Pie Face Investor Presentation

11

WELCOME TO August 2014 INVESTOR PRESENTATION 1

-

Upload

real-world -

Category

Investor Relations

-

view

57 -

download

1

Transcript of Pie Face Investor Presentation

WELCOME TO

August 2014

INVESTOR PRESENTATION

1

We

ma

ke p

ies

with

funn

y lit

tle fa

ce

s o

n th

em

. The

y’re

da

mn

tast

y.

Introduction to Pie Face

Management and Board

Investment Highlights

Financial Information

Appendices

AGENDA the best damn pies in the world !sweet & savoury pies, coffee, sandwiches, cakes & pastries

1

2

3

4

5

4

1

2

3

4

5

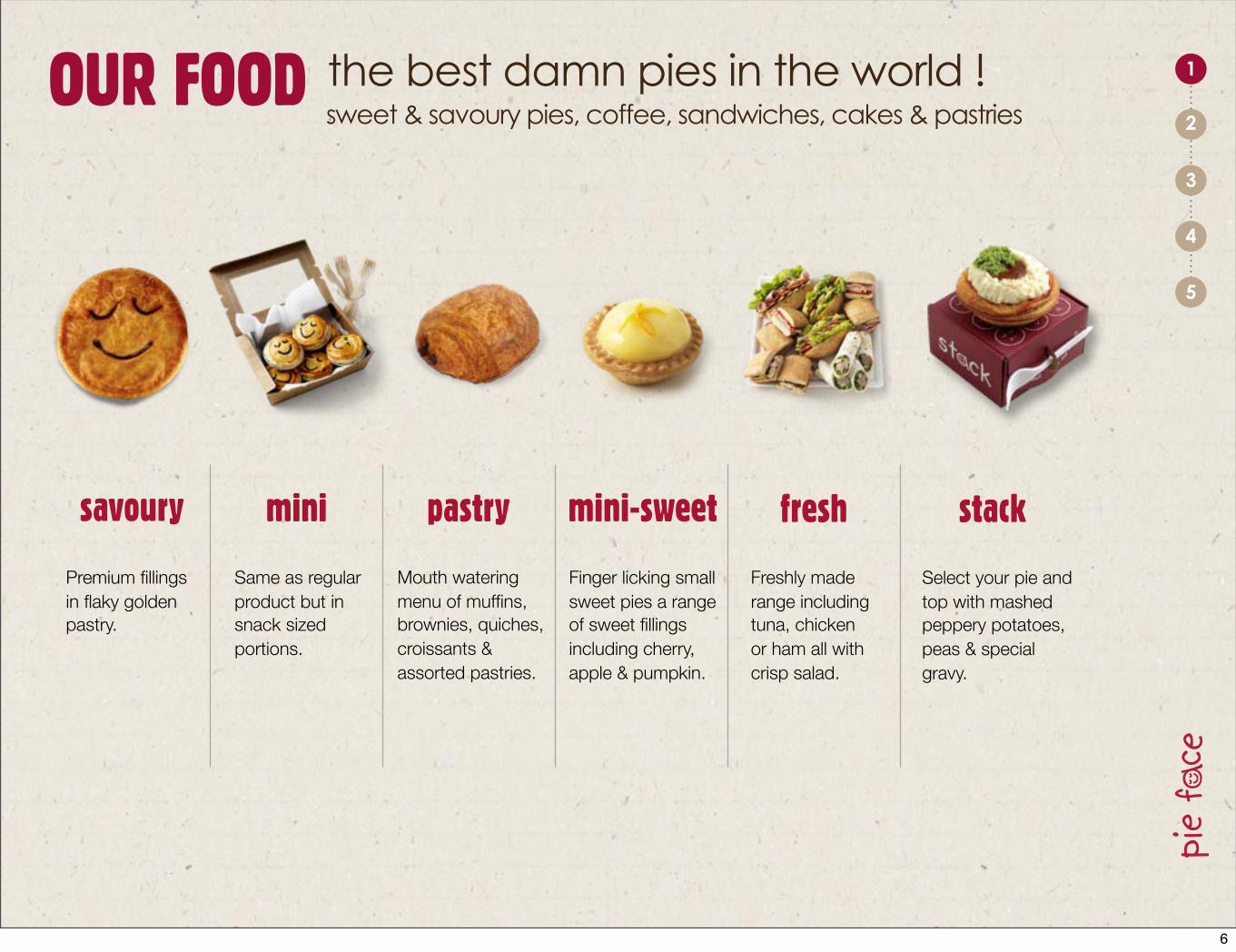

OUR FOOD the best damn pies in the world !sweet & savoury pies, coffee, sandwiches, cakes & pastries

Premium fillingsin flaky golden pastry.

savoury mini-sweetpastrymini

Same as regular product but in snack sized portions.

