Things Fall Apart BY, PARKER KIMES, GRIFFIN BAYLE, AUGUSTINE STANLEY, WILLY R., DEVANTE KOS.

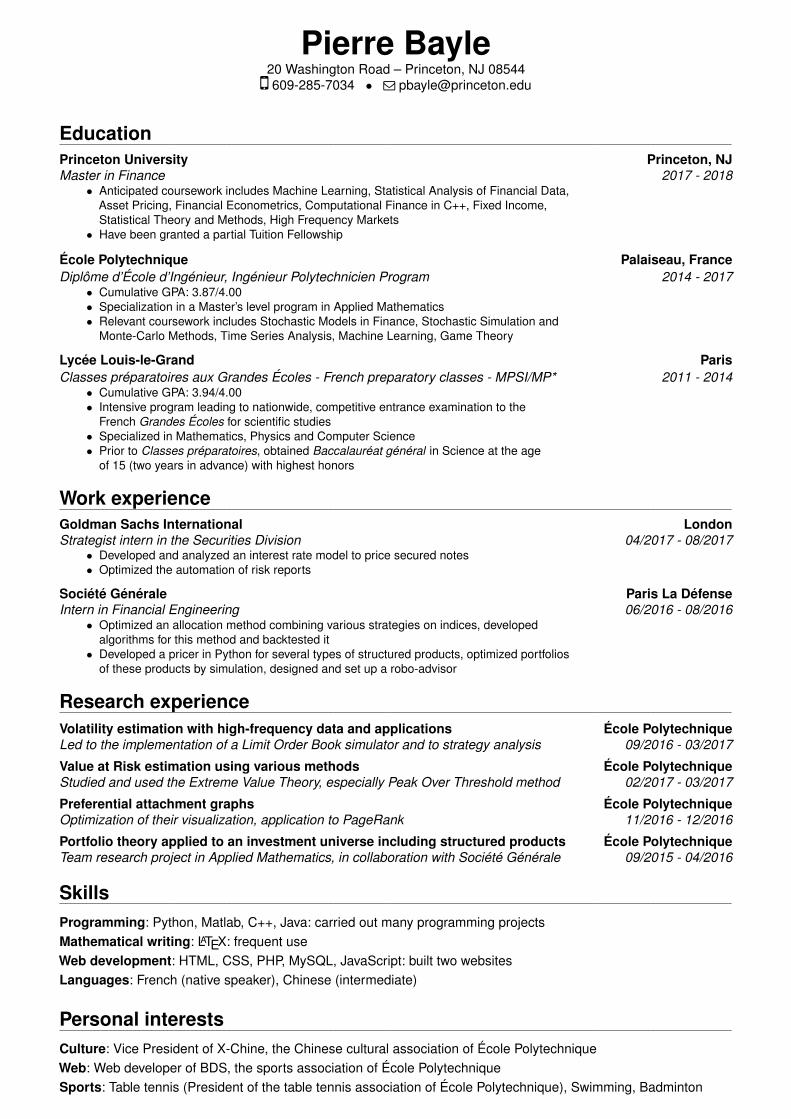

Pierre Bayle20 Washington Road – Princeton, NJ 08544Æ 609-285-7034 • Q [email protected]

EducationPrinceton University Princeton, NJMaster in Finance 2017 - 2018

• Anticipated coursework includes Machine Learning, Statistical Analysis of Financial Data,Asset Pricing, Financial Econometrics, Computational Finance in C++, Fixed Income,Statistical Theory and Methods, High Frequency Markets

• Have been granted a partial Tuition Fellowship

École Polytechnique Palaiseau, FranceDiplôme d’École d’Ingénieur, Ingénieur Polytechnicien Program 2014 - 2017

• Cumulative GPA: 3.87/4.00• Specialization in a Master’s level program in Applied Mathematics• Relevant coursework includes Stochastic Models in Finance, Stochastic Simulation and

Monte-Carlo Methods, Time Series Analysis, Machine Learning, Game Theory

Lycée Louis-le-Grand ParisClasses préparatoires aux Grandes Écoles - French preparatory classes - MPSI/MP* 2011 - 2014

• Cumulative GPA: 3.94/4.00• Intensive program leading to nationwide, competitive entrance examination to the

French Grandes Écoles for scientific studies• Specialized in Mathematics, Physics and Computer Science• Prior to Classes préparatoires, obtained Baccalauréat général in Science at the age

of 15 (two years in advance) with highest honors

Work experienceGoldman Sachs International LondonStrategist intern in the Securities Division 04/2017 - 08/2017

• Developed and analyzed an interest rate model to price secured notes• Optimized the automation of risk reports

Société Générale Paris La DéfenseIntern in Financial Engineering 06/2016 - 08/2016

• Optimized an allocation method combining various strategies on indices, developedalgorithms for this method and backtested it

• Developed a pricer in Python for several types of structured products, optimized portfoliosof these products by simulation, designed and set up a robo-advisor

Research experienceVolatility estimation with high-frequency data and applications École PolytechniqueLed to the implementation of a Limit Order Book simulator and to strategy analysis 09/2016 - 03/2017

Value at Risk estimation using various methods École PolytechniqueStudied and used the Extreme Value Theory, especially Peak Over Threshold method 02/2017 - 03/2017

Preferential attachment graphs École PolytechniqueOptimization of their visualization, application to PageRank 11/2016 - 12/2016

Portfolio theory applied to an investment universe including structured products École PolytechniqueTeam research project in Applied Mathematics, in collaboration with Société Générale 09/2015 - 04/2016

SkillsProgramming: Python, Matlab, C++, Java: carried out many programming projectsMathematical writing: LATEX: frequent useWeb development: HTML, CSS, PHP, MySQL, JavaScript: built two websitesLanguages: French (native speaker), Chinese (intermediate)

Personal interestsCulture: Vice President of X-Chine, the Chinese cultural association of École PolytechniqueWeb: Web developer of BDS, the sports association of École PolytechniqueSports: Table tennis (President of the table tennis association of École Polytechnique), Swimming, Badminton

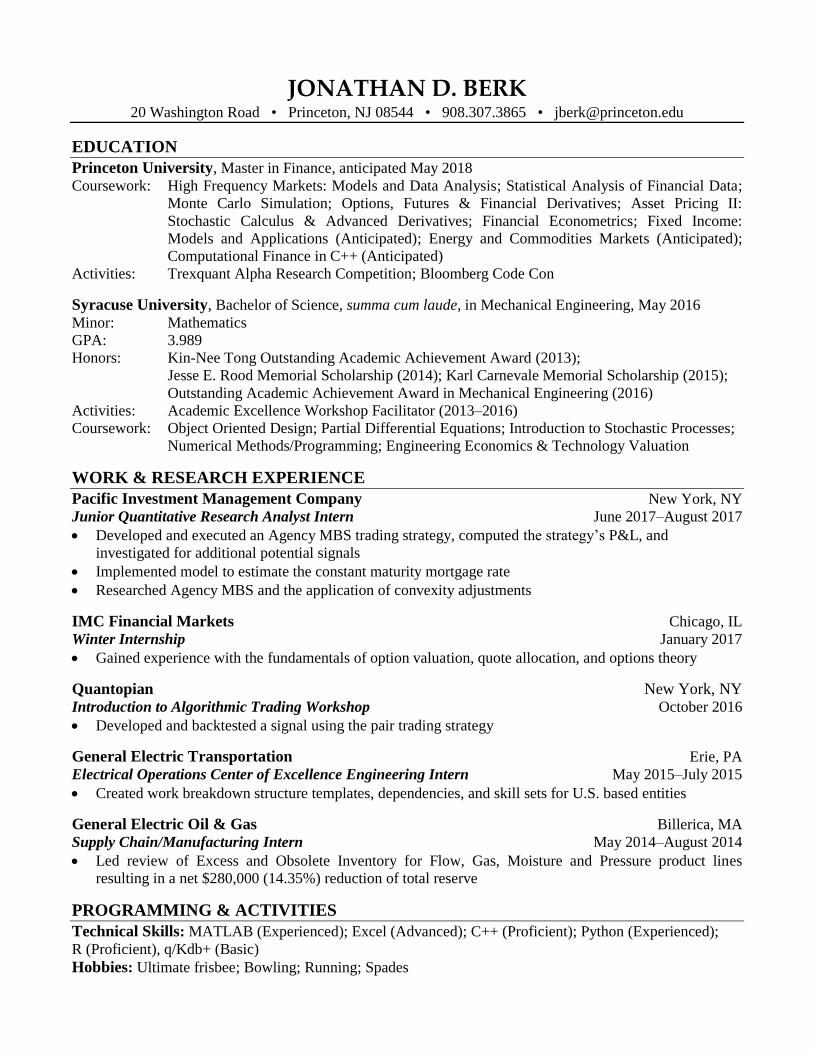

JONATHAN D. BERK 20 Washington Road • Princeton, NJ 08544 • 908.307.3865 • [email protected]

