PLAG.2789.02.06 Critical Illness Insurance … NOW is the Time! Mary Grahovac, ACS Regional Vice...

30

PLAG.2789.02.0 6 Critical Illness Insurance … NOW is the Time! Mary Grahovac, ACS Mary Grahovac, ACS Regional Vice President Regional Vice President Protective Life Insurance Company Protective Life Insurance Company R. J. (Bob) Ley, RHU R. J. (Bob) Ley, RHU Vice President, A&H Sales Vice President, A&H Sales AIG American General AIG American General

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of PLAG.2789.02.06 Critical Illness Insurance … NOW is the Time! Mary Grahovac, ACS Regional Vice...

PLAG.2789.02.06

Critical Illness Insurance … NOW is the Time!

Mary Grahovac, ACSMary Grahovac, ACS

Regional Vice PresidentRegional Vice President

Protective Life Insurance CompanyProtective Life Insurance Company

R. J. (Bob) Ley, RHUR. J. (Bob) Ley, RHU

Vice President, A&H SalesVice President, A&H Sales

AIG American GeneralAIG American General

““Not because you are going to die, but because Not because you are going to die, but because you are going to survive!”you are going to survive!”

Dr. Marius BarnardDr. Marius Barnard

Surviving Critical Illness

We all know someone who has survived

Cancer…a Heart Attack…a Stroke.

But what was the financial impact on their family?

There is a solution to help prevent a critical illness from becoming a financial

catastrophe and destroying lives.

Historical Perspective

South Africa – 1983 Asia – Late 1980’s United Kingdom – 1987 Australia – 1990 Japan - 1993 Canada - 1995

Critical Illness was only accepted by 3% of the Critical Illness was only accepted by 3% of the producer market in England 10 years ago. Now producer market in England 10 years ago. Now it is promoted by 99% of the same market.it is promoted by 99% of the same market.

Peter DoddPegasus LifeLondon, England November 1999

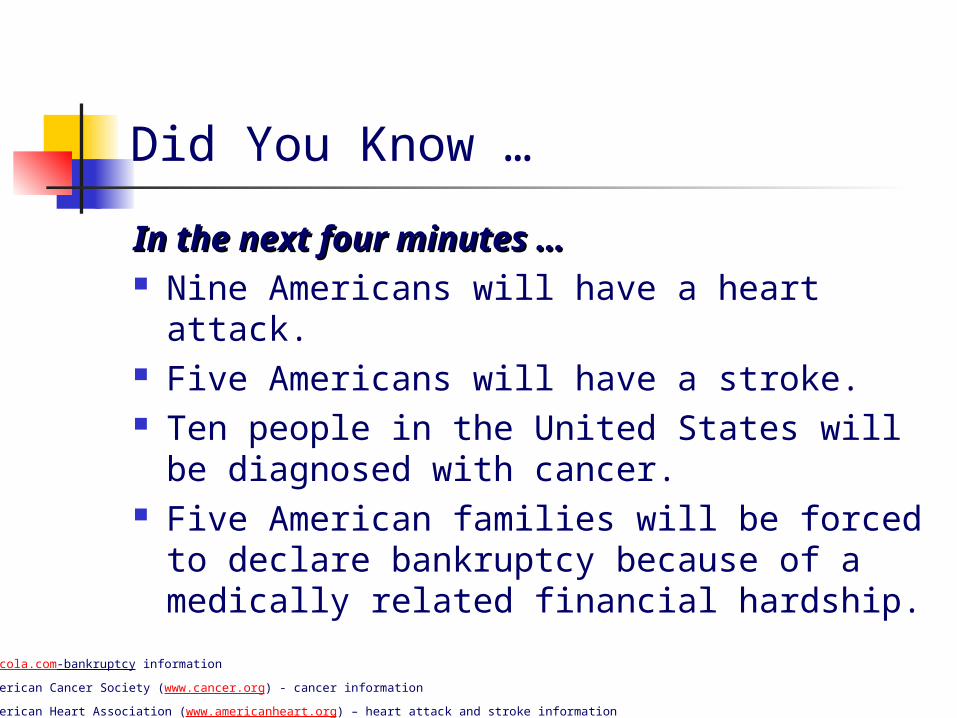

Did You Know …

In the next four minutes …In the next four minutes … Nine Americans will have a heart attack. Five Americans will have a stroke. Ten people in the United States will be

diagnosed with cancer. Five American families will be forced to

declare bankruptcy because of a medically related financial hardship.

Sources: www.mercola.com-bankruptcy information

American Cancer Society (www.cancer.org) - cancer information

American Heart Association (www.americanheart.org) – heart attack and stroke information

Did You Know …

Every 45 seconds, someone will have a stroke. This number 3 killer is the leading cause of severe, long-term disability.

The leading cause of disease in women is cardiovascular disease, more than cancer, and only 13% of women consider cardiovascular disease their greatest risk. And, 40,000 more women than men have a stroke annually.

In 2000, 9.6 million Americans were alive having survived a history of cancer.

Sources: “Heart Disease and Stroke Statistics – 2005 Update” American Heart Association. Dallas, Texas. 2005. “Heart Disease and Stroke Statistics – 2004 Update” American Heart Association. Dallas, Texas. 2004.

