POF_Week_9_SB (2)

53

PD Hahn 1 Principles of Finance BS 2100 Hedging & Derivatives Introduction Pete Hahn Faculty of Finance Room 5012 Cass Building

-

Upload

partyycrasher -

Category

Documents

-

view

215 -

download

0

Transcript of POF_Week_9_SB (2)

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 1/53

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 2/53

PD Hahn 2

Topics Covered

• Introduction to Hedging Tools

• Forwards, Futures, Swaps

• Calls, Puts and Shares• Derivative Securities

• Financial Alchemy with Options

• What Determines Option Values?

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 3/53

PD Hahn 3

Hedging with Forwards andFutures

All Businesses Have Risk (for example)

Intrinsic Risk (of the firm/industry) - variable costs

Extrinsic (Market) Risk - Interest rate changes

Goal = Eliminate risk

HOW?

Hedging & Forward Contracts» What i f you cou ld know and commit to a pr ice for

buying and sell ing in 3 month s or 3 years from

now?

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 4/53

PD Hahn 4

Hedging with Forwards and Futures

For example….Kellogg produces breakfast cereal. A majorcomponent and cost factor is sugar. Imagine YOU ARE Kellogg

• Tesco and Sainsbury can order cereal for the next 6 months attoday’s list price.

• However, sugar prices could go up next week increasing costs andlowering Kellogg’s profit margin when producing cereal to meetorders.

• To fix your profit margin, you would ideally like to purchase all yoursugar today, since you like today’s price, and set your price forcereal based on it. But, you cannot.

• You can, however, sign a contract to purchase sugar at variouspoints in the future for a price negotiated today.

• This contract is called a “Forward” or a “Futures” Contract.

• Kellog’s managing it’s sugar costs is Hedging.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 5/53

PD Hahn 5

Hedging with Forwards and Futures

1- Spot Contract - A contract for immediate sale & delivery of an

asset.

2- Forward Contract - A contract between two people for the

delivery of an asset at a negotiated price on a set date in the future.

3- Futures Contract - A contract similar to a forward contract,

except there is an intermediary that creates a standardized

contract. Thus, the two parties do not have to negotiate the terms

of the contract.

The intermediary in a Futures contract is a an Exchange and it

guarantees all trades & “ provides” a secondary market for the

trading in Futures.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 6/53

PD Hahn 6

Types of Futures

Commodity Futures

-Sugar -Corn -OJ

-Wheat -Soy beans -Pork bellies

Financial Futures

-T-bills -Yen -GNMA

-Stocks -Eurodollars

Index Futures

-S&P 500 -Value Line Index

-Vanguard Index

SUGAR

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 7/53

Commodity Futures

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 8/53

Financial Futures

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 9/53

PD Hahn 9

Futures Contract Concepts

Not an actual sale

Always a winner & a loser (unlike stocks)

K are “settled” every day. (Marked to Market)

Hedge - K used to eliminate risk by locking in prices

Speculation - K used to gamble

Margin - not a sale - post partial amount (use leverage)

Hog K = 30,000 lbs ( “K ” is a contract )

T-bill K = $1.0 mil

“Valueline” Index K = $index x 500

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 10/53

PD Hahn 10

Futures and Spot Contracts

yieldDividendratefreeRisk

pricespotsToday'

lengthtof contracton pricefutures

)1(

0

0

yr

S

F

yr S F

f

t

t

f t

The basic relationship between futures prices and spot prices for equity securities.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 11/53

PD Hahn 11

Futures and Spot Contracts

ExampleThe DAX spot price is 5,952.38. The interest rate is 3.6% and thedividend yield on the DAX index is 2.0%. What is the expected priceof the 6 month DAX futures contract?

000,6

)01.018.1(38.952,5

)1(0

t

f t yr S F

Adjusted for 6 months

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 12/53

PD Hahn 12

Futures and Spot Contracts

yieldeConvenienc NetcoststorageExpresssc

yieldeConvenienc

ratefreeRisk

pricespotsToday'

lengthtof contracton pricefutures

)1(

0

0

sccyncy

cy

r

S

F

cy scr S F

f

t

t

f t

The basic relationship between futures prices and spot prices for commodities.

N.B. – ncy can

sometimes be positive(negative effect) if

supply/demand is

changing.

