Philippine IT-BPO Road Map 2016: Driving to Global Leaderships3.amazonaws.com/zanran_storage/ ·...

25

Philippine IT-BPO Road Map 2016: Driving to Global Leadership Funded by the Commission on Information and Communications Technology (CICT)/Office of the President IT-BPO = information technology and business process outsourcing Commissioned by the Business Processing Association of the Philippines (BPAP and partner associations)

Transcript of Philippine IT-BPO Road Map 2016: Driving to Global Leaderships3.amazonaws.com/zanran_storage/ ·...

Philippine IT-BPO Road Map 2016: Driving to Global Leadership

Funded by the Commission on Information and Communications Technology (CICT)/Office of the President

ITBPO = information technology and business process outsourcing

Commissioned by the Business Processing Association of the Philippines (BPAP and partner associations)

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.2

Contents

Road Map 2016 study overview

Philippine ITBPO industry: current state and competitive positioning

Global market trends in ITBPO and target for Road Map 2016

Initiatives to achieve Road Map 2016

Call to action and publicprivate partnership

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.3

Road Map 2016 is based on a robust fact-base and insights from multiple sources

Workshops with leadership and

members of BPAP and partner associations

Survey of 200+ companies across Philippine ITBPO

industry

Best practices and learnings from initiatives of other destinations

Inputs from global industry experts,

analysts, investors, and customers

Role of BPAP

Ecosystem

Marketing and Branding

Talent

Road Map2016

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.4

The study is an inclusive exercise, incorporating perspectives from over 60 stakeholders within the Philippines

BPAP and partner associations

Industry participantsShared Services and Global

SuppliersPhilippinesbased

Industry enablers

Government agencies

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.5

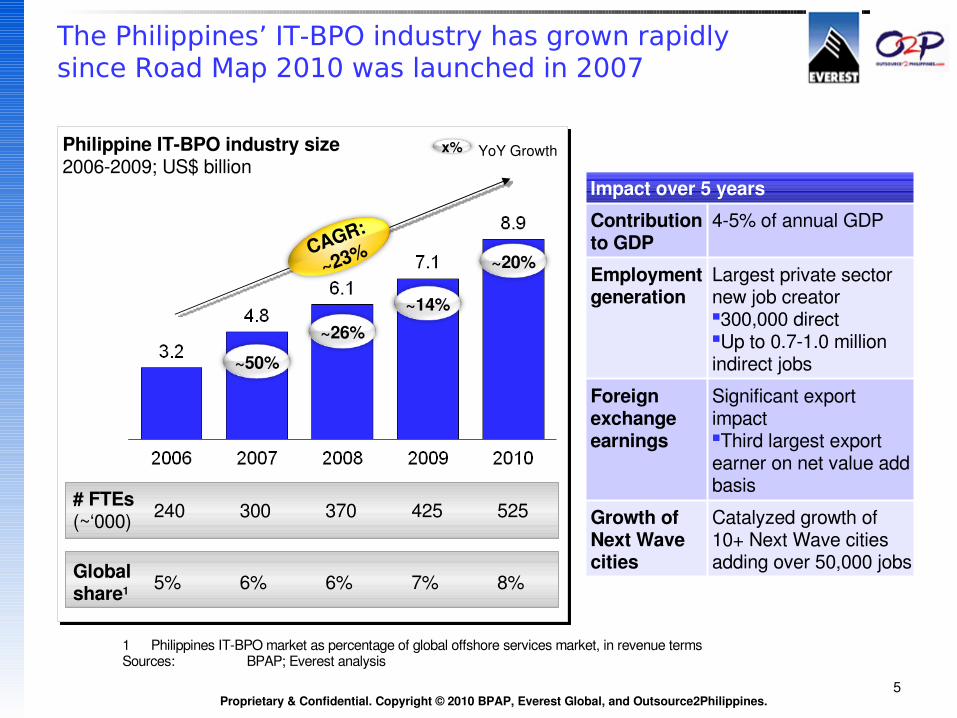

The Philippines’ IT-BPO industry has grown rapidly since Road Map 2010 was launched in 2007

Philippine ITBPO industry size20062009; US$ billion

x% YoY Growth

1 Philippines ITBPO market as percentage of global offshore services market, in revenue termsSources: BPAP; Everest analysis

