Popcash Research Report: Payday Loans, Debt Culture and Banks

41

FUTUREGOV Research Summary & Product Definition Promoting financial resilience and preventing crises debt in Lewes District and Eastbourne

description

http://popcashapp.com Popcash is a mobile and web-based app designed to encourage financial confidence, Popcash clarifies your financial landscape and puts you in control of your money, helping you stop late payments, overspending and unwanted charges.

Transcript of Popcash Research Report: Payday Loans, Debt Culture and Banks

FUTUREGOV

Research Summary & Product Definition

Promoting financial resilience and preventing crises debtin Lewes District and Eastbourne

By the time people get to me they are already desperate. It’s about

prevention. It’s about getting that message across and how you do

that. It’s also about having a point of contact.

(Councillor, Lewes)

© FutureGov 2014

Project TeamProject Team

Contact

FutureGov:Project Sponsor: Dominic CampbellProject Managers: Amanda Gore, Zoë BiermanHead of Delivery: Tim FowlerDesign Lead: Harriet McDougallProduct Developer: Ben AshmanResearch: Kieran Dhillon, Tom Tobia, Amanda Gore, Harriet McDougall

Eastbourne:Project Sponsor: Pat TaylorDebt Consultants: John Nelson, Andi Edwards

[email protected]@[email protected]

The Lewes & Eastbourne LAB

The Lab is an Innovation Space for Lewes District and Eastbourne Borough Council, working with the councils and other service providers to develop and test new ideas for improving financial resilience in the area.

http://www.leweslab.org/

Contents

1 An Introduction3 Financial resilience in Lewes District4 Thefirstdesignbrief5 Research methods and approach6 Headline lessons about credit unions8 Credit union loan approval service map10 Key lessons: payday loans, debt culture and banks12 Acommontaleofdebt-catalystsandbehaviours14 Thenewdesignbrief15 Principlesofamoneymanagementtool16 Whoistheproductfor?17 Jamie-youngprofessional18 Roxanne-indebtedmother19 Lesley-incapacityclaimant20 Mobilefirstanddigitalinclusivity21 HowdoesPopcashwork?22 Needsweidentified...23 ...andhowPopcashcanmeetthem24 IntroducingPopcash-featureslist25 Contact details25 Appendix

© FutureGov 2014

My older boy says to me ‘how are you going to pay for food mum?’.

He’s 10 and already worrying about bills. He goes out and earns

pocket money at my mum’s house, he gives it to me. He shouldn’t have

to do that at 10. That’s what it’s like.

(Ella, 34, Lewes)

© FutureGov 2014

1© FutureGov 2014 © FutureGov 2014

An Introduction

Thecostoflivingisrising;incomesarestagnatingorfallingandbenefitsaregettingcut.Thenumberofpeopleand households likely to encounter difficultiesissignificant.

A Resolution Foundation* report suggeststhattwothirdsofthoseonlow-to-middleincomesarestrugglingtokeepupwithbillsorfallingbehind.Aquarter are unable to replace or repair brokenelectricalgoods.

As the recession bites, there’s a growing needforwaysofsupportingmanagementofpersonalfinance.

This means equipping those most at risk

ofdebttomakeproactive,responsiblefinancialdecisions.Enhancingrelationshipswithproviders(eg.councils,sociallandlords,creditunions),iskeytofosteringacultureoftrustandrespect.

Popcashisamobileandweb-basedappdesignedtoencouragefinancialconfidenceandcontrol.Itgivesclaritytofinancesbymanaging essential outgoings, encouraging proactive budgeting action and prompting userstoseekhelpfromtherightplacesatthefirstsignsoftrouble.

Bornoutofextensiveresearchintotheriseofshort-term,highinterestloancultureandfinancialvulnerability,Popcashaimstopreventthoseatriskofproblemdebtfromfallingintocommontraps:latepaymentcharges,overspending,andavoidance.

Executive Summary What is a Product Definition?

This document is a comprehensive overviewofthePopcashresearchprojectandtheresultingproduct.

It’spurposeittotogivea360ºviewoftheproject,fromtheoriginalresearchconductedandconceptionoftheidea, right through to the concluding productspecification.It’sgoalisto provide clarity around decisions takenbytheprojectteam,featuresofthefinalproductandplansforimplementationandscaling.

*Seethefullreporthere:www.resolutionfoundation.org/publications/state-living-standards/

That’s the thing, I think they’re meant to be doing that benefit

cut thing soon for certain families but how are people going to

survive? If it were me, I’d do all my food shopping and that first

before I pay any bills. A lot of people are going to be evicted.

(Leo, Eastbourne resident)

© FutureGov 2014

3© FutureGov 2014

Inthecontextofpublicsectorcutsandwelfarereforms,it’sbecomingclearthatthefinancialresilienceoflowincomehouseholdshasdecreased.

Research began working alongside LewesDistrictCouncil;lookingathowthey and their partners might be able to help people who are struggling financially,particularlyinthelightofupcomingwelfarechanges.

Ourconversationsconfirmedexpectations about what people were struggling with – household costs, little capacity to deal with unanticipated costs or events such as their cars breaking down, increasing debt, findingfulfillingwork.Thelistofwhatpeople are struggling with is mostly as expected, but the research was revealingintermsofhowpeoplemightbebestsupported.

Financial resilience in Lewes District

Too little, too lateAlthoughtherewasmuchpraiseforsupport services in Lewes, we also heard repeatedtalesofpeopleaccessingformalsupport ‘too late’, where crisis could have beenavertedifonlypeoplehadsoughtouthelpearlier.

Emotional supportAnd yet when we spoke to people about howtheyfeltwhentheybegantostrugglefinancially,weheardthemexpressarangeofemotions–falseoptimism,denial,pride,shameandstigma.Emotionally,theyarenot always in a place where they are ready togooutandseekformalsupportand

they’lloftenturntomoreinformalsupportnetworks–familyandfriends–first.

Offer a kind handThese insights into people’s experiences raised questions about how support could bebestprovidedandledustoasetofprinciples that underpinned our solutions: Design‘soft’(or,sensitive) solutions that incorporate how people feel andfindwaysof reaching people, rather than expectingthemtocomeandfindservices.

Youcanseetheintial‘BeyondBenefits’reportandreadKiranDhillon’ssummaryofit’sfindings here.

Important lessons from first-stage research

Design ‘soft’ solutions that incorporate how people feel and find ways of reaching people, rather than expecting them to come and find services.

After the first-stage research,

we started work on a concept

for a mobile product that would

encourage people to access low

interest loans from responsible

lenders, such as credit unions, to

rival high-interest payday lenders.

The first design brief

© FutureGov 2014

5© FutureGov 2014

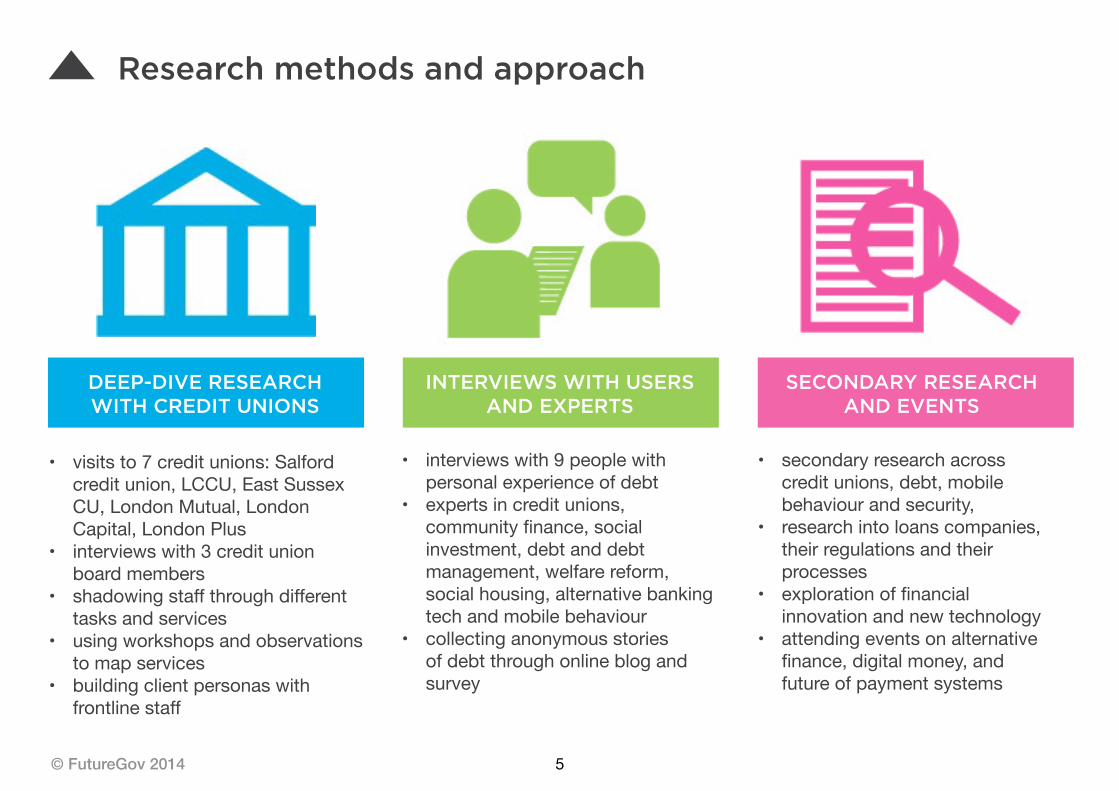

Research methods and approach

• interviews with 9 people with personalexperienceofdebt

• experts in credit unions, communityfinance,socialinvestment, debt and debt management,welfarereform,social housing, alternative banking tech and mobile behaviour

• collecting anonymous stories ofdebtthroughonlineblogandsurvey

INTERVIEWS WITH USERS AND EXPERTS

• secondary research across credit unions, debt, mobile behaviour and security,

• research into loans companies, their regulations and their processes

• explorationoffinancialinnovation and new technology

• attending events on alternative finance,digitalmoney,andfutureofpaymentsystems

SECONDARY RESEARCH AND EVENTS

• visitsto7creditunions:Salfordcredit union, LCCU, East Sussex CU, London Mutual, London Capital, London Plus

• interviews with 3 credit union board members

• shadowingstaffthroughdifferenttasks and services

• using workshops and observations to map services

• building client personas with frontlinestaff

DEEP-DIVE RESEARCH WITH CREDIT UNIONS

6© FutureGov 2014

Headline lessons about credit unions

Big changes on the horizonThelandscapeisshiftngforCreditUnions;changinglegislation,consolidationandon-goingmodernisation programmes (such as ABCUL initiative) mean they’ll be experiencing a state of fluxforatleastthenext18-24months.

