Potential of takaful in pakistan

83

SCOPE OF TAKAFUL IN PAKISTAN The Scope of Takaful Insurance in Pakistani Market __________________ A thesis Presented to The faculty of Management Sciences Bahria Institute of Management & Computer Sciences, Karachi In Partial Fulfillment Of the Requirements for the Degree Master in Business Administration ____________________ By ABDUL WAHAB Reg # 12927 Dec, 2013 Page 1

-

Upload

abdul-wahab -

Category

Education

-

view

214 -

download

1

description

Transcript of Potential of takaful in pakistan

SCOPE OF TAKAFUL IN PAKISTAN

The Scope of Takaful Insurance in Pakistani Market

__________________

A thesis Presented toThe faculty of

Management SciencesBahria Institute of Management & Computer Sciences, Karachi

In Partial FulfillmentOf the Requirements for the

Degree Master in Business Administration ____________________

By

ABDUL WAHABReg # 12927

Dec, 2013

Page 1

SCOPE OF TAKAFUL IN PAKISTAN

BAHRIA UNIVERSITY

INSTITUTE OF MANAGEMENT AND COMPUTER SCIENCES, KARACHI

RECOMMENDATION FOR ORAL EXAMINATION

This Project/thesis hereto attached, entitled,“ The Scope of Takaful Insurance in Pakistani Market”, prepared and submitted by Abdul Wahab, in partial fulfillment of the requirements for the degree MASTER IN BUSINESS ADMINSTRATION, is hereby recommended for appropriate action.

Date: _______ _________________

Advisor

Name: Muhammad Faisal ([email protected])

Page 2

SCOPE OF TAKAFUL IN PAKISTAN

PROJECT/ THESIS COMMITTEE

In partial fulfillment of the requirements for the degree of MASTER IN BUSINESS ADMINSTRATION, this thesis entitled, “The Scope of Takaful Insurance in Pakistani Market” is hereby recommended for Oral Examination.

_________________________

Chairman

Name: __________________

_____________________ __________________ ____________________

Member Member Member

Name: _____________ Name: _____________ Name: ______________

__________________

Date

Page 3

SCOPE OF TAKAFUL IN PAKISTAN

BAHRIA UNIVERSITYINSTITUTE OF MANAGEMENT AND COMPUTER SCIENCES, KARACHI

Project/Thesis: “Potential The Scope of Takaful Insurance in Pakistani Market”

Date: ____________

Time: ____________

PANEL OF ORAL EXAMINERS ACTION

_________________________ ____________

Chairman

Name: _________________

____________________________ ____________

Member

Name: _________________

_____________________________ ____________

Member

Name: _______________

____________________________

Advisor

Name: ______________

Page 4

SCOPE OF TAKAFUL IN PAKISTAN

BAHRIA UNIVERSITY

INSTITUTE OF MANAGEMENT AND COMPUTER SCIENCES, KARACHI

APPROVAL SHEET

This Project/ thesis entitled, “Potential The Scope of Takaful Insurance in Pakistani Market”, prepared and submitted by Abdul Wahab, in partial fulfillment of the requirements for the degree of MASTER IN BUSINESS ADMINISTRATION has been examined and recommended for acceptance and approval.

THESIS COMMITTEE

____________________________

Chairman

Name: ___________________________________

_______________ _____________

Member Member Member

Name: ____________ Name: ____________ Name: ____________

PANEL OF EXAMINERS

Approved by the Committee on Oral Examination with a Grade of __________

__________________________

Chairman

Name: _________________________________

__________________ ______________

Member Member Member

Name: _____________ Name: _____________ Name: ____________

__________________________________

Head of the Department

Management Sciences

Page 5

SCOPE OF TAKAFUL IN PAKISTAN

DEDICATION

I would like to dedicate this thesis to my parents who gave me courage and supported me in this task. I would also like to dedicate this to my teachers who support me in Bahria University in my whole tenure.

Page 6

SCOPE OF TAKAFUL IN PAKISTAN

ACKNOWLEDGMENT

I am thankful to Allah who gave help, knowledge, courage, support and strength to complete this task.

I am also thankful to my co-coordinator – Sir Muhammad Faisal and my Examiner Sir Akbar saeed, who supported me and helped me with their advices and suggestion and their guidelines with which I would not be able to complete this task.

I would also appreciate for Pak – Qatar Takaful Company Ltd to entertain my questions and to solve my queries. Those who help me gather data for this research I am thankful to them too.

Last but not least: I would thank my parents for their support and for allowing me to have an opportunity to be a part of a prestigious institute of Pakistan; Bahria University.

Page 7

SCOPE OF TAKAFUL IN PAKISTAN

ABSTRACT:

This research is based upon how Takaful industry of Pakistan is growing and what is potential and

future of this market. In this research paper the scope of takaful insurance is highlighted making

Pak Qatar Takaful Company an example. Pak Qatar takaful company is chosen for the research paper because it is pioneer of takaful insurance in Pakistan as well as, it has the maximum resource and research and experience in this area. The study is important because it identifies that why and how takaful insurance is better than conventional insurance and on the other hand, it also determines the future of takaful in Pakistani market. The research is based on data gathered though a questionnaire filled by 80 individuals. All of them are user of Insurance either congenital or Islamic. Conclusions and recommandations are totally based on data analysis of questionnaire.

Page 8

SCOPE OF TAKAFUL IN PAKISTAN

INTRODUCTION - 01

Page 9

SCOPE OF TAKAFUL IN PAKISTAN

SCOPE OF TAKAFUL IN PAKISTAN

INTRODUCTION

The process of globalization, every year makes people with different cultural values and

conceptions of the world more closely interact with each other. In order to find a common

language cannot do without mutual respect based on a thorough knowledge of the globe

neighboring cultures, traditions, religious and historical reasons specific to a particular nation or

people.

Today we'll discuss one of the most numerous of the world community, united by a common

religion of Islam. According to «The World Fact book 2004", Muslims make up one fifth of the

world population. The main set of rules and regulations, which must adhere to a devout Muslim,

sharia, is based on the Quran and the Sunnah, the main books of Islam. Sharia requires not only

complying with the numerous religious traditions and rituals, guided by certain principles in

daily life, but also imposes certain requirements for finance and business. And insurance is an

important component of the economy, is no exception. Traditional insurance in the form in

which it is taken in the western world, is not Sharia compliant, and therefore - forbidden.

CONCEPT OF TAKAFUL

Takaful (the mutual provision of guarantees to each other) is the main Islamic insurance product.

Its primary difference from traditional commercial insurance is the absence of elements of gharar

(uncertainty) and riba (usury). Element of gharar in the contract of insurance exceeds the

permitted level of Sharia, because at least for the insured, there is uncertainty as to the terms of

the contract (time, subject, etc.). In addition, the insurer is in the dark as to whether the funds

Page 10

SCOPE OF TAKAFUL IN PAKISTAN

paid to them as fees, to be used for permitted or forbidden by Islamic law transactions. The

element of riba may occur in the payment of interest on certain types of insurance, and in the

event that the amount collected as fees, participate in activities related to the charging or

payment of interest, as well as other operations not permitted by Sharia.

