POLARCUS LIMITED an exempted company incorporated under ...

160

1 POLARCUS LIMITED (an exempted company incorporated under the laws of the Cayman Islands) The information contained in this prospectus (the "Prospectus") relates to the contemplated listing on Oslo Børs of (i) 230,769,231 new shares in Polarcus Limited ("Polarcus" or the "Company", and when taken together with its consolidated subsidiaries, the "Group" or the "Polarcus Group"), each with a par value of USD 0.10 (the "Private Placement Shares") and (ii) 98,809,712 new shares in Polarcus, with a par value of USD 0.10 each (the "Bond Conversion Shares" and together with the Private Placement Shares the "New Shares"). The Private Placement Shares were issued on 1 March 2018 to investors that were allocated shares in the private placement that was successfully placed on 26 January 2018 (the "Private Placement"). The Bond Conversion Shares were issued on 13 March 2018 to holders of unsecured bonds who accepted the offer described in the summons published on 26 January 2018 to convert part of their bonds to new shares (the "Bond Conversion Offer"). The contemplated listing of the New Shares on Oslo Børs is expected to take place on or about 22 March 2018. In addition, the Prospectus relates to the repair offering (the "Repair Offering") by the Company of 30,769,231 new shares with a par value of USD 0.10 each (the "Offer Shares") at a subscription price of NOK 1.30 per Offer Share. In connection with the Repair Offering, non-transferable subscription rights (the "Subscription Rights") will be granted to shareholders of the Company as of 25 January 2018, as registered in the Norwegian Central Securities Depositary (the "VPS") on 29 January 2018 (the "Record Date"), who were not invited to participate in the Private Placement (the "Eligible Shareholders"). Each Eligible Shareholder will be granted 0.303 non-transferable Subscription Rights for each existing share registered as held by such Eligible Shareholder at the Record Date. The number of Subscription Rights granted to each Eligible Shareholder will be rounded down to the nearest whole Subscription Right. Each Subscription Right gives the right to subscribe for, and be allocated, one Offer Share in the Repair Offering. Over-subscription and subscription without Subscription Rights will be permitted; however there can be no assurance that Offer Shares will be allocated for such subscriptions. The subscription period for the Repair Offering will commence at 09.00 (CET) on 22 March 2018 and end at 12.00 (CET) on 5 April 2018 (the "Subscription Period"). Subscription Rights that are not used to subscribe for Offer Shares before the expiry of the Subscription Period will have no value and will lapse without compensation to the holder. Assuming due payment of the Offer Shares subscribed for and allocated in the Repair Offering, delivery of the Offer Shares in the VPS is expected to take place on or about 11 April 2018. The Subscription Rights and the Offer Shares have not been and will not be registered under the Securities Act or the securities laws of any state of the United States and may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. Outside the United States, the Subscription Rights and Offer Shares are being offered to non-US persons in offshore transactions (each as defined in Regulation S) in reliance on Regulation S under the Securities Act. The Offer Shares are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable securities laws and regulations. See Section 17 "Selling and Transfer Restrictions". Investors should be aware that they may be required to bear the financial risks of this investment for an indefinite period of time. For the definitions of capitalized terms used throughout this Prospectus, see Section 19 “Definitions”. Prospective investors should read this Prospectus in its entirety. Investing in the Shares involves a high degree of risk. See Section 2 "Risk factors". Managers: The date of this Prospectus is 21 March 2018 ABG Sundal Collier ASA DNB Markets, a part of DNB Bank ASA

Transcript of POLARCUS LIMITED an exempted company incorporated under ...

1

POLARCUS LIMITED (an exempted company incorporated under the laws of the Cayman Islands)

The information contained in this prospectus (the "Prospectus") relates to the contemplated listing on Oslo Børs of (i) 230,769,231 new shares in Polarcus Limited ("Polarcus" or the "Company", and when taken together with its consolidated subsidiaries, the "Group" or the "Polarcus Group"), each with a par value of USD 0.10 (the "Private Placement Shares") and (ii) 98,809,712 new shares in Polarcus, with a par value of USD 0.10 each (the "Bond Conversion Shares" and together with the Private Placement Shares the "New Shares"). The Private Placement Shares were issued on 1 March 2018 to investors that were allocated shares in the private placement that was successfully placed on 26 January 2018 (the "Private Placement"). The Bond Conversion Shares were issued on 13 March 2018 to holders of unsecured bonds who accepted the offer described in the summons published on 26 January 2018 to convert part of their bonds to new shares (the "Bond Conversion Offer"). The contemplated listing of the New Shares on Oslo Børs is expected to take place on or about 22 March 2018.

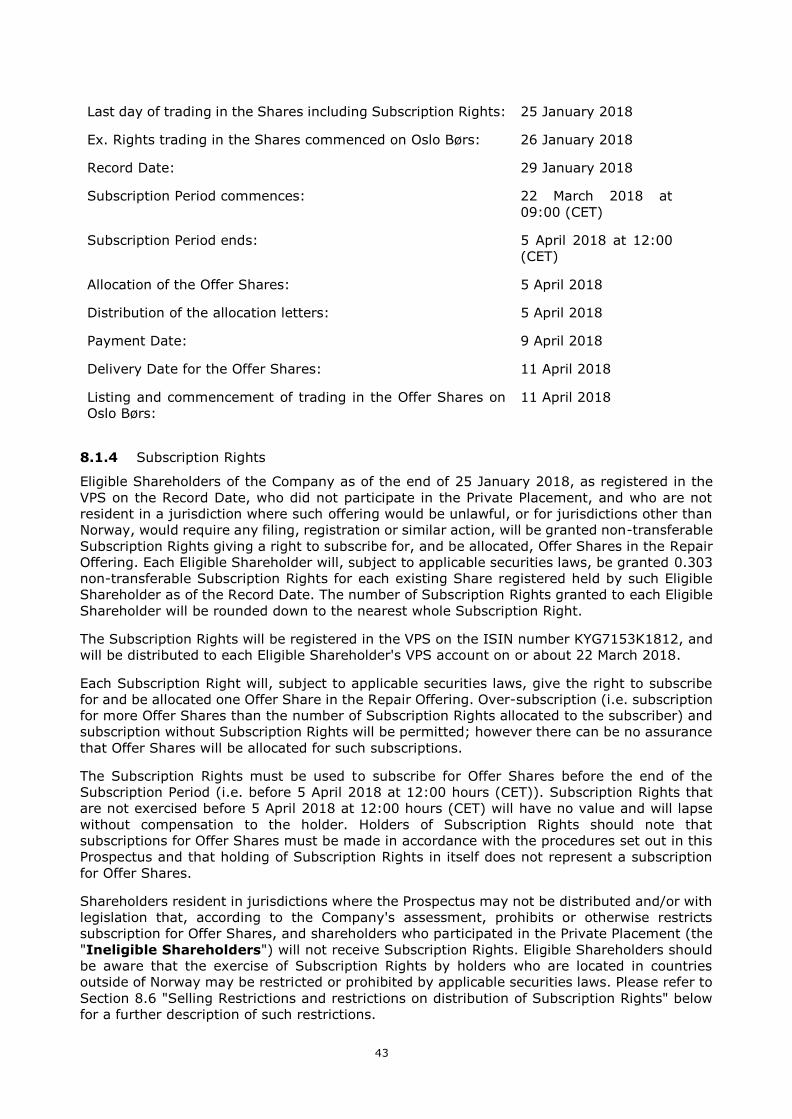

In addition, the Prospectus relates to the repair offering (the "Repair Offering") by the Company of 30,769,231 new shares with a par value of USD 0.10 each (the "Offer Shares") at a subscription price of NOK 1.30 per Offer Share. In connection with the Repair Offering, non-transferable subscription rights (the "Subscription Rights") will be granted to shareholders of the Company as of 25 January 2018, as registered in the Norwegian Central Securities Depositary (the "VPS") on 29 January 2018 (the "Record Date"), who were not invited to participate in the Private Placement (the "Eligible Shareholders"). Each Eligible Shareholder will be granted 0.303 non-transferable Subscription Rights for each existing share registered as held by such Eligible Shareholder at the Record Date. The number of Subscription Rights granted to each Eligible Shareholder will be rounded down to the nearest whole Subscription Right. Each Subscription Right gives the right to subscribe for, and be allocated, one Offer Share in the Repair Offering. Over-subscription and subscription without Subscription Rights will be permitted; however there can be no assurance that Offer Shares will be allocated for such subscriptions. The subscription period for the Repair Offering will commence at 09.00 (CET) on 22 March 2018 and end at 12.00 (CET) on 5 April 2018 (the "Subscription Period"). Subscription Rights that are not used to subscribe for Offer Shares before the expiry of the Subscription Period will have no value and will lapse without compensation to the holder.

Assuming due payment of the Offer Shares subscribed for and allocated in the Repair Offering, delivery of the Offer Shares in the VPS is expected to take place on or about 11 April 2018.

The Subscription Rights and the Offer Shares have not been and will not be registered under the Securities Act or the securities laws of any state of the United States and may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. Outside the United States, the Subscription Rights and Offer Shares are being offered to non-US persons in offshore transactions (each as defined in Regulation S) in reliance on Regulation S under the Securities Act. The Offer Shares are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable securities laws and regulations. See Section 17 "Selling and Transfer Restrictions". Investors should be aware that they may be required to bear the financial risks of this investment for an indefinite period of time.

For the definitions of capitalized terms used throughout this Prospectus, see Section 19 “Definitions”. Prospective investors should read this Prospectus in its entirety. Investing in the Shares involves a high degree of risk. See Section 2 "Risk factors".