F t = S

0 (1 + r

f - ncy)

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 13/53

PD Hahn 13

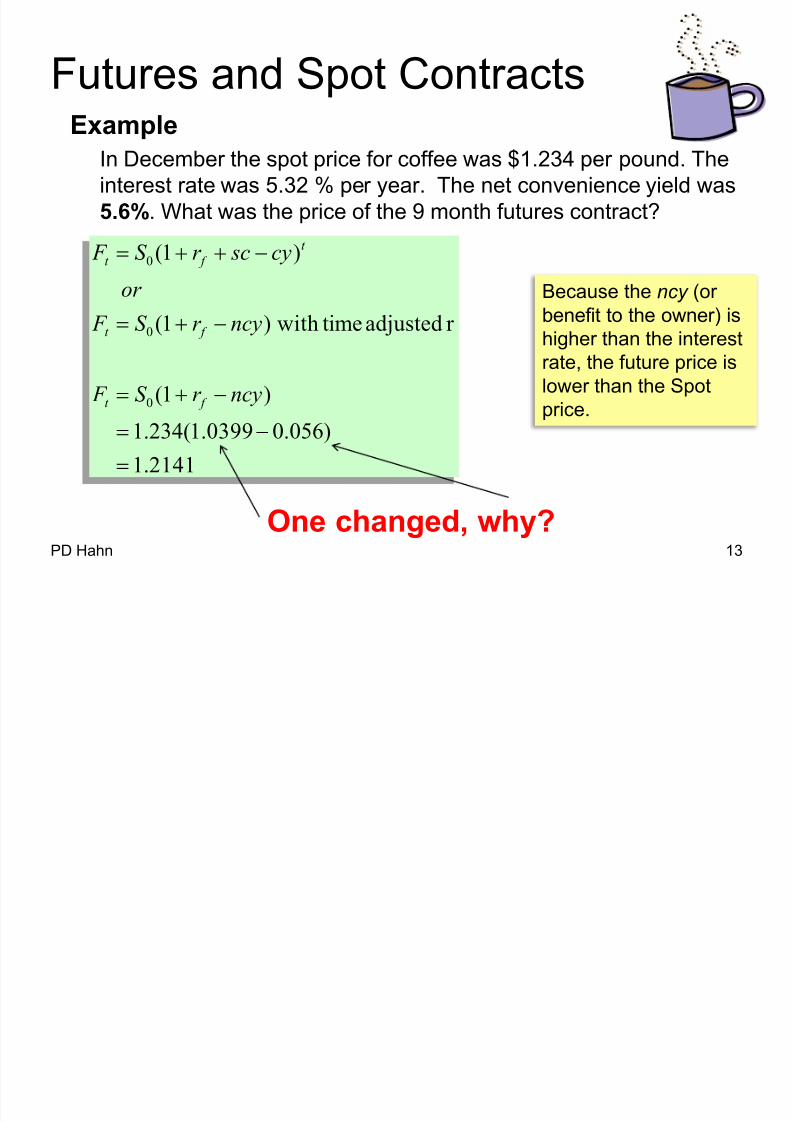

Futures and Spot ContractsExample

In December the spot price for coffee was $1.234 per pound. Theinterest rate was 5.32 % per year. The net convenience yield was5.6%. What was the price of the 9 month futures contract?

2141.1

)056.00399.1(234.1

)1(

r adjustedtimewith)1(

)1(

0

0

0

ncyr S F

ncyr S F

or

cy scr S F

f t

f t

t

f t

One changed, why?

Because the ncy (orbenefit to the owner) ishigher than the interestrate, the future price islower than the Spot

price.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 14/53

Futures and Spot Contracts

ExampleIn January the spot price for oil was $41.68 barrel. The interest ratewas 0.44 % per year. Given a one year futures price of $58.73,what was the net convenience yield?

