Portfolio Management Prof. Ian Giddy New York University Stern School of Business.

47

Portfolio Management Prof. Ian Giddy New York University New York University Stern School of Business

-

Upload

candace-alexander -

Category

Documents

-

view

219 -

download

2

Transcript of Portfolio Management Prof. Ian Giddy New York University Stern School of Business.

Portfolio Management

Prof. Ian GiddyNew York University

New York University

Stern School of Business

Copyright ©1998 Ian H. Giddy Portfolio Management 2

Agenda

How to evaluate portfolio performance What portfolio theory tells us

How to put stocks or funds that outperform the market into your “active” portfolio

Copyright ©1998 Ian H. Giddy Portfolio Management 3

Performance evaluation: “the science of attribution”

Example: Why did this taxi take so long?The traffic; the driver; my lousy

instructions? How much should I tip this taxi

driver? Would I use this taxi company

again?

Why Measure Performance?

Copyright ©1998 Ian H. Giddy Portfolio Management 4

Portfolio Performance Evaluation

How well did the portfolio do? How do we adjust for risk, to compare

different managers? Why?

RiskTimingAsset allocationSecurity selection

Copyright ©1998 Ian H. Giddy Portfolio Management 5

Abnormal Performance

What is abnormal?

Performance can be measured against: Benchmark portfolio Market adjusted Market model / index model adjusted Reward to risk measures such as the Sharpe

measure:E (rp-rf) / p

Copyright ©1998 Ian H. Giddy Portfolio Management 6

Performance Evaluation Issues

Theoretically correct measures are difficult to construct

Different statistics or measures are appropriate for different types of investment decisions or portfolios

Many industry and academic measures are different

The nature of active management leads to measurement problems

Copyright ©1998 Ian H. Giddy Portfolio Management 7

Measuring Portfolio Returns

Dollar-weighted return (IRR)

vs Time-weighted return

Arithmetic average

vs Geometric average

Copyright ©1998 Ian H. Giddy Portfolio Management 8

Performance Evaluation Measures

Sharpe’s measureThe portfolio’s average excess return per unit of total risk

Treynor’s measureThe portfolio’s average excess return per unit of systematic

risk

Jensen’s measureThe excess of the portfolio’s return over that predicted by the

CAPM

Appraisal ratioPortfolio’s abnormal return per unit of risk that could be

diversified by holding a market index portfolio

Copyright ©1998 Ian H. Giddy Portfolio Management 9

Performance Evaluation Measures

Sharpe’s measure

Treynor’s measure

Jensen’s measure

Appraisal ratio

( ) /r rP f P

( ) /r rP f P

P r r r rP f P M f [ ( )]

( / ( ) P Pe

Copyright ©1998 Ian H. Giddy Portfolio Management 10

Risk Adjusted Performance: Sharpe

1) Sharpe Index

rp = Average return on the portfolio

rf = Average risk free rate

p= Standard deviation of portfolio

return

( ) /r rP f P

Copyright ©1998 Ian H. Giddy Portfolio Management 11

Risk Adjusted Performance: Treynor

2) Treynor Measure

rp = Average return on the portfolio

rf = Average risk free rate

ßp = Weighted average for portfolio

( ) /r rP f P

Copyright ©1998 Ian H. Giddy Portfolio Management 12

3) 3) Jensen’s Measure

p = Alpha for the portfolio

rrpp = Average return on the portfolio

ßßpp = Weighted average Beta

rrff = Average risk free rate

rrmm = Avg. return on market index port.

Risk Adjusted Performance: Jensen

P r r r rP f P M f [ ( )]

Copyright ©1998 Ian H. Giddy Portfolio Management 13

Which Measure is Appropriate?

It depends on investment assumptions

1) If the portfolio represents the entire investment for an individual, Sharpe Index compared to the Sharpe Index for the market.