Managers:

The date of this Prospectus is 21 March 2018

ABG Sundal Collier ASA DNB Markets, a part of DNB Bank ASA

2

IMPORTANT INFORMATION

This Prospectus has been prepared solely for use in connection with the listing of the New

Shares and the Repair Offering. Please see Section 19 "Definitions and glossary" for definitions

of terms used in this Prospectus.

The Prospectus has been prepared to comply with the Norwegian Securities Trading Act of 29

June 2007 No. 75 (the "Norwegian Securities Trading Act") and related secondary

legislation, including the Commission Regulation (EC) No. 809/2004 implementing Directive

2003/71/EC of the European Parliament and of the Council of 4 November 2003 regarding

information contained in Prospectuses, as amended, and as implemented in Norway (the

"Prospectus Directive"). This Prospectus has been prepared solely in the English language.

The Financial Supervisory Authority of Norway (the "Norwegian FSA") has reviewed and

approved this Prospectus in accordance with sections 7-7 and 7-8 of the Norwegian Securities

Trading Act on 21 March 2018. The Prospectus is valid for a twelve-month period following its

approval. The Norwegian FSA has not controlled or approved the accuracy or completeness of

the information given in this Prospectus. The approval given by the Norwegian FSA only relates

to the information included in accordance with pre-defined disclosure requirements. The

Norwegian FSA has not made any form of control or approval relating to corporate matters

described or referred to in this Prospectus.

The Company falls under the definition of a small and medium-sized enterprise under the

Prospectus Directive due to its market capitalisation. Thus, the Prospectus has been prepared

in accordance with the proportionate schedules for small and medium-sized enterprises

pursuant to EC Commission Regulation 486/2012 regarding the format and content of the

prospectus, the base prospectus, the summary and the final terms and in regards the disclosure

requirements. Consequently, the Company has applied checklist annex XXV and annex III for

this Prospectus.

Neither the Company nor the Managers, or any of their respective affiliates, representatives,

advisers or selling agents, are making any representation to any subscriber or purchaser of

Offer Shares regarding the legality or suitability of an investment in the Offer Shares. Each

investor should consult with his or her own advisers as to the legal, tax, business, financial and

related aspects of a subscription or purchase of the Offer Shares. No person is authorised to

give information or to make any representation concerning the Group or in connection with the

Private Placement, the Bond Conversion Offer and the Repair Offering other than as contained

in this Prospectus. If any such information is given or made, it must not be relied upon as

having been authorised by the Company or the Managers or by any of their affiliates, advisers

or selling agents.

The distribution of this Prospectus and the sale of the Offer Shares may be restricted by law in

certain jurisdictions. This Prospectus does not constitute an offer to sell, or a solicitation of an

offer to buy, any Offer Shares in any jurisdiction in which such offer or solicitation is not

authorized, or it is unlawful to make such an offer or solicitation. No one has taken any action

that would permit a public offering of the Offer Shares to occur outside of Norway. Accordingly,

neither this Prospectus nor any advertisement or any other offering material may be distributed

or published in any jurisdiction except under circumstances that will result in compliance with

applicable laws and regulations. Persons in possession of this Prospectus are required to inform

themselves about, and to observe, any such restrictions. In addition, the Offer Shares are

subject to restrictions on transferability and resale in certain jurisdictions and may not be

transferred or resold except as permitted under applicable securities laws and regulations. Any

failure to comply with these restrictions may constitute a violation of applicable securities laws.

For further information on the sale and transfer restrictions of the Company's shares (the

"Shares"), see Section 17 "Selling and transfer restrictions".

This Prospectus and the terms and conditions of the Repair Offering as set out herein shall be

governed by and construed in accordance with Norwegian law. The courts of Norway, with Oslo

as legal venue, shall have exclusive jurisdiction to settle any dispute which may arise out of or

in connection with the Private Placement, the Bond Conversion Offer, the Repair Offering or

this Prospectus.

3

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE

HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES WITH

THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY

REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A

FINDING BY THE SECRETARY OF STATE OF NEW HAMPSHIRE THAT ANY DOCUMENT FILED

UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR

THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A

TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE

MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON,

SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY

PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT

WITH THE PROVISIONS OF THIS PARAGRAPH.

NOTICE TO INVESTORS IN THE UNITED STATES

Because of the following restrictions, prospective investors are advised to consult legal counsel

prior to making any offer, resale, pledge or other transfer of the Shares. The Offer Shares have

not been and will not be registered under the U.S. Securities Act or with any securities

regulatory authority of any state or other jurisdiction in the United States and may not be

offered, sold, pledged or otherwise transferred within the United States except pursuant to an

exemption from, or in a transaction not subject to, the registration requirements of the U.S.

Securities Act and in compliance with any applicable state securities laws. Accordingly, the Offer

Shares will not be offered or sold within the United States, except in reliance on the exemption

from the registration requirements of the U.S. Securities Act under Rule 144A. The Offer Shares

will be offered outside the United States in compliance with Regulation S. Prospective

purchasers are hereby notified that sellers of Offer Shares may be relying on the exemption

from the provisions of Section 5 of the U.S. Securities Act provided by Rule 144A under the

U.S. Securities Act. See Section 17.2.1 "Selling and transfer restrictions—Selling restrictions—

United States".

Any Shares offered or sold in the United States will be subject to certain transfer restrictions

as set forth under Section 17.3.1 "Selling and transfer restrictions—Transfer restrictions—

United States".

The securities offered hereby have not been recommended by any United States federal or

state securities commission or regulatory authority. Further, the foregoing authorities have not

passed upon the merits of the Repair Offering or confirmed the accuracy or determined the

adequacy of this Prospectus. Any representation to the contrary is a criminal offense under the

laws of the United States.

4

TABLE OF CONTENTS

1. SUMMARY ........................................................................................................... 7

2. RISK FACTORS .................................................................................................. 19

RISK FACTORS RELATED TO THE INDUSTRY IN WHICH POLARCUS OPERATES ............................. 19 RISK FACTORS RELATED TO THE COMPANY AND THE GROUP ............................................... 20 RISKS FACTORS RELATED TO FINANCE ........................................................................ 24 RISK FACTORS RELATED TO THE SHARES AND THE REPAIR OFFERING .................................... 27

3. RESPONSIBILITY FOR THE PROSPECTUS .......................................................... 30

4. PRESENTATION OF INFORMATION .................................................................... 31

DATE OF INFORMATION ......................................................................................... 31 PRESENTATION OF FINANCIAL INFORMATION ................................................................. 31 ROUNDING ........................................................................................................ 31 INDUSTRY AND MARKET DATA .................................................................................. 31 FORWARD-LOOKING STATEMENTS ............................................................................. 32 MANAGERS ....................................................................................................... 33 NO ADVICE ....................................................................................................... 33 THIRD PARTY INFORMATION .................................................................................... 33 ENFORCEMENT OF CIVIL LIABILITY ............................................................................. 33

5. THE RESTRUCTURING ....................................................................................... 35

FLEET BANK FACILITY ........................................................................................... 35 SWAP TERMINATION ............................................................................................. 35 WORKING CAPITAL FACILITY ................................................................................... 35 SECURED BONDS ................................................................................................ 36 CASH SWEEP ..................................................................................................... 36 UNSECURED BONDS ............................................................................................. 36 SALE AND LEASE TERMINATION ................................................................................ 37

6. LISTING OF THE PRIVATE PLACEMENT SHARES ................................................ 38

BACKGROUND .................................................................................................... 38 USE OF PROCEEDS ............................................................................................... 38 EXPENSES RELATED TO THE LISTING OF THE PRIVATE PLACEMENT SHARES .............................. 38 SHARE CAPITAL FOLLOWING COMPLETION OF THE PRIVATE PLACEMENT .................................. 38 DILUTION ......................................................................................................... 39 SELLING AND TRANSFER RESTRICTIONS ...................................................................... 39 ADVISORS ........................................................................................................ 39 LOCK-UP .......................................................................................................... 39 INTEREST OF NATURAL AND LEGAL PERSONS INVOLVED IN THE PRIVATE PLACEMENT ................... 39 JURISDICTION .................................................................................................... 39

7. LISTING OF THE BOND CONVERSION SHARES .................................................. 40

BACKGROUND .................................................................................................... 40 EXPENSES RELATED TO THE LISTING OF THE BOND CONVERSION SHARES ............................... 40 SHARE CAPITAL FOLLOWING COMPLETION OF THE BOND CONVERSION OFFER .......................... 40 DILUTION ......................................................................................................... 40 SELLING AND TRANSFER RESTRICTIONS ...................................................................... 40 ADVISORS ........................................................................................................ 40 LOCK-UP .......................................................................................................... 40 INTEREST OF NATURAL AND LEGAL PERSONS INVOLVED IN THE BOND CONVERSION OFFER ........... 41 JURISDICTION .................................................................................................... 41