COMMERCIAL INSURANCE & ITS BASIS

In the commercial insurance include such elements as riba (usury), maysir (gambling) and gharar

(uncertainty). These elements are unacceptable from the point of view of Sharia law, though

Muslim jurists still cannot come to a consensus on the degree of the presence of these factors in

the traditional ways of the insured and the insurer. However, the laws of the business world and

impose its own requirements for the protection and preservation of financial and property

interests had developed an alternative form of insurance, known as "takaful" which in Arabic

means giving each other mutual guarantees.

Basis of takaful insurance

Takaful or Islamic insurance, based on the particular mechanism of distribution of profits and

losses, consistent with the principles of Sharia, and therefore satisfies the needs of the Muslim

world. The main objective of Islamic insurance - not just protecting their interests against

unforeseen circumstances by the joint participation of losses, but also making a profit. Because

of this, takaful companies can bring more profits than the traditional (Western-style) insurance

company. This goal is achieved by means of the division of responsibility, based on the model of

"Mudaraba", which is a recognized institute of Islamic economics.

Page 11

SCOPE OF TAKAFUL IN PAKISTAN

DIFFERING THE CONCEPT OF TAKAFUL & CONVENTIONAL INSURANCE

Risks are characteristic of human life, and they cannot be completely eliminated. Islam is not

prohibited risk or uncertainty itself, and the sale or exchange of risk or transfer risk to another

person with the contracts of purchase / sale. Takaful - meets the requirements of Sharia

agreement on the mutual sharing of risks, which includes participants and operators.

Unlike the traditional takaful insurance is risk assessment and management, as well as in the

management of takaful fund. In addition, there are differences in the relationship between the

operator (in the traditional insurance - the insurer) and the participants (policyholders).

If there is a traditional insurance risk transfer mechanism by which a person or organization can

exchange for a fee, to the certainty of its uncertainty, the takaful insurance, such a mechanism is

prohibited. Exchange losses on certain unspecified (insurance premium), as implemented in the

traditional insurance falls under the concept of gharar and is not allowed in Islam.

As an alternative to the principle of risk-sharing between the parties for the purpose of mutual

aid. Risk is shared between the parties in accordance with the scheme of mutual guarantee or

takaful scheme. Takaful operator must only organize the scheme. One of the responsibilities of

the operator - to ensure that each participant pays a fair contribution and that in the event of loss

participant will receive appropriate compensation.

Managing Risk in Takaful

In assessing and managing risk (underwriting) are not allowed in the takaful gharar (uncertainty

or speculation) and maysir (gambling). In the investment and management of the fund is not

allowed riba (usury). These three concepts (gharar, maysir and riba) should be completely

excluded from the takaful operations.

Page 12

SCOPE OF TAKAFUL IN PAKISTAN

Although Islam and imposes a number of restrictions on business, but he also preaches and

economic activity. The logic is simple: inattention to the economy can be harmful to Islam,

because it will be weakened financial base.

In practice, this means specific prohibitions, and one of the top cover gharar - the transaction, the

terms of which contain unnecessary or excessive risk-taking, for example, where the outcome

depends on the occurrence of a specified event. Because of him, first of all, require a substantial

revision of the classic insurance schemes. Another known limitation prohibits riba - usury, that

is, the percentage of loans. Simply speaking, it is impossible for the money to buy money;

fundraising should be based on a division of profits and risks. Therefore, most Islamic loans

become a joint venture between the bank and the borrower, in the classical interpretation of

reminding financial direct investment. Islamic insurance as a form of business has tremendous

potential and has a great potential of growth and development in the creation of new, unique

products and innovative technologies to promote them.

In order to avoid gharar (uncertainty), there should be complete clarity or disclosure of any

takaful contract. Full disclosure is applicable to both sides, as well as to the object and conditions

of the contract (the amount of coverage, etc.). It is not allowed to enter into Takaful contract if

there is at least one unknown element in the object of the contract and / or unknown risk under

the contract.

Since this is difficult to achieve an ideal situation, the takaful contract should be drafted so as to

avoid any exchange of gharar (uncertainty) between the parties to the contract.

Page 13

SCOPE OF TAKAFUL IN PAKISTAN

Maysir (gambling) is redundant side gharar. The participants (policyholders) may have an

insurable interest in respect of the contract object, but if the distribution of risk (in Takaful)

contains any speculative element, such an agreement is prohibited under the takaful.

Forbidden of Riba in Takaful

Riba (usury) is completely forbidden by Sharia law and, as a consequence, within the takaful. To

avoid riba fee for the participants in the distribution of risk is not considered a premium in terms

of traditional insurance. Under the takaful similar fee as a contribution or payment

(Mushahamah) in the form of donations to the condition of compensation (Tabarru). Moreover,

the fund generated from such contributions or donations to parties should be managed and

invested in accordance with the laws of Sharia. Participants or policyholders in the traditional

sense transmit their contributions to the operator or the insurer as a gift for their effective use

with the proviso that when the insured event the money will be refunded. Part of the

contributions received in the savings fund from investing which participants have the opportunity

to receive a regular income in the amount stipulated in the contract of the share which is usually

50 or 60%. With this investment should be made only in the shares or assets of companies that

do not lead contrary to the principles of Sharia activities indicated above. Typically, investments

are made in stocks in the Dow Jones Islamic Market Index.

BACKGROUND OF TAKAFUL INSURANCE

In 1985, the Supreme Council of the Muslim jurists recognized system of takaful alternative

form of insurance that meets all the rules and requirements of Sharia. The first attempts to

introduce Islamic insurance was implemented in 1970 in Egypt, Sudan and the United Arab

Emirates, in the same year, the largest financial-industrial group in Saudi Arabia, "Dalla Al

Page 14

SCOPE OF TAKAFUL IN PAKISTAN

Baraka Group» (Dallah Al Baraka Group - DAG) established the first insurance company in

Manama.

Currently, Islamic insurance companies operating in Dubai (Islamic Arab Insurance Company

since 1979), Bahrain (Islamic Insurance & Reinsurance Co), Tunisia (BEST Reinsurance), as

well as Islamic Mutual Insurance Company, established in 1994, Jordan Islamic Bank and

subdivision Al Baraka Investment & Development (ABID). In 1987, it established two insurance

and investment company ABID to provide services in accordance with the provisions of Sharia

and the promotion of investment activities of individuals, banks and corporations (Al Tawfeek

Company for Investment Funds Ltd and Al Amin Company for Securities and Investment

Funds).

Saudi Arabia is considered as pioneer in takaful industry whereas Malaysia –is considered as the

successor. It is in this country published the first (and only) Takaful Act, which defined its legal

basis, taking into account the European and Islamic law. With the development of the Islamic

financial services market develop this market and regulatory mechanisms. In 1990, Algeria has

established a Commission on Accounting and Auditing of Islamic Financial Institutions

(AAOIFI), responsible for the production of accounting, auditing and other standards for Islamic

financial institutions. Until recently, the standard of its subordinate mainly Islamic banks, but in

2005 the Bahraini financial regulator (Bahrain Monetary Agency, BMA) plans to introduce them

in the Takaful insurance and reinsurance (retakaful). In December 2002 in Kuala Lumpur

commission was established by the Islamic Financial Services (IFSB) to create a global system

of regulation of Islamic financial market. The Commission was established by central banks of

Bahrain, Saudi Arabia, Indonesia, Malaysia, Pakistan, Kuwait, Iran, Sudan and Qatar.

Page 15

SCOPE OF TAKAFUL IN PAKISTAN

Study by Takaful Insurance

Takaful is a brilliant example of a business based on supply and demand-driven customers.

