Portfolio Tutorial

119

FACULTY OF ENGINEERING AND SCIENCE UKFF3283 PORTFOLIO MANAGEMENT == Tutorial 1 == 1. Objective: This unit aims to present the issues and strategies needed to function in complex global markets. This includes the investment terms and concepts as well as being able to understand and apply many of the techniques used in analyzing and managing investments. It aims at understanding the steps necessary to group different financial assets into a portfolio to solve the asset allocation problem faced by investors, and portfolio performance evaluation. 2. Learning Outcomes: Topic Learning outcomes Content Topic 1: Introduction to investing Explain the principles of investment and differentiate the different types of investments. Explain the transactions in money markets and capital markets. Describe the investment process and types of investors. Explain the investment process and types of investors. Explain the steps in investing, investing Investments and the investment process Investment vehicles Making investment plans Meeting liquidity needs: Investing in short tem vehicles - 1 -

Transcript of Portfolio Tutorial

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 1 ==

1. Objective:

This unit aims to present the issues and strategies needed to function in complex global markets. This includes the investment terms and concepts as well as being able to understand and apply many of the techniques used in analyzing and managing investments. It aims at understanding the steps necessary to group different financial assets into a portfolio to solve the asset allocation problem faced by investors, and portfolio performance evaluation.

2. Learning Outcomes:

Topic Learning outcomes Content Topic 1: Introduction to investing

Explain the principles of investment and differentiate the different types of investments.

Explain the transactions in money markets and capital markets.

Describe the investment process and types of investors.

Explain the investment process and types of investors.

Explain the steps in investing, investing over the life cycle and in different economic environments.

Investments and the investment process

Investment vehicles

Making investment plans

Meeting liquidity needs: Investing in short tem vehicles

Topic 2: Trading of Securities: - Market and transactions- Investment information and securities transaction

Differentiate the transactions in money markets and capital markets.

Explain the general conditions of securities markets.

Explain long purchases, margin transaction, and short sales.

Identify major types and sources of traditional and online investment information.

Securities markets

Globalization of securities markets

Trading hours and regulation of securities markets

Basic types of securities transactions

Online investing

- 1 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Explain the key aspects of the commonly cited stock and bond market averages and indexes.

Describe the basic types of orders, online transactions, transaction costs, and legal aspects of investor protection.

Types and sources of investment information.

Understanding market averages and indexes

Making securities transactions

Investment advisers and investment clubs

Topic 3: Return and Risks: - Introduction to Financial calculators

Measure and analyze risk and return of single asset and portfolio using financial calculators and interest factor tables.

Explain the forces that affect the level of return, and historical returns.

Explain the key sources that affect potential investment vehicles.

The concept of return

The time value of money

Measuring return

Risk: The other side of the coin

Interest: The basic Return to Savers

Computational aids for use in time value calculations

Future value Present value

Topic 4: Modern Portfolio Concepts

Explain portfolio objectives and the procedures used to calculate portfolio return and standard deviation.

Measure and analyze risk and return of portfolios.

Explain the concepts of correlation and diversification.

Explain and measure required rate of return using capital asset pricing model.

Compare traditional portfolio management with modern portfolio theory.

Principles of portfolio planning

The Capital Asset Pricing Model (CAPM)

Traditional versus modern portfolio management

Constructing a portfolio using asset allocation scheme

- 2 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Explain; measure and analyze portfolio betas and the risk-return tradeoff.

Topic 5: Mutual Fund: Professionally Managed Portfolios

Explain the basic features of mutual funds and how diversification and professional management are the cornerstones of the industry.

Explain and differentiate the types of funds available and the variety of investment objectives these funds seek to fulfill.

Analyze the factors to consider when assessing and selecting funds for investment purposes.

Explain the sources of return and compute the rate of return earned on a mutual fund investment.

The mutual fund concept and phenomenon

Types of funds and services

Investing in mutual funds

Investment company performance

Topic 6: Managing Your Own Portfolio

Explain how the economic, industry and company factors affect investment decisions.

Develop a procedure for building a portfolio using an asset allocation scheme.

Explain the ways to use an asset allocation scheme to construct a portfolio consistent with investor objectives.

Analyze the investment performance using data and indexes.

Analyze the portfolio’s performance using risk-adjusted measures.

Explain the role and logic of dollar-cost averaging, constant-dollar plans, constant-ratio plans, and variable-constant plans.

Constructing a portfolio using an asset allocation scheme

Portfolio planning in action

Evaluating the performance of individual investments

Assessing portfolio performance

Timing transactions

- 3 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Topic 7: Investing Common Stock

Explain the basic features of common stocks.

Differentiate the different kinds of common stock values.

Explain common stock dividends; differentiate types of dividends and dividends reinvestment plans.

Compare and contrast various types of common stocks.

Analyze and apply the theories surrounding investment, and be able to make investment decisions.

Explain the security analysis. Ensure financial ratios to

gauge the financial vitality of a company.

What stocks have to offer?

Basic characteristics of common stock

Common stock dividends

Types and uses of common stock

Analyzing and managing common stocks

Security analysis

Economic analysis

Industry analysis

Fundamental analysis

Topic 8: Stock valuation

Explain the role that a company’s future plays in the stock valuation process and use various models to value equity instruments.

Develop a forecast of a stock’s expected cash flow, starting with corporate sales and earnings, and then moving to expected dividends and share price.

Explain and apply the concepts of intrinsic value and required return.

Differentiate and measure the underlying value of a stock using the zero-growth, constant-growth and variable-growth dividend valuation models.

Differentiate and measure the intrinsic value of a stock using present-value based models and price-relative procedures.

Analyze and apply the

Valuation: Obtaining a standard of performance

Preferred Stock valuation models

Common Stock valuation models

- 4 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

theories surrounding investment, and be able to make investment decisions.

Topic 9: Technical Analysis, Market Efficiency and Behavioral Finance

Analyze and apply the theories surrounding investment, and be able to make investment decisions.

Explain and analyze the technical condition of the market using technical analysis.

Explain the random walks and efficient markets.

Differentiate efficient market hypothesis and market anomalies.

Explain how the psychological factors can affect investors’ decision and challenge the concept of market efficiency.

Technical analysis

Random walks and efficient markets

Behavioral finance: A challenge to the efficient market hypothesis

Topic 10: Fixed Income Securities

Explain the investment attributes of bonds and their use as investment vehicles.

Describe the essential features of a bond and the roles of bond ratings.

Analyze components of bond returns and types of risk to which bond investors are exposed, and use various models to value debt instruments.

Explain how bonds are priced in the market and analyze the volatility of bonds.

Differentiate the types of bonds and kinds of investment objectives these securities can fulfill.

Why invest in bonds?

Essential features of a bond

The market for debt securities

Convertible securities

Trading bonds

Topic 11: Bond Valuation

Explain the behavior of market interest rates, and

The behavior of market

- 5 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

identify the forces that cause interest rate to change.

Describe the term structure of interest rates, and how yield curves can be used by investors.

Analyze components of bond returns and types of risk to which bond investors are exposed, and use various models to value debt instruments.

Calculate and analyze value of bonds in the market place.

Explain and measure yield and return of bonds.

Explain the concepts of duration and various bond investment strategies.

interest rates The pricing of

bonds Measures of

yield and return Duration and

immunization Bond

investment strategies

Analysis and management of bonds

Topic 12: Options: Puts and Calls

Explain the investment attributes of options (puts and calls) and their use as investment vehicles.

Analyze the risk and return behavior of various put and call investment strategies.

Explain and measure the profit potential of puts and calls from option holders and writers perspectives.

Explain the ways to use options as a strategy for enhancing investment returns.

Put and call options

Options pricing and trading

Stock index and other types of options

Warrants An investor’s

perspective on puts and calls

Topic 13: Commodities and Financial Futures

Explain the investment attributes of futures and their use as investment vehicles.

Explain the role that hedgers and speculators play in the futures market.

Differentiate commodity and financial futures.

Discuss the trading techniques that can be used with financial and commodity

The futures market

The mechanics of trading

Commodities Financial futures

- 6 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

futures.

3. Reading List

Main Text Book:1. Smart, S.B., Gitman, L.J. & Joehnk, M.D. (2014). Fundamentals of Investing.

(12th ed.). U.S.A: Pearson/Prentice Hall.

Supplementary Reading:1. Bodie, Z., Kane, A., Marcus, A. & Jain, R. (2014). Investments AGE (Asia Global

Edition). Singapore: McGraw Hill/Irwin.

2. Jones, C.P. (2013). Investments: Principles and Concepts. (12th ed.). Singapore: John Wiley & Sons.

3. Reilly, F.K. & Brown, K.C. (2012). Analysis of Investments & Management of Portfolios (10th ed.). Canada: South-Western/Cengage Learning.

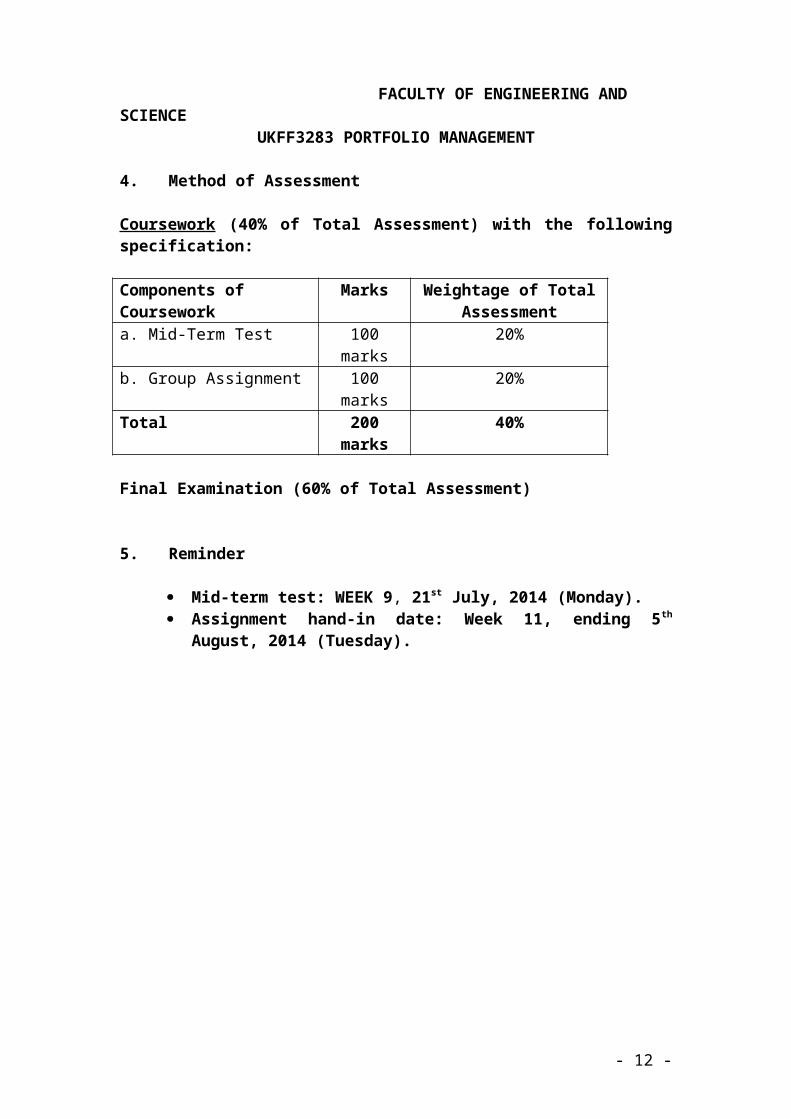

4. Method of Assessment

Coursework (40% of Total Assessment) with the following specification:

Components of Coursework

Marks Weightage of Total Assessment

a. Mid-Term Test 100 marks 20%b. Group Assignment 100 marks 20%Total 200 marks 40%

Final Examination (60% of Total Assessment)

5. Reminder

Mid-term test: WEEK 9, 21st July, 2014 (Monday). Assignment hand-in date: Week 11, ending 5th August, 2014

(Tuesday).

