PIMCO Funds CommodityRealReturn Strategy Fund Portfolio Holdings 731

PIMCO Europe Ltd.

February 2015

For professional use only

1

Important information

For professional use only

The services and products described in this communication are only available to professional clients as defined in the Financial Conduct Authority's Handbook.

This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to

change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but

do not warrant its accuracy or completeness.

PIMCO Europe Ltd (Company No. 2604517), PIMCO Europe Ltd Amsterdam Branch (Company No. 24319743), and PIMCO Europe Ltd – Italy (Company No. 07533910969) are

authorised and regulated by the Financial Conduct Authority (25 The North Colonnade, Canary Wharf, London E14 5HS) in the UK. The Amsterdam and Italy Branches are

additionally regulated by the AFM and CONSOB in accordance with Article 27 of the Italian Consolidated Financial Act, respectively. PIMCO Europe Ltd services and products

are available only to professional clients as defined in the Financial Conduct Authority’s Handbook and are not available to individual investors, who should not rely on this

communication. | PIMCO Deutschland GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany) is authorised and regulated by the German Federal Financial

Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 32 of the German Banking Act (KWG). The services

and products provided by PIMCO Deutschland GmbH are available only to professional clients as defined in Section 31a para. 2 German Securities Trading Act (WpHG).

They are not available to individual investors, who should not rely on this communication.

(Presented in the UK)

2

Biographical information

Mike Amey

Mr. Amey is a managing director and portfolio manager in the London office. He is

responsible for sterling portfolios, the European insurance (ex Germany) and the

European LDI (liability-driven investing) portfolio management groups. Prior to joining

PIMCO in 2003, he was head of U.K. fixed income at Rothschild Asset Management and

after their merger, at Insight Investment. Prior to joining Rothschild in 1994, Mr. Amey

spent two years tutoring in the Department of Economics at the University of Durham. He

has 21 years of investment experience and holds undergraduate and master's degrees in

corporate and international finance from the University of Durham. Mr. Amey is also a

member of the U.K. Society of Investment Professionals.

3

Government bond yields at historic lows

As of 20 January 2015

SOURCE: Bloomberg, Bank of England

The high interest rates of the 70s and 80s, not today’s low yields, were the aberration

3cs_intl_outlook_02

0

2

4

6

8

10

12

14

16

1713 1763 1813 1863 1913 1963 2013

Yie

ld (

%)

Three centuries of long-term yields in the UK

4

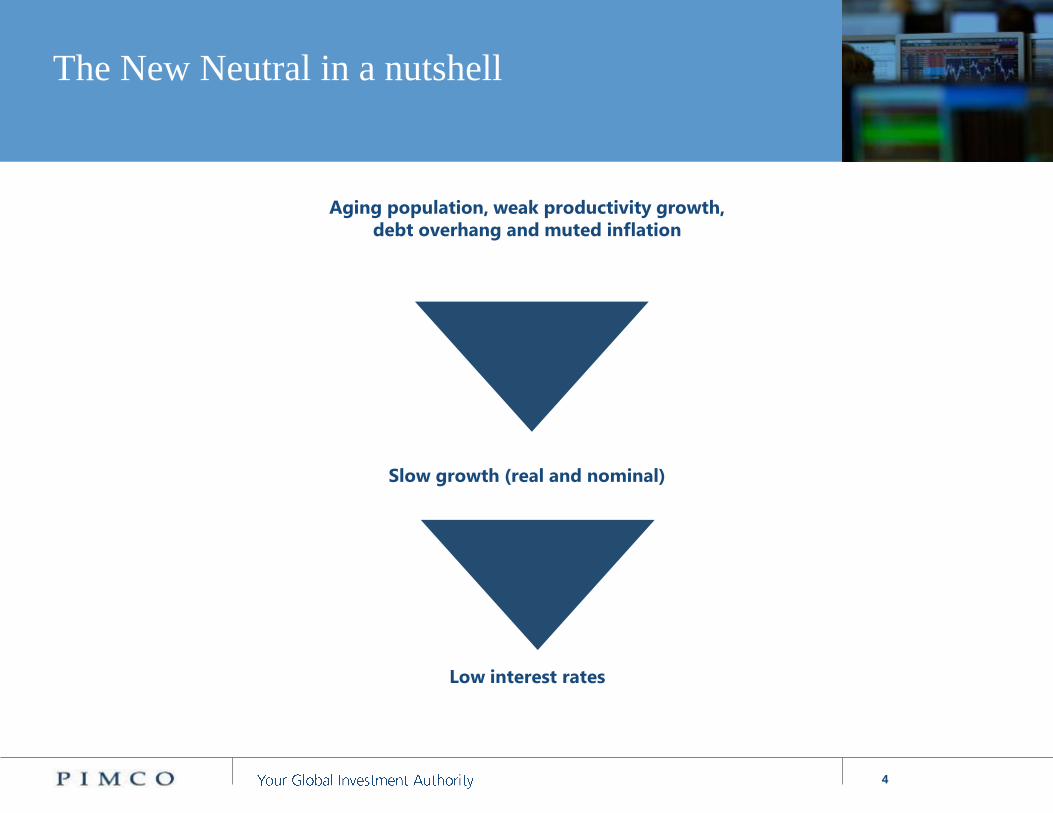

The New Neutral in a nutshell

Aging population, weak productivity growth,

debt overhang and muted inflation

Slow growth (real and nominal)