# FTEs(~‘000) 240 300 370 425 525

Global share1 5% 6% 6% 7% 8%

Impact over 5 years

Contribution to GDP

45% of annual GDP

Employment generation

Largest private sector new job creator300,000 directUp to 0.71.0 million indirect jobs

Foreign exchange earnings

Significant export impact Third largest export earner on net value add basis

Growth of Next Wave cities

Catalyzed growth of 10+ Next Wave cities adding over 50,000 jobs

~50%

~26%~14%

~20%CAGR:

~23%

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.6

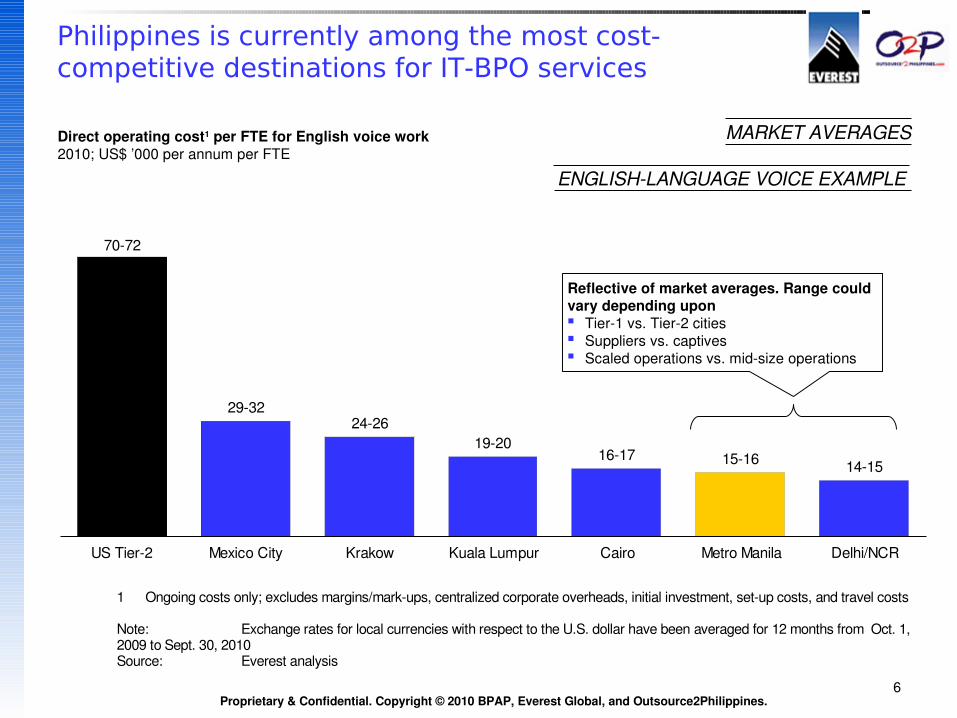

1 Ongoing costs only; excludes margins/markups, centralized corporate overheads, initial investment, setup costs, and travel costs

Note: Exchange rates for local currencies with respect to the U.S. dollar have been averaged for 12 months from Oct. 1, 2009 to Sept. 30, 2010Source: Everest analysis

Philippines is currently among the most cost-competitive destinations for IT-BPO services

29322426

19201617 1516 1415

7072

US Tier2 Mexico City Krakow Kuala Lumpur Cairo Metro Manila Delhi/NCR

Reflective of market averages. Range could vary depending upon Tier1 vs. Tier2 cities Suppliers vs. captives Scaled operations vs. midsize operations

Direct operating cost1 per FTE for English voice work2010; US$ ’000 per annum per FTE

