Political€Risk€and€Firm€Default€Probabilitygreta.it/credit/credit2006/poster/13_Sandstrom.pdf ·...

38

Political Risk and Firm Default Probability - Exploring Export Credits to High-Risk Countries August, 2006 Preliminary version, comments welcome Annika Sandström Department of Finance and Statistics Swedish School of Economics and Business Administration P.O.Box 479, FIN-00101 Helsinki, FINLAND e-mail: [email protected]

Transcript of Political€Risk€and€Firm€Default€Probabilitygreta.it/credit/credit2006/poster/13_Sandstrom.pdf ·...

Political Risk and Firm Default Probability

Exploring Export Credits to HighRisk Countries

August, 2006

Preliminary version, comments welcome

Annika SandströmDepartment of Finance and Statistics

Swedish School of Economics and Business Administration

P.O.Box 479, FIN00101 Helsinki, FINLANDemail: [email protected]

Political Risk and Firm Default Probability

Exploring Export Credits to HighRisk Countries

Abstract

Despite the increased presence and importance of political risk and export credit financing in the

world economy, these topics have not been well covered in the empirical credit risk literature. In

this article, we model default probabilities for private firms from selected highrisk countries,

and condition these on a vector of country specific political risk variables, indicators of the level

of democracy, legal environments and the quality of credit information, in addition to the

traditional firm specific financial variables usually employed. The study is an empirical

application to a unique dataset on export credit facilities, not studied previously in a credit risk

framework. The preliminary results from Argentina, Indonesia, Nigeria, Poland and Saudi

Arabia indicate that information on socioeconomic conditions, military in politics and external

conflict in a country constitute significant predictors for firm default, that may not otherwise be

detected with scarcely available, or unreliable accounting information.

Key Words: Probability of Default; Company Failure Risk; Export Credits; Political Risk

1

1. Introduction

Analysis of financial statements is the starting point in any classification of companies into

healthy and financially distressed (or bankrupt) firms. Among the first known attempts to

distinguish companies based on their accounting is Fitzpatrick (1932), who compared financial

ratios between successful industrial enterprises from those that failed, and found that the

probability of default was related to the individual characteristics of firms. Since then, a large

number of empirical studies has been published and well known applications of credit scoring,

e.g. the Altman’s ZScore model (Altman, 1968) and the Moody’s KMV EDF RiskCalc

Model, are widely used in the industry. These accountingbased models are usually applied when

no publicly traded securities are available or when secondary market prices are unreliable.

Meanwhile, some of the caveats of the accountingbased models is that they rely on financial

statements that capture the past performance of the firm rather than its future performance. As

noted by Hol et al. (2002), it still seems that the extensive research effort on bankruptcy, and

default prediction has failed to produce an agreement on which variables are good predictors and

why. This may be partly attributed to the fact that the studies refer to different time periods,

countries and industries. Most studies are also claimed to lack a theoretical framework to guide

the empirical research effort1. Traditionally, default probability is estimated from failed and

nonfailed firms, given historical data using annual financial statements. In this paper, we ask

whether there could be other important factors to consider, in order to improve model

performance, especially in situations when the financial information is scarcely available or

unreliable, as might be the case in developing countries.

1 Hol et al. (2002) have recently suggested a capital structure based default theory.

2

While the financial figures of a company are the basis for evaluating its credit profile, non

financial and environmental characteristics seem necessary to complete the picture. The new

approach in this paper is to discuss linkages between firm default probability and the political

and legal risk environments that prevail in the country where the borrowing company operates.

To what extent do political events or unstable legal environments constitute a risk for foreign

lenders, that might not otherwise be reflected in the financial figures of the borrowing company?

The main objective of this study is to assess whether political and commercial factors can be

distinguished in the credit risk assessment process.

A novel feature of the present study is also the use of export credit guaranteed debt contracts in

the attempt to model default probabilities from realized payment interruptions2. We empirically

explore the relationships between default probabilities and political risk for a group of firms from

selected highrisk countries, including Argentina, Indonesia, Nigeria, Poland and Saudi Arabia.

In this version of the paper, these countries are selected to represent examples of most active

recipients of worldwide export credits among developing countries, and reflect also the largest

export streams from Finland to developing countries in the last two decades.

The remainder of this paper is organized as follows. Section 2 provides a brief literature review

on default probability estimation. In section 3, we discuss the question of the impact of political

risk on credit defaults and formulate our main research hypothesis. Section 4 presents our

research design and data in more detail. In section 5, we present our results with a short analysis

of our target countries. Section 6 concludes with suggestions for further research.

2 This type of data has not been previously addressed in similar credit risk or default probability studies, due to a general secrecysurrounding Export Credit Agencies and consequently, the unavailability of data. For the purposes of this research project,initiated in cooperation with the Finnish Export Credit Agency, Finnvera plc, we have the unique opportunity to explore archivesof historical credit and political risk data from various countries.

3

2. Default probability estimation

There are two schools of thought in the use of statistical methods to predict firm default. One

holds that default is modeled using accounting data, whereas the other recommends using market

information. Accordingly, the existing models are usually classified into the marketbased

models, which rely on security prices, and the so called fundamentalsbased models, which can

further be divided in models that rely on accounting, systematic market and economic factors, or

rating information. In this study, for brevity reasons and in order to follow our research setup for

private firms, we will focus mainly on the accountingbased models4.

Fundamentalsbased estimation with accounting info

The literature on credit scoring is based on the original work of Beaver (1966) and Altman

(1968). Being a classic among the early studies, Beaver (1966) conducted a comprehensive study

using a variety of financial ratios and concluded that the cash flow to debt ratio was the single

best predictor of firm default. Beaver’s univariate approach of discriminant analysis led the way

to a multivariate analysis by Altman (1968) who adopted a multivariate discriminant analysis

(MDA) framework in his effort to find a bankruptcy prediction model. This became the popular

Zscore model, where the financial ratios used are: 1) working capital over total assets; 2)

retained earnings over total assets; 3) earnings before interest and taxation over total assets; 4)

market value of equity over book value of liabilities; and 5) sales over total assets. In Altman’s

study, the ZScore correctly classified 94% of the bankrupt companies and 97% of the non

bankrupt companies one year prior to bankruptcy. Later, Altman has revised the model for

private firms by substituting book value for market value in the calculation of the ratio of market

4 For a good review of the marketbased models, see e.g. ChanLau (2006)

4

value of equities to the book value of liabilities5. The popularity of the Altman Zscore is

explained by its parsimony and ease of interpretation. Some of its shortcomings are discussed in

Engelmann et al (2003).

Explanatory variables and statistical techniques

A large number of financial ratios can be used as explanatory variables in the accounting based

models. Typically, the greatest variations in the probabilities of default come from ratios

capturing firms’ profitability, growth opportunities, level of indebtness, and liquidity. To obtain a

parsimonious model, some selection criteria are needed, and the variables selected are usually

those with the higher discriminating power for explaining the default frequency after performing

univariate analysis. However, these steps can only be taken once a robust database has been

compiled. There is usually also the risk of “overfitting”, that is, the model functions only on the

sample data but fails to engage with realworld data that it has not “seen” before.

Once variables have been selected, a variety of statistical techniques have been used to assess the

default probability of a firm, including econometric models, linear discriminant analysis, k

nearest neighbor classifier, neural networks, and support vector machine classifier among others

(ChanLau, 2006). For obvious problems with the assumptions of the initially employed

discriminant analysis, discrete dependent variable econometric models (i.e. logit or probit

models), have become more popular tools for credit scoring. Ohlson (1980) and Platt & Platt

(1990) present some of the early studies using the logit. A more recent example is Laitinen

(1999), who used automatic selection procedures to select the set of variables to be used in

logistic and linear models, which were then thoroughly tested outofsample.

5 A summary of the methodologies is given in Chuvakhin & Gertmenian (2003)

5

3. Political risk and credit

Political risk may be defined as "the probability of the occurrence of some political event that

will change the prospects for the profitability of a given investment”. This definition, originally

given by Haendel (1979), appears often in studies of political risk due to its simplicity and

flexibility against the interest and need of the definer (e.g. a corporate, a private insurance firm,

an export credit agency, a bank or a multinational organization). In the credit risk framework,

political risk may be defined as “the possibility of delayed, reduced, or nonpayment of interest

and principal where the outcome is attributable to the country of the borrower” (Caouette,

Altman and Narayanan, 1998).

There has been a growing interest in the academic literature on the link between political

institutions and political risks facing multinational corporations. A large part of this research is

devoted on domestic institutions and FDI inflows (see e.g. Henisz 2002, and Jensen 2006).

Meanwhile, only few authors have investigated the relationship between political risk and credit,

and the focus has been mainly on sovereign borrowing (see e.g. Citron and Nickelsburg 1987,

Balkan 1992, Edwards 1986, Brewer and Rivoli 1989 and Peter 2000) and the relationship

between democratic institutions and borrowing (see e.g. Schultz and Weingast 2003 and Saiegh

2005). To the best of our knowledge, there are no prior studies using political risk factors to

study corporate credit defaults.

Hypothesis development

The overall hypothesis in the present study is that outcomes from lending decisions to

importing/borrowing companies are uncertain not only because of the company as an individual

obligor, but also due to surrounding political and legal risk factors, that may have nothing to do

with the firm itself. We ask to what extent comprehensive measures of political risk would be

6

useful in the assessment of default probabilities at the transaction level.

We conjecture that the political risk in a country affects the credit risk of firms operating in the

country through subcategories of political risk, identified as 1) risk of expropriation or

confiscation (e.g. of the exported merchandise by a foreign government); 2) risk of currency

convertibility and transferability (i.e. the customer in the foreign country is unable to obtain

foreign exchange in order to pay or is unable to send payments out of the country due to

governmental restrictions or foreign exchange transfers); and 3) political violence (war, sabotage

or terrorism). All these situations involve specific risks that might cause a buying firm that would

otherwise be willing to pay the creditor to be unable to do so. In addition, there might be other

unanticipated changes in regulations, corruption or failure by the government to implement tariff

adjustments because of political considerations. Further, quasicommercial risks may arise when

the project or business of the company is facing stateowed suppliers or customers, whose ability

or willingness to fulfill their contractual obligations towards the project might be questionable.

Ultimately, political risk relates to the preferences of political leaders, parties, and actions, as

well as their capacity to execute their stated policies when confronted with internal and external

challenges. Changes in the regulatory environment, attitudes towards corporate governance,

reaction to international competition, labour laws, witholding and other taxes are concerns,

which may all affect the firm in an extent leading to nonpayment of its obligations. The causes

for the above conditions may be influenced by hard to discern shifts in the political landscape

(Bremmer et al. 2006), so the big challenge in any studies on political risk is how to measure it.

7

Measuring Political and Legal Risk

In this study, we analyze political and legal risk through selected indicators employed in the

International Country Risk Guide (ICRG), Polity IV Project and the World Bank’s “Doing

Business” database. These ratings are all illustrative of the above stated conditions from a

project and company perspective.

The ICRG system by the PRS Group is a numerical rating system that scores a number of

components for political, economic and financial risk to determine a rating for each category6.