8. THE TERMS OF THE REPAIR OFFERING ............................................................. 42

THE REPAIR OFFERING .......................................................................................... 42

5

PARTICIPATION OF MAJOR EXISTING SHAREHOLDERS AND MEMBERS OF THE COMPANY'S MANAGEMENT,

SUPERVISORY OR ADMINISTRATIVE BODIES IN THE REPAIR OFFERING ............................................ 47 DELIVERY AND LISTING OF THE OFFER SHARES ............................................................. 47 MANDATORY ANTI-MONEY LAUNDERING PROCEDURES ...................................................... 47 FINANCIAL INTERMEDIARIES .................................................................................... 48 SELLING RESTRICTIONS AND RESTRICTIONS ON DISTRIBUTION OF SUBSCRIPTION RIGHTS ........... 48 THE OFFER SHARES ............................................................................................. 49 SHARES FOLLOWING THE REPAIR OFFERING ................................................................. 49 DILUTION ......................................................................................................... 49 ADVISORS ........................................................................................................ 49 NET PROCEEDS AND EXPENSES RELATED TO THE REPAIR OFFERING ...................................... 50 INTERESTS OF NATURAL AND LEGAL PERSONS INVOLVED IN THE REPAIR OFFERING .................... 50 PUBLICATION OF INFORMATION RELATING TO THE REPAIR OFFERING..................................... 50 JURISDICTION AND GOVERNING LAW .......................................................................... 50 LOCK-UP .......................................................................................................... 50 SUPPLEMENTARY PROSPECTUS ................................................................................. 50

9. INDUSTRY AND MARKET ................................................................................... 51

MARKET OVERVIEW .............................................................................................. 51 SEISMIC FLEET OVERVIEW ...................................................................................... 52 POSITIONING OF POLARCUS IN THE MARKET ................................................................. 54

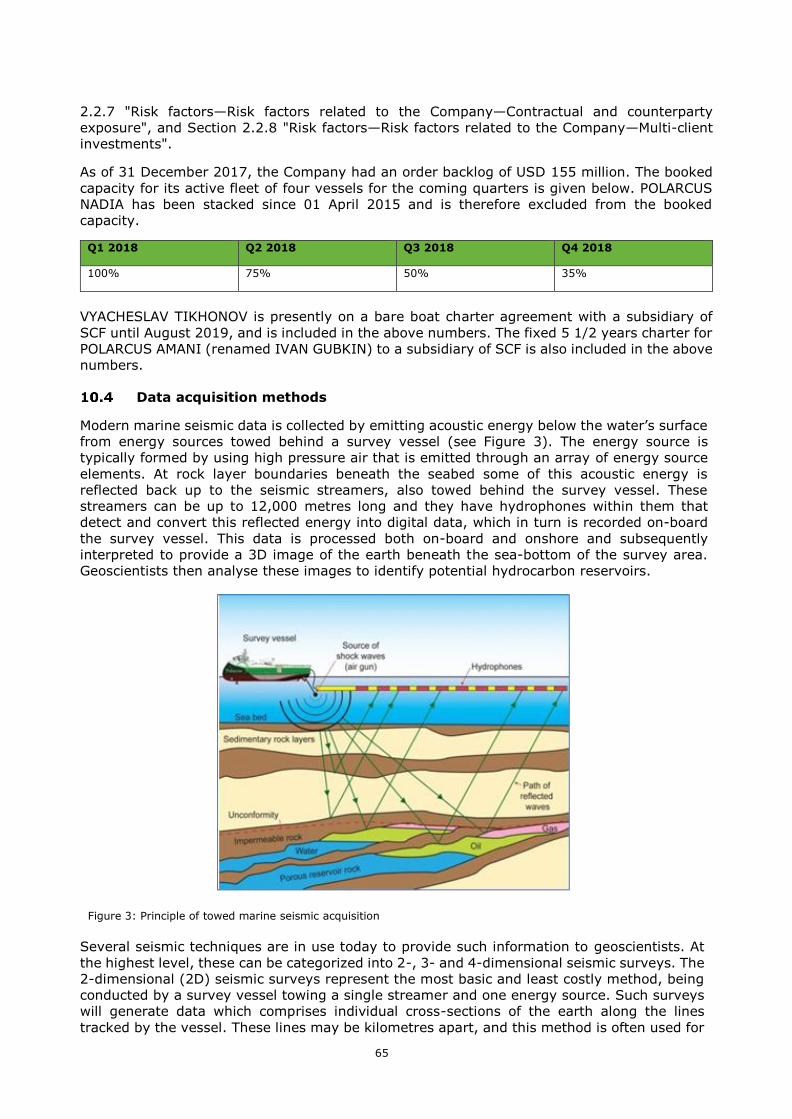

10. BUSINESS ...................................................................................................... 59

INCORPORATION, REGISTERED OFFICE AND REGISTRATION NUMBER ...................................... 59 GROUP HISTORY ................................................................................................. 59 OVERVIEW OF BUSINESS ACTIVITIES .......................................................................... 61 DATA ACQUISITION METHODS .................................................................................. 65 VISION AND STRATEGY .......................................................................................... 67 ORGANIZATION AND BUSINESS LINES ......................................................................... 68 THE POLARCUS FLEET ........................................................................................... 71 MATERIAL CONTRACTS .......................................................................................... 75 ORGANIZATIONAL STRUCTURE ................................................................................. 85 LEGAL AND ARBITRATION PROCEEDINGS ................................................................... 86

11. SELECTED FINANCIAL INFORMATION ............................................................ 88

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES .......................................................... 88 CONSOLIDATED HISTORICAL FINANCIAL INFORMATION ..................................................... 88 SUMMARY OF KEY FINANCIALS ................................................................................. 92 SEGMENT INFORMATION ........................................................................................ 93 VESSEL UTILIZATION ............................................................................................ 95 LIQUIDITY AND CAPITAL RESOURCES .......................................................................... 95 WORKING CAPITAL STATEMENT ................................................................................ 97 IMPAIRMENT CHARGES RECOGNIZED IN THE THREE MONTHS ENDING 31 DECEMBER 2017 ........... 97 SIGNIFICANT CHANGES IN FINANCIAL AND TRADING POSITION IN THE GROUP AFTER 31 DECEMBER

2017 98 TREND INFORMATION ......................................................................................... 98 INVESTMENTS ................................................................................................. 98 SUMMARY OF FINANCING ..................................................................................... 99 CAPITALIZATION AND INDEBTEDNESS .................................................................... 108 AUDITORS .................................................................................................... 111

12. BOARD OF DIRECTORS, MANAGEMENT, EMPLOYEES AND CORPORATE

GOVERNANCE ....................................................................................................... 112

INTRODUCTION ................................................................................................. 112 NOMINATION COMMITTEE ..................................................................................... 112 BOARD OF DIRECTORS ........................................................................................ 112 MANAGEMENT .................................................................................................. 117 NUMBER OF EMPLOYEES ....................................................................................... 119

6

EMPLOYEE REMUNERATION.................................................................................... 120 EMPLOYEE LONG TERM INCENTIVE SCHEMES ............................................................... 120 EMPLOYEE HEALTH PROTECTION ............................................................................. 121 BENEFITS UPON TERMINATION ............................................................................... 121 PENSION SCHEME ........................................................................................... 121 CORPORATE GOVERNANCE ................................................................................. 122 CONFLICTS OF INTERESTS ................................................................................. 123 CONVICTIONS FOR FRAUDULENT OFFENCES, BANKRUPTCY ETC. ....................................... 123

13. RELATED PARTY TRANSACTIONS ................................................................. 124

RELATED PARTY TRANSACTION FOR THE TWELVE MONTHS ENDED 31 DECEMBER 2017 ............. 124 RELATED PARTY TRANSACTION AFTER 31 DECEMBER 2017 ............................................. 124

14. CORPORATE INFORMATION AND DESCRIPTION OF THE SHARE CAPITAL .... 125

GENERAL CORPORATE INFORMATION ........................................................................ 125 SHARES AND SHARE CAPITAL ................................................................................. 125

15. SECURITIES TRADING IN NORWAY .............................................................. 137

INTRODUCTION ................................................................................................. 137 TRADING AND SETTLEMENT ................................................................................... 137 INFORMATION, CONTROL AND SURVEILLANCE .............................................................. 137 THE VPS AND TRANSFER OF SHARES ........................................................................ 138 SHAREHOLDER REGISTER – NORWEGIAN LAW ............................................................. 138 FOREIGN INVESTMENT IN NORWEGIAN SHARES ............................................................ 138 DISCLOSURE OBLIGATIONS ................................................................................... 138 INSIDER TRADING.............................................................................................. 138 MANDATORY OFFER REQUIREMENTS ......................................................................... 139

16. TAXATION .................................................................................................... 141

INTRODUCTION ................................................................................................. 141 TAXATION ON DIVIDENDS ..................................................................................... 141 NORWEGIAN TAX ON CAPITAL GAINS ON SHARES ........................................................ 142 NORWEGIAN NET WEALTH TAX .............................................................................. 142 NORWEGIAN DUTIES ON TRANSFER OF SHARES ........................................................... 143 NORWEGIAN CFC-LEGISLATION ............................................................................. 143 CAYMAN ISLAND TAXATION .................................................................................. 143

17. SELLING AND TRANSFER RESTRICTIONS ..................................................... 144

GENERAL ........................................................................................................ 144 SELLING RESTRICTIONS ....................................................................................... 144 TRANSFER RESTRICTIONS ..................................................................................... 146