MARKET AVERAGES

ENGLISHLANGUAGE VOICE EXAMPLE

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.7

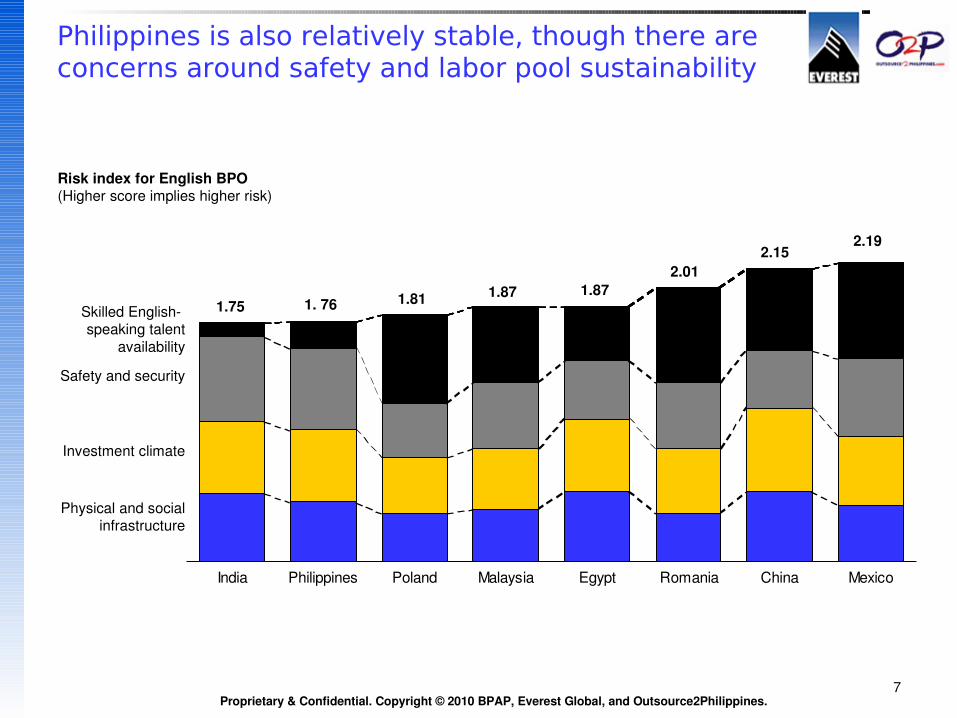

India Philippines Poland Malaysia Egypt Romania China Mexico

Philippines is also relatively stable, though there are concerns around safety and labor pool sustainability

Skilled English speaking talent

availability

Safety and security

Investment climate

Risk index for English BPO(Higher score implies higher risk)

Physical and social infrastructure

1.751.871.811. 76

1.872.01

2.152.19

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.8

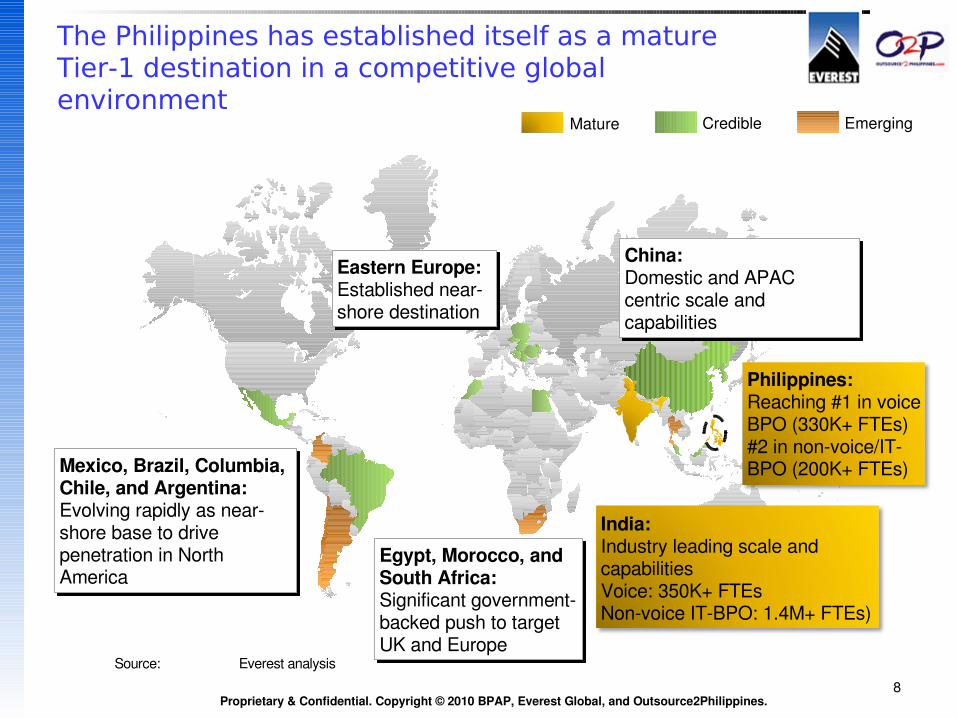

The Philippines has established itself as a mature Tier-1 destination in a competitive global environment

