Prentice Hall, Inc. © 2006 5-1 A Human Resource Management Approach STRATEGIC COMPENSATION Prepared...

23

Prentice Hall, Inc. © 2006 5-1 A Human Resource A Human Resource Management Approach Management Approach STRATEGIC STRATEGIC COMPENSATION COMPENSATION Prepared by David Oake Chapter 5 Chapter 5 Incentive Pay Incentive Pay

-

Upload

kenneth-merritt -

Category

Documents

-

view

218 -

download

4

Transcript of Prentice Hall, Inc. © 2006 5-1 A Human Resource Management Approach STRATEGIC COMPENSATION Prepared...

Prentice Hall, Inc. © 2006

5-1

A Human Resource A Human Resource Management ApproachManagement Approach

STRATEGIC STRATEGIC COMPENSATIONCOMPENSATION

Prepared by David Oakes

Chapter 5Chapter 5

Incentive PayIncentive Pay

Prentice Hall, Inc. © 2006

5-2

Incentive PayIncentive Pay

Compensation fluctuates according to A pre-established formula Individual or group goals Company earnings

Adds to base pay Controls costs Motivates employees

Prentice Hall, Inc. © 2006

5-3

Incentive Pay CategoriesIncentive Pay Categories

Individual

Group

Company-wide

Prentice Hall, Inc. © 2006

5-4

Performance MeasuresPerformance Measures

Individual incentive plans

Quantity of work output

Quality of work output

Monthly sales

Work safety record

Work attendance

Prentice Hall, Inc. © 2006

5-5

Group Incentive Group Incentive Performance MeasuresPerformance Measures

Group incentive plans Customer satisfaction

Labor cost savings

Materials cost savings

Reduction in accidents

Services cost savings

Prentice Hall, Inc. © 2006

5-6

Company-WideCompany-WidePerformance MeasuresPerformance Measures

Company-wide incentive plans

Company profits

Cost containment

Market share

Sales revenue

Prentice Hall, Inc. © 2006

5-7

Types of Individual Types of Individual Incentive Plans Incentive Plans

Piecework plans

Management incentive plans

Behavior encouragement plans

Referral plans

Prentice Hall, Inc. © 2006

5-8

Piecework PlansPiecework Plans

Awards based on individual production v. objective standards

Awards based on individual performance standards using objective & Subjective criteria