Mouth watering menu of muffins, brownies, quiches, croissants & assorted pastries.

Finger licking small sweet pies a range of sweet fillings including cherry, apple & pumpkin.

Freshly made range including tuna, chickenor ham all withcrisp salad.

Select your pie and top with mashed peppery potatoes,peas & special gravy.

fresh stack

6

1

2

3

4

5

OUR MENU the best damn pies in the world !sweet & savoury pies, coffee, sandwiches, cakes & pastries

7

1

2

3

4

5

11 4 2

VIC

QLD

NSW / ACT

18 15 6 1

8 6 1 1

1

WA

1

AUSTRALIAN BUSINESS MODEL

National Central Kitchen Facility / PF Distribution

Hub and spoke distribution to multiple store formats

DistributorUnder development

MallHigh St Transit Drive thru Drive up Convenience

1

SA

49

11

1

2

3

4

5

ATTRACTIVE OFFERING - Strong Brand

Selfie

14

1

2

3

4

5

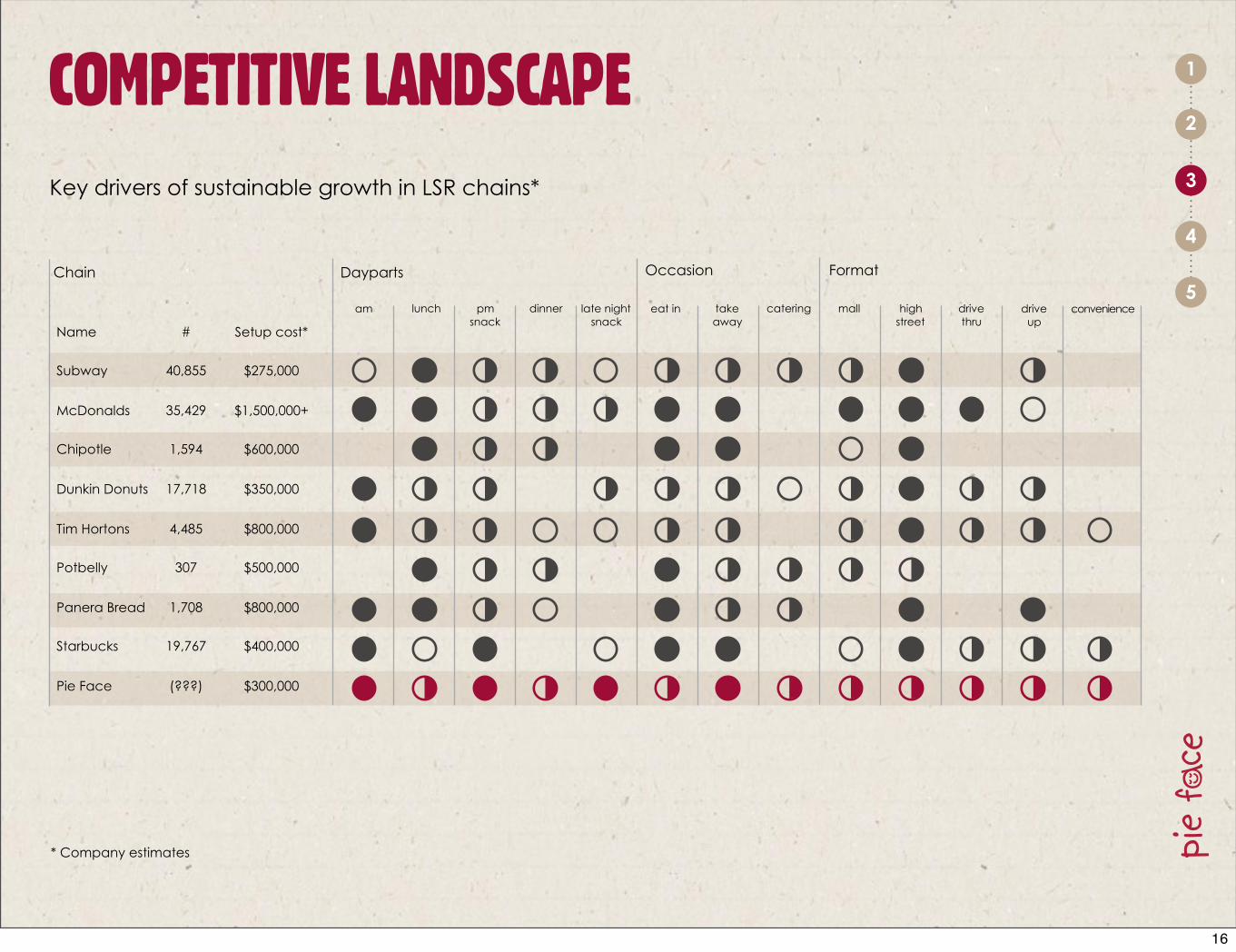

COMPETITIVE LANDSCAPE

Key drivers of sustainable growth in LSR chains*

pmsnack

Chain Dayparts Occasion Format

Name

Subway

McDonalds

Chipotle

Dunkin Donuts

Tim Hortons

Potbelly

Panera Bread

Starbucks

Pie Face

#

40,855

35,429

1,594

17,718

4,485

307

1,708

19,767

(???)