Low interest rates

5

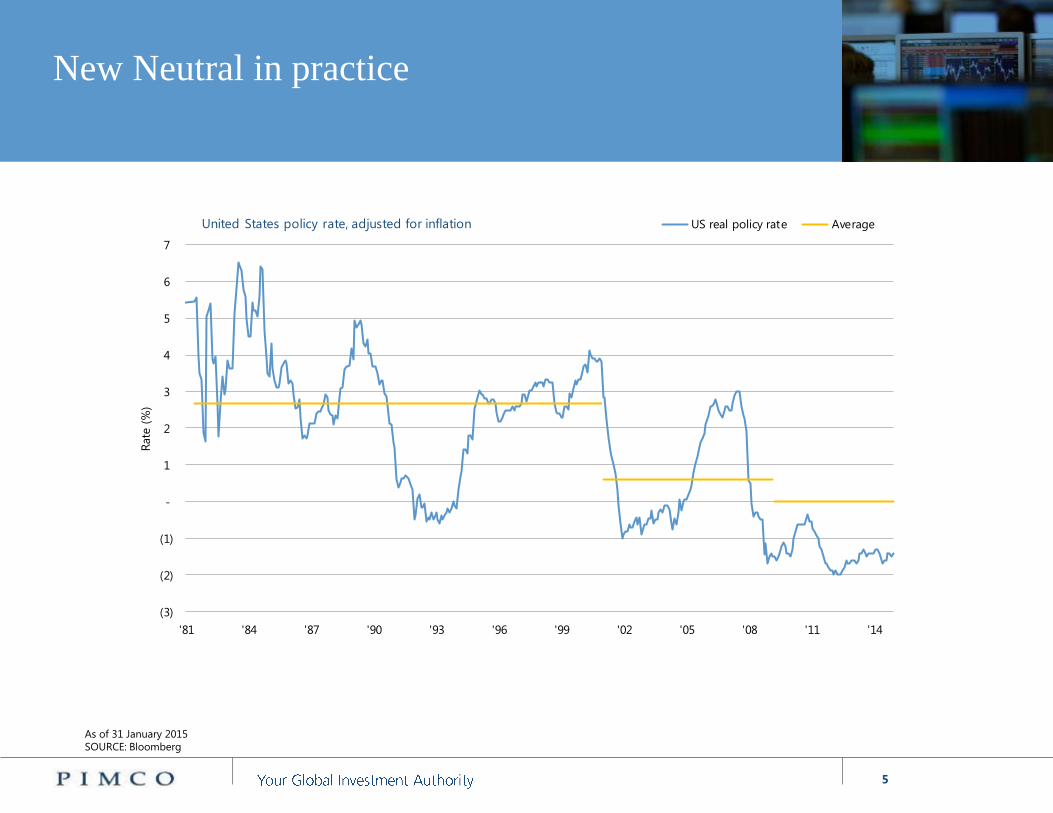

New Neutral in practice

As of 31 January 2015

SOURCE: Bloomberg

2cs_euro_outlook_02

(3)

(2)

(1)

-

1

2

3

4

5

6

7

'81 '84 '87 '90 '93 '96 '99 '02 '05 '08 '11 '14

Rate

(%

)

United States policy rate, adjusted for inflation US real policy rate Average

6

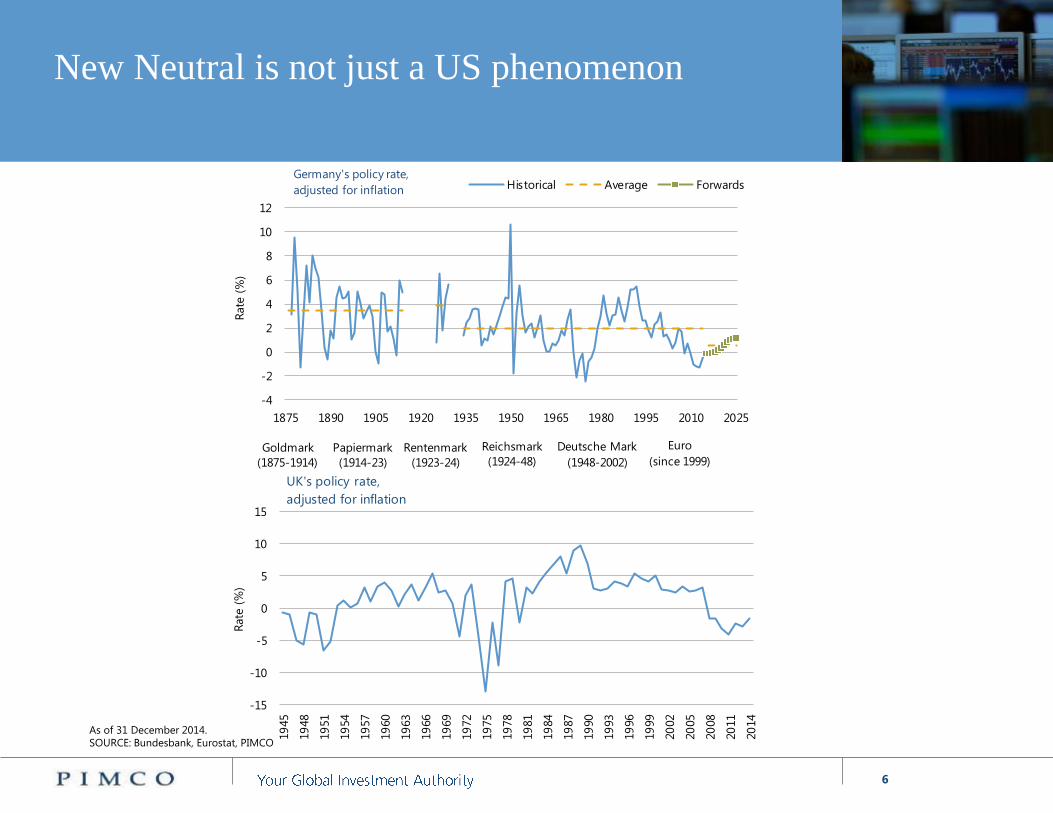

As of 31 December 2014.