EDUCATION

Princeton University, Master in Finance, anticipated May 2018

Coursework: High Frequency Markets: Models and Data Analysis; Statistical Analysis of Financial Data;

Monte Carlo Simulation; Options, Futures & Financial Derivatives; Asset Pricing II:

Stochastic Calculus & Advanced Derivatives; Financial Econometrics; Fixed Income:

Models and Applications (Anticipated); Energy and Commodities Markets (Anticipated);

Computational Finance in C++ (Anticipated)

Activities: Trexquant Alpha Research Competition; Bloomberg Code Con

Syracuse University, Bachelor of Science, summa cum laude, in Mechanical Engineering, May 2016

Minor: Mathematics

GPA: 3.989

Honors: Kin-Nee Tong Outstanding Academic Achievement Award (2013);

Jesse E. Rood Memorial Scholarship (2014); Karl Carnevale Memorial Scholarship (2015);

Outstanding Academic Achievement Award in Mechanical Engineering (2016)

Activities: Academic Excellence Workshop Facilitator (2013–2016)

Coursework: Object Oriented Design; Partial Differential Equations; Introduction to Stochastic Processes;

Numerical Methods/Programming; Engineering Economics & Technology Valuation

WORK & RESEARCH EXPERIENCE

Pacific Investment Management Company New York, NY Junior Quantitative Research Analyst Intern June 2017–August 2017

• Developed and executed an Agency MBS trading strategy, computed the strategy’s P&L, and

investigated for additional potential signals

• Implemented model to estimate the constant maturity mortgage rate

• Researched Agency MBS and the application of convexity adjustments

IMC Financial Markets Chicago, IL Winter Internship January 2017

• Gained experience with the fundamentals of option valuation, quote allocation, and options theory

Quantopian New York, NY Introduction to Algorithmic Trading Workshop October 2016

• Developed and backtested a signal using the pair trading strategy

General Electric Transportation Erie, PA Electrical Operations Center of Excellence Engineering Intern May 2015–July 2015

• Created work breakdown structure templates, dependencies, and skill sets for U.S. based entities

General Electric Oil & Gas Billerica, MA Supply Chain/Manufacturing Intern May 2014–August 2014

• Led review of Excess and Obsolete Inventory for Flow, Gas, Moisture and Pressure product lines

resulting in a net $280,000 (14.35%) reduction of total reserve

PROGRAMMING & ACTIVITIES

Technical Skills: MATLAB (Experienced); Excel (Advanced); C++ (Proficient); Python (Experienced);

R (Proficient), q/Kdb+ (Basic)

Hobbies: Ultimate frisbee; Bowling; Running; Spades

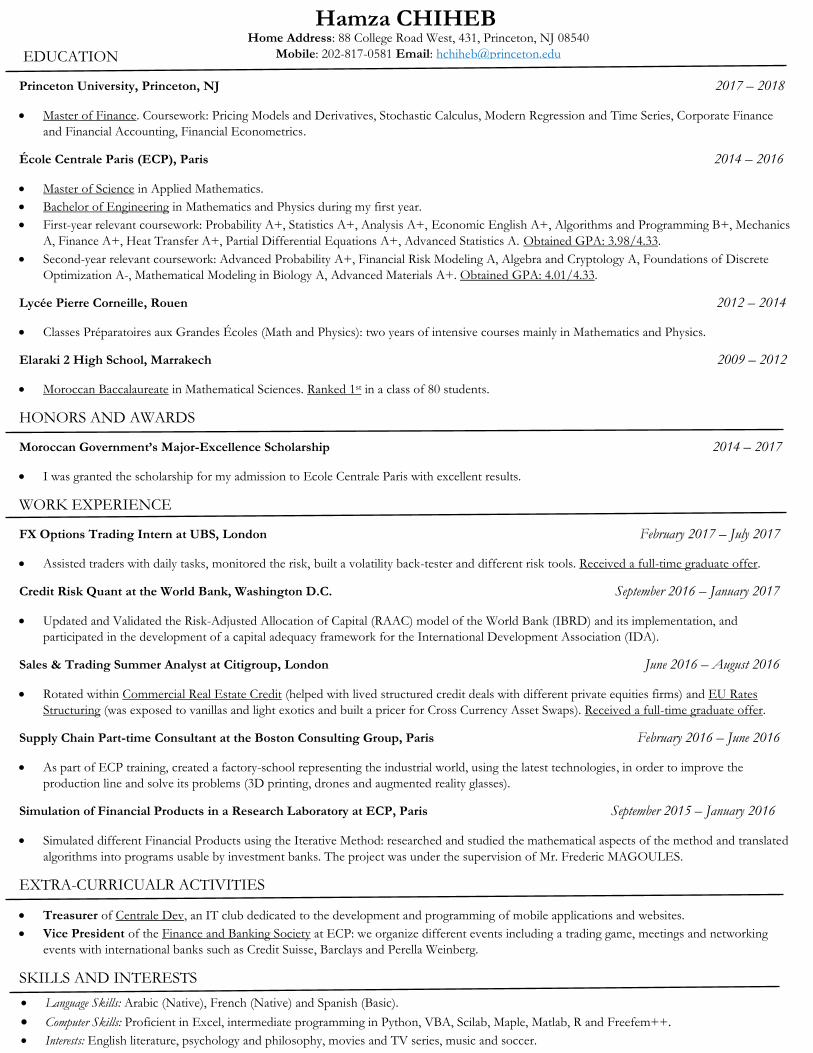

Home Address: 88 College Road West, 431, Princeton, NJ 08540

Mobile: 202-817-0581 Email: [email protected]

Hamza CHIHEB

• Language Skills: Arabic (Native), French (Native) and Spanish (Basic).

• Computer Skills: Proficient in Excel, intermediate programming in Python, VBA, Scilab, Maple, Matlab, R and Freefem++.

• Interests: English literature, psychology and philosophy, movies and TV series, music and soccer.

EDUCATION

Princeton University, Princeton, NJ 2017 – 2018

• Master of Finance. Coursework: Pricing Models and Derivatives, Stochastic Calculus, Modern Regression and Time Series, Corporate Finance

and Financial Accounting, Financial Econometrics.

École Centrale Paris (ECP), Paris 2014 – 2016

• Master of Science in Applied Mathematics.

• Bachelor of Engineering in Mathematics and Physics during my first year.

• First-year relevant coursework: Probability A+, Statistics A+, Analysis A+, Economic English A+, Algorithms and Programming B+, Mechanics

A, Finance A+, Heat Transfer A+, Partial Differential Equations A+, Advanced Statistics A. Obtained GPA: 3.98/4.33.