F t = S 0 (1 + r f + sc - cy)t

58.73 = 41.68 (1 + 0.0044 - ncy)

ncy = -0.405

14

-0.405 = -40.5% , in otherwords, it wasn’t very valuableto hold oil during this period.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 15/53

Net Convenience Yield

A n n u a l i z e d N e t C o n v e n i e

n c e Y i e l d ,

%

-60.00

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

0 1 / 0 1 / 1 9 9 5

0 1 / 0 8 / 1 9 9 5

0 1 / 0 3 / 1 9 9 6

0 1 / 1 0 / 1 9 9 6

0 1 / 0 5 / 1 9 9 7

0 1 / 1 2 / 1 9 9 7

0 1 / 0 7 / 1 9 9 8

0 1 / 0 2 / 1 9 9 9

0 1 / 0 9 / 1 9 9 9

0 1 / 0 4 / 2 0 0 0

0 1 / 1 1 / 2 0 0 0

0 1 / 0 6 / 2 0 0 1

0 1 / 0 1 / 2 0 0 2

0 1 / 0 8 / 2 0 0 2

0 1 / 0 3 / 2 0 0 3

0 1 / 1 0 / 2 0 0 3

0 1 / 0 5 / 2 0 0 4

0 1 / 1 2 / 2 0 0 4

0 1 / 0 7 / 2 0 0 5

0 1 / 0 2 / 2 0 0 6

0 1 / 0 9 / 2 0 0 6

0 1 / 0 4 / 2 0 0 7

0 1 / 1 1 / 2 0 0 7

0 1 / 0 6 / 2 0 0 8

0 1 / 0 1 / 2 0 0 9

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 16/53

PD Hahn 16

SWAPS

Definition - An agreement between two firms, in which eachfirm agrees to exchange the “interest ratecharacteristics” of two different financial instruments ofidentical principal

Key points

Credit Spread inefficiencies (markets price risk differently)Same notation principal (the basis of deal size)

Only interest payments exchanged

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 17/53

PD Hahn 17

SWAPS

• Fixed rate payer (ABC), S&P rated A

• Floating rate payer (XYZ), Moody’s rated Aaa

• Counterparties

• Settlement dates (in our example, once peryear)

• Swap Benefit = reduction in borrowing cost

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 18/53

PD Hahn 18

SWAPSexample (annually settled) - Borrowing Options for XYZ & ABC

XYZ ABCFixed rate (Bond YTM) 10% 11.5%

Floating rate (Bank Loan) LIBOR + .25 LIBOR + .50

Assume LIBOR = 7%, do a swap (assume $1mil face value loans)

XYZ issues bond for $1mil @ 10% fixed

ABC borrows from bank $1mil @ 7.5% floating

The Swap: XYZ pays (ABC) floating (LIBOR) @ 7.00% ABC pays (XYZ) fixed @ 10.25%

We say the ‘ swap rate ’ is 10.25%

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 19/53

Swap Curves(similar to the term structure)

