Philippines - PwCfiles.pwc.at/.../philippines-insurance-taxation-2011.pdf · Philippines: General...

13

International comparison o Philippines General insurance – overvi Definition Accountin Definition of property and casualty insurance company Non-life in insurance o marine, fir surety, fide and such o Insurance Casualty in liability ari certain typ considered other types It includes insurance, glass insur personal ac by non- life substantial Sec. 174, In Commercial accounts/ tax and regulatory returns Accountin Basis for the company’s commercial accounts Financial s with Philip (“PFRS”)w Financial R The term P PFRS, Phil interpretat Committee Committee Reporting which have Reporting adopted by Commissio Regulatory return Based on t insurance c issued by t Letter No. The audite Insurance 77 of insurance taxation iew ng Taxation nsurance company is one which solicits on the security of property such as: re and casualty insurance companies; elity, indemnity and bonding companies; other persons as may be authorised by the Commission. (RMC 30- 2008). nsurance is insurance covering loss or ising from accident or mishap, excluding pes of loss, which by law or custom, are d as falling exclusively within the scope of s of insurance such as fire or marine. s, but is not limited to, employer's liability , motor vehicle liability insurance, plate rance, burglary and theft insurance, ccident and health insurance as written e insurance companies and other lly similar kinds of insurance. (Title 3 nsurance Code). A company offer insurance would company which as one which sol property such as insurance compa and bonding com may be authoris (RMC 30-2008) ng Taxation statements are prepared in accordance ppine Financial Reporting Standards which is aligned with International Reporting Standards (“IFRS”). PFRS in general includes all applicable lippine Accounting Standards (“PAS”), tions of the Philippine Interpretations e(“PIC”), Standing Interpretations e(“SIC”) and International Financial Interpretations Committee (“IFRIC”) e been approved by the Financial Standards Council (“FRSC”) and y the Securities and Exchange on (“SEC”). Audited commer statements whic return would be financial reporti Taxation is base accounts as adju the uniform chart of accounts for general companies and professional reinsurer the Insurance Commission (Circular 34- 2006). ed financial statements are filed with the Commission (“IC”) and SEC. Not applicable. ring property and casualty d be considered a non-life insurance is defined under existing tax rules licits insurance on the security of s: marine, fire and casualty anies; surety, fidelity, indemnity mpanies; and such other persons as sed by the Insurance Commission. ). rcial accounts or financial ch are attached to the annual tax e the same as the one prepared for ing purposes. ed on the audited commercial usted according to tax rules.

-

Upload

phamnguyet -

Category

Documents

-

view

217 -

download

0

Transcript of Philippines - PwCfiles.pwc.at/.../philippines-insurance-taxation-2011.pdf · Philippines: General...

International comparison of

Philippines

General insurance – overview

Definition Accounting

Definition of property andcasualty insurance company

Nonlife insurance company is one which solicitsinsurance on the security of property such as:marine, fire and casualty insurance companies;surety, fidelity, indemnity and bonding companies;and such other persons as may be authorInsurance

Casualty insurance is insurance covering loss orliability arising from accident or mishap, excludingcertain types of loss, which by law or custom, areconsidered as falling exclusively within the scope ofother types of insura

It includes, but is not limited to, employer's liabilityinsurance, motor vehicle liability insurance, plateglass insurance, burglary and theft insurance,personal accident and health insurance as writtenby non life insurancsubstantially similar kinds ofSec. 174, Insurance Code)

Commercial accounts/tax and regulatory returns Accounting

Basis for the company’scommercial accounts

Financial statements are prepared in accordancewith Philippine Financial Reporting Standards(“PFRS”) which is aligned with InternationalFinancial Reporting Standards (

The term PFRS in general includes all applicablePFRS, Philippine Accounting Standards (interpretations of the Philippine InterpretationsCommittee (Committee (Reporting Interpretations Committee (which have been approved by the FinancialReporting Standards Council (adopted by the Securities and ExchangeCommission (

Regulatory return Based on the uniform chart of accounts for generalinsurance companies and professional reinsurerissued by the Insurance Commission (CircularLetter No. 34

The audited financial statements are filed with theInsurance Commission (

77

omparison of insurance taxation

verview

Accounting Taxation

life insurance company is one which solicitsinsurance on the security of property such as:marine, fire and casualty insurance companies;surety, fidelity, indemnity and bonding companies;and such other persons as may be authorised by theInsurance Commission. (RMC 30 2008).

Casualty insurance is insurance covering loss orliability arising from accident or mishap, excludingcertain types of loss, which by law or custom, areconsidered as falling exclusively within the scope ofother types of insurance such as fire or marine.

It includes, but is not limited to, employer's liabilityinsurance, motor vehicle liability insurance, plateglass insurance, burglary and theft insurance,personal accident and health insurance as written

life insurance companies and othersubstantially similar kinds of insurance. (Title 3

Insurance Code).

A company offering property and casualtyinsurance would be considered a noncompany which is defined under existing tax rulesas one which solicits insurance on the security ofproperty such as: marine, fire and casualtyinsurance companies; surety, fidelity, indemnityand bonding companies; and such other persons asmay be authorised(RMC 302008).

Accounting Taxation

Financial statements are prepared in accordancewith Philippine Financial Reporting Standards

) which is aligned with InternationalFinancial Reporting Standards (“IFRS”).

The term PFRS in general includes all applicablePFRS, Philippine Accounting Standards (“PAS”),interpretations of the Philippine InterpretationsCommittee (“PIC”), Standing InterpretationsCommittee (“SIC”) and International FinancialReporting Interpretations Committee (“IFRIC”)which have been approved by the FinancialReporting Standards Council (“FRSC”) andadopted by the Securities and ExchangeCommission (“SEC”).

Audited commercial accounts or financialstatements which are attached to the annual taxreturn would be the same as the one prepared forfinancial reporting purposes.

Taxation is based on the audited commercialaccounts as adjusted according to tax rules.

Based on the uniform chart of accounts for generalinsurance companies and professional reinsurerissued by the Insurance Commission (CircularLetter No. 34 2006).

The audited financial statements are filed with theInsurance Commission (“IC”) and SEC.

Not applicable.

A company offering property and casualtyinsurance would be considered a nonlife insurancecompany which is defined under existing tax rulesone which solicits insurance on the security of

property such as: marine, fire and casualtyinsurance companies; surety, fidelity, indemnityand bonding companies; and such other persons as

ised by the Insurance Commission.2008).

Audited commercial accounts or financialstatements which are attached to the annual taxreturn would be the same as the one prepared forfinancial reporting purposes.

Taxation is based on the audited commercialaccounts as adjusted according to tax rules.