2) If many alternatives are possible, use the Jensen or the Treynor measure

The Treynor measure is more complete because it adjusts for risk

Copyright ©1998 Ian H. Giddy Portfolio Management 14

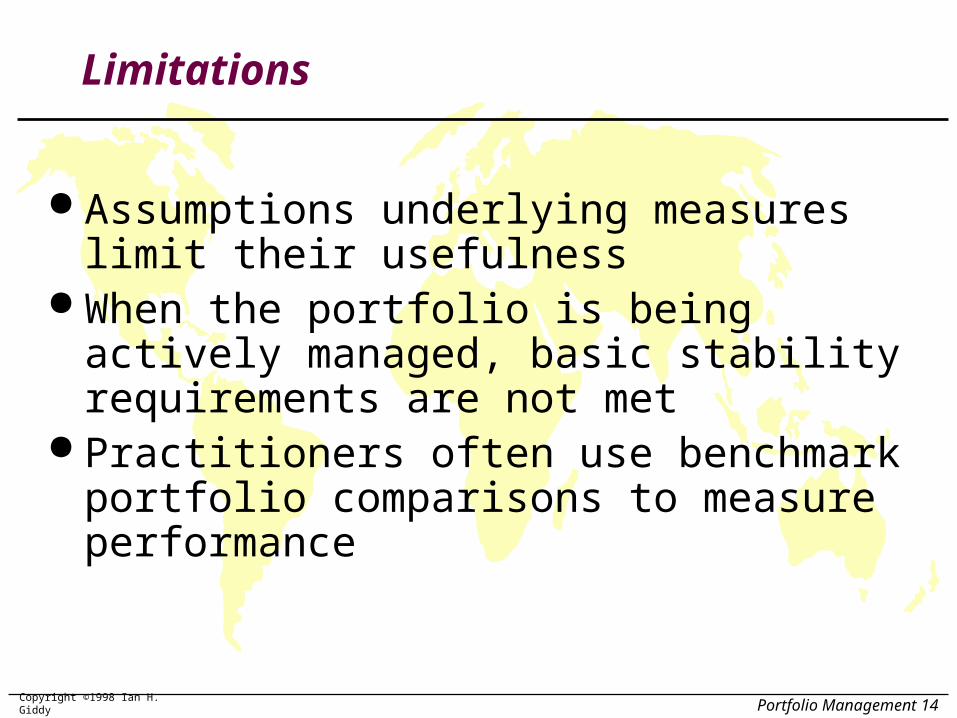

Limitations

Assumptions underlying measures limit their usefulness

When the portfolio is being actively managed, basic stability requirements are not met

Practitioners often use benchmark portfolio comparisons to measure performance

Copyright ©1998 Ian H. Giddy Portfolio Management 15

Factors That Lead to Abnormal Performance

Market timing Superior selection

Sectors or industriesIndividual companies

Copyright ©1998 Ian H. Giddy Portfolio Management 16

Performance Attribution

Decomposing overall performance into components

Components are related to specific elements of performance

Example componentsBroad AllocationIndustrySecurity ChoiceUp and Down Markets

Copyright ©1998 Ian H. Giddy Portfolio Management 17

Performance Attribution

Asset allocation choicesBroad market allocations: equity, bonds,

etc.Industry choicesSecurity selection

Evaluation: compare the portfolio returns at each level with returns on the appropriate index (benchmark portfolio or passive strategy)

Copyright ©1998 Ian H. Giddy Portfolio Management 18

Process of Attributing Performance to Components

Set up a ‘Benchmark’ or ‘Bogey’ portfolio Use indexes for each component Use target weight structure

Copyright ©1998 Ian H. Giddy Portfolio Management 19

Calculate the return on the ‘Bogey’ and on the managed portfolio

Explain the difference in return based on component weights or selection

Summarize the performance differences into appropriate categories

Process of Attributing Performance to Components

Copyright ©1998 Ian H. Giddy Portfolio Management 20

Performance Attribution:1. Excess Return

Excess Return: Managed Portfolio vs Benchmark

ComponentBenchmark Weight

Return of Index during Period Performance

Equity (FUSEX) 60% 5.81% 3.49%Bonds (VUSTX) 30% 1.45% 0.44%Cash 10% 0.48% 0.05%

Bogey (Benchmark Portfolio) Return 3.97%Return of Managed Portfolio 5.34%Excess return of managed portfolio 1.37%

Copyright ©1998 Ian H. Giddy Portfolio Management 21

Performance Attribution:2. Asset Allocation

Contribution of Asset Allocation to Performance

(1) (2) (3) (4) (3)x(4)