Quantity and / or quality goals

Prentice Hall, Inc. © 2006

5-9

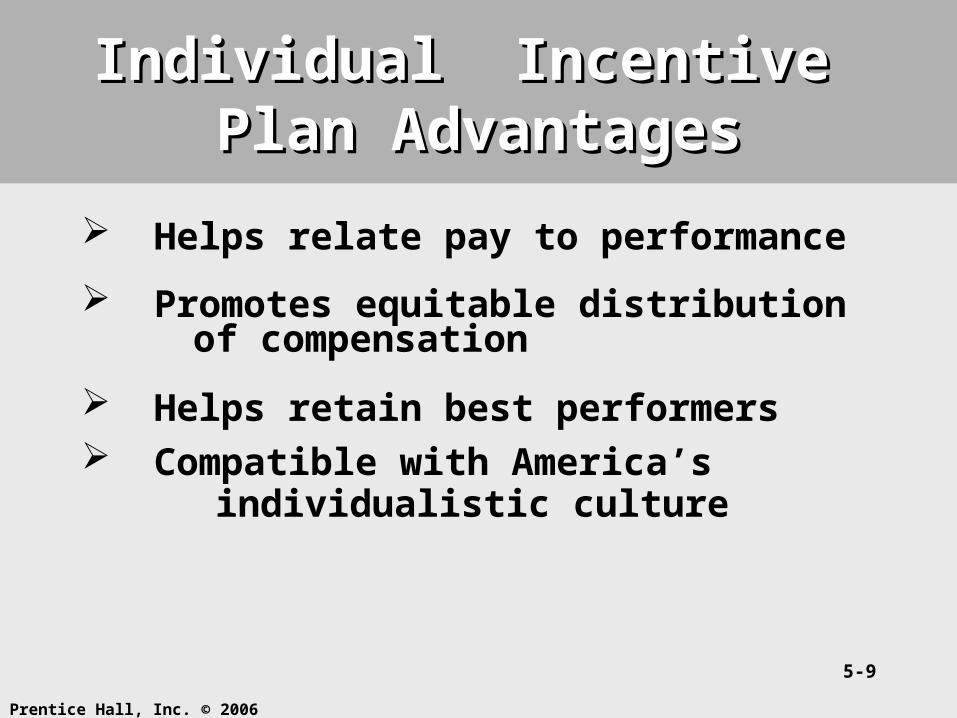

Individual Incentive Plan Individual Incentive Plan AdvantagesAdvantages

Helps relate pay to performance

Promotes equitable distribution of compensation

Helps retain best performers Compatible with America’s individualistic culture

Prentice Hall, Inc. © 2006

5-10

DisadvantagesDisadvantages May promote inflexibility Unrealistic standards may hamper employee motivation

Setting performance standards is time consuming Factors beyond employee’s control may affect outcomes Factors not rewarded may be overlooked