Saving and membership are turn-offsCreditUnionsaresetuptoencouragesavingbeforeloans are made, something many payday loan users do not want,insteadlookingforimmediateaccesstocash.

Credit Unions don’t like Payday loansBecause the public are so used to the payday loans model, and CUs can massively undercut thecompetitions’highratesofAPRwhilstalsosupporting saving, we came at the research with the assumption that helping Credit Unions get into the paydayloanmarketwouldbeabeneficialstep.However,creditunionshaveverydifferentviewsonpaydayloans,withmanyfeelingthatthe model behind fast repayments goes against their ethos toteachresponsiblefinancialbehaviour.Severaltoldustheywouldprefertogivelargeramountsofmoneyoverlongerperiodsoftime.

Payday loans aren’t financially viable DuetothecurrentAPRcapof26.8%,Credit Unions make a loss on servicing small loan amounts.Onaloanof£300foronemonththeycanonlychargeamaximum£6interest.

Lack of identity and visabilityCredit Unions have a big image problem: Many people are unaware of Credit Unions, and those thatareoftenthinkofthemasa’poormansbank’.Thisiscompoundedbythelookandfeel,bothon the ground and online, with no coherent brand identity and very limited marketing materials, dependent on each Credit Unions available budget andstaffexpertise.

Out-dated, disparate systems and ITTechnologically,theback-endsystemsusedbytheCUs we spoke to varied dramatically, meaning a digital product could not be easily designed for use across unions.Wecameacrossthreedifferenttypesofsoftwareimplemented,allofwhichwereoriginallydevelopedover30yearsago.Morethanonereliedonpaperwork-and-filingsystemsinplaceofITsystems.

There are many issues which would make working with Credit Unions difficult

WedelvedintotheworldofCreditUnions,personalfinance,andmoneymanagementto get to grips with where the real problems lay,andidentifywhatanaccessibleandusefulmobileproducttosupportthiscouldlooklike.

We spent time with Credit Union staff,membersandboardmembers,collatedpeople’sstoriesofdebt,metwithandinterviewedanumberofexpertsincommunityfinance,debtanddebtmanagement,welfarereform,social housing and alternative banking technology, and immersed ourselves in the mostrecentliteraturewecouldfind.

Our headline discoveries made us question ifworkingwithcreditunionswasafeasibleoption,andhelpedustoseeamoredetailedpictureofthewiderculturaland behavioural issues which can be the catalystsforproblemdebt.

Interrogating the brief

These findings made it clear that it was not going to be possible to create an app which would be compatible with credit unions yet. They are still dealing with problems beyond the scope of influence, and as yet don’t have the capacity or financial viability to compete with payday lenders.

... you’re just thrown out into the world and you don’t know about

your tax, your P45, your P6 ... to this day I still don’t have a clue...

I was only young and dead selfish, I just spent it on other things.

I’m devastated now because think if i want to get a mortgage in

the future there’s no way I could do that so I’m gutted

(Rebecca, 20, Manchester)

© FutureGov 2014

8© FutureGov 2014

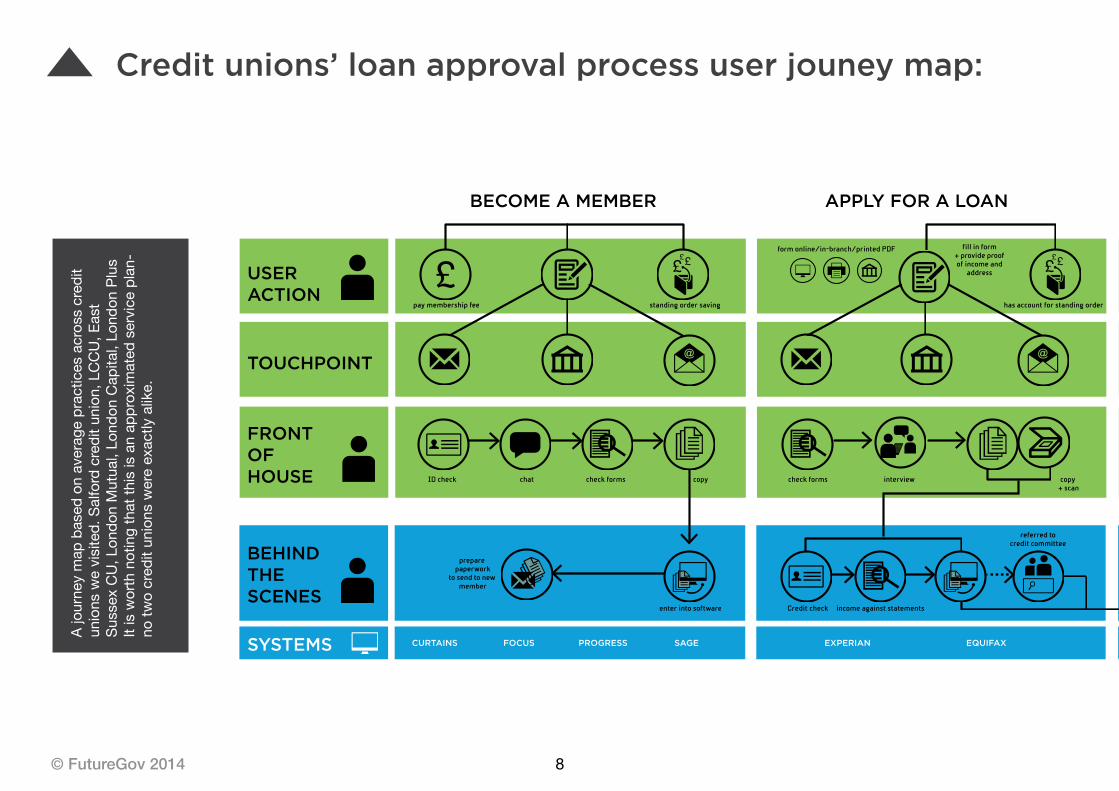

Credit unions’ loan approval process user jouney map: A

jour

ney

map

bas

ed o

n av

erag

e pr

actic

es a

cros

s cr

edit

unionswevisited.Salfordcreditu

nion

,LCCU,E

ast

Suss

ex C

U, L

ondo

n M

utua

l, Lo

ndon

Cap

ital,

Lond

on P

lus

Itisworthnotingthatth

isisanap

proximated

serviceplan-

notw

ocred

itunionswereexactlyalike.

EXPERIAN EQUIFAX BACS

BECOME A MEMBER

USERACTION

TOUCHPOINT

FRONTOFHOUSE

BEHINDTHESCENES

SYSTEMS

APPLY FOR A LOAN DECISION MADE

?

LOAN IS PAID IN LOAN IS REPAID

CURTAINS FOCUS PROGRESS SAGE CURTAINS FOCUS PROGRESS SAGE

X BACS

DWP DCA

? ?pay membership fee

ID check chat check forms check forms

Credit check income against statements transfer (60p) pre-pay card cheque (sometimes manual)decision by

credit controllerreferred to outside

agency for debt collection

standing order no payment

contact to notify

and offer advice

no response

Departmentfor

Work +Pensions

(if on benefits)

independentdebt

collectionagency

manual check

referred tocredit committee Decision to grant

loan or not

call to discuss options

letter to notify text to come in-branch letter with contract

signs loanagreement

returnsform

interview copy + scan

copy

enter into software

prepare paperwork

to send to new member

standing order saving has account for standing order

form online/in-branch/printed PDF fill in form+ provide proofof income and

address

9© FutureGov 2014

EXPERIAN EQUIFAX BACS

BECOME A MEMBER

USERACTION

TOUCHPOINT

FRONTOFHOUSE

BEHINDTHESCENES

SYSTEMS

APPLY FOR A LOAN DECISION MADE

?

LOAN IS PAID IN LOAN IS REPAID

CURTAINS FOCUS PROGRESS SAGE CURTAINS FOCUS PROGRESS SAGE

X BACS

DWP DCA

? ?pay membership fee

ID check chat check forms check forms

Credit check income against statements transfer (60p) pre-pay card cheque (sometimes manual)decision by

credit controllerreferred to outside

agency for debt collection

standing order no payment

contact to notify

and offer advice

no response

Departmentfor

Work +Pensions

(if on benefits)