Philippines: General insurance

Commercial accounts/tax and regulatory returns Accounting

Tax return Not applicable.

78

nsurance – overview (continued)

Accounting Taxation

Not applicable. Nonlife insurance companies are generallyrequired to file income tax returns,(“VAT”) returns,premiums on health and accident insurancereceived by nonwithholding tax returns,returns, and documentary stamp tax (returns.

Generally, the payment of tax shall be madesame date the return is filed.

! Corporate income tax returns are filed on aquarterly and annual basis. The quarterlydeclaration shall be filed within 60 daysfollowing the close of each of the first 3of the taxable year. The finalshall be filed on or before the 15month following the close ofon or before Aprilcalendar year basis)

! VAT declarations/and quarterly basis. The deadline for filing is 20and 25 days following the close of each monthquarter, respectively.

! Premium tax returns are filed on a monthlybasis, on or beforeof each month

! For monthly withholding tax returns (expanded,final and withholding tax on compensation), andwithholding VAT returns (if applicable)deadline for filing is 10 days after the end of eachmonth, except foris filed on or befyear.

! FBT returns, if applicable,quarterly basis no later than 10end of each quarter.

! DST returns, areclose of the month when theexecuted.

Nonlife insurance companies arelocal business tax which shall be paid to the localgovernment of the city or municipality wherehead office and branches are located, noJanuary 20 of each year.

Further, if the insuranceproperty, it shall be subject to realwhich may be paid in four equalduring the year, i.e.30, September 30, and

life insurance companies are generallyrequired to file income tax returns, valueadded tax

returns, premium tax returns (for thepremiums on health and accident insurance

life insurance companies),withholding tax returns, fringe benefit tax (“FBT”)

and documentary stamp tax (“DST”)

enerally, the payment of tax shall be made on thesame date the return is filed.

Corporate income tax returns are filed on auarterly and annual basis. The quarterlydeclaration shall be filed within 60 daysollowing the close of each of the first 3 quartersof the taxable year. The final adjustment returnshall be filed on or before the 15th day of the 4thmonth following the close of the fiscal year (e.g.,

April 15 for those operating oncalendar year basis).

declarations/returns are filed on a monthlyquarterly basis. The deadline for filing is 2025 days following the close of each month or

quarter, respectively.Premium tax returns are filed on a monthlybasis, on or before the 20th day following the end

month.or monthly withholding tax returns (expanded,final and withholding tax on compensation), andwithholding VAT returns (if applicable), thedeadline for filing is 10 days after the end of eachmonth, except for the month of December whichis filed on or before January 15th of the following

, if applicable, are filed on aquarterly basis no later than 10 days after theend of each quarter.

are filed within 5 days after theclose of the month when the taxable document is

life insurance companies are also subject totax which shall be paid to the local

government of the city or municipality where itshead office and branches are located, no later thanJanuary 20 of each year.

Further, if the insurance company has realproperty, it shall be subject to real property tax,which may be paid in four equal installmentsduring the year, i.e., on or before March 31, June30, September 30, and December 31.

Philippines: General insurance

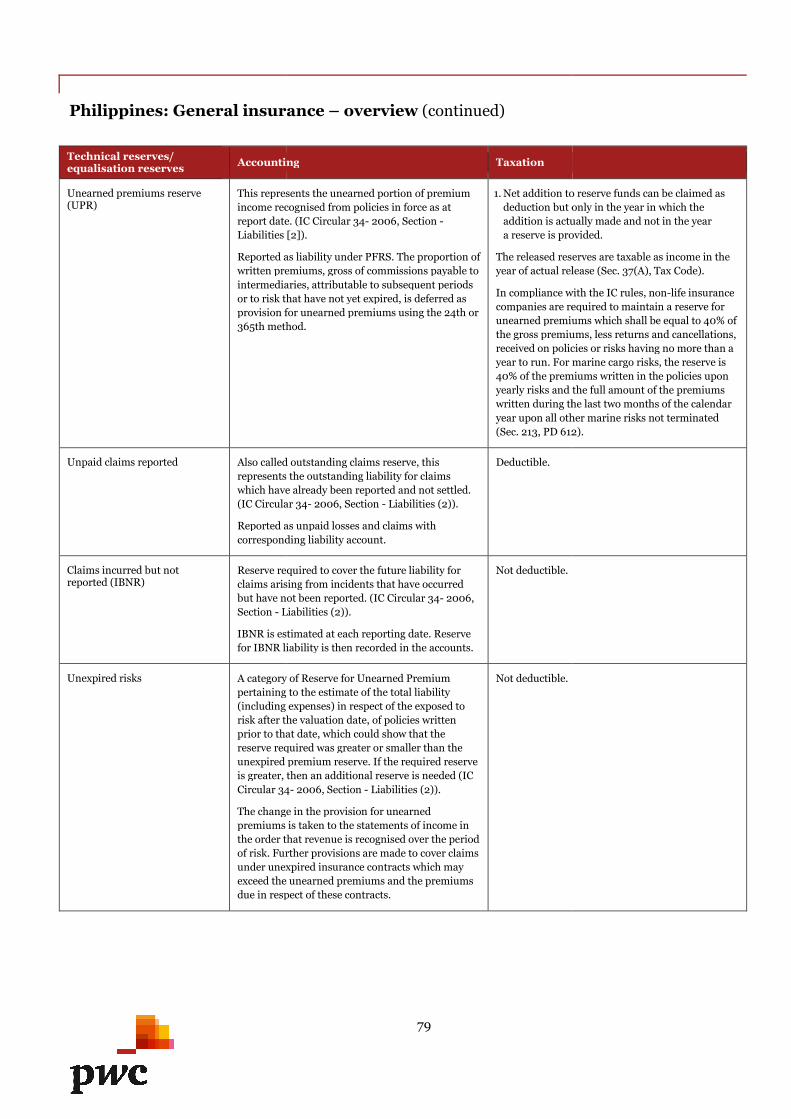

Technical reserves/equalisation reserves Accounting

Unearned premiums reserve(UPR)

This represents the unearned portion of premiumincome recognreport date. (IC Circular 34Liabilities [2]

Reported as liability under PFRS.written premiums, gross of commissions payable tointermediaries, attributable to subsequent periodsor to risk that have not yet expired, is deferred asprovision for unearned premiums365th method.

Unpaid claims reported Also called outstanding claims reserve, thisrepresents the outstanding liability for claimswhich have already been reported and not settled.(IC Circular 34

Reported as unpaid losses and claims withcorresponding liability account.

Claims incurred but notreported (IBNR)

Reserve required toclaims arisingbut have notSection Liabilities (2)).