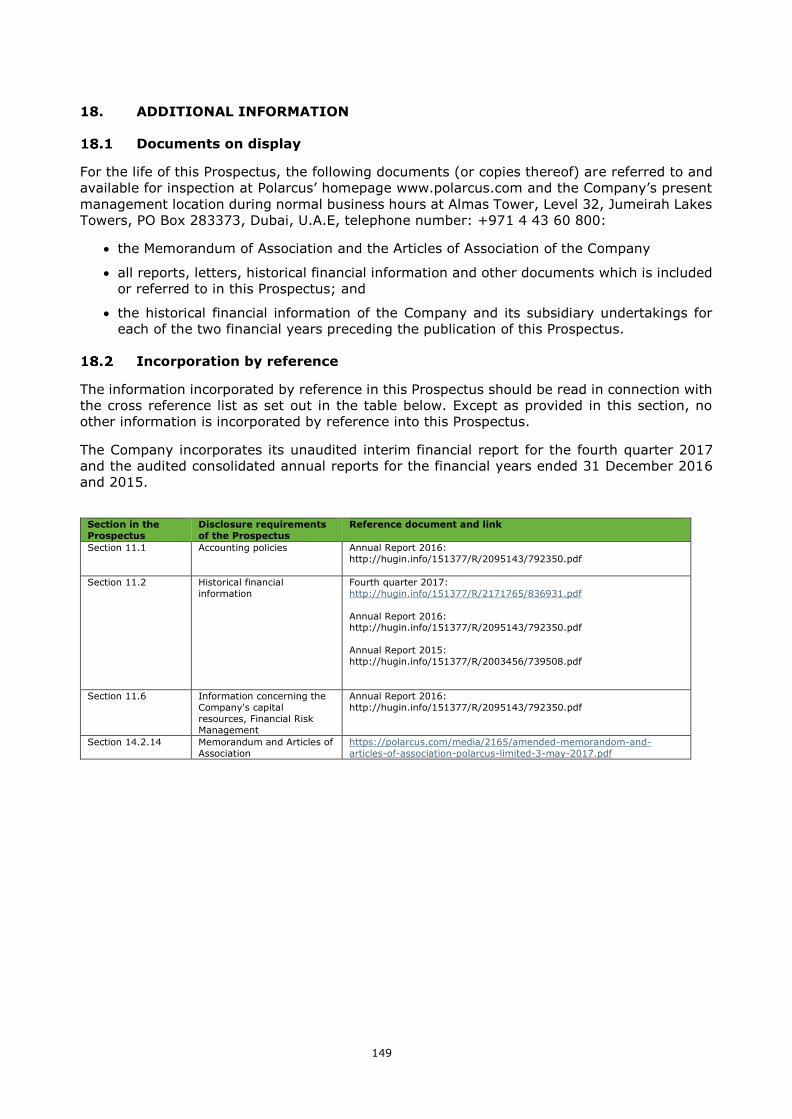

18. ADDITIONAL INFORMATION ........................................................................ 149

DOCUMENTS ON DISPLAY ..................................................................................... 149 INCORPORATION BY REFERENCE ............................................................................. 149

19. DEFINITIONS AND GLOSSARY ...................................................................... 150

7

1. SUMMARY

Summaries are made up of disclosure requirements known as "Elements". These Elements are

numbered in Sections A– E (A.1 – E.7) below. This summary contains all the Elements required

to be included in a summary for this type of securities and the issuer. Because some Elements

are not required to be addressed, there may be gaps in the numbering sequence of the

Elements. Even though an Element may be required to be inserted in the summary because of

the type of securities and issuer, it is possible that no relevant information can be given

regarding the Element. In this case a short description of the Element is included in the

summary with the mention of "not applicable".

Section A – Introduction and Warnings

A.1 Warning This summary should be read as an introduction to the

Prospectus.

Any decision to invest in the Offer Shares should be based

on consideration of the Prospectus as a whole by the

investor.

Where a claim relating to the information contained in the

Prospectus is brought before a court, the plaintiff investor

might, under the national legislation in its Member State,

have to bear the costs of translating the Prospectus before

the legal proceedings are initiated.

Civil liability attaches only to those persons who have

tabled the summary including any translation thereof, but

only if the summary is misleading, inaccurate or

inconsistent when read together with the other parts of the

Prospectus or it does not provide, when read together with

the other parts of the Prospectus, key information in order

to aid investors when considering whether to invest in such

securities.

A.2 Resale or final

placement of

securities by financial

intermediaries

Not applicable. This Prospectus will not be used in

subsequent resales by financial intermediaries.

Section B - Issuer

B.1 Legal and

commercial name

The legal name of the Company is Polarcus Limited and the

Company's commercial name is Polarcus.

B.2 Domicile/Legal

form/Legislation/Co

untry of

incorporation

The Company is an exempted company validly

incorporated with limited liability in the Cayman Islands, is

registered with the Cayman Islands Registrar of Companies

with registration number 201867 and regulated by the

Companies Law.

B.3 Current operations,

principal activities

and markets

Polarcus is one of the five global marine three dimensional

(3D) towed streamer geophysical service providers. The

other providers are WesternGeco (Schlumberger), CGG,

PGS and SGS. The seismic data acquired by the Company's

vessels is used by oil and gas companies to evaluate

hydrocarbon structures and to increase chances of

commercial success ahead of the exponentially more

expensive drilling phase. The data is also used to

8

determine size and structure of known reservoirs in order

to maximize field recovery and ongoing production rates.

Polarcus has two principal business activities: (i) contract

seismic services and (ii) multi-client services. In addition,

the Company charters two seismic vessels under long term

Bareboat agreement to Sovcomflot, and also provides

management services related to the seismic operation of

one vessel for Turkish Petroleum International Company.

B.4a Significant recent

trends affecting the

issuer and the

industry in which it

operates

Not applicable. There are no significant recent trends

affecting the issuer and the industry in which it operates.

B.5 The Group The Company is the parent company of the Group.

B.6 Persons having an

interest in the

issuer's capital or

voting rights

Shareholders owning 5% or more of the Shares have an

interest in the Company's share capital, which is notifiable

pursuant to the Norwegian Securities Trading Act.

The Company is not aware of any persons or entities,

except for those set out below, who, directly or indirectly,

have an interest of 5% or more of the Shares as of the date

of this Prospectus. The following persons or entities have

notified of an interest of 5% or more of the Shares in the

Company:

Carl-Peter Zickerman (through his wholly owned

companies Zickerman Holding Ltd and Zickerman Group

Ltd), has holdings corresponding to a total of 34,925,401

Shares, corresponding to 7.23% of the issued share

capital.

Bybrook Capital LLP who, through Bybrook Capital

Master Fund LP, Bybrook Capital Hazelton Master Fund

LP, Bybrook Capital Badminton Fund LP and Bybrook

Capital Burton Partnership, in aggregate, have holdings

corresponding to a total of 89,331,697 Shares following

the Private Placemenet, corresponding to 23.3% of the

issued share capital prior to the Bond Conversion Offer

and the Repair Offering.

The Company is not aware that the Company is controlled

or owned, directly or indirectly, by any Shareholder or

related Shareholders.

B.7 Selected historical

key financial

information

9

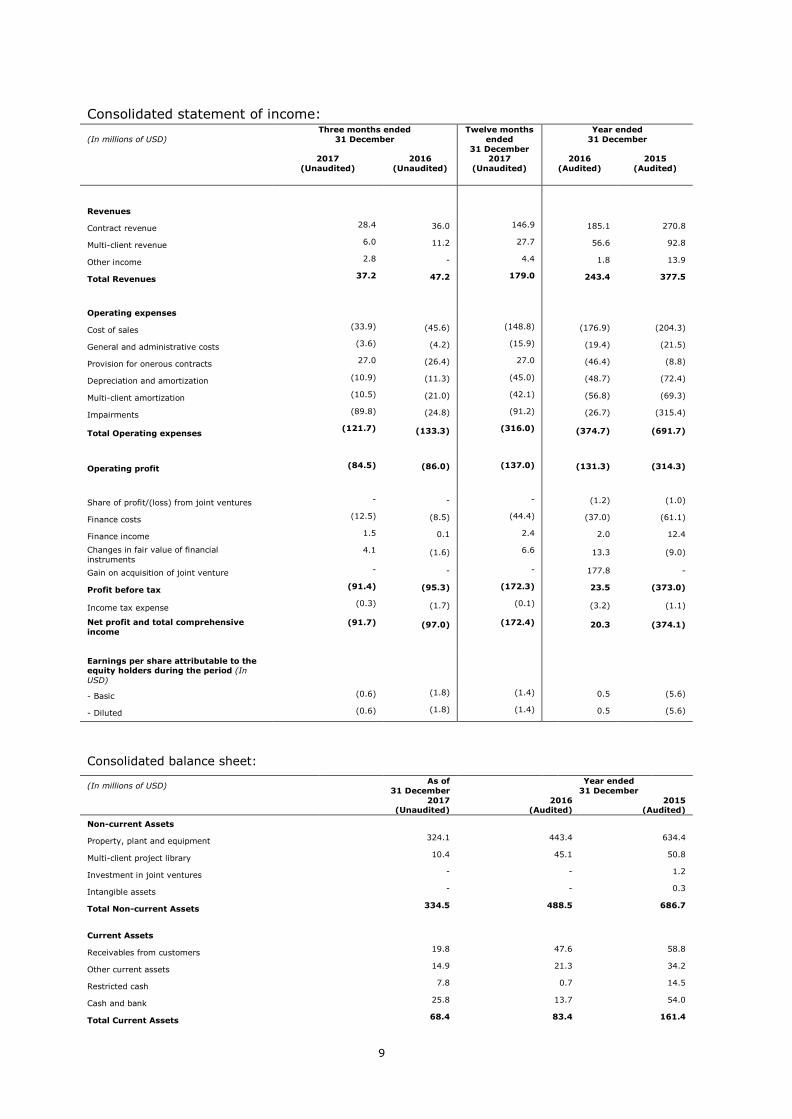

Consolidated statement of income:

(In millions of USD)

Three months ended

31 December

Twelve months

ended

31 December

Year ended

31 December

2017

(Unaudited)