independentdebt

collectionagency

manual check

referred tocredit committee Decision to grant

loan or not

call to discuss options

letter to notify text to come in-branch letter with contract

signs loanagreement

returnsform

interview copy + scan

copy

enter into software

prepare paperwork

to send to new member

standing order saving has account for standing order

form online/in-branch/printed PDF fill in form+ provide proofof income and

address

10© FutureGov 2014

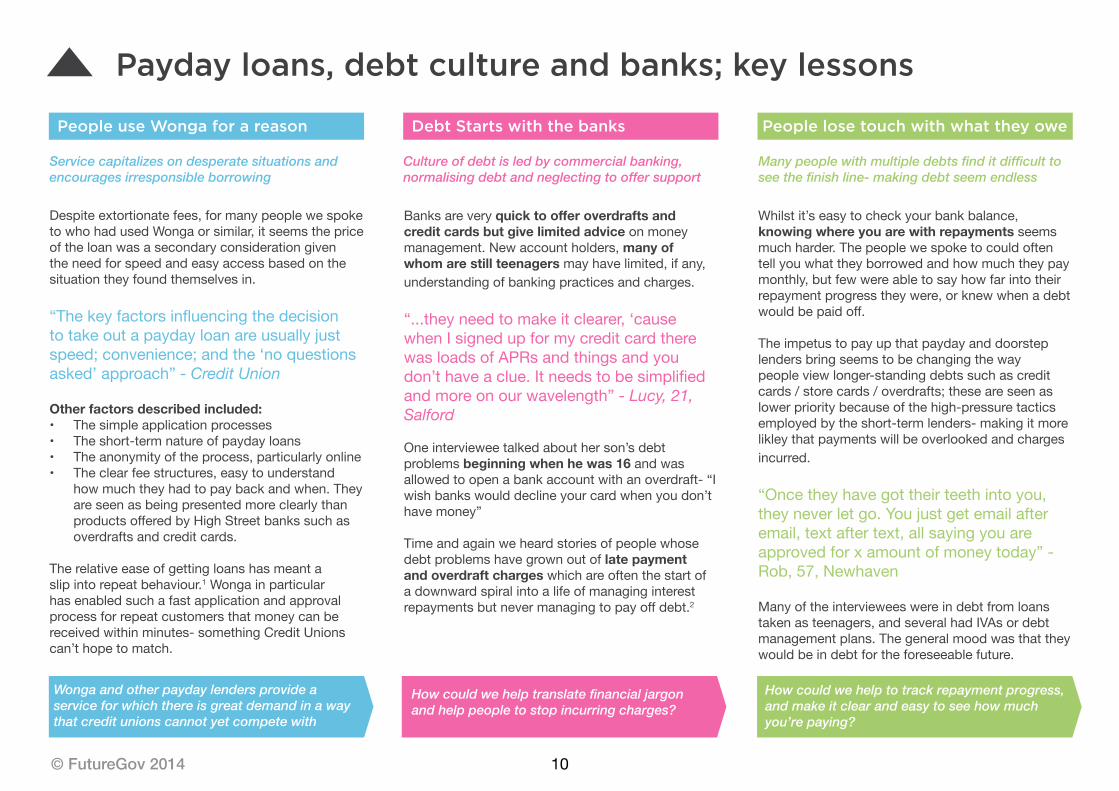

Payday loans, debt culture and banks; key lessons

Banks are very quick to offer overdrafts and credit cards but give limited advice on money management.Newaccountholders,many of whom are still teenagersmayhavelimited,ifany,understandingofbankingpracticesandcharges.

“...theyneedtomakeitclearer,‘causewhenIsignedupformycreditcardtherewasloadsofAPRsandthingsandyoudon’thaveaclue.Itneedstobesimplifiedand more on our wavelength” - Lucy, 21, Salford

One interviewee talked about her son’s debt problems beginning when he was 16 and was allowedtoopenabankaccountwithanoverdraft-“Iwish banks would decline your card when you don’t have money”

Timeandagainweheardstoriesofpeoplewhosedebtproblemshavegrownoutoflate payment and overdraft chargeswhichareoftenthestartofadownwardspiralintoalifeofmanaginginterestrepaymentsbutnevermanagingtopayoffdebt.2

Whilstitʼseasytocheckyourbankbalance, knowing where you are with repayments seems muchharder.Thepeoplewespoketocouldoftentell you what they borrowed and how much they pay monthly,butfewwereabletosayhowfarintotheirrepayment progress they were, or knew when a debt wouldbepaidoff.

The impetus to pay up that payday and doorstep lenders bring seems to be changing the way peopleviewlonger-standingdebtssuchascreditcards/storecards/overdrafts;theseareseenaslowerprioritybecauseofthehigh-pressuretacticsemployedbytheshort-termlenders-makingitmorelikley that payments will be overlooked and charges incurred.

“Once they have got their teeth into you, theyneverletgo.Youjustgetemailafteremail,textaftertext,allsayingyouareapprovedforxamountofmoneytoday”-Rob, 57, Newhaven

Manyoftheintervieweeswereindebtfromloanstaken as teenagers, and several had IVAs or debt managementplans.Thegeneralmoodwasthattheywouldbeindebtfortheforeseeablefuture.

Despiteextortionatefees,formanypeoplewespoketo who had used Wonga or similar, it seems the price oftheloanwasasecondaryconsiderationgiventheneedforspeedandeasyaccessbasedonthesituationtheyfoundthemselvesin.

“Thekeyfactorsinfluencingthedecisionto take out a payday loan are usually just speed;convenience;andthe‘noquestionsasked’ approach” - Credit Union

Other factors described included:• The simple application processes• Theshort-termnatureofpaydayloans• Theanonymityoftheprocess,particularlyonline• Theclearfeestructures,easytounderstand

howmuchtheyhadtopaybackandwhen.Theyare seen as being presented more clearly than productsofferedbyHighStreetbankssuchasoverdraftsandcreditcards.

Therelativeeaseofgettingloanshasmeantaslipintorepeatbehaviour.1 Wonga in particular hasenabledsuchafastapplicationandapprovalprocessforrepeatcustomersthatmoneycanbereceivedwithinminutes-somethingCreditUnionscan’thopetomatch.

Debt Starts with the banks People lose touch with what they owePeople use Wonga for a reason

Service capitalizes on desperate situations and encourages irresponsible borrowing

Culture of debt is led by commercial banking, normalising debt and neglecting to offer support

Many people with multiple debts find it difficult to see the finish line- making debt seem endless

Wonga and other payday lenders provide a service for which there is great demand in a way that credit unions cannot yet compete with

How could we help translate financial jargon and help people to stop incurring charges?

How could we help to track repayment progress, and make it clear and easy to see how much you’re paying?

11© FutureGov 2014

I have exhausted all possible solutions, with me taking out a loan

with my bank but unable to do so as I have consolidated my cards

etc, I pay everything on time but the amount is quite hefty (due to

me being an idiot when I was a teenager).

I pay everything on time but have a low credit score due to all of

my existing cards and I’m considering taking a loan out to pay the

debt that she owes, she [my partner] is falling apart in front of my

eyes and absolutely kills me.

(paydayidiot, on Moneysavingexpert.com’s forum)

© FutureGov 2014

12© FutureGov 2014

Aggressive marketing and questionable decisions to grant credit by mainstream lenders

Alackofunderstandingofloanterms3

Moreandmorebusinessesoffering‘buynow,paylater’andstorecreditcards.Temptationto take credit is stronger than ever

Oftenpersonisinagoodfinancialposition,thereforefeeltheycanaffordtotakealoan

Feeling that debt is normal: ‘everybody has debt’solessconcernoverapplyingforloaninfirstplace

Redundancy,illness,familybereavementandmarriagebreakdownaresomeofthemostcommoncausesofbeingpushedintodebt

Emergency repairs to a car or household implementcanalsobeexpensivepressure-pointsthatcancatchpeopleoff-guard4

Lackofsavingsputsthematsignificantrisktoa change in situation or unexpected event5

Goingintoanoverdrafttopayanunexpectedbill, or neglecting to meet a repayment installmentcanmeantheimpositionofaheftyfine

In desperation, many in this situation are temptedtoturntoalternativelinesofcreditbecause they don’t want to add to their [already substantial] outstanding debt with commercial lenders6

StudiesshowthemajorityofWonga’scustomers believe or believe that it will be a‘one-off’andtheywon’thaveaproblempayingitoffattheirnextpayday7

Key catalysts and behaviours which lead to crisis debt

Take out loans and credit from mainstream lenders

Unforeseen circumstance means a repayment is missed, incurring fines

Has to take out another loan in order to help pay off first one

13© FutureGov 2014

Pressure piles up as it becomes more and more difficult to pay bills

Begins avoiding correspondence and banking due to stress

Seeking help; needing intensive support, lack of knowledge/resource

Can get drawn in to ‘debt consolidation schemes’ by unscrupulous lenders keen to take advantage8

Mental health issues begin to develop as theyfallunderincreasingpressuretomeetrepayments and pay bills9

Fallsintodenial-believestheywillbeabletosort it out next week10

Turnstofamilyorfriendstoborrowmoneyinsteadofseekinghelpfromoutside11

Losingtrackofwhattheyowe-debtstartstoseem endless and hopeless

Latepaymentfeesbegintobuildupasavoidance means more payments are missed

Relationships begin to break down due to informaliseddebtsorthestressoffinancialburdens 12

Fallsintostateofdepressionoranxietywhichmakesitmoredifficulttoact 13

Changes phone number, stops opening letters,andbecomesafraidtoanswerthedoor 14

Begin missing out on meals or other essentials in order to meet payments 15

Unawareofwhatservicesareavailablemeanthattheythinktheydon’tqualifyorthere’snothing anyone can do to help them

Notknowingwhatbenefitsthey’reentitledto at times when they most needed bailing out-tryingtologbackdatedclaimsgetsverycomplicated 16

Financessooutofcontrolthatittakesalongtimeandalotofthesupportservicestimetobegin to help them in a tangible way 17

Fearofbeingjudgedbysupportservicesorpeersorfeelingtooembarrassedtoadmitthat they need help 18

14© FutureGov 2014

“How might we support people in

keeping on top of their bills and

repayments, and encourage them

to seek help at the first signs of

trouble?”