SOURCE: Bundesbank, Eurostat, PIMCO

New Neutral is not just a US phenomenon

-15

-10

-5

0

5

10

15

19

45

19

48

19

51

19

54

19

57

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

Rate

(%

)

UK's policy rate,

adjusted for inflation

-4

-2

0

2

4

6

8

10

12

1875 1890 1905 1920 1935 1950 1965 1980 1995 2010 2025

Rate

(%

)

Germany's policy rate,

adjusted for inflation Historical Average Forwards

Goldmark

(1875-1914)

Papiermark

(1914-23)

Rentenmark

(1923-24)

Reichsmark

(1924-48)

Deutsche Mark

(1948-2002)

Euro

(since 1999)

7

PIMCO’s cyclical outlook: increased divergence

ahead

* PIMCO Forecast as of 31 December 2014

BRIM is Brazil, Russia, India, Mexico. Refer to appendix for further outlook information.

Real GDP and inflation projections represent PIMCO’s forecasts for the four quarters ending Q4 2015

4cs_intl_outlook_01

U.S.

3%

GDP

1%

Inflation

BRIM

2%

GDP

5.75%

Inflation

U.K.

2.75%

GDP

1.25%

Inflation

Eurozone

1%

GDP

0.75%

Inflation

China

6.5%

GDP

2%

Inflation

Japan

1.5%

GDP

1%

Inflation

8

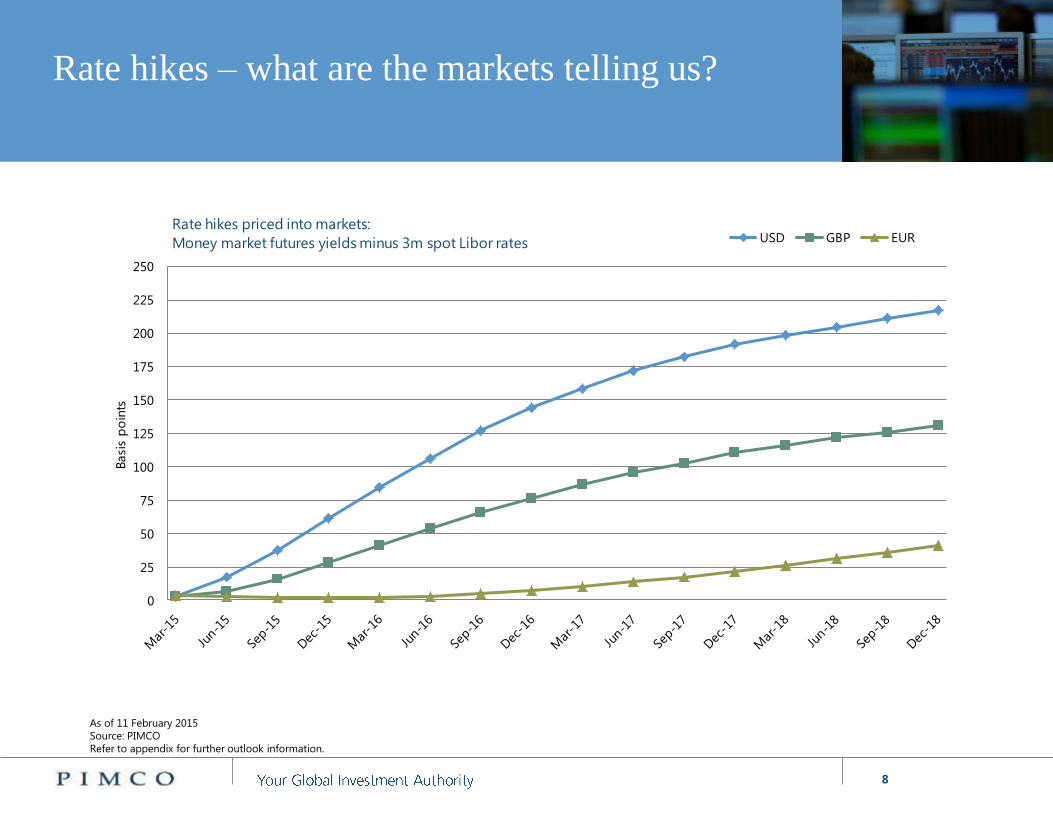

Rate hikes – what are the markets telling us?

As of 11 February 2015

Source: PIMCO

Refer to appendix for further outlook information.

0

25

50

75

100

125

150

175

200

225

250

Basi

s p

oin

ts

Rate hikes priced into markets:

Money market futures yields minus 3m spot Libor rates USD GBP EUR

9

Low interest rates plague the insurance industry

Source: Spence Johnson “IAM European Insurance Asset Management 2013”. For illustrative purposes only