• Second-year relevant coursework: Advanced Probability A+, Financial Risk Modeling A, Algebra and Cryptology A, Foundations of Discrete

Optimization A-, Mathematical Modeling in Biology A, Advanced Materials A+. Obtained GPA: 4.01/4.33.

Lycée Pierre Corneille, Rouen 2012 – 2014

• Classes Préparatoires aux Grandes Écoles (Math and Physics): two years of intensive courses mainly in Mathematics and Physics.

Elaraki 2 High School, Marrakech 2009 – 2012

• Moroccan Baccalaureate in Mathematical Sciences. Ranked 1st in a class of 80 students.

HONORS AND AWARDS

Moroccan Government’s Major-Excellence Scholarship 2014 – 2017

• I was granted the scholarship for my admission to Ecole Centrale Paris with excellent results.

WORK EXPERIENCE

FX Options Trading Intern at UBS, London February 2017 – July 2017

• Assisted traders with daily tasks, monitored the risk, built a volatility back-tester and different risk tools. Received a full-time graduate offer.

Credit Risk Quant at the World Bank, Washington D.C. September 2016 – January 2017

• Updated and Validated the Risk-Adjusted Allocation of Capital (RAAC) model of the World Bank (IBRD) and its implementation, and

participated in the development of a capital adequacy framework for the International Development Association (IDA).

Sales & Trading Summer Analyst at Citigroup, London June 2016 – August 2016

• Rotated within Commercial Real Estate Credit (helped with lived structured credit deals with different private equities firms) and EU Rates

Structuring (was exposed to vanillas and light exotics and built a pricer for Cross Currency Asset Swaps). Received a full-time graduate offer.

Supply Chain Part-time Consultant at the Boston Consulting Group, Paris February 2016 – June 2016

• As part of ECP training, created a factory-school representing the industrial world, using the latest technologies, in order to improve the

production line and solve its problems (3D printing, drones and augmented reality glasses).

Simulation of Financial Products in a Research Laboratory at ECP, Paris September 2015 – January 2016

• Simulated different Financial Products using the Iterative Method: researched and studied the mathematical aspects of the method and translated

algorithms into programs usable by investment banks. The project was under the supervision of Mr. Frederic MAGOULES.

EXTRA-CURRICUALR ACTIVITIES

• Treasurer of Centrale Dev, an IT club dedicated to the development and programming of mobile applications and websites.

• Vice President of the Finance and Banking Society at ECP: we organize different events including a trading game, meetings and networking

events with international banks such as Credit Suisse, Barclays and Perella Weinberg.

SKILLS AND INTERESTS

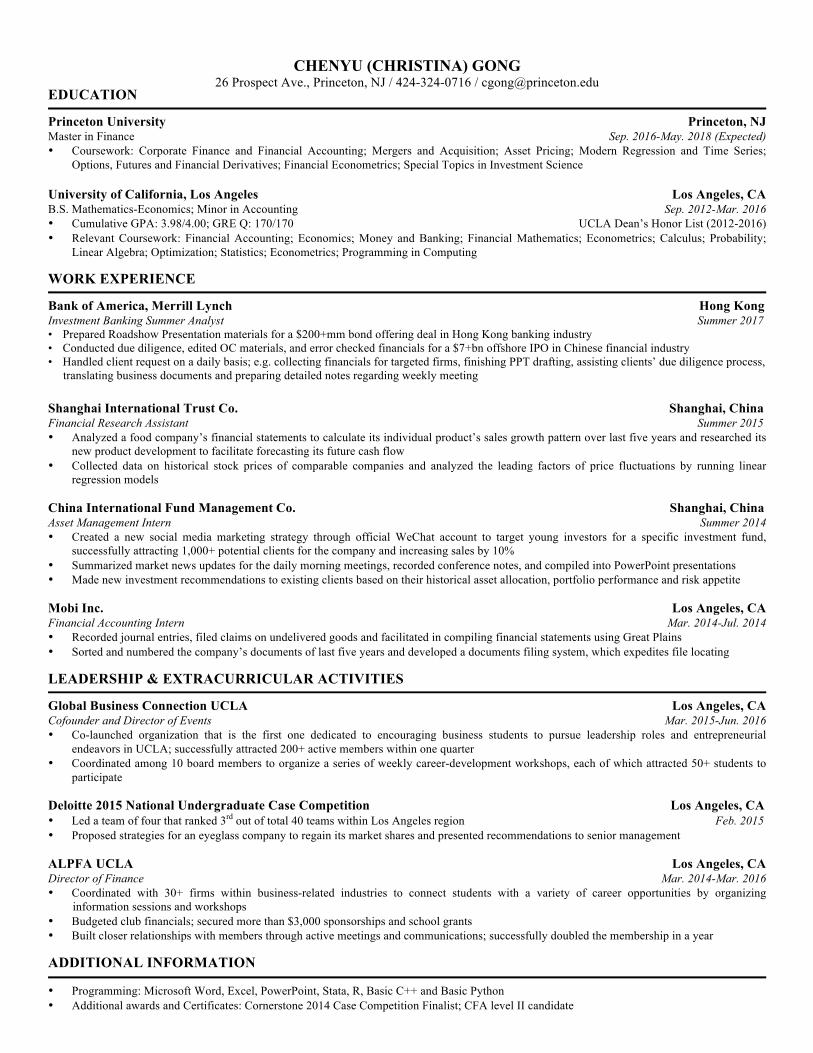

CHENYU (CHRISTINA) GONG

26 Prospect Ave., Princeton, NJ / 424-324-0716 / [email protected] EDUCATION

Princeton University Princeton, NJ Master in Finance Sep. 2016-May. 2018 (Expected) • Coursework: Corporate Finance and Financial Accounting; Mergers and Acquisition; Asset Pricing; Modern Regression and Time Series;

Options, Futures and Financial Derivatives; Financial Econometrics; Special Topics in Investment Science

University of California, Los Angeles Los Angeles, CA B.S. Mathematics-Economics; Minor in Accounting Sep. 2012-Mar. 2016 • Cumulative GPA: 3.98/4.00; GRE Q: 170/170 UCLA Dean’s Honor List (2012-2016) • Relevant Coursework: Financial Accounting; Economics; Money and Banking; Financial Mathematics; Econometrics; Calculus; Probability;

Linear Algebra; Optimization; Statistics; Econometrics; Programming in Computing

WORK EXPERIENCE

Bank of America, Merrill Lynch Hong Kong Investment Banking Summer Analyst Summer 2017 • Prepared Roadshow Presentation materials for a $200+mm bond offering deal in Hong Kong banking industry • Conducted due diligence, edited OC materials, and error checked financials for a $7+bn offshore IPO in Chinese financial industry • Handled client request on a daily basis; e.g. collecting financials for targeted firms, finishing PPT drafting, assisting clients’ due diligence process, translating business documents and preparing detailed notes regarding weekly meeting Shanghai International Trust Co. Shanghai, China Financial Research Assistant Summer 2015 • Analyzed a food company’s financial statements to calculate its individual product’s sales growth pattern over last five years and researched its

new product development to facilitate forecasting its future cash flow • Collected data on historical stock prices of comparable companies and analyzed the leading factors of price fluctuations by running linear

regression models China International Fund Management Co. Shanghai, China Asset Management Intern Summer 2014 • Created a new social media marketing strategy through official WeChat account to target young investors for a specific investment fund,

successfully attracting 1,000+ potential clients for the company and increasing sales by 10% • Summarized market news updates for the daily morning meetings, recorded conference notes, and compiled into PowerPoint presentations • Made new investment recommendations to existing clients based on their historical asset allocation, portfolio performance and risk appetite Mobi Inc. Los Angeles, CA Financial Accounting Intern Mar. 2014-Jul. 2014 • Recorded journal entries, filed claims on undelivered goods and facilitated in compiling financial statements using Great Plains • Sorted and numbered the company’s documents of last five years and developed a documents filing system, which expedites file locating LEADERSHIP & EXTRACURRICULAR ACTIVITIES