The new design brief

© FutureGov 2014

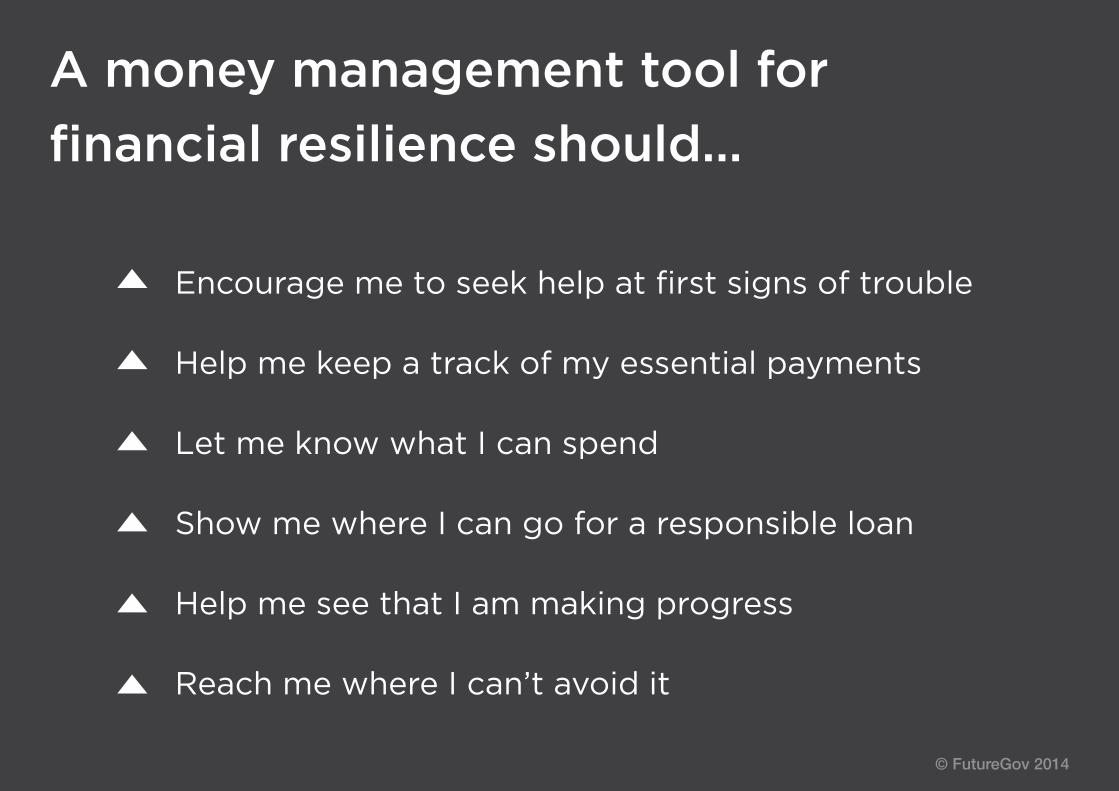

A money management tool for

financial resilience should...

Encourage me to seek help at first signs of trouble

Help me keep a track of my essential payments

Let me know what I can spend

Show me where I can go for a responsible loan

Help me see that I am making progress

Reach me where I can’t avoid it

© FutureGov 2014

16© FutureGov 2014

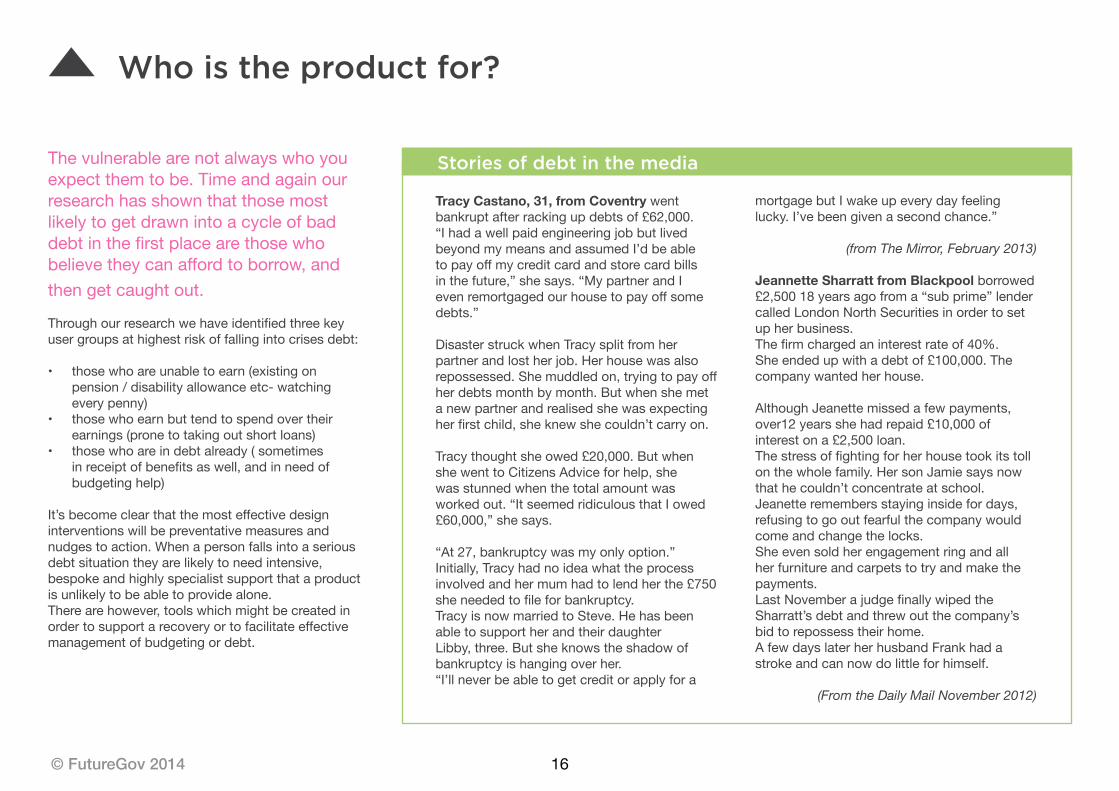

Who is the product for?

The vulnerable are not always who you expectthemtobe.Timeandagainourresearch has shown that those most likelytogetdrawnintoacycleofbaddebtinthefirstplacearethosewhobelievetheycanaffordtoborrow,andthengetcaughtout.

Throughourresearchwehaveidentifiedthreekeyusergroupsathighestriskoffallingintocrisesdebt:

• those who are unable to earn (existing on pension/disabilityallowanceetc-watchingevery penny)

• those who earn but tend to spend over their earnings (prone to taking out short loans)

• those who are in debt already ( sometimes inreceiptofbenefitsaswell,andinneedofbudgeting help)

It’sbecomeclearthatthemosteffectivedesigninterventions will be preventative measures and nudgestoaction.Whenapersonfallsintoaseriousdebt situation they are likely to need intensive, bespoke and highly specialist support that a product isunlikelytobeabletoprovidealone.There are however, tools which might be created in ordertosupportarecoveryortofacilitateeffectivemanagementofbudgetingordebt.

Tracy Castano, 31, from Coventry went bankruptafterrackingupdebtsof£62,000.“I had a well paid engineering job but lived beyond my means and assumed I’d be able topayoffmycreditcardandstorecardbillsinthefuture,”shesays.“MypartnerandIevenremortgagedourhousetopayoffsomedebts.”

DisasterstruckwhenTracysplitfromherpartnerandlostherjob.Herhousewasalsorepossessed.Shemuddledon,tryingtopayoffherdebtsmonthbymonth.Butwhenshemeta new partner and realised she was expecting herfirstchild,sheknewshecouldn’tcarryon.

Tracythoughtsheowed£20,000.ButwhenshewenttoCitizensAdviceforhelp,shewas stunned when the total amount was workedout.“ItseemedridiculousthatIowed£60,000,”shesays.

“At27,bankruptcywasmyonlyoption.”Initially, Tracy had no idea what the process involvedandhermumhadtolendherthe£750sheneededtofileforbankruptcy.TracyisnowmarriedtoSteve.Hehasbeenable to support her and their daughter Libby,three.Butsheknowstheshadowofbankruptcyishangingoverher.“I’llneverbeabletogetcreditorapplyfora

mortgagebutIwakeupeverydayfeelinglucky.I’vebeengivenasecondchance.”

(from The Mirror, February 2013)

Jeannette Sharratt from Blackpool borrowed£2,50018yearsagofroma“subprime”lendercalled London North Securities in order to set upherbusiness.Thefirmchargedaninterestrateof40%.Sheendedupwithadebtof£100,000.Thecompanywantedherhouse.

AlthoughJeanettemissedafewpayments,over12yearsshehadrepaid£10,000ofinterestona£2,500loan.Thestressoffightingforherhousetookitstollonthewholefamily.HersonJamiesaysnowthathecouldn’tconcentrateatschool.Jeanetteremembersstayinginsidefordays,refusingtogooutfearfulthecompanywouldcomeandchangethelocks.She even sold her engagement ring and allherfurnitureandcarpetstotryandmakethepayments.LastNovemberajudgefinallywipedtheSharratt’s debt and threw out the company’s bidtorepossesstheirhome.AfewdayslaterherhusbandFrankhadastrokeandcannowdolittleforhimself.

(From the Daily Mail November 2012)

Stories of debt in the media

17© FutureGov 2014

JAMIEYOUNG PROFESSIONAL

• MALE

• Big city & suburbs

• Professional

• Full-time job

• Single

• No dependents

I’m alright for money, but I don’t know much about my banking options and I tend to spend too much.

“”

HEADLINE STATMENTS:• Self-aware and keen to help himself• Struggles to budget for payments - likes to have a good time.• Impatient - short attention span• Independent of all financial support services

TOUCHPOINTS AND TECH LITERACY: Extrememly tech savvy: regular online-banking, smart phone usage every day

SPENDING HABITS: High levels of disposable income, but usually finding it quite hard to cope or manage money. Lots of money is spent on transport (commuting) and bills, with whatever’s leftover going on high spec. consumer electronics, clothes etc.

BANKING HABITS: Current account and often one credit card with a high-street bank.Sometimes a mortgage, too. Little to no savings- particularly as he hasjust bought first house

DESIGN NEEDS:CHECK BALANCE: Stop over-spending - know how much he has available

ACCESS BILLS + REPAYMENTS DETAILSEasily organise oblugatory out-goings so he doesn’t need to worry about them

READ/GET ADVICE ABOUT BANK ACCOUNTS Better understand money options so he can make better tactical financial decisions

WANTS AND EXPECTATIONS OF POPCASH:• Quick access to balance• Beautifully designed and easy to use• Detailed bill and repayment info in one place• Quick set-up• Easily taylored notifications and settings

STATEMENTS DESIGN NEEDS

TOUCHPOINTS & TECH LITERACY

SPENDING HABITS

BANKING HABITS

18© FutureGov 2014

ROXANNEINDEBTED MOTHER

• FEMALE

• 46

• Fringe towns

• Low paid part-time job

• Married

• Children at school

We used to think it was normal to be in a bit of debt, but nowit’s all getting a bit out of hand.

“”

• Money confuses her which makes her nervous• Juggles debts, never feels she’s getting anywhere. Manages family finances• Underconfident and prone to giving up• Receives some child benefit and working tax credits. Has sought advice from CAB before.

TOUCHPOINTS AND TECH LITERACY: Most banking happens in-branch, though does a little online banking. She owns a smartphone, though mostly uses it to browse the web and is easily intimidated by anything perceived as complicated technology.