2016

(Unaudited)

2017

(Unaudited)

2016

(Audited)

2015

(Audited)

Revenues

Contract revenue 28.4 36.0 146.9 185.1 270.8

Multi-client revenue 6.0 11.2 27.7 56.6 92.8

Other income 2.8 - 4.4 1.8 13.9

Total Revenues 37.2 47.2 179.0 243.4 377.5

Operating expenses

Cost of sales (33.9) (45.6) (148.8) (176.9) (204.3)

General and administrative costs (3.6) (4.2) (15.9) (19.4) (21.5)

Provision for onerous contracts 27.0 (26.4) 27.0 (46.4) (8.8)

Depreciation and amortization (10.9) (11.3) (45.0) (48.7) (72.4)

Multi-client amortization (10.5) (21.0) (42.1) (56.8) (69.3)

Impairments (89.8) (24.8) (91.2) (26.7) (315.4)

Total Operating expenses (121.7) (133.3) (316.0) (374.7) (691.7)

Operating profit (84.5) (86.0) (137.0) (131.3) (314.3)

Share of profit/(loss) from joint ventures - - - (1.2) (1.0)

Finance costs (12.5) (8.5) (44.4) (37.0) (61.1)

Finance income 1.5 0.1 2.4 2.0 12.4

Changes in fair value of financial

instruments 4.1 (1.6) 6.6 13.3 (9.0)

Gain on acquisition of joint venture - - - 177.8 -

Profit before tax (91.4) (95.3) (172.3) 23.5 (373.0)

Income tax expense (0.3) (1.7) (0.1) (3.2) (1.1)

Net profit and total comprehensive

income (91.7) (97.0) (172.4) 20.3 (374.1)

Earnings per share attributable to the equity holders during the period (In

USD)

- Basic (0.6) (1.8) (1.4) 0.5 (5.6)

- Diluted (0.6) (1.8) (1.4) 0.5 (5.6)

Consolidated balance sheet:

(In millions of USD) As of

31 December

Year ended

31 December

2017

(Unaudited) 2016

(Audited) 2015

(Audited)

Non-current Assets

Property, plant and equipment 324.1 443.4 634.4

Multi-client project library 10.4 45.1 50.8

Investment in joint ventures - - 1.2

Intangible assets - - 0.3

Total Non-current Assets 334.5 488.5 686.7

Current Assets

Receivables from customers 19.8 47.6 58.8

Other current assets 14.9 21.3 34.2

Restricted cash 7.8 0.7 14.5

Cash and bank 25.8 13.7 54.0

Total Current Assets 68.4 83.4 161.4

10

TOTAL ASSETS 402.9 571.9 848.2

EQUITY and LIABILITIES

Equity

Issued share capital 15,3 5.3 13.4

Share premium 614.2 586.4 532.2

Other reserves 24.4 29.9 32.6

Retained earnings/(loss) (609.2) (442.8) (466.3)

Total Equity 44.7 178.8 111.9

Non-current Liabilities

Bond loans - 34.6 -

Other interest bearing debt - 0.9 0.6

Long term provisions - 37.3 -

Other financial liabilities 8.6 10.5 22.3

Total Non-current Liabilities 8.6 83.3 23.0

Current Liabilities

Bond loans 48.6 - 220.6

Finance leases - - 166.0

Other interest bearing debt 245.6 249.6 256.9

Provisions 5.5 6.8 8.8

Accounts payable 13.4 18.9 30.1

Other accruals and payables 36.4 34.4 30.9

Total Current Liabilities 349.5 309.8 713.3

TOTAL EQUITY and LIABILITIES 402.9 571.9 848.2

Consolidated cash flow statement:

(In millions of USD)

Three months ended

31 December

Twelve months

ended

31 December

Year ended

31 December

2017

(Unaudited) 2016

(Unaudited) 2017

(Unaudited) 2016

(Audited) 2015

(Audited)

Profit/(loss) for period (91.7) (97.0) (172.5) 20.3 (374.1)

Adjustment for:

Depreciation and amortization 10.9 11.3 45.0 48.7 72.4

Multi-Client amortization 10.5 21.0 42.1 56.8 69.3

Impairments 89.8 24.8 91.2 26.7 315.4

Changes in fair value of financial

instruments

(4.1) 1.6 (6.6) (13.3) 9.0

Employee share option expenses 0.1 0.1 0.5 0.6 0.5

Interest expense 10.7 8.8 39.7 32.7 55.1

Interest income (0.1) - (0.2) (0.1) (0.8)

Gain on financial restructuring - - - (177.8) -

Effect of currency (gain)/loss (0.1) (3.1) 1.2 (0.6) (4.8)

Gain on buyback of convertible

bonds

- - - - (1.2)

Net movement in provisions (31.8) 26.4 (35.7) 30.6 8.8

Share of (profit)/loss from joint

ventures

- - - 1.2 1.0

Working capital adjustments:

Decrease/(Increase) in current

assets

16.9 2.2 32.0 19.7 22.3

Increase/(Decrease) in trade

payables and accruals

7.2 1.5 (2.6) 2.7 3.4

Net cash flows from operating activities

18.5 (2.6) 34.1 48.1 167.5

Cash flows from investing

activities

11

Payments for property, plant and equipment

(1.7) (1.0) (7.3) (16.4) (15.1)

Proceeds from the disposal of

multi-client projects

- - - - 25.2

Payments for multi-client project library

(6.9) (12.6) (20.6) (44.6) (96.7)

Payments to acquire intangible

assets

- - - - (12.4)

Net cash flows used in investing activities

(8.7) (13.5) (28.0) (61.0) (99.3)

Cash flows from financing

activities

Net receipt from bank loans - - - 7.9 -

Proceeds from the issue of ordinary

shares

- - 39.0 - -

Repayment of bond loans - - - (0.8)

Repayment of finance lease - - - (7.7)

Repayment of other interest

bearing debt

(2.2) (2.3) (6.9) (14.4) (15.1)

Interest paid (3.9) (4.3) (18.6) (24.4) (41.6)

Financial restructuring fees paid - - - (6.2) -

Other finance costs paid (0.4) (0.4) (0.9) (1.0) (6.4)

Decrease/(Increase) in restricted

cash

(1.1) - (7.1) 13.8 (6.3)

Net cash flow for currency swaps (1.4) (1.6) 1.8 (3.9) (0.5)

Interest received 0.1 - 0.2 0.1 0.8

Net cash flows from financing

activities

(8.9) (8.5) 6.3 (28.2) (77.6)

Effect of foreign currency

revaluation on cash

0.1 1.2 (0.3) 0.9 (2.1)

Net increase in cash and cash equivalents

1.0 (23.5) 12.1 (40.2) (11.5)