10

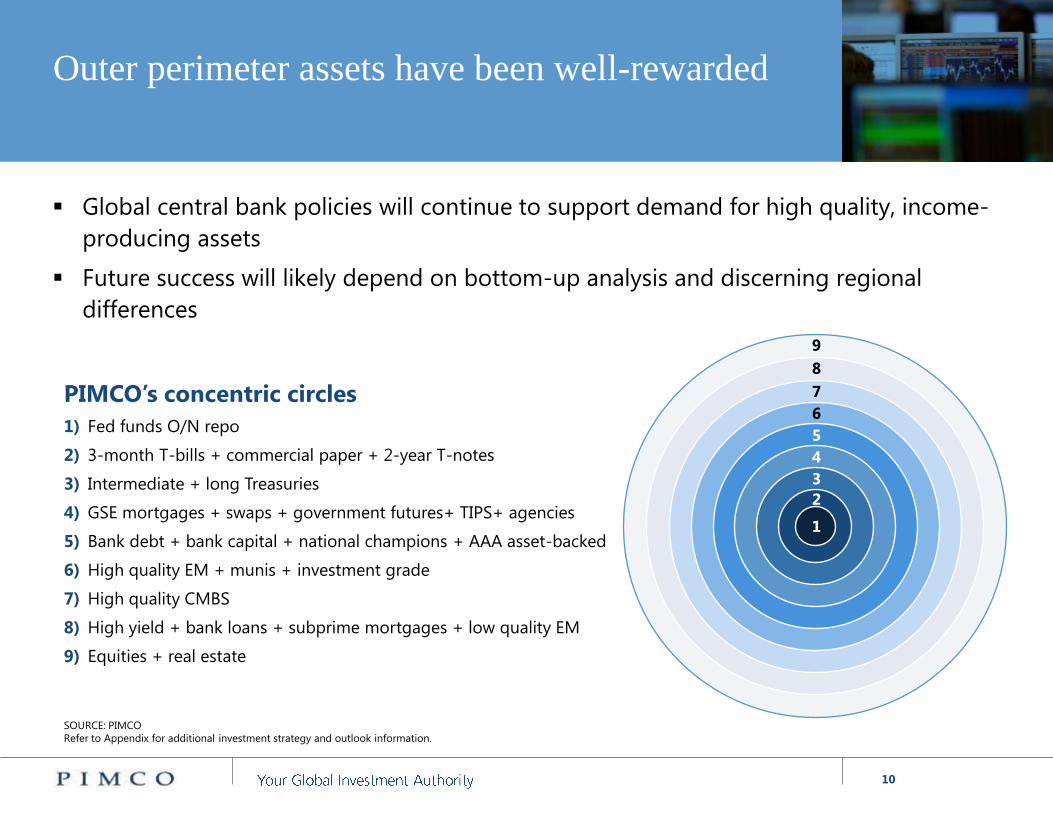

Outer perimeter assets have been well-rewarded

Global central bank policies will continue to support demand for high quality, income-

producing assets

Future success will likely depend on bottom-up analysis and discerning regional

differences

9

8

7

6

5

4

3

2

1

PIMCO’s concentric circles

1) Fed funds O/N repo

2) 3-month T-bills + commercial paper + 2-year T-notes

3) Intermediate + long Treasuries

4) GSE mortgages + swaps + government futures+ TIPS+ agencies

5) Bank debt + bank capital + national champions + AAA asset-backed

6) High quality EM + munis + investment grade

7) High quality CMBS

8) High yield + bank loans + subprime mortgages + low quality EM

9) Equities + real estate

SOURCE: PIMCO

Refer to Appendix for additional investment strategy and outlook information.

11

Duration risk: Markets already pricing in the New

Neutral

mk_4cs_income_review_02

As of 31 December 2014

SOURCE: Bloomberg

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012 2013 2014

Rate

(%

)

U.S. German Japan Australia Canada

Global developed markets 5yr. 5yr. interest rate forwards

12

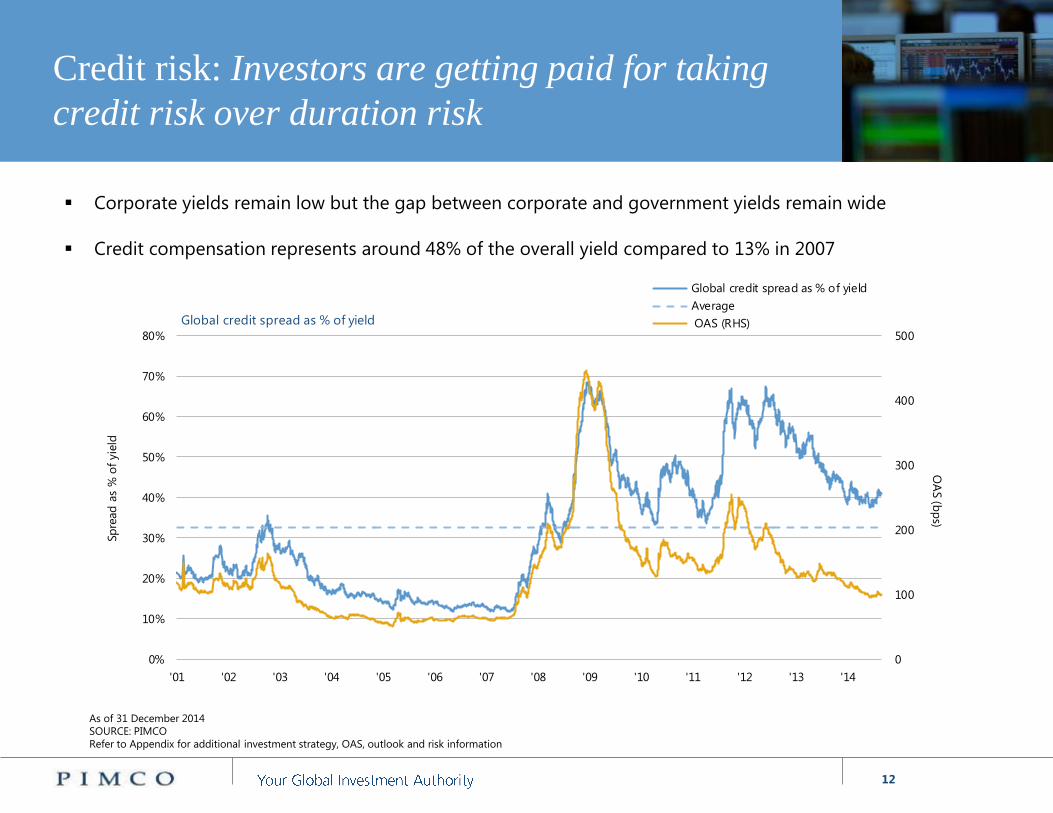

Credit risk: Investors are getting paid for taking

credit risk over duration risk

Corporate yields remain low but the gap between corporate and government yields remain wide

