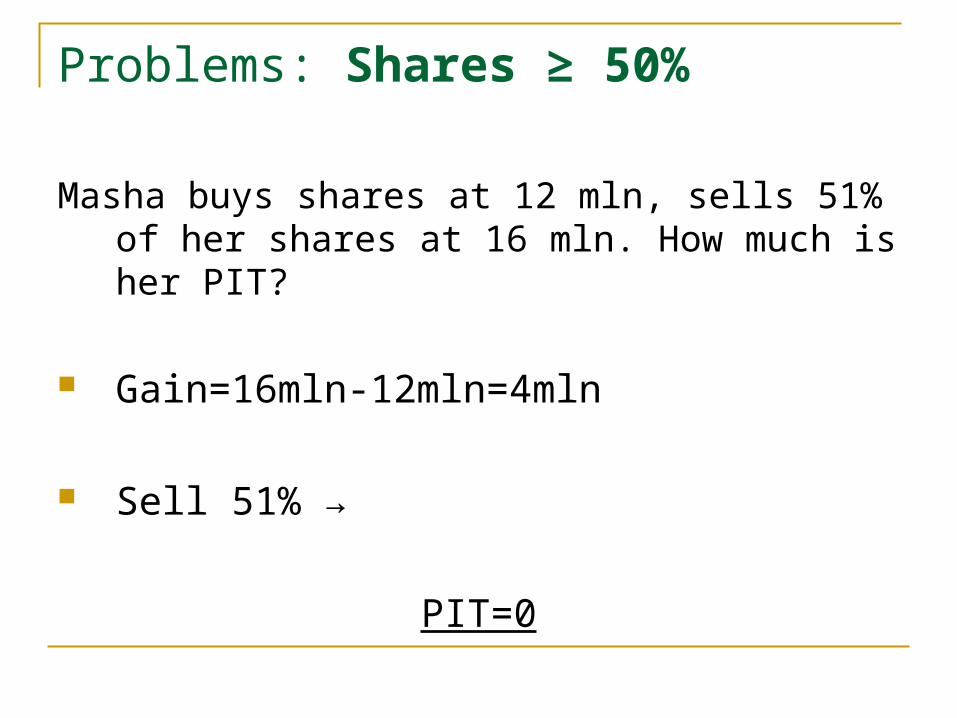

Problems: Shares ≥ 50%

Masha buys shares at 12 mln, sells 51% of her shares at 16 mln. How much is her PIT?

Gain=16mln-12mln=4mln

Sell 51% →

PIT=0

Problems: Shares < 50%

Masha buys shares at 11 mln, sells 30% of her shares at 13 mln. How much is her PIT?

Gain = 13mln – 11mln = 2 mln

Sell 30% →

PIT = 2mln * 0.1 = 200,000

Good Luck!