We use the ICRG Political Risk Rating and its subcomponents, which aim to provide a means of

assessing the political stability of countries on a comparable basis. ICRG assigns risk points to a

preset of group of factors, termed political risk components. The range of points that can be

assigned to each component varies between zero and a fixed weight, that the particular

component is given in the overall political risk assessment. The lower the risk point total

indicates for higher political risk, so we expect an inverse relationship with firm default

probabilities.

Appendix I lists the political risk components for the ICRG Political Risk Rating (icrg). Among

the components, for example, Democratic accountability (Component K) is an indicator of

whether a government will take precipitous actions such as expropriation. Law and Order

(Component I) is seen as an indicator of the stability and transparency of the legal system and an

indication of whether contracts might be abrogated. Ethnic tensions (Component J) are often a

preliminary condition to strife that leads to political violence against investors and creditors, or

on their property.

6 These three ratings are used to determine an overall composite rating, a number from 0 to 100 (zero being high risk, 100 beingthe lowest risk).

8

In addition to the ICRG risk components, we will also test for other measures of the legal and

political system in a country (also listed in Appendix 1). We describe the quality of a country’s

political institutions in terms of the exposure to democracy; using the "Polity Index" from the

Polity IV dataset. This index measures the degree to which a nation is either autocratic or

democratic on a scale from 10 (strongly autocratic) to +10 (strongly democratic). According to

the “democratic advantage” argument, democracies pay lower interest rates for the sovereign

debt than authoritarian regimes because they are better able to make credible commitments (see

e.g. Schultz and Weingast 1996, 1998). We test whether this argument is reflected also on firm

level and expect a negative relationship between default probabilities and the level of host

country democracy.

We define political stability also in terms of the frequency of regime change. This is

approximated in the “Polity IV Regime Durability Variable” (durable), that measures the years

since the most recent regime change or the end of a transition period defined by the lack of stable

political institutions. We expect a negative relationship with firm default probabilities, that is, the

longer the time since last regime change, the lower is the firm probability of default.

Finally, we ask how legal and financial rights of the creditor and debtor affect default

probabilities? On the one hand, legal costs may prevent the borrower to incur a “strategic

default”, where the firm fails to pay the amount stipulated in the debt contract even though it

possesses resources to do so. On the other, with costly liquidation, creditors may prefer to

forgive part of debt, which may result in equityholders’ incentives to default opportunistically7.

7 See e.g. Davydenko and Strebulaev (2003).9 This includes manually kept records from the 1980s as well as electronic registers from the later decade.

9

To capture the effects of legal risk, we include two additional indices from the World Bank’s

Doing Business database, that measure credit information registries and the effectiveness of

collateral and bankruptcy laws in facilitating lending. The legal rights index (legal) reflects the

legal rights of borrowers and lenders, by measuring the degree to which collateral and

bankruptcy laws facilitate lending. The index includes 3 aspects related to legal rights in

bankruptcy and 7 aspects found in collateral law. It has a scale from 0 to 10, with higher scores

indicating that collateral and bankruptcy laws are better designed to expand access to credit. The

credit information index (credit) measures rules affecting the scope, accessibility and quality of

credit information available through either public or private bureaus. The index ranges from 0 to

6, featuring the credit information system. Higher values indicate that more credit information is

available from either a public registry or a private bureau to facilitate lending decisions. A

negative sign is expected for these variables, that is, better laws in place or more credit

information available lowers the firm probability of default.

4. Research Design

We model the default probability for a set of borrowing firms, using a dynamic binary estimation

method where the dependent variable is 1 if the firm defaults in a specific year and 0 otherwise.

The estimated default probabilities are conditioned over a vector of lagged explanatory variables

including firmspecific financial ratios and countryspecific political and legal risk indicators.

We use export credit guaranteed debt contracts, and to the greatest extent possible, we aim to

picture a realistic decision making process at the time when the lending decision was made.

What comes to lending to highrisk countries, there is usually a special concern regarding the

availability and reliability of the financial information.

10

Data Considerations

The main data for our research project is obtained from the official Export Credit Agency (ECA)

of Finland, Finnvera plc, that consists of trade credit contracts (i.e. commercial loans between

Finnish exporters and foreign buying companies), between years 19802005. These loans are

granted by banks or other financial institutions and guaranteed by Finnvera plc against

commercial and political risks. Detailed credit information underlying each guarantee is

collected by combining data from comprehensive records of Finnvera plc9. This information

includes dates of initiation and the end of the contract; identification number for each guarantee,

information on the parties involved, default date and indemnifications (if any), contract values,

currencies, trade items etc. During the 25year study period, some 30 000 contracts were in force

between Finland and importing companies from over 132 different countries around the world.

Country and Sample Selection

The selected data for this study consists of export credit guaranteed debt contracts between the

Finnvera plc and companies from Argentina, Indonesia, Nigeria, Poland and Saudi Arabia10. The

selection of these countries for this version of the paper is based on choosing the most active

‘highrisk’ export countries of Finland during the last decades, representing five different world

regions. Also on a larger scale, these countries represent type examples of countries that have

received the majority of world export credit. For example, in 1996, Indonesia, Nigeria and

Poland were among the top ten countries, that together accounted for 30 percent of the industrial

country ECAs’ contribution (see Table 1). Argentina, is our example country from the financial

crisis affected Latin American region and Saudi Arabia represents an oildependent, arab nation.

At the policy level, there are of course no obvious reasons to compare these countries as such.

10 In our further research agenda, we plan to append our country selection.

11

Instead, we consider them as type examples of countries facing various economic, commercial

and political risks, where an increasing number of western businesses may still find it desirable

to export and invest in.

We employ the following criteria in our further sample selection;

§ Only firms that are outside governmental control are included in the sample. Thus, credit

counterparts that are public bodies or stateowned enterprises, are excluded11.

§ All industries, except financial sector firms, are included. As common in similar studies,

we exclude banks and financial firms due to the specificity of their financial statements.

§ All different types of guarantee contracts issued by Finnvera are included in the sample.

The most common forms of export credit are buyer credit, credit risk and letter of credit

guarantees, which are also the most common forms of contracts in our sample12.

§ We include contracts that have been effective during some time period between 1980

2005. Thus, some guarantees in the sample have been initiated before 1980 but are still in

force during our study period.

§ Due to limitations in the oldest data and the problem of changes in accounting methods,

we collect data on firm financial variables for firms/guarantees effective after year 1989.

§ We define default as any payment interruption by the debtor company, that deviates from

the scheduled payments stipulated in the guarantee contract.

With these criteria and definitions, our sample consists of 1003 guarantees of which 128 (12.8%)

have experienced a default. Summary statistics of the credit data employed are presented in

Figures 12 and Tables 24.

11 Due to their specific relation to political risk, these are treated separately in an earlier article (Sandström, 2005).

12

For our modeling purposes, we measure our data in firm years, taking into account the yearly

stock of undefaulted effective guarantees and the stock of nonexpired guarantees in a default

state. For each guarantee, we know whether there has been an application for loss on the

underlying claim as well as the indemnifications by Finnvera. We don’t know the exact dates for

the loss claim decision, but have the dates for the corresponding first and last indemnification

payments. Accordingly, we consider the loan in a default state between these dates and analyze

the data in yearly intervals. According to Basel II, we specify the time horizon for the future

probability of default as one year which is consistent with the use in the banking practice and

prevalent in credit risk models.