SPENDING HABITS: Family-focused, and finds it hard to say ‘no’ to the needs of her children, putting financial pressure on at Christmas. Lifestyles not lavish, but used to taking family holiday every year.

BANKING HABITS: A current account and several thousand pounds of debts, spread acrossseveral credit cards, hire purchase agreements and personal loans. She has used doorstep credit in the past. No savings.

DESIGN NEEDS:BALANCE INCOME AND OUTGOINGMake sure there’s always enough money in her account to pay all her bills.

TRACK HER REPAYMENTSSee how much debt she is in, to whom and howlong it will take her to pay off.

KNOW WHERE AND WHEN TO SEEK HELP When she is feeling confused or overwhelmedwho should she contact and is she entitled to?

WANTS AND EXPECTATIONS OF POPCASH:• Finances become clear and simple to understand • Easy to use - no tech or finance knowledge needed• Doesn’t need to check on it regularly• Reassuring

STATEMENTS

TOUCHPOINTS & TECH LITERACY

SPENDING HABITS

BANKING HABITS

DESIGN NEEDS

19© FutureGov 2014

LESLEYINCAPACITY CLAIMANT

• FEMALE

• 62

• Disabled

• Divorced-lives alone

• Grown-up children with

grandchildren close by

Because I’m on fixed income I’m alwayshaving to budget so carefully - it gets trickyto keep a track of everything.

“”

HEADLINE STATMENTS:• Set amount of money each month means having to be aware of fincances all the time• Constantly having to check online banking to make sure balance and billsare in check• Money-savvy but exhausted by it• Claims full incapacity benefits for ongoing illness

TOUCHPOINTS AND TECH LITERACY: Mostly in-branch or over the phone. Doesn’t own a computer or a smartphoneand is intimidated by technology and will avoid it if possible.

SPENDING HABITS: Very careful. Maintains a fairly modest but comfortable living, but always sticksto strict spending regime as money is tight and has no savings - an unexpected payment can tip her over the edge.

BANKING HABITS: A current account, some catalogue debt and a credit union loan.Small amount of debt and manageable repayments.

DESIGN NEEDS:TAKE THE HARD WORK OUT OF BANKINGLet her know what’s going on without her having to figure it out.

SEE HER AVAILABLE BALANCELet her know how much he has available so she doesn’t have to go to the cash-machine beforea direct debit is due.

KNOW WHERE AND WHEN TO SEEK HELP Who should she turn to if she has an emergency payment to make? Point her towards support and financially responsible loans.

WANTS AND EXPECTATIONS OF POPCASH:• Save her the constant anxiety of having to keepon top of things• She doesn’t want to go anywhere near a computerif she can possibly avoid it• Clear and simple - time saving and to-the-point• Not patronising

STATEMENTS

TOUCHPOINTS & TECH LITERACY

SPENDING HABITS

BANKING HABITS

DESIGN NEEDS

20© FutureGov 2014

Mobile first and digital inclusivity

In October 2013, research showed that50%ofmobilephoneownersusemobile as their primary internet source19

AccordingtothelatestresearchbyOfcomover91%ofUKadultsstatedthattheypersonallyownedamobilephone,ofwhichjustoverhalf(56%)saidtheir mobile phone was a smartphone (comparedto45%thepreviousyear).

Ofthepeopleinterviewedduringthecourseofresearch,wefoundthatthesefigureswereconsistent-withapproximately3/5ofthosesurveyedowningasmartphone.Conversationswithfinancialsupportprovidersconfirmedthatthemajorityoftheirclientsusedmobileforregularinternetaccess.Itismorepracticallyaffordabletoownacontract-operated smartphone than it is to buy a computerandaseperatebroadbandpackage.

This evidence pointed toward building Popcashformobile-firstuse,developingappsforbothiOSandAndroidplatforms,backedupwithawebappwhich syncs with your devices in real time.

imagefrom:mobilemarketingmagazine.com

Ofcourse,noteveryoneiscomfortablewithdigitalsolutions;forPopcashtobeaneffectivetoolforanybodywhomightwant to use it, it must be accessible to those who have limited access to, or aren’tabletousetheinternet.

Byfacilitatingafastandintelligentset-upprocess,itispossibleforacaseworker,familymemberorfriendtosetupyourPopcashaccountforyouinonego.

Start by attaching your bank account, selecting your regular bills and choosing yournotificationsettingsinonequicksession.Afterthat,you’llcarryonreceivingtextnotificationsofyourbalance, when bills are due to be paid andifyou’relookingalittlelowonfunds.

Digital Inclusivity

21© FutureGov 2014

How does Popcash work?

1 / Popcash checks your bank statments and pulls in direct debit information for quick set-up

4 / Choose which bills and repayments you would like to receive notifications for, and how (text, push or email)

5 / Popcash will alert you of who, how much and when a bill is due, as well as your current balance, and pointing you toward advice if you can’t pay it

2 / It sorts your payments into categories: Bills, Repayments and Income

3 / Add any other essential bills and repayments that you pay in cash or through bank transfer

We know that it’s very important to our users that Popcash be as quick, simple andintelligenttoset-upaspossible.

Byusingathird-partyintermediaryservice-Yodlee-Popcashhastheabilitytoscrapeinformationfromyouonlinebankingdata,making it very easy to see what regularly leaves youraccount.

Wealsoknowthatourusersoftenpayessentialpaymentsincash.Popcashallowsyoutoaddmanualcashpaymentsorbanktransfersquickly and simply, so you can make your Popcashaccountasdetailedasyouneed.

22© FutureGov 2014

Needs we discovered...

high-streetloan

dwp

social loan Gran

! credit cards

catalogues

overdraft

-£250.00

X

no balance :( competetive!

APR!interest rates!

!

high-streetloan

dwp

social loan Gran

! credit cards

catalogues

overdraft

-£250.00

X

no balance :( competetive!

APR!interest rates!

!

Complex financial landscapeRoxanne has so many debts that she findsitalmostimpossibletokeeptrackofthemall;shedoesn’tknowwhat they are costing her, or when theywillallbepaidoff.

Pays by cash Doesn’tknowifdirectdebitisvalueformoney-goestothebankinperson once a month to pay credit carddebts-sometimessheforgetsor misses the date, incurring more charges.

Caught out by direct debtsShelosestrackofpaymentdates,orisconfusedby‘on-or-around’dates.Andsheoftencaughtoutbydirectdebitsleavingheraccountbeforeherbenefitsgetpaidin.Thishadleadtomounting penalty charges and admin feeswhichshecan’taffordtopay.

Prefers automatic repaymentShe has a social loan, which she findsmuchless‘painful’andeasiertomanageasit’stakendirectlyoutofherbenefits.Italsoisareliefthatshecan’taccidentallyspendthatmoney.

Confusing financial languageWhen taking out a new loan, credit cardoroverdraftaccount,sheisconfusedbythefinancialjargonthatthebanksuse.Shewishestheywould explain things better so she knewwhatshewasgettinginto.

Wants to be notifiedWhen out shopping with her kids or husband,shefindsithardtoholdbackonherspending.Shewishesshe’d be told when her balance is low becausesheavoidscheckingit.

name: Roxanneage: 46status: married, 2 children

frustrations: money ‘just going’;nothavinganideaofwhatshespendsondebts;missing payments and getting penalties;financesfeelconfusingandintimidating

aims: to gain understanding ofherfinances,controlofheroutgoings and to stop getting penalty charges

Bank accounts: Halifaxcurrentaccount;creditunionsavingsaccount.

Debts: Halifaxoverdraft;Severalcataloguedebts;creditcardsandasocialloan.Previously she had a cash converters loan

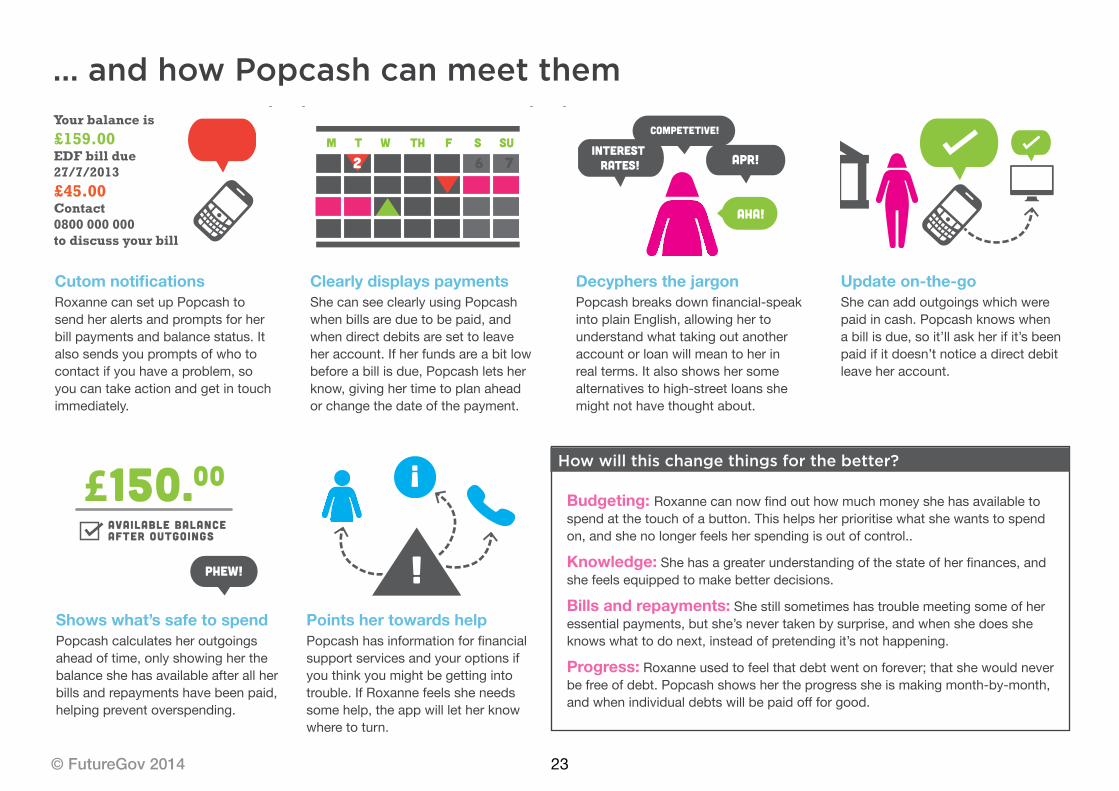

23© FutureGov 2014

... and how Popcash can meet them

Your balance is£159.00EDF bill due 27/7/2013£45.00Contact0800 000 000to discuss your bill

competetive!

