PowerPoint Presentation - Dr. Asad Karim Khan Priyo · expansion phase of the business cycle. 2....

36

17 CHAPTER ECONOMIC GROWTH

Transcript of PowerPoint Presentation - Dr. Asad Karim Khan Priyo · expansion phase of the business cycle. 2....

17CHAPTERECONOMIC GROWTH

U.S. real GDP per person and the standard of living tripled

between 1960 and 2010.

We see even more dramatic change in China, where

incomes have tripled not in 50 years but in the 13 years

since 1999.

Incomes are growing rapidly in some other economies of

Asia, Africa, and South America.

What are the forces that make real GDP grow?

The Basics of Economic Growth

The Basics of Economic Growth

Economic growth is the sustained expansion of production

possibilities measured as the increase in real GDP over a

given period.

Calculating Growth Rates

The economic growth rate is the annual percentage

change of real GDP.

The economic growth rate tells us how rapidly the total

economy is expanding.

The Basics of Economic Growth

The standard of living depends on real GDP per person.

Real GDP per person is real GDP divided by the

population.

Real GDP per person grows only if real GDP grows faster

than the population grows.

The Basics of Economic Growth

Economic Growth Versus Business Cycle Expansion

Real GDP can increase for two distinct reasons:

1. The economy might be returning to full employment in an

expansion phase of the business cycle.

2. Potential GDP might be increasing.

The return to full employment in an expansion phase of the

business cycle isn’t economic growth.

The expansion of potential GDP is economic growth.

The Basics of Economic Growth

This Figure illustrates the

distinction.

A return to full employment

in a business cycle

expansion is a movement

from inside the PPF (point

A) to a point on the PPF

(point B).

Economic growth is the

outward shift of the PPF

from PPF0 to PPF1 and the

movement from point B on

PPF0 to point C on PPF1.

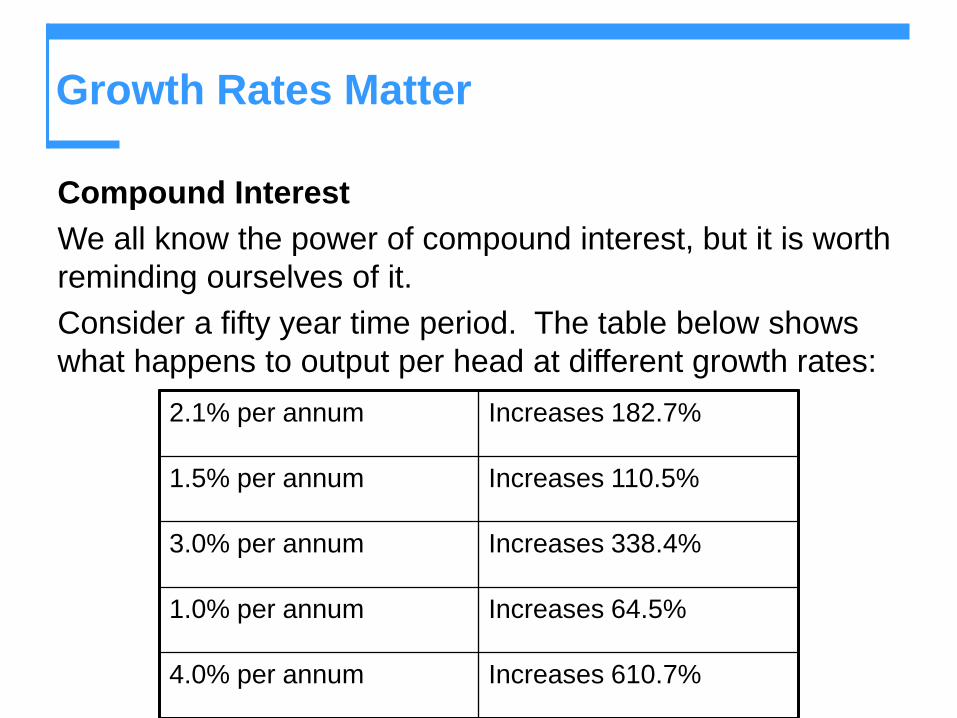

Growth Rates Matter

Compound Interest

We all know the power of compound interest, but it is worth

reminding ourselves of it.