- 7 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 2 (Topic 1) ==

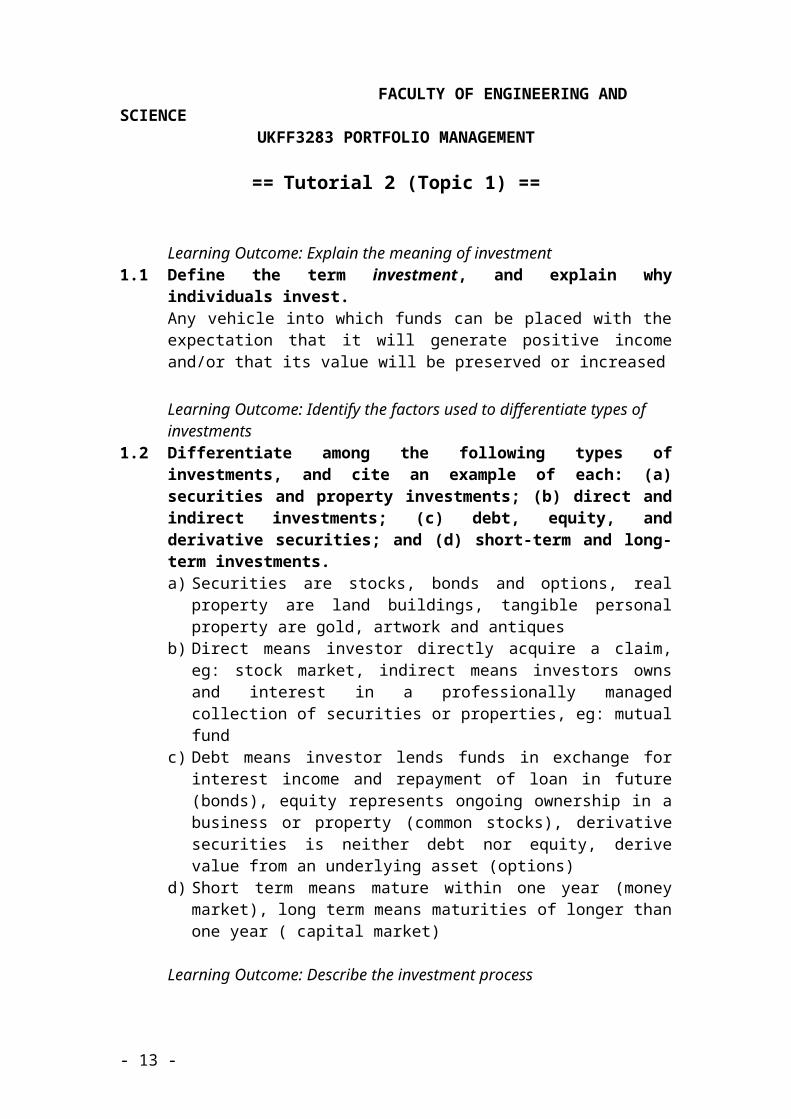

Learning Outcome: Explain the meaning of investment1.1 Define the term investment, and explain why individuals invest.

Any vehicle into which funds can be placed with the expectation that it will generate positive income and/or that its value will be preserved or increased

Learning Outcome: Identify the factors used to differentiate types of investments

1.2 Differentiate among the following types of investments, and cite an example of each: (a) securities and property investments; (b) direct and indirect investments; (c) debt, equity, and derivative securities; and (d) short-term and long-term investments.a) Securities are stocks, bonds and options, real property are land buildings,

tangible personal property are gold, artwork and antiquesb) Direct means investor directly acquire a claim, eg: stock market, indirect

means investors owns and interest in a professionally managed collection of securities or properties, eg: mutual fund

c) Debt means investor lends funds in exchange for interest income and repayment of loan in future (bonds), equity represents ongoing ownership in a business or property (common stocks), derivative securities is neither debt nor equity, derive value from an underlying asset (options)

d) Short term means mature within one year (money market), long term means maturities of longer than one year ( capital market)

Learning Outcome: Describe the investment process1.5 Describe the structure of the overall investment process. Explain the role

played by financial institutions and financial markets. Suppliers of funds (individuals) deposit money to financial market and financial institution and the money is then borrowed to demanders of funds (government, business)

Learning Outcome: Describe types of investors1.6 Classify the role of (a) government, (b) business, and (c) individuals as net

suppliers or net demanders of funds.a) Demanders of funds, federal, state and local projects & operationsb) Demanders of funds, investments in production of goods and servicesc) Suppliers of funds, some need for loans

Learning Outcome: Describe types of investors1.7 Differentiate between individual investors and institutional investors.

Individual investors: invest for personal finance goalInstitutional investors: paid to manage other people’s money, trade large volume of securities, include banks, life insurance companies, mutual funds and pension funds

Learning Outcome: Describe the steps in investing

- 8 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

1.11 What should an investor first establish before developing and executing an investment program? Briefly describe each of the seven steps involved in investing.1) Meeting Investment prerequisites2) Establishing investment goals3) Adopting an investment plan4) Evaluating investment vehicles5) Selecting suitable investments6) Constructing a diversified portfolio7) Managing the portfolio

Learning Outcome: Describe the steps in investing1.12 What are four common investment goals?

1) accumulating retirement funds2) enhancing current income3) Saving for major expenditures4) Sheltering income from taxes

Learning Outcome: Discuss investing over the life cycle1.14 Describe the differing investment philosophies typically applied during

each of the following stages of an investor’s life cycle.a) Youth (ages 20 to 45)

Growth-oriented investment, higher potential growth; higher potential risk, stress capital gains over current income. Common stocks, options or futures

b) Middle age (ages 45 to 60)Family demands & responsibilities become important (edu expenses, retirement savings), move towards less risky investments to preserve capital, transition to higher-quality securities with lower risk. Low-risk growth and income stocks, preferred stocks, convertible stocks, high grade bonds

c) Retirement years (age 60 on)Preservation of capital becomes primary goal, highly conservative investment portfolio, current income needed to supplement retirement income. Low-risk income stocks and mutual funds, government bonds, quality corporate bonds, bank certificates of deposit

Learning Outcome: Identify the short-term investment vehicles1.16 What makes an asset liquid? Why hold liquid assets? Would 100 shares of

IBM stock be considered a liquid investment? Explain.The ability of the asset to be converted into cash quickly with little or no loss in value. For emergency cash reserve or to save for a specific short-term financial goal. No, because it might take time to be sold on the stock market and its value is not stable, depending on market

- 9 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Discuss investing over the life cycleQ1.1 Assume that you are 35 years old, are married with two young children,

are renting a condo, and have an annual income of $90,000. Use the following questions to guide your preparation of a rough investment plan consistent with these facts.a) What are your key investment goals?b) How might your stage in the life cycle affect the types of risk you

might take?

Case Problem 1.1 Investments or Golf?

Judd Read and Judi Todd, senior accounting majors at a large Midwestern university, have been good friends since high school. Each has already found a job that will begin after graduation. Judd has accepted a position as an internal auditor in a medium-sized manufacturing firm. Judi will be working for one of the major public accounting firms. Each is looking forward to the challenge of a new career and to the prospect of achieving success both professionally and financially.

Judd and Judi are preparing to register for their final semester. Each has one free elective to select. Judd is considering taking a golf course offered by the physical education department, which he says will help him socialize in his business career. Judi is planning to take a basic investments course. Judi has been trying to convince Judd to take investments instead of golf. Judd believes he doesn’t need to take investments, because he already knows what common stock is. He believes that whenever he has accumulated excess funds, he can invest in the stock of a company that is doing well. Judi argues that there is much more to it than simply choosing common stock. She feels that exposure to the field of investments would be more beneficial than learning how to play golf.

QuestionsLearning Outcome: Describe the investment process

a. Explain to Judd the structure of the investment process and the economic importance of investing

Learning Outcome: Discuss the principal types of investment vehiclesb. List and discuss the other types of investment vehicles with which Judd is

apparently unfamiliar.Learning Outcome: Discuss the meaning of investment

c. Assuming that Judd already gets plenty of exercise, what arguments would you give to convince Judd to take investments rather than golf?