Prentice Hall, Inc. © 2006

5-11

Group Incentive PlansGroup Incentive Plans

Rewards employees for their collective performance Use has increased in industry

2 types Team - based or small group Gain sharing

Prentice Hall, Inc. © 2006

5-12

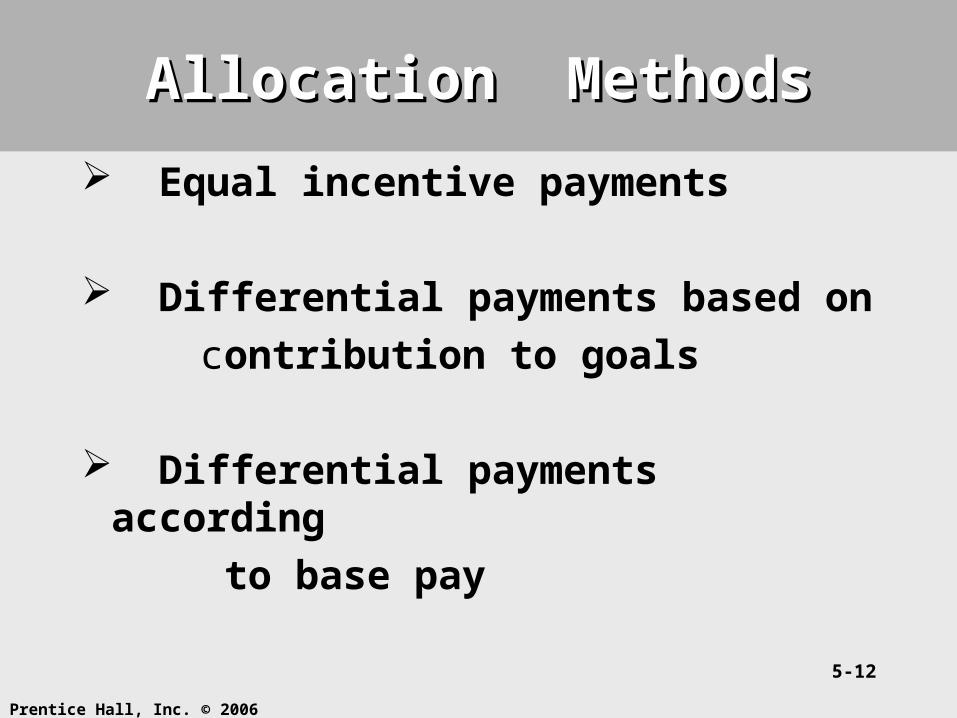

Allocation MethodsAllocation Methods

Equal incentive payments

Differential payments based on

contribution to goals

Differential payments according

to base pay

Prentice Hall, Inc. © 2006

5-13

Gain SharingGain Sharing

Incentives based on company’s improved productivity

Based on open leadership

Involves employee participation

Includes bonuses

Prentice Hall, Inc. © 2006

5-14

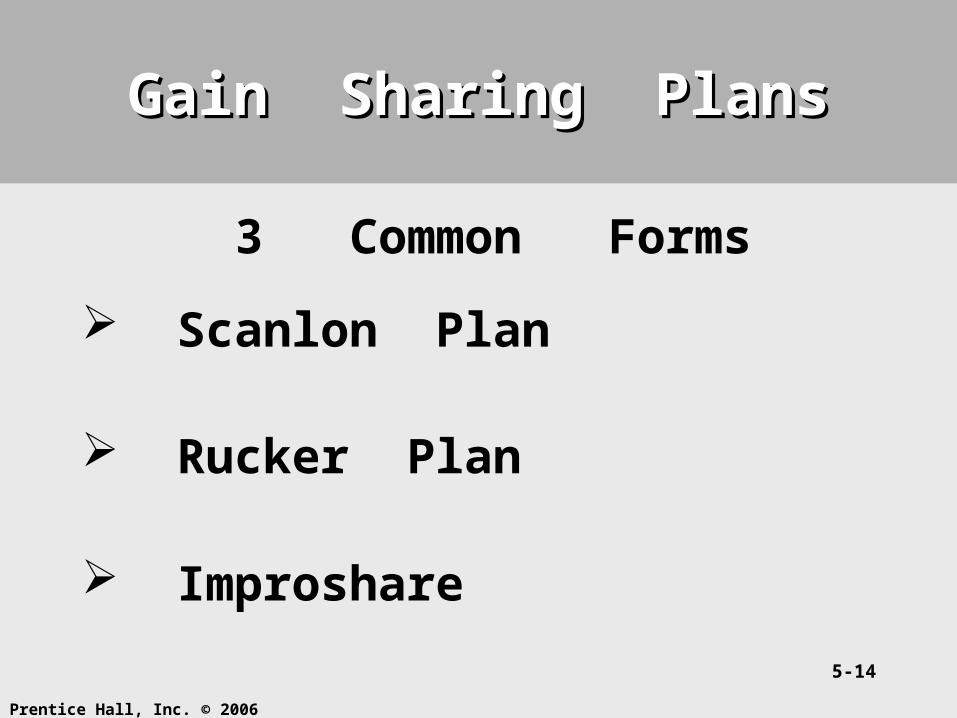

Gain Sharing PlansGain Sharing Plans

3 Common Forms

Scanlon Plan

Rucker Plan

Improshare

Prentice Hall, Inc. © 2006

5-15

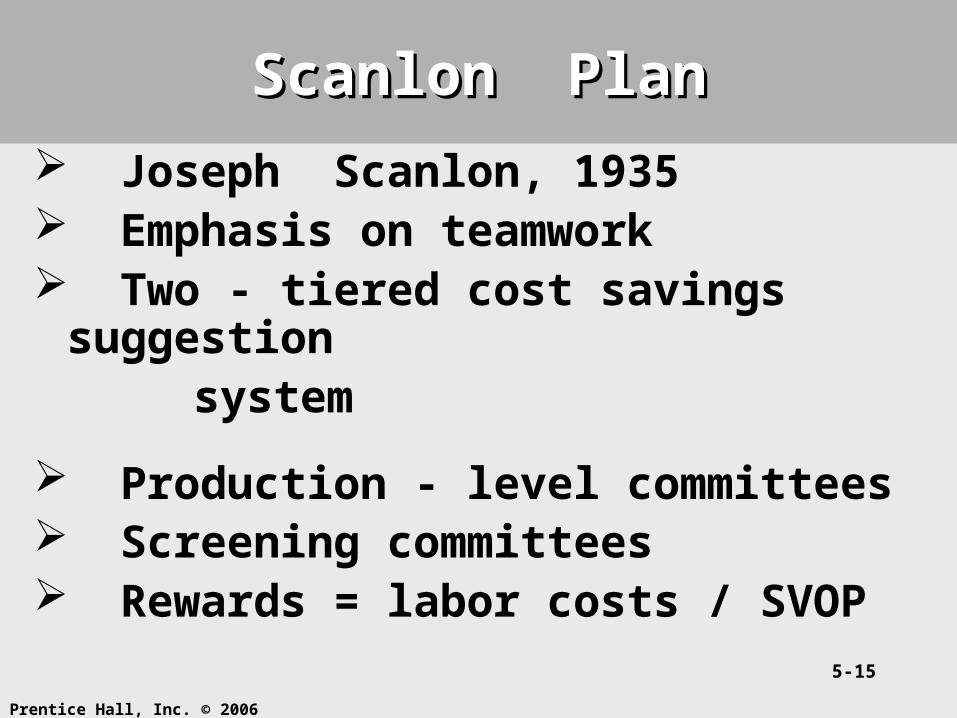

Scanlon PlanScanlon Plan

Joseph Scanlon, 1935 Emphasis on teamwork Two - tiered cost savings suggestion system