Mature Credible Emerging

Eastern Europe: Established nearshore destination

China:Domestic and APAC centric scale and capabilities

Mexico, Brazil, Columbia, Chile, and Argentina: Evolving rapidly as nearshore base to drive penetration in North America

Philippines: Reaching #1 in voice BPO (330K+ FTEs)#2 in nonvoice/ITBPO (200K+ FTEs)

India: Industry leading scale and capabilities Voice: 350K+ FTEsNonvoice ITBPO: 1.4M+ FTEs)

Egypt, Morocco, and South Africa: Significant governmentbacked push to target UK and Europe

Source: Everest analysis

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.9

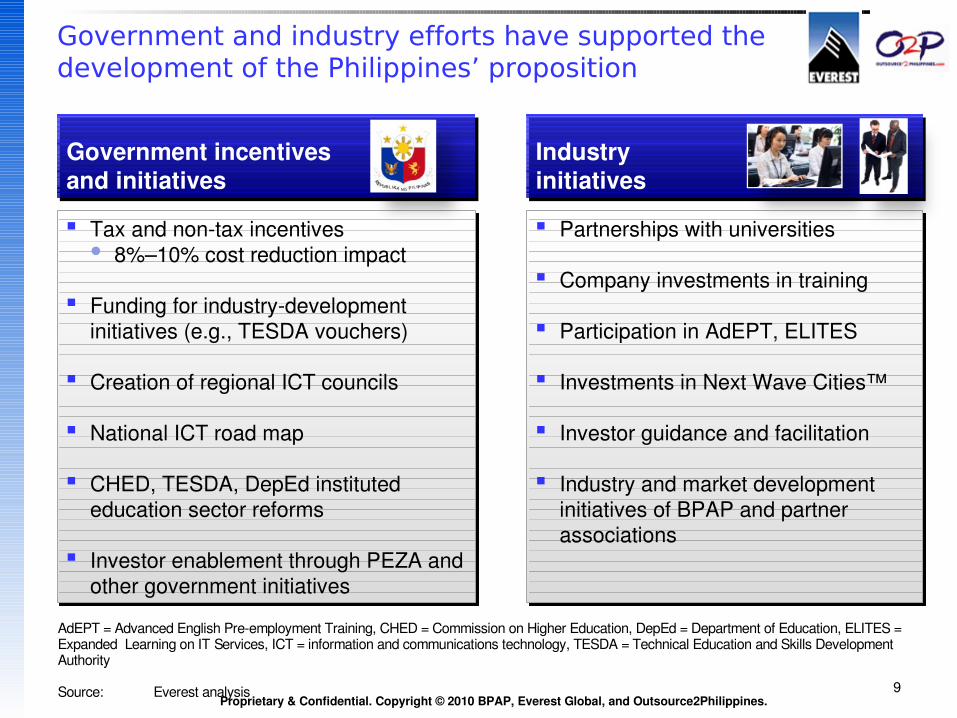

Government and industry efforts have supported the development of the Philippines’ proposition

Government incentives and initiatives

Industry initiatives

Partnerships with universities

Company investments in training

Participation in AdEPT, ELITES

Investments in Next Wave Cities™

Investor guidance and facilitation

Industry and market development initiatives of BPAP and partner associations

Tax and nontax incentives 8%–10% cost reduction impact

Funding for industrydevelopment initiatives (e.g., TESDA vouchers)

Creation of regional ICT councils

National ICT road map

CHED, TESDA, DepEd instituted education sector reforms

Investor enablement through PEZA and other government initiatives

AdEPT = Advanced English Preemployment Training, CHED = Commission on Higher Education, DepEd = Department of Education, ELITES = Expanded Learning on IT Services, ICT = information and communications technology, TESDA = Technical Education and Skills Development Authority