Component

Managed Portfolio Weights

Benchmark Portfolio Weights

Excess Weight

Component Return minus Total Benchmark Return

Contribution to Performance

Equity 70% 60% 10% 1.84% 0.184%Bonds 7% 30% -23% -2.52% 0.579%Cash 23% 10% 13% -3.49% -0.454%

Contribution of Asset Allocation 0.310%

Copyright ©1998 Ian H. Giddy Portfolio Management 22

Performance Attribution:3. Security Selection

Contribution of Security Selection to Performance

(1) (2) (3) (4) (3)x(4)

Component

Managed Portfolio Performance

Component Index Performance

Excess Performance

Managed Portfolio Weight

Contribution to Performance

Equity 7.28% 5.81% 1.47% 70.00% 1.029%Bonds 1.89% 1.45% 0.44% 7.00% 0.031%Cash 0.48% 0.48% 0.00% 23.00% 0.000%

Contribution of Security Selection 1.060%

Copyright ©1998 Ian H. Giddy Portfolio Management 23

Performance Attribution:4. Summary

Portfolio Attribution Summary

Contribution1 Asset Allocation 0.310%2 Selection

1 Equity excess return 1.029%2 Bonds excess return 0.031%3 Cash excess return 0.000% 1.060%

Total excess return on portfolio 1.370%

Portfolio Attribution Summary

Contribution1 Asset Allocation 0.310%2 Selection

1 Equity excess return 1.029%2 Bonds excess return 0.031%3 Cash excess return 0.000% 1.060%

Total excess return on portfolio 1.370%

Source: http://www.stern.nyu.edu/~igiddy/performance.xls

Copyright ©1998 Ian H. Giddy Portfolio Management 24

Active Portfolio Management

Stock-picking and active portfolio management must pay, else the market would not be efficient!

The optimal risky portfolio maximizes the reward-to-variability ratio; the slope of the CAL:

PASSIVE

CAPITAL ALLOCATON LINE

ACTIVE

CAPITAL ALLOCATON LINEE(rp)

Copyright ©1998 Ian H. Giddy Portfolio Management 25

Lure of Active Management

Are markets totally efficient? Some managers outperform the market for extended

periods While the abnormal performance may not be too

large, it is too large to be attributed solely to noise Evidence of anomalies such as the turn of the year

exist

The evidence suggests that there is some role for active management

Copyright ©1998 Ian H. Giddy Portfolio Management 26

Market Timing

Adjusting portfolio for up and down movements in the market

Low Market Return - low ßeta High Market Return - high ßeta

Copyright ©1998 Ian H. Giddy Portfolio Management 27

Market Timing

Adjust the portfolio for movements in the market

Shift between stocks and money market instruments or bonds

Results: higher returns, lower risk (downside is eliminated)

With perfect ability to forecast behaves like an option

Copyright ©1998 Ian H. Giddy Portfolio Management 28

Example of Market Timing

**

****

**

**

**

**

**

**

****

****

******

******

****

****

rrpp - r - rff

rrmm - r - rff

Steadily Increasing the BetaSteadily Increasing the Beta

Copyright ©1998 Ian H. Giddy Portfolio Management 29

Market Timing: An Option on the S&P

Value of perfect timing is a call option worth C

Timing ability measured by PBull+ PBear-1

Value of timing ability is (PBull+ PBear -1)C

P = the proportion of correct forecasts

rf

rfrM

Copyright ©1998 Ian H. Giddy Portfolio Management 30

rrff

rrff

rrMM

Rate of Return of a Perfect Market Timer

Copyright ©1998 Ian H. Giddy Portfolio Management 31

YearYear7171727273737474757576767777787879798080

Stock Ret.Stock Ret..1431 .1431 .1898 .1898

-.1466 -.1466 -.2647 -.2647 .3720 .3720 .2384 .2384

-.0718 -.0718 .0656 .0656 .1844 .1844 .3242 .3242

T-Bill RetT-Bill Ret.0439.0439.0384.0384.0693.0693.0800.0800.0580.0580.0508.0508.0512.0512.0718.0718.1038.1038.1124.1124

Avg. Ret.Avg. Ret.S.D. Ret.S.D. Ret.