Study by the International Monetary Fund (IMF) shows that Islamic economics and Islamic

banking, in particular, contribute to the equitable distribution of resources, less exposed to the

risks of illiquidity and insolvency. The growth rate of Islamic insurance in some countries is up

to 40% per year. Takaful companies are developing dynamically; offering services not only

Muslims, but also the rest of the population.

Major financial players and Takaful Insurance

Such a large insurance field causes the interest of major financial players such as Lloyd's of

London and the British bank HSBC, the introduction into the sphere of Islamic insurance and the

provision of insurance services to Muslims living in the UK (about 2 million) and the EU

(around 15 million people) . Takaful - still a young institution that is gaining popularity in the

world. While it accounts for less than 0.1% of the total global annual insurance premium.

SCOPE OF TAKAFUL IN PAKISTAN

The scope of takaful cannot be overlooked in Pakistani market, as Pakistan is a Muslim country

where people believe in the principles laid down by Holy Quran and Sunnah and according to

Quran Gharar, Maiser and Riba all these terminologies are haram in Islam. Therefore, for a

Muslim it seems to be a sin when following the conventional system of Insurance. This belief

and concept of Islam led the growth and development of Takaful insurance fly high in the

financial markets. Now international companies are also following the concept of takaful

insurance in spite of conventional insurance. The takaful insurance has been introduced in

Pakistani market in 2005. There were only two players in the market at that time but with the

Page 16

SCOPE OF TAKAFUL IN PAKISTAN

passage of time and witnessing the growth prospects most of the private and commercial banks

starts their own takaful insurance products. According to Mr. Jamil-ur-Rehman (SBP, PSD) the

scope of takaful insurance would one day eat up the share of conventional insurance because it is

free from gambling and interest. According a survey conducted by Gallop Pakistan, there are

43% people who are in favor of takaful insurance while there are 21% who have doubts and

didn’t agree that there is a difference between takaful and conventional insurance.

Although Pakistan is regarded as one of the most densely populated countries of the world,

however the share of takaful is stick to only 3 % annually the share is on increasing trend but not

with the pace as it was expected too. According Omar Mustafa Ansari, the partner of

EnYSidaatHyder, the most important thing is that it is the time we need to maintain strong base

and relationships among the people to clarify their misconceptions. Most of the people didn’t

even know completely about the methodology while others don’t even try to. In the near 2017

we would be expecting some great numbers in the industry expansion. Now London and markets

of UK are also showing their interest in Islamic insurance sector however their advent in the

market would be fruitful enough to reap the benefits.

PROBLEM STSTEMENT

“The Scope of Takaful Insurance In Pakistani Market”

SCOPE OF THE STUDY

In this research paper the scope of takaful insurance can be highlighted making Pak Qatar

Takaful Company an example. This example would lead us to finding the change and growth of

takaful industry in Pakistan. Pak Qatar takaful company is chosen for the research paper because

Page 17

SCOPE OF TAKAFUL IN PAKISTAN

it is pioneer of takaful insurance in Pakistan as well as, it has the maximum resource and

research and experience in this area.

SIGNIFICANCE OF THE STUDY

The study is important because it identifies that why and how takaful insurance is better than

conventional insurance and on the other hand, it also determines the future of takaful in Pakistani

market.

Page 18

SCOPE OF TAKAFUL IN PAKISTAN

RESEARCH METHODOLOGY– 02

Page 19

SCOPE OF TAKAFUL IN PAKISTAN

RESEARCH DESIGN

The research design for this research study “THE SCOPE OF TAKAFUL

INPAKISTAN” is ‘Exploratory”. In this research study I would be exploring some important

facts and figures through a detailed questionnaire study in order to determine the views of people

which lead to the scope of takaful industry in Pakistan.

RESEARCH OBJECTIVES

The main objective of this research is to highlight and demonstrate the scope of takaful

insurance and its role in the Pakistani industry. The main objective of this research is to put light

to the concept of Takaful and its role in the banking industry of Pakistan.

The study has following research questions to examine through analysis. The questions are:-

What is takaful insurance and why it is gaining growth in the whole world?

How Takaful Insurance can be differing through Conventional setting?

Why people go for takaful insurance?

What are the main attributes and competitive advantage’s on conventional setup

SOURCES OF DATA

The data for this research has been gathered and compiled from a number of sources.

These sources are from different authors and researchers and also include interviews and

questionnaire.

A. Primary Source

B. Secondary Source

Page 20

SCOPE OF TAKAFUL IN PAKISTAN

PRIMARY SOURCES

Interviews would be taken from the people of Pak Qatar takaful who define the takaful industry

and its scope in Pakistan in real terms. On the other hand, a questionnaire would be filled from

the respondents in order to know their perspective about the takaful insurance and their response

in Pakistan.

SECONDARY SOURCES

SydatHyder Report

SBP Pakistan Journal

Emerald

RESEARCH INSTRUMENTS

I. Questionnaire analysis

QUALITATIVE QUANTITATIVE RESEARCH

The research is both qualitative and quantitative in nature.

UNIT OF ANALYSIS

a) Pak Qatar Takaful

b) Takaful Insurance

EXTENT OF THE RESEARCHER INTERFERENCE

The researcher interference for this research is minimal.

Page 21

SCOPE OF TAKAFUL IN PAKISTAN

TIME HORIZON

The time horizon for this research is Cross-Sectional. The study is cross sectional so as to save

the cost and time as we have only 6 months to complete the thesis.

Page 22

SCOPE OF TAKAFUL IN PAKISTAN

REVIEWING LITERATURE CRITICALLY

Page 23

SCOPE OF TAKAFUL IN PAKISTAN

According to the report published by the SECP Pakistan in 2007, the analysts are of the view that

the scope of Islamic insurance is becoming brighter as the number of companies are still

increasing there are now 49 Islamic insurance companies in Pakistan.

According to the research conducted by the Muhammad Ayub, the takaful insurance is under

some misconceptions. The people are of the view that there is only one way y to strengthen the

Pakistani economy that the government should favor the Islamic products as they do it for

attracting international investments. However from the research it has also comes to the

knowledge that the Government believes on true and fair competition in the insurance therefore

giving leverage and advantages would de-motivate the other players. In his research Ayub

suggest some recommendations that the Islamic insurance companies should have to design such

policies and marketing their product in such a way that they would lead from the front and it is

not ban.

According to ZulfiqarHasan in 2011, Takaful is the most preferred insurance is the fastest

growing business models throughout the world the major share is still with the Saudi and Middle

Eastern players however it also strengthens its roots. According to Zulfiqar the Islamic insurance

is a balanced approach based on the Islamic principles acting upon which is a binding for a

Muslim.

According to Abdul Wahab in 2002, the takaful insurance is the most charming and up beating

sector of Islamic economy. In Pakistan the scope of takaful of increasing as awareness and

knowledge about religion is increasing. In his research along with the SydatHyder associates

Wahab is of the view that, there are a number of obstacles which the Islamic insurance had to

face but according to the international Reports and the industry professional the Islamic

Page 24

SCOPE OF TAKAFUL IN PAKISTAN

insurance sector in Pakistan is increasing by 16 to 20% annually. In his research Abdul wahab

has also given some recommendations to the Companies so that they can make it better.