Consider a fifty year time period. The table below shows

what happens to output per head at different growth rates:

2.1% per annum Increases 182.7%

1.5% per annum Increases 110.5%

3.0% per annum Increases 338.4%

1.0% per annum Increases 64.5%

4.0% per annum Increases 610.7%

Growth Rates Matter

The Magic of Sustained Growth

The Rule of 70 states that the number of years it takes for

the level of a variable to double is approximately 70 divided

by the annual percentage growth rate of the variable.

Growth Rates Matter

Applying the Rule of 70

This Figure shows the doubling time for growth rates.

A variable that grows at 7 percent a year doubles in 10 years.

A variable that grows at 2 percent a year doubles in 35 years.

A variable that grows at 1 percent a year doubles in 70 years.

Long-Term Growth Trends

Real GDP Growth in the World Economy

This Figure shows the growth in the rich countries.

Japan grew rapidly in

the 1960s, slower in the

1980s, and stagnated

during the 1990s.

Growth in Europe Big 4,

Canada, and the United

States has been similar.

Economic Growth Trends

This Figure shows the

growth of real GDP per

person in a group of

poor countries.

The gaps between real

GDP per person in the

United States and in

these countries have

widened.

The Causes of Economic Growth:

A First Look

Preconditions for Economic Growth

The basic precondition or prerequisite for economic

growth is an appropriate incentive system.

Three institutions that help with the creation of appropriate

incentives are:

Markets

Clear and certain property rights

Monetary exchange

The Causes of Economic Growth:

A First Look

For economic growth to persist, society somehow needs to

ensure these three activities:

Saving and investment in new capital

Investment in human capital

Discovery of new technologies

Appropriate incentives allow these activities to occur in a

decentralized market, society.

The Causes of Economic Growth:

A First Look

Saving and Investment in New Capital

The accumulation of capital dramatically increases output and

productivity; one US farmer can feed many, many households.

Investment in Human Capital

Human capital acquired through education, on-the-job training,

and learning-by-doing can also dramatically increase output and

productivity.

Discovery of New Technologies

Technological advances contribute immensely to increasing

productivity; think what you can do with a PC, things that were

impossible for your parents without months of work.

Growth Accounting

The quantity of real GDP supplied, Y, depends on the

quantity of labor, L, the quantity of capital, K, and the state

of technology, T.

The purpose of growth accounting is to estimate how

much real GDP growth comes from growth of labor and

capital inputs, and how much is apparently because of

technological change

Growth accounting is based on the aggregate production

function,

Y = F(L, K, T ).

Growth Accounting

Labor Productivity

Labor productivity is real GDP per hour of labor or per

unit of labor; it equals real GDP divided by aggregate

hours or real GDP divided by total number of labor.

Growth Accounting

Growth accounting divides growth in productivity into two

sources:

Growth in capital per unit of labor

Technological change

Any productivity growth not accounted for by growth in

capital is allocated to technological change, so this

category is a broad catch-all concept, which also includes

for example efficiency improvements from better

organization, economic system, or management.

Growth Accounting

The Productivity Curve

The productivity curve is the relationship between real

GDP per unit of labor and the amount of capital per unit of

labor, with technology held constant.

Growth Accounting

This Figure illustrates the productivity curve.

An increase in

capital per unit of

labor brings a

movement along

the productivity

curve.Technological

change shifts the

productivity curve.

Growth Accounting

The shape of the productivity curve reflects the law of

diminishing returns.

The law of diminishing returns states that, as the

quantity of one input increases with the quantities of all

other inputs remaining the same, output increases but

eventually by ever smaller increments.

Robert Solow discovered that diminishing returns are well

described by the one-third rule: with no change in

technology, on the average, a 1 percent increase in capital

per hour of work brings a one-third of 1 percent increase in

output per hour of labor.

Growth Accounting

Achieving Faster Growth

Growth accounting suggests if we increase the growth rate

of capital per hour of labor, or increase the pace of

technological advance, we should be able to achieve

faster economic growth.

Some ways to do this are:

Stimulate saving

Higher saving rates may increase the growth rate of

capital. Tax incentives might be provided to boost saving.

Growth Accounting

Stimulate research and development

Because new discoveries can be used by everyone, not

all the benefit of a discovery is captured by the initial

discoverer.