SWAP Curves for three currencies during March 2009

5-year swap rate in dollars

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 20/53

PD Hahn 20

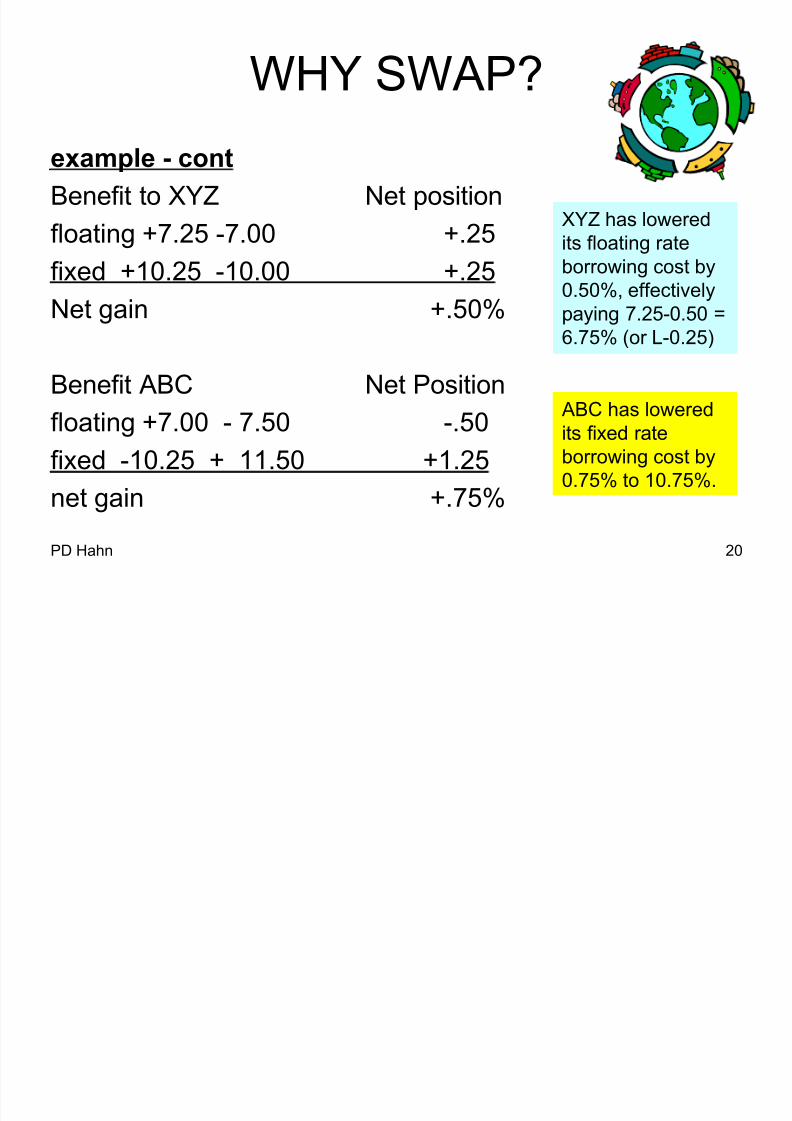

WHY SWAP?

example - cont

Benefit to XYZ Net position

floating +7.25 -7.00 +.25

fixed +10.25 -10.00 +.25Net gain +.50%

Benefit ABC Net Position

floating +7.00 - 7.50 -.50fixed -10.25 + 11.50 +1.25

net gain +.75%

XYZ has loweredits floating rateborrowing cost by0.50%, effectivelypaying 7.25-0.50 =6.75% (or L-0.25)

ABC has loweredits fixed rateborrowing cost by0.75% to 10.75%.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 21/53

PD Hahn 21

SWAPS

example - cont

Settlement date (assuming LIBOR doesn’t change)

ABC pmt 10.25% x 1mil = 102,500

XYZ pmt 7.00% x 1mil = 70,000

net cash pmt by ABC = 32,500

i f Libor r ises to 9%

settlement date

ABC pmt 10.25 x 1mil = 102,500XYZ pmt 9.00 x 1mil = 90,000

net cash pmt by ABC = 12,500

XYZ which haschanged its costto floating willpay more

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 22/53

An Easier Way…..

XYZ ABC-10%

-10

+10.25

-L

-(L-.25%)

10.25%

L%

-.50%

-L

-L

-.50

+L

-10.25

-10.75

BOND

ISSUE

BANK

BORROW

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 23/53

PD Hahn 23

SWAPS

A Forward or a Future?• rarely done direct

• banks = middleman

• bank profit = part of “swap gain”

example - same continued with a bank in betweenXYZ & ABC go to bank separately

XYZ term = SWAP floating @ LIBOR for fixed @ 10.25%

ABC terms = swap floating LIBOR + for fixed 10.50%

(was 10.25%)

Bank gets 0.25% p.a. (or $2500) for taking each side risk

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 24/53

Changes…

PD Hahn 24

New global banking regulation requires interestrate swaps to done outside of banks in coming

years and on financial exchanges with centralclearing parties (CCPs). Thus, the majority ofinterest swaps will become _________ fromtoday’s ________.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 25/53

PD Hahn 25

Speculation

Example - You are speculating in Hog Futures. You thinkthat the Spot Price of hogs will rise in the future. Thus, yougo Long on 10 Hog Futures. If the price drops .17 centsper pound ($.0017) what is total change in your position?

Long ± Own or Buy

and willbenefit fromprice rise

Short ± Sell or willbenefit fromprice fall

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 26/53

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 27/53

PD Hahn 27

Commodity Hedging1) In June, farmer John Smith expects to harvest

10,000 bushels of corn during the month of August. – He knows the cost of seed and fertilizer ($2.60 per

bushel or $26,000), but can’t be sure of his sale price, itcould go up or down.

2) In June, September corn futures are selling for$2.94 per bushel (1K = 5,000 bushels). FarmerSmith wishes to lock in this price (and his profit, hedoes not want to risk selling at a loss,

2K=$29,400).Show the futures transactions if the Sept spot price

rises to $3.05.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 28/53

PD Hahn 28

Commodity HedgeIn June, farmer John Smith expects to harvest 10,000

bushels of corn during the month of August. In June, theSeptember corn futures are selling for $2.94 per bushel(1K = 5,000 bushels). Farmer Smith wishes to lock inthis price.