APR!interest

rates!

!

M T W TH F S SU

1 2 3 4 5 6 7

Aha!

PHEW!

AVAILABLE BALANCEAFTER OUTGOINGS

£150.00

!

!

Your balance is£159.00EDF bill due 27/7/2013£45.00Contact0800 000 000to discuss your bill

competetive!

APR!interest

rates!

!

M T W TH F S SU

1 2 3 4 5 6 7

Aha!

PHEW!

AVAILABLE BALANCEAFTER OUTGOINGS

£150.00

!

!

Your balance is£159.00EDF bill due 27/7/2013£45.00Contact0800 000 000to discuss your bill

competetive!

APR!interest

rates!

!

M T W TH F S SU

1 2 3 4 5 6 7

Aha!

PHEW!

AVAILABLE BALANCEAFTER OUTGOINGS

£150.00

!

!

Cutom notificationsRoxanne can set up Popcash to sendheralertsandpromptsforherbillpaymentsandbalancestatus.Italsosendsyoupromptsofwhotocontactifyouhaveaproblem,soyou can take action and get in touch immediately.

Update on-the-goShe can add outgoings which were paidincash.Popcashknowswhenabillisdue,soit’llaskherifit’sbeenpaidifitdoesn’tnoticeadirectdebitleaveheraccount.

Clearly displays paymentsShe can see clearly using Popcash when bills are due to be paid, and when direct debits are set to leave heraccount.Ifherfundsareabitlowbeforeabillisdue,Popcashletsherknow, giving her time to plan ahead orchangethedateofthepayment.

Shows what’s safe to spendPopcash calculates her outgoings aheadoftime,onlyshowingherthebalanceshehasavailableafterallherbills and repayments have been paid, helpingpreventoverspending.

Decyphers the jargonPopcashbreaksdownfinancial-speakinto plain English, allowing her to understand what taking out another account or loan will mean to her in realterms.Italsoshowshersomealternativestohigh-streetloansshemightnothavethoughtabout.

Points her towards helpPopcashhasinformationforfinancialsupportservicesandyouroptionsifyou think you might be getting into trouble.IfRoxannefeelssheneedssome help, the app will let her know wheretoturn.

Budgeting: Roxannecannowfindouthowmuchmoneyshehasavailabletospendatthetouchofabutton.Thishelpsherprioritisewhatshewantstospendon,andshenolongerfeelsherspendingisoutofcontrol..

Knowledge:Shehasagreaterunderstandingofthestateofherfinances,andshefeelsequippedtomakebetterdecisions.

Bills and repayments:Shestillsometimeshastroublemeetingsomeofheressential payments, but she’s never taken by surprise, and when she does she knowswhattodonext,insteadofpretendingit’snothappening.

Progress: Roxanneusedtofeelthatdebtwentonforever;thatshewouldnever befreeofdebt.Popcashshowshertheprogresssheismakingmonth-by-month,andwhenindividualdebtswillbepaidoffforgood.

How will this change things for the better?

24© FutureGov 2014

25© FutureGov 2014

Wireframes

QUICK-ADDNEWPAYMENTMAIN NAV

REPRESENTED BALANCE-UP-COMINGPAYMENTS

SWIPE UPWARDS TO REVEAL FULL PAyMENTS LIST

LINKTOLISTOFUP-COMINGPAyMENTS

PRIMARy ACCOUNT ANDBUDGETING INFO

LINK TO PAyMENT CALENDAR VIEW

3 SOONEST OR OVERDUEUP-COMINGPAYMENTS

From the insights and needs we’d uncovered through our research, we began to turn thoughts into interactions, visualsandlayouts-elementsofthefinalappwhichcombine to be known as UX or,UserExperience.

We wanted Popcash to be clear, unintimidatingandattractive.Theresearchwasplaininthattheinterfacehadtobeassimpleaspossible-andasfarawayfroma spreadsheet, bar chart or pie chart as possible.

The scheme chosen is clean and elegant, withfinancesbrokendownintothreecategories:income,repaymentsandbills.Aesthetically,thecategorisationisfurtheraccentuated using explanetory icons and colour-coding.

26© FutureGov 2014

SETTINGS (EDIT NAME, CHANGE DETAILS, NOTIFICATIONS ETC)

SHOWS AMOUNT DUE

SHOWS NAME OF BILL

SHOWS DATE DUE

SHOWS METHOD OF PAyMENT

(CASH: TAP TO CONFIRM)

SHOWS ACCOUNT DETAILS(NAMEONACC.ANDID#)

LINKS TO PROVIDER CONTACTDETAILS/DETAILS EDITABLE

IN‘SETTINGS’/FREQ.OFBILL AND DATE OF NEXT

PAyMENT

SEE PAyMENT HISTORy SCREEN

QUICK-ADDNEWPAYMENT

LIST FILTER BUTTONS (By CATEGORy)

LINKTOLISTOFUP-COMINGPAyMENTS

LIST ORGANISED By SOONEST FIRST

LINK TO PAyMENT CALENDAR VIEW

AMOUNT,PROvIDER/LENDERAND DATE DUE

27© FutureGov 2014

SETTINGS (EDIT NAME, CHANGE DETAILS,

NOTIFICATIONS ETC)

SHOWS AMOUNT DUE

SHOWS NAME OF BILL

SHOWS DATE DUE

SHOWS METHOD OF PAyMENT

(CASH: TAP TO CONFIRM)

SHOWS ACCOUNT DETAILS(NAMEONACC.ANDID#)

LINKS TO PROVIDER CONTACTDETAILS/DETAILS EDITABLE

IN‘SETTINGS’/FREQ.OFBILL AND DATE OF NEXT

PAyMENT

SEE PAyMENT HISTORy SCREEN

SHOWS AVAILABLE BALANCE

(PRIMARy ONLy)SHOWS NAME OF BILL

SHOWS DATE DUE

SHOWS FULL BALANCELINK TO LIST OF FUTURE PAyMENTS DEDUCTED

SHOWS ACCOUNT DETAILS(NAMEONACC.,BANKNAME

SORTCODEAND#)

DIVDES AVAILABLE BALANCE By DAyS BEFORE NEXT INCOME

PAyMENT

LINKS TO LIST OF PAyMENTS FROM/TOTHISACCOUNT

SEE REPAyMENT PROGRESS SCREEN

SETTINGS (EDIT NAME, CHANGE DETAILS ETC)

ACCOUNT NAME (NICKNAME)

28© FutureGov 2014

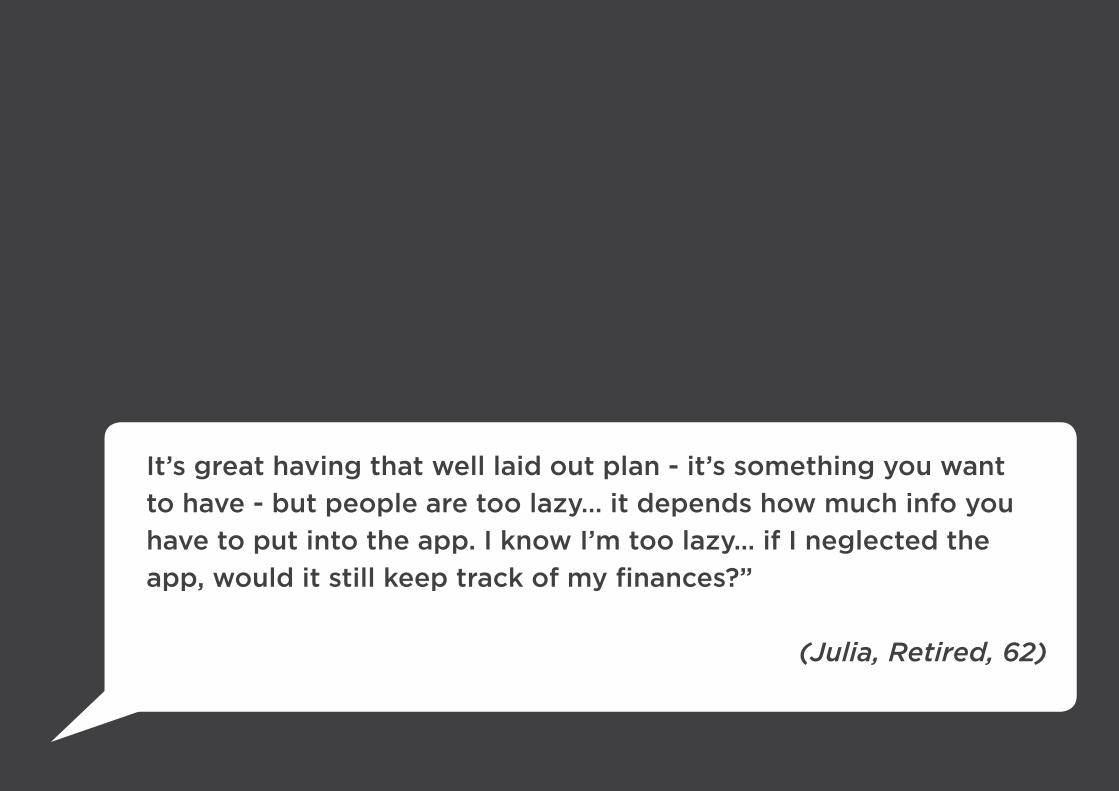

User testing 2: process and outcomes

It’s great having that well laid out plan - it’s something you want

to have - but people are too lazy… it depends how much info you

have to put into the app. I know I’m too lazy… if I neglected the

app, would it still keep track of my finances?”

(Julia, Retired, 62)

29© FutureGov 2014

We wanted to challenge the decisions we’d made based on our research whenwewerestillhalfwaythroughtheprototypebuild-givingustimetochangeoradjusteitherfunctionalityorvisualdesign.