So there can be a tendency to underinvest in research

and development activity, i.e. to do less than would be

socially optimal.

Government financing or subsidies of research and

development might counter this tendency to

underinvestment.

Growth Accounting

Encourage international trade

Free international trade stimulates growth by extracting all

the available gains from specialization and exchange, and

increasing competition to innovate and be efficient.

The fastest growing nations tend to be the ones with the

fastest growing exports and imports.

Improve the quality of education

Benefits from education extend beyond the person being

educated. Improvement in quality of education results in

improvement in human capital and hence improves

productivity

Growth Theories

Classical Growth Theory

Classical growth theory came to the conclusion that real

GDP growth was temporary; when real GDP per person

rises above the subsistence level, a population explosion

brings real GDP per person back to the subsistence level.

This may sound stupid now, but in the early 1800s it was a

not unreasonable conclusion – it was not clear that living

standards in most of the world were any higher than in

Roman times.

Growth Theories

The basic classical idea

There is a subsistence real wage rate, which is the

minimum real wage rate needed to maintain life and match

births to deaths.

Advances in technology shifts the productivity curve up.

Labor productivity increases and the real wage rate rises

above the subsistence level.

When the real wage rate is above the subsistence level,

the population grows – births exceed deaths.

Population growth increases the supply of labor, which

lowers the real wage rate.

Growth Theories

The population continues to increase until the real wage

rate has been driven back down to the subsistence real

wage rate, where deaths match births again.

At this real wage rate, both population growth and

economic growth stop.

Contrary to the assumption of the classical theory, the

historical evidence is that population growth is not tightly

linked to income per person, and rising incomes do not

result in population growth driving incomes back down to

subsistence levels.

Growth Theories

This Figure

illustrates

the

classical

growth

theory.

Growth Theories

Neoclassical Growth Theory

Neoclassical growth theory posits that real GDP per

person grows because technological change induces a

level of saving and investment that makes capital per hour

of labor grow.

Growth ends only if technological change stops.

Growth Theories

The neoclassical economics of population growth

The neoclassical view is that the population growth rate is independent of both real GDP per person and its growth rate.

The population growth rate equals the birth rate minus the death rate.

The birth rate is influenced by the opportunity cost of a woman’s time.

As women’s wage rates have increased, the opportunity cost of having children has also increased and the birth rate has fallen.

Growth Theories

The death rate is influenced by nutrition, sanitation, public

health policy, and the quality and availability of health care.

As the quality and availability of health care has improved,

the death rate has fallen.

The falls in both the birth rate and the death rate have

tended to offset each other and to make the population

growth rate independent of the level of income; in most

high-income societies the death rate exceeds the birth rate

and population is tending to fall [immigration and an

unusually high birth rate make the US an exception].

Growth Theories

Target Rate of Return and Saving

Ceteris paribus, the higher the real interest rate, the greater is the amount that people save. To decide how much to save, people compare the real interest rate with a target rate of return. If the real interest rate exceeds the target rate of return, saving is sufficient to make capital per hour of labor grow. If the target rate of return exceeds the real interest rate, saving is not sufficient to maintain the current level of capital per hour of labor, so capital per hour of labor shrinks. And if the real interest rate equals a target rate of return, saving is just sufficient to maintain the quantity of capital per hour of labor at its current level.

Growth Theories

The basic neoclassical idea

Technology begins to advance more rapidly.

New profit opportunities arise.

Investment and saving increase.

As technology advances and the capital stock grows, real

GDP per person rises.

Diminishing returns to capital per hour of labor lower the

real interest rate and eventually growth stops unless

technology keeps on advancing.

Growth Theories

This

Figure

illustrates

neo-

classical

growth

theory.

Growth Theories

New Growth Theory

“New growth theory” holds that real GDP per person grows because of choices that people make in the pursuit of profit and concludes that growth can persist indefinitely.

The theory emphasizes that

People are always in pursuit of profit

Discoveries bring profit

In a market economy, profit brings competition and competition destroys profit

People look for more profit, more discoveries take place, more knowledge is gathered, more growth takes place

Knowledge is not subject to diminishing returns

Growth Theories

This

Figure

illustrates

new

growth

theory.

Growth Theories

This Figure summarizes the ideas of new growth theory as

a perpetual motion machine.