PLG Consulting Appalachian logistics League May 5, 2015

20

Logistics Engineering Supply Chain The North American Energy Revolution: Implications for Logistics Prepared for: Appalachian Logistics League Taylor Robinson, President, PLG Consulting May 5, 2015

-

Upload

plg-consulting -

Category

Business

-

view

198 -

download

1

Transcript of PLG Consulting Appalachian logistics League May 5, 2015

Logistics Engineering Supply Chain

The North American Energy Revolution:

Implications for Logistics

Prepared for:

Appalachian Logistics League

Taylor Robinson, President, PLG Consulting

May 5, 2015

2

Experience

Delivering value to over

200 clients since 2001

Real-world, industry

veterans

Logistics, engineering &

supply chain experts with

operational experience

Core Expertise

Bulk Logistics

Freight Rail

Energy & Chemical

Markets

Investment Advisory and

Corporate Development

Partial Client List

Services

Diagnostic assessments &

optimization

Logistics Infrastructure

design

Supply chain design &

operational improvement

Investment strategy, target

identification, due diligence,

post-transactional support

Crude by rail (CBR) and rail

tank car (RTC) forecasts

Independent technology

assessment &

implementation

Hazmat training, auditing &

risk assessment

About PLG Consulting

The North American Energy Revolution: Implications for Logistics

3

ssSource: CAPP, About Oil Sands

Source: EIA, May 2014

US Shale

Unconventional Energy Resources and Extraction Technologies

The North American Energy Revolution: Implications for Logistics

Western Canadian (WC)

Oil Sands

Source: www.epmag.com

SAGD

Horizontal Drilling & Hydraulic Fracturing

Source: Marathon, February 2014

“Moore’s Law” at play: Exponential

advances in technology, resulting in

Declining costs

Surging production

Representative Producer Gains, Eagle Ford

Source: RBN Energy, December 2014

4

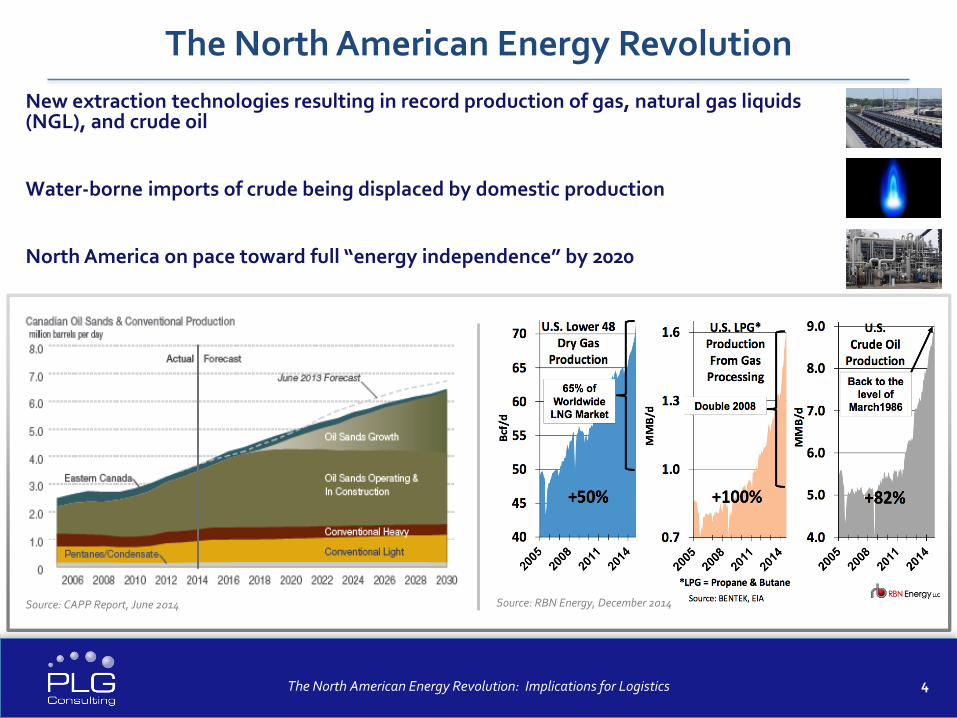

New extraction technologies resulting in record production of gas, natural gas liquids (NGL), and crude oil