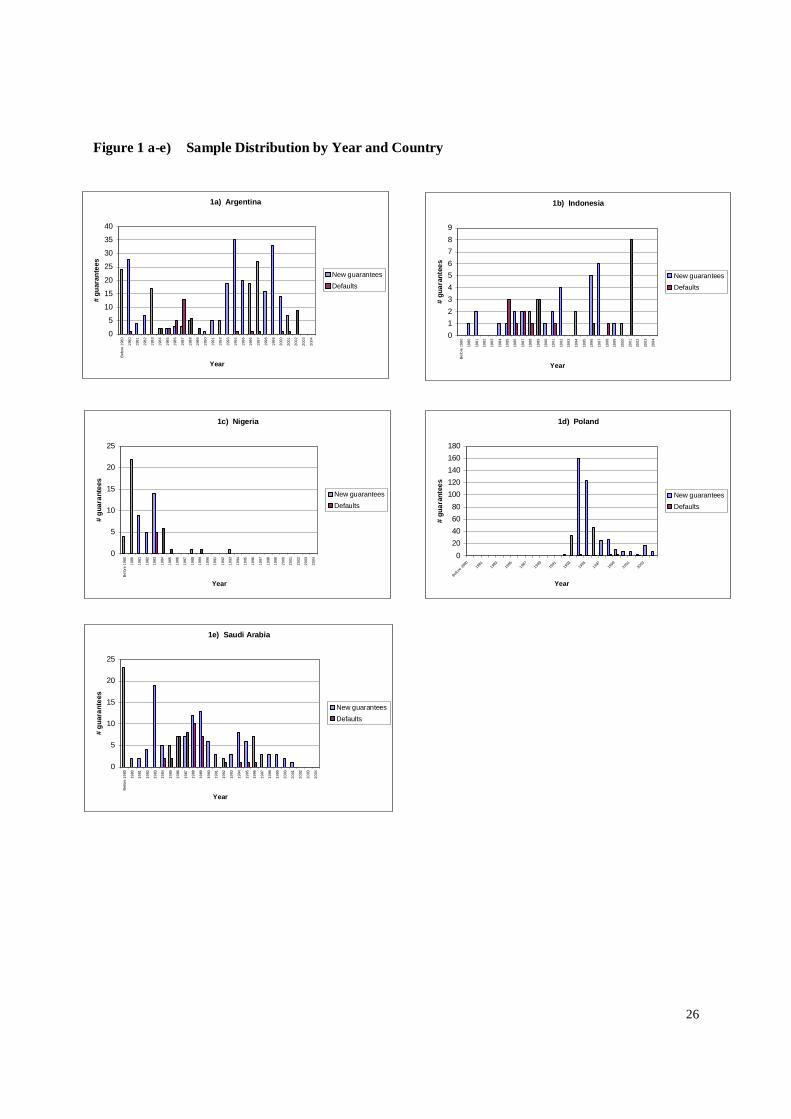

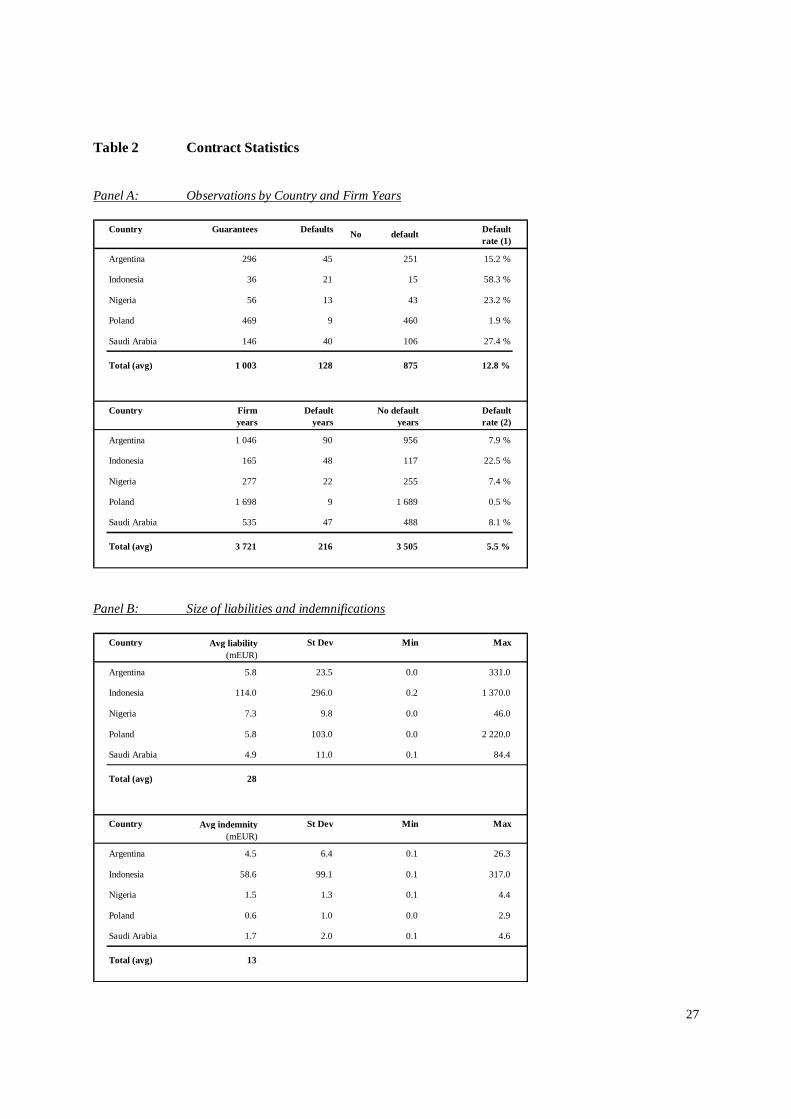

Figures 1ae) illustrate the yearly distribution of new issued guarantees and the number of

defaults by sample countries. Summary statistics on credit contracts and firmyears by default

status and by country are summarized in Table 2 (Panel A). Average liabilities and

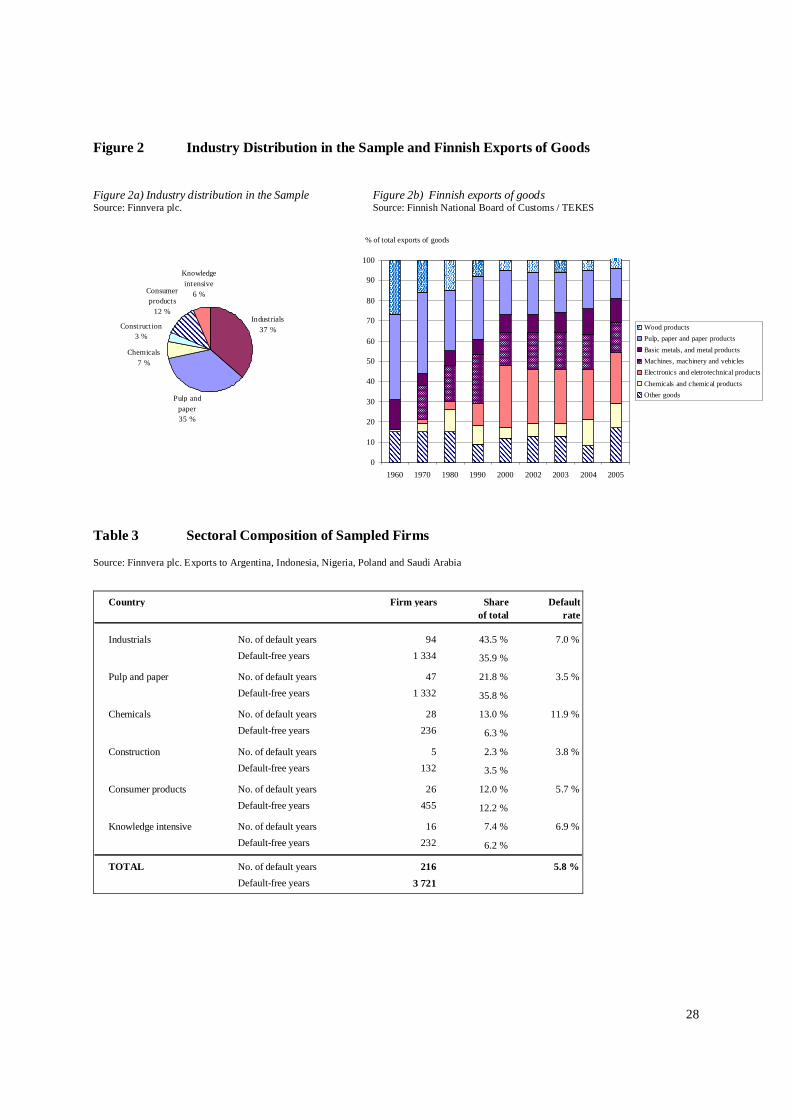

indemnifications by country are summarized in Table 2 (Panel B). Figures 2a and 2b compare

the industry distribution in our sample with the total Finnish Exports given by industry. Pulp and

paper have traditionally accounted for most of the Finnish exports. However, in the 1980s, its

majority share of exports started to fall as a result of the rapid growth in the industrial sector (e.g.

basic metals and metalworking; transport equipment; and electrical equipment). Shipbuilding in

particular, has led the development of heavy industry, and is the most important branch of the

transport sector13. The woodworking industry fostered also the industrials sector through its need

of papermaking equipment (e.g. mechanical and machine building) as well as the chemical sector

(bleaching, water purification, packaging materials etc.). As shown in Table 3 our sample is

fairly evenly split up in the industry groups, both in number of guarantees and in defaults.

12 A special type, an Investment Guarantee emerges a few times in our sample. The difference is that it is bigger in size, and theforms of investment which can be covered under this include equity investments, shareholder loans and guarantees granted by ashareholder. For our purposes, the nature of the guarantee does not affect model estimation.

13

Firm Financial Variables

We choose accounting variables based on how the decision process was initially undertaken,

considering the available information when the credit was granted. Following previous literature,

we select available ratios that measure different dimensions of companies’ healthiness, including

size, age, turnover, profitability, leverage liquidity and solidity. The definitions of the selected

financial ratios are provided in Appendix 2.

In order to collect the available financial figures, a sample of 108 annual, endofyear corporate

financial statement summaries are extracted from Finnvera's credit report database. These yearly

statements belong to 402 unique guarantees, from 1989 to 2005, of which 23 (5.7%) have had at

least one payment interruption or default in a given year. The financial accounts have been

originally obtained from reliable sources including Suomen Asiakastieto Oy, the leading

business and credit information company in Finland, whose data sources comprise the data

subjects, the authorities, and reliable partners14. A smaller part of the credit reports were obtained

from Dun & Bradstreet Credit Bureau and some complements were made directly from available

company financial reports. Summary statistics of the firm financial ratios are given in Table 4,

where Panel A presents the whole sample and Panel B the compares defaulting and non

defaulting firms. Summary statistics for political and legal risk indices (introduced in Section 3)

are presented in Table 5. Table 6 presents the correlations between firm financial (Panel A) and

political (Panel B) and the combined group (Panel C) of explanatory variables. The correlations

are generally very low (in most cases under ±0.2 ), except for icrg and its components, which are

naturally not tested jointly.

13 The biggest guarantee offers by Finnvera are applied to telecommunications and to shipping and shipbuilding.

14

Estimation Technique

The dependent variable yit in our model is the binary discrete variable indicating whether firm i

has defaulted or not in year t. The general representation of the model is

itkitkti eXfy += − ),( 1, β (1)

where kitX 1− represents the values of the k explanatory variables of firm i, (or a country specific

risk index) one year before the evaluation of the dependent variable. To examine the likelihood

of firm default, we estimate

pi,t = Pr ( tiy , = 1) = E ( tiy , | kitX 1− ) (2)

where pi,t is the probability that firm i will default in period t, conditional on the observed

covariates kitX 1− in the previous period. The functional form selected for this study is a dynamic

Logit model. Here, we assume that the variable yit ∈ {0,1} is related to an unobservable index

yi* by a linear function of the lagged explanatory variables xi1, xi2, … . , xik , and the random term

uit such that:

yi* = 0 + 1 xi1 + 2 xi2 + … + k xik + uit ( 3 )

yi = 1 if yi* > 0

yi = 0 otherwise

By this structure, we have

P(yi,t = 1| ‘Xi,t1 ) = P(ui > ‘Xi,t1 ) ( 4 )

= 1 F( ‘Xi,t1 )

with F( ) being the cumulative logistic distribution for u.

14 Suomen Asiakastieto Oy complies with the rules of good data processing practice of the international credit informationagencies FEBIS (Federation of Business Information Services) and ACCIS (Association of Consumer Credit InformationSuppliers).

15

Our methodology is an attempt to respond to the concerns of a singleperiod logit approach15, as

suggested in Shumway (2001) and Beck et al (1998), and will be further refined in our further

research work (e.g. to account for intertemporal correlation). Beck et al. (1998) demonstrate that

the use of ordinary singleperiod logit or probit on binary timeseries/crosssectional data (such

as default study data) can result in biased and inconsistent coefficients, as well as inflated t

statistics. A logistic discrete hazard model overcomes these methodological problems by

formally incorporating the dynamic nature of corporate default (see e.g. Hillegeist et al. 2004).

A logistic discrete hazard model, which is a discrete approximation to the Cox proportional

hazard model has the following form:

X ti,+=−

)(1

log,

, tp

p

ti

ti α , or (4)

X

X

ti

ti

,

,

)(

)(

, 1 +

+

+= t

t

ti eep α

α

(5)

where X ti, represents the independent variables observable at the end of year t and )(tα is a

timevarying covariate that captures the underlying “baseline” hazard rate. This maximum

likelihood estimator differs from ordinary logit by 1) the subscript t , that reflects the use of

multiple years of data for the same firm, and 2) discrete hazard model that includes the baseline

hazard rate )(tα . This allows a firm’s probability of default (and the associated covariates) to

change over time. In this version of the paper, we run the multiyear logit regressions by

assuming that the baseline hazard is constant.

15 Including 1) a sample selection bias from using only one, nonrandomly selected observation per defaulting firm, and 2) afailure to model timevarying changes in the underlying or baseline risk of default that induces crosssectional dependence in thedata.

16

5. Results

We estimate logit regressions for three broad model groups, including the traditional firm

financial ratios (Table 7); political and legal risk variables, either separately (Table 8); or in

combination with the firm financial ratios (Table 9). The hypothesis regarding firm size is not

supported with the data, why we disregard reporting models where the size and age variables are

included.