IBNR is estimatedfor IBNR liability is then recorded in the accounts.

Unexpired risks A category of Reserve for Unearned Premiumpertaining to the estimate of the total liability(including expenses) in respect of the exposed torisk after the valuation date, of policies writtenprior to that date, which could show that thereserve required was greater or smaller than theunexpired premium reserve. If the required reserveis greater, then an additional reserve is needed (ICCircular 34

The change in the provision for unearnedpremiums is taken to the statements of income inthe order that revenueof risk. Further provisions are made to cover claimsunder unexpired insurance contracts which mayexceed the unearned premiums and the premiumsdue in respect of these contracts.

79

nsurance – overview (continued)

Accounting Taxation

This represents the unearned portion of premiumincome recognised from policies in force as atreport date. (IC Circular 34 2006, Section

ties [2]).

Reported as liability under PFRS. The proportion ofwritten premiums, gross of commissions payable tointermediaries, attributable to subsequent periodsor to risk that have not yet expired, is deferred asprovision for unearned premiums using the 24th or365th method.

1. Net addition to reserve funds can be claimed asdeduction but only in the year in which theaddition is actually made and not in the yeara reserve is provided.

The released reserves are taxable asyear of actual release (Sec.

In compliance with the ICcompanies are required to maintain aunearned premiums which shallthe gross premiums, lessreceived on policies or risks having no more than ayear to run. For marine cargo risks, the reserve is40% of the premiums written in the policiesyearly risks and the full amount of thewritten during the last two monthsyear upon all othe(Sec. 213, PD 612

Also called outstanding claims reserve, thisrepresents the outstanding liability for claimswhich have already been reported and not settled.(IC Circular 34 2006, Section Liabilities (2)).

Reported as unpaid losses and claims withcorresponding liability account.

Deductible.

Reserve required to cover the future liability forclaims arising from incidents that have occurredbut have not been reported. (IC Circular 34 2006,

Liabilities (2)).

IBNR is estimated at each reporting date. Reservefor IBNR liability is then recorded in the accounts.

Not deductible.

A category of Reserve for Unearned Premiumpertaining to the estimate of the total liability(including expenses) in respect of the exposed torisk after the valuation date, of policies writtenprior to that date, which could show that thereserve required was greater or smaller than the

d premium reserve. If the required reserveis greater, then an additional reserve is needed (ICCircular 34 2006, Section Liabilities (2)).

The change in the provision for unearnedpremiums is taken to the statements of income inthe order that revenue is recognised over the periodof risk. Further provisions are made to cover claimsunder unexpired insurance contracts which mayexceed the unearned premiums and the premiumsdue in respect of these contracts.

Not deductible.

Net addition to reserve funds can be claimed asdeduction but only in the year in which theaddition is actually made and not in the yeara reserve is provided.

released reserves are taxable as income in theactual release (Sec. 37(A), Tax Code).

In compliance with the IC rules, nonlife insurancecompanies are required to maintain a reserve forunearned premiums which shall be equal to 40% ofthe gross premiums, less returns and cancellations,

icies or risks having no more than ato run. For marine cargo risks, the reserve is

40% of the premiums written in the policies uponyearly risks and the full amount of the premiumswritten during the last two months of the calendaryear upon all other marine risks not terminated

, PD 612).

Philippines: General insurance

Technical reserves/equalisation reserves Accounting

General contingency/ solvencyreserves

General contingency for losses are notbe reflected in the financial

Solvency reserves representing additional capitalcontributions from stockholders to meet theminimumMargin of Solvency is reported as part ofEquity accounts.

Contingency surplus represents contributions ofthe stockholders to cover any deficiency in tMargin of Solvency as required under theInsurance Code and can be withdrawn only uponthe approval of the Insurance Commission. (ICCircular 34

Equalisation reserves Claims Equalization Reserve is in addition to thespecific provisions already detailed and its purposeis to cushion any large year to year fluctuations inthe actual claims experience. By definition thelarge claim at the tail of the frequency distributiis a rate event but must happen some time. Oneyear may well havea cushion, the company’s accounts would progressirregularly. This reserve including catastrophereserve may not be held explicitly but may inpractice be represented by the stockholders’ equityor in the case of a mutual company, excess assets.(IC Circular 34

Catastrophe Reserve is occasionally a single eventor combination of events (e.g., earthquake) maygive rise to multiple claims of huge totaldimensions far beyond that would be regarded asadequate provision for claims to be expected withinnormal experisevere strain or even extinguish the assets of thecompany, especially if the company is operating ona worldwide basis. (IC Circular 34Section Liabilities (2)).

Reserve for Catastrophe Loss represents thecompany’s reserve for allied perils caused bycatastrophic events. (IC Circular 34Section Liabilities (2)).

Reserve for catastrophe loss is not allowed underPFRS/IFRS but is allowed and reflected in theregulatory return filed with the IC.

80

nsurance – overview (continued)

Accounting Taxation

General contingency for losses are not allowed tobe reflected in the financial statements.

Solvency reserves representing additional capitalcontributions from stockholders to meet theminimumMargin of Solvency is reported as part ofEquity accounts.

Contingency surplus represents contributions ofthe stockholders to cover any deficiency in theMargin of Solvency as required under theInsurance Code and can be withdrawn only uponthe approval of the Insurance Commission. (ICCircular 34 2006, Section Equity (3)).

Not deductible.

Claims Equalization Reserve is in addition to thespecific provisions already detailed and its purposeis to cushion any large year to year fluctuations inthe actual claims experience. By definition thelarge claim at the tail of the frequency distributionis a rate event but must happen some time. Oneyear may well have more than another and withoutcushion, the company’s accounts would progressirregularly. This reserve including catastrophereserve may not be held explicitly but may in

e represented by the stockholders’ equityor in the case of a mutual company, excess assets.(IC Circular 34 2006, Section Liabilities (2)).

Catastrophe Reserve is occasionally a single eventor combination of events (e.g., earthquake) maygive rise to multiple claims of huge totaldimensions far beyond that would be regarded asadequate provision for claims to be expected withinnormal experience. The catastrophe could put asevere strain or even extinguish the assets of thecompany, especially if the company is operating ona worldwide basis. (IC Circular 34 2006,

Liabilities (2)).

Reserve for Catastrophe Loss represents thepany’s reserve for allied perils caused by

catastrophic events. (IC Circular 34 2006,Liabilities (2)).

Reserve for catastrophe loss is not allowed underPFRS/IFRS but is allowed and reflected in theregulatory return filed with the IC.

Not deductible.

.