- 10 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 3 (Topic 2) ==

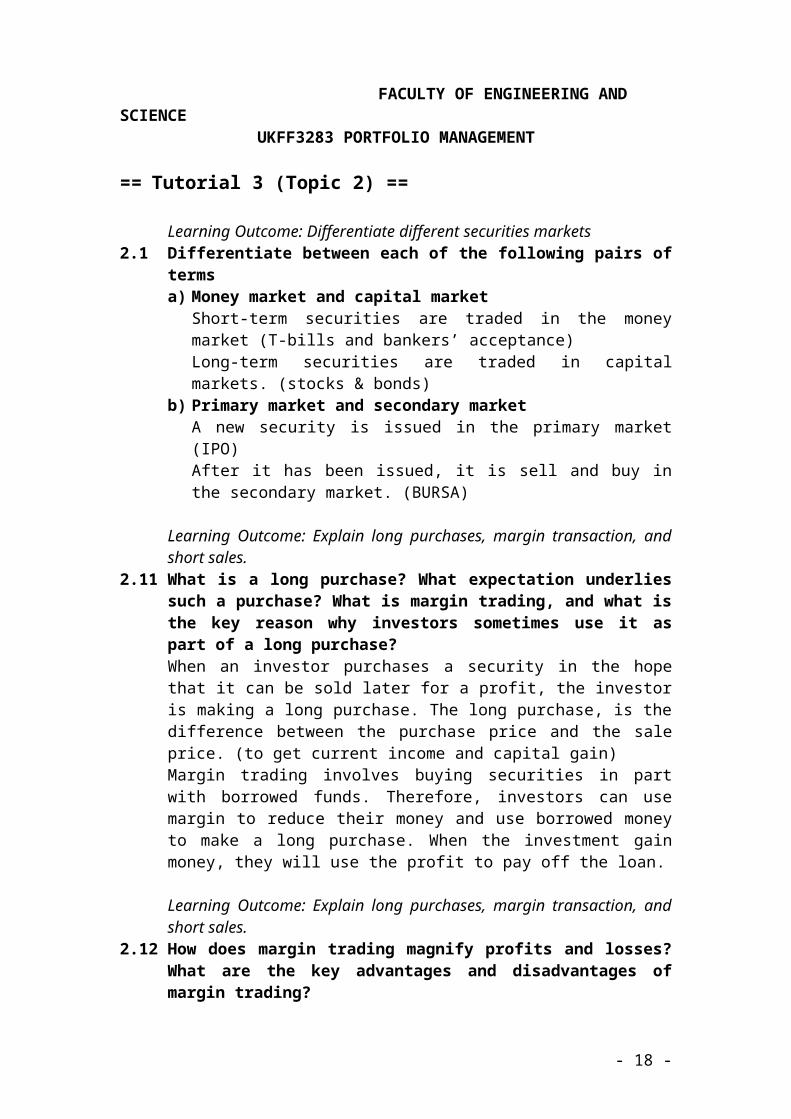

Learning Outcome: Differentiate different securities markets2.1 Differentiate between each of the following pairs of terms

a) Money market and capital marketShort-term securities are traded in the money market (T-bills and bankers’ acceptance)Long-term securities are traded in capital markets. (stocks & bonds)

b) Primary market and secondary marketA new security is issued in the primary market (IPO)After it has been issued, it is sell and buy in the secondary market. (BURSA)

Learning Outcome: Explain long purchases, margin transaction, and short sales.

2.11 What is a long purchase? What expectation underlies such a purchase? What is margin trading, and what is the key reason why investors sometimes use it as part of a long purchase?When an investor purchases a security in the hope that it can be sold later for a profit, the investor is making a long purchase. The long purchase, is the difference between the purchase price and the sale price. (to get current income and capital gain)Margin trading involves buying securities in part with borrowed funds. Therefore, investors can use margin to reduce their money and use borrowed money to make a long purchase. When the investment gain money, they will use the profit to pay off the loan.

Learning Outcome: Explain long purchases, margin transaction, and short sales.

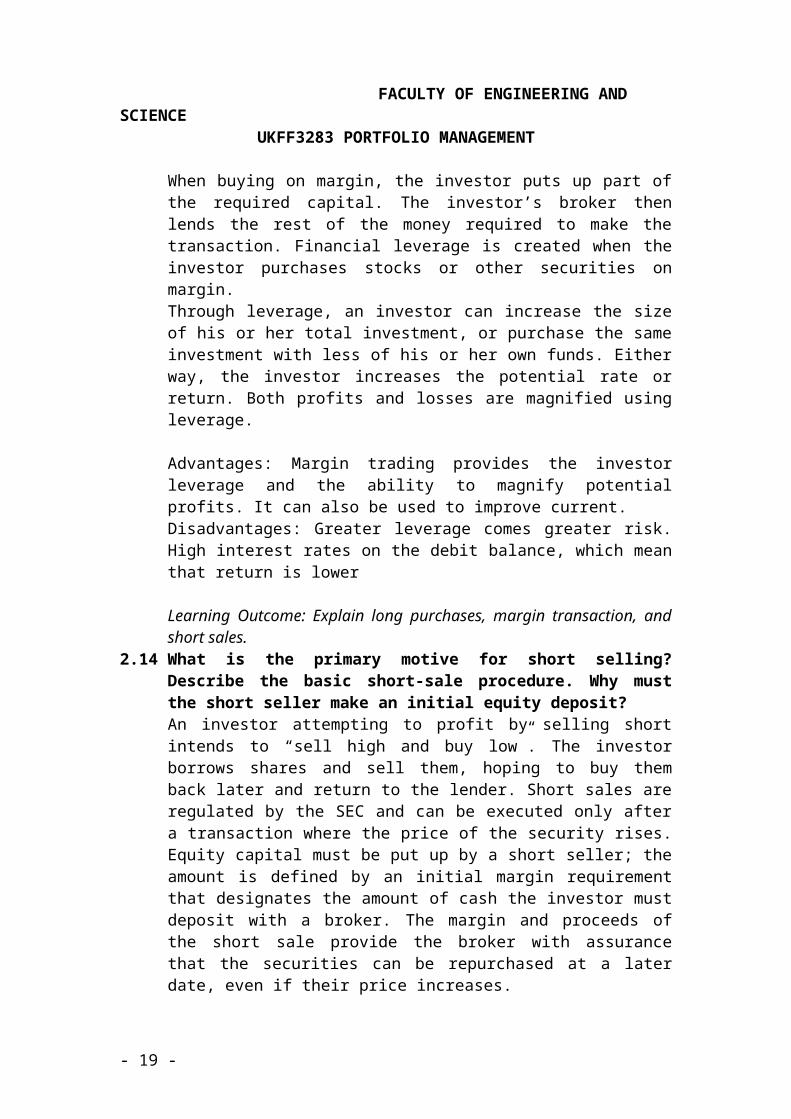

2.12 How does margin trading magnify profits and losses? What are the key advantages and disadvantages of margin trading?When buying on margin, the investor puts up part of the required capital. The investor’s broker then lends the rest of the money required to make the transaction. Financial leverage is created when the investor purchases stocks or other securities on margin.Through leverage, an investor can increase the size of his or her total investment, or purchase the same investment with less of his or her own funds. Either way, the investor increases the potential rate or return. Both profits and losses are magnified using leverage.

Advantages: Margin trading provides the investor leverage and the ability to magnify potential profits. It can also be used to improve current.Disadvantages: Greater leverage comes greater risk. High interest rates on the debit balance, which mean that return is lower

Learning Outcome: Explain long purchases, margin transaction, and short sales.

- 11 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

2.14 What is the primary motive for short selling? Describe the basic short-sale procedure. Why must the short seller make an initial equity deposit? An investor attempting to profit by selling short intends to “sell high and buy low”. The investor borrows shares and sell them, hoping to buy them back later and return to the lender. Short sales are regulated by the SEC and can be executed only after a transaction where the price of the security rises. Equity capital must be put up by a short seller; the amount is defined by an initial margin requirement that designates the amount of cash the investor must deposit with a broker. The margin and proceeds of the short sale provide the broker with assurance that the securities can be repurchased at a later date, even if their price increases.

Learning Outcome: Explain long purchases, margin transaction, and short sales.

2.16 Describe the key advantages and disadvantages of short selling. How are short sales used to earn speculative profits?Advantage: the chance to convert a price into a profit-making situation. The technique can also be used to protect profits already earned and to defer taxes on those profitsDisadvantage: High risk exposure in the face of limited return opportunities. Short sellers never earn dividends, but must pay them as long as the transaction is outstanding.Speculative profits. The investor is betting against the market, which involves considerable risk exposure. If the market moves up instead of down, the investor could lose all the short sale proceeds and margin.

Learning Outcome: Explain long purchases, margin transaction, and short sales.

P2.6 Elmo Inc.'s stock is currently selling at $60 per share. For each of the following situations (ignoring brokerage commissions), calculate the gain or loss that Maureen Katz realizes if she makes a l00-share transaction.a. She sells short and repurchases the borrowed shares at $70 per share.

A loss of $1000. ($6000-$7000)The short sale gain is $6000, while the replacement of the shares cost her $7000

b. She takes a long position and sells the stock at $75 per share.A profit of $1500. ($6000+$7500)The long position would initially cost her 6000 but gain $7500 when she sells at $75 per share

c. She sells short and repurchases the borrowed shares at $45 per share.A profit of $1500. ($6000-$4500)The short sale brings in $6000, while return of the shares to the owner costs only $4500

d. She takes a long position and sells the stock at $60 per share.A breakeven situation. The long position costs $6000 and the sale of the stock brings in $6000, thereby providing neither a profit nor a loss

- 12 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Explain long purchases, margin transaction, and short sales.

P2.10 James purchased 100 shares of Can’tWin.com for $50 per share, using as little of his own money as he could. His broker has a 50% initial margin requirement and 30% maintenance margin requirement. This price of the stock falls to $30 per share. What does James need to do?

James needs to cover a margin call.

Margin = (value of securities – debit balance)/value of securities

Debit balance = amount borrowed in the transaction

= value of securities – (margin x value of securities)

His new margin is 16.7% = ($3000-$2500)/$3000, below the 30% maintenance requirement

Value of securities = $30 x 100 = $3000

Old debit balance = $5000 – (0.5x$5000) = $2500

New debit balance = $3000 – (0.3x$3000) = $2100

In order to get back to the maintenance margin requirement of 30%, James must top up the difference between the old and new debit balance which is $400

Learning Outcome: Explain long purchases, margin transaction, and short sales.

P2.17 An investor short sells 100 shares of a stock for $20 per share. The initial margin is 50%, and the maintenance margin is 30%. The price of the stock falls to $12 per share. What is the margin, and will there be a margin call?Margin = (value of securities – debit balance / value of securities

= Account equity / calue of securities at purchaseValue of securities at purchase = $1200Value of securities at sale = $2000

Account equity = margin deposit of $1000 + net proceeds from the short sale= $1000 + ($2000-$1200)= $1800

The new margin 1800/1200 = 150%Since the margin of 150% is far above the maintenance margin of 30%, there is no

margin call.

Learning Outcome: Explain long purchases, margin transaction, and short sales.Case Problem 2.1 Dara’s Dilemma: What to Buy?