Accounting Ratios

Table 7 reports the results for Models 14 where lagged firm financial ratios measuring

Profitability and Leverage are tested jointly as predictors of firm default probability. The

indebtnessratio (indebt), measured by total liabilities to total assets, has the expected positive

influence on default probability in Models 1bd. However, it looses its explanatory power as

soon as it is combined with other financial variables or the icrg index (see e.g. Model 2b).

Similarly, the equity ratio (er) has the expected sign, and is significant in Models 1d, 2d and 2e.

The other variables measuring solidity or liquidity have the expected signs, but are not

significant except for the quick ratio (quick) in model 1e, and the net worth ratio (nw_ta) in

model 4b.

A surprising result is that profitability, as measured by earnings before interest, taxes,

depreciation and amortization to total sales (ebitda) seem to have a significant but positive effect

on firm default probability. This would suggest, that the more profitable the firm was (before

interest, depreciation and amortization payments) the more it was likely to default on its debt.

This result has no clear interpretation; however, it allows oneself to be enticed in speculating on

the use of funds by the firms. It seems that these were profitable at first, but still unable or

unwilling to pay their foreign debts. The ratio is, on average, positive for most of the sample

17

firms with a mean value around 10% for the nondefaulting firms, and 20% for the defaulting

firms (see Table 4). This result may, of course, be caused by too few observations (the ebitda

figure is available for only 9 defaulting firms). Firm net profit as a percentage of total assets

(profit_ta) has the expected negative sign and is significant in Models 3a, 3b, 4a, and 4b. While

the significance of some of the individual coefficients in the model are indicative, they do not

provide evidence concerning the collective group significance of accounting information.

We continue our analysis in Table 7 by combining firm financial ratios with the ICRG

Composite Political Risk Index (icrg) in Models 2 and 4. In all except one of the Models (4e),

this ratio gives the expected sign and is highly significant (at 1% level in Models 2ad, 4a and at

5% level in Models 4b4c). Looking at the overall pvalues for the models in Table 7, one can

conclude that they are statistically significant.

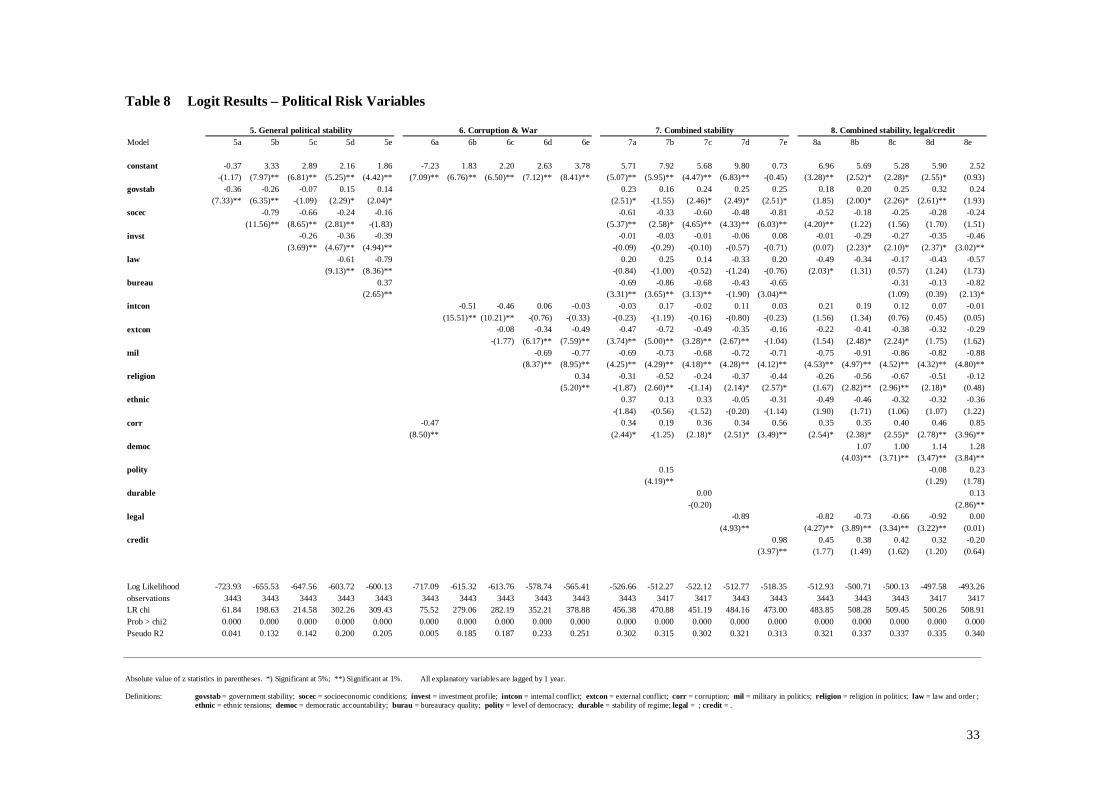

Political and Legal Risk

We next focus on political and legal risk indicators as predictors of firm default probabilities.

The general principle, when interpreting these results is that a negative coefficient for any

political or legal variable, indicates that an increase in the ratio (less risk) reduces the

probability of firm default. In various logit regressions16, most of the ICRG components show

the expected sign and are significant when tested separately. Combined in with each other, the

significance usually diminishes, except for the components measuring Socioeconomic Conditions

(socec), External Conflict (extcon) and Military in Politics (mil). Socioeconomic pressures at

work in a society may constrain government action or fuel social dissatisfaction, leading to

further instabilities. The risk rating is the sum of three subcomponents, including unemployment,

consumer confidence and poverty. It is conceivable that these malfunctions in society may well

16 Not reported here for brevity reasons; details on these are available from the author upon request.

18

lead also to firm deteoriation, and subsequently to its default. The External Conflict measure is

an assessment both of the risk to the incumbent government from foreign action, ranging from

nonviolent external pressure (diplomatic pressures, withholding of aid, trade restrictions,

territorial disputes, sanctions, etc) to violent external pressure (crossborder conflicts to allout

war). One interpretation for the obtained result is that different forms of bilateral punishments do

not seem to act as enforcement mechanisms for debt repayments, but rather the opposite (see e.g.

Rose, 2002). However, external conflicts may also affect businesses adversely in other ways,

ranging from restrictions on operations, to trade and investment sanctions, to distortions in the

allocation of economic resources. Thus, any interpretation of the external conflictvariable

should be adjusted to the country and circumstances in question. Generally, these results would

suggest that the more external pressure a country has, the more the firms operating in that

country are likely to default on their foreign obligations.

It would be misleading to claim that only one political risk rating would serve as a single

predictor variable for firm default. Thus, we present the results in groups measuring 1. General

Political Stability (including government stability, socioeconomic conditions, investment

climate, law and order and bureaucratic accountability); 2. Corruption&War (including

components of corruption, internal and external conflict, military and religion in politics as

well as ethnic tensions); and 3. Combined stability (with all included). Table 8 report the various

results for these groupings. Again, the component measuring Socioeconomic Conditions, remains

a significant predictor of firm default probability (7ae, 8a). Similarly, in models 6de, 7ad, 8bc

the External Conflict component is again negative and significant. Regarding the other political

and legal risk indices, no clearcut patterns may be observed from this data17.

17 The measure of corruption, is significant when measured alone. However, when combined with other components, it changessign and becomes insignificant. The Legal rights Index is significant only in models 7d and 8ae. The Creditor Rights Indexremains insignificant with a opposite sign to the hypothesized.

19

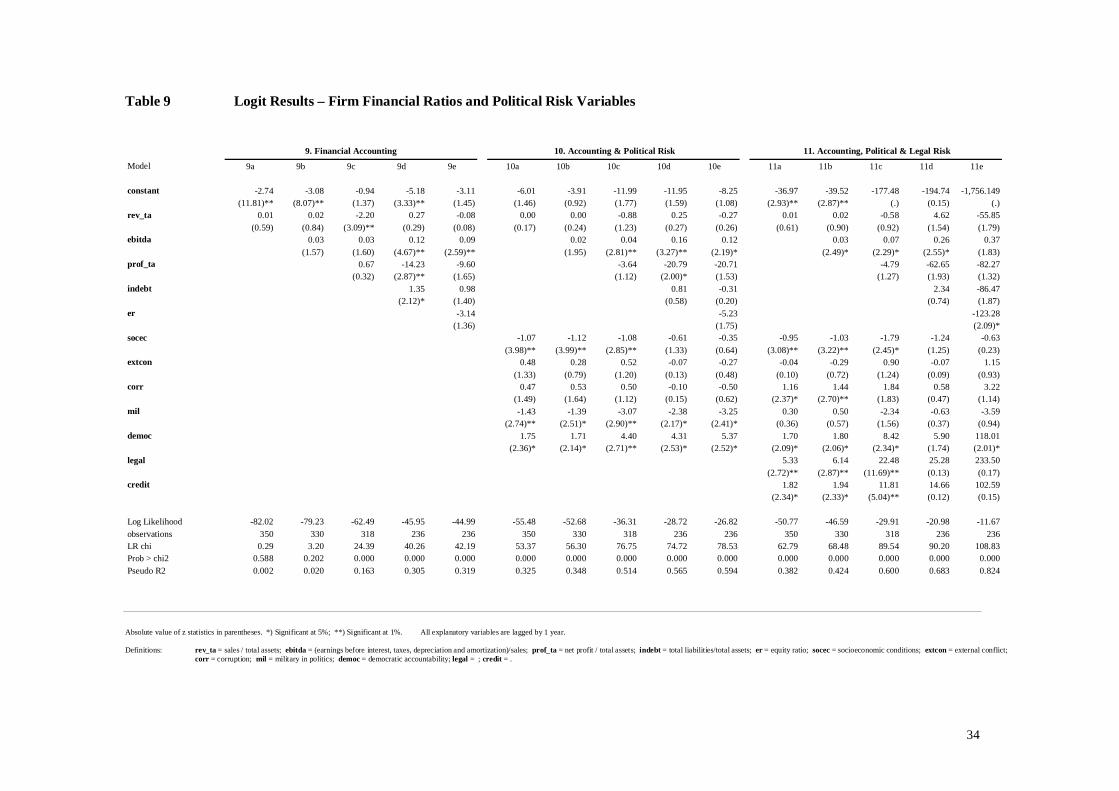

Combined Accounting Information, Political and Legal Risk

Finally, table 9 reports the results for the models, where financial ratios are combined with

selected political and legal indicators. Again, we find interesting results for the ebitdameasure,

which shows positive and significant coefficients (see e.g. models 9de, 10de and 11bd).

Meanwhile, the indebtness measure is significant only in one of the models (9d). On the political

risk side, the Socioeconomic conditions component show again the same significant patterns as

before. Also the Military in Politics component (mil) is significant and negative (e.g. models

10ae). The military’s involvement in politics, even at a peripheral level, can be seen as a

diminution of democratic accountability, and an indication that the government is unable to

function effectively. The signs for the other political and legal indices, when combined with

firm financial ratios, are insignificant or sometimes positive, why they can not be interpreted

within our stated hypothesis framework.