According Omar Mustafa Ansari, the partner of EnYSidaatHyder, the most important thing is

that it is the time we need to maintain strong base and relationships among the people to clarify

their misconceptions. Most of the people didn’t even know completely about the methodology

while others don’t even try to. In the near 2017 we would be expecting some great numbers in

the industry expansion. Now London and markets of UK are also showing their interest in

Islamic insurance sector however their advent in the market would be fruitful enough to reap the

benefits.

Page 25

SCOPE OF TAKAFUL IN PAKISTAN

INTEGRATION OF DATA

Page 26

SCOPE OF TAKAFUL IN PAKISTAN

DATA ANALYSIS

The integration and analysis of data for this research is through collecting the views of

respondent’s i.e. from the questionnaire analysis. The questionnaire analysis helps us to examine

and determine the views of the selected people.

The respondents are randomly selected for this research but they are selected keeping in view

that they should be clients of even the conventional insurance or they are from the Islamic

insurance. The main aim is to analyze the scope of takaful insurance in Pakistan and this can

only be gauged through their reviews.

Page 27

SCOPE OF TAKAFUL IN PAKISTAN

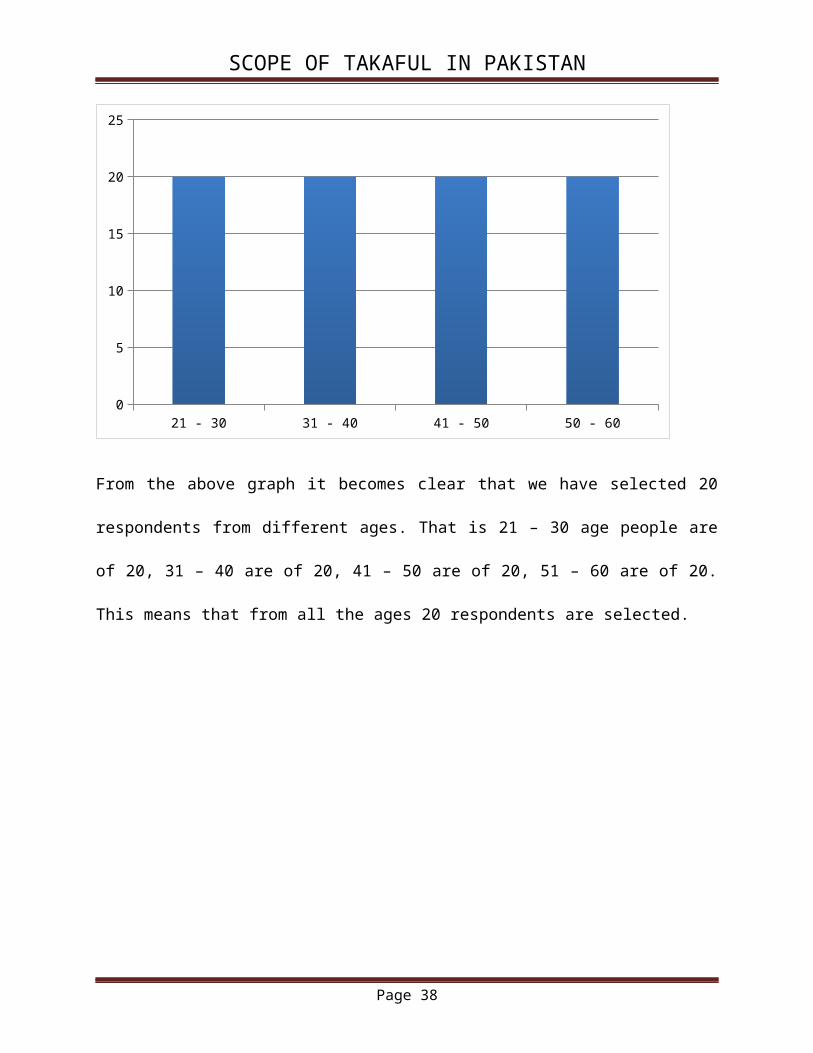

Q. What is your Age Group?

21 – 30 years

31 – 40 years

41 – 50 years

51 – 60 years\

21 - 30 31 - 40 41 - 50 50 - 600

5

10

15

20

25

From the above graph it becomes clear that we have selected 20 respondents from different ages.

That is 21 – 30 age people are of 20, 31 – 40 are of 20, 41 – 50 are of 20, 51 – 60 are of 20. This

means that from all the ages 20 respondents are selected.

Page 28

SCOPE OF TAKAFUL IN PAKISTAN

What is your Gender?

Male

Female

Male Female0

10

20

30

40

50

60

From the above graph it becomes clear that, most of the respondents for this research are Males

as they better know about the matters like insurance while on the other hand, the females

selected for this research are 29 and those 29 female respondents are working women.

Page 29

SCOPE OF TAKAFUL IN PAKISTAN

Have you ever purchase any kind of insurance?

Yes

No

Yes No0

10

20

30

40

50

60

70

80

90

From the above graph it becomes crystal clear that the respondents selected for this research

have purchase some kind of insurance in any manner that is, health insurance, Car Insurance,

Family insurance etc. for this research only those respondents are selected who have purchase

any kind of insurance in any manner. The reason of selecting these respondents is to have a

better overview based on all the respondents.

Page 30

SCOPE OF TAKAFUL IN PAKISTAN

Are you a customer of Conventional OR Islamic Insurance (Takaful)?

Conventional Or General Insurance

Takaful / Islamic Insurance.

Conventional Takaful0

10

20

30

40

50

60

From the above graph it becomes crystal clear that, the respondents are the customers of both

conventional and Islamic insurance i.e. out of 80 respondents 30 are those who are customers of

conventional insurance like (Car Insurance, Home Insurance, Business Insurance) while on the

other hand, the remaining 50 are the customers of Islamic insurance like (Islamic Ijarah, Family

Takaful etc). This means that most of the respondents are the customers of Islamic insurance this

is because the hype of Islamic banking and Islamic insurance.

What is the reason why you purchase Islamic Insurance (Takaful)?

Page 31

SCOPE OF TAKAFUL IN PAKISTAN

It is Islamic

Religious reasons

Personal Satisfaction

Others Influence

It is Islamic Religious Reasons Personal Satisfaction Other Influences 0

5

10

15

20

25

30

35

When a question regarding the reason for the usage of Islamic insurance is asked from the

respondents they have of the view that, out of 80 respondents 22 are of the view that they have

selected the takaful model because it is Islamic, 16 are of the view that they are using it because

of religious reasons while 30 respondents when asked said that, it is because they are personally

satisfied with the Islamic insurance on the other hand, 15 are of the view that, they have chosen

takaful because others (Family and friends) ask them to choose it.

Page 32

SCOPE OF TAKAFUL IN PAKISTAN

Are you a prior customer of Conventional Insurance?

Yes

No

Yes No0

10

20

30

40

50

60

When respondents are asked about their prior experience with the conventional type of insurance

they are of the view that, out of 80 respondents 51 are of the view that they were priory the

customers of conventional insurance while on the other hand, 29 are of the view they didn’t have

prior experience of Insurance. This means that, most of the customer has prior experience of

insurance and they can better differentiate in the service.