WesetupcampinLewesLibraryforaday,anddidsomelight-touchresearchwithlocalstofindoutwhattheythoughtofPopcash’sdesign

We wanted to challenge the decisions we’d made based on our research when we were still halfwaythroughtheprototypebuild-givingustimetochangeoradjusteitherfunctionalityorvisualdesign.

Todothis,wetooksomeprint-outsoftheappdesignsandaskedeachpersonasetofquestions based on a) their demographic b)theirfeelingsabouttheirfinancesc) thoughts about the appd)aprioritisedlistoffeatures

Testing our assumptions - user testing in Lewes Library

Who did we speak to?

Age range: Internet use

25-4073%everyday18%fairlyoften9%occasionally

40-54 55-69

45% 35% 20%

73%18%

9%

Technology ownership

72%

13/18

89%

16/18

Only 5/18 disagreed with “I rarely get caught out by a payment...” Most people we spoke tosaidtheyfeltincontroloftheirfinances,but15/18 said they had “worried about debt in the past”

10/18 did not know where they would go for financial advice - when pressed most would ask their bank or would search the internet

8/18 interviewed were self-employed or on 0 hours contracts and so their income was unpredictable

15/18 said they “would recommend Popcash to someone I know”, and 11/18felttheywouldusetheapp‘everyday’orregularly’.Manypeople thought they would recommend it to a young person.

7/18 felt they wouldn’t know “what to do if I can’t pay a bill.”

“I’m not sure what I would do if I got into trouble...I guess I would go to someone in my family, or go and plead with my bank”

“My son could really do with this- he’s bloomin’ terrible with money!”

30© FutureGov 2014

Security information needs to be clear and friencly, but is not as important to people as we thought

Self-emloyment, 0 hours contracts and variable incomes are a big issue that we haven’t yet dealt with

Therewereverymixedfeelingsonthis-itvariedfrompersontoperson.Manydidnot ask and when we brought it up they seemedhappytotakeourwordforit.Acoupleofpeoplebroughtupworriesabouttheirinfobeingaccessibleifsomeonegotholdoftheirphone.Onepersonaskedabout how the resultant data on the phone would be used, and expressed concerns aroundthat.

“I’m not sure about the security… someone could get hold of my phone on the bus… all my information would be available immediately to someone with my phone”“I’m the sort of person who just closes their eyes and hopes to be honest.”

Action: A timeout and PIN access is really important-bothforrealsecurityofinfoandfortheuser’speaceofmind.There also needs to be very clear and friendlysecurityinformationavailableimmediatelyandthroughouttheservice.

Ahighpercentageofthepeoplewespoketodidn’tliveonafixedincome.Thisispartlyduetothecontextoftheusertesting,This is clearly a big issue which Popcash hasnotaddressed.Howcantheappcalculatewhat’ssafetospendifthere’snowayofrecordingwhenthenextincomewillbe?

Action: There’s some more Is there some thoughtneededhere.

Partoftheregistrationquestionscouldaskifyouhaveregularincome(PAYE,full-time,Benefits)orifit’svariable(Freelance,0-hourscontractetc.)andtakethatintoaccount.Istherevalueinshowingtherealbalanceofyourbankaccountandsimplyhighlighting green or red as to whether you cancoveryourbillsforthenext30days?

User testing insights

Wehavebeentestingthefully-functioningPopcashprototypewithavarietyofpeople,includingend-users,financialsupportpractitionersandexpertsinthefield.

Theaimofthiswastogetfeedbackabout the User Experience (the design, interfaceandinteractions)andfeatures.

Through these conversations we’ve gained valuable insights that point to somereallyexcitingopportunitiesforhow the Popcash tool could develop overthecomingmonths.Asummaryofwhatwehaveheardissetoutonthefollowingpages.

31© FutureGov 2014

People want to be notified

Therewasaveryhighlevelofapprovalfortheideaofnotifications.Afewpeoplesaidthey wouldn’t want to be contacted ‘all the time,foreverylittlething’.Afewalreadyreceivenotificationsfromtheirbanksandfindthemveryuseful.

“It would be good to have trigger prompts ... so you know when you absolutely can’t avoid it any more.”

Action:Makenotificationsmoreprominentwithinthedesignoftheapp.Thinkaboutallowingcustomisationofnotificationsfromlist view so that it’s clearer

Daily ‘safe to spend’ is better than a monthly total

There was some mix, but in general daily seemed to get a more positive response frompeople-mostlybecauseoftheimmediacyofitsrelevance.Thiscameoffthebackofcasualoverspends:sfewpeople mentioned spending too much when they went out to the pub, or on school holidayswiththeirkids.Afewsaidtheythoughtthedaily‘safetospend’ would incentivise them to spend lesstoseetheirdailyamountincrease.

Action: We decided to swap out the monthlyavailableincomeforadailybreakdown.Thismeansthatpeople’simmediateactionswillbeaffected-thegamificationelementofspending.

Most people said that when presented with the‘safe-to-spend’balancenumberonthehome screen, they wanted to know how andwhyithadbeencalculated.

Wehavefoundthatmanypeoplesaidtheydistrustfulofadviceconcerningmoney,andwouldliketobeofferedtheopportunitytounderstandtheirsituationforthemselfratherthansimplytakingitatfacevalue

Action: It is essential that Popcash is completelytransparentinit’sfunctions.Atthenextstageofdesigndevelopment,wewillneedtothinkcarefullyabouthowinformationcanbeintegratedandeasilyaccessible at every point where a user mightwanttohaveaccesstoit.

People want to know what ‘safe’ really means

User testing insights

32© FutureGov 2014

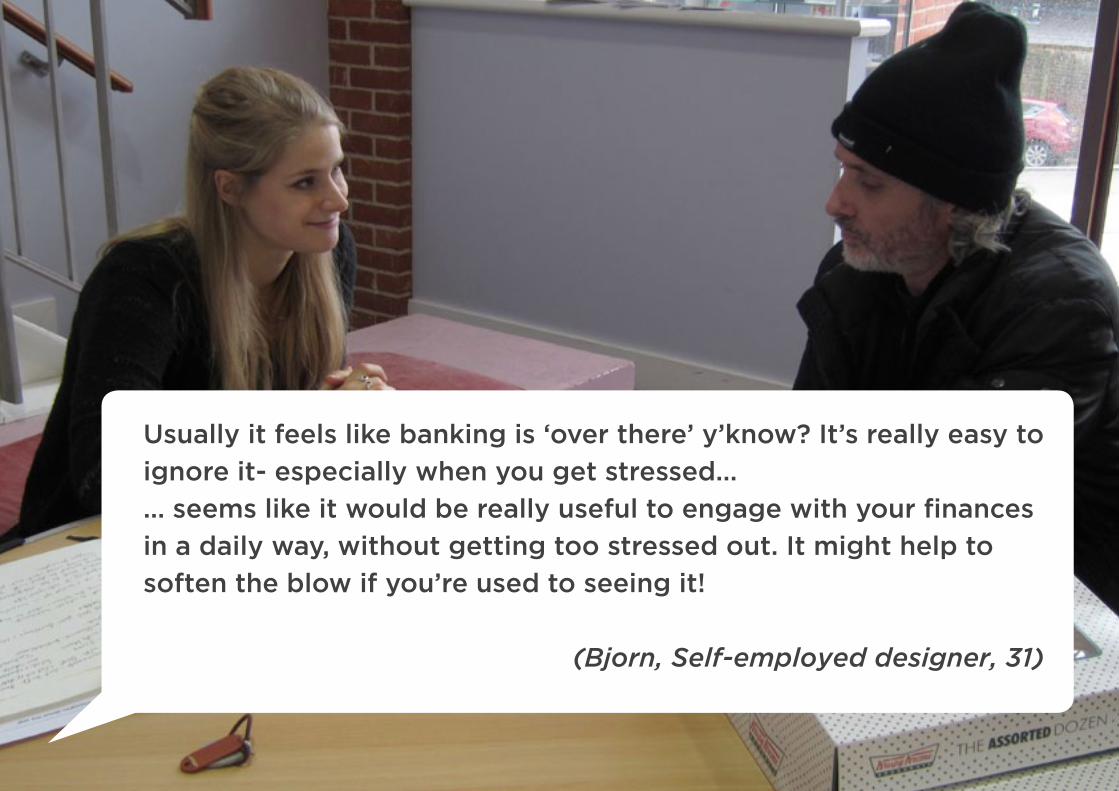

Wireframes

Usually it feels like banking is ‘over there’ y’know? It’s really easy to

ignore it- especially when you get stressed...

... seems like it would be really useful to engage with your finances

in a daily way, without getting too stressed out. It might help to

soften the blow if you’re used to seeing it!

(Bjorn, Self-employed designer, 31)

33© FutureGov 2014

Next Steps

From our discovery research to date we have heard most strongly that the needforsimplificationoffinancesandclear,unintimidatinginformationaboutfinancialsupportserviceswouldbemostusefulforboththosedealingwithandtryingtoavoidproblemdebt.

We’ve also heard that Popcash could be usefulinsupportingfront-linefinancialsupportstaffbyintegratingapersonalbudgeting tool like the one they use to initially help their clients understand theirincomeandoutgoings.

An unresolved issue which will need to be addressed early in the next stage ofdevelopmentishowPopcashcanhelpsupportthoselivingonzero-hourscontracts,areself-employedorhavevariableincome.Therewillbesomeadaptionneededinthefunctionalityofthe‘safetospend’feature.

• Immediatebugfixingandtweaksfromusertestingandfeedback

• Beginlookingatmethodologiesofdatabasingservicesandorganisationsforsupportsignposting.Lookatsomehyper-localoptions.

• Designofthetext-notificationalgurythmsaround signposting

• Moreusertestingandfeedbackfromend-usersandfront-linestaff

• Communication around the MVP begins

• Marketing plan and distribution model

• Assessingprosandconsofdistributionviacommercialoutletsi.e.Appstoreetc.

• Exploring design solutions to assisting variable-incomeuserstobudget

• Exploringpotentialusesfordatageneratedonpersonalfinancebehavioursandtrends

What’s next?