Water-borne imports of crude being displaced by domestic production

North America on pace toward full “energy independence” by 2020

Source: CAPP Report, June 2014 Source: RBN Energy, December 2014

The North American Energy Revolution

The North American Energy Revolution: Implications for Logistics

5

Shale Supply Chain and Downstream Impacts

Feedstock (Ethane)

Byproduct (Condensate)

Home Heating (Propane)

Other Fuels

Other Fuels

Gasoline

Gas

NGLs

Crude

Proppants

OCTG

Chemicals

Water

Cement

Generation

Process Feedstocks

All Manufacturing

Steel

Fertilizer (Ammonia)

Methanol

Chemicals

Petroleum Products

Petro-chemicals

Inputs Wellhead Direct

Output Thermal Fuels Raw Materials

The next wave:Manufacturing renaissance in the US based on abundant, low cost

energy and feedstocks

Impacts to-date include: Dramatic reduction in crude imports, lower electricity costs, lower

gasoline prices, increased refined products exports

Downstream Products

The North American Energy Revolution: Implications for Logistics

6

0

2,000

4,000

6,000

8,000

10,000

12,000

1970

1972

1974

1976

1978

198

0

198

3

198

5

198

7

198

9

199

1

199

3

199

6

199

8

20

00

20

02

20

04

20

06

20

09

20

11

20

13

U.S. Crude Oil Production (kbpd)

Source: EIA, February 2015

U.S. crude oil production growth Crude oil production over 9 MMbpd, up from 5

MMbpd in 2008

Growth has come primarily from shale oil production of light crude

2015 production close to US record of 1970

Decrease in crude oil imports Shale crude has been pushing out light crude

imports

Heavy sour crude imports have been steady, with Canada growing to become the primary US supplier

North America now supplies 2/3 of the U.S. crude demand

0

2,000

4,000

6,000

8,000

10,000

12,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

U.S. Crude Oil Imports (kbpd)

Source: EIA, February 2015

Historical U.S. Crude Oil Production and Imports

The North American Energy Revolution: Implications for Logistics

7

Source: RBN Energy, January 2015

WTI, Brent & Natural Gas 2014 and 2015

Citibank cut its crude price forecasts, saying West Texas Intermediate (WTI) could go as low as the $20 per barrel range before recovering to reach a new equilibrium.- Reuters (2/9/2015)

The market doesn’t understand just how quickly oil companies are scaling back their activities, and as a result, oil prices could rebound faster than many observers expect.- Continental Resources CEO Harold Hamm (Fuelfix, 1/28/2015)