Show the transactions if the Sept spot price rises to $3.05.

Revenue from Crop: 10,000 x 3.05 30,500

June: Short 2K @ 2.94 = 29,400

Sept: Long 2K @ 3.05 = 30,500 .

Loss on Position------------------------------- ( 1,100 )

Total Revenue $ 29,400

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 29/53

PD Hahn 29

Commodity Speculation

You have lived in London your whole life and areindependently wealthy. You think you know everythingthere is to know about pork bellies (uncured bacon)because your butler fixes it for you every morning.

Because you have decided to go on a diet, you think

the price will drop over the next few months.

On the CME, each PB K is 38,000 lbs (pounds weight).Today, you decide to short three May Ks @ 44.00 cents

per lbs. In Feb, the price rises to 48.5 cents and youdecide to close your position. What is your gain/loss?

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 30/53

PD Hahn 30

The Market Needs Speculators

-----Why?Nov: Short 3 May K (.4400 x 38,000 x 3 ) = + 50,160

Feb: Long 3 May K (.4850 x 38,000 x 3 ) = - 55,290

Loss of 10.23 % = - 5,130

If you w ere Farmer Smith, and you on ly planted

one of two f ie lds , and you saw that speculators

had pushed the price of Sept co rn to $3.50,what wou ld you do?

Speculators can influence (provide information to) producers

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 31/53

PD Hahn 31

Margin

• The amount (percentage) of a Futures Contract Valuethat must be on deposit with a broker (the exchange).

• Since a Futures Contract is not an actual sale, you needonly pay a fraction of the asset value to open a position =margin.

• CME margin requirements are 15%

• Thus, you can control $100,000 of assets with only

$15,000.

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 32/53

PD Hahn 32

Nov: Short 3 May K (.4400 x 38,000 x 3 ) = + 50,160Feb: Long 3 May K (.4850 x 38,000 x 3 ) = - 55,290

Loss = - 5,130

Loss 5130 5130

Margin 50160 x.15 7524------------ = -------------------- = ------------ = 68% loss

Our wealthy London friend now buys….On the CME, each PB K is

38,000 lbs. Today, you decide to short three May Ks @ 44.00 cents perlbs. In Feb, the price rises to 48.5 cents and you decide to close yourposition. What is your gain/loss?

Commodity Speculation with margin

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 33/53

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 34/53

PD Hahn 34

Option Obligations

Buyer Seller

Call option Right to buy asset Obligation to sell asset

Put option Right to sell asset Obligation to buy asset

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 35/53

PD Hahn 35

Options

TerminologyDerivatives - Any financial instrument that is derived from

another. (e.g.. options, warrants, futures, swaps, etc.)

Opt ion - Gives the holder the right to buy or sell a security at aspecified price during a specified period of time.

Call Optio n - The right to buy a security at a specified pricewithin a specified time.

Put Option - The right to sell a security at a specified price withina specified time.

Opt ion Premium - The price paid for the option, above the price

of the underlying security.Intr ins ic Value - Diff between the strike price and the stock price

Time Prem ium - Value of option above the intrinsic value

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 36/53

PD Hahn 36

OptionsTerminology

Exercise Price - (Striking Price) The price at which you buy orsell the security.

Expirat ion Date - The last date on which the option can beexercised.

American Option - Can be exercised at any time prior to and

including the expiration date.European Option - Can be exercised only on the expiration

date.

Al l opt ions “usual ly ” act l ike Europ ean op t ions because you

make mo re money i f y ou sell the opt ion b efore expiration

(vs . exerc ising it) .