Dara Simmons, a 40-year-old financial analyst and divorced mother of two teenage children, considers herself a savvy investor. She has increased her investment portfolio considerably over the past 5 years. Although she has been

- 13 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

fairly conservative with her investments, she now feels more confident in her investment knowledge and would like to branch out into some new areas that could bring higher returns. She has between $20,000 and $25,000 to invest.

Attracted to the hot market for technology stocks, Dara was interested in purchasing a tech IPO stock and identified "NewestHighTech.com," a company that make sophisticated computer chips for wireless Internet connections, as a likely prospect. The 1-year-old company had received some favorable press when it got early-stage financing and again when its chip was accepted by a major cell phone manufacturer.

Dara also was considering an investment in 400 shares of Casinos International common stock, currently selling for $54 per share. After a discussion with a friend who is an economist with a major commercial bank, Dara believes that the long-running bull market is due to cool off and that economic activity will slow down. With the aid of he stockbroker, Dara researches Casinos International's current financial situation and finds that the future success of the company may hinge on the outcome of pending court proceedings on the firm's application to open a new floating casino on a nearby river. If the permit is granted, it seems likely that the firm's stock will experience a rapid increase (in value, regardless of economic conditions. On the other hand, if the company fails to get the permit, the falling stock price will make it a good candidate for a short sale.

Dara felt that the following alternatives were open to her:Alternative 1: Invest $20,000 in NewestHighTech.com when it goes public.Alternative 2: Buy Casinos International now at $54 per share and follow the company closely.Alternative 3: Sell Casinos short at $54 in anticipation that the company's fortunes will change for the worse.Alternative 4: Wait to see what happens with the casino permit and then decide whether to buy or short the Casinos International stock.

Questions

a. Evaluate each of these alternatives. On the basis of the limited information presented, recommend the one you feel is best.Alternative 4

b. If Casinos International's stock price rises to $60, what will happen under alternatives 2 and 3? Evaluate the pros and cons of these outcomes.Alternative 2: the stock should be sold, yielding a total profit of $2,400 ($6 per share × 400 shares). A disadvantage of Alternative 2 is that if the stock price had risen to, say, $59 and then fallen, the order would not have been executed.

- 14 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Alternative 3: the stop-loss order would not have been executed. Alternative 3 would have helped Dara minimize her losses in the event of a price decline.

c. If the stock price drops to $45, what will happen under alternatives 2 and 3? Evaluate the pros and cons of these outcomes.Alternative 2: would be meaningless, and the limit order would expire unexecuted. If any sale then would bring in approximately $18,000 (400 shares × $45 per share). Thus, Dara’s loss would be held to $3,600 (400 shares × $54 per share− 400 shares × $45 per share). Alternative 3: the loss could be greater if the price fell below $45 before the sell order was actually executed.

Learning Outcome: Describe the basic types of orders, and online transactions.3.15 Differentiate among market orders, limit orders, and stop-loss orders. What

is the rationale for using a stop-loss order rather than a limit order?market order

an order to buy or sell a security at the best price available when order is placed

fastest way to make transactions. limit order

an order to buy stock at or below or to sell stock at or above a specified price If price limits are not met, order will not be executed

stop-loss order “Suspended” order is placed to sell a stock if price reaches or falls below a

specific level used to protect investors from stock price decline Once activated, becomes a market order The stop-loss order gives them the opportunity to sell the stock when

the price declines to the stop price, thereby reducing their potential losses

Learning Outcome: Describe the basic types of orders, and online transactions.3.16 What is day trading, and why is it risky? How can you avoid problems as

an online trader?Day Trader:an investor who buys and sells stocks quickly throughout the day in hopes of making quick profits, it is risky because it often used with margin trading and high brokerage commissions due to frequent tradingslide 2-32

• Know how to place and confirm orders• Verify stock ticker symbols• Use limit orders• Check and recheck orders—you pay for typos• Don’t get carried away

• Follow a strategy• Don’t churn

- 15 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

• Avoid or limit margin orders• Open accounts with two brokers• Double-check orders for accuracy after completion

Learning Outcome: Describe the basic types of orders, and online transactions.P3.6 Imagine that you have placed a limit order to buy 100 shares of Sallisaw

Tool at a price of $38, though the stock is currently selling for $41. Discuss the consequences, if any, of each of the following.a. The stock price drops to $39 per share 2 months before cancellation of

the limit order.The limit order will be executed only if the stock price falls to $38 or less than $38, thus, the order will not be executed.

b. The stock price drops to $38 per share.The order will be executed, your broker will buy 100 shares of Sallisaw Tool stock with $38 per share, total costs is $3800

c. The minimum stock price achieved before cancellation of the limit order was $38.50. When the limit order was canceled, the stock was selling for $47.50 per share.Since the stock price is more than $38, the order will not be executed. If you buy the stock at $41 per share instead of placing the order limit, you can now sell it at $47.50 per share, earning $6.5 per share with total profit of $650

Learning Outcome: Describe the basic types of orders, and online transactions.P3.7 If you place a stop-loss order to sell at $23 on a stock currently selling for

$26.50 per share, what is likely to be the minimum loss you will experience on 50 shares if the stock price rapidly declines to $20.50 per share? Explain. What if you had placed a stop-limit order to sell at $23, and the stock price tumbled to $20.50?Minimum loss = $3.5/share, total minimum loss = $175 ($3.5*50)When the stock price falls to $23, the stop-loss order is converted to market order to sell at best price available at that time. For stop limit order, if the stock price drop to $20.50, the loss would be $6 per share or in total $300.

Learning Outcome: Describe the basic types of orders, and online transactions.P3.8 You sell 100 shares of a stock short for $40 per share. You want to limit

your loss on this transaction to no more than $500. What order should you place?Stop-loss order to buy shares at $45/share. (limit your loss not more than $5/share)

- 16 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Describe the basic types of orders, and online transactions.P3.9 You have been researching a stock that you like, which is currently

trading at $50 per share. You would like to buy the stock if it were a little less expensive - say, $47 per share. You believe that the stock price will go to $70 by year-end, and then level off or decline. You decide to place a limit order to buy 100 shares of the stock at $47, and a limit order to sell it at $70. It turns out that you were right about the direction of the stock price, and it goes straight to $75. What is your current position? Since the stock did not fall to the limit order buy price, so it will not be executed, you are not buying it. However, you sold it at $70 per share. Since the stock is currently selling for $75, you loss $5/share, total loss = $500

- 17 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 4 (Topic 3) ==

Learning Outcome: Review the concept of return and its components.4.1 Explain what is meant by the return on an investment. Differentiate

between the two components of return – current income and capital gains (or losses).Return is the level of profit from an investment or the reward of investing. Total return is the sum of the current income and the capital gain (or loss) earned on an investment over a specified period of time.Current income is cash or near cash that is received as a result of owning an investment.Capital gains is the difference between the proceeds from the sale of an investment and its original purchase price

Learning Outcome: Define a satisfactory investment.4.3 What is a satisfactory investment? When the present value of benefits

exceeds the cost of an investment, what is true of the rate of return earned by the investor relative to the discount rate?Satisfactory investment is one for which the present value of benefits equals or exceed the present value of its costs. When PV inflow > PV outflow, net PV is positive.This IRR > discount rateHence acceptable (satisfactory) investment.

Learning Outcome: Explain the concept of yield.4.6 Define yield (internal rate of return). When is it appropriate to use yield

rather than the HPR to measure the return on an investment?IRR determines the compound annual rate of return earned on an investment held for longer than one year. For long term investment.

Learning Outcome: Discuss the key sources of risk.4.9 Define risk. Explain what we mean by the risk-return tradeoff. What

happens to the required return as risk increases? Explain.Risk is the chance that the actual return from an investment may differ from what is expected. Risk-return tradeoff is the relationship between risk and return, in which investments with more risk should provide higher return and vice versa. Return should be higher as risk increases.

Learning Outcome: Discuss the key sources of risk.4.10 Define and briefly discuss each of the following sources of risk.

a) Business riskDegree of uncertainty associated with an investment’s earnings and the investment’s ability to pay the returns owed to investors. Types of investments affected are common stocks and preferred stocks. Examples: decline in company profits or market share

b) Financial riskDegree of uncertainty of payment resulting from a firm’s mix of debt and equity; the larger the proportion of debt financing, the greater the risk.

- 18 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Types of investments affected are common stocks and corporate bonds. Example: company can’t get additional loans for growth or to fund operations

c) Purchasing power riskChance that changing price levels (inflation or deflation) will adversely affect investment returns. Types of investments affected are bonds (fixed income) and fixed deposits. Example: Movie that was RM8 last year is RM9 this year

d) Interest rate riskChance that changes in interest rates will adversely affect a security’s value. Types of investments affected are bonds(fixed income) and preferred stocks. Example: market value of existing bonds decreases as market interest rates increase.

e) Liquidity riskRisk of not being able to liquidate an investment conveniently and at a reasonable price. Affects all types of investments. Example: Decrease in value of insurance company stock after a major hurricane.

f) Market riskRisk of decline in investment returns because of market factors independent of the given investment. Affects all types of investments. Example: changes in economic conditions.

g) Event riskUnexpected event that has a significant and unusually immediate effect on the underlying value of an investment. Affects all types of investments. Example: decrease in value of real estate after a major earthquake

Learning Outcome: Review the concept of return and its components.P4.4 Assume you purchased a bond for $9,500. The bond pays $300 interest

every 6 months. You sell the bond after 18 months for $10,000. Calculate the following:a. Current income.

$300x3 = $900b. Capital gain or loss.

$10000-$9500 = $500c. Total return in dollars and as a percentage of the original investment.

Total return in dollars = dividend income + capital gain / beginning investment= (900+500)/9500 = 14.74%

- 19 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Calculation and application of holding period returnP4.10 You are considering two investment alternatives. The first is a stock that

pays quarterly dividends of $0.50 per share and is trading at $25 per share; you expect to sell the stock in 6 months for $27. The second is a stock that pays quarterly dividends of $0.60 per share and is trading at $27 per share; you expect to sell the stock in 1 year for $30. Which stock will provide the better annualized holding period return?Investment 1: Dividend = $0.50 * 2 = $1Capital gain = 27-25 = $2Holding period return = (1+2) / 25 = 0.12Annualized holding period return = 0.12 * 2 = 0.24 = 24%Investment 2:Dividend = $0.60 * 4 = $2.40Capital gain = 30-27 = $3Holding period return = (2.40+3) / 27 = 0.2Annualized holding period return = 0.2 * 1 = 0.20 = 20%

Therefore, the first option is better because it provides better annualized holding period return.