Credit compensation represents around 48% of the overall yield compared to 13% in 2007

mk_GIGC_outlook_10

As of 31 December 2014

SOURCE: PIMCO

Refer to Appendix for additional investment strategy, OAS, outlook and risk information

0

100

200

300

400

500

0%

10%

20%

30%

40%

50%

60%

70%

80%

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

OA

S (b

ps)

Sp

read

as

% o

f yie

ld

Global credit spread as % of yield

Global credit spread as % of yield

Average

OAS (RHS)

13

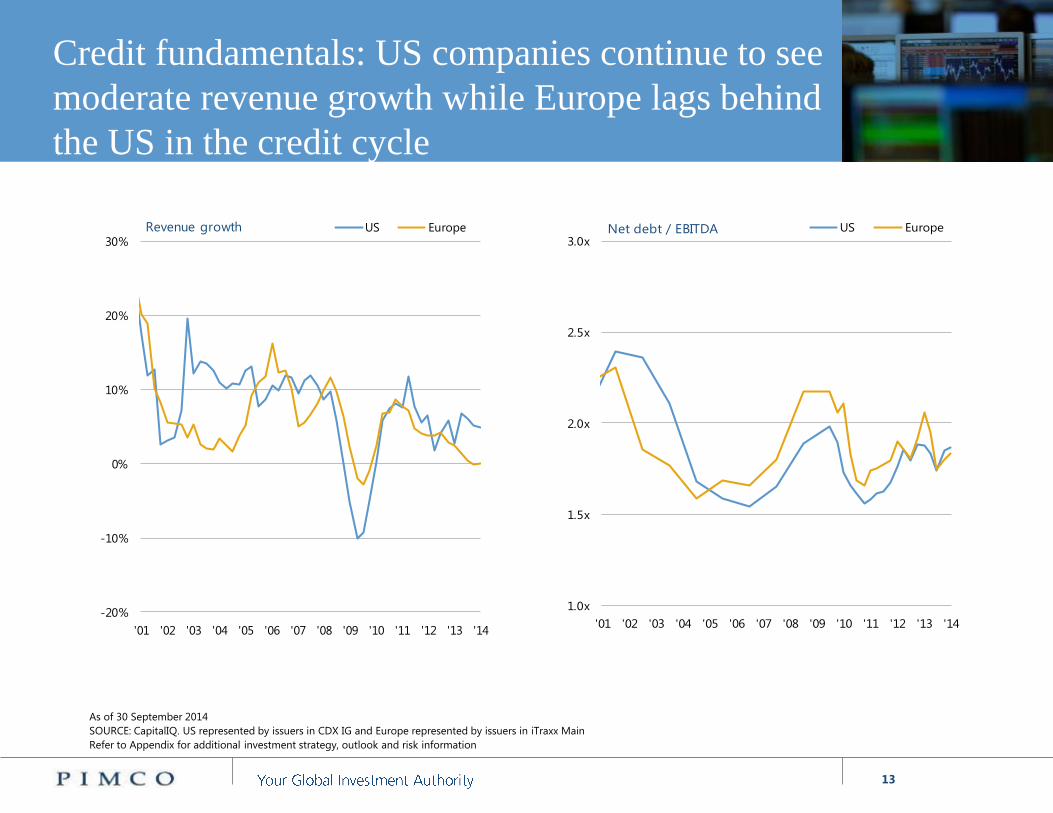

Credit fundamentals: US companies continue to see

moderate revenue growth while Europe lags behind

the US in the credit cycle

As of 30 September 2014

SOURCE: CapitalIQ. US represented by issuers in CDX IG and Europe represented by issuers in iTraxx Main

Refer to Appendix for additional investment strategy, outlook and risk information

mk_GIGC_outlook_04

-20%

-10%

0%

10%

20%

30%

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Revenue growth US Europe

1.0x

1.5x

2.0x

2.5x

3.0x

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Net debt / EBITDA US Europe

14

0

100

200

300

400

500

600

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

OA

S (

bp

s)

Barclays Long U.S. Corporate OAS Sterling Non-Gilts 10+

Barclays Long U.S. Corporate Average OAS Sterling Non-Gilts 10+ Average OAS

Long-dated spreads have become more attractive

2cs_euro_outlook_03

As of January 2015. SOURCE: PIMCO

Refer to Appendix for further outlook, OAS, investment strategy and isk information.

15

PIMCO believes non-agency MBS offer attractive

risk/reward profiles across a variety of housing

scenarios

As of 5 January 2015

SOURCE: PIMCO

* Based on non-agency MBS loss adjusted yields (based on pricing from PIMCO’s survey on the market). Loss adjusted yields represent the yield earned after expected losses on a specific

mortgage bond, across a variety of scenarios. PIMCO’s loss adjusted yield calculation is currently at the same range with an addition of factoring in the default risk level.

** The 2 Yrs. Home Price Appreciation axis illustrates the different home price depreciation and appreciation level (i.e., -10% represents 10 depreciation).

Refer to Appendix for additional forecast and risk information.