Global Business Connection UCLA Los Angeles, CA Cofounder and Director of Events Mar. 2015-Jun. 2016 • Co-launched organization that is the first one dedicated to encouraging business students to pursue leadership roles and entrepreneurial

endeavors in UCLA; successfully attracted 200+ active members within one quarter • Coordinated among 10 board members to organize a series of weekly career-development workshops, each of which attracted 50+ students to

participate

Deloitte 2015 National Undergraduate Case Competition Los Angeles, CA • Led a team of four that ranked 3rd out of total 40 teams within Los Angeles region Feb. 2015 • Proposed strategies for an eyeglass company to regain its market shares and presented recommendations to senior management

ALPFA UCLA Los Angeles, CA Director of Finance Mar. 2014-Mar. 2016 • Coordinated with 30+ firms within business-related industries to connect students with a variety of career opportunities by organizing

information sessions and workshops • Budgeted club financials; secured more than $3,000 sponsorships and school grants • Built closer relationships with members through active meetings and communications; successfully doubled the membership in a year

ADDITIONAL INFORMATION

• Programming: Microsoft Word, Excel, PowerPoint, Stata, R, Basic C++ and Basic Python • Additional awards and Certificates: Cornerstone 2014 Case Competition Finalist; CFA level II candidate

Yingyi (Lily) Gu133 Faculty Rd, Princeton, NJ 08540 • [email protected] • (860) 834-0728

EDUCATION

Princeton University Princeton, NJ• Master of Finance 08/2016 - 05/2018 (Expected)

• Selected Coursework : Asset Pricing, Statistical Analysis of Financial Data, Financial Econometrics,Stochastic Calculus, High Frequency Markets: Models and Data Analysis

Wesleyan University Middletown, CT• B.A. in Computer Science & B.A. in Economics 09/2010 - 05/2014

• Selected Coursework : Microeconomics, Macroeconomics, Corporate Finance, Data Structure and Al-gorithms, Computer Architecture, Data Mining Tutorial

• spent one year at Harvard University as Visiting Undergraduate Student 08/2012 - 05/2013

EXPERIENCE

Volant Trading New York, NYSummer Quantitative Trader 06/2017-08/2017

• Monitor trading positions, flows, and risks across various option products; help price and determinefitness and levels for inter-broker trades.

• Analysis of our trades relative to the market trades; solve trade breaks, notify traders of approachingpin-risk, dividend exposure etc.

• Complete 4-week training in decision making, option theories, and market microstructure in the class-room and mock trading.

• Collect and analyze match-away auction trades behavior, and explore possible trading opportunities;simulate swings and edge collection with different system settings.

Nine Chapters Capital Management LLC Short Hills, NJAnalyst, Research and Development at an equity long/short systematic hedge fund 05/2014-03/2016

• Processed and analyzed EOD and tick data for new trading strategies from major vendors (Bloomberg,NYSE, Thomas Reuters, MSCI etc).

• Involved with development, QA, and deployment of trading applications and backtest tools; gained agood understanding of equity market microstructure and electronic trading system.

• Streamlined daily operations tasks with Java/Shell script tools that enforcing error checking and accesscontrol.

Goldman Sachs & Co. New York, NYSummer Analyst, Cash Management 06/2011-08/2011• Facilitated trading desk risk control, and led the intern group project on treasury risk management.

Summer Analyst, Prime Brokerage 06/2012-08/2012

• Worked closely with clients to provide security lending, reports and metrics; automated futures clearingprocess and prototyped the application.

SKILLS & INTERESTS

• Programming: Java, Python, R, Javascript, MySQL, Linux.

• Languages: native Mandarin Chinese

• Interests: Wesleyan Equestrian Team, Hiking, Bouldering, Volleyball

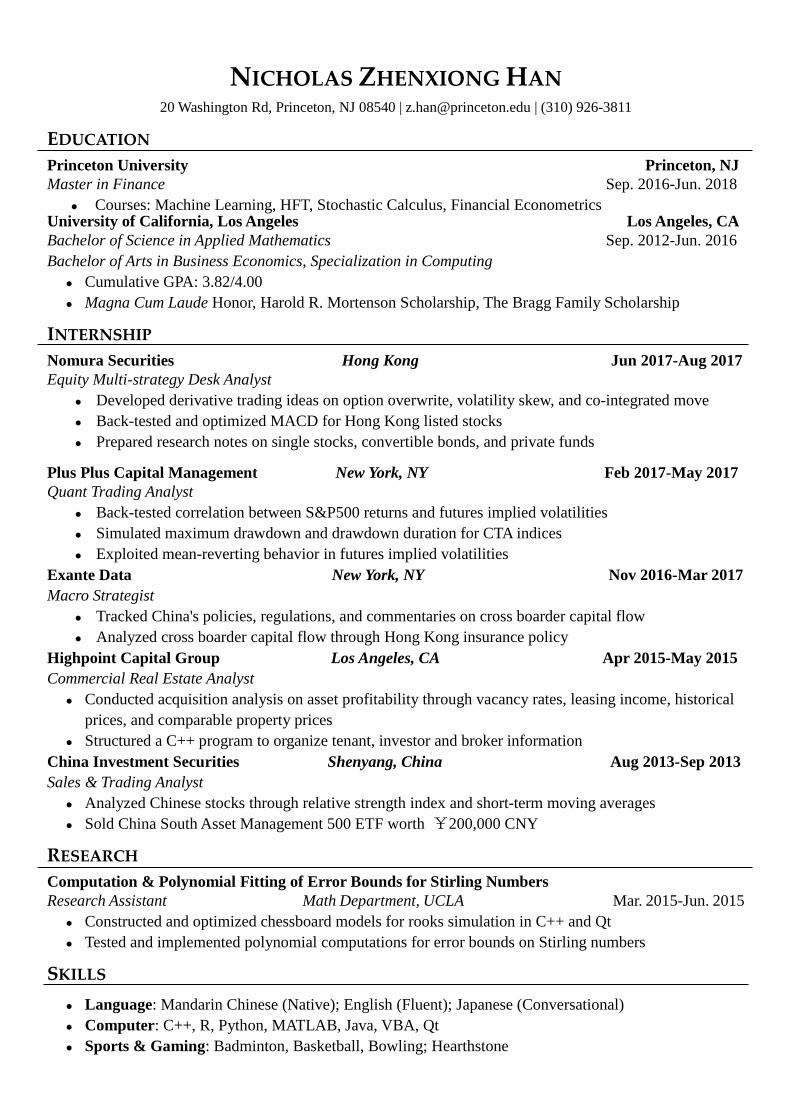

NICHOLAS ZHENXIONG HAN

20 Washington Rd, Princeton, NJ 08540 | [email protected] | (310) 926-3811

EDUCATION

Princeton University Princeton, NJ

Master in Finance Sep. 2016-Jun. 2018

Courses: Machine Learning, HFT, Stochastic Calculus, Financial Econometrics University of California, Los Angeles Los Angeles, CA

Bachelor of Science in Applied Mathematics Sep. 2012-Jun. 2016

Bachelor of Arts in Business Economics, Specialization in Computing

Cumulative GPA: 3.82/4.00

Magna Cum Laude Honor, Harold R. Mortenson Scholarship, The Bragg Family Scholarship

INTERNSHIP

Nomura Securities Hong Kong Jun 2017-Aug 2017

Equity Multi-strategy Desk Analyst

Developed derivative trading ideas on option overwrite, volatility skew, and co-integrated move

Back-tested and optimized MACD for Hong Kong listed stocks

Prepared research notes on single stocks, convertible bonds, and private funds Plus Plus Capital Management New York, NY Feb 2017-May 2017