3 vs. 70-68=2

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 37/53

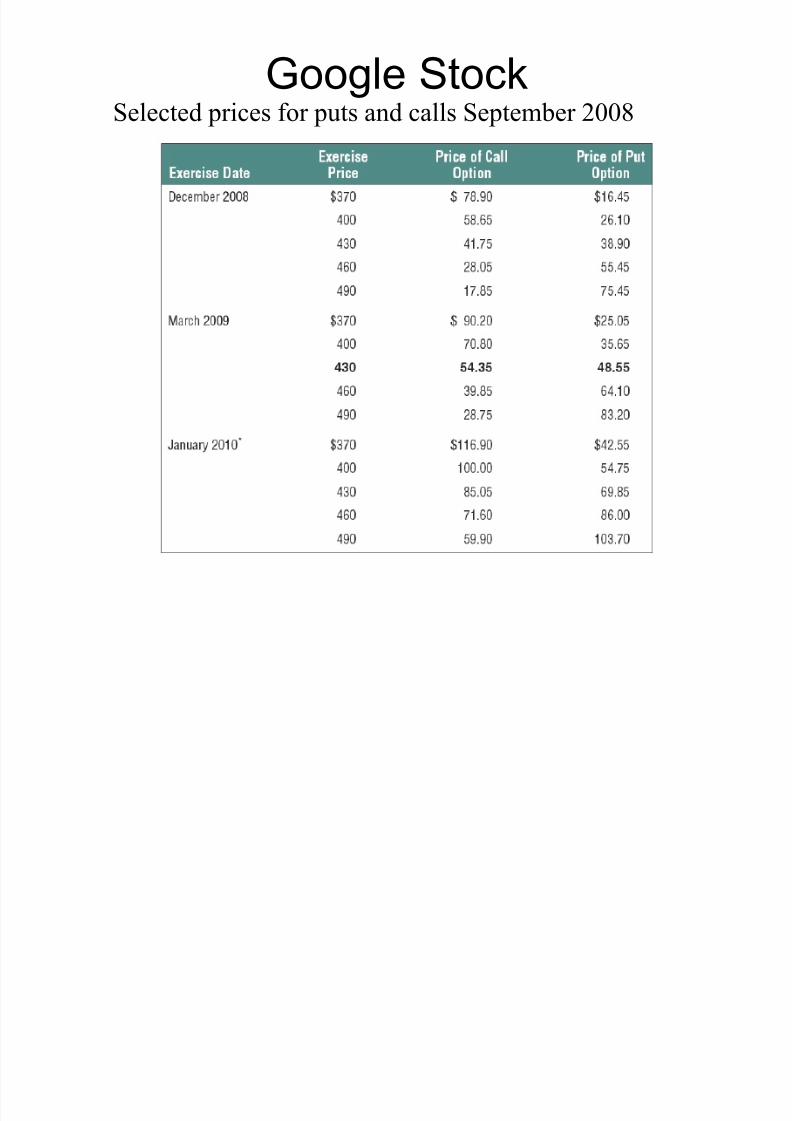

Google StockSelected prices for puts and calls September 2008

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 38/53

PD Hahn 38

Colgate-Palmolive StockSelected prices for puts and calls June 2011

Shareprice is$80.00

Exercise Date or Exercise Price of Call Price of Put

Option Maturity Price Option Option

September 2011 $70 $14.30 $0.75

75 9.90 1.40

80 6.50 2.75

85 3.70 5.10

90 1.90 8.70

December 2011 $70 $15.10 $2.20

75 12.20 2.65

80 9.00 4.60

85 6.20 7.70

90 4.10 9.46

March 2012 $70 $20.50 $4.3075 18.00 5.70

80 14.90 7.30

85 12.00 10.40

90 9.90 12.70

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 39/53

PD Hahn 39

Option Value

• The value of an option at expiration is afunction of the stock price and the exerciseprice.

Example - Option values given an exercise priceof $80

00001020ValuePut

302010000ValueCall

110100908070$60PriceStock

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 40/53

PD Hahn 40

Option Value

Call option value (position diagram) given a $80 exercise price, for the buyer of the call option.