Learning Outcome: Calculation of yieldP4.14 Your friend asks you to invest $10,000 in a business venture. Based on

your estimates, you would receive nothing for 4 years, at the end of years 5 you would receive interest on the investment compounded annually at 8%, and at the end of year 6 you would receive $14,500. If your estimates are correct, what would be the yield on this investment?Interest = 10000 (1+0.08 - 10000 = 4693.28IRR = 12.02%

Learning Outcome: Calculation of yieldP4.18 Elliott Dumack must earn a minimum rate of return of 11% to be

adequately compensated for the risk of the following investment.

Initial Investment $14,000 End of Year Income

1 $ 6,0002 3,0003 5,0004 2,0005 1,000

a. Use present-value techniques to estimate the yield on this investment.IRR = 8.85%

b. On the basis of your finding in part a, should Elliott make the proposed investment? Explain.No, because IRR < min. rate of return

- 20 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Assess the risk of assetsP 4.23 The historical returns for two investments – A and B – are summarized in

the table below for the period 2004 to 2008. Use the data to answer the questions that follow.

Investment_____Year A B 2004 19% 8%2005 1 102006 10 122007 26 142008 4 16Average 12% 12%

a. On the basis of a review of the return data, which investment appears to be more risky? Why?A has 2 outliers (1% and 4%) compared to B.A has a larger percentage range of return than B

b. Calculate the standard deviation and the coefficient of variation for each investment’s returns.Std deviation of A = 10.416%Std deviation of B = 3%Coefficient of Variation of A = 0.868Coefficient of Variation of B = 0.25

c. On the basis of your calculations in part b, which investment is more risky? Compare this conclusion to your observation in part a.A is more risky than B : Std dev A > B, CV A > CV B

d. Does the coefficient of variation provide better risk comparison than the standard deviation in the case? Why or why not?No. Since both have the same expected return and CV is useful in comparing risks of assets with differing expected return.

Learning Outcome: Apply the concept of time value of money & calculation of yieldCase Problem 4.1 Solomon’s Decision

Dave Solomon, a 23-year-old mathematics teacher at Xavier High School, recently received a tax refund of $1,100. Because Dave didn't need this money for his current living expenses, he decided to make a long-term investment. After surveying a number of alternative investments costing no more than $1,100, Dave isolated 2 that seemed most suitable to his needs.

Each of the investments cost $1,050 and was expected to provide income over a 10-year period. Investment A provided a relatively certain stream of income. Dave was a little less certain of the income provided by investment B. From his search for suitable alternatives, Dave found that the appropriate discount rate for a relatively certain investment was 12%. Because he felt a bit uncomfortable with an investment like B, he estimated that such an investment would have to provide a return at least 4% higher than investment A. Although Dave planned to reinvest funds returned from the investments in other vehicles providing

- 21 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

similar returns, he wished to keep the extra $50 ($1,100 - $1,050) invested for the full 10 years in a savings account paying 5% interest compounded annually.

As he makes his investment decision, Dave has asked for your help in answering the questions that follow the expected return data for these investments.

Expected Returns Year A B 2009 $ 150 $100 2010 150 150 2011 150 200 2012 150 250 2013 150 300 2014 150 350 2015 150 300 2016 150 250 2017 150 200 2018 1,150 150

Questions

a. Assuming that investments A and B are equally risky and using the 12% discount rate, apply the present-value technique to assess the acceptability of each investment and to determine the preferred investment. Explain your findings.NPV A = 119.51NPV B = 164.74Hence, investment B is preferred as NPV of investment B is higher than NPV of investment Ab. Recognizing that investment B is more risky than investment A, reassess the 2 alternatives, adding the 4% risk premium to the 12% discount rate for investment A and therefore applying a 16% discount rate to investment B. Compare your findings relative to acceptability and preference to those found for question a.NPV A = -98.33NPV B = -30.63Hence, both investments are not acceptable, never invest in projects which has negative NPV.

c. From your findings in questions a and b, indicate whether the yield for investment A is above or below 12% and whether that for investment B is above or below 16%.Explain.Since the investment A is acceptable at 12%, its yield should be above 12%. Since the investment B is acceptable at 12%, its yield should be above 12%.However, the yield of investment should be below 16% because the PV of benefit is less than the cost. Its yield should be at 15.31.

- 22 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

d. Use the present-value technique to estimate the yield on each investment. Compare your findings and contrast them with your response to question c.Investment A = 14.04Investment B = 15.31For A, yield > 12% = 14.04%For B, yield < 16% = 15.31%

e. From the information given, which, if either, of the two investments would you recommend that Dave make? Explain your answer.Investment A. This is because the IRR of investment is 14.04 which is higher than the expected 12% rate.

f. Indicate to Dave how much money the extra $50 will have grown to by the end of 2018, assuming he makes no withdrawals from the savings account.

- 23 -

=

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 5 (Topic 4) ==

Learning Outcome: Discuss the concepts of correlation and diversification5.3 What is correlation, and why is it important with respect to asset returns?

Describe the characteristics of returns that are (a) positively correlated, (b) negatively correlated, and (c) uncorrelated. Differentiate between perfect positive correlation and perfect negative correlation.Correlation is a statistical measure of the relationship between two series of numbers representing data. It combines two assets to reduce overall risk in our portfolio.a) Positively correlated – both assets returns move in same directionb) Negatively correlated – both assets returns move in opposite directionc) Uncorrelated – two series that lack any relationship and have a correlation

coefficient of nearly zero

Perfect positive correlation – two positively correlated series having a correlation coefficient of +1

Perfect negative correlation – two negatively correlated series having a correlation coefficient of -1

Learning Outcome: Discuss the concepts of correlation and diversification5.4 What is diversification? How does the diversification of risk affect the

risk of the portfolio compared to the risk of the individual assets it contains?Diversification is a process of risk reduction achieved by including in the

portfolio a variety of vehicles having returns that are less than perfectly positive correlated with each other. The goal is to reduce overall risk in a portfolio.It allows investor to reduce the risk by combining negatively correlated assets so that the risk of the portfolio is less than the risk of the individual assets.

Learning Outcome: Describe the components of risk and the use of beta to measure risk

5.7 Briefly define and give examples of each of the following components of total risk. Which is the relevant risk, and why?(a) Diversifiable risk (b) Nondiversifiable riska) Diversifiable risk is the results from uncontrollable or random events that are firm-specific. It can be eliminated through diversification. Examples are labor strikes and lawsuits.b) Nondiversifiable risk is also known as relevant risk/market risk. It is attributable to forces that affect all similar investments. It cannot be eliminated through diversification. Examples are war, inflation, political events. It is considered the only relevant risk because diversifiable (unsystematic) risk can be removed by creating a portfolio of assets which are not perfectly positively correlated or through diversification.

Learning Outcome: Describe the components of risk and the use of beta to measure risk

- 24 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

5.8 Explain what is meant by beta. What is the relevant risk measured by beta? What is the market return? How is the interpretation of beta related to the market return?Beta is a measure of systematic risk. It indicates how the price of a security responds to market forces and compares historical return of an investment to the market return. The higher the beta, the riskier the security. The relevant risk measured by beta is the nondiversifiable risk of an investment since the investor can eliminate the unsystematic risk by holding a diversified portfolio of securities.Market return is measured by the average return of all stocks.Beta for the overall market is the benchmark beta and is 1.0. The positive or negative sign on a beta indicates whether the stock’s return changes in the same direction as the general market or opposite direction. Stocks with betas greater than 1.0 are more risky than the overall market and vice versa.

Learning Outcome: Review the traditional & modern approaches to portfolio management

5.12 Describe traditional portfolio management. Give three reasons why traditional portfolio managers like to invest in well-established companies.Traditional portfolio management emphasizes “balancing” the portfolio using a wide variety of stocks or bonds. The three reasons are:-a) perceived as less riskyb) stocks are more liquid and available in large quantitiesc) familiarity provides higher “comfort” levels for investors

Learning Outcome: Review the traditional & modern approaches to portfolio management

5.13 What is modern portfolio theory (MPT)? What is the feasible or attainable set of all possible portfolios? How is it derived for a given group of investment vehicles?MPT emphasizes statistical measures to develop a portfolio plan. It focuses on expected returns, standard deviation of returns and correlation between returns. It combines securities with negative or low positive correlation to reduce risk through diversification.The feasible or attainable set of all possible portfolios refers to the risk-return combinations achieved with all possible portfolios. It is derived by calculating the return and risk of all possible portfolios and then plotting them on a set of risk-return axes.

- 25 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Describe risk-return tradeoff of portfolio5.14 What is efficient frontier? How is it related to the attainable set of all

possible portfolios? How can it be used with an investor’s utility function to find the optimal portfolio?Efficient frontier is the site of all efficient portfolios (with the best risk-return tradeoff). All portfolios on the efficient frontier are preferable to the others in the feasible or attainable set. Investor’s utility function is plotted on the graph with the feasible or attainable set of portfolios – indicate the investor’s optimal portfolio (curve meets the efficient frontier). This represents the highest level of satisfaction for that investor