Source: Everest analysis

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.10

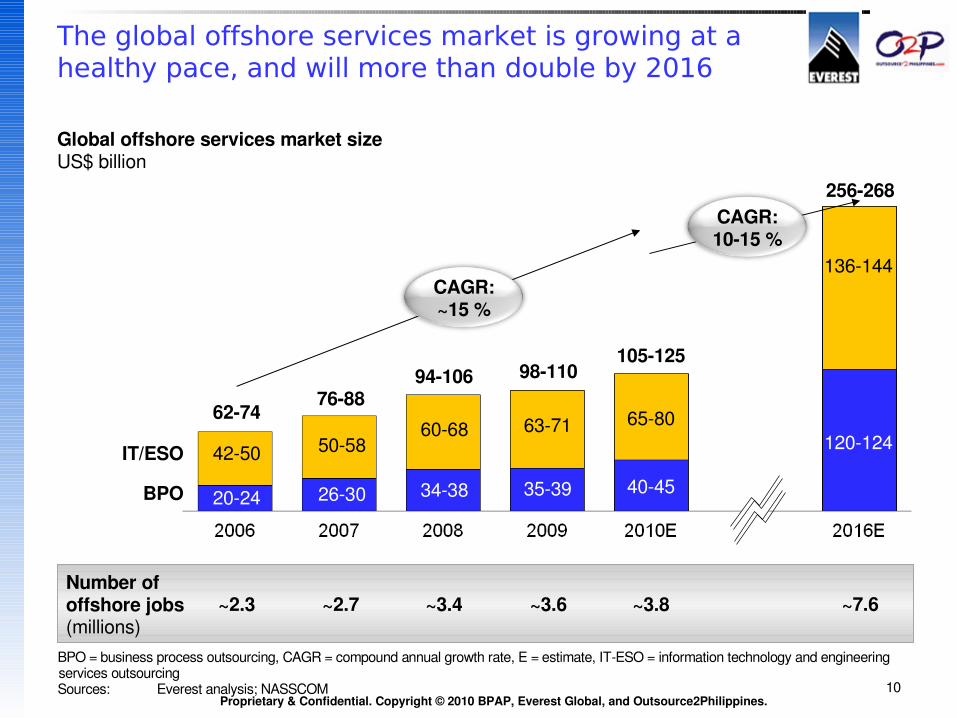

The global offshore services market is growing at a healthy pace, and will more than double by 2016

BPO = business process outsourcing, CAGR = compound annual growth rate, E = estimate, ITESO = information technology and engineering services outsourcingSources: Everest analysis; NASSCOM

Global offshore services market sizeUS$ billion

~2.3 ~2.7 ~3.4 ~3.6 ~7.6Number ofoffshore jobs(millions)