Share Price

C

a l l o p t i o n v a

l u e

80 95

$15

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 41/53

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 42/53

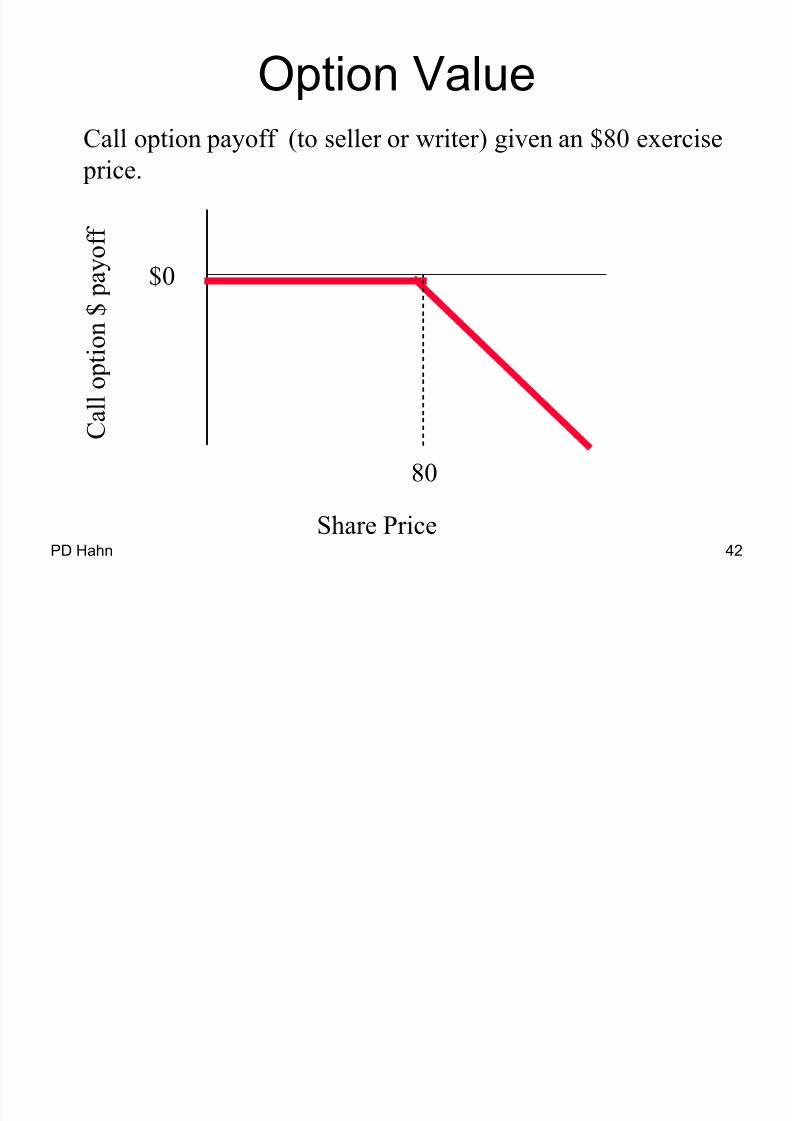

PD Hahn 42

Option Value

Call option payoff (to seller or writer) given an $80 exercise price.

Share Price

C a

l l o p t i o n $ p a

y o f f

80

$0

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 43/53

PD Hahn 43

Option Value

Put option payoff (to seller) given a $80 exercise price.

Share Price

P u t o p t i o n $ p a

y o f f

80

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 44/53

PD Hahn 44

Option ValueCall buyer profit – assume strike of $80 and

option price of $9.00 (a profit diagram)