Page 33

SCOPE OF TAKAFUL IN PAKISTAN

Q. Did you find any Difference in Islamic and Conventional Insurance?

Yes, they are Different

No, they are Same

Yes, They Are Different No, They are Same0

10

20

30

40

50

60

When respondents are asked about their views on the question that what they feel about Islamic

and conventional insurance is there any difference. Out of 80 respondents 52 are of the view that

yes, both of them are different with distinctive ideas and separate origins. However, there are 28

out of those 80 who are of the view that they are both the same without any significant difference

is to put a tag of being Islamic and earn the same interest in the name of Rent. This concludes

that most of the respondents are of the view that, Islamic concept of insurance is different from

the conventional insurance.

Page 34

SCOPE OF TAKAFUL IN PAKISTAN

Q. What do you think in Pakistan the companies are implementing the proper model of Takaful

or not?

SCALE1 2 3 4 5

Strongly Disagree

Disagree Neither/Neutral

Agree Strongly Agree

1 Properly Implementing the model 11 15 10 16 27

2 Somewhat Implementing

From the above scale table it becomes clear that how respondents and customers of insurance

companies feels and views about the implementation of the basic model upon which the Islamic

insurance is based. Most of the respondents are of the view that the insurance companies are

implementing the full fledge model of takaful. While some of them i.e. 15 shows disagreement

and 11 are Strongly Disagree. On the other hand, it comes also into consideration that some of

the respondents didn’t have proper understanding of the model.

Page 35

SCOPE OF TAKAFUL IN PAKISTAN

Q. Rate the following?

SCALE1 2 3 4 5

Strongly Disagree

Disagree Neither/Neutral

Agree Strongly Agree

1 Takaful is free from element of gharar (uncertainty), riba (interest) and Maysir (gambling)

7 4 9 15 35

2 The refusal of uncertainty, gambling and usury elements differentiate Takaful from the conventional insurance

4 9 2 15 40

Page 36

SCOPE OF TAKAFUL IN PAKISTAN

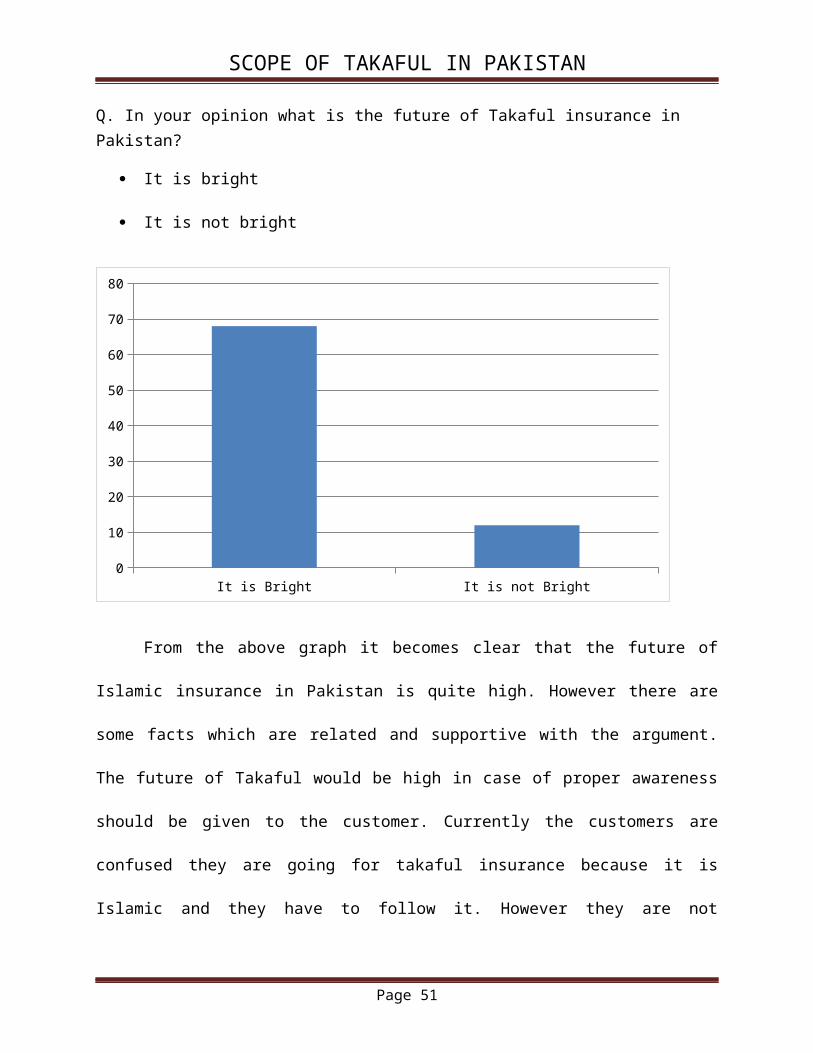

Q. In your opinion what is the future of Takaful insurance in Pakistan?

It is bright

It is not bright

It is Bright It is not Bright0

10

20

30

40

50

60

70

80

From the above graph it becomes clear that the future of Islamic insurance in Pakistan is

quite high. However there are some facts which are related and supportive with the argument.

The future of Takaful would be high in case of proper awareness should be given to the

customer. Currently the customers are confused they are going for takaful insurance because it is

Islamic and they have to follow it. However they are not following the Islamic insurance

according to their own will and choice.

Page 37

SCOPE OF TAKAFUL IN PAKISTAN

Q. Is government of Pakistan Supporting or giving some benefits or advantage on Islamic

insurance?

Yes

No

Yes No0

10

20

30

40

50

60

70

80

When respondents are asked that if the government of Pakistan is giving any kind of

favor or relaxation for choosing the Islamic insurance, the respondents are of the view that no the

government is not giving any kind of advantage. Out of 80 responds only 12 are of the view that

yes the government is giving them some advantage while on the other hand, 62 out of 80

respondents are of the view that the government of Pakistan is not giving any kind of advantage

and favor to them even in taxes.