Learning Outcome: Calculate portfolio return and standard deviation, correlation

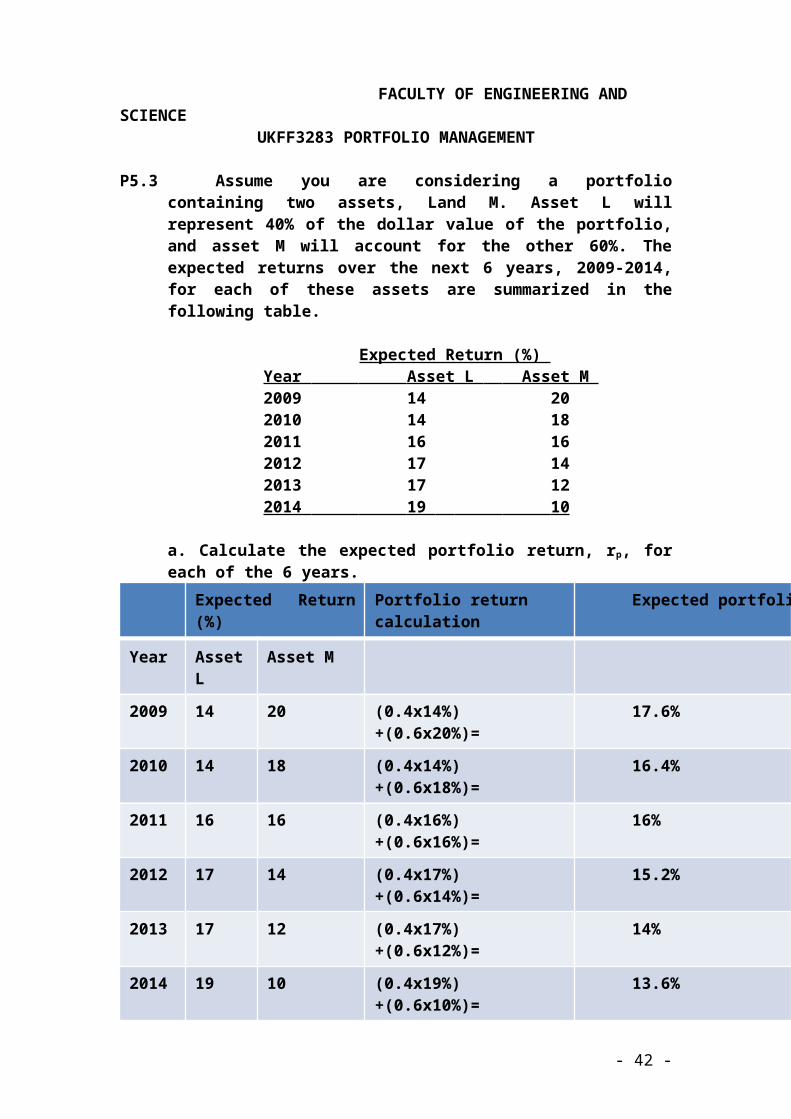

P5.3 Assume you are considering a portfolio containing two assets, Land M. Asset L will represent 40% of the dollar value of the portfolio, and asset M will account for the other 60%. The expected returns over the next 6 years, 2009-2014, for each of these assets are summarized in the following table.

Expected Return (%) Year Asset L Asset M 2009 14 20 2010 14 18 2011 16 16 2012 17 14 2013 17 12 2014 19 10

- 26 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

a. Calculate the expected portfolio return, rp, for each of the 6 years.

Expected Return (%) Portfolio return calculation Expected portfolio return (r

Year Asset L Asset M

2009 14 20 (0.4x14%)+(0.6x20%)= 17.6%

2010 14 18 (0.4x14%)+(0.6x18%)= 16.4%

2011 16 16 (0.4x16%)+(0.6x16%)= 16%

2012 17 14 (0.4x17%)+(0.6x14%)= 15.2%

2013 17 12 (0.4x17%)+(0.6x12%)= 14%

2014 19 10 (0.4x19%)+(0.6x10%)= 13.6%

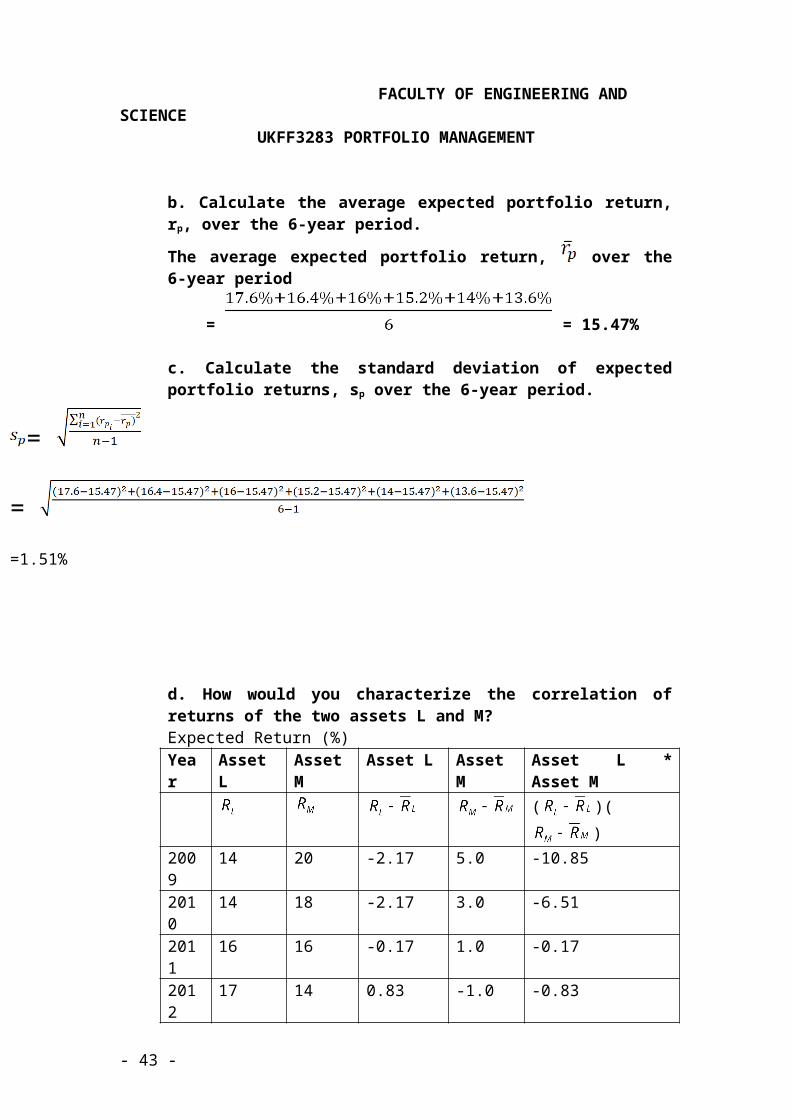

b. Calculate the average expected portfolio return, rp, over the 6-year period.

The average expected portfolio return, over the 6-year period

= = 15.47%

c. Calculate the standard deviation of expected portfolio returns, sp over the 6-year period.

d. How would you characterize the correlation of returns of the two assets L and M? Expected Return (%)Year Asset L Asset M Asset L Asset M Asset L * Asset M

( )( )

2009 14 20 -2.17 5.0 -10.85

- 27 -

=

=

=1.51%

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

2010 14 18 -2.17 3.0 -6.512011 16 16 -0.17 1.0 -0.172012 17 14 0.83 -1.0 -0.832013 17 12 0.83 -3.0 -2.492014 19 10 2.83 -5.0 -14.15Mean 16.17 15.0 Sum = -35

Year Asset L Asset M

( (

2009 -2.17 4.71 5.0 25.02010 -2.17 4.71 3.0 9.02011 -0.17 0.03 1.0 1.02012 0.83 0.69 -1.0 1.02013 0.83 0.69 -3.0 9.02014 2.83 8.01 -5.0 25.0

Sum=18.84 Sum=70.0

The correlation of returns of the two assets L and M are negatively correlated.

e. Discuss any benefits of diversification achieved through creation of the portfolio.By combining two assets L and M that have a negative correlation will be reducing overall risk more effectively compare invest in high positive correlation.

- 28 -

=

=

= 3.74

Correlation, =

=

= 3.74

Correlation, =

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

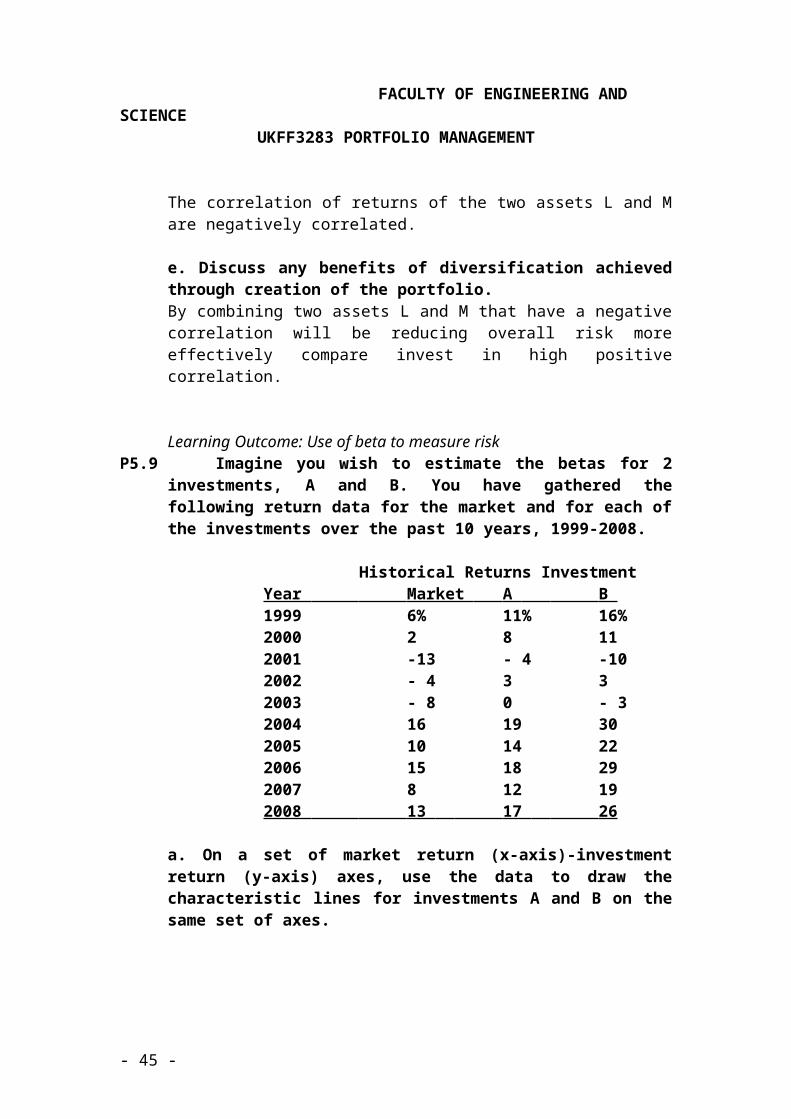

Learning Outcome: Use of beta to measure riskP5.9 Imagine you wish to estimate the betas for 2 investments, A and B. You

have gathered the following return data for the market and for each of the investments over the past 10 years, 1999-2008.