• U.S. shale oil industry has now entered

uncharted territories in its brief history

• Natural Gas and NGL pricing has also

dropped dramatically in a similar

timeframe…due to oversupply and NGL

ties to oil prices

• Market experts have widely varied

opinions on what the rest of the year

holds for pricing - ~$10-$70 per barrel…

2014: Oversupply Has Caused Precipitous Price Declines

The North American Energy Revolution: Implications for Logistics

8

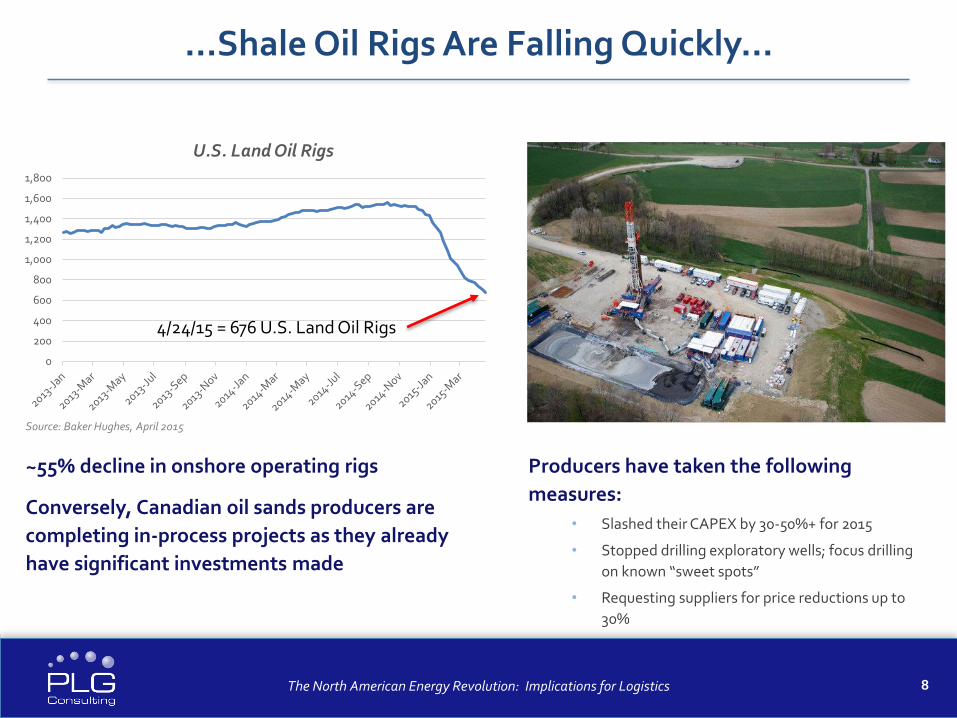

Producers have taken the following

measures:

• Slashed their CAPEX by 30-50%+ for 2015

• Stopped drilling exploratory wells; focus drilling

on known “sweet spots”

• Requesting suppliers for price reductions up to

30%

~55% decline in onshore operating rigs

Conversely, Canadian oil sands producers are

completing in-process projects as they already

have significant investments made

…Shale Oil Rigs Are Falling Quickly…

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

U.S. Land Oil Rigs

Source: Baker Hughes, April 2015

4/24/15 = 676 U.S. Land Oil Rigs

The North American Energy Revolution: Implications for Logistics

9

…However, Crude Oil Production Will Continue at High Levels

0

1

2

3

4

5

6

7

8

9

Lower 48 States (excl GOM) Crude Oil Production (MMBPD), Includes Lease Condensate

Source: EIA, February 2015 Source: CAPP, January 2015

Cost reduction focus and “sweet spot” drilling will continue to lower break even cost

Held by Production (HBP) lease clauses will help support production

Smaller, weaker players will fall while stronger producers will actually grow during downturn

Oil sands has a 20-50 year view on projects

R&D budgets cut; new greenfield projects delayed

SAGD wells have lower break even costs compared to shale wells

Current pricing is a short term issue from their perspective

The North American Energy Revolution: Implications for Logistics

10

Source: RBN Energy, February 2015

At $50/bbl oil, producers are mostly at or below breakeven

Producer Rates of Return by Play and Product(Before Cost Reductions)

The North American Energy Revolution: Implications for Logistics

11

Producer Rates of Return by Play and Product(After Cost Reductions)

Source: RBN Energy, February 2015

Producers can be profitable at $50/bbl oil with cost reductions

The North American Energy Revolution: Implications for Logistics

12

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2015 2016 2017 2018 2019 2020 2025

WTI (Cushing) Forecast Pricing ($/bbl)