Philippines: General insurance

Expenses/ refunds Accounting

Acquisition expenses Commission and other acquisition costs incurredduring the financial period that vary with and arerelated to securing new insurance contracts and orrenewing existing insurance contracts, but whichrelates to subsequent financial periods, aredeferred toof future revenue margins. All other acquisitioncosts are recogn

Subsequent to initial recognition, these costs areamortisedthe contracstatements of income. The unamortacquisition costs are shown as Deferred acquisitioncosts in the assets section of the balance sheets.

Loss adjustment expenses onunsettled claims (claimshandling expenses)

Estimated at each reporting date and included aspart of provisions.

Experiencerated refunds Not a common practice in the Philippines.Accounted as a credit whenbooked as a receivable if prudently estimated.

Investments Accounting

Gains and losses oninvestments

Gains and losses are recognised based on PAS32/39 (similar to IAS 32/39).

Investment reserves Based on marked to market valuation andamortised costs. Recognised under PAS32/39.

Investment income Interest income is recognised based on effectiveinterest method.

Dividend incomecompany’s right to receive the payment isestablished.

Gain and losses from sale of irecognisedGain and lossesthe difference between the carrying amount of theinvestment and actual proceeds from the sale.

81

nsurance – overview (continued)

Accounting Taxation

Commission and other acquisition costs incurredduring the financial period that vary with and arerelated to securing new insurance contracts and orrenewing existing insurance contracts, but whichrelates to subsequent financial periods, aredeferred to the extent that they are recoverable outof future revenue margins. All other acquisitioncosts are recognised as an expense when incurred.

Subsequent to initial recognition, these costs areised on a straight line basis over the life of

the contract. Amortization is charged to thestatements of income. The unamortisedacquisition costs are shown as Deferred acquisitioncosts in the assets section of the balance sheets.

Deductible if actually incurred.

Estimated at each reporting date and included aspart of provisions.

Not deductible.

Not a common practice in the Philippines.Accounted as a credit when earned or may bebooked as a receivable if prudently estimated.

Taxable when earned

Accounting Taxation

Gains and losses are recognised based on PAS32/39 (similar to IAS 32/39).

Gains/losses are

Based on marked to market valuation andamortised costs. Recognised under PAS32/39.

Not deductible.

Interest income is recognised based on effectiveinterest method.

Dividend income is recognised when theompany’s right to receive the payment isestablished.

and losses from sale of investments isised when investments are sold or disposed.and losses from sale of Investment is based on

the difference between the carrying amount of theinvestment and actual proceeds from the sale.

Unless specifically exempt, investmentgenerally subject to final withholding tax.

Deductible if actually incurred.

Taxable when earned/realised.

e taxable/deductible when realised.

Unless specifically exempt, investment income isgenerally subject to final withholding tax.

Philippines: General insurance

Reinsurance Accounting

Reinsurance premiums andclaims

Reinsurance premiums assumed represent theaggregate premiums assumed from cedingcompanies under treaty or facultative agreements.(IC Circular 34(4)).

Reinsurance premiums ceded represent premiumon outward cessions under treaty or facultativeagreements with reinsurers. (IC Circular 34Section Income Accounts (4)).

Losses on reinsurance assumed represent theaggregate losses and claims the company hasincurred on its acceptances under treaty orfacultative agreements. (IC Circular 34Section Underwriting Expense Accounts (5

Loss recoveries on reinsurance ceded representsthe aggregate share of the reinsurers on the claimsand losses and adjustment expenses of thecompany on business ceded under treaty orfacultative agreements. (IC Circular 34Section Underwri

Recognised similar to premium and claims.

Mutual companies Accounting

Mutual companies (all profitsreturned to members)

If a new insurance company is organised as amutual company, in lieuhave available cash assets of at least five millionpesos above all liabilities for losses reported,expenses, taxes, legal reserve and reinsurance of alloutstanding risks and the contributed surplus fundequal to the amounts requicorporations.

A stock insurance company doing business in thePhilippines may, subject to the pertinent law andregulations which now are of hereafter may be inforce, alter its organisation and transform itselfinto a mutual insurance compa(Section 188 of the Insurance Code)

Accounted in the same principles as thoseapplicable to common insurance companies and inaccordance with PFRS.

82

nsurance – overview (continued)

Accounting Taxation

Reinsurance premiums assumed represent theaggregate premiums assumed from cedingcompanies under treaty or facultative agreements.(IC Circular 34 2006, Section Income Accounts

Reinsurance premiums ceded represent premiumon outward cessions under treaty or facultativeagreements with reinsurers. (IC Circular 34 2006,

Income Accounts (4)).

Losses on reinsurance assumed represent theaggregate losses and claims the company hasincurred on its acceptances under treaty orfacultative agreements. (IC Circular 34 2006,

Underwriting Expense Accounts (5)).

Loss recoveries on reinsurance ceded representsthe aggregate share of the reinsurers on the claimsand losses and adjustment expenses of thecompany on business ceded under treaty orfacultative agreements. (IC Circular 34 2006,

Underwriting Expense Accounts (5)).

Recognised similar to premium and claims.

Reinsurance assumed (net of returns,cancellations) is tlosses, maturities and benefits net of reinsurancerecoveries form part of direct cost thus,in the year incurred for income tax

Accounting Taxation

If a new insurance company is organised as amutual company, in lieu of capital stock, it musthave available cash assets of at least five millionpesos above all liabilities for losses reported,expenses, taxes, legal reserve and reinsurance of alloutstanding risks and the contributed surplus fundequal to the amounts required of stockcorporations.

A stock insurance company doing business in thePhilippines may, subject to the pertinent law andregulations which now are of hereafter may be inforce, alter its organisation and transform itselfinto a mutual insurance company.(Section 188 of the Insurance Code).

Accounted in the same principles as thoseapplicable to common insurance companies and inaccordance with PFRS.

Subject to income tax and VAT. The insurancepolicies issued by mutual insurance companies areexempt from DST.

Mutual Insurance CompaniesIn the case of mutual fire and mutualliability and mutual workmen’smutual casualty insurancecompanies shall not returnof the premium deposits returned to theirpolicyholders, butincomereceived by them from all other sources plusportion of the premium deposits as arethe companies for purposesof losses and expenses and reinsurance reserves.(Sec. 37(B), Tax Code)

Mutual Marine Insurance Companies.Mutual marine insurance companies shallin their return of gross income, grosscollected and received by themfor reinsurance, but shallthe deductions fromto policyholders on account of premiumspreviously paid by them and interest paithose amounts between thepayment thereof (Sec.

Reinsurance assumed (net of returns,cancellations) is taxable. Ceded reinsurance, claimslosses, maturities and benefits net of reinsurance

part of direct cost thus, deductiblein the year incurred for income tax purposes.