Quant Trading Analyst

Back-tested correlation between S&P500 returns and futures implied volatilities

Simulated maximum drawdown and drawdown duration for CTA indices

Exploited mean-reverting behavior in futures implied volatilities

Exante Data New York, NY Nov 2016-Mar 2017

Macro Strategist

Tracked China's policies, regulations, and commentaries on cross boarder capital flow

Analyzed cross boarder capital flow through Hong Kong insurance policy

Highpoint Capital Group Los Angeles, CA Apr 2015-May 2015

Commercial Real Estate Analyst

Conducted acquisition analysis on asset profitability through vacancy rates, leasing income, historical

prices, and comparable property prices

Structured a C++ program to organize tenant, investor and broker information

China Investment Securities Shenyang, China Aug 2013-Sep 2013

Sales & Trading Analyst

Analyzed Chinese stocks through relative strength index and short-term moving averages

Sold China South Asset Management 500 ETF worth ¥200,000 CNY

RESEARCH

Computation & Polynomial Fitting of Error Bounds for Stirling Numbers

Research Assistant Math Department, UCLA Mar. 2015-Jun. 2015

Constructed and optimized chessboard models for rooks simulation in C++ and Qt

Tested and implemented polynomial computations for error bounds on Stirling numbers

SKILLS

Language: Mandarin Chinese (Native); English (Fluent); Japanese (Conversational)

Computer: C++, R, Python, MATLAB, Java, VBA, Qt

Sports & Gaming: Badminton, Basketball, Bowling; Hearthstone

�

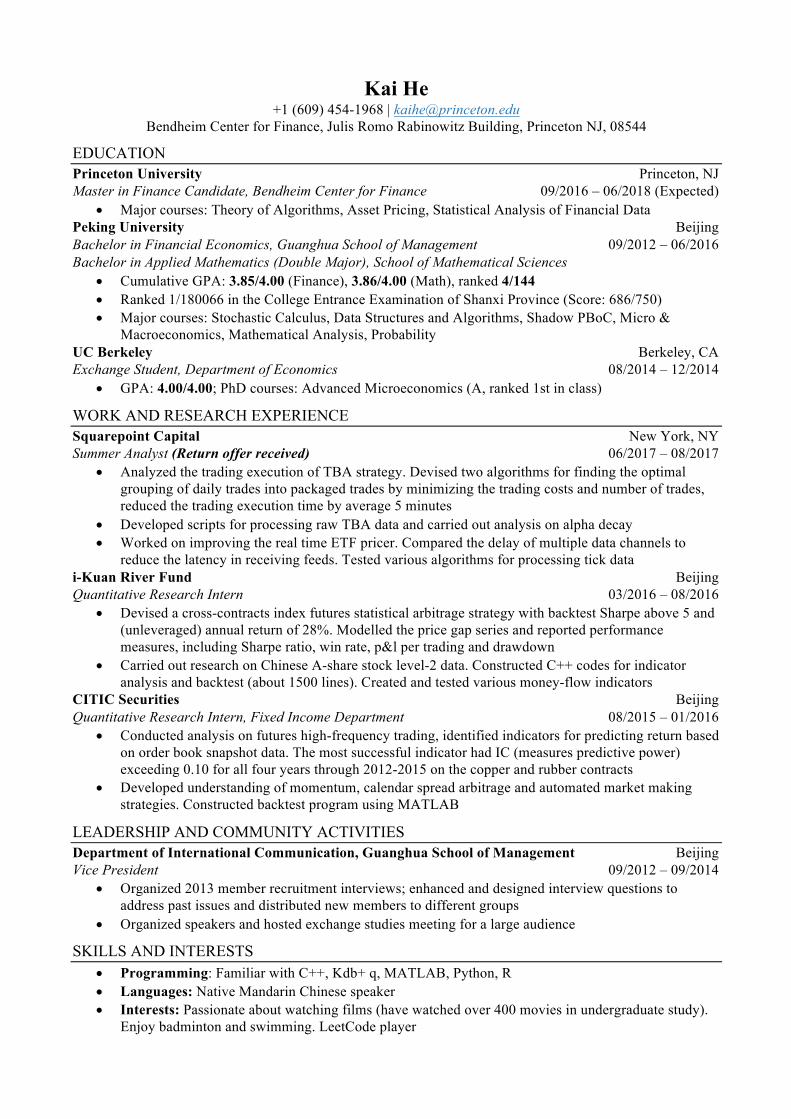

Kai He +1 (609) 454-1968 | [email protected]

Bendheim Center for Finance, Julis Romo Rabinowitz Building, Princeton NJ, 08544

EDUCATION Princeton University Princeton, NJ Master in Finance Candidate, Bendheim Center for Finance 09/2016 – 06/2018 (Expected)

• Major courses: Theory of Algorithms, Asset Pricing, Statistical Analysis of Financial Data Peking University Beijing Bachelor in Financial Economics, Guanghua School of Management 09/2012 – 06/2016 Bachelor in Applied Mathematics (Double Major), School of Mathematical Sciences

• Cumulative GPA: 3.85/4.00 (Finance), 3.86/4.00 (Math), ranked 4/144 • Ranked 1/180066 in the College Entrance Examination of Shanxi Province (Score: 686/750) • Major courses: Stochastic Calculus, Data Structures and Algorithms, Shadow PBoC, Micro &

Macroeconomics, Mathematical Analysis, Probability UC Berkeley Berkeley, CA Exchange Student, Department of Economics 08/2014 – 12/2014

• GPA: 4.00/4.00; PhD courses: Advanced Microeconomics (A, ranked 1st in class)

WORK AND RESEARCH EXPERIENCE Squarepoint Capital New York, NY Summer Analyst (Return offer received) 06/2017 – 08/2017

• Analyzed the trading execution of TBA strategy. Devised two algorithms for finding the optimal grouping of daily trades into packaged trades by minimizing the trading costs and number of trades, reduced the trading execution time by average 5 minutes

• Developed scripts for processing raw TBA data and carried out analysis on alpha decay • Worked on improving the real time ETF pricer. Compared the delay of multiple data channels to

reduce the latency in receiving feeds. Tested various algorithms for processing tick data i-Kuan River Fund Beijing Quantitative Research Intern 03/2016 – 08/2016

• Devised a cross-contracts index futures statistical arbitrage strategy with backtest Sharpe above 5 and (unleveraged) annual return of 28%. Modelled the price gap series and reported performance measures, including Sharpe ratio, win rate, p&l per trading and drawdown

• Carried out research on Chinese A-share stock level-2 data. Constructed C++ codes for indicator analysis and backtest (about 1500 lines). Created and tested various money-flow indicators

CITIC Securities Beijing Quantitative Research Intern, Fixed Income Department 08/2015 – 01/2016

• Conducted analysis on futures high-frequency trading, identified indicators for predicting return based on order book snapshot data. The most successful indicator had IC (measures predictive power) exceeding 0.10 for all four years through 2012-2015 on the copper and rubber contracts

• Developed understanding of momentum, calendar spread arbitrage and automated market making strategies. Constructed backtest program using MATLAB

LEADERSHIP AND COMMUNITY ACTIVITIES Department of International Communication, Guanghua School of Management Beijing Vice President 09/2012 – 09/2014

• Organized 2013 member recruitment interviews; enhanced and designed interview questions to address past issues and distributed new members to different groups

• Organized speakers and hosted exchange studies meeting for a large audience

SKILLS AND INTERESTS • Programming: Familiar with C++, Kdb+ q, MATLAB, Python, R • Languages: Native Mandarin Chinese speaker • Interests: Passionate about watching films (have watched over 400 movies in undergraduate study).