Source: Turner Mason, February 2015

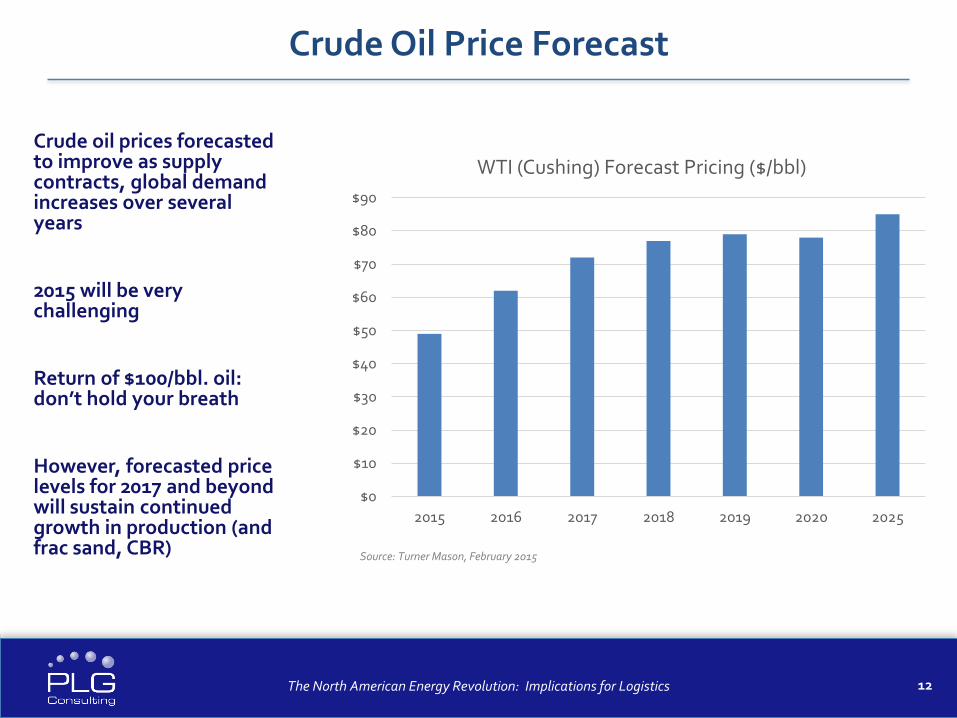

Crude oil prices forecasted to improve as supply contracts, global demand increases over several years

2015 will be very challenging

Return of $100/bbl. oil: don’t hold your breath

However, forecasted price levels for 2017 and beyond will sustain continued growth in production (and frac sand, CBR)

Crude Oil Price Forecast

The North American Energy Revolution: Implications for Logistics

13

NA Crude Logistics Today

Sources: EIA, PLG analysis (Google Earth)

Light/Sweet

Heavy/Sour

Pacific Northwest Refiners

California Refiners

2,525kbpd

PADD VDemand

Midwest Refiners

3,375kbpd

PADD II Demand

East Coast Refiners

PADD I Demand1,075kbpd

LA Gulf Coast Refiners

TX Gulf Coast Refiners

PADD III Demand8,150

kbpd

Eagle Ford

Permian

Bakken

Rail

Pipeline

Marine

Oil Sands

GOM

The North American Energy Revolution: Implications for Logistics

14

New tank car standard (DOT 117) 9/16” shell, jacketed, full-height head

shield

Retrofit timeline 2018 – 2025 depending on Packing Group (“PG”) and CPC1232/non-CPC1232

ECP braking required for unit trains 2021 for PG I and 2023 for PG II & III

Other parts of the ruling Ruling restricts flammable trains to 50-

mph in all areas and if train contains any new non-enhanced tank car then speed is restricted to 40-mph in high-threat urban areas

Document sampling and testing program for all unrefined petroleum-based products, such as crude oil

Railroads operating flammable trains required to perform a routing analysis that considers, at a minimum, 27 safety and security factors and select a route based on its findings