Subject to income tax and VAT. The insurancepolicies issued by mutual insurance companies areexempt from DST. (Sec. 199(A), Tax Code).

Mutual Insurance CompaniesIn the case of mutual fire and mutual employers’liability and mutual workmen’s compensation andmutual casualty insurance companies, saidcompanies shall not return as income any portion

deposits returned to theirpolicyholders, but shall return as taxable income all

received by them from all other sources plus suchportion of the premium deposits as are retained bythe companies for purposes other than the payment

expenses and reinsurance reserves., Tax Code).

Mutual Marine Insurance Companies.Mutual marine insurance companies shall includein their return of gross income, gross premiumscollected and received by them less amounts paidfor reinsurance, but shall be entitled to include inthe deductions from gross income amounts repaidpolicyholders on account of premiums

previously paid by them and interest paid uponthose amounts between the ascertainment andpayment thereof (Sec. 37(C), Tax Code).

Philippines: General insurance

Further corporate taxfeatures Taxation

Loss carryovers Net operating loss of the business for any taxable year immediatelywhich had notfrom gross income for the next 3 consecutive taxable years

Any loss incurred in a taxable year duringallowed as a deduction

Foreign branch income Generally, taxable. The tax paid overseas is creditable.

Domestic branch income Combined with head office income and taxed at normal

However, premiums earned may be subjected to varying local business tax rates if suchgenerated by the branches located in various cities and/or municipalities.

Corporate tax rate 30% regular corporate income tax (corporate i

Note that MCIT shall only be applicableyear in which such corporation commenced its business operations.

Other tax features Taxation

Premium taxes Generally, premiums received by a non

However, premiums onconsidered as premium on life insurance, therefore, subject to premium tax (RMC 59

Capital taxes and taxes onsecurities

On the sale of shares of stock not traded ingain) plus 10%((Sec. 27 (D), Tax Code).

However, sale of shares of stock listed1% percentage tax

Captive insurance companies No special treatment.

Value added tax (VAT) Premiums collected by nonand accident insurance.

Reinsurance premiums arethe direct insurer

Insurance and reinsurance commissions are subject to 12% VAT (RR

83

nsurance – other tax features

Net operating loss of the business for any taxable year immediately proceeding the currentwhich had not been previously offset as deduction from gross income shallfrom gross income for the next 3 consecutive taxable years immediately following the year of such loss.

Any loss incurred in a taxable year during which the taxpayer was exempt from income tax shall not beallowed as a deduction (Sec. 34(D) (3), Tax Code).

Generally, taxable. The tax paid overseas is creditable.

Combined with head office income and taxed at normal corporate income tax rates

However, premiums earned may be subjected to varying local business tax rates if suchgenerated by the branches located in various cities and/or municipalities.

regular corporate income tax (“RCIT”) which is based on taxable net incomeincome tax (“MCIT”) which is based on taxable gross income, whichever is higher.

Note that MCIT shall only be applicable beginning on the fourth taxableyear in which such corporation commenced its business operations.

Generally, premiums received by a nonlife insurance company are not subject to premium tax.

However, premiums on health and accident insurance received by a nonconsidered as premium on life insurance, therefore, subject to premium tax (RMC 59

the sale of shares of stock not traded in the stock exchange, a final tax of 5% () plus 10%(for gains in excess of P100,000) on the net capital gains real

(Sec. 27 (D), Tax Code).

However, sale of shares of stock listed and traded though the local stock exchange shall be subject to 1/2 of1% percentage tax (Sec. 127 (A), Tax Code).

No special treatment.

Premiums collected by nonlife insurance companies are subject to 12% VATand accident insurance.

einsurance premiums are not subject to VAT because the tax on such premiums had already been paidthe direct insurer (RMC 302008, RR 42007).

Insurance and reinsurance commissions are subject to 12% VAT (RR 42007).

roceeding the current taxable year,been previously offset as deduction from gross income shall be carried over as a deduction

immediately following the year of such loss.

r was exempt from income tax shall not be

corporate income tax rates.

However, premiums earned may be subjected to varying local business tax rates if such premiums weregenerated by the branches located in various cities and/or municipalities.

which is based on taxable net income or 2% minimumwhich is based on taxable gross income, whichever is higher.

beginning on the fourth taxable year immediately following the

ot subject to premium tax.

health and accident insurance received by a nonlife insurance company shall beconsidered as premium on life insurance, therefore, subject to premium tax (RMC 592008).

final tax of 5% (on the first P100,000net capital gains realised during the taxable year

local stock exchange shall be subject to 1/2 of

life insurance companies are subject to 12% VAT, except premiums on health

because the tax on such premiums had already been paid by

2007).