The overall presentiment of the above results is that, analyzed separately, both financial figures

and political risk indices, should be used in the credit evaluation of individual firms in foreign

countries. However, in combination, they might result in overfitting, and may be of little use for

predicting future outcomes.

The sample countries

It is clear that the choice of our sample countries (Argentina, Indonesia, Nigeria, Poland and

Saudi Arabia) may reveal patterns in the default history, that are driven by outside factors. We

briefly point out the main events in our sample countries, in order to assess the relevancy and

interpretability of the obtained results.

20

Among other things;

• The Argentine economic crisis was part of the situation that affected Argentina's whole

economy during the late 1990s and early 2000s. While the high level of Argentinian

defaults in our sample in year 2002 seem selfexplanatory, the situation is more

complicated, as almost all companies operating in the country were affected by the crisis,

but due to renegotiations of the debt contracts, many of them “survived” the difficult

period. The impact of the IMF bailouts and other forms of debt restructurings will be

further analyzed in our future versions of this paper.

• Indonesia is also a crisisaffected country, mainly by the 199798 Asian financial crisis,

which is shown in the default history in our data. However, other patterns of Indonesia

may be reflected in our data including the heavy borrowing from official creditors during

the 1980s. Overall, trading with and investing in Indonesia has for long been perceived to

entail a significant risk of financial loss as the legal system in the country has been

regarded very poor. Throughout the postwar history of Indonesia, the military have

played a key role in the politics of the country.

• In Nigeria, years of military rule, corruption, and mismanagement have hobbled

economic activity and output, and the indebtness situation is complex stemming from

immense interest arrears and external political factors concerning debt reductions. As

demonstrated by Udry (1994) for rural credit in Northern Nigeria, credit imperfections

can arise entirely from the problem of enforcement, rather than eg. imperfect information.

• Poland experienced a transition from a centrally planned to a market orientated economy,

some decade ago. The number of issued guarantees as well as defaults in Poland reflect

the general positive developments in the country during the 1990s as well as the fact, that

the country had rejoined international capital markets and regained favorable credit

ratings, triggering investment inflows.

• Saudi Arabia represents an example of an oildependent arab economy, that has strong

government controls over major economic activities. The country has not been able to

secure oil income for its own finances, which has led to substantial budgetary deficits and

borrowings every year since the early 1980s. The interpretation of the default causes in

Saudi Arabia are far from straightforward.

21

6. Some Conclusions and Suggestions for Further Research

In this study, we have constructed and compared default prediction models for two sets of

explanatory variables; traditional accounting ratios, and countryspecific political and legal risk

indicators. The models applied in this study were tested using export credit guaranteed debt as

underlying credit data. Following previous research, we included firmspecific accounting ratios

as traditional determinants of firm default probability. These included measures of profitability,

leverage, liquidity and solidity. Our new approach is to include measures of political and legal

risk in the analysis. In the second part of the analysis, we thus proxy the general political

stability, corruption, conflict/war, level of democracy, and legal and creditor rights, in

respective sample country by indices from wellestablished country risk experts, and test whether

these may work as good signals of future firm default risk.

Subject to the limitations with our preliminary data from five countries; Argentina, Indonesia,

Nigeria, Poland and Saudi Arabia, the results presented here suggest that indicators of political

risk, indeed affect the firm default probabilities. Without assessing the political and legal risk

landscape, the default probabilities may not be properly estimated using only scarcely available

accounting data. The firm financial variables alone, suggest that measures of indebtness may

indicate for future payment difficulties. Meanwhile, the profitability level is not clear in its

interpretation as the obtained coefficients and significance for the ebitdameasure suggest that

even the more profitable firms tend to default on their debts. This result, together with the high

significance of the ICRG Political Risk Index led our way to further tests with the political and

legal risk components as explanatory variables. From these tests, we can make a preliminary

conclusion that countryspecific measures on socioeconomic conditions, external conflict and

military in politics, seem to serve as justified indicators for firm default.

22

Some explanations for these preliminary results can of course be found by looking at the country

backgrounds. For example, the MENA region (and Saudi Arabia) has been for long the scene of

both internal crises and external conflicts. On several occasions, these crises have affected either

the flow energy exports or the development of energy production and thus, the export and

import capacity of the country. Also the socioeconomic conditions in Poland after the events of

1989 as well as the regime's ultimate collapse and the deflationary shock and rapid transition to a

market economy in 1990, certainly had its impact on the payment ability of the Polish

companies. The story in Indonesia is to a certain extent similar, with our data supporting for the

additional claim that military in politics may ultimately affect also firm defaults in the country.

This is conceivable, looking at Indonesia with the dramatic turnaround and political and

economic crises since 1997, the downfall of Suharto etc. Further, the anecdotal evidence on the

magnitude of corruption in Nigeria can hardly ignored, when considering payback ability and –

willingness of firms operating in Nigeria.

The political, economic, and legal risk dynamics that shape threats to international credit

contracts are complex. Understanding the factors behind these diverse forces as well as future

trends, needs detailed assessment of each country in question, taking each conceivable variable

into careful consideration. Our preliminary results from this study are only indicative, and

subject to further testing with more countries in our sample, further model validation and outof

sample testing. Whereas data drive default prediction models, it is our plan to augment the

sample countries, and include more advanced econometric models in our further research.

23

References

Altman, E.I. 1968. “Financial ratios, Discriminant analysis and the prediction of corporatebankruptcy“. Journal of Finance Vol. 23, pp. 589609

Altman, E.I. 1991. “Techniques for Predicting Bankruptcy and Their Use in a FinancialTurnaround“. In Levine, S.N. (ed.) : Investing in Bankruptcies and Turnarounds:Spotting Investment Values in Distressed Business. New York, NY : HarperCollinsPublishers.

Balkan, E.M. 1992. “Political instability, country risk and probability of default”AppliedEconomics, 24, pp. 9991008.

Beaver, W. 1966. “Financial Ratios as predictors of bankruptcy.”Journal of AccountingResearch (Supplement), pp. 71102.

Beck, N., Katz, J. and Turcker. R. 1998. “Beyond Ordinary Logit: Taking Time Series Seriouslyin BinaryTimeSeriesCrossSection Models”. American Journal of Political Science2(4): 12601288.

Bremmer, I. and DiPiazza. S.A. 2006. “Why political risk Matters” in Integrating Political RiskManagement Into Enterprise Risk Management. PricewaterhouseCoopers and EurasiaGroup.

Brewer, T.L. and Rivoli. P. 1990. "Politics and perceived country creditworthiness ininternational banking", Journal of Money, Credit and Banking, 22 (3), pp. 357369

Caouette, J., Altman E., and Narayanan,P. 1998. Managing Credit Risk: The Next GreatFinancial Challenge. John Wiley & Sons, N.Y.

ChanLau, J.A. 2006. “MarketBased Estimation of Default Probabilities and Its Application toFinancial Surveillance” IMF Working Paper 06/104. Washington; the IMF.

Chuvakhin, N. and Gertmenian, L. 2003. “Predicting Bankruptcy in the WorldCom Age”http://gbr.pepperdine.edu/031/bankruptcy.html [downloaded March, 2005]

Citron, J.T. and Nickelsburg, G. 1987. "Country Risk and Political Instability", Journal ofDevelopment Economics. 25, 2 pp. 385392 Cosset, J.C. and Roy, J. (1991). "Thedeterminants of country risk ratings". Journal of International Business Studies. 22,pp.135142

Davydenko, S.A., and Strebulaev, I.A. 2003. “Strategic Actions and Credit Spreads: AnEmpirical Investigation.” Mimeo. London Business School.

Dewatripont, M., Maskin, E. and Roland, G. (2000). “Soft Budget Constraints and Transition” ineds. Eric Maskin and Adras Simonovits, Planning, Shortage, and Transformation: Essaysin Honor of Janos Kornai, MIT press

Edwards, S. 1984. "LDC foreign borrowing and default risk: An empirical investigation”.American Economic Revue, Sept, vol 74. no. 3. pp. 726735.

Fiztpatrick, P. 1932. “A Comparison of Ratios of Successful Industrial Enterprises with those ofFailed Firms”. Certified Public Accountant 12, pp. 598605.

Gianturco, D.E. 2001. Export Credit Agencies: The Unsung Giants of International Trade andFinance. Quorum/Greenwood.

24

Haendel, D. 1979. Foreign Investments and the Management of Political Risk. WestviewSpecial Studies in International Economics and Business.

Henisz, W.J. 2002. “The Institutional Environment for Infrastructure Investment”. Industrialand Corporate Change 11 (2), pp.35589.

Hillegeist, S.A., E.K.Keating, D.P. Crams and K.G. Lundstedt. 2004. “Assessing the Probabilityof Bankruptcy”. Journal of Accounting Studies, 9. pp. 534.

Hopwood, W.S., J.C. Mckeown, and J.P. Mutchler. 1989. A Test of the Incremental ExplanatoryPower of Opinions Qualified for Consistency and Uncertainty. The Accounting Review64(January): 28–48.

Jensen, N.M. 2006. NationStates and the Multinational Corporation: Political Economy ofForeign Direct Investment. Princeton University Press.

Laitinen, E.K. 1999. “Predicting a Corporate Credit Analysts’s Risk Estimate by Logistic andLinear Models”. International Review of Financial Analysis, 8(2), pp97121.

Maddala, G.S. (1983). Limited Dependent and Qualitative Variables in Econometrics,Cambridge University Press.

Ohlson, J. (1980) “Financial ratios and the probabilistic prediction of bankruptcy.”Journal ofAccounting Research 18(1), pp. 109131.

Peter, M. 2000. “Estimating Default Probabilities of Emerging Market Sovereigns: A New Lookat a NotSoNew Literature”. Working paper, Graduate Institute of International Studies,Geneva.

Platt, H and M. Platt (1990) “Development of a class of state predictive variables: the case ofbankruptcy prediction”Journal fo Business Finance and Accounting, 17, 3151.

Rose, A.K. 2002. “One Reason Countries Repay Their Debts: Renegotiation and InternationalTrade”. NBER Working Paper 8852 (March). http://www.nber.org/papers/W8853.

Saiegh, S. 2005. “Do Countries Have a “Democratic Advantage”?” Political Institutions,Multilateral Agencies and Sovereign Borrowing. Comparative Political Studies 38 (4),pp. 366387.

Sandström, A. 2005. “Public default and Political risk”Working paper. The Swedish School ofEconomics and Business Administration, Helsinki, Finland.

Shumway, T. 2001. "Forecasting bankruptcy more accurately: A simple hazard model", Journalof Business, 74, pp. 101124

Schultz, K. and B. Weingast. 2003. “The Democratic Advantage”. International Organization57. pp. 342.

Schultz, K. and Weingast, B. 1996. “The Democratic Advantage: The Institutional Sources ofInternational Competition”. Ms, Stanford University. Sharpio, A.C. (1981). "Risk inInternational Banking", Journal of Financial and Quantitative Analysis, 17, pp. 72839

Sobehart, J., S. Keenan, and R.Stein (2000). “Benchmarking Quantitative Default Risk Models:A Validation Methodology”, New York: Moody’s Investor Services.