0

1

2

3

4

5

6

7

8

9

10

-10% -5% 0% 5% 10% 15%

Lo

ss-A

dju

sted

Yie

ld (

%)

2–year national home price depreciation / appreciation²

Non-Agency MBS provide positive returns across a range of home price scenarios¹

PIMCO’s Base Case:

National house prices increase by

4-8% over the next two years

Upside potential if home

prices exceed market

expectations

Downside resilience in

weaker housing scenarios

4cs_DI_outlook_03

16

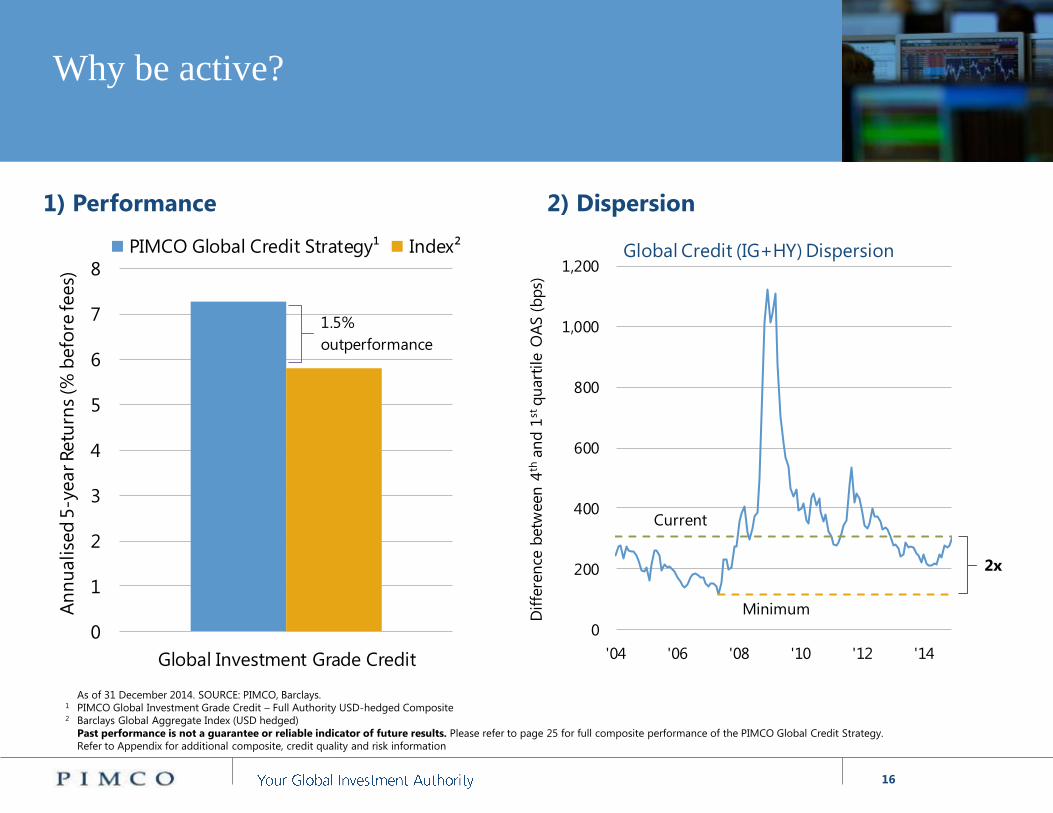

Why be active?

As of 31 December 2014. SOURCE: PIMCO, Barclays.

1 PIMCO Global Investment Grade Credit – Full Authority USD-hedged Composite 2 Barclays Global Aggregate Index (USD hedged)

Past performance is not a guarantee or reliable indicator of future results. Please refer to page 25 for full composite performance of the PIMCO Global Credit Strategy.

Refer to Appendix for additional composite, credit quality and risk information

2) Dispersion

0

200

400

600

800

1,000

1,200

'04 '06 '08 '10 '12 '14

Dif

fere

nce

betw

een

4th

an

d 1

stq

uart

ile O

AS

(b

ps)

Global Credit (IG+HY) Dispersion

Current

Minimum

2x

1) Performance

0

1

2

3

4

5

6

7

8

Global Investment Grade Credit

An

nu

alise

d 5

-year Retu

rns

(% b

efo

re fees)

PIMCO Global Credit Strategy¹ Index²

1.5%

outperformance

17

Five reasons to favour fixed income management

Potential advantages of active management

1. Differences create opportunities

2. Avoidance of structural biases created by

market indices

3. New issuance can offer potential

for price appreciation

4. Independent research and analysis

can inform valuation

5. Playing defense can potentially boost

performance

Investment considerations

1. Investors’ objectives differ meaningfully

2. Indices’ weightings based on stock of debt not

fundamentals

3. Importance of new issuance

4. Purchases and sales are negotiations

5. Fixed income returns are skewed to the left

Refer to Appendix for additional investment strategy and risk information.

18

Appendix

PERFORMANCE AND FEES

Past performance is not a guarantee or a reliable indicator of future results. The “gross of fees” performance figures above are presented before management fees and custodial fees (in

the case of both separate accounts and mutual funds), but do reflect commissions, other expenses and reinvestment of earnings. The “net of fees" performance figures reflect the deduction of

actual investment advisory fees but do not reflect the deduction of custodial fees.

ALPHA

Alpha represents a portfolio's risk-adjusted performance (the difference between a portfolio's actual returns and the expected performance, given the portfolio's level of risk as measured by

beta). It is possible that during any timeframe, the alpha of a portfolio can be positive while the actual total return performance of the portfolio is negative.

CHARTS

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results.

CREDIT QUALITY

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to

indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

CORRELATION

The correlation of various indices or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially in the future or

over different time periods that can result in greater volatility.

CURRENCY

Currency rates in non-U.S. countries may fluctuate significantly over short periods of time and may reduce the returns of a portfolio.

