Portfolio Theory Capital Asset Pricing Model and Arbitrage Pricing Theory.

19

Portfolio Theory Capital Asset Pricing Model and Arbitrage Pricing Theory

-

Upload

augustus-foster -

Category

Documents

-

view

265 -

download

2

Transcript of Portfolio Theory Capital Asset Pricing Model and Arbitrage Pricing Theory.

Portfolio Theory

Capital Asset Pricing Model and Arbitrage Pricing Theory

Contribution of MPT

Establish diversifiable versus nondiversifiable risks

Quantify diversifiable and nondiversifiable risk

Market Equilibrium Condition

Law of one pricePrice of risk = Reward-to-risk ratioFor well diversified portfolios, the only

remaining risks are systematic riskHence,

j Fi F

i j

r rr r

CAPM

Assumptions (see recommended textbook)The Equilibrium World

– The Market Portfolio is the Optimal Risky Portfolio

– the Capital Market Line is the Optimal CAL

The Separation Theorem– aka Mutual Fund Theorem

Market Risk Premium

Market Risk Premium: rM - rf = A 2M

– depends on aggregate investors’ risk aversion (A)– and market’s volatility (2

M)Historically:

– rM - rf = 12.5% - 3.76% = 8.74%– M = 20.39%– 2

M = 0.20392 = 0.0416 Implying an average investor has:

– A = 2.1

Reward and Risk in CAPM

Reward– Risk Premium: [E(ri) - rF]

Risk– Systematic Risk: i = iM/M

2

Ratio of Risk Premium to Systematic Risk= [E(ri) - rF] / i

Equilibrium in a CAPM World

This condition must apply to all assets, including the market portfolio

Define M = 1CAPM equation:E(ri) = rF + i x [E(rM) - rF]

( )( ) j Fi F

i j

E r rE r r

Systematic Risk of a Portfolio

Systematic Risk of a Portfolio is a weighted average

= wi i

The Security Market Line

The Security Market Line (SML)– return-beta () relationship for individual

securities

The Capital Market(Allocation) Line (CML/CAL)– return-standard deviation relationship for

efficient portfolios

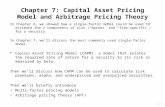

Security Market Line (SML)

0%

5%

10%

15%

20%

25%

0.0 0.5 1.0 1.5 2.0 2.5

beta ()

Exp

ecte

d R

etu

rn

MStock i

SML

rf=7%

Market Risk premium=8%

Uses of CAPM

BenchmarkingCapital BudgetingRegulation

CAPM and Index Models

Index models - uses actual portfoliosTest for mean-variance efficiency of the

indexBad index or bad model?

Security Characteristic Line (SCL) (A Scatter Diagram)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

-15% -10% -5% 0% 5% 10% 15%

Market Excess Return (RM)

Sto

ck's

Excess R

etu

rn (

R i)

= -0.0006

= 1.0177

= 0.5715

Estimating Beta

Past does not always predict the futureRegression toward the meanIs Beta and CAPM dead?

Arbitrage Pricing Theory (APT)

Assumption– Risk-free arbitrage cannot exist in an efficient

market– Arbitrage

• A zero-investment portfolio with sure profit– e.g. violation of law of one price

APT Equilibrium Condition

Law of One PriceIf two portfolios, A and B, both only have

one systematic factor (k),

, ,

A F B F

k A k B

r r r r

There can be many risk factors. The equilibrium condition holds for each risk factor.

APT example

Economy Stock A Stock BGood 10% 12%Bad 5% 6%

Stock A sells for $10 per share Stock B sells for $50 per share Arbitrage strategy

– Short sell 500 shares of stock A ($5000)– Buy 100 shares of stock B ($5000)

• Net investment = $5000 - $5000 = $0

Arbitrage returnEconomy PortfolioGood -500+600 = 100 =2%Bad -250+300 = 50 = 1%

Multi-factor Models

Factor Portfolio (RMK)

– A well-diversified portfolio with beta=1 on one factor and beta=0 on any other factor

Ri = rfi + i1RM1 + i2RM2 + ei

– rfi is the risk-free rate

– RM1 is the excess return on factor portfolio 1

– RM2 is the excess return on factor portfolio 2

Summary

CAPM– Empirical application of CAPM needs a proxy for the

market portfolio– Empirical evidence lacks support

• Could be due to poor proxy or poor model

APT– Difficult to apply empirically– The model does not identify systematic risk factors

Empirical Models– Lacks economic intuition– E.g. Market-to-book ratio as a systematic risk factor