Did You Know …

Approximately 1.7 million Americans suffer a heart attack each year. Of these individuals, 1.2 million will survive at least 3 years …75% are under the age of 47!1

The survival rate for cancer patients is 73% today.2

A person who has a heart attack at age 45 has a 57% chance of surviving for 5 years or longer.2

1 Source: National Center for Health Statistics/OptimumRe

2 Source: American Cancer Society and American Heart Association/OptimumRe

Sources: LIMRA’s Marketfacts Spring 2002 “Critical Illness Insurance: A Lump-Sum Review”

“Know the Facts, Get the Stats: American Heart Association 2002-2004”. (55-0576).2003

Are you prepared inthe event of a critical illness?

According to the U. S. Department of Housing and Urban Development, 50% of home foreclosures are the result of the homeowner suffering from a critical illness.

American Heart Association estimates Americans paid about $368 billion in 2004 for heart disease related medical costs and disability.

Research shows 33% of all families deplete all or most of their savings because of a serious illness.

The Cost of SurvivalExpenses usually covered by healthcare insurance:

Surgery Hospitalization Prescription

Medications Doctors Office Visits

Expenses not usually covered by healthcare plans:

Experimental Treatment Childcare, Housekeeping Transportation & Lodging

During Treatment for Family

Home or Auto Modifications

Home Healthcare Needs Lost Income

Product Designs

Stand Alone Critical Illness product built on a health

chassis Acceleration

A Critical Illness rider added to a life chassis product

Product Designs

First Generation Lump sum benefit paid upon first

occurrence and diagnosis of a covered critical illness; policy lapses following payment

Second Generation Lump sum benefit paid upon first

occurrence and diagnosis of a covered critical illness; policy remains in-force to pay subsequent benefits

Product Designs

Subsequent Benefits Additional benefit payment for a subsequent

first occurrence and diagnosis of an additional covered critical illness

Additional benefit payment for second occurrence of critical illness for which a benefit has already been paid

Product Strategies

Fully Underwritten Generally benefit amounts up to $500,000

Simplified Issue Generally worksite products with lower

benefit amounts usually up to $100,000 Guarantee Issue

Group Chassis – generally benefit amounts of $5,000 to $20,000

Critical Illnesses Covered by Various Carriers

Heart Attack Coronary By-Pass Angioplasty Invasive Cancer Cancer in Situ Stroke End Stage Renal Failure Major Organ Transplant Coma Aortic Surgery

Severe Burns Blindness Deafness Paralysis Advanced Alzheimer’s

Disease Loss of Independent

Living Multiple Sclerosis Motor Neuron Disease Benign Brain Tumor Heart Valve Surgery

Product Differentiators

Benefit Extension Riders Continuance Recurrence

Multiple Payment Benefit Benefits for Spouse/Children Return of Premium Upon Death Best Doctors

Underwriting Critical Illness Insurance

Remember … incidence occurs before mortality

Morbidity based underwriting versus mortality based underwriting For example, in assessing coronary risk,

there is a higher occurrence for the event of either a heart attack or coronary bypass surgery than the probability of dying from either one of these.

Source: OptimumRe

Underwriting Critical Illness Insurance

Family history typically has a greater impact on CI underwriting than life underwriting. Variables associated with family (natural parents and siblings) history include: The number of affected first degree relatives

(FDR) The FDR’s age at diagnosis – not death The current age of the applicant The sex of the applicant (in some cases)

Source: OptimumRe

Potential Impact of Family History on CII

18

23

28

33

38

43

48

53

58

63

18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63

Age of Applicant

Age o

f D

iagnosi

s of FD

R

Less Impact

Greater Impact

Underwriting Critical Illness Insurance

Build is an important factor in critical illness underwriting; obesity is a major contributor to cancer and heart disease

Generally, APSs will be ordered more frequently on CI applications

Typically the best candidates for standard CI underwriting would be the those individuals eligible to qualify for Select Preferred or Preferred life underwriting

Source: OptimumRe

Business Market Key Person Buy-Sell Worksite/PRD

Professionals/Highly Compensated maxed-out on personal DI protection

Singles, Single Parents Family Market – one or both spouses

employed

Selling Critical Illness … Who’s a Prospect?

Selling Critical Illness … Who’s a Prospect?

Alternative to DI to those who can’t qualify for traditional product Stay-at-home Moms/Dads Truckers, Barbers, Work out of home

“Assets under management” protection

Mortgage Market Only 3% of Mortgage foreclosures are due

to death1

Source: 1 Ken Smith, Assurity Life

President, National Association for Critical Illness Insurance

Consumer Focus Groups

Reinsurance Companies conducted consumer focus groups to get input on the concept of CI insurance protection

They found these participants to be among the most enthusiastic of any focus groups ever conducted on any insurance product

Source: Ken Smith, Assurity Life

President, National Association for Critical Illness Insurance

The Gap Between What ProducersOffer and What Clients Want

Long Term Care Insurance

Longevity Insurance Critical Illness Insurance

28%21%

8%5%

13%

2%

Currently obtain from advisor

Would like to discuss with advisor

Source: Fidelity Advisor 2006 Survey of Investors at Retirement

McKinsey & Company 2006 Consumer Retirement Survey

Effective and Compelling Marketing - Consumers

Focus on the need for CII - They don’t already have it It’s hard to self-fund Health insurance isn’t full coverage They are financially ill-prepared

Communicate what the product is and what the product is not

Issues and Concerns

Education/Awareness by both producers and consumers

Evolving Medical Technology Future of US Health Care

The Future?

Embedded benefits, Optional riders Product Evolutions

More triggers Unique payouts Conversion options

Packaging Mortgage, DI, LTC

More carriers entering the market with ongoing product development

PLAG.2789.02.06

Critical Illness Insurance …NOW is the Time!