Udry, C. 1994. “Risk and Insurance in a Rural Credit Market: An Empirical Investigation inNorthern Nigeria”. Review of Economic Studies, 61, pp. 495526.

25

Table 1 Twenty Main Recipients of Export Credits Among Developing Countries andCountries in Transition, 1996 (in billions of USD)

Source: Berne Union and International Monetary Fund (IMF), Gianturco (2001)

Country.

USDbnx

Russia 52.9

China 44.8

Indonesia 28.2

Nigeria 24.8

Brazil 24.7

Algeria 23.9

Poland 22.7

Turkey 18.0

Argentina 16.6

Mexico 16.4

Thailand 15.4

Iran, Islamic Republic 14.0

Eqypt 13.6

India 13.0

Iraq 11.2

Philippines 10.5

Hong Kong, SAR 10.1

Venezuela 6.2

South Africa 6.1

Morocco 6.0

26

Figure 1 ae) Sample Distribution by Year and Country

1b) Indonesia

0123456789

Bef

ore

1980

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

# gu

aran

tees

New guaranteesDefaults

1d) Poland

020406080

100120140160180

Before

1980

1981

1983

1985

1987

198919

911993

1995

199719

99200

120

03

Year

# gu

aran

tees

New guaranteesDefaults

1c) Nigeria

0

5

10

15

20

25

Bef

ore

1980

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

# gu

aran

tees

New guaranteesDefaults

1a) Argentina

0

5

10

15

20

25

30

35

40

Bef

ore

1980

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

# gu

aran

tees

New guaranteesDefaults

1e) Saudi Arabia

0

5

10

15

20

25

Bef

ore

1980

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

# gu

aran

tees

New guaranteesDefaults

27

Table 2 Contract Statistics

Panel A: Observations by Country and Firm Years

Country.

Guarantees.

Defaults.

No default Defaultrate (1)

Argentina 296 45 251 15.2 %

Indonesia 36 21 15 58.3 %

Nigeria 56 13 43 23.2 %

Poland 469 9 460 1.9 %

Saudi Arabia 146 40 106 27.4 %

Total (avg) 1 003 128 875 12.8 %

Country.

Firmyears

Defaultyears

No defaultyears

Defaultrate (2)

Argentina 1 046 90 956 7.9 %

Indonesia 165 48 117 22.5 %

Nigeria 277 22 255 7.4 %

Poland 1 698 9 1 689 0.5 %

Saudi Arabia 535 47 488 8.1 %

Total (avg) 3 721 216 3 505 5.5 %

Panel B: Size of liabilities and indemnifications

Country.

Avg liability(mEUR)

St Dev.

Min.

Max.

Argentina 5.8 23.5 0.0 331.0

Indonesia 114.0 296.0 0.2 1 370.0

Nigeria 7.3 9.8 0.0 46.0

Poland 5.8 103.0 0.0 2 220.0

Saudi Arabia 4.9 11.0 0.1 84.4

Total (avg) 28

Country.

Avg indemnity(mEUR)

St Dev.

Min.

Max.

Argentina 4.5 6.4 0.1 26.3

Indonesia 58.6 99.1 0.1 317.0

Nigeria 1.5 1.3 0.1 4.4

Poland 0.6 1.0 0.0 2.9

Saudi Arabia 1.7 2.0 0.1 4.6

Total (avg) 13

28

Figure 2 Industry Distribution in the Sample and Finnish Exports of Goods

Figure 2a) Industry distribution in the Sample Figure 2b) Finnish exports of goodsSource: Finnvera plc. Source: Finnish National Board of Customs / TEKES

% of total exports of goods

Industrials37 %

Pulp andpaper35 %

Chemicals7 %

Construct ion3 %

Consumerproducts

12 %

Knowledgeintensive

6 %

0

10

20

30

40

50

60

70

80

90

100

1960 1970 1980 1990 2000 2002 2003 2004 2005

Wood productsPulp, paper and paper productsBasic metals, and metal productsMachines, machinery and vehiclesElectronics and eletrotechnical productsChemicals and chemical productsOther goods

Table 3 Sectoral Composition of Sampled Firms

Source: Finnvera plc. Exports to Argentina, Indonesia, Nigeria, Poland and Saudi Arabia

Country.

Firm years.

Shareof total

Defaultrate

Industrials No. of default years 94 43.5 % 7.0 %Defaultfree years 1 334 35.9 %

Pulp and paper No. of default years 47 21.8 % 3.5 %Defaultfree years 1 332 35.8 %

Chemicals No. of default years 28 13.0 % 11.9 %Defaultfree years 236 6.3 %

Construction No. of default years 5 2.3 % 3.8 %Defaultfree years 132 3.5 %

Consumer products No. of default years 26 12.0 % 5.7 %Defaultfree years 455 12.2 %

Knowledge intensive No. of default years 16 7.4 % 6.9 %Defaultfree years 232 6.2 %

TOTAL No. of default years 216 5.8 %Defaultfree years 3 721

29

Table 4 Descriptive Statistics – Firm Variables

Panel A: Observations by Firm Years

Variable

agerevprofit

wcnwassetsliabequity

rev_taebitdaprof_taerindebtcurrentquicknw_ta

MaxObs Mean Std.Dev Min

64.0788 85.1 138.1 0.0 785.02470 24.2 19.5 1.0

139.8727 6.3 19.6 3.8

12.7700 32.0 70.9 19.3 403.9188 6.3 24.7 102.2

1085.1705 51.6 139.1 0.4 792.0749 93.2 208.6 0.0

403.9716 31.0 66.7 1.6

90.3711 0.1 0.2 1.3 0.5740 6.3 18.2 0.0

1.1705 0.2 1.3 5.1 1.1716 0.0 0.2 1.0

2.3509 2.7 10.1 0.0 83.3533 0.5 0.4 0.0

4.6690 0.5 0.3 0.5 1.2355 1.1 0.7 0.0

Panel B: Comparison Between Defaulting and Nondefaulting Firms

Variable

Comparison y = 0 y = 1 y = 0 y = 1 y = 0 y = 1 y = 0 y = 1 y = 0 y = 1

age 317 9 24.1 31.6 19.4 25.7 1.0 6.0 64.0 64.0rev 349 23 84.3 248.6 144.4 253.9 0.0 0.0 785.0 530.0profit 323 21 6.8 21.9 19.9 23.1 3.8 0.4 139.8 45.6

wc 93 3 7.2 5.9 24.5 3.3 93.5 2.1 7.8 7.8nw 304 21 39.2 104.1 83.2 101.6 19.3 0.9 359.8 207.9assets 336 23 100.4 452.6 208.8 491.6 0.0 0.0 1085.1 999.9liab 308 21 58.5 391.6 144.7 391.9 0.4 2.1 792.0 792.0equity 315 18 34.3 85.0 69.6 63.1 1.6 1.6 359.9 138.9

rev_ta 336 23 3.7 4.0 12.2 10.8 0.0 0.0 86.2 38.3ebitda 316 23 0.1 0.2 0.2 0.3 1.3 1.3 0.5 0.5prof_ta 317 21 0.0 0.0 0.1 0.0 0.8 0.1 1.1 0.1er 313 21 0.3 0.2 0.9 0.2 5.1 0.4 0.9 0.5indebt 236 20 0.6 1.0 0.4 0.6 0.0 0.0 2.3 1.5current 241 20 3.3 0.9 11.6 0.3 0.2 0.2 83.3 1.2quick 157 10 1.1 1.3 0.7 0.6 0.0 0.6 4.6 2.0nw_ta 303 21 0.4 0.3 0.3 0.2 0.5 0.3 1.2 0.6

MaxObs Mean Std.Dev Min

Definitions: age = years since firm establishment; rev = sales (USDm); profit = net profit (USDm); wc = working capital (USDm); nw = net worth (USDm); assets = total assets (USDm);liab = total liabilities (USDm); equity = owners equity (USDm); rev_ta = sales / total assets; ebitda = (earnings before interest, taxes, depreciation and amortization)/sales;prof_ta = net profit / total assets; er = equity ratio; indebt = total liabilities/total assets; current = current ratio; quick = quick ratio; nw_ta = net worth / total assets.

30

Table 5 Descriptive Statistics – Political Risk Variables by Country

Rating Obs Mean Std. Dev. Min Max Rating Obs Mean Std. Dev. Min Max

icrg Argentina 21 66.10 8.20 53.67 76.42 religion Argentina 21 5.56 0.50 5.00 6.00Indonesia 21 50.95 8.76 39.83 66.92 Indonesia 21 2.53 1.39 1.00 5.00Nigeria 21 46.61 4.81 38.79 54.33 Nigeria 21 1.98 0.71 0.50 3.00Poland 21 69.26 12.31 47.57 86.58 Poland 21 3.81 1.57 1.00 5.00Saudi Arabia 21 61.51 7.59 49.25 70.00 Saudi Arabia 21 2.47 1.15 1.00 4.00

govstab Argentina 21 6.70 1.89 4.25 10.33 law Argentina 21 3.68 1.09 1.50 5.00Indonesia 21 7.39 1.40 5.50 10.75 Indonesia 21 2.68 1.02 1.50 4.75Nigeria 21 6.67 2.02 3.75 10.50 Nigeria 21 2.05 0.92 1.00 3.00Poland 21 6.87 1.67 4.50 10.58 Poland 21 4.52 0.75 4.00 6.00Saudi Arabia 21 8.22 1.70 5.92 10.92 Saudi Arabia 21 4.53 0.66 3.00 5.50

socec Argentina 21 4.90 1.34 2.13 6.75 ethnic Argentina 21 6.00 0.00 6.00 6.00Indonesia 21 5.31 2.22 2.00 8.58 Indonesia 21 2.13 0.75 1.00 3.00Nigeria 21 4.06 1.94 1.50 7.00 Nigeria 21 2.54 0.90 1.00 4.00Poland 21 5.22 0.62 4.08 6.92 Poland 21 5.55 0.50 5.00 6.00Saudi Arabia 21 6.85 1.17 5.46 9.75 Saudi Arabia 21 4.34 0.91 2.00 5.00

invest Argentina 21 5.57 1.41 3.33 8.00 democ Argentina 21 4.44 0.49 3.67 5.00Indonesia 21 6.12 1.31 4.00 8.92 Indonesia 21 3.15 0.76 1.00 4.83Nigeria 21 5.40 0.84 4.00 7.00 Nigeria 21 2.45 0.86 0.50 3.58Poland 21 7.26 2.79 3.17 11.50 Poland 21 4.13 1.72 1.57 6.00Saudi Arabia 21 7.70 1.88 5.33 11.00 Saudi Arabia 21 1.14 0.98 0.00 2.00

intcon Argentina 21 9.53 1.56 6.17 12.00 buerau Argentina 21 2.35 0.48 2.00 3.00Indonesia 21 6.88 1.41 4.08 9.00 Indonesia 21 1.31 1.10 0.00 3.00Nigeria 21 7.41 1.91 4.58 11.00 Nigeria 21 1.28 0.66 0.00 2.00Poland 21 10.08 1.46 8.00 12.00 Poland 21 2.44 0.95 1.00 3.33Saudi Arabia 21 8.74 2.02 4.67 12.00 Saudi Arabia 21 2.37 0.48 2.00 3.00

extcon Argentina 21 10.53 1.27 8.75 12.00 polity Argentina 24 5.54 5.38 9.00 8.00Indonesia 21 10.49 1.00 8.83 12.00 Indonesia 24 4.00 5.78 7.00 7.00Nigeria 21 10.03 0.79 7.58 11.50 Nigeria 24 5.29 18.53 88.00 7.00Poland 21 10.79 1.78 7.00 12.00 Poland 24 2.63 7.63 8.00 10.00Saudi Arabia 21 8.59 1.81 5.08 11.04 Saudi Arabia 24 10.00 0.00 10.00 10.00

corr Argentina 21 3.18 0.78 2.00 4.00 durable Argentina 24 9.38 6.03 0.00 20.00Indonesia 21 1.43 1.07 0.00 3.00 Indonesia 24 16.54 9.93 0.00 30.00Nigeria 21 1.67 0.45 1.00 2.00 Nigeria 24 4.63 3.99 0.00 13.00Poland 21 3.97 1.11 2.00 5.00 Poland 24 17.13 16.14 0.00 41.00Saudi Arabia 21 2.21 0.44 2.00 3.33 Saudi Arabia 24 65.50 7.07 54.00 77.00

mil Argentina 21 3.67 0.88 2.00 5.00Indonesia 21 1.52 0.78 0.00 2.50Nigeria 21 1.06 0.79 0.00 2.67Poland 21 4.63 2.06 1.00 6.00Saudi Arabia 21 4.37 0.87 3.00 5.00

Definitions: icrg = composite ICRG political risk index; govstab = government stability; socec = socioeconomic conditions; invest = investment profile; intcon = internal conflict;extcon = external conflict; corr = corruption; mil = military in politics; religion = religion in politics; law = law and order ; ethnic = ethnic tensions;democ = democratic accountability; burau = bureauracy quality; polity = level of democracy; durable = stability of regime.

31

Table 6 Correlation Among Explanatory Variables

Panel A: Firm Variables

rev_ta ebitda prof_ta indebt nw_ta er current quickrev_ta 1ebitda 0.052 1prof_ta 0.825 0.348 1indebt 0.385 0.446 0.298 1nw_ta 0.362 0.225 0.347 0.268 1er 0.011 0.161 0.167 0.052 0.467 1current 0.045 0.099 0.028 0.283 0.191 0.294 1quick 0.037 0.374 0.185 0.052 0.196 0.179 0.093 1

Panel B: Political Risk Variables

icrg govstab socec invest intconfl extconfl corrupt military religion law ethnic democ buerauc autoc polity durableicrg 1govstab 0.366 1socec 0.379 0.011 1invest 0.564 0.550 0.504 1intconfl 0.832 0.199 0.240 0.283 1extconfl 0.488 0.076 0.046 0.092 0.493 1corrupt 0.556 0.222 0.138 0.033 0.484 0.184 1military 0.849 0.320 0.243 0.468 0.646 0.304 0.467 1religion 0.777 0.092 0.122 0.175 0.656 0.529 0.469 0.544 1law 0.804 0.385 0.409 0.389 0.727 0.174 0.520 0.734 0.499 1ethnic 0.812 0.061 0.175 0.233 0.754 0.240 0.689 0.698 0.751 0.664 1democ 0.427 0.131 0.200 0.076 0.274 0.449 0.297 0.306 0.571 0.027 0.342 1buerauc 0.621 0.169 0.112 0.237 0.382 0.065 0.494 0.660 0.453 0.518 0.583 0.313 1autoc 0.001 0.146 0.388 0.095 0.030 0.063 0.070 0.034 0.136 0.039 0.040 0.161 0.087 1polity 0.374 0.141 0.174 0.057 0.247 0.432 0.331 0.368 0.431 0.089 0.400 0.657 0.411 0.423 1durable 0.127 0.314 0.548 0.388 0.084 0.453 0.135 0.258 0.201 0.434 0.088 0.624 0.108 0.403 0.391 1

Panel C: Combined

rev_ta ebitda prof_ta indebt current quick er nw_ta icrg polity durable legal creditrev_ta 1ebitda 0.051 1prof_ta 0.826 0.348 1indebt 0.395 0.455 0.303 1current 0.030 0.099 0.026 0.245 1quick 0.035 0.373 0.184 0.062 0.072 1er 0.005 0.159 0.167 0.077 0.253 0.172 1nw_ta 0.368 0.224 0.350 0.287 0.165 0.191 0.460 1icrg 0.074 0.125 0.218 0.123 0.109 0.143 0.103 0.009 1polity 0.122 0.097 0.046 0.278 0.054 0.314 0.035 0.094 0.452 1durable 0.196 0.171 0.123 0.331 0.005 0.325 0.023 0.072 0.446 0.955 1legal 0.133 0.159 0.077 0.281 0.024 0.298 0.040 0.048 0.449 0.988 0.974 1credit 0.013 0.433 0.183 0.002 0.522 0.059 0.530 0.305 0.078 0.288 0.328 0.402 1.000

Definitions: age = years since firm establishment; rev = sales (USDm); profit = net profit (USDm); wc = working capital (USDm); nw = net worth (USDm); assets = total assets (USDm); liab = total liabilities (USDm); equity = owners equity (USDm); rev_ta = sales / total assets; ebitda = (earnings before interest, taxes, depreciation and amortization)/sales;

prof_ta = net profit / total assets; er = equity ratio; indebt = total liabilities/total assets; current = current ratio; quick = quick ratio; nw_ta = net worth / total assets.

icrg = composite ICRG political risk index; govstab = government stability; socec = socioeconomic conditions; invest = investment profile; intcon = internal conflict;extcon = external conflict; corr = corruption; mil = military in politics; religion = religion in politics; law = law and order ; ethnic = ethnic tensions;democ = democratic accountability; burau = bureauracy quality; polity = level of democracy; durable = stability of regime.

32

Table 7 Logit Results – Firm Variables and ICRGIndex

Model 1a 1b 1c 1d 1e 2a 2b 2c 2d 2e 3a 3b 3c 3d 3e 4a 4b 4c 4d 4e

constant 0.94 3.78 3.11 1.63 0.68 5.01 5.59 6.60 7.69 5.74 5.18 3.89 2.54 2.01 4.56 1.58 3.56 4.81 5.95 8.55(1.37) (8.10)** (4.57)** (2.19)* (0.34) (3.38)** (2.21)* (2.45)* (2.89)** (0.72) (3.33)** (2.41)* (1.16) (0.63) (1.12) (0.53) (1.00) (1.32) (1.39) (0.93)

rev_ta 2.20 1.03 0.27 0.36 0.06 0.32 1.06 0.40 0.32 0.06 0.41 0.94(3.09)** (1.54) (0.29) (0.39) (0.05) (0.20) (0.67) (0.45) (0.38) (0.07) (0.28) (0.55)

ebitda 0.03 0.03 0.12 0.14 0.12 0.11 0.12 0.10 0.12 0.09 0.08 0.12(1.60) (2.16)* (4.67)** (4.52)** (3.19)** (2.29)* (1.98)* (3.83)** (3.67)** (2.43)* (1.73) (1.95)

prof_ta 0.67 0.04 14.23 12.65 10.34 9.19 8.91 14.70 12.60 10.08 8.51 8.04(0.32) (0.02) (2.87)** (2.24)* (1.73) (1.60) (1.61) (2.81)** (2.21)* (1.70) (1.57) (1.41)

indebt 1.79 1.57 1.22 0.12 0.21 0.15 0.36 0.35 1.35 0.78 0.54 0.51 3.70 0.41 0.43 0.60 0.67 3.66(3.90)** (3.24)** (2.56)* (0.06) (0.31) (0.20) (0.50) (0.16) (2.12)* (1.16) (0.75) (0.55) (1.05) (0.55) (0.46) (0.66) (0.60) (1.05)

nw_ta 1.32 1.05 2.65 1.60 0.24 1.80 3.98 3.94 4.25 2.43 4.26 4.12 4.70 2.01(1.10) (0.76) (0.96) (1.41) (0.17) (0.65) (1.91) (1.78) (1.82) (0.84) (1.98)* (1.79) (1.88) (0.68)

er 6.61 3.12 6.17 6.52 2.01 2.79 4.80 2.21 2.82 4.92(3.52)** (1.07) (3.25)** (2.60)** (0.89) (1.08) (1.65) (0.93) (0.99) (1.68)

current 1.81 0.13 0.42(1.46) (0.23) (0.39)

quick 1.62 0.39 0.04 0.03(2.09)* (0.77) (0.06) (0.04)

icrg 0.10 0.12 0.12 0.12 0.05 0.09 0.09 0.09 0.09 0.05(4.16)** (3.73)** (3.71)** (3.64)** (0.51) (2.61)** (2.38)* (2.41)* (2.49)* (0.48)

Log Likelihood 62.49 59.76 58.54 52.13 25.20 53.41 51.40 50.09 44.16 28.52 45.95 42.80 42.40 41.31 24.73 42.19 39.47 39.03 37.68 24.60observations 318 249 237 237 162 318 249 237 237 162 236 228 228 214 153 236 228 228 214 153LR chi 24.39 14.76 15.26 28.08 19.12 42.55 31.48 32.15 44.01 12.47 40.26 45.20 46.00 45.67 18.99 47.78 51.86 52.74 52.92 19.25Prob > chi2 0.000 0.000 0.001 0.000 0.002 0.000 0.000 0.000 0.000 0.029 0.000 0.000 0.000 0.000 0.008 0.000 0.000 0.000 0.000 0.014Pseudo R2 0.163 0.110 0.115 0.212 0.275 0.285 0.234 0.243 0.333 0.179 0.305 0.346 0.352 0.356 0.277 0.362 0.397 0.403 0.413 0.281

1. Profitability vs. indebtness 2. Profitability, indebtness & ICRG 3. Profitability and leverage 4. Profitability, leverage & ICRG

Absolute value of z statistics in parentheses. *) Significant at 5%; **) Significant at 1%.

Definitions: rev_ta = sales / total assets; ebitda = (earnings before interest, taxes, depreciation and amortization)/sales; prof_ta = net profit / total assets; indebt = total liabilities/total assets; nw_ta = net worth / total assets er = equity ratio;current = current ratio; quick = quick ratio; icrg = composite ICRG political risk index.

All explanatory variables are lagged by 1 year.

33

Table 8 Logit Results – Political Risk Variables

Model 5a 5b 5c 5d 5e 6a 6b 6c 6d 6e 7a 7b 7c 7d 7e 8a 8b 8c 8d 8e

constant 0.37 3.33 2.89 2.16 1.86 7.23 1.83 2.20 2.63 3.78 5.71 7.92 5.68 9.80 0.73 6.96 5.69 5.28 5.90 2.52(1.17) (7.97)** (6.81)** (5.25)** (4.42)** (7.09)** (6.76)** (6.50)** (7.12)** (8.41)** (5.07)** (5.95)** (4.47)** (6.83)** (0.45) (3.28)** (2.52)* (2.28)* (2.55)* (0.93)

govstab 0.36 0.26 0.07 0.15 0.14 0.23 0.16 0.24 0.25 0.25 0.18 0.20 0.25 0.32 0.24(7.33)** (6.35)** (1.09) (2.29)* (2.04)* (2.51)* (1.55) (2.46)* (2.49)* (2.51)* (1.85) (2.00)* (2.26)* (2.61)** (1.93)

socec 0.79 0.66 0.24 0.16 0.61 0.33 0.60 0.48 0.81 0.52 0.18 0.25 0.28 0.24(11.56)** (8.65)** (2.81)** (1.83) (5.37)** (2.58)* (4.65)** (4.33)** (6.03)** (4.20)** (1.22) (1.56) (1.70) (1.51)

invst 0.26 0.36 0.39 0.01 0.03 0.01 0.06 0.08 0.01 0.29 0.27 0.35 0.46(3.69)** (4.67)** (4.94)** (0.09) (0.29) (0.10) (0.57) (0.71) (0.07) (2.23)* (2.10)* (2.37)* (3.02)**

law 0.61 0.79 0.20 0.25 0.14 0.33 0.20 0.49 0.34 0.17 0.43 0.57(9.13)** (8.36)** (0.84) (1.00) (0.52) (1.24) (0.76) (2.03)* (1.31) (0.57) (1.24) (1.73)

bureau 0.37 0.69 0.86 0.68 0.43 0.65 0.31 0.13 0.82(2.65)** (3.31)** (3.65)** (3.13)** (1.90) (3.04)** (1.09) (0.39) (2.13)*

intcon 0.51 0.46 0.06 0.03 0.03 0.17 0.02 0.11 0.03 0.21 0.19 0.12 0.07 0.01(15.51)** (10.21)** (0.76) (0.33) (0.23) (1.19) (0.16) (0.80) (0.23) (1.56) (1.34) (0.76) (0.45) (0.05)

extcon 0.08 0.34 0.49 0.47 0.72 0.49 0.35 0.16 0.22 0.41 0.38 0.32 0.29(1.77) (6.17)** (7.59)** (3.74)** (5.00)** (3.28)** (2.67)** (1.04) (1.54) (2.48)* (2.24)* (1.75) (1.62)

mil 0.69 0.77 0.69 0.73 0.68 0.72 0.71 0.75 0.91 0.86 0.82 0.88(8.37)** (8.95)** (4.25)** (4.29)** (4.18)** (4.28)** (4.12)** (4.53)** (4.97)** (4.52)** (4.32)** (4.80)**

religion 0.34 0.31 0.52 0.24 0.37 0.44 0.26 0.56 0.67 0.51 0.12(5.20)** (1.87) (2.60)** (1.14) (2.14)* (2.57)* (1.67) (2.82)** (2.96)** (2.18)* (0.48)

ethnic 0.37 0.13 0.33 0.05 0.31 0.49 0.46 0.32 0.32 0.36(1.84) (0.56) (1.52) (0.20) (1.14) (1.90) (1.71) (1.06) (1.07) (1.22)

corr 0.47 0.34 0.19 0.36 0.34 0.56 0.35 0.35 0.40 0.46 0.85(8.50)** (2.44)* (1.25) (2.18)* (2.51)* (3.49)** (2.54)* (2.38)* (2.55)* (2.78)** (3.96)**

democ 1.07 1.00 1.14 1.28(4.03)** (3.71)** (3.47)** (3.84)**

polity 0.15 0.08 0.23(4.19)** (1.29) (1.78)

durable 0.00 0.13(0.20) (2.86)**

legal 0.89 0.82 0.73 0.66 0.92 0.00(4.93)** (4.27)** (3.89)** (3.34)** (3.22)** (0.01)

credit 0.98 0.45 0.38 0.42 0.32 0.20(3.97)** (1.77) (1.49) (1.62) (1.20) (0.64)

Log Likelihood 723.93 655.53 647.56 603.72 600.13 717.09 615.32 613.76 578.74 565.41 526.66 512.27 522.12 512.77 518.35 512.93 500.71 500.13 497.58 493.26observations 3443 3443 3443 3443 3443 3443 3443 3443 3443 3443 3443 3417 3417 3443 3443 3443 3443 3443 3417 3417LR chi 61.84 198.63 214.58 302.26 309.43 75.52 279.06 282.19 352.21 378.88 456.38 470.88 451.19 484.16 473.00 483.85 508.28 509.45 500.26 508.91Prob > chi2 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000Pseudo R2 0.041 0.132 0.142 0.200 0.205 0.005 0.185 0.187 0.233 0.251 0.302 0.315 0.302 0.321 0.313 0.321 0.337 0.337 0.335 0.340

5. General political stability 7. Combined stability 6. Corruption & War 8. Combined stability, legal/credit

Absolute value of z statistics in parentheses. *) Significant at 5%; **) Significant at 1%. All explanatory variables are lagged by 1 year.

Definitions: govstab = government stability; socec = socioeconomic conditions; invest = investment profile; intcon = internal conflict; extcon = external conflict; corr = corruption; mil = military in politics; religion = religion in politics; law = law and order ;ethnic = ethnic tensions; democ = democratic accountability; burau = bureauracy quality; polity = level of democracy; durable = stability of regime; legal = ; credit = .

34

Table 9 Logit Results – Firm Financial Ratios and Political Risk Variables

Model 9a 9b 9c 9d 9e 10a 10b 10c 10d 10e 11a 11b 11c 11d 11e

constant 2.74 3.08 0.94 5.18 3.11 6.01 3.91 11.99 11.95 8.25 36.97 39.52 177.48 194.74 1,756.149(11.81)** (8.07)** (1.37) (3.33)** (1.45) (1.46) (0.92) (1.77) (1.59) (1.08) (2.93)** (2.87)** (.) (0.15) (.)

rev_ta 0.01 0.02 2.20 0.27 0.08 0.00 0.00 0.88 0.25 0.27 0.01 0.02 0.58 4.62 55.85(0.59) (0.84) (3.09)** (0.29) (0.08) (0.17) (0.24) (1.23) (0.27) (0.26) (0.61) (0.90) (0.92) (1.54) (1.79)

ebitda 0.03 0.03 0.12 0.09 0.02 0.04 0.16 0.12 0.03 0.07 0.26 0.37(1.57) (1.60) (4.67)** (2.59)** (1.95) (2.81)** (3.27)** (2.19)* (2.49)* (2.29)* (2.55)* (1.83)

prof_ta 0.67 14.23 9.60 3.64 20.79 20.71 4.79 62.65 82.27(0.32) (2.87)** (1.65) (1.12) (2.00)* (1.53) (1.27) (1.93) (1.32)

indebt 1.35 0.98 0.81 0.31 2.34 86.47(2.12)* (1.40) (0.58) (0.20) (0.74) (1.87)

er 3.14 5.23 123.28(1.36) (1.75) (2.09)*

socec 1.07 1.12 1.08 0.61 0.35 0.95 1.03 1.79 1.24 0.63(3.98)** (3.99)** (2.85)** (1.33) (0.64) (3.08)** (3.22)** (2.45)* (1.25) (0.23)

extcon 0.48 0.28 0.52 0.07 0.27 0.04 0.29 0.90 0.07 1.15(1.33) (0.79) (1.20) (0.13) (0.48) (0.10) (0.72) (1.24) (0.09) (0.93)

corr 0.47 0.53 0.50 0.10 0.50 1.16 1.44 1.84 0.58 3.22(1.49) (1.64) (1.12) (0.15) (0.62) (2.37)* (2.70)** (1.83) (0.47) (1.14)

mil 1.43 1.39 3.07 2.38 3.25 0.30 0.50 2.34 0.63 3.59(2.74)** (2.51)* (2.90)** (2.17)* (2.41)* (0.36) (0.57) (1.56) (0.37) (0.94)

democ 1.75 1.71 4.40 4.31 5.37 1.70 1.80 8.42 5.90 118.01(2.36)* (2.14)* (2.71)** (2.53)* (2.52)* (2.09)* (2.06)* (2.34)* (1.74) (2.01)*

legal 5.33 6.14 22.48 25.28 233.50(2.72)** (2.87)** (11.69)** (0.13) (0.17)

credit 1.82 1.94 11.81 14.66 102.59(2.34)* (2.33)* (5.04)** (0.12) (0.15)

Log Likelihood 82.02 79.23 62.49 45.95 44.99 55.48 52.68 36.31 28.72 26.82 50.77 46.59 29.91 20.98 11.67observations 350 330 318 236 236 350 330 318 236 236 350 330 318 236 236LR chi 0.29 3.20 24.39 40.26 42.19 53.37 56.30 76.75 74.72 78.53 62.79 68.48 89.54 90.20 108.83Prob > chi2 0.588 0.202 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000Pseudo R2 0.002 0.020 0.163 0.305 0.319 0.325 0.348 0.514 0.565 0.594 0.382 0.424 0.600 0.683 0.824

9. Financial Accounting 10. Accounting & Political Risk 11. Accounting, Political & Legal Risk

Absolute value of z statistics in parentheses. *) Significant at 5%; **) Significant at 1%. All explanatory variables are lagged by 1 year.

Definitions: rev_ta = sales / total assets; ebitda = (earnings before interest, taxes, depreciation and amortization)/sales; prof_ta = net profit / total assets; indebt = total liabilities/total assets; er = equity ratio; socec = socioeconomic conditions; extcon = external conflict;corr = corruption; mil = military in politics; democ = democratic accountability; legal = ; credit = .

35

Appendix I Description of Political Risk Variables

1) The International Country Risk Guide (ICRG)Source: Researchers Dataset (April, 2005), The PRS Group.

The ICRG rating comprises 22 variables in three subcategories of risk: political, financial, and economic. We apply thePolitical Risk index that is based on 100 points. The following risk components and weights are used to produce thepolitical risk rating.

Risk Component Weight Short name

A.Government Stability (12) govstabB. Socioeconomic Conditions (12) socecC. Investment Profile (12) investD. Internal conflict (12) intconE. External Conflict (12) extconF. Corruption (6) corrG. Military in Politics (6) milH. Religion in Politics (6) religionI. Law and Order (6) lawJ. Ethnic Tensions (6) ethnicK. Democratic Accountability (6) democL. Bureaucracy Quality (4) bureauComposite ICRG Political Risk (100) icrg

2) POLITY IVSource: Center for International Development and Conflict Management, University of Maryland.

The POLITY IV project rates the levels of democracy of all independent states from 1800 to 1999 resulting in a "PolityIndex", which has scale from 10 to +10 measuring the degree to which a nation is either autocratic or democratic. A scoreof +10 indicates a strongly democratic state; a score of 10 a strongly autocratic state. The Polity IV Regime DurabilityVariable measures the years since the most recent regime change (defined by a three point change in the POLITY scoreover a period of three years or less) or the end of a transition period defined by the lack of stable political institutions.

Variable Short name