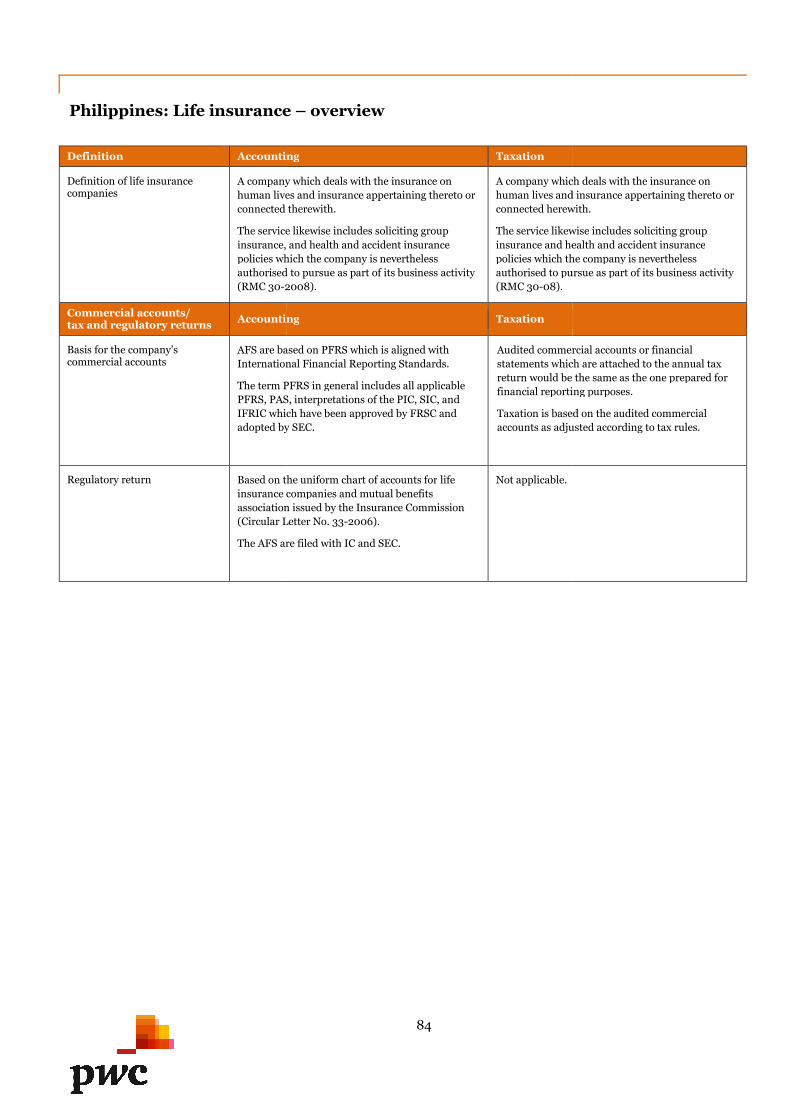

Philippines: Life insurance

Definition Accounting

Definition of life insurancecompanies

A company which deals with the insurance onhuman lives and insurance appertaining thereto orconnected therewith.

The serviceinsurance, and health and accident insurancepolicies which theauthorised(RMC 3020

Commercial accounts/tax and regulatory returns Accounting

Basis for the company’scommercial accounts

AFS are based onInternational Financial

The term PFRS in general includes all applicablePFRS, PASIFRIC which have been approved byadopted by

Regulatory return Based on the uniform chart of accounts forinsurance companies andassociation(Circular Letter No.

The AFS are filed with IC

84

nsurance – overview

Accounting Taxation

company which deals with the insurance onlives and insurance appertaining thereto or

connected therewith.

The service likewise includes soliciting groupinsurance, and health and accident insurancepolicies which the company is nevertheless

ised to pursue as part of its business activity2008).

A company which deals with thehuman lives andconnected herewith.

The service likewise includes soliciting groupinsurance and health and accident insurancepolicies which the company is neverthelessauthorised to pursue as part of its business(RMC 3008).

Accounting Taxation

based on PFRS which is aligned withInternational Financial Reporting Standards.

The term PFRS in general includes all applicablePAS, interpretations of the PIC, SIC, andwhich have been approved by FRSC and

adopted by SEC.

Audited commercial accounts or financialstatements which are attached to the annual taxreturn would be the same as the one prepared forfinancial reporting purposes.

Taxation is based on the audited commercialaccounts as adjusted according to tax rules.

Based on the uniform chart of accounts for lifeinsurance companies and mutual benefitsassociation issued by the Insurance Commission(Circular Letter No. 332006).

The AFS are filed with IC and SEC.

Not applicable.

company which deals with the insurance onhuman lives and insurance appertaining thereto orconnected herewith.

The service likewise includes soliciting groupinsurance and health and accident insurancepolicies which the company is nevertheless

to pursue as part of its business activity

Audited commercial accounts or financialstatements which are attached to the annual taxreturn would be the same as the one prepared for

reporting purposes.

Taxation is based on the audited commercialaccounts as adjusted according to tax rules.

Philippines: Life insurance

Commercial accounts/tax and regulatory returns Accounting

Tax return The annualcompany is filed with the AFS toInternal Revenue on orfourth monthtaxable year.

Other tax returns are accounted for in theprinciple as described in Taxation.

85

nsurance – overview (continued)

Accounting Taxation

The annual income tax return of the insurancecompany is filed with the AFS to the Bureau ofInternal Revenue on or before the 15th day of thefourth month following the close of the tax payer’staxable year.

Other tax returns are accounted for in the samele as described in Taxation.

Life insurance companies are generallyfile income tax returns,(premium tax and gross receipts tax)(as applicable), withholding tax returnsreturns and DST returns. Generathe tax shall be madefiled.

! Corporate income tax returns are filed on aquarterly and annual basis. The quarterlydeclaration shall be filed within 60 daysfollowing the close of each of the first 3of the taxable year. The finalshall be filed on or before the 15month following the close ofon or before Aprilcalendar year basis)

! VAT declarations/and quarterly basis. The deadline for filing is 20and 25 days following the close of each monthquarter, respectively.

! Percentage tax returnsclose of each month;

! For monthly withholding tax returnsfinal and withholding tax on compensation), andwithholding VAT returns (if applicable)deadline for filing is 10 days after the end of eachmonth, except foris filed on or before January 15year.

! FBT returns, if applicable,quarterly basis not later than 10end of each quarter.

! DST returns areclose of the monthexecuted.

Life insurance companies arebusiness tax which shall be paid to the localgovernment of the city or municipality wherehead office an branches are located, notJanuary 20 of each year.

Further, if the insurance company has realproperty, it shall be subject to realwhich may be paid in four equalduring the year, i.e. on or before30, September 3 and

Life insurance companies are generally required tofile income tax returns, percentage tax returns(premium tax and gross receipts tax), VAT returns

withholding tax returns, FBTand DST returns. Generally, the payment of

the tax shall be made on the same date the return is

Corporate income tax returns are filed on auarterly and annual basis. The quarterlydeclaration shall be filed within 60 daysfollowing the close of each of the first 3 quartersof the taxable year. The final adjustment returnshall be filed on or before the 15th day of the 4thmonth following the close of the fiscal year (e.g.,

April 15 for those operating oncalendar year basis).

declarations/returns are filed on a monthlyquarterly basis. The deadline for filing is 2025 days following the close of each month or

quarter, respectively.

tax returns are filed 20 days after theclose of each month;

For monthly withholding tax returns (expanded,final and withholding tax on compensation), andwithholding VAT returns (if applicable), thedeadline for filing is 10 days after the end of eachmonth, except for the month of December whichis filed on or before January 15th of the following

returns, if applicable, are filed on aquarterly basis not later than 10 days after theend of each quarter.

are filed within 5 days after theclose of the month when the taxable document is

Life insurance companies are also subject to localbusiness tax which shall be paid to the localgovernment of the city or municipality where its

branches are located, not later thanJanuary 20 of each year.

Further, if the insurance company has realshall be subject to real property tax,

which may be paid in four equal installmentsduring the year, i.e. on or before March 31, June30, September 3 and December 31.

Philippines: Life insurance

General approach tocalculation of income Accounting

Allocation of income betweenshareholders and policyholders

Income attributable to shareholders is dividendsand is reported as reduction to equity.

Income attributable to premium deposits and anyother return onis reported as liability, either as dividend or interestpayable.