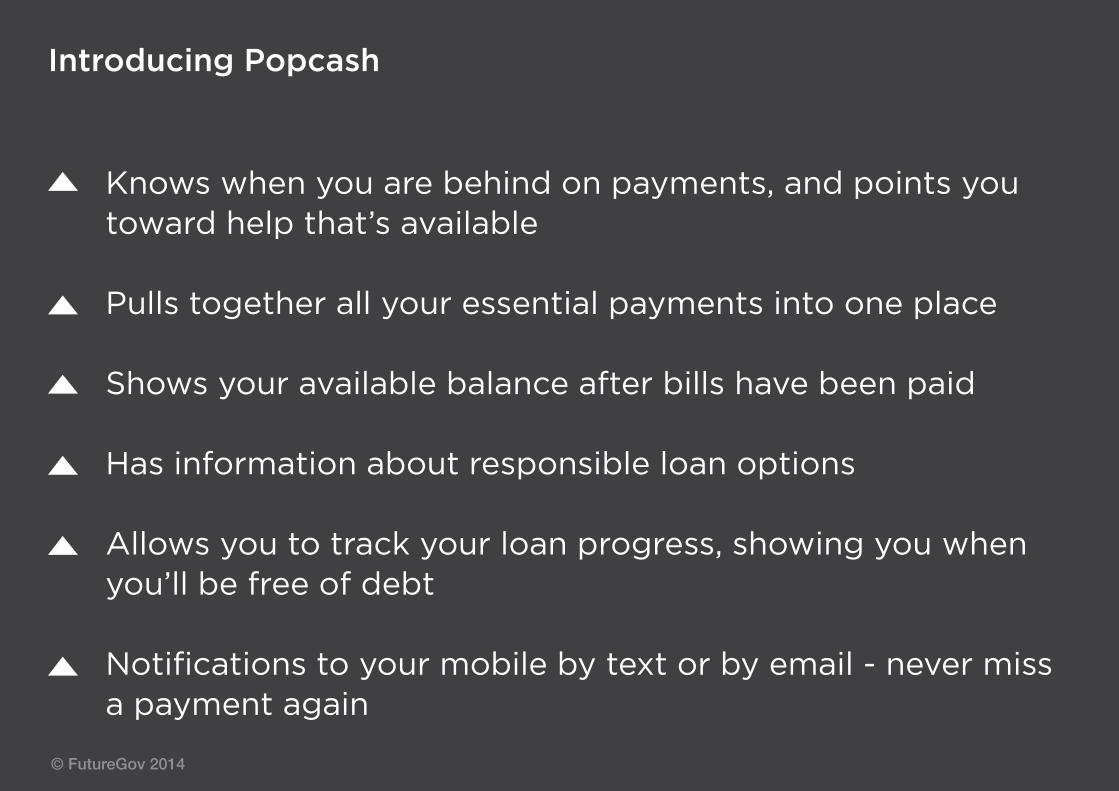

Introducing Popcash

Knows when you are behind on payments, and points you toward help that’s available

Pulls together all your essential payments into one place

Shows your available balance after bills have been paid

Has information about responsible loan options Allows you to track your loan progress, showing you when you’ll be free of debt

Notifications to your mobile by text or by email - never miss a payment again

© FutureGov 2014

35© FutureGov 2014

A simple app for complicated personal finances.

Stay up-to-date:

@popcashpopcashapp.com

© FutureGov 2014

36© FutureGov 2014

1. Payplan have seen cases where clients had an excessof20paydayloans.Thishasresultedinconsumersgettingintomoredebtbeforeseekinghelp.CitizensAdvicesaythatonaverage,theyfoundintheyears2012-2013thattheirclientswithpaydayloans had eight debts, while those without payday loanshadfive.Oneintervieweetoldusthattheuseofpaydayloans “started as a necessity, but became an impulsivity”.

2. oneintervieweelivingoffhispensiontoldushegot into problems when he missed a direct debit and gotcharged£40sowenttoWonga.Hehasbeenlivingattheendofhis£300overdraftforawhileandpays£20permonthtothebankbutthinksthisispurelyforchargesasthedebtisn’treducing.An interviewee in her early 20s described how she hasn’thadabankaccountforthepast3yearsbecauseshegotintoalotofdebtthroughcreditcardsandoverdraftswhenshewas18andowesmoneytothreedifferentbanks.Shenowhasbadcreditrating,acoupleofCCJs(county court judgements) and though she works in Tescoisunabletopayoffherdebts-‘I can barelypay my bills now let alone extra bills on top of it’.

3. 5 million adults lack adequateliteracy skills (NIACE 2011), and an estimated 7 millionlack‘functionalnumeracy’(Leitch2006;alsoseeCarpentierietal.2010)

4. A Resolution Foundation report suggests that two thirds(66%)ofthoseonlow-to-middleincomesare

strugglingtokeepupwithbillsorfallingbehind,andaquarter(26%)areunabletoreplaceorrepairbrokenelectricalgoods.

5. 63%ofhouseholdslivingonbelowaverageincomeshadnosavings.76%oflow-incomehouseholdshadnosavingsoronlysavingsofupto£1,500.

6. Commercial debt management companies have foundthatborrowersareusingpaydayloanstopayoffdebtsintheshorttermratherthandealingwiththerootcausesoftheirdebtproblems.Payplanhaveseencaseswhereclientshadanexcessof20paydayloans.Thishasresultedinconsumersgettingintomoredebtbeforeseekinghelp.

7. DrGathergood,aneconomistattheUniversityofNottingham,definedthemarketasbeingusedbytwotypesofpeople:I-Peoplewhohavehadafinancialshockandneedmoney quickly to address that, who intend to repay, will be in a position to repay and need the money now,forwhomapaydayloancanactasahighcostbuteffectiveformofinsuranceII-Peoplewholackcontrolintheirexpendituresandmight take out debt in order to purchase something theywantatshortnoticewithoutanabilitytorepay.Forthemapaydayloanisanopportunityforthemtobeavictimoftheirownbehaviour

8. A report by StepChange debt charity report showsthattheaveragepaydayloandebt(£1,657)nowexceedsaveragemonthlyincome(£1,320)forclients.Over65%ofclientswithapaydayloanhave

contractualpaymentsworthmorethan100%oftheirincome,comparedto14%ofotherclients

9. 80%ofpeopleseekinghelpfromChristiansAgainstPovertysaidtheirhealthsufferedduetothestressofdebt.68%wereprescribedmedicationbytheirGP,and2in5hadconsideredorattemptedsuicide.

10. “[So what did that feel like - the first week you couldn’t pay your bill?] Yeah it’ll be alright I can just sort it next week. And then next week comes and you don’t catch up and it goes on... I just tried not to think about it. If you don’t think about it, don’t know. It is worrying ‘cos when you come back to it and think I haven’t paid that for 6 months” (Kim)

11. Anincreaseinfamilylendinghascausedstresses on relationships, particularly between generations.Oneintervieweespokeofhersonusinghergrandsonasanemotionalblackmailtooltoforceher into loaning him money that he has no intention ofrepaying;‘Theythinkparentsshouldhelptheirchildren’Severalyoungerintervieweestalkedofparents‘helpingout’whentheyhaverunoutofmoneyorgotintounexpecteddebt.

12.InthreeoutoffourcasessurveyedbyStepChange, anxieties over unmanageable debt had underminedtheirconfidencetosupportthemselvesandtheirfamilies.Nearly40%saidtheirrelationshipwithfamilyandfriendshadbeenaffectedbytheirdebtproblemsAnILCreportondebtamongolderpeoplefound

Appendix

37© FutureGov 2014

that couples who struggle with debt are more than twiceaslikelytosuffermarriagebreakdownthanthosewhosefinancesaresteady

13. “They bury their head in the sand. I’ve been there. They don’t realise they are in as much trouble as they are, they think they can get out of it, they hope for better times, they are in so deep when they hit a personal crisis that they can’t see a way out, they get ill, mentally ill and then they can’t deal with it because of the stress and the stigma and the pride issue” (Credit Union)

14.CAPdon’tringpeoplefromlandlinesastheassumption is that it’s a creditor so the call isn’t answered, and when they go round to people’s housesforpre-arrangedappointmentsoftenfindthatpeopledon’tanswerthedoor.Theythinkthisisduetothepersonnotwantingtofaceuptotherealityoftheirdebt

15.OfpeoplewhosoughthelpfromChristiansAgainstPoverty,72%hadsacrificedmealsduetodebt,and21%saidtheymissedmealsregularly

16. “Very often with the backdated claims you have people saying ‘I didn’t know I could claim’ . Along with that you have people saying ‘I thought I’d get another job’. Perhaps a sense of false opti¬mism that they think they are going to find work. Half a million don’t claim straight away. People are seeking help but they are seeking help by borrowing money, either off a relative or door¬step lender or payday loan or something like that. They don’t think or know about us.”(Hous¬ingBenefitTechnicalAssessor)

17. “I had one lady who came to us on Monday and she was being evicted on Thursday. We had no contact whatsoever from her. She had rent ar¬rears, she had problems with her housing ben¬efit, she’d been given notice to quit, which is 2 months. If she had come to us 2 and half months ago we could have looked at her income, made sure she was getting right rate, why has hous¬ing benefit got into a mess. Child credit had got into mess and we could have sorted that out for her. We don’t want people to be home¬less, would rather people had a roof over their head.”(HousingAdviceOfficer)

18. “I was mortified, couldn’t deal with it, couldn’t answer the phone, didn’t know what to do. Went to the CAB and felt like a leper. Terrible. The information was good. They couldn’t support me as much as I needed it really. I never claimed any benefit. I was mentally unable to deal with it and because I’m not silly, I’m quite an intelligent person, they didn’t offer me the case work where they would write letters for me. I had to do it all myself and didn’t because I wasn’t able to” (Ella)

StepChangeDebtCharitysayoutof950clientssurveyed,over40%hadstruggledwithmountingdebtsforayearormorebeforeseekinghelp.Research on the debt problems experienced by workinghouseholdsfoundthatalthoughpeopletriedtodealwiththeirfinancialdifficultiesinanumberofdifferentways,theycontinuedonadownwardslopetounmanageabledebt.veryoftentheseresponsesinvolvedmoreborrowingas people held on to the hope that they could sort it out themselves or ‘because they were tooembarrassedtoadmitotherwise’.

19. http://www.digitalbuzzblog.com/infographic-2013-mobile-growth-statistics/