Enjoy badminton and swimming. LeetCode player

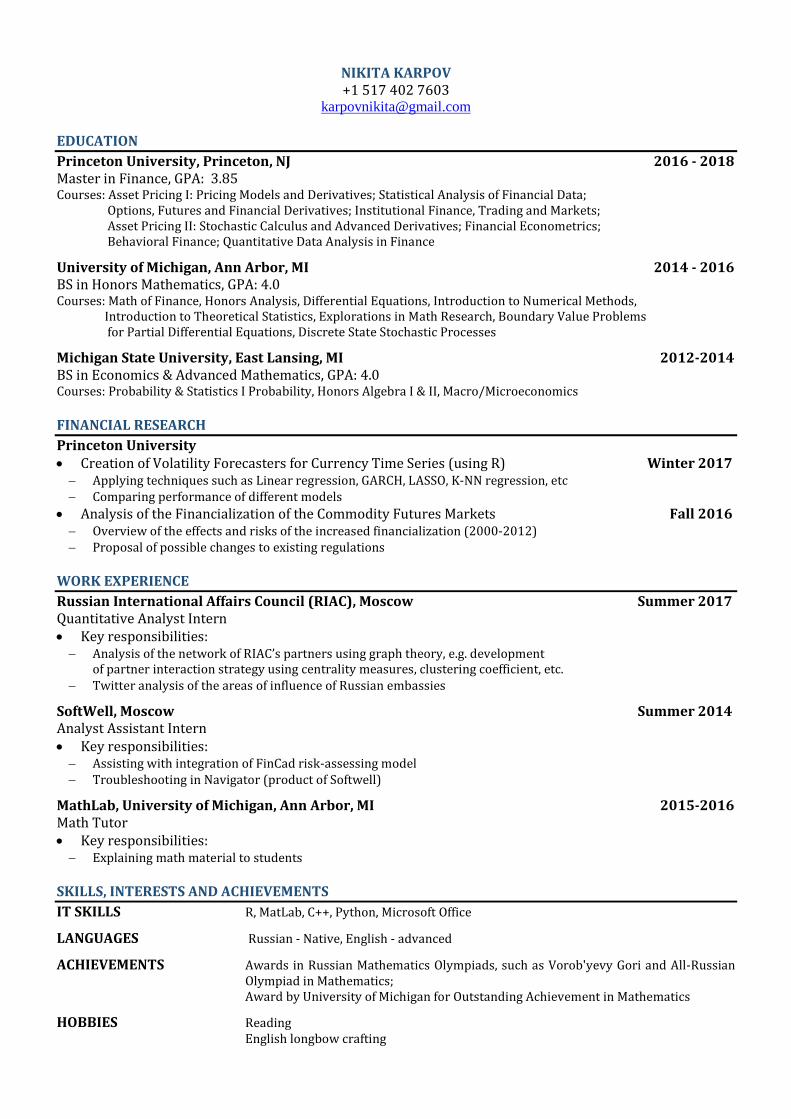

NIKITA KARPOV +1 517 402 7603

EDUCATION Princeton University, Princeton, NJ 2016 - 2018 Master in Finance, GPA: 3.85 Courses: Asset Pricing I: Pricing Models and Derivatives; Statistical Analysis of Financial Data;

Options, Futures and Financial Derivatives; Institutional Finance, Trading and Markets; Asset Pricing II: Stochastic Calculus and Advanced Derivatives; Financial Econometrics; Behavioral Finance; Quantitative Data Analysis in Finance

University of Michigan, Ann Arbor, MI 2014 - 2016 BS in Honors Mathematics, GPA: 4.0 Courses: Math of Finance, Honors Analysis, Differential Equations, Introduction to Numerical Methods,

Introduction to Theoretical Statistics, Explorations in Math Research, Boundary Value Problems for Partial Differential Equations, Discrete State Stochastic Processes

Michigan State University, East Lansing, MI 2012-2014 BS in Economics & Advanced Mathematics, GPA: 4.0 Courses: Probability & Statistics I Probability, Honors Algebra I & II, Macro/Microeconomics FINANCIAL RESEARCH Princeton University • Creation of Volatility Forecasters for Currency Time Series (using R) Winter 2017 − Applying techniques such as Linear regression, GARCH, LASSO, K-NN regression, etc − Comparing performance of different models

• Analysis of the Financialization of the Commodity Futures Markets Fall 2016 − Overview of the effects and risks of the increased financialization (2000-2012) − Proposal of possible changes to existing regulations

WORK EXPERIENCE Russian International Affairs Council (RIAC), Moscow Summer 2017 Quantitative Analyst Intern • Key responsibilities: − Analysis of the network of RIAC’s partners using graph theory, e.g. development

of partner interaction strategy using centrality measures, clustering coefficient, etc. − Twitter analysis of the areas of influence of Russian embassies

SoftWell, Moscow Summer 2014 Analyst Assistant Intern • Key responsibilities: − Assisting with integration of FinCad risk-assessing model − Troubleshooting in Navigator (product of Softwell)

MathLab, University of Michigan, Ann Arbor, MI 2015-2016 Math Tutor • Key responsibilities: − Explaining math material to students

SKILLS, INTERESTS AND ACHIEVEMENTS IT SKILLS R, MatLab, C++, Python, Microsoft Office

LANGUAGES Russian - Native, English - advanced

ACHIEVEMENTS Awards in Russian Mathematics Olympiads, such as Vorob'yevy Gori and All-Russian Olympiad in Mathematics; Award by University of Michigan for Outstanding Achievement in Mathematics

HOBBIES Reading English longbow crafting

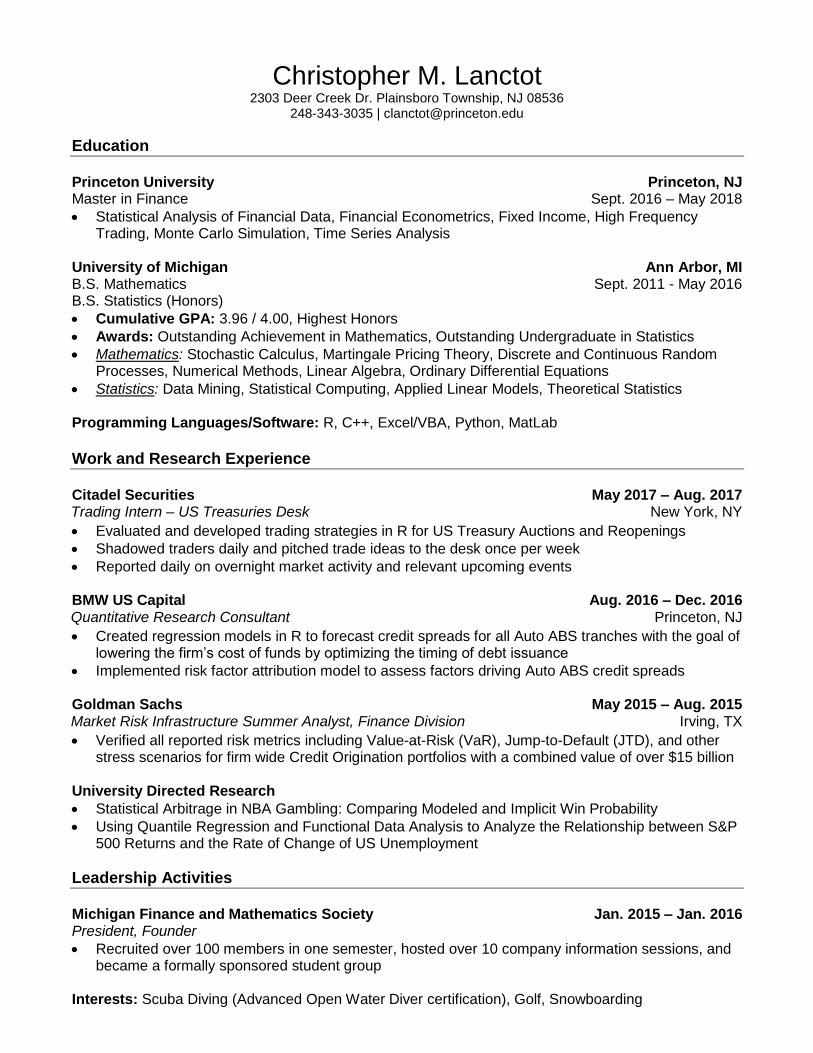

Christopher M. Lanctot 2303 Deer Creek Dr. Plainsboro Township, NJ 08536

248-343-3035 | [email protected]