DOT Final Flammable Trains Final Ruling

The North American Energy Revolution: Implications for Logistics

15

US gas demand will grow due to: Coal-fired generation plant converting to

gas

More industrial use – steel, fertilizer, methanol

Mexican export via pipeline and LNG export overseas

Increasing use as transportation fuel

US gas cost competitiveness is sustainable

30+ year supply at ~$4 mm/btu; cost of production decreasing

Supply will overwhelm demand as prices approach $5/

US government will likely limit LNG export to protect US from world gas market price

Low-cost gas and NGLs driving US industrial “renaissance”

Source: EIA, February 2015

60

65

70

75

80

85

2008 2009 2010 2011

U.S. Natural Gas Production (Bcf/day)

Actual Forecast

0

2

4

6

8

10

12

14

Natural Gas Price at Henry Hub ($/MMBTU)

Historical Futures

Source: EIA for historical and CME Group for futures as of Jan. 14, 2015

US Shale Gas Background and Future

The North American Energy Revolution: Implications for Logistics

16

Ethane and propane production growth with shale gas Raw NGLs (y-grade) are extracted creating dry gas and y-grade streams; dry gas primarily used as a fuel for heat and power

Y-grade is sent to a fractionator where it is made into “purity” NGLs – ethane, propane, butane, iso-butane, natural gasoline

Ethane and propane are the largest components of the y-grade and are therefore seeing large growth in the U.S.

U.S. infrastructure build-out continues to process the huge low cost production volume increase in ethane and propane

Source: OPIS, December 2014 & CME Group, December 2014

Gas Value Chain

Source: Bentek: North American NGLs 4Q2014

Shale Gas, NGLs, and Downstream Chemical Processing

The North American Energy Revolution: Implications for Rail

17

Ethylene and Propylene

Ammonia and Derivatives

Methanol

Polymers and Resins

Chlor-alkali

Other

Source: American Chemistry Council and PLG analysis

Over $135B of New Shale-Related CAPEX Investments Have Been Announced

The North American Energy Revolution: Implications for Logistics

18

Abundant feedstock, structural cost advantages, and domestic market growth driving US petrochemical industry expansion

Rate of expansion growth will be slowed by Lack of EPC capacity

Shortage of craft labor resources in the U.S. Gulf Coast

Increasing regulatory hurdles and delays

Expansion peak will be dampened and overall build-out will take longer than announced schedules

U.S. chemical industry is entering a historic growth period with incredible growth opportunities and challenges

Source: ACC and PLG Analysis, December 2014

ACC Estimate

PLG Estimate

U.S. Chemical Industry Capital Investment: Incremental Due to Shale Gas

0

200

400

600

800

1,000

1,200

1,400

SaudiEthane

US Ethane USWeighted

WE LowCost

AsiaNaphtha

USNaphtha

Dec. 2013

Dec. 2014

Source: Townsend Solutions, December 2014

Cash Cost US$/ton (Ethylene)

US Chemical Industry Build-Out

The North American Energy Revolution: Implications for Logistics

19

We are in the early innings of the North American energy revolution

Natural gas – the first shale “oversupply” example

Crude oil – new shale and maturation of Canadian oil sands

NGL – a valuable byproduct from natural gas and crude drilling

Downstream chemicals and manufacturing – coming soon!

Lower hydrocarbon pricing environment is mainly caused by oversupply

Pricing will speed up cost reduction throughout supply chain

Industry consolidation will ensure long term global competitiveness

Lower oil prices will dampen growth profile for frac sand and crude by rail volume in the short term

Tank car and small covered hopper market has shifted gears to “neutral” for now

Near-term (2015-2016) turbulence on the way to 10+ years of growth and industrial expansion

Net positive for rail industry; growth opportunities for wide variety of railcar types

Presentation Summary

The North American Energy Revolution: Implications for Logistics

Logistics Engineering Supply Chain

Thank You !For follow up questions and information,

please contact:

Taylor Robinson, President+1 (508) 982-1319 / [email protected]

This presentation is available for download at:http://plgconsulting.com/category/presentations/