Page 38

SCOPE OF TAKAFUL IN PAKISTAN

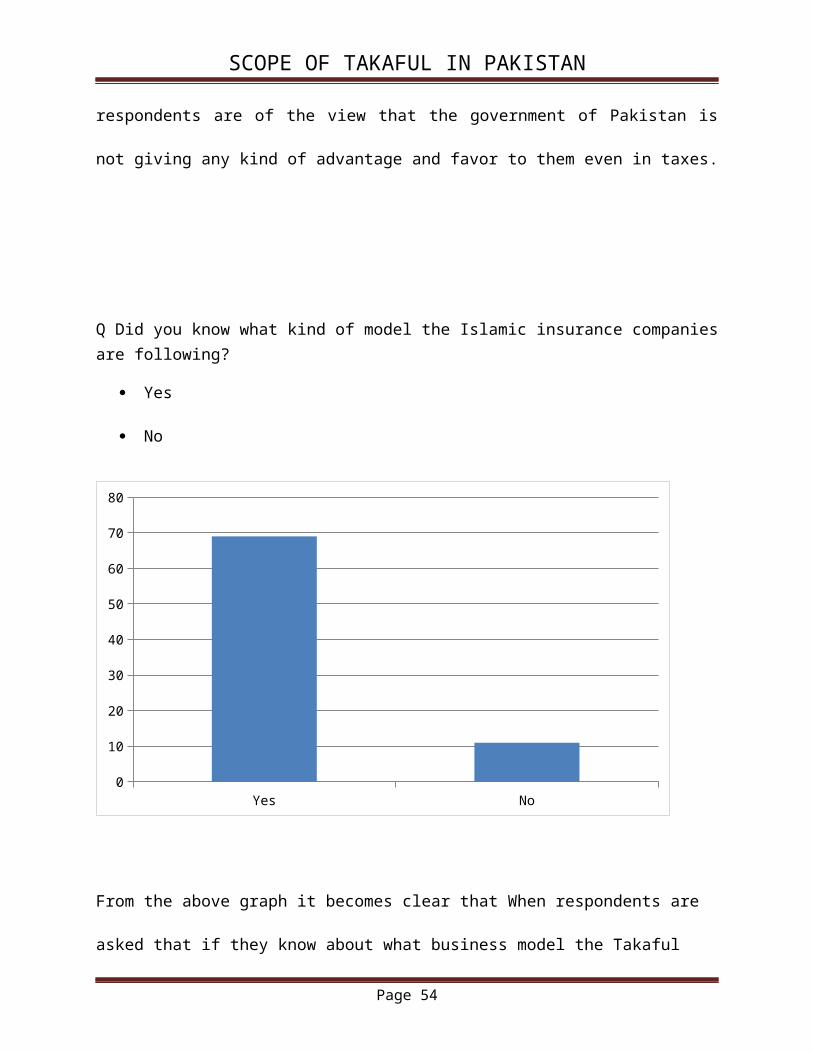

Q Did you know what kind of model the Islamic insurance companies are following?

Yes

No

Yes No0

10

20

30

40

50

60

70

80

From the above graph it becomes clear that When respondents are asked that if they know about

what business model the Takaful companies are following then out of 80 respondents 69 were of

the view that they dint have any idea and the company didn’t even mention them this. On the

other hand, only 11 are of the view that they know which model the company is following for

this business. This means that most of the people who are even clients have any kind of

knowledge about the model

Page 39

SCOPE OF TAKAFUL IN PAKISTAN

Q. What is the main point which a takaful company needs to enhance the scope of Islamic

insurance?

Awareness Sessions

Leverages and discount Offers

Market the Islamic Factor

Contract Directly with Banks

Awareness Sessions Leverages Market Islamic Factor Contract Directly With Banks

0

5

10

15

20

25

30

When respondents are asked that how the takaful insurance would tend to grow in the Pakistani

environment. They were of the view that the scope of takaful insurance is quite higher in

Pakistani market. The market capitalization is also big and these companies need to adopt certain

measures to lead the market. Out of 80 respondents, 27 are of the view that through awareness

sessions that can be developed because people are not aware of the facts about the Islamic

insurance however 20 are of the view that, they should market the Islamic factor in it

Page 40

SCOPE OF TAKAFUL IN PAKISTAN

Q. what is the major product which is frequently used by you?

Marine Insurance

Motor vehicle Insurance

Home Insurance

Health Insurance

Business Insurance

Marine Auto Home Helath Home Business0

5

10

15

20

25

When Respondents are asked about what kind of insurance product they would use frequently

they were of the view that, 80% of the people use Auto Insurance and Business Insurance

products. While for the business purpose most of them are insured as marine insurance. This

concludes that in Pakistan two major products are used i.e. Business insurance and Auto

Insurance. From the respondents reviews it comes to knowledge that, people use these insurance

because of burglary and dacoits.

Page 41

SCOPE OF TAKAFUL IN PAKISTAN

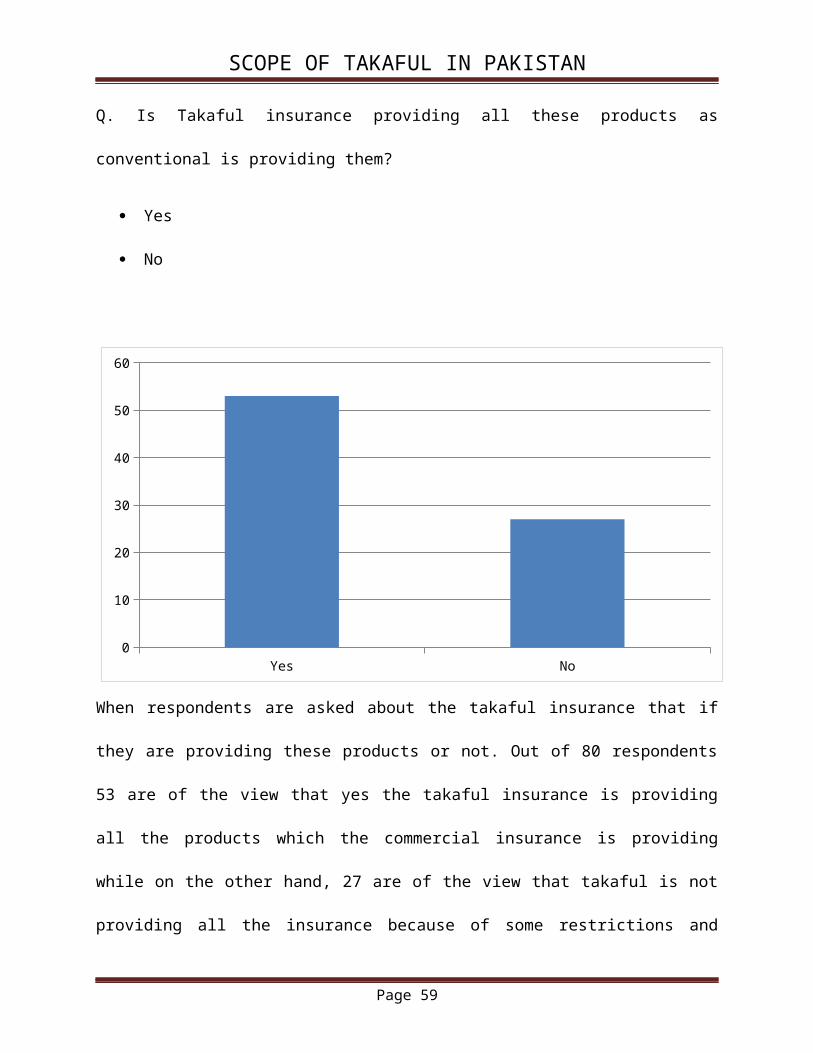

Q. Is Takaful insurance providing all these products as conventional is providing them?

Yes

No

When respondents are asked about the takaful insurance that if they are providing these products

or not. Out of 80 respondents 53 are of the view that yes the takaful insurance is providing all the

products which the commercial insurance is providing while on the other hand, 27 are of the

view that takaful is not providing all the insurance because of some restrictions and because they

are also new in the market. The people who are saying that takaful is not providing the insurance

are of the view that it takes time for takaful insurance to change the belief of a common man

because most of the people think that they are the same.

Page 42

Yes No0

10

20

30

40

50

60

SCOPE OF TAKAFUL IN PAKISTAN

Page 43

SCOPE OF TAKAFUL IN PAKISTAN

INTERNATIONAL TAKAFUL INDUSTRY AND ITS INCREASING SCOPE

From the current estimates it has been come to the knowledge that the current takaful

industry reaches up to US$11b in 2012 (from US$9.4b in 2011). However the contribution in

these increasing trends includes Saudi Arabia with the highest 51% share. However in some

parts of the world the scope of takaful is connected with the awareness among people and the

growth rate remains in between 13% to 16% annually. The potential of growth in these countries

are higher but some strategic kind of activities needs to be done on priority basis so as to boost

up the ratio.