Education

Princeton University Princeton, NJ Master in Finance Sept. 2016 – May 2018

• Statistical Analysis of Financial Data, Financial Econometrics, Fixed Income, High Frequency Trading, Monte Carlo Simulation, Time Series Analysis

University of Michigan Ann Arbor, MI B.S. Mathematics Sept. 2011 - May 2016 B.S. Statistics (Honors)

• Cumulative GPA: 3.96 / 4.00, Highest Honors

• Awards: Outstanding Achievement in Mathematics, Outstanding Undergraduate in Statistics

• Mathematics: Stochastic Calculus, Martingale Pricing Theory, Discrete and Continuous Random Processes, Numerical Methods, Linear Algebra, Ordinary Differential Equations

• Statistics: Data Mining, Statistical Computing, Applied Linear Models, Theoretical Statistics Programming Languages/Software: R, C++, Excel/VBA, Python, MatLab

Work and Research Experience

Citadel Securities May 2017 – Aug. 2017 Trading Intern – US Treasuries Desk New York, NY

• Evaluated and developed trading strategies in R for US Treasury Auctions and Reopenings

• Shadowed traders daily and pitched trade ideas to the desk once per week

• Reported daily on overnight market activity and relevant upcoming events BMW US Capital Aug. 2016 – Dec. 2016 Quantitative Research Consultant Princeton, NJ

• Created regression models in R to forecast credit spreads for all Auto ABS tranches with the goal of lowering the firm’s cost of funds by optimizing the timing of debt issuance

• Implemented risk factor attribution model to assess factors driving Auto ABS credit spreads

Goldman Sachs May 2015 – Aug. 2015 Market Risk Infrastructure Summer Analyst, Finance Division Irving, TX

• Verified all reported risk metrics including Value-at-Risk (VaR), Jump-to-Default (JTD), and other stress scenarios for firm wide Credit Origination portfolios with a combined value of over $15 billion

University Directed Research

• Statistical Arbitrage in NBA Gambling: Comparing Modeled and Implicit Win Probability

• Using Quantile Regression and Functional Data Analysis to Analyze the Relationship between S&P 500 Returns and the Rate of Change of US Unemployment

Leadership Activities

Michigan Finance and Mathematics Society Jan. 2015 – Jan. 2016 President, Founder

• Recruited over 100 members in one semester, hosted over 10 company information sessions, and became a formally sponsored student group

Interests: Scuba Diving (Advanced Open Water Diver certification), Golf, Snowboarding

Xuefan (Sherry) Li

10 Lawrence Drive, Princeton, NJ | [email protected] | +1 (609)608-5268

EDUCATION

Princeton University Princeton, NJ

Master in Finance Sept. 2016 – May 2018(expected)

• GPA: 3.95/4.00. Coursework: Stochastic Calculus, Financial Econometrics, Introduction to Machine Learning, Fixed

Income Models and Applications, Theory of Algorithms, Asset Pricing

Guanghua School of Management, Peking University (PKU) Beijing

Bachelor of Science in Finance, Double Major in Applied Mathematics Sept. 2012 – July 2016

• Cumulative GPA: 3.76/4.00, graduated with distinction (5%); GRE: 159+170; TOEFL: 109

• 2014 & 2015 Merit Student Scholarship (top 2% of the department); 2013 Founder Scholarship (top 4 out of 800

undergraduates); 2013 PKU Outstanding Undergraduate Leader (top 4% of the university)

University of California, Berkeley Berkeley, CA

Exchange student at the Department of Economics (4.0/4.0) Sept. 2014 – Dec. 2014

PROFESSIONAL EXPERIENCE

J.P. Morgan New York, NY

Summer Analyst, Asset Management, Institutional Strategy and Analytics May 2017 – Aug. 2017

• Conducted strategic asset allocation for institutional clients under certain constraints such as duration and liability match,

nearly optimal results to seek for highest Sharpe ratio or optimal risk based capital using optimization model in Matlab

• Modified Economic Scenario Generator to simulate yield curve paths by Diebold Li model and fixed income return by

multi-factor model, and calculated distributions and risk factors of assets under different economic scenarios in Matlab

• Built automation code for standard strategic asset allocation output and largely improved efficiency

• Tested performance and feasibility of introducing commodities to portfolio using correlation and portfolio analysis

Beijing Renaissance Era Investment Corporation Beijing

Intern, Quantitative Researcher Mar. 2016 – June 2016

• Estimated future dividend impact on index and wrote a Python project to monitor the instant difference between

theoretical and real basis points on index futures, thus providing support for futures arbitrage trading

Conducted a pair-trading strategy on rebar and iron ore futures by ADF test, optimal hedge ratio calculation, and entry

points determination under different variance models using Python

Van Eck Global New York, NY

Intern, ETF Equity Department July 2015 – Sept. 2015

• Initiated an index strategy to capture periodic momentum with 20 years excess annual return of 13.47% and tested it with

Monte Carlo simulation using VBA

• Participated in the quarterly portfolio rebalance process and conducted first-round stock selection by event study

RESEARCH AND PROJECTS

Empirical Performance of CEV Stochastic Volatility Option Pricing Model (Thesis, 97/100): Estimated model parameter

with closed-form expansion and Panel MLE, analyzed the parameter of S&P500 options across the crisis, and compared

theoretical volatility with observed ones to test pricing effectiveness of the model (Matlab)

LEADERSHIP AND ACTIVITIES

Hedge Fund Association of PKU Beijing

Trader for Separate Account Management Project and Seamew Capital July 2014 –June 2016

• Executed trading in 30 accounts ($1.5mil.) for the separate account management project, with +11.2% low-volatility

market neutral IRR using A-share IPO flipping arbitrage and structured fund

• Carried out data analysis regarding strategies on index futures arbitrage for Seamew Capital (a personal fund with $4

million AUM) and reached annual return of 64.7%

SKILLS AND INTERESTS

• Skills: Python, C++, Matlab, R, SAS, Stata, Bloomberg, Wind; CFA Level III candidate

• Interests: Piano (Grade 10), Horse Riding (Novice), Debate (Won the championship of PKU’s debate competition)

Gustavo Mena 3125 NGC, 88 College Road West, Princeton, NJ 08544

(415) 941-1139 | [email protected]

EDUCATION

Princeton University

Master in Finance Princeton, NJ

(Expected) June 2018

• Anticipated Coursework: Corporate Finance, Valuation and Security Analysis, Venture Capital and Private Equity

Investment, Portfolio Management, Behavioral Finance, Financial Econometrics, Asset Pricing

• Finalist in Princeton’s 2017 PUGCC consulting case team competition (recommended M&A for Spotify)

University of San Francisco

BSBA; Accounting Major, Math Minor; GPA: 3.8/4.0 San Francisco, CA

Class of 2014

• Recipient of the HSF/Morgan Stanley Foundation Scholarship, Father George Lucey Business Scholarship

• Division 1 Track & Field/Cross Country athlete; middle-distance track captain and school record holder

• Co-Founder and President of Dons Capital Investment Club

WORK EXPERIENCE

The Glenmede Trust Company, N.A. ($37B AUM) Summer Analyst

Philadelphia, PA

June 2017 – August 2017

• Work directly with the Director of Private Investments to manage the Private Investments portfolio of the Pew

Charitable Trusts, research the private capital markets, and map out investment themes

• Perform valuation analysis on portfolio companies and live deals, as well as support the fundamental and

quantitative equity research teams with computationally and mathematically intensive ad-hoc projects

• Built a Private Equity allocation model to determine the optimal amount to invest in Private Equity across time