~3.8

62747688

94106 98110

256268

IT/ESO

BPO 2024

4250

2630

5058

3438

6068

3539

6371120124

136144

105125

4045

6580

CAGR:~15 %

CAGR:1015 %

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.11

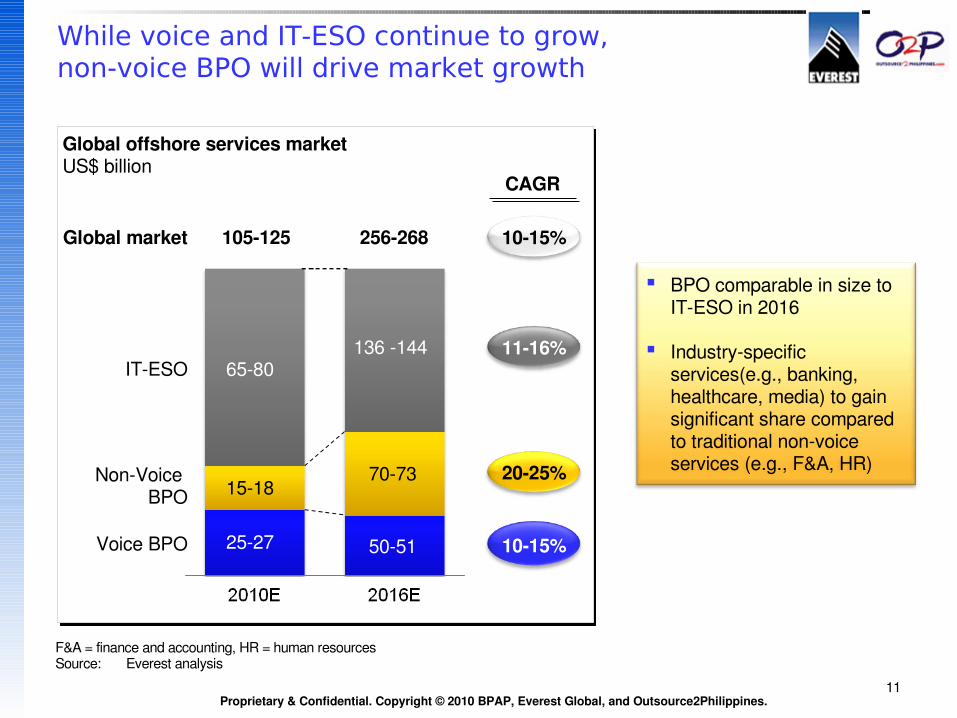

While voice and IT-ESO continue to grow, non-voice BPO will drive market growth

Global offshore services marketUS$ billion

1015%

2025%

1116%

2527 5051

105125

6580

7073

1015%256268

136 144 ITESO

1518

Voice BPO

NonVoice BPO

Global market

CAGR

BPO comparable in size to ITESO in 2016

Industryspecific services(e.g., banking, healthcare, media) to gain significant share compared to traditional nonvoice services (e.g., F&A, HR)

F&A = finance and accounting, HR = human resourcesSource: Everest analysis

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.12

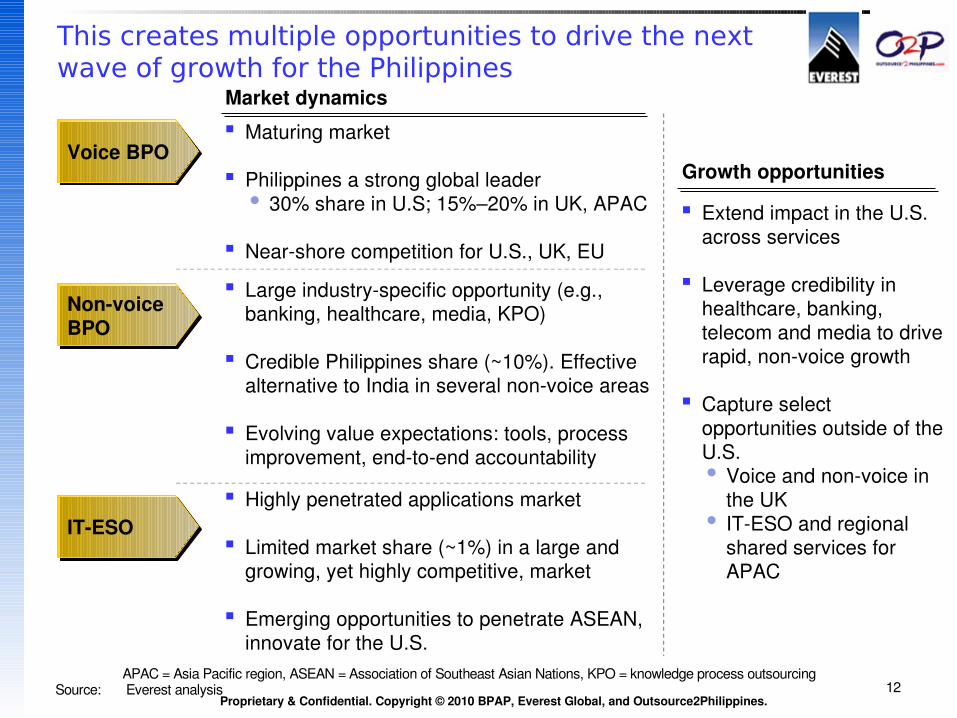

This creates multiple opportunities to drive the next wave of growth for the Philippines

Voice BPO

Nonvoice BPO

ITESO

Market dynamics Maturing market

Philippines a strong global leader 30% share in U.S; 15%–20% in UK, APAC

Nearshore competition for U.S., UK, EU

Large industryspecific opportunity (e.g., banking, healthcare, media, KPO)

Credible Philippines share (~10%). Effective alternative to India in several nonvoice areas

Evolving value expectations: tools, process improvement, endtoend accountability

Highly penetrated applications market

Limited market share (~1%) in a large and growing, yet highly competitive, market

Emerging opportunities to penetrate ASEAN, innovate for the U.S.

Growth opportunities

Extend impact in the U.S. across services

Leverage credibility in healthcare, banking, telecom and media to drive rapid, nonvoice growth

Capture select opportunities outside of the U.S. Voice and nonvoice in

the UK ITESO and regional

shared services for APAC

APAC = Asia Pacific region, ASEAN = Association of Southeast Asian Nations, KPO = knowledge process outsourcingSource: Everest analysis

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.13