Historical Returns Investment Year Market A B 1999 6% 11% 16% 2000 2 8 11 2001 -13 - 4 -10 2002 - 4 3 3 2003 - 8 0 - 3 2004 16 19 30 2005 10 14 22 2006 15 18 29 2007 8 12 19 2008 13 17 26

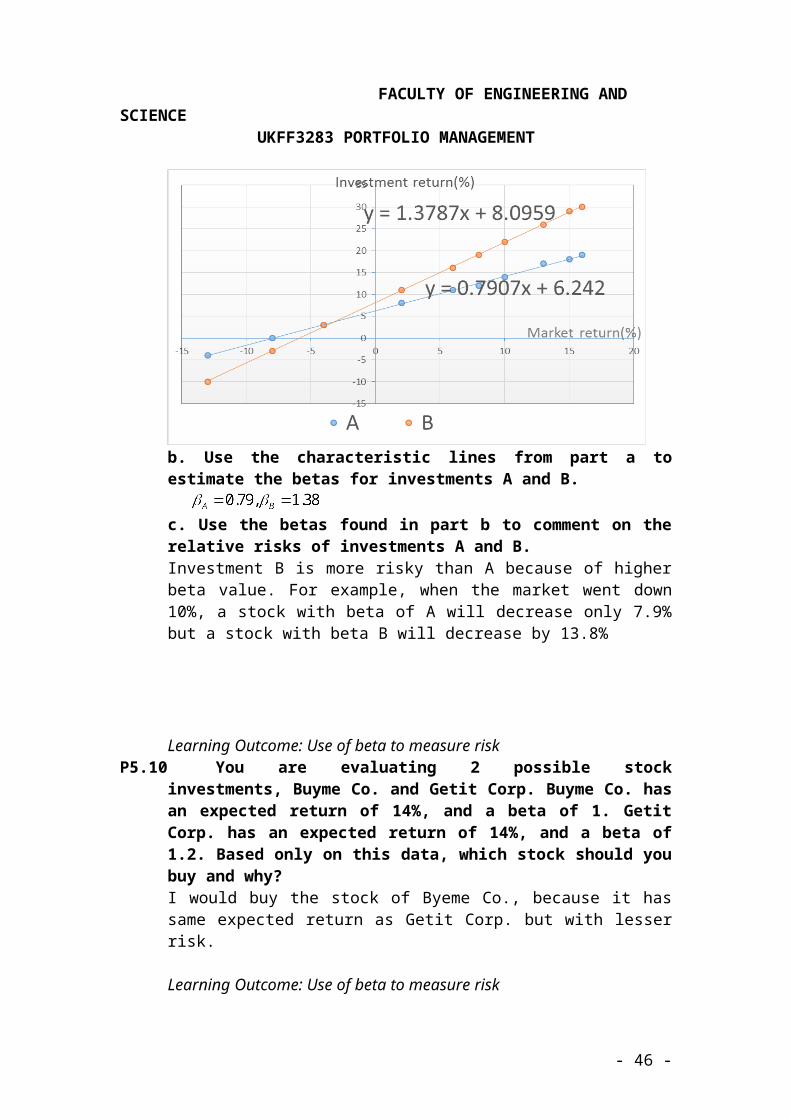

a. On a set of market return (x-axis)-investment return (y-axis) axes, use the data to draw the characteristic lines for investments A and B on the same set of axes.

b. Use the characteristic lines from part a to estimate the betas for investments A and B.

c. Use the betas found in part b to comment on the relative risks of investments A and B.Investment B is more risky than A because of higher beta value. For example, when the market went down 10%, a stock with beta of A will decrease only 7.9% but a stock with beta B will decrease by 13.8%

- 29 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Use of beta to measure riskP5.10 You are evaluating 2 possible stock investments, Buyme Co. and Getit

Corp. Buyme Co. has an expected return of 14%, and a beta of 1. Getit Corp. has an expected return of 14%, and a beta of 1.2. Based only on this data, which stock should you buy and why?I would buy the stock of Byeme Co., because it has same expected return as Getit Corp. but with lesser risk.

Learning Outcome: Use of beta to measure riskP5.12 A security has a beta of 1.20. Is this security more or less risky than the

market? Explain. Assess the impact on the required return of this security in each of the following cases.The security is more risky than the market because it has a beta of 1.20 which is higher than the beta of market which is 1.00a. The market return increases by 15%.Change in security return = Beta X change in market return1.20 * 15% = 18% increaseb. The market return decreases by 8%.1.20 * (-8%) = -9.6% decreasec. The market return remains unchanged.1.20 * 0% = 0% no change

Learning Outcome: Use of beta to measure riskP5.13 Assume the betas for securities A, B, and C are as shown here.

Security Beta A 1.40 B 0.80C -0.90

a. Calculate the change in return for each security if the market experiences an increase in its rate of return of 13.2 % over the next period.Security A return = 1.40 * 13.2% = 18.48%Security B return = 0.80 * 13.2% = 10.56%Security C return = -0.90 * 13.2% = -11.88%b. Calculate the change in return for each security if the market experiences a decrease in its rate of return of 10.8% over the next period.Security A return = 1.40 * (-10.8%) = -15.12%Security B return = 0.80 * (-10.8%) = -8.64%Security C return = -0.90 * (-10.8%) = 9.72%

- 30 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

c. Rank and discuss the relative risk of each security on the basis of your findings. Which security might perform best during an economic downturn? Explain.Through the beta values and changes of security A’s return in the market return, it shows that security A is most risky of all. Security C moves in the opposite direction from the market in a defensive manner. While security B is the least responsive in the market which makes it in the category of least risky.The market can probably be assumed that the market return will decrease during the economic downturn. In this situation, Security C will outperform others. If security C did not perform as expected, the least responsive will be the best which is security B.

Learning Outcome: Calculate portfolio betasP5.23 Rose Berry is attempting to evaluate 2 possible portfolios consisting of the

same 5 asset but held in different proportions. She is particularly interested in using beta to compare the risk of the portfolios and, in this regard, has gathered the following data:

Portfolio Weights (%) Asset Asset Beta Portfolio A Portfolio B 1 1.30 10 30 2 0.70 30 10 3 1.25 10 20 4 1.10 10 20 5 0.90 40 20

Total 100 100

a. Calculate the betas for portfolios A and B.Beta of portfolio A = 1.30(0.1) + 0.70(0.3) + 1.25(0.1) + 1.10(0.1) + 0.90(0.4) = 0.935Beta of portfolio B = 1.30(0.3) + 0.70(0.1) + 1.25(0.2) + 1.10(0.2) + 0.90(0.2)= 1.11b. Compare the risk of each portfolio to the market as well as to each other. Which portfolio is more risky?The risk of Portfolio A is slightly less than the market while the risk of Portfolio B is more than the market. Therefore, Portfolio B is more risky

- 31 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 6 (Topic 5) ==

Learning Outcome: Describe the basic features of mutual funds12.1 What is a mutual fund? Discuss the mutual fund concept, including the

importance of diversification and professional management.A mutual fund invests in a diversified portfolio of securities and issues shares in the portfolio to individual investors; mutual funds represent ownership in a managed portfolio of securities. The mutual fund concept, therefore, revolves around diversification. Diversification, which reduces the overall risk borne by the investor, is available through a mutual fund. This, coupled with the fact that mutual funds have professional management, which frees the individual investor from managing his own portfolio, makes mutual funds attractive to individuals.

Learning Outcome: Describe the basic features of mutual funds12.3 Briefly describe how a mutual fund is organized. Who are the key players

in a typical mutual fund organization?Mutual funds are frequently open-ended investment companies; investors in mutual funds are essentially buying a small piece of a large, well-diversified portfolio of securities. A mutual fund is a financial services organization that receives money from its shareholders and invests those funds in a portfolio of securities. The investors in a given mutual fund are all part-owners of that portfolio. Individual mutual funds are created by management companies, like Fidelity, Dreyfus, and Vanguard. They also run the funds’ daily operations and usually serve as the investment advisor. The investment advisor buys and sells securities and otherwise oversees the fund’s portfolio. This is normally carried out by: the money manager, who actually runs the portfolio; security analysts, who look for viable investment candidates; and traders, who attempt to trade large blocks of securities at the best possible price. In addition, there are fund distributors, who actually buy and sell the fund shares; custodians, who take physical possession of the fund’s securities and other assets; and the transfer agent, who keeps track of fund shareholders. (Note: All these participants are part of open-end mutual funds; however, closed-end investment companies do not require a distributor. Shares in these funds trade in the open markets.)

Learning Outcome: Discuss the various types investment companies12.4 Define each of the following:

a) Open-end investment companiesAn open-end investment company is a mutual fund in which investors actually buy their shares from and sell them back to the mutual fund itself. There is no limit on the number of shares an open-end fund can issue, and this is by far the most common type of mutual fund.

b) Closed-end investment companiesA closed-end investment company is a fund that operates with a fixed number of outstanding shares and does not regularly issue new shares of stock. These funds, which are few in number relative to open-end funds, operate with a fixed capital structure and trade in the stock market—most are listed on the NYSE

c) Exchange-traded fundsAn exchange-traded fund (ETF) is a type of open-end investment company that trades as a listed security on one of the stock exchanges.

- 32 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

d) Real estate investment trustsA real estate investment trust (REIT) is a type of closed-end investment company that invests money in mortgages and various types of real estate investments. REITs allow investors to receive both the capital appreciation and current income from real estate ownership without having to manage the property.

e) Hedge fundsLike mutual funds, hedge funds sell shares (or participation) units in a professionally managed portfolio of securities. However, hedge funds are private partnerships that tend to limit their clientele to rich individuals. The manager is a general partner, while the investors are limited partners. Hedge funds have very limited reporting requirements and are generally unregulated. Some hedge funds attempt to limit the downside risk through employment of options and futures, while others invest in any opportunity that has the potential of a positive return.

Learning Outcome: Discuss the various types of funds12.7 Briefly describe each of the following types of mutual funds:

a) Aggressive growth fundsAggressive growth funds are highly speculative funds that concentrate on obtaining large capital gains. These funds tend to be small and their portfolios consist of speculative common stocks. Returns on these funds generally move with the market, but in larger increments: when the market’s up, these funds do great, but when the market falls, they do really poorly.

b) Equity-income fundsEquity-income funds emphasize current income by investing primarily in high yielding common stocks. In addition to high-grade common stocks, these funds also invest in convertible securities, preferred stocks and even bonds. They like securities that provide high current yields, but also consider potential price appreciation over the longer haul. These funds are generally viewed as a fairly low risk way of investing in stocks.

c) Growth-and-income fundsGrowth-and-income funds seek a balanced return made up of both current income and long-term capital gains, with the greatest emphasis placed on growth of capital. Unlike balanced funds, growth and income funds have 80–90 percent of their capital in common stocks). They tend to invest in growth-oriented blue chips (for their capital gains) and high-yield common stocks (for their current income due to high dividends).

d) Bond fundsBond funds come in all shapes and colors (from government bond funds to high yield [junk] corporate bond funds) and they all have one thing in common: they invest principally (or exclusively) in some type(s) of fixed-income security. While current income is the primary objective of these funds, capital gains is not ignored altogether. Today, there’s a full range of bond funds, ranging from the very conservative to the very risky.