DEFAULT RATE

The Investment Grade default percentages are calculated using cost of the defaulted security over the market values of PIMCO GIS Global Investment Credit Fund on the day prior to the default

date. For the purposes of this analysis, a security is considered defaulted if it was held in the Portfolio on the securities reported default date. The High Yield defaults are measured by the sum

of the cost value of defaulted issues divided by the respective market value of the representative account in the month in which the default occurred.

DIVERSIFICATION

Diversification does not ensure against losses.

GIGC_appendix_01_euro

19

Appendix

Unless otherwise stated in the prospectus or in the relevant key investor information document, the Fund referenced in this material is not managed against a particular benchmark or index,

and any reference to a particular benchmark or index in this material is made solely for risk or performance comparison purposes. This material may contain additional information, not explicit

in the prospectus, on how the Fund or strategy is currently managed. Such information is current as at the date of the presentation and may be subject to change without notice.

In accordance with the UCITS regulations and subject to any investment restrictions outlined in the Fund’s prospectus, the Fund may invest over 35% of net assets in different transferable

securities and money market instruments issued or guaranteed by any of the following: OECD Governments (provided the relevant issues are investment grade), Government of Singapore,

European Investment Bank, European Bank for Reconstruction and Development, International Finance Corporation, International Monetary Fund, Euratom, The Asian Development Bank,

European Central Bank, Council of Europe, Eurofima, African Development Bank, International Bank for Reconstruction and Development (The World Bank), The Inter American Development

Bank, European Union, Federal National Mortgage Association (Fannie Mae), Federal Home Loan Mortgage Corporation (Freddie Mac), Government National Mortgage Association (Ginnie

Mae), Student Loan Marketing Association (Sallie Mae), Federal Home Loan Bank, Federal Farm Credit Bank, Tennessee Valley Authority, Straight-A Funding LLC.

HYPOTHETICAL EXAMPLE

No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Hypothetical or simulated performance

results have several inherent limitations. Unlike an actual performance record, simulated results do not represent actual performance and are generally prepared with the benefit of hindsight.

There are frequently sharp differences between simulated performance results and the actual results subsequently achieved by any particular account, product, or strategy. In addition, since

trades have not actually been executed, simulated results cannot account for the impact of certain market risks such as lack of liquidity. There are numerous other factors related to the

markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect

actual results.

INVESTMENT STRATEGIES

There is no guarantee that these investment strategies will work under all market conditions and each investor should evaluate their ability to invest for a long-term especially during periods of

downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown.

ISSUER

The issuers referenced are examples of issuers PIMCO considers to be well known and that may fall into the stated sectors. References to specific issuers are not intended and should not be

interpreted as recommendations to purchase, sell or hold securities of those issuers. PIMCO products and strategies may or may not include the securities of the issuers referenced and, if such

securities are included, no representation is being made that such securities will continue to be included.

OPTION ADJUSTED SPREAD (OAS)

The Option Adjusted Spread (OAS) measures the spread over a variety of possible interest rate paths. A security's OAS is the average return an investor will earn over Treasury returns, taking all

possible future interest rate scenarios into account.

OPINIONS

This material contains the current opinions of the manager and such opinions are subject to change without notice.

OUTLOOK AND STRATEGY

Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market

conditions, and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market. Outlook and strategies are subject to change

without notice.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will

work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market.

Outlook and strategies are subject to change without notice.

PORTFOLIO STRUCTURE

Portfolio structure is subject to change without notice and may not be representative of current or future allocations.

GIGC_appendix_01_euro

20

Appendix

REPRESENTATIVE ACCOUNT

These accounts were chosen because they represent the accounts with the largest market value in their respective composites. No guarantee is being made that the structure or actual account

holdings of any account will be the same or that similar returns will be achieved. PIMCO may or may not own the securities referenced and, if such securities are owned, no representation is

being made that such securities will continue to be held.

RETURN TARGET

The return objectives presented are not a prediction or a projection of return. The portfolio manager expects to run these portfolios such that the risk factor exposures scale in accordance with

the factor multipliers in in the information shown. The return objectives scale differently from the factor multipliers due to other factors such as the timing of cash flows and differences in

guideline constraints, including leverage.

RISK

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by

changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates

rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price

volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to

currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Mortgage and asset-backed securities may be sensitive to changes in interest rates,

subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or

private guarantee there is no assurance that private guarantors will meet their obligations. High-yield, lower-rated, securities involve greater risk than higher-rated securities; portfolios that

invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Equities may decline in value due to both real and perceived general market, economic,

and industry conditions. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most

advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

SECURITIES REFERENCED

The table above is provided for illustrative purposes only and is not intended to be a recommendation to purchase or sell such securities. PIMCO may or may not own the securities referenced

and, if such securities are owned, no representation is being made that such securities will continue to be held.

TOTAL CARRY

Total Carry refers to the assumed total return a portfolio would potentially achieve over a 3 month period provided that par rates and option adjusted spread (OAS) of each security held in the

portfolio and currency exchange rates remain unchanged. This hypothetical example also assumes no defaults are held in the account for the time period calculated. PIMCO makes no

representation that any account will achieve similar results and the statistical information provided as total carry in no way reflects the actual returns of any current PIMCO portfolio.

GIGC_appendix_01_euro

21

Appendix

INDEX DESCRIPTION

The Barclays Global Aggregate Credit Index is an unmanaged market index representative of the global credit taxable fixed income universe.

The Barclays Global Aggregate Credit (Ex-Gov't Ex-Sec) Index is an unmanaged Index that provides a broad-based measure of the global investment-grade fixed income markets. The three

major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. This index excludes Government and Securitized Securities. The

index also includes Eurodollar and Euro-Yen corporate bonds, Canadian securities, and USD investment grade 144A securities. It is not possible to invest directly in this index.