Setup cost*

$275,000

$1,500,000+

$600,000

$350,000

$800,000

$500,000

$800,000

$400,000

$300,000

am lunch dinner late nightsnack

eat in takeaway

catering mall highstreet

drivethru

driveup

convenience

* Company estimates

16

1

2

3

4

5

Philippines6 stores

by end 2015

INTERNATIONAL LICENCING

Australia69 stores open

80 stores by end 2015

New Zealand4 stores open

14 storesby end 2015

USA6 stores open21 storesby end 2015

Indonesia

Japan

Malaysia /Singapore

8 storesby end 2015

Brazil

Canada

Discussions regarding partnerships occurring

Middle East14 stores

by end 2015

Existing company stores or established partnerships

GreaterChina

RussiaSouth Korea

4 storesby end 2015

18

1

2

3

4

5

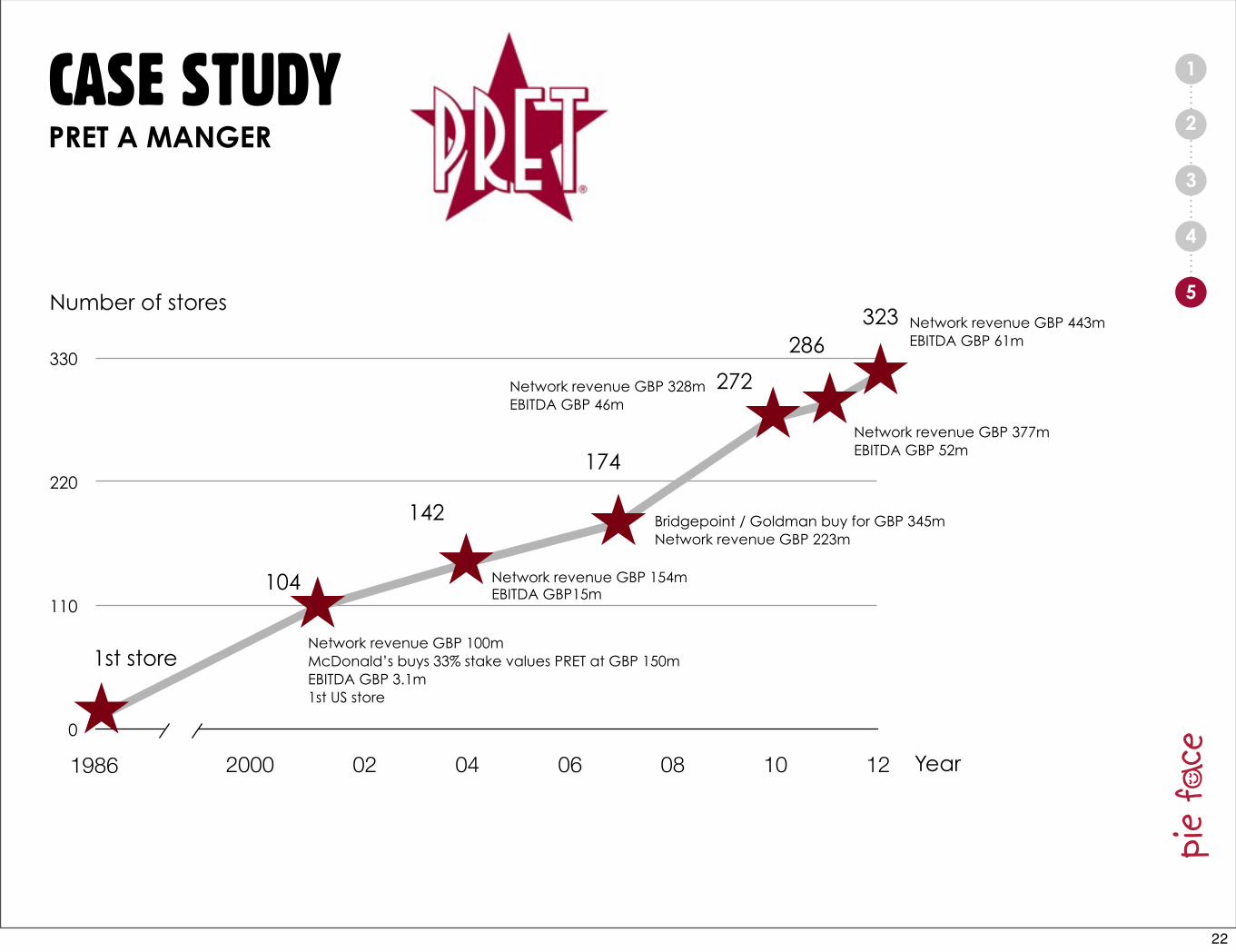

CASE STUDY

Number of stores

PRET A MANGER

0

110

220

330

86 88 90 92 94 96 98 2000 02 04 06 08 10 12 Year

1st storeNetwork revenue GBP 100mMcDonald’s buys 33% stake values PRET at GBP 150mEBITDA GBP 3.1m1st US store