Cash and cash equivalents at the

beginning of the period

24.9 37.2 13.7 54.0 65.5

Cash and cash equivalents at

the end of the period

25.8 13.7 25.8 13.7 54.0

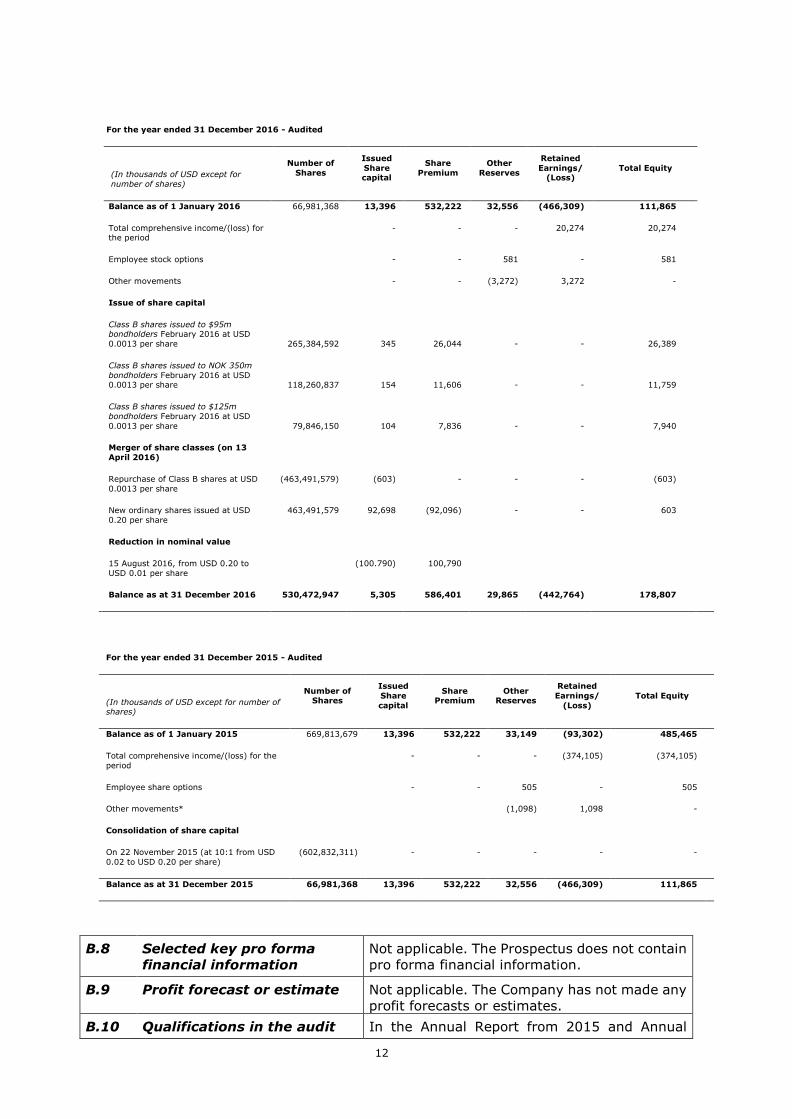

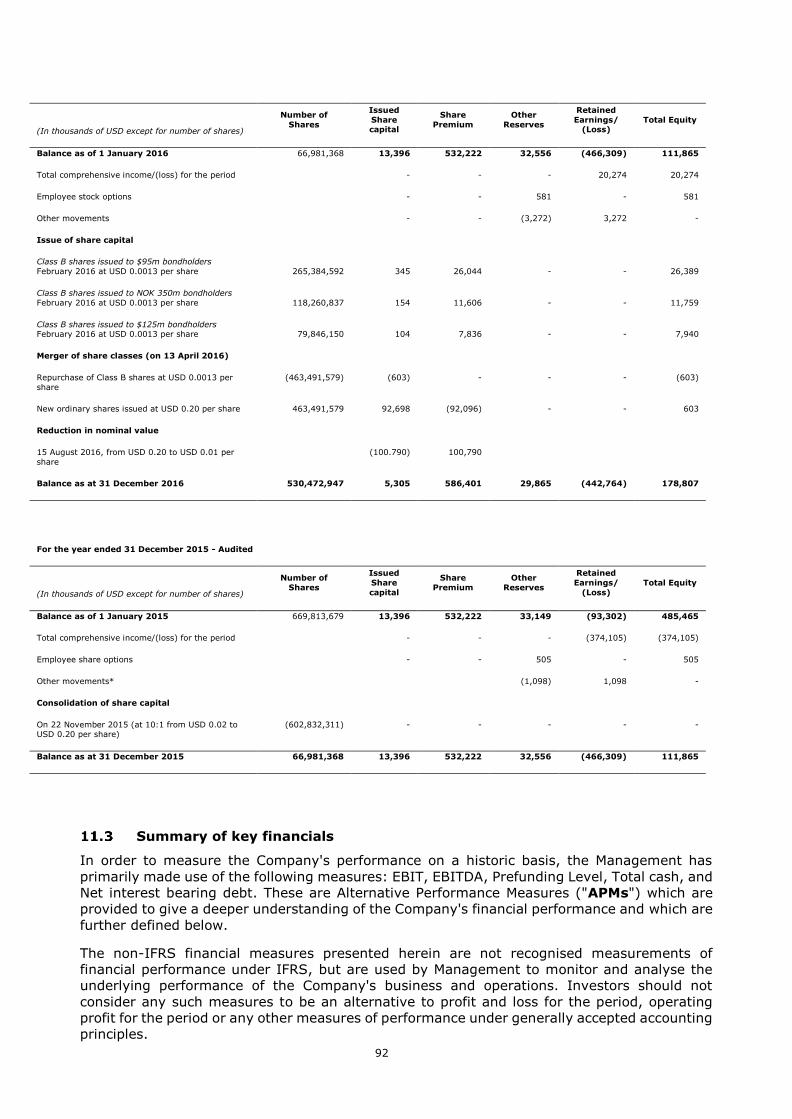

Consolidated statement of changes in equity:

For the twelve months ended 31 December 2017

Number of

Shares

Issued Share

capital

Share

Premium

Other

Reserves

Retained Earnings/

(Loss)

Total Equity (In thousands of USD except

for number of shares)

Balance as of 1 January 2017

530,472,947 5,305 586,401 29,865 (442,764) 178,807

Total comprehensive

income/(loss) for the period

- - - (172,453) (172,453)

Employee stock options - - 534 - 534

Other movements (5,988) 5,988 -

Issue of share capital

08 March 2017 at NOK 0.33

per share

1,000,000,000 10,000 28,853 - - 38,853

07 April 2017 at NOK 0.33 per share

3,912,439 39 111 - - 150

Transaction costs on issue of

shares

- (1,173) - - (1,173)

Consolidation of share capital

New share issued 4 - - - - -

10:1 consolidation 16 May

2017

(1,380,946,851) - - - - -

12

For the year ended 31 December 2016 - Audited

Number of

Shares

Issued

Share capital

Share

Premium

Other

Reserves

Retained

Earnings/ (Loss)

Total Equity (In thousands of USD except for

number of shares)

Balance as of 1 January 2016 66,981,368 13,396 532,222 32,556 (466,309) 111,865

Total comprehensive income/(loss) for the period

- - - 20,274 20,274

Employee stock options - - 581 - 581

Other movements - - (3,272) 3,272 -

Issue of share capital

Class B shares issued to $95m bondholders February 2016 at USD

0.0013 per share 265,384,592 345 26,044 - - 26,389

Class B shares issued to NOK 350m

bondholders February 2016 at USD 0.0013 per share 118,260,837 154 11,606 - - 11,759

Class B shares issued to $125m

bondholders February 2016 at USD

0.0013 per share 79,846,150 104 7,836 - - 7,940

Merger of share classes (on 13

April 2016)

Repurchase of Class B shares at USD

0.0013 per share

(463,491,579) (603) - - - (603)

New ordinary shares issued at USD

0.20 per share

463,491,579 92,698 (92,096) - - 603

Reduction in nominal value

15 August 2016, from USD 0.20 to

USD 0.01 per share

(100.790) 100,790

Balance as at 31 December 2016 530,472,947 5,305 586,401 29,865 (442,764) 178,807

For the year ended 31 December 2015 - Audited

Number of Shares

Issued

Share

capital

Share Premium

Other Reserves

Retained

Earnings/

(Loss)

Total Equity (In thousands of USD except for number of shares)

Balance as of 1 January 2015 669,813,679 13,396 532,222 33,149 (93,302) 485,465

Total comprehensive income/(loss) for the

period

- - - (374,105) (374,105)

Employee share options - - 505 - 505

Other movements* (1,098) 1,098 -

Consolidation of share capital

On 22 November 2015 (at 10:1 from USD

0.02 to USD 0.20 per share)

(602,832,311) - - - - -

Balance as at 31 December 2015 66,981,368 13,396 532,222 32,556 (466,309) 111,865

B.8 Selected key pro forma

financial information

Not applicable. The Prospectus does not contain

pro forma financial information.

B.9 Profit forecast or estimate Not applicable. The Company has not made any

profit forecasts or estimates.

B.10 Qualifications in the audit In the Annual Report from 2015 and Annual

13

report on the historical

financial information

Report from 2016 there are no qualifications in

the audit report.

B.11 Working capital The Company has sufficient working capital for

its present requirements for the next 12

months.

Section C - Securities

C.1 Type and class of

securities admitted

to trading and

identification number

All the issued shares are in registered form and will, following

the publication of this Prospectus, be registered with the

Norwegian Central Securities Depository ("VPS") register

with ISIN KYG7153K1085. The New Shares are currently

registered with ISIN KYG7153K1739. The Registrar of the

Company is DNB Bank ASA, Verdipapirservice, Dronning

Eufemias gate 30, 0191 Oslo.

C.2 Currency The Offer Shares are issued in USD.

C.3 Number of shares

and par value

The Company's issued share capital is USD 48,301,748.2

divided into 483,017,482 Shares each with a nominal or par

value of USD 0.10, all fully paid and issued in accordance

with Cayman Islands law.

C.4 Rights attached to

the securities

The New Shares and the Offer Shares are shares of the

Company with no special rights attached to them.

C.5 Restrictions on free

transferability

The Offer Shares are freely transferable, subject to any local

regulatory transfer restrictions.

C.6 Admission to trading The Company's shares were admitted to trading on Oslo Børs

on 20 June 2012.

C.7 Dividend policy Polarcus is committed to maximizing the shareholder value,

by inter alia declaring dividends to the Shareholders from its

profit. However, the Company is restricted from declaring

dividends under its loan facility and bonds.

Polarcus has not issued any dividends in the Company's

history.

Section D - Risks

D.1 Key information on

the key risks that are

specific to the issuer

or its industry

Economic development and trends

The demand for the Company's services will depend

substantially on the level of activity and capital spending by

oil and gas companies and specifically in relation to

development and exploration expenditure.

Government regulation and political risk

Changes in the legislative and fiscal framework governing

the activities of oil and gas business could have a material

impact on exploration and development activities or affect

Polarcus' operations or financial results directly or indirectly.

Competition

Polarcus operates in a highly competitive global market.

Fluctuating revenues from period to period

14

The Company's future revenues may fluctuate significantly

from quarter to quarter and from year to year as a result of

various factors driven by both supply and demand influences.

Insurance coverage

Although the Company has taken out insurance coverage

that the Company considers customary in the industry, such

insurance arrangements will not carry full coverage of all its

operating risks.

Contractual and counter-party exposure

The revenues of the Company will be dependent on contract

awards at competitive terms. Furthermore, the revenues of

the Company will depend on the financial position of its

customers and the willingness and ability of these customers

to honour their obligations towards Polarcus in a timely

manner.

Multi-client investments

The Company has made considerable investments in

acquiring and processing seismic data that the Company

owns ("multi-client data"). The multi-client data is being

licensed to third parties for non-exclusive use in oil and gas

exploration, development and production activities.

However, the Company does not know with certainty how

much of the multi-client data it will be able to license or at

what price.

Operating risks

The Company's assets are concentrated in a single industry

and the Group may be more vulnerable to particular

economic, political, regulatory, environmental or other

developments than a company with a more diversified

portfolio of activities.

The seismic data acquisition operations are exposed to

extreme weather and other potentially hazardous conditions.