Production - level committees Screening committees Rewards = labor costs / SVOP

Prentice Hall, Inc. © 2006

5-16

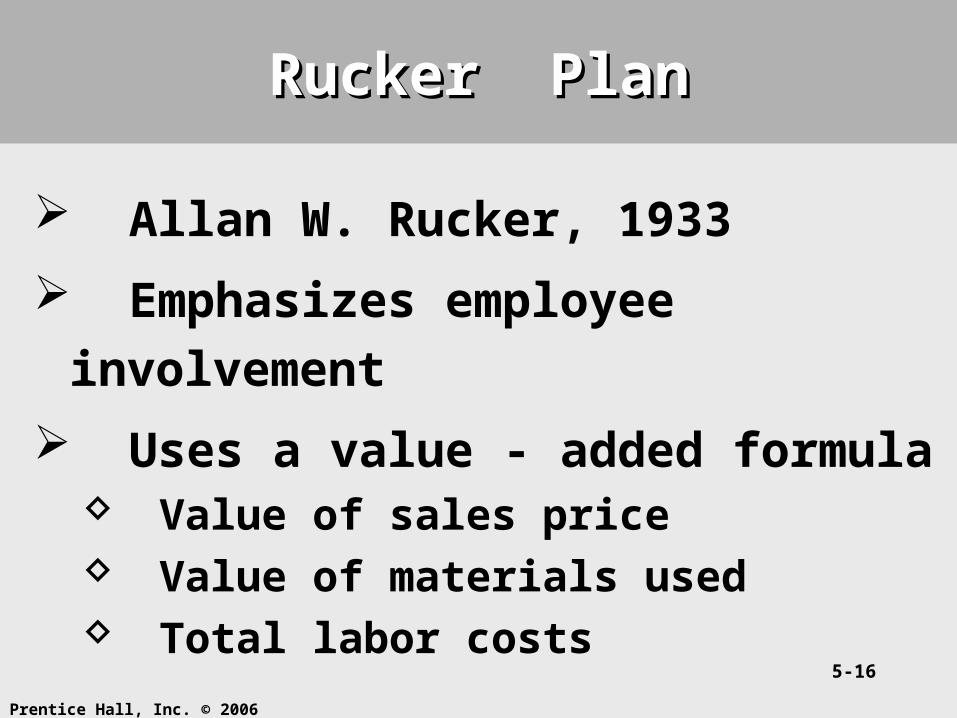

Rucker PlanRucker Plan

Allan W. Rucker, 1933

Emphasizes employee involvement

Uses a value - added formula Value of sales price Value of materials used Total labor costs