Share Price

P o s i t i o n V a l u e

Long call

80 89

- 9.00

Break even

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 45/53

PD Hahn 45

Option ValuePut seller profit – assume strike of $80 and

option price of $4.60

Share Price

P o s i t i o n V a l u e

Short put

75.40 80

+4.60

Break even

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 46/53

PD Hahn 46

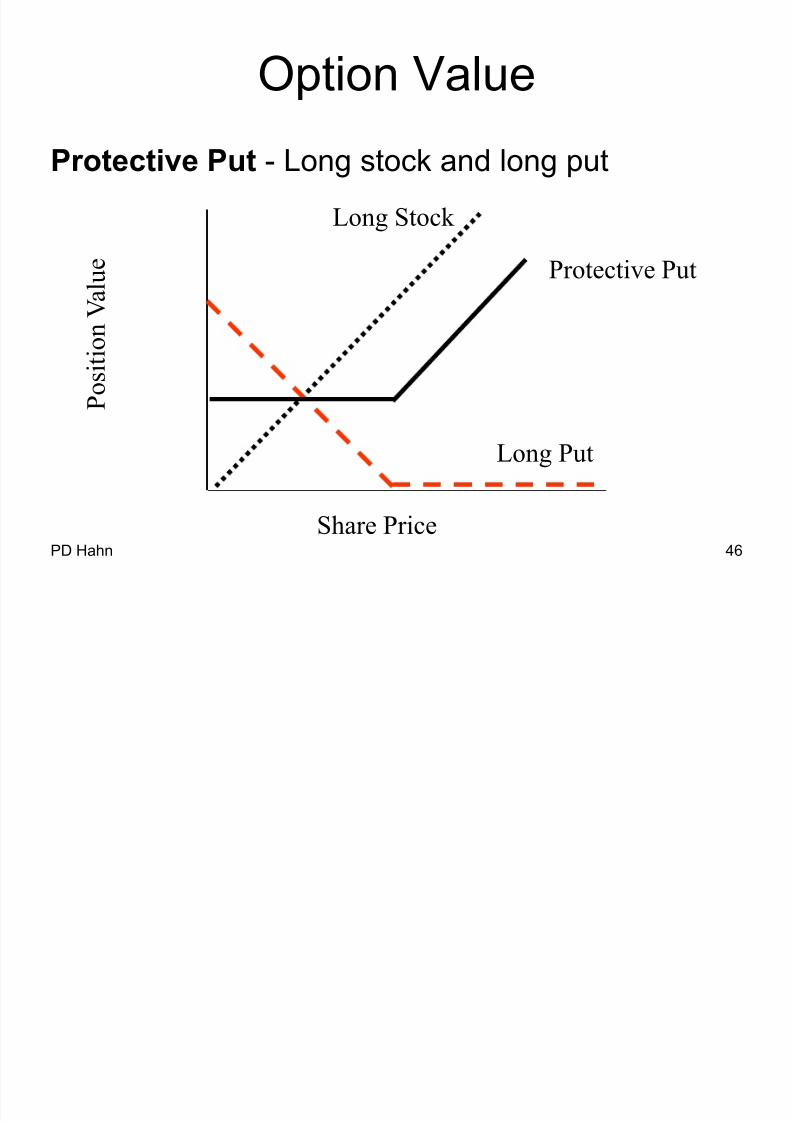

Option Value

Protective Put - Long stock and long put

Share Price

P o s i t i o n V a l u e

Protective Put

Long Put

Long Stock

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 47/53

PD Hahn 47

Option ValueStraddle - Long call and long put

- Strategy for profiting from high volatility

Share Price

P o s i t i o n V a l u e

Straddle

Long put Long call

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 48/53

PD Hahn 48

Option Value

Components of the Option Price

1 - Underlying stock price = Ps

2 - Striking or Exercise price = S

3 - Volatility of the stock returns (standarddeviation of annual returns) = v

4 - Time to option expiration = t = days/3655 - Time value of money (discount rate) = r

6 - PV of Dividends = D = (div)e-rt

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 49/53

PD Hahn 49

Time Decay Chart

OptionPrice

Stock Price

Option prices decline, ceribus paribus, when

the time to expiration declines.

90 days to expiration

60 days to expiration

30 days to expiration

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 50/53

PD Hahn 50

Option Value

The greater the distribution ofpossible outcomes, relative tothe final price of the stock, thehigher the value of the option.This is due to the greater

potential for profit. Thus, Y willhave a higher option price,ceribus paribus. Share Y hasa higher σ or has more risk(volatility).

Option value goes up withvolatility. Why?

T i C d

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 51/53

PD Hahn 51

Topics Covered

– Introduction to Hedging Tools

– Forwards, Futures, Swaps

– Calls, Puts and Shares

– Derivative Securities

– Financial Alchemy with Options

– What Determines Option Values?We l l review next week

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 52/53

8/12/2019 POF_Week_9_SB (2)

http://slidepdf.com/reader/full/pofweek9sb-2 53/53

PD Hahn 53

See you next week

We will review options at the beginning of

next week’s lecture.

![[XLS] · Web view1 2 2 2 3 2 4 2 5 2 6 2 7 8 2 9 2 10 11 12 2 13 2 14 2 15 2 16 2 17 2 18 2 19 2 20 2 21 2 22 2 23 2 24 2 25 2 26 2 27 28 2 29 2 30 2 31 2 32 2 33 2 34 2 35 2 36 2](https://static.fdocuments.in/doc/165x107/5ae0cb6a7f8b9a97518daca8/xls-view1-2-2-2-3-2-4-2-5-2-6-2-7-8-2-9-2-10-11-12-2-13-2-14-2-15-2-16-2-17-2.jpg)