Cohen Capital Management, Inc. ($500M AUM)

Equity Research Summer Analyst

Corte Madera, CA

May 2016 – August 2016

• Presented two equity research reports to management with recommendations that each produced a positive

differential to the S&P 500 of ~10% and ~40% over one year (recommended to take no positions in Starbucks and

Hain)

• Created and maintained two valuation models for Hain and Starbucks after performing thorough due diligence

• Conducted research on the consumer packaged goods, retail, and restaurant industries

Deloitte & Touche LLP

Senior Audit Assistant – Investment Management

San Francisco, CA

September 2014 – May 2016

• Analyzed asset managers’ assumptions in absolute and relative valuation models through the due diligence process,

which included discussions with management, reviews of deal documents and research of the capital markets

• Validated the operations, credit processes, and financial reporting processes of a technology-based provider of

personal loans, a venture lender and other alternative asset managers

• Built 10 flux analysis models on Excel to calculate and explain variances across the three primary financial

statements

LEADERSHIP

Latinos in Finance San Francisco, CA

7th Annual Finance Boot Camp Committee Chair April 2015 – August 2016

• Coordinated the finance boot camp at the BlackRock San Francisco office for ~70 high school and college students

• Raised $5,000 from the BlackRock Foundation, Charles Schwab, and New York Life to cover all expenses

OTHER INFORMATION

Languages:

Computer: Certifications:

Interests:

Fluent Spanish speaker

Expert in Microsoft Office and proficient in Python, MATLAB, R, VBA, and C++

CPA (Inactive), passed CFA Level I

Running, reading, riding horses, and community service

PUNEET [email protected], 702 Hibben Magie Road, Princeton, +1 6099335175

EDUCATION

Princeton University 2016-2018Master in FinanceRelevant Coursework: High Frequency Trading, Analysis of Financial Data, Fixed Income, Asset PricingAnticipated Coursework: Computational Finance in C++, Monte Carlo Simulation, Macroeconomics

Indian Institute of Technology Kanpur 2010 - 2015MSc (Int) Mathematics and Scientific Computing GPA: 9.0/10Relevant Coursework: Mathematical Finance, Machine Learning, Data Structures and Algorithms, Prob-ability and Statistics, Time Series, Regression Analysis, Statistical Simulation, Data Mining

WORK EXPERIENCE

Citadel LLC June’17 - Aug’17Equities Market Making - Internship Chicago

· Developed ’Event Study Framework’ for intra-day PnL analysis of strategies across the equities desk

· Extracted M&A rumours, analyst upgrades/downgrades from news sentiment analysis dataset

· Programmed execution prices for illiquid symbols not traded for 15 days in Python and display in GUI

Two Roads Tech. Pvt. Ltd. Dec’15 - Aug’16High Frequency Trading - Full Time Bengaluru, India

· Traded future indices in Singapore Exchange and CME with appropriate MUR, TTC, vol. and drawdown.

· Developed ‘composite indicators’, combining features via conditional variables to predict regressors. Cor-relation increase w.r.t individual indicators by more than 30% for ≥ 15 traded products across exchanges.

Goldman Sachs Jun’15 - Nov’15Equities One Delta Strats - Full Time Bengaluru, India

· Created share buyback model which predicts the number of shares that would be executed in a quarter.

· Drew inferences from one-delta securities execution data for Hedge Funds to predict market sentiments

IDRBT, Reserve Bank of India May’13 - Jul’13Research Associate - Internship Hyderabad, India

· Analysed data to predict bankruptcy improving accuracy by 4.81% using ‘Extreme Learning Machine’.

· Published at IEEE-2104, titled “Auto-associative extreme learning factory as a single class classifier”

SCHOLASTIC ACHIEVEMENTS

· Published 3 academic research papers in the field of Machine Learning and Computer Vision(’14-’15)

· Received Academic Excellence Award (awarded to top 5% students), IIT Kanpur (2012 -2013)

· Titled Gandhian Young Technological Innovator in rural development category by IIM-A (Jan’14)

· Recipient of KVPY and INSPIRE Scholarship by Dept. of Science, Govt of India (2010-2015)

· $8500 CAD scholarship to pursue machine learning internship at Simon Fraser University, Canada (2014)

· Stood runners up for ‘Solve a Social Challenge’ competition at Harvard US India Initiative (2015)

POSTIONS OF RESPONSIBILTY

· Assistant Instructor (TA) for the course in Machine Learning (Princeton) and programming (IITK)

· Head, Events (Design) at IITK technical festival managing publicity and INR 13.3 million budget (2012)

· Manager, Expansion at BloodConnect and volunteer at Lions Club blood donation camp (2015)

SKILLS AND INTERESTS

Computer Skills R, Python, C, C++, Perl, MATLABHobbies Soccer (represented school at nationals), Himalayan Trekking, Rafting

Jessica Zhu 412-245-8284 ⎪ 20 Washington Road, Princeton, NJ⎪ [email protected]

Education Princeton University Princeton, NJ Master in Finance Aug 2017-Jun 2018 Expected Coursework: Asset Pricing, Statistical Analysis of Financial Data, Financial Econometrics, Corporate Finance, Portfolio Theory and Asset Management, Stochastic Calculus, Risk Management

Carnegie Mellon University Pittsburgh, PA BSc in Computational Finance with an additional major in Statistics Aug 2013-Dec 2016 University and College Honors GPA: 3.9/4.0 Relevant Coursework: Financial Engineering, Financial Computing, Advanced Methods for Data Analysis, Stochastic Calculus, Operational Research, Microeconomics, Macroeconomics

Work and Research Experience Tudor Investment Corporation New York, NY Summer Intern, Flow of Funds Jun-Aug 2016, Apr-Jul 2017 • Designed a program that tracked the positions of market players using exchange traded options data

• split trading activities by agents to monitor exposure of dealers, customers, and firms • further analyzed their behaviors by estimating greeks of their positions

• Developed a program that monitored OTC options trading activities for risk management • designed a script in Python (Pandas) that automatically processed trading data from DTCC website • added 700+ time series comprising greeks, notionals, expirations to the database to track all traded asset markets

• Built a package that backtests trading signals by evaluating the historical return and significance of those signals • Devised a regression model that forecast the changes in long/short positions based on rate of return, open interest,

volume, survey results, etc.

Carnegie Mellon University Pittsburgh, PA Research Assistant May 2015-May 2016 • Mentored by Dr. William Hrusa, who lectures mathematical finance at Carnegie Mellon • Focused on the pricing strategies of various securities under the incomplete trinomial model • Studied optimal order sizes and indifference prices for different types of investors by looking at various utility

functions and found that investment behavior was directly related to risk averseness and initial capital • Presented at university wide undergraduate research symposium

Math Department Teaching Assistant Aug 2015-May 2016 • Served as a Teaching Assistant for Methods and Models for Optimization and Introduction to Mathematical Finance • Led weekly recitations for 30+ students through problem solving, held weekly office hours and assisted students

individually with class materials, and graded homework, exams for a class of 100+ students

Extracurricular Activities and Leadership Carnegie Mellon University Pittsburgh, PA QUANT co-founder and VP Administration Dec 2015-Dec 2016

• Initiated the first quantitative finance club at Carnegie Mellon University • Worked closely with club advisor Dr. Steve Shreve to organize administrative issues • Managed regular events such as quant talks, projects, workshops and coordinated with other divisions of the club

Skills and Interests Technicals: Python (Pandas), C++, R, LaTex, Bloomberg, C, Matlab Languages: Mandarin Interests: Texas Hold’em, yoga, food, crime shows

![[Bracken Harry] Bayle, Berkeley, And Hume(Bookos.org)](https://static.fdocuments.in/doc/165x107/545de41bb0af9ff1168b4918/bracken-harry-bayle-berkeley-and-humebookosorg.jpg)