Prentice Hall, Inc. © 2006

5-17

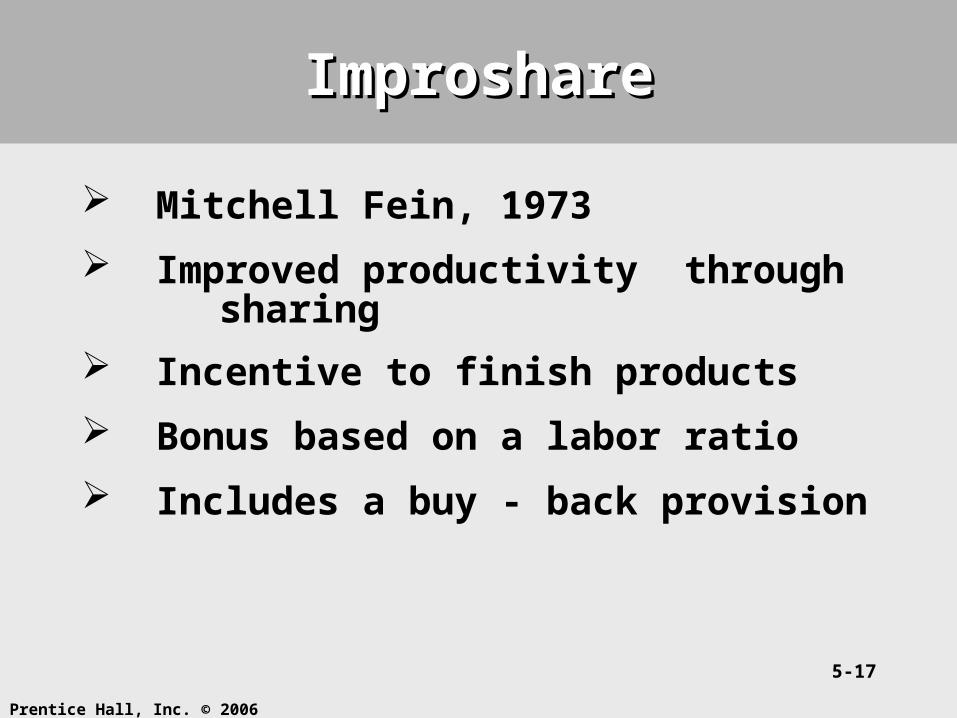

ImproshareImproshare

Mitchell Fein, 1973

Improved productivity through sharing

Incentive to finish products

Bonus based on a labor ratio

Includes a buy - back provision

Prentice Hall, Inc. © 2006

5-18

Company - Wide Incentive PlansCompany - Wide Incentive Plans

Rewards employees when company meets performance standards

2 Types Profit sharing plans Employee stock option plans

Prentice Hall, Inc. © 2006

5-19

Profit Sharing PlansProfit Sharing Plans

Current profit sharing plans

Deferred profit sharing plans

Prentice Hall, Inc. © 2006

5-20

Profit Sharing FormulasProfit Sharing Formulas

Fixed-first-dollar-of-profits Graduated first-dollar-of profits Probability threshold formula

Prentice Hall, Inc. © 2006

5-21

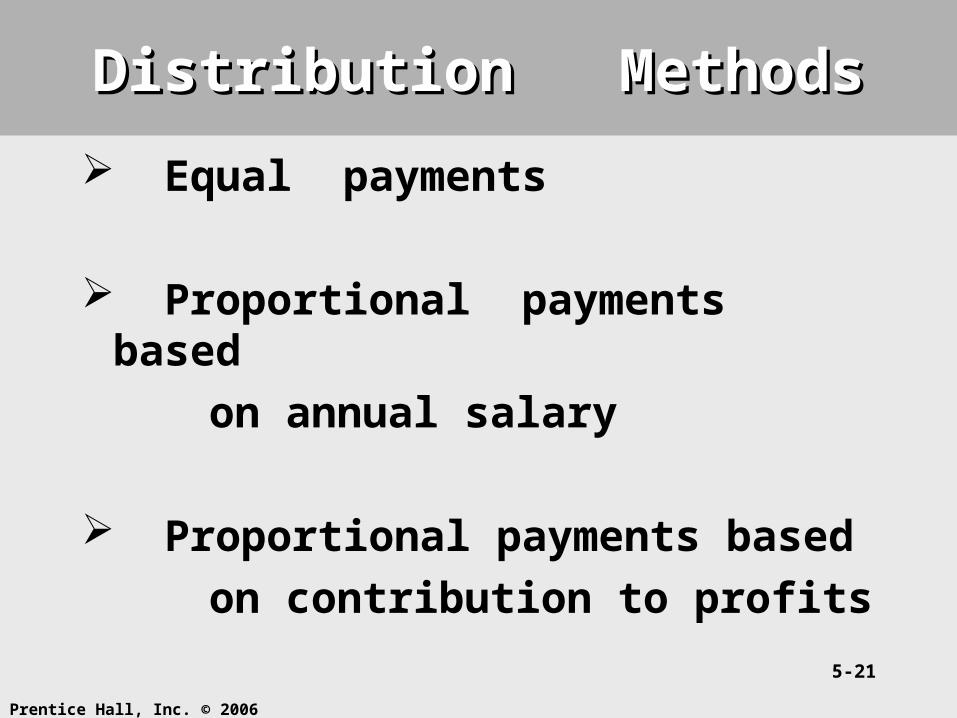

Distribution MethodsDistribution Methods

Equal payments

Proportional payments based

on annual salary

Proportional payments based

on contribution to profits

Prentice Hall, Inc. © 2006

5-22

Incentive Pay Considerations Incentive Pay Considerations

Based on individual or group performance?

Acceptable level of risk?

Replace traditional pay?

Performance criteria evaluated?

Appropriate time horizon?

Prentice Hall, Inc. © 2006

5-23

Competitive Strategies Competitive Strategies

Lowest - cost Lower output costs per employee Individual & group incentive plans Behavioral encouragement plans

Differentiation Unique product or services Creative, risk - taking employees Long - term focus Team - based incentives