Calculation of investmentreturn

Calculation of investmentincome and capital gains

Interest incomecomputed under the effective interest

Gain from sale of Investment is based ondifference between the carrying amountinvestment and actual proceeds from

Capital gains tax based on tax rules arethe right column

Calculation of investmentincome and capital gains Accounting

Actuarial reserves Based on standard set of actuarial

All valuationsdividends, and all other obligations outstandingshall be made upon the net premiums basis,according to the standard adopted by the company,which standard shall be stated in its annual report

Such standard of valuationpremium, full preliminary term, any modifiedpreliminary term, or select and ultimate reservebasis, shall be according to a standard table ofmortality with interest at not more than six percentum (6%)the Insurance Commi

Acquisition expenses Expensed as incurred.

Gains and losses oninvestments

Recognised

Gain and lossesthe difference between the carrying amount of theinvestment and actual proceeds from the sale.

Reserves against market losseson investments

Gains/ losses arising from fair valueavailableforto equity.

Losses/gains on financial assets at fairthrough profitincome during the period

Recognised32/39).

86

nsurance – overview (continued)

Accounting Taxation

Income attributable to shareholders is dividendsand is reported as reduction to equity.

Income attributable to premium deposits and anyother return on “investment” portion of the policyis reported as liability, either as dividend or interest

Taxation will follow accounting allocation.

Interest income on investment in securities iscomputed under the effective interest method.

Gain from sale of Investment is based on thedifference between the carrying amount of theinvestment and actual proceeds from the sale.

Capital gains tax based on tax rules are discussed inthe right column below.

Same as for general insurance.

Accounting Taxation

Based on standard set of actuarial assumptions.

valuations of policies, additions thereto, unpaiddividends, and all other obligations outstandingshall be made upon the net premiums basis,according to the standard adopted by the company,which standard shall be stated in its annual report.

Such standard of valuation, whether of the net levelpremium, full preliminary term, any modifiedpreliminary term, or select and ultimate reservebasis, shall be according to a standard table ofmortality with interest at not more than six per

(6%) compound interest as mandated bythe Insurance Commission.

Additions required by law to reserve funddeductible in the year incurred and classifiedpart of direct cost of life insurance

The released reserves are taxable asyear of actual release (Sec.

Expensed as incurred. Deductible.

ised when investments are sold or disposed.

and losses from sale of Investment is based onthe difference between the carrying amount of theinvestment and actual proceeds from the sale.

The recognition of gains/losses should ariseclosed and completed transaction.

Thus, gains/losses are taxable/deducrealised.

losses arising from fair value changes offorsale securities are charged /credited

Losses/gains on financial assets at fair valuethrough profit or loss are directly treated as part ofincome during the period.

ised based on PAS 32/39 (similar to IAS

Not deductible.

Taxation will follow accounting allocation.

Same as for general insurance.

Additions required by law to reserve funds aredeductible in the year incurred and classified aspart of direct cost of life insurance companies.

he released reserves are taxable as income in theyear of actual release (Sec. 37(A), Tax Code).

The recognition of gains/losses should arise from aclosed and completed transaction.

Thus, gains/losses are taxable/deductible when

Philippines: Life insurance

Calculation of investmentincome and capital gains Accounting

Dividend income Dividend income is recognwhen the right to receive the payment isestablished

Policyholder bonuses Reported as part of benefit payments

Other special deductions None.

Reinsurance Accounting

Reinsurance premiums andclaims

Recorded as reinsurance assets and

Premiums and claims on assumed reinsurance arerecognisedmanner as if the reinsurance were considereddirect business

Related premiumsincome as reinsurancethe gross insurance premium.

Mutual companies/stock companies Accounting

Mutual Companies Any domestic stock life insurance companybusiness in the Philippines mayan incorporated mutualmay provide andacquisition of thestock for the benefit of its policyholders, or anyclass or classes of its policyholders, by complyingwith the specific requirements of theCode (Section 262 of the

Once the corporation is conducted forbenefit, ratclasses for whose benefit theshall have power toa reserve basis subject to all provisions of lawapplicable to incorporated life insurersnonassessable policies on aso issued may beparticipationand the insured (Section 266 of the InsuranceCode).

Accounted in the same principles as tapplicable to common insuranceaccordance with PFRS.

87

nsurance – overview (continued)

Accounting Taxation

Dividend income is recognised in profit or lossright to receive the payment is

established.

Generally taxable at 3

However, dividends received by a domesticresident foreign insurance corporationdomestic corporation are exempt fromTax Code).

Reported as part of benefit payments when due. Deductible for RCIT purposes. May also bedeductible for MCIT purposes if the sameas benefits granted to

Only investment expenses relating to investmentincome that has not been subjected to final taxshall be allowed as deduction to arrive at thetaxable income. However, it cannot form part of thedirect cost (RMC 59

Accounting Taxation

Recorded as reinsurance assets and liabilities.

Premiums and claims on assumed reinsurance areised as income and expenses in the same

manner as if the reinsurance were considereddirect business.

Related premiums are recorded in a statement ofincome as reinsurance premium or deducted from

insurance premium.

Reinsurance assumed (net of returcancellations) is tlosses, maturities and benefits net of reinsurancerecoveries form part of direct cost thus,in the year incurred for income tax

Accounting Taxation

Any domestic stock life insurance company doingbusiness in the Philippines may convert itself intoan incorporated mutual life insurer. To that end itmay provide and carry out a plan for theacquisition of the outstanding shares of its capital

the benefit of its policyholders, or anyor classes of its policyholders, by complying

with the specific requirements of the InsuranceCode (Section 262 of the Insurance Code).

Once the corporation is conducted for mutualfit, ratably, of its policyholders of the class or

classes for whose benefit the stock was acquired, itshall have power to issue nonassessable policies on

basis subject to all provisions of lawapplicable to incorporated life insurers issuing

assessable policies on a reserve basis. Policiesso issued may be upon the basis of full or partialparticipation therein as agreed between the insurerthe insured (Section 266 of the Insurance

Accounted in the same principles as thoseapplicable to common insurance companies and inaccordance with PFRS.

Subject to income tax but exempt from premiumtax and DST if purely cooperative company

Generally taxable at 30%.

However, dividends received by a domestic orresident foreign insurance corporation from adomestic corporation are exempt from tax (Sec. 28,

Deductible for RCIT purposes. May also bedeductible for MCIT purposes if the same qualifiesas benefits granted to policyholders.

Only investment expenses relating to investmentincome that has not been subjected to final taxshall be allowed as deduction to arrive at thetaxable income. However, it cannot form part of the

st (RMC 592008).

Reinsurance assumed (net of returns,cancellations) is taxable. Ceded reinsurance, claimslosses, maturities and benefits net of reinsurance

part of direct cost thus, deductiblein the year incurred for income tax purposes.