Page 44

SCOPE OF TAKAFUL IN PAKISTAN

Figure 1 Country Wise Growth Chart

The Main Business Centers of Takaful INSURANCE

Their business centers are basically the countries in which we are analyzing the growing trend of

takaful insurance. One of the main reason for faster growth in these countries is that they have

proper awareness sessions or mostly they are densely populated Muslim world with Strong

Governments.

Page 45

SCOPE OF TAKAFUL IN PAKISTAN

The above picture shows the growing trend of takaful in different parts of the world. Saudi

Arabia being the center of Islam and practices is on the highest trend. The GCC countries include

North African countries.

FINANCIAL PERFORMANCE OF TAKAFUL COMPANIES IN PAKISTAN

2010 2011 2012

CLAIMS RATIO 63 50 48

CUSTOMER BASE 14 27 49

Page 46

SCOPE OF TAKAFUL IN PAKISTAN

EXPENSE RATIO 38 23 21

ROE 1.2 5 14

Figure 2: Financial performance of takaful companies 2010 – 2012at a glace report

The above Financials shows that the takaful companies are on a better and increasing

trend in Pakistan. According to Jaweriyia Ahsan (Assistant Director, Pak Qatar Takaful) the

takaful industry is in the developing phase in Pakistan and we are the biggest institution to lead

from the front. It is still a long way to go and we are working on the new and innovated Islamic

products. Our customer base is increasing day and day and globally. In order to boost up the ratio

of takaful insurance the company has already designed a phase wise plan. The company is also

focusing on the future marks i.e. enhancing the Motor Vehicle and Marine insurance plans so

that we can make it better.

Page 47

SCOPE OF TAKAFUL IN PAKISTAN

CRITICAL DEBATE

Page 48

SCOPE OF TAKAFUL IN PAKISTAN

CONCLUSION

The takaful industry has now become one of the leading and most emerging Islamic economic

and financial segments of the economy. it is not only recognized in Pakistan but its recognitions

was also remarked by international financial institutions, Stock Markets and economies. The

main aim of Islamic insurance is to maintain a balance in the economy and treat it in an Islamic

manner which is free from the elements of gharar, Interest and gambling. The Islamic insurance

is based on the principles of Sharia. The trend of Islamic insurance is growing in rapid manner

and this is the sign of change in the economy and in the minds and perception of people.

The main aim of this research paper is to analyze the scope of Islamic insurance in the Pakistani

market. In Pakistan the insurance sector is divided into Private as well as public companies, in

private there are 50 companies while in public there are 4 companies operating with maximum

market share. However Islamic insurance begin to start their operations with a tough competition

but being Islamic is one of the most contrasting and competitive edge for them. Islamic insurance

has defined its own business model totally based upon the Islamic practices of sharia.

In this research paper the scope of Takaful insurance in Pakistan is analyzed with the help of

interviews and questionnaire floated among the general public who are clients and customers of

conventional and non-conventional insurance. The main aim is to analyze the perception of the

people because it is the perception which becomes the final decision. However we have

witnessed that people are quite satisfied from the Islamic insurance and welcomes the growth of

takaful in Pakistan.

Page 49

SCOPE OF TAKAFUL IN PAKISTAN

From the research it has also been concluded that the future of Islamic insurance in Pakistan is

brighter but there are some obstacles and misconceptions. This can be eliminated with the help of

continuous awareness sessions and defining the real aim of takaful for the public. Still the people

who prefer Takaful over conventional didn’t even know the difference between the two. The

companies need to consider a number of factors keeping in view the Pakistani culture and

environment which has now become a mixture of western and eastern values.

Important Findings from the Research

According to the statisticsof 2008 published in the report of SydatHyder Associates

Pakistanindicated the insurance market premium is of Rs. 12.5 billion with the operation of 40

companies.

a) Population Base:

The Population of Pakistan is approximately reached up to 18 billion and around 95% of the

population is Muslim. Muslims are those who practice the things as defined by their religion.

Interest and Gambling which is the basic elements of conventional insurance is totally forbidden

in Islam therefore, keeping in view this factor the takaful companies could brand their name as

Islamic and market them as much as they can to beat the local market.

b) Industry Base

Currently the insurance industry of Pakistan is totally dependent upon the conventional

insurance companies as they are greater in numbers, have professional employees even the

Government of Pakistan which is Islamic republic of Pakistan is following the conventional

setup. This means that the major share of the market is under the control of these conventional

players.

Page 50

SCOPE OF TAKAFUL IN PAKISTAN

c) Misconceptions

From the research it has been analyzed that a number of people have misconceptions about

the Islamic insurance they are mostly of the view that there is no difference among the one

another both of them are same the only different is they call it interest and Islamic called it rent.

This misconception among the people is the major obstacle among the growth of Islamic

insurance in Pakistan however, still the people believe on the Fatwa and are opting the Islamic

insurance because of being Islamic and interest free.

d) Preferences

People now prefer the Islamic insurance because of the fact that it is Islamic and they are of

the view that they have selected the right choice as said by the religion and sharia. Still the

Islamic insurance market is in the growing phase in Pakistan because they are lack with the

professionals.

e) Major Business Products

The people of Pakistan mostly used three main insurance products: Vehicle insurance, Home

insurance and business insurance. These products are widely in Pakistan especially the Motor

vehicle insurance however the major market share in this sector is with banks and local

conventional insurance companies because they have direct linked and contracted with the banks

and companies.

f) Industry Professionals

One of the major facts which also become the factor for the future growth of takaful in

Pakistan is the professional experts. From the research we have analyzed the fact that there is

still a shortage of the industry professionals in takaful insurance. On the other hand, in the

Page 51

SCOPE OF TAKAFUL IN PAKISTAN

conventional setup there are a number of professionals and policy makers who define and design

such a policy so that their market share is still on the higher side.

g) Government Advantage and Leverage

From the research it has come to the knowledge that the government of Pakistan is not giving

and offering any kind of advantage to the Islamic insurance clients. This is the need of the hour

and the government should focus on this. However in countries where the Islamic insurance is on

its boom like Saudi countries the Government of Pakistan has strict bans on Conventional

insurance however in some parts of UK and Middle East the local government is offering some

leverages in taxes and they are giving other benefits too.

The people are of the view that there is only one way y to strengthen the Pakistani economy

that the government should favor the Islamic products as they do it for attracting international

investments. However from the research it has also comes to the knowledge that the Government

believes on true and fair competition in the insurance therefore giving leverage and advantages

would de-motivate the other players. The Islamic insurance companies should have to design

such policies and marketing their product in such a way that they would lead from the front and

it is not ban.

h) Islamic Insurance Business Model

The research also clarifies that the business model which is followed b the Islamic insurance

companies is unique but not known by the clients.

Page 52

SCOPE OF TAKAFUL IN PAKISTAN

Page 53

SCOPE OF TAKAFUL IN PAKISTAN

RECOMMENDATIONS

Based on the above research insights some of the important recommendation which in

my opinion becomes the growth prospect of the future of Islamic insurance companies is as

follows:

1. The population of Pakistan is increasing and hence the consumer base is also increasing.

The people of Pakistan have now become more conscious about the insurance and

mitigating the risk however there is still a huge market to go on with. The Islamic

insurance companies

2. The insurance companies hold has to initiate awareness sessions free phase wise. In the

initial phase they have t to train the people of banking institutions so that they can guide

the pubic in a better way while on the other hand, in the second phase they have to come

to public and inaugurate public awareness sessions in which they market the Islamic

point of view.