.1034.1034

.2068.2068.0680.0680.0248.0248

Returns on Stocks and Bills

Copyright ©1998 Ian H. Giddy Portfolio Management 32

With Perfect Forecasting Ability

Switch to T-Bills in ‘73, ‘74, ‘77, ‘78 No negative returns or losses Average Ret. = .1724 S.D. Ret. = .1118 Results with perfect timing

70% increase in mean return46% lower S.D.

Copyright ©1998 Ian H. Giddy Portfolio Management 33

With Imperfect Ability to Forecast

Long horizon to judge the ability Judge proportions of correct calls Bull markets and bear market calls

Copyright ©1998 Ian H. Giddy Portfolio Management 34

Conclusion: Hold Three Things

Risk-free asset Passive portfolio Active portfolio

Copyright ©1998 Ian H. Giddy Portfolio Management 35

Superior Selection Ability

Concentrate funds in undervalued stocks or undervalued sectors or industries

Balance funds in an active portfolio and in a passive portfolio

Active selection will mean some unsystematic risk

Copyright ©1998 Ian H. Giddy Portfolio Management 36

Sharpe’s Ratio

PASSIVE CAL

ACTIVE CALE(rp)

SE r rP f

P

( )

Used to guage performance of professional portfolios

Copyright ©1998 Ian H. Giddy Portfolio Management 37

Treynor-Black Model

Model used to combine actively managed stocks with a passively managed portfolio

Using a reward-to-risk measure that is similar to the the Sharpe Measure, the optimal combination of active and passive portfolios can be determined

Copyright ©1998 Ian H. Giddy Portfolio Management 38

Security Selection

Alpha is the expected return on a security above that explained by its beta and the security market line:

Treynor-Black model says weight of each security should be based on ratio of its mispricing to its nonsystematic risk:

r r r r ei i f i M f i ( )

i

i ie2 ( )

Copyright ©1998 Ian H. Giddy Portfolio Management 39

Treynor-Black Model: Assumptions

Analysts will have a limited ability to find a select number of undervalued securities

Portfolio managers can estimate the expected return and risk, and the abnormal performance for the actively-managed portfolio

Portfolio managers can estimate the expected risk and return parameters for a broad market (passively managed) portfolio

Copyright ©1998 Ian H. Giddy Portfolio Management 40

Reward to Variability Measures

Passive Portfolio Passive Portfolio ::

S2m = [E(rm) - rf

m]2

Copyright ©1998 Ian H. Giddy Portfolio Management 41

Appraisal RatioAppraisal Ratio

AA

AA = Alpha for the active portfolio= Alpha for the active portfolio

(ep)

(Ap)(Ap) = Unsystematic standard= Unsystematic standard deviation for activedeviation for active

Reward to Variability Measures

Copyright ©1998 Ian H. Giddy Portfolio Management 42

Reward to Variability Measures

Combined Portfolio Combined Portfolio ::

S2p = [E(rm) - rf

m

]2 + eA

[ A]

2

Copyright ©1998 Ian H. Giddy Portfolio Management 43

Market Portfolio

Active Portfolio

E(r)E(r)

CMLCMLCALCAL

Rf

Treynor-Black Allocation

Optimal Portfolio

Copyright ©1998 Ian H. Giddy Portfolio Management 44

Implementing the Treynor-Black Approach

Use passive portfolio (index fund) as baseline; find its E(rM) and E(VarM)

Analyze a few securities; find mispriced ones

For each security, use estimates of Alpha, Beta and residual risk to determine optimum weights

Determine optimal weights for active and passive portfolios

Copyright ©1998 Ian H. Giddy Portfolio Management 45

Summary Points: Treynor-Black Model

Sharpe Measure will increase with added ability to pick stocks

Slope of CAL>CML

(rp-rf)/p > (rm-rf)/p

P is the portfolio that combines the passively managed portfolio with the actively managed portfolio

The combined efficient frontier has a higher return for the same level of risk

Copyright ©1998 Ian H. Giddy Portfolio Management 46

Summary

How to evaluate portfolio performance How to put stocks or funds that

outperform the market into your “active” portfolio

Portfolio theory helps construct the right active/passive/riskfree mix.

Copyright ©1998 Ian H. Giddy Portfolio Management 50

Ian Giddy

Ian H. Giddy

NYU Stern School of Business

Tel 212-998-0332; Fax 212-995-4233

http://giddy.org