Subject to income tax but exempt from premiumand DST if purely cooperative company.

Philippines: Life insurance

Further corporate taxfeatures Taxation

Loss carryovers Net operating loss of the business for any taxable year immediatelywhich had not been previously offset as deduction from gross income shallfrom gross income

Any loss incurred in a taxable year duringallowed as a deduction

Foreign branch income Generally, taxable. The tax paid overseas is creditable.

Domestic branch income Combined with head office income and taxed at normal corporate income tax rates

However, premiums earned may be subjected to varying lgenerated by the branches located in various cities and/or municipalities.

Corporate tax rate 30% RCITwhichever is higher.

Note that MCIT shall only be applicableyear in which such corporation commenced its business operations.

Policyholder taxation Taxation

Premium taxes 2% of the totalcompanies or associationsCode).

Premiums on health and accident insurance received by a nonas premium on life insurance, therefore, likewise subject to the 2% premium tax (RMC 59

Capital taxes and taxes onsecurities

On the sale ofgain) plus 10%((Sec. 27 (D), Tax Code). However, sale of shares of stock lshall be subject to 1/2 of 1% percentage tax

Captive insurance companies No special treatment.

Value added tax (VAT) Insurance and reinsurance commissions, repaid to a life insurance company are subject to 12% VAT (RMC 59

Management fees, rental income, or income earned by a life insurance company from services which canbe pursued independently of t

88

nsurance – other tax features

Net operating loss of the business for any taxable year immediately proceeding the currentwhich had not been previously offset as deduction from gross income shallfrom gross income for the next 3 consecutive taxable years immediately following the year of such loss.

Any loss incurred in a taxable year during which the taxpayer was exempt from income tax shall not beallowed as a deduction (Sec. 34(D)(3), Tax Code).

Generally, taxable. The tax paid overseas is creditable.

Combined with head office income and taxed at normal corporate income tax rates

However, premiums earned may be subjected to varying local business tax rates if suchgenerated by the branches located in various cities and/or municipalities.

which is based on taxable net income or 2% MCIT which is based on taxable gross income,whichever is higher.

Note that MCIT shall only be applicable beginning on the fourth taxable year immediately following theyear in which such corporation commenced its business operations.

% of the total premium collected from every person, company or corporationcompanies or associations, doing life insurance business of any sort in the Philippines. (Sec. 123, Tax

Premiums on health and accident insurance received by a nonlife insurance company shall be consideredas premium on life insurance, therefore, likewise subject to the 2% premium tax (RMC 59

the sale of shares of stock not traded in the stock exchange, a final tax of 5% () plus 10%(for gains in excess of P100,000) on the net capital gains real

(Sec. 27 (D), Tax Code). However, sale of shares of stock listed and traded though the local stock exchangeshall be subject to 1/2 of 1% percentage tax (Sec. 127 (A), Tax Code).

No special treatment.

Insurance and reinsurance commissions, reinsurance fees, reinstatement fees, renewal fees, and penaltiespaid to a life insurance company are subject to 12% VAT (RMC 592008; RR 4

Management fees, rental income, or income earned by a life insurance company from services which canbe pursued independently of the insurance business activity are also subject to 12% VAT.

roceeding the current taxable year,which had not been previously offset as deduction from gross income shall be carried over as a deduction

immediately following the year of such loss.

which the taxpayer was exempt from income tax shall not be

Combined with head office income and taxed at normal corporate income tax rates. (RCIT or MCIT)

ocal business tax rates if such premiums weregenerated by the branches located in various cities and/or municipalities.

MCIT which is based on taxable gross income,

beginning on the fourth taxable year immediately following the

premium collected from every person, company or corporation, except purely cooperativethe Philippines. (Sec. 123, Tax

life insurance company shall be consideredas premium on life insurance, therefore, likewise subject to the 2% premium tax (RMC 592008).

final tax of 5% (on the first P100,000net capital gains realised during the taxable year

and traded though the local stock exchange

statement fees, renewal fees, and penalties2008; RR 42007).

Management fees, rental income, or income earned by a life insurance company from services which canhe insurance business activity are also subject to 12% VAT.

Malou P. LimPartner, TaxTel: +63 2 459 2016Email: [email protected]

Roderick DanaoPartner, AssuranceTel: +63 2 459 3065Email: [email protected]

Philippines: Life insurance

Other tax features Taxation

Premium taxes 2% of the total premium collected from every person, company or corporationcompanies or associationsCode).

Premiums on health and accident insurance received by a nonas premium on life insurance,

Capital taxes and taxes onsecurities

On the sale of shares of stock not traded in the stock exchange, again) plus 10%((Sec. 27 (D), Tax Code). However, sale of shares of stock listedshall be subject to 1/2 of 1% percentage tax

Captive insurance companies No special treatment.

Value added tax (VAT) Insurance and reinsurance commissions, repaid to a life insurance company are subject to 12% VAT (RMC 59

Management fees, rental income, or income earned by a life insurance company from services which canbe pursued independently of the insurance business activity are also subject to 12% VAT.

Contact persons Philippines

89

nsurance – other tax features

% of the total premium collected from every person, company or corporationcompanies or associations, doing life insurance business of any sort in the Philippines. (Sec. 123, Tax

Premiums on health and accident insurance received by a nonlife insurance company shall be consideredas premium on life insurance, therefore, likewise subject to the 2% premium tax (RMC 59

the sale of shares of stock not traded in the stock exchange, a final tax of 5% () plus 10%(for gains in excess of P100,000) on the net capital gains real

(Sec. 27 (D), Tax Code). However, sale of shares of stock listed and traded though the local stock exchangeshall be subject to 1/2 of 1% percentage tax (Sec. 127 (A), Tax Code).

No special treatment.

Insurance and reinsurance commissions, reinsurance fees, reinstatement fees, renewal fees, and penaltiespaid to a life insurance company are subject to 12% VAT (RMC 592008; RR 4

agement fees, rental income, or income earned by a life insurance company from services which canbe pursued independently of the insurance business activity are also subject to 12% VAT.

Philippines

% of the total premium collected from every person, company or corporation, except purely cooperativethe Philippines. (Sec. 123, Tax

life insurance company shall be consideredtherefore, likewise subject to the 2% premium tax (RMC 592008).

final tax of 5% (on the first P100,000net capital gains realised during the taxable year

and traded though the local stock exchange

insurance fees, reinstatement fees, renewal fees, and penalties2008; RR 42007).

agement fees, rental income, or income earned by a life insurance company from services which canbe pursued independently of the insurance business activity are also subject to 12% VAT.