3. The Islamic insurance companies would have to clarify the misconceptions regarding the

Islamic insurance and their match with the conventional ones.

4. The Government of Pakistan would have to focus on implementing the Islamic insurance

however if they didn’t do it, just give some benefit to the users of Islamic insurance.

Being an Islamic Republic of Pakistan the country Government should have to focus on

it.

5. Strategic collaboration with the Saudi companies and other Middle Eastern companies

should be strengthen and develop with a view to have more groomed product.

Page 54

SCOPE OF TAKAFUL IN PAKISTAN

6. The major sectors of insurance sector growth are Automobile sector, Business insurance

and home insurance sector. The Islamic insurance companies should have to focus on this

avenue to groom up this opportunity.

7. Regulatory framework for the policy should be made and policies are designed in such a

way that the new customers would feel some flexibility.

Page 55

SCOPE OF TAKAFUL IN PAKISTAN

References

Anwar, M., & Hussain, M. (1994). Comparative Study of Insurance and" Takafol"(Islamic

Insurance)[with Comments]. The Pakistan Development Review, 33(4), 1315-1330.

Bekkin, R. I. (2007). Islamic insurance: National features and legal regulation. Arab Law

Quarterly, 21(1), 3-34.

Bhatty, A. (2005). The growing importance of Takaful insurance.In Asia Regional Seminar

organized by OECD and Bank Negara Malaysia under the sponsorship of the

government of] apan (pp. 23-24).

Bhatty, Ajmal, "Takaful Industry: Global Profile and Trends, 2001" , New Horizon, Institute of

Islamic Banking & Insurance, London, April 2001

Data Retrieved From http://www.kantakji.com/fiqh/Files/Insurance/DiffbwConvIns.pdfDated,

08th December, 2013

Data Retrieved From http://www.sbp.org.pk/departments/ibd/Takaful.pdf Dated, 08th December,

2013

Dr. M.M. Billah, "Life Insurance-an Islamic View". Arab Quartely, Vol. 8 part 4. 1993 Institute

of Islamic Banking and Insurance, Directory of Takaful Companies 2000, London

Fisher, Omar, "Growth of Islamic Finance and Scope for Retakaful", speech International

Takaful Conference, KL Malaysia, June 2000.

Page 56

SCOPE OF TAKAFUL IN PAKISTAN

Kader, H. A., Adams, M., & Hardwick, P. (2010).The Cost Efficiency of Takaful Insurance

Companies&ast. The Geneva Papers on Risk and Insurance-Issues and Practice, 35(1),

161-181.

Khorshid, A. (2013). Islamic insurance: a modern approach to Islamic banking. Routledge.

Mankabady, S. (1989). Insurance and Islamic Law: The Islamic Insurance Company. Arab Law

Quarterly, 4(3), 199-205.

Maysami, R. C., & Williams, J. J. (2006).Evidence on the relationship between Takaful

insurance and fundamental perception of Islamic principles.Applied Financial Economics

Letters, 2(4), 229-232.

Taylor, Dawood, "Developing Takaful Taawuni in Saudi Arabia" speech International Takaful

Conference, KL. Malaysia, June 2000

Wahab, A. R. A., Lewis, M. K., & Hassan, M. K. (2007). Islamic takaful: Business models,

Shariah concerns, and proposed solutions. Thunderbird International Business

Review, 49(3), 371-396.

Page 57

SCOPE OF TAKAFUL IN PAKISTAN

APPENDIX

OBSTACLES in Takaful

Legal (Takaful Rules / Shariah Board) Aspects

1. As per the Insurance Ordinance 2000, “Takaful” means a scheme based on mutual

assistance in compliance with the provisions of Islamic shariah, and which provides for

mutual financial aid and assistance to the participants in case of occurrence of certain

contingencies and whereby the participants mutually agree to contribute to the common

fund for that purpose.

2. There are at these stage legal obstacles in the establishment of a takaful operator. Takaful

Rules need to be developed so that a takaful operator can be given permission to operate

under the guidelines of those rules.

3. There would also be a need to have a central Shariah Advisory Board with which SECP

would need to take approval/advice prior to approval of products and other

documentation filed by insurance companies.

Consumer Mindset

Consumer’s mindset has become such that they have the tendency to try to recover the

premium that they have paid to an insurance company. A number of malpractices have crept into

the system because of this mindset. Changing this mindset can become a major challenge for a

takaful operator. It would need to ensure that like the conventional system, compromises do not

creep into the system due to pressures from clients. It may be important for a takaful operator to

avoid insuring such consumers as they can affect the credibility of the takaful system and ensure

that operational controls are not compromised.

Page 58

SCOPE OF TAKAFUL IN PAKISTAN

TAKAFUL BUSINESS MODELS

Presently different takaful models are prevalent in different countries. The basic models

being two i.e. Mudaraba based (Malaysian Model) and Wakalah Model (Middle Eastern

model). However there are a number of finer issues and combinations of models that

exist in practice which have been discussed briefly in Annex 1.

Discussions with scholars in the country show a clear preference for the Wakalah model

due to less serious Shariah related concerns with this approach as opposed to the

Modaraba model where scholars have a number of serious concerns. A refinement of the

Wakalah model has also been made which is called Wakalah with WAQF Fund that has

been evolved by DaroolUloom, Karachi. I had the opportunity of assisting in this process

and a model has taken shape which still needs to be discussed on a larger platform before

it can be considered as being ready for implementation by Takaful operators.

The general perception also is that people would be more comfortable with the approach

acceptable to Middle Eastern Shariah scholars compared to the Malaysian approach

which is generally considered as more liberal even in Islamic banking.

A final consensus needs to be developed and decision taken on the model that we wish to

adopt for Pakistan. It is hoped that urgent discussions take place on the model issue and

consultations are done with Shariah scholars from other countries to arrive at a consensus

approach. A central Shariah Board would also be required to advice SECP on the

approval of specific products that would later be submitted to SECP by different

companies.

Once a consensus has been reached, it is equally important to emphasize that the Takaful

Rules should specify the specific model to be adopted to avoid confusing the public at

large with different models and further different variations of models being adopted by

different companies. The Rules may however allow for some flexibility in certain aspects

which may be left to the Individual Shariah Boards. This step would go a long way in

ensuring public faith and acceptability of the takaful system and avoid creating confusion

and interpretations of different models.

Page 59

SCOPE OF TAKAFUL IN PAKISTAN

In conclusion, Islamic Finance and Islamic Takaful are ethical financing and cooperative risk

protection methods that are superior alternatives precisely because they reinvigorate human

capital, emphasize personal dignity, community self-help, and economic self-

development..generating manifold benefits for all participants. Islam is an integrated way of life.

Thus, interest-free financing and Takaful are mutually reinforcing systems that promote at once

economic efficiency, communal risk-sharing and individual rewards through self-purification. In

as much as the Takaful system resolves around active participation by members of the

community, it is imperative that public awareness be enhanced. As Muslims and non-Muslims

alike come to understand the real benefits of Takaful and cooperative risk sharing, the evolution

of the Takaful industry will accelerate making the projections described herein overly

conservative.

Page 60