- 33 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

e) Sector fundsSector funds are mutual funds that concentrate their holdings in one or more industries that make up a target sector. For instance, a health care sector fund may hold drug companies, medical suppliers, biotech companies, and hospital management companies. They are not widely diversified and therefore are riskier than diversified funds.

f) Socially responsible fundsSocially responsible funds are mutual funds that actively and directly incorporate ethics and morality into the investment decision. These funds will consider only socially responsible companies for inclusion in their portfolios. For example, these funds generally will not invest in companies that derive revenues from tobacco, alcohol, or gambling; companies that are weapons contractors; or that operate nuclear power plants.

Learning Outcome: Discuss the various types of fundsQ12.3 For each pair of funds listed below, select the one that is likely to be the

less risky. Briefly explain your answer.

a) Growth versus growth-and-income fundsGrowth versus growth and income funds: Growth funds have more risk due to greater investment for capital gain and therefore newer growing companies.

b) Equity-income versus high-grade corporate bond fundsEquity-income versus high-grade corporate bond funds: Bonds are less risky since they are rated investment quality as compared to ordinary common stock dividends that are declared after interest income to bondholders is paid.

c) Balanced versus sector fundsBalanced versus sector funds: Sector funds lack diversification and therefore may contain higher nonsystematic risk than a balanced more diversified fund.

d) Global versus aggressive growth fundsGlobal versus aggressive growth funds: This depends on what type of global fund is used. Global funds may also have aggressive growth targets but have political risk not associated with domestic aggressive growth funds.

e) Intermediate-term bonds versus high-yield municipal bond fundsIntermediate-term bonds versus high-yield municipal bond funds: High-yield municipal bonds usually have less risk since they are associated with cities and municipalities. However, these governmental units can have high risk depending on their credit ratings.

Case Problem 12.1 Reverend Billy Bob Ponders Mutual Funds

Reverend Billy Bob is the minister of a church in the San Diego area. He is married, has one young child, and earns a "modest income." Because religious organizations are not notorious for their generous retirement programs, the reverend has decided he should do some investing on his own. He would like to set up a program that enables him to supplement the church's retirement program and at the same time provide some funds for his child's college education (which is still some 12 years away). He is not out to break any

- 34 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

investment records but wants some backup to provide for the long-run needs of his family.

Although he has a modest income, Billy Bob believes that with careful planning, he can probably invest about $250 a quarter (and, with luck, increase this amount over time). He currently has about $15,000 in a savings account that he would be willing to use to begin this program. In view of his investment objectives, he is not interested in taking a lot of risk. Because his knowledge of investments extends to savings accounts, Series EE savings bonds, and a little bit about mutual funds, he approaches you for some investment advice.

Questions

Learning Outcome: Discuss the variety of investment objectivesa. In light of Reverend Billy Bob's long-term investment goals, do you think mutual funds are an appropriate investment vehicle for him?Yes, since Reverend Billy Bob earns a modest amount of income, it should be sufficient to start investing in a mutual fund. Also, since he has little knowledge about investment, it would be wise to invest in mutual fund becayse investments are done by professional money managers.

Learning Outcome: Discuss the variety of investment objectivesb. Do you think he should use his $15,000 savings to start a mutual fund investment program?Yes, he should invest as soon as possible because generally the earlier you invest the more interests you will get by time to time

Learning Outcome: Assess and select funds for investment purposesc. What type of mutual fund investment program would you set up for the Reverend?Include in your answer some discussion of the types of funds you would consider, the investment objectives you would set, and any investment services (e.g., withdrawal plans) you would seek. Would taxes be an important consideration in your investment advice? Explain. Since Reverend Billy Bob goals are to supplement his retirement and college education for his child, it would be best to invest in a growth fund or growth-income fund. He can also invest in a retirement plan if he wants to defer the tax payment until he decides to withdraw the investment at retirement

Case Problem 12.2 Tom Lasnicka Seeks the Good Life

Tom Lasnicka is a widower who recently retired after a long career with a major Midwestern manufacturer. Beginning as a skilled craftsman, he worked his way up to the level of shop supervisor over a period of more than 30 years with the firm. Tom receives Social Security benefits and a generous company pension. Together, these two sources amount to over $4,500 per month (part of which is tax-free). The Lasnickas had no children, so he lives alone. Tom owns a two-

- 35 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

bedroom rental house that is next to his home, and the rental income from it covers the mortgage payments for both the rental house and his house.

Over the years, Tom and his late wife, Camille, always tried to put a little money aside each month. The results have been nothing short of phenomenal. The value of Tom's liquid investments (all held in bank CDs and savings accounts) runs well into the six figures. Up to now, Tom has just let his money grow and has not used any of his savings to supplement his Social Security, pension, and rental income. But things are about to change. Tom has decided, "What the heck, it's time I start living the good life!" Tom wants to travel and, in effect, start reaping the benefits of his labors. He has therefore decided to move $100,000 from one of his savings accounts to one or two high-yielding mutual funds. He would like to receive $1,000-$1,500 a month from the fund(s) for as long as possible, because he plans to be around for a long time.

QuestionsLearning Outcome: Assess and select funds for investment purposesa. Given Tom's financial resources and investment objectives, what kinds of mutual funds do you think he should consider?Given Tom’s existing financial condition, he can take on a certain amount of risk. Also, Tom wants to consume immediately. In that sense, an income fund seems attractive. He could obviously use the current income such a fund can provide. Although he seems financially capable of assuming increased risk to generate a higher return, he has also stated that he “intends to be around for a long time.” Therefore, preservation of capital would seem to be another of Tom’s objectives. As a result, he might also consider a money market fund, or perhaps an intermediate-term bond fund. The choice will boil down to Tom’s greatest need; or perhaps he can invest in both.

Learning Outcome: Discuss the variety of investment objectivesb. What factors in Tom's situation should be taken into consideration in the fund selection process? How might these affect Tom's course of action?The factors that must be taken into consideration are (1) Tom’s existing wealth level, (2) his ability to take on risk, (3) his demand for current income, and (4) his desire for capital preservation. These considerations will clearly dictate the kind of mutual fund Tom should select. His demand for current income and his desire for preservation of capital should be paramount in the selection process. He is financially well off; he has no children and is a widower, so he can afford to take some risk. But he is also in his retirement years, and he knows the importance of capital preservation. Taxes are not an issue, so he should avoid municipal bond funds and similar tax-sheltered funds.Some viable investment candidates could include one or more of the following: high-yield money funds for yield and capital preservation; corporate bond funds that invest heavily in A– and Baa–rated issues for high yield (note that extensive portfolio diversification would be essential to keep risk to a minimum); government bond funds with intermediate (three- to ten-year) maturities for safety, yield, and preservation of capital; or possibly even equity-income funds, which could provide not only current income but also some capital appreciation for the long-haul. However, Tom should

- 36 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

understand that this option could involve some periodic/short-term sacrifice of his capital preservation goal.

Learning Outcome: Discuss the investor services offered by mutual fundsc. What types of services do you think he should look for in a mutual fund?Tom is clearly not in need of any savings plan. He already has a considerable amount of savings and is able to manage things well on his own. What he needs is a withdrawal plan because Tom would like to receive the income periodically and at regular intervals. There are several popular variations of withdrawal plans, and he should pick the one that best suits his needs. Since Tom would like to receive $1,000–$1,500 monthly, he should initiate a fixed dollar amount withdrawal plan. A conversion privilege would also be a plus.

Learning Outcome: Identify the sources of return and compute the rate of returnd. Assume Tom invests in a mutual fund that earns about 10% annually from dividend income and capital gains. Given that Tom wants to receive $1,000 to $1,500 a month from his mutual fund, what would be the size of his investment account 5 years from now? How large would the account be if the fund earned 15% on average and everything else remained the same? How important is the fund's rate of return to Tom's investment situation? Explain. Fund earns 12 percent: Starting balance is $100,000. At the end of the first year, this would be worth $100,000 ´ 1.10 = $110,000. Let us assume (for ease of calculation) that Tom withdraws $15,000 per year at the end of each year and compute the value after he makes his fifth withdrawal:Year Initial Sum Ending

SumLess Annual Withdrawal

Balance

1 100000*1.10 = 110000 - 15000 = 950002 95000*1.10 = 104500 - 15000 = 895003 91400*1.10 = 98450 - 15000 = 834504 83450*1.10 = 91795 - 15000 = 767955 76795*1.10 = 84474 - 15000 = 69474Thus, at a 10% earning rate, the value of his $100,000 investment will steadily decline to $69,474 by the end of the 5th year. The reason for this is simple: he’s taking out more than he’s earning. This will eventually result in total capital consumption, something Tom would like to avoid. Obviously, the earning rate is important to the preservation of capital—in fact, the only way to avoid depletion of capital in this case is to invest in a fund earning at least 15 percent. Such a rate will yield $15,000 a year from a $100,000 investment. Short of this (i.e., finding a fund that yields 15%), Tom has three choices:(1) accept the fact that his capital will decline over time.(2) reduce the size of his withdrawals to something closer to the earning rate on the fund (e.g., to $10,000 per year from a fund that earns 10%); or(3) increase the size of the initial investment so the annual pay-off is closer to his needs—e.g., he would have to invest $150,000 to receive $15,000 per year from a fund that earns 10%.

- 37 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

== Tutorial 7 (Topic 6) ==

Learning Outcome: Explain what is asset allocation13.3 What is asset allocation? How does it differ from diversification? What

role does asset allocation play in constructing an investment portfolio?Asset allocation is the process of dividing a portfolio into various asset classes to preserve capital by protecting against negative developments while taking advantage of positive ones.It is based on the belief that the total return of a portfolio is influenced more by the way investments are allocated than by the actual investments.Asset allocation has a much greater impact on reducing total risk exposure than picking an investment vehicle in any single category (diversification)

For example, you may allocate 60% of your savings in common stock and 40% in bonds.

Learning Outcome: Explain Sharpe, Treynor, and Jensen measures13.17 Briefly describe each of the following return measures available for

assessing portfolio performance, and explain how they are used.

(a) Sharpe’s measure

(b) Treynor’s measure

(c) Jensen’s measure

- 38 -

FACULTY OF ENGINEERING AND SCIENCEUKFF3283 PORTFOLIO MANAGEMENT

Learning Outcome: Discuss portfolio revision13.19 Explain the role of portfolio revision in the process of managing a