There is an inherent exposure to technical risks, which may

lead to operational problems, and increased operational

costs and/or loss of earnings, additional investments,

penalty payments, and other such costs which may have a

material effect on the earnings and financial position of the

Company.

Technology may become obsolete

The company monitors technology developments in the

industry and also monitors client sentiment toward

technology. However, the Company's technology could be

rendered obsolete as new and enhanced products and

services are introduced to the seismic market.

Tax

Operating internationally, Polarcus will be subject to taxation

in several jurisdictions around the world. With increasingly

complex and ever-changing tax regulations and their

15

interpretation, the taxation of the Company could increase in

certain jurisdictions. The Company may also in the future be

subject to review of past years tax returns and be subjected

to additional taxes and penalties. These conditions may have

a material effect on the Company's financial results.

If Polarcus is controlled by Norwegian taxpayers, the

Norwegian CFC-regulation ("NOKUS"- rules) may, in certain

conditions, result in the Company being taxed under

Norwegian law as if it had been a Norwegian company.

Pursuant to the Company's Articles of Association, the

Company may refuse to accept shareholder positions leading

to the CFC-regulations becoming applicable. Also, other

amendments to applicable tax provisions may have negative

impact on the return on the investment of Norwegian

taxpayers.

Access to funding

The Company may require additional capital in the future due

to unforeseen liabilities or in order for it to take advantage

of opportunities for acquisitions, joint ventures, capital

expenditure investments or other business opportunities that

may be identified by the Company.

Should the current working capital and cash flow from

operations not be sufficient to meet the Company's financing

needs, the Company may be forced to reduce or delay capital

expenditures or research and development expenditures,

and/or sell assets or businesses at unanticipated times

and/or at unfavourable prices or other terms, and/or to seek

additional equity capital or to restructure or refinance its

debt.

Losses in the past

The Group has experienced substantial losses. If the Group

continues to suffer substantial losses or does not generate

sufficient profit, the Group's cash flow from operations may

not be sufficient to fund ongoing activities and implement the

Group's business plans.

Financial leverage and breach of covenants

The financial leverage of the Company or any breach of

covenants (or other circumstances which entail that loans fall

due prior to the final maturity date) may have several

adverse consequences, including the need to refinance,

restructure or dispose of certain parts of the Company's

businesses in order to fulfil the Company's financial

obligations.

Defaults and insolvency of subsidiaries

In the event of insolvency, liquidation or a similar event

relating to one of the Company's subsidiaries, all creditors of

such subsidiary would be entitled to payment in full out of

the assets of such subsidiary before the Company, as a

shareholder, would be entitled to any distributions. Such an

event would likely cause a cross-default under all the Group's

16

current financing instruments entitling the Group's secured

creditors to enforce their security rights in priority to the

Company, a shareholder.

Exchange rate fluctuations

Currency exchange rate fluctuations and currency

devaluations could have a material impact on the Company's

results from time to time.

High fixed costs

The Group is subject to high fixed costs, which primarily

consist of depreciation, maintenance expenses associated

with the Group’s seismic data acquisition, processing and

interpretation equipment and certain crew costs. Extended

periods of significant unanticipated downtime or low

productivity caused by reduced demand, weather

interruptions, equipment failures, permit delays or other

causes could reduce the Group’s profitability and have a

material adverse effect on the Group’s financial condition and

results of operations because the Group will not be able to

reduce the Group’s fixed costs as fast as revenues decline.

Increased debt service from 1 January 2022

From 1 January 2022, the amortisation payments under the

Fleet Bank Facility and the bonds in CB Tranche A under the

Convertible Bond Loan will increase as the amortisation

profiles prior to the Restructuring will apply. From the same

date, amortisation payments will become payable under the

New Fleet Facility. The ability to make principal and interest

payments when due, and to fund ongoing operations, will

depend on the Group's future performance and ability to

generate cash and profit, which is subject to market

conditions and general economic, financial and competitive

factors beyond the Group's control.

D.3 Key information on

the key risks that are

specific to the

securities

Volatility of share price

There can be no assurance that an active market for the

Company's Shares can be sustained. The Company's share

price may experience substantial volatility. The market

price of the Shares could fluctuate significantly.

Risks related to issuance of Shares or other securities

It is possible that the Company may decide to offer

additional Shares in the future in order to strengthen its

capital base or for other reasons. Any additional offering of

Shares may be made at a significant discount to the

prevailing market price and could have a material adverse

effect on the market price of the outstanding Shares.

Risks associated with dilution

Due to regulatory requirements under foreign securities

laws or other factors, foreign investors may not be able to

participate in a new issuance of Shares or other securities

and may face dilution as a result.

Any investor that is unable or unwilling to participate in the

17

Company's future share issuances will have their

percentage shareholding diluted.

Section E - Offer

E.1 The total net

proceeds and an

estimate of the total

expenses

The gross proceeds to the Company from the Repair

Offering will be approximately NOK 40 million. The

Company's total costs and expenses of, and incidental to,

the Repair Offering are estimated to amount to

approximately NOK 3.6 million. Based on these

assumptions the net proceeds to the Company will be NOK

36.4 million.

E.2a Reasons for the

Offering and use of

proceeds

The reasons for the Repair Offering are to give Eligible

Shareholders the right to subscribe for new Shares at the

same subscription price as shareholders that were invited

to subscribe for Private Placement Shares in the Private

Placement, and to strengthen the Company's equity.

The net proceeds from the Repair Offering will be used to

strengthen the Company's financial position.

E.3 Terms and conditions

of the Offering

There are no conditions for the Repair Offering.

E.4 Material interests in

the Offering

The Managers or their affiliates have provided advisory

investment and commercial banking services to the

Company and its affiliates in the ordinary course of

business, for which they may have received customary

transaction-related fees. The Managers may also have a

non-material investment interest in parties involved in the

Restructuring.

The Underwriter will receive an underwriting commission

for the underwriting in connection with the Repair Offering.

Beyond the above-mentioned, the Company is not aware

of any interest, including conflicting ones, of any natural or

legal persons involved in the Private Placement and the

Repair Offering.

E.5 Selling shareholders

and lock-up

agreements

There are no selling shareholders.

No lock-up agreements were entered into in connection

with the Repair Offering.

E.6 Dilution resulting

from the Offering

Taken together with the dilution resulting from the Private

Placement and the Bond Conversion, the Repair Offering

will result in a dilution of the shareholders of the Company

prior to the Private Placement, to the extent such

shareholders elect not to participate in the Repair Offering,

of approximately 6%. The aggregate dilution for

shareholders not participating in the Private Placement or

the Bond Conversion Issue, but participating in the Repair

Offering to the extent of their Subscription Rights is 68%.

The immediate dilution for shareholders not participating

in the Repair Offering is approximately 70%.

18

E.7 Estimated expenses

charged to investor

No expenses or taxes will be charged by the Company or

the Managers to the applicants in the Repair Offering.

19

2. RISK FACTORS

An investment in the Company and the Offer Shares involves inherent risks. Before making an

investment decision with respect to the Offer Shares, investors should carefully consider the

risk factors set forth below and all information contained in this Prospectus, including the

Financial Statements and related notes. The risks and uncertainties described in this Section 2

are the material known risks and uncertainties faced by the Group as of the date hereof that

the Company believes are relevant to an investment in the Offer Shares.

An investment in the Offer Shares is suitable only for investors who understand the risks

associated with this type of investment and who can afford to lose all or part of their investment.

The absence of negative past experience associated with a given risk factor does not mean that

the risks and uncertainties described in that risk factor are not a genuine potential threat to an

investment in the Offer Shares. If any of the following risks were to materialise, individually or

together with other circumstances, they could have a material and adverse effect on the Group

and/or its business, financial condition, results of operations, cash flows and/or prospects,

which could cause a decline in the value and trading price of the Offer Shares, resulting in the

loss of all or part of an investment in the Offer Shares.

The order in which the risks are presented does not reflect the likelihood of their occurrence or

the magnitude of their potential impact on the Group’s business, financial condition, results of

operations, cash flows and/or prospects. The risks mentioned herein could materialise

individually or cumulatively. The information in this Section 2 is as of the date of this

Prospectus.

Risk factors related to the industry in which Polarcus operates

2.1.1 Economic development trends

The demand for the Company’s services will depend substantially on the level of activity and

capital spending by oil and gas companies and specifically in relation to development and

exploration expenditure. The activities of the oil and gas companies tend to follow the prices

of oil and gas which have fluctuated over recent years, but have generally been depressed

compared to historical prices. A decrease in oil and gas prices may have a negative impact on

the expenditure on exploration activities which may affect demand for the services of the

Company. Financial projections for and valuation of Polarcus’ assets are largely based on

certain assumptions including those related to future conditions for the markets in which

Polarcus will sell its services. Actual changes in market conditions may affect the accuracy

of the assumptions and future prospects of Polarcus. Historically, the markets for oil and

gas have been volatile.

2.1.2 Multi-jurisdictional operations

Operations in international markets are subject to risks inherent in international business

activities which might significantly affect the Company’s financial performance and

competitiveness, including, but not limited to;

general economic conditions in each relevant country,

changes in taxation and other fiscal regulations,

unexpected changes in regulatory requirements,

environmental protest activity,

compliance with a variety of foreign laws and regulations,

war, terrorist activities, piracy, political, civil or labour disturbances, economic sanctions,

trade policies, embargos, border disputes, military activity,

renegotiation or cancellation of contracts by client

restrictions in currency repatriation,

20

challenges in enforcing contractual rights including the right to payment, and

changes in laws that restrict operations or increase the cost.