The Barclays Credit Index is an unmanaged, market-weighted index generally representative of investment grade corporations and non-corporate entities. Prior to November 1, 2008, this index

was published by Lehman Brothers.

Barclays Credit Investment Grade Index is an unmanaged index comprised of publicly issued U.S. corporate and specified non-U.S. debentures and secured notes that meet the specified

maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. Prior to November 1, 2008, this index was published by Lehman Brothers.

The Barclays Euro-Aggregate Corporate Index contains fixed-rate, investment-grade Euro-denominated securities from industrial, utility and financial issuers only. Inclusion is based on the

currency of the issue, and not the domicile of the issuer. Securities in the index are also part of the Euro-Aggregate, Pan-European Aggregate and the Global Aggregate Indices. The Euro-

Aggregate Corporate Index was launched on July 1, 1998.

The Barclays U.S. Credit Index is the U.S. Credit component of the U.S. Government/Credit Index. It consists of publicly issued U.S. corporate and specific foreign debentures and secured notes

that meet the specified maturity, liquidity, and quality requirements. Prior to November 1, 2008, this index was published by Lehman Brothers.

The BofA Merrill Lynch EMU Corporate Index measures the performance of the EMU investment-grade euro-denominated corporate bond market.

It is not possible to invest in an unmanaged index.

This presentation contains the current opinions of the manager and such opinions are subject to change without notice. This presentation has been distributed for informational purposes only

and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from

sources believed to be reliable, but not guaranteed. No part of this presentation may be reproduced in any form, or referred to in any other publication, without express written permission.

PIMCO Europe Ltd (Company No. 2604517), PIMCO Europe, Ltd Amsterdam Branch (Company No. 24319743), and PIMCO Europe Ltd – Italy (Company No. 07533910969) are authorised and

regulated by the Financial Conduct Authority (25 The North Colonnade, Canary Wharf, London E14 5HS) in the UK. The Amsterdam and Italy Branches are additionally regulated by the AFM

and CONSOB in accordance with Article 27 of the Italian Consolidated Financial Act, respectively. PIMCO Europe Ltd services and products are available only to professional clients as defined

in the Financial Conduct Authority’s Handbook and are not available to individual investors, who should not rely on this communication. | PIMCO Deutschland GmbH (Company No. 192083,

Seidlstr. 24-24a, 80335 Munich, Germany) is authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in

Germany in accordance with Section 32 of the German Banking Act (KWG). The services and products provided by PIMCO Deutschland GmbH are available only to professional clients as

defined in Section 31a para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication.

GIGC_appendix_01_euro

22

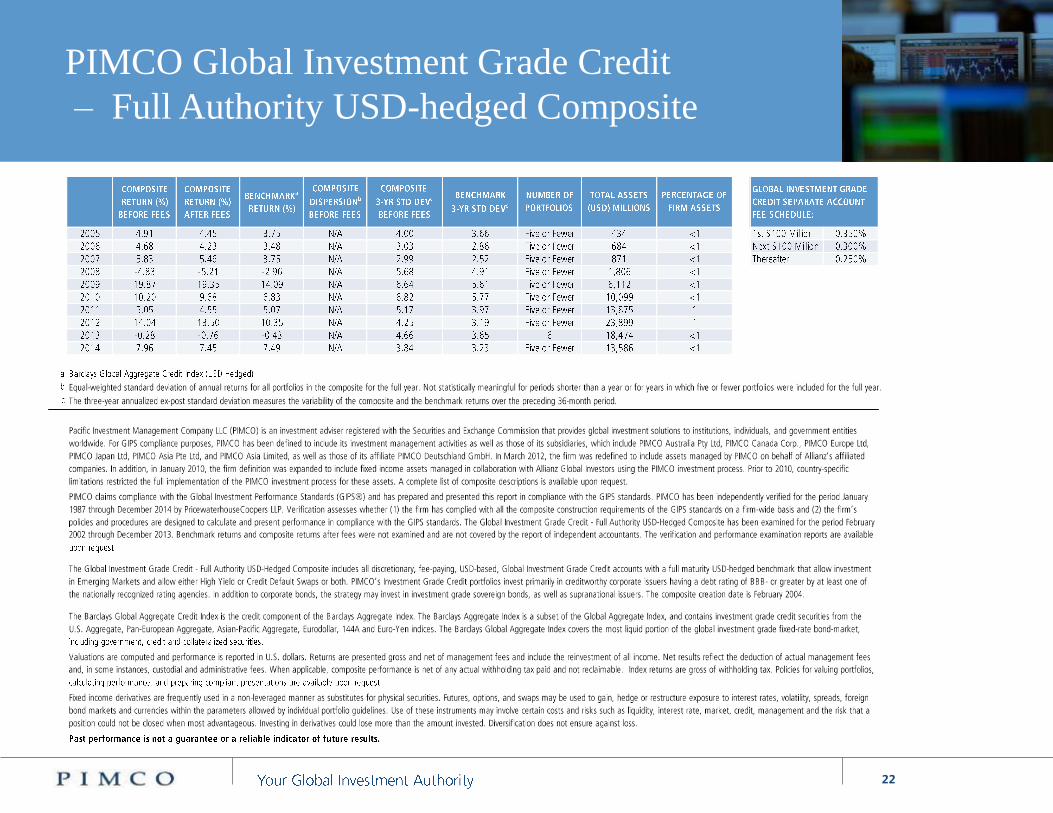

PIMCO Global Investment Grade Credit

– Full Authority USD-hedged Composite

GIPS_1051