Network revenue GBP 154mEBITDA GBP15m

Bridgepoint / Goldman buy for GBP 345mNetwork revenue GBP 223m

Network revenue GBP 443mEBITDA GBP 61m

104

142

174

323

272Network revenue GBP 328mEBITDA GBP 46m

1986 2000 02 04 06 08 10 12

286

Network revenue GBP 377mEBITDA GBP 52m

22

1

2

3

4

5

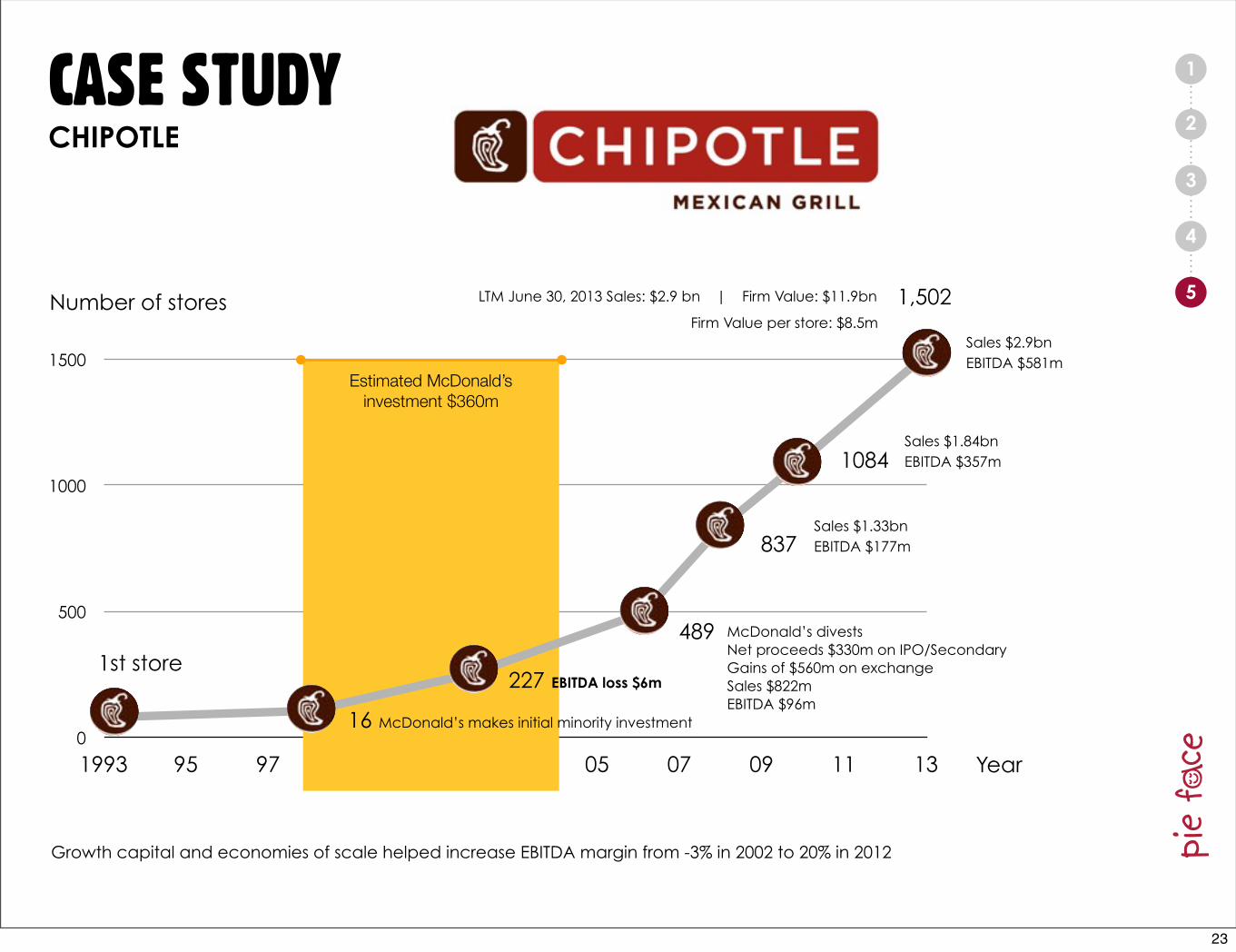

CASE STUDYCHIPOTLE

0

500

1000

1500

1993 95 97 99 01 03 05 07 09 11 13

Estimated McDonald’sinvestment $360m

Year

1st store

16 McDonald’s makes initial minority investment

McDonald’s divests Net proceeds $330m on IPO/SecondaryGains of $560m on exchangeSales $822mEBITDA $96m

227 EBITDA loss $6m

1,502LTM June 30, 2013 Sales: $2.9 bn | Firm Value: $11.9bn

489

837

1084

Sales $1.33bnEBITDA $177m

Sales $1.84bnEBITDA $357m

Growth capital and economies of scale helped increase EBITDA margin from -3% in 2002 to 20% in 2012

Firm Value per store: $8.5mSales $2.9bnEBITDA $581m

Number of stores

23

1

2

3

4

5

$106,830

$1,490,592

14.0x

$421,419

$10,066,890

23.9x

$167,705

$2,005,197

12.0x

EBITDA / Avg Store

EV/Avg Store

EV / EBITDA

COMPARABLE COMPANY SNAPSHOT

$289.010

$3,147,067

10.9x

$161,356

$2,815,825

17.5x

$19,036

$381,698

20.1x

EBITDA / Avg Store

EV/Avg Store

EV / EBITDA

26

![SCface surveillance cameras face databasescface.org/SCface - Surveillance Cameras Face Database.pdf · SCface – surveillance cameras face database ... CMU PIE [18], FERET [16, 17]](https://static.fdocuments.in/doc/165x107/5b15d5d87f8b9a961e8b91c5/scface-surveillance-cameras-face-surveillance-cameras-face-databasepdf-scface.jpg)