2.1.3 Government regulation and political risk

Changes in the legislative and fiscal framework governing the activities of oil and gas business

could have a material impact on exploration and development activities or affect the

Company's operations or financial results directly. Changes in political regimes might

constitute a material risk factor for Polarcus' operations in foreign countries, including

contract and bareboat chartering arrangements for the Polarcus vessels. In a worst case

scenario, political authorities will in certain circumstances be in a position to seize Polarcus'

vessels when these are operating within or flagged under a particular jurisdiction.

In certain countries there is an inherent risk of bribery, corruption and unethical work

practices. The Company has developed clear policies and operating procedures to avoid these

risks, and to the extent reasonably possible, the Company will ensure that all external bodies

that it is required to interact with, operate to the same high standards. Nevertheless, the

Company’s operations could be impacted through the actions of these external bodies. The

Company’s operations are subject to numerous international conventions as well as national,

state and local law, and regulations in force in the jurisdictions in which the Company

conducts, or will conduct, its business. These laws and regulations relate to, inter alia, the

protection of the environment, natural resources, human health and safety, taxes, certification

and visa regulations, licensing and permits for offshore blocks and other requirements. In

particular, compliance with environmental regulations may require significant expenditures

and breaches may result in fines and penalties, which could be material. Whereas the

Company pays and has paid particular attention to safety, conduct and the environment in

its execution of business, stricter regulation or changes in the application of existing

regulations may impose increased costs for operating the business of the Company, or

otherwise impact the Company’s financial condition, operating results or future prospects.

The Company also operates to strict international standards prohibiting unlawful commercial

practices.

The Company cannot predict the extent to which its future cash flow and earnings might be

affected by mandatory compliance with any such new legislation or regulations.

2.1.4 Competition

Polarcus operates in a highly competitive global market. The Company may face competition

from other marine seismic companies as well as other ship owners that introduce capacity

into the market place. This, as well as overcapacity in the seismic market, could adversely

affect the operating results of the Company. Polarcus’ revenue and operating results can vary significantly from quarter-to-quarter and

year-to-year driven by competitor fleet size and global fleet distribution relative to market

demand. Polarcus’ operating income is challenging to forecast due to changes in market

demand driven, in large part, by changes in oil and gas company expenditures.

2.1.5 Commodity prices

Any large fluctuations in oil price could materially impact the demand for seismic services.

Risk factors related to the Company and the Group

2.2.1 Service life and technical performance

The service life of a modern seismic vessel is generally considered to be approximately thirty

years, but could vary depending on its efficiency, periodic vessel maintenance and demand for

such vessels. The service life of streamers and seismic equipment deployed from seismic

vessels is generally considered to be up to ten years subject to similar factors. There can be

21

no guarantee that the vessels or equipment deployed by Polarcus will have a long service life.

The vessels may have particular unforeseen technical problems or deficiencies, new

environmental requirements might be enforced or new technical solutions or vessels might be

introduced to the industry.

The complex operations of the Company may lead to technical and operational difficulties that

result in downtime for the vessel or inability of the vessel to complete a contract. Such risks

may materially affect the operating results and reputation of the Company.

2.2.2 Fluctuating revenues from period to period

The Company’s future revenues may fluctuate significantly from quarter to quarter and

from year to year as a result of various factors including the following:

increases and decreases in industry-wide capacity to acquire seismic data;

fluctuating oil and gas prices, which may impact customer demand for the Company’s

services;

different levels of activity planned by customers;

the timing of offshore lease sales and licensing rounds and the effect of such timing on

the demand for seismic data and geophysical services;

the timing of award and commencement of significant contracts for geophysical data

acquisition services;

weather, marine activity (e.g. barnacle growth reducing vessels’ operational efficiency),

commercial fishing activity restricting access to survey sites and other seasonal factors;

seasonality and other variations in the licensing of geophysical data from the Company’s

multi-client data library; and

reduced vessel utilization due to longer than scheduled yard stays, transits and/or delays

in obtaining necessary permits.

2.2.3 The Group's order book is based on assumptions

The Group’s order book (or backlog) estimates represent those estimated future revenues

relating to projects for which a client has executed a contract and has a scheduled start date

for the project and projects for which the Group has a written letter of intent to award a

contract from the Group’s customers. Order book estimates are based on a number of

assumptions and estimates including operating performance of contracts and assumptions

related to foreign exchange rates.

In accordance with industry practice, contracts for the provision of seismic services typically

can be cancelled at the sole discretion of the client without payment of significant cancellation

costs to the service provider. As a result, even if contracts are included in the order book,

there can be no assurance that such contracts will be wholly executed by the Group, generate

actual revenue or not be renegotiated at a lower price, or even that the total costs already

incurred by the Group in connection with the contract would be covered in full pursuant to

any cancellation clause. Even where a project proceeds as scheduled, it is possible that the

client may default and fail to pay amounts owed to the Group. Material delays, payment

defaults and cancellations could reduce the amount of order book currently reported, and

consequently, could inhibit the conversion of that order book into revenues.

2.2.4 Access to personnel

The Company’s development and business success are significantly dependent upon senior

management and other key personnel. Attracting and retaining qualified field and office based

personnel is of material importance for the operation of the Company’s business. The maritime

and seismic industries are highly competitive for skilled personnel. There is no guarantee that

the Company will be able to attract and retain the personnel required to continue its business

22

and successfully execute the business strategy which might have negative effects on the

Company’s operating results and financial performance.

2.2.5 Insurance coverage

Although the Company has taken out insurance coverage that the Company considers

customary in the industry, such insurance arrangements will not fully cover all its operating

risks. The Company’s insurance policies invariably include deductibles which are discounted

from the amount of any insurance claim. Operation of the vessels represents a potential risk

of loss of or damage to the vessels and equipment. In addition, the Group may not be able to

maintain adequate insurance cover for its vessels and equipment in the future or do so at

premiums that are considered reasonable. An accident involving any of the Group’s assets

could result in loss of earnings, fines or penalties, higher insurance costs and damage to the

reputation of the Company. The Group may not have sufficient insurance cover for the entire

range of risks or there may be a dispute with underwriters on whether a particular risk is

insured or the extent of such insurance, in each case resulting in particular losses not being

covered. Any significant loss or liability not insured could have a material adverse effect on its

business, financial condition and results of operations. In addition, the loss of or continuing

unavailability of one or several of its vessels could have an adverse effect on the Group even

if effective insurance cover should be available.

2.2.6 Contractual and counter-party exposure

The revenues of the Company are dependent on contract awards at competitive terms.

Furthermore, the revenues of the Company will depend on the financial position of customers

and the willingness of these customers to honour their obligations towards Polarcus in a timely

manner. There can be no guarantees that the financial position of counterparties will be

sufficient to adhere to their obligations under the contracts with the Company. The inability of

one or more counterparties to make payment under such contracts might have a significant

adverse effect on the financial position of the Company.

Polarcus is and will in the future be party to various contracts related to its business, most

importantly seismic survey contracts and bareboat chartering arrangements. Consequently,

the Company is and will be exposed to counter party risks. Any potential default by such

counterparties or their inability or lack of willingness to fulfil their commitments may have a

material adverse impact on the Company’s operating results and financial position.

The Company has currently no new building projects or concrete plans for new projects, but

may in the future enter into contracts related to construction of vessels. Any material delays

related to the construction of vessels or other contracts of importance for the construction and

equipment of a vessel may have a material adverse effect on the Company and its financial

position. A potential default or delay by any counterparty, including the shipyard, could have

an adverse effect on the Company and its financial position.

2.2.7 Multi-client investments

The Company has made considerable investments in acquiring and processing seismic data

that the Company owns (“multi-client data”). The multi-client data is licensed to third parties

for non-exclusive use in oil and gas exploration, development and production activities.

However, the Company does not know with certainty how much of the multi-client data it will

be able to licence or at what price. There can be no assurance that the Company will be able

to recover all costs and investments associated with acquiring and processing multi-client

data. If there is a material adverse change in the general prospects for oil and gas exploration,

development and production activities in areas where the Company acquires multi-client data,

the value of such multi-client data could be impaired and the Company could be required to

take a charge against its earnings. The value of multi-client data could also be impaired by

technological or regulatory changes and by other industry or general economic developments.

In general, the Company’s future sales of multi-client data licences are uncertain and depend

on a variety of factors, many of which will be beyond the Company’s control.

23

2.2.8 Operating risks

The Company’s assets are concentrated in a single industry and the Group may be more

vulnerable to particular economic, political, regulatory, environmental or other developments

than a company with a more diversified portfolio of revenue generating activities. It is not

possible to give any guarantees that the vessels will be employed for the duration of their

service life. There is an inherent exposure to technical risks, which may lead to operational

problems, and increased operational costs and/or loss of earnings, additional investments,

penalty payments, and other such costs which may have a material effect on the earnings and

financial position of the Company.

Seismic data acquisition operations are exposed to extreme weather and other hazardous

conditions. In particular, a substantial portion of the Group’s operations are subject to risks

that are customary for marine operations, including capsizing, grounding, collision, interruption

and damage or loss from severe weather or marine conditions, fire, explosions and

environmental contamination from spillage. Any of these risks, whether in the marine or

onshore operations, could result in damage to or destruction of vessels or equipment, injury to

personnel or property damage, and/or suspension of operations or environmental damage. In

addition, the operations involve risks of a technical and operational nature due to the complex

systems that are utilized. If any of these risks materialize, the Group’s business could be

interrupted and the Group could incur significant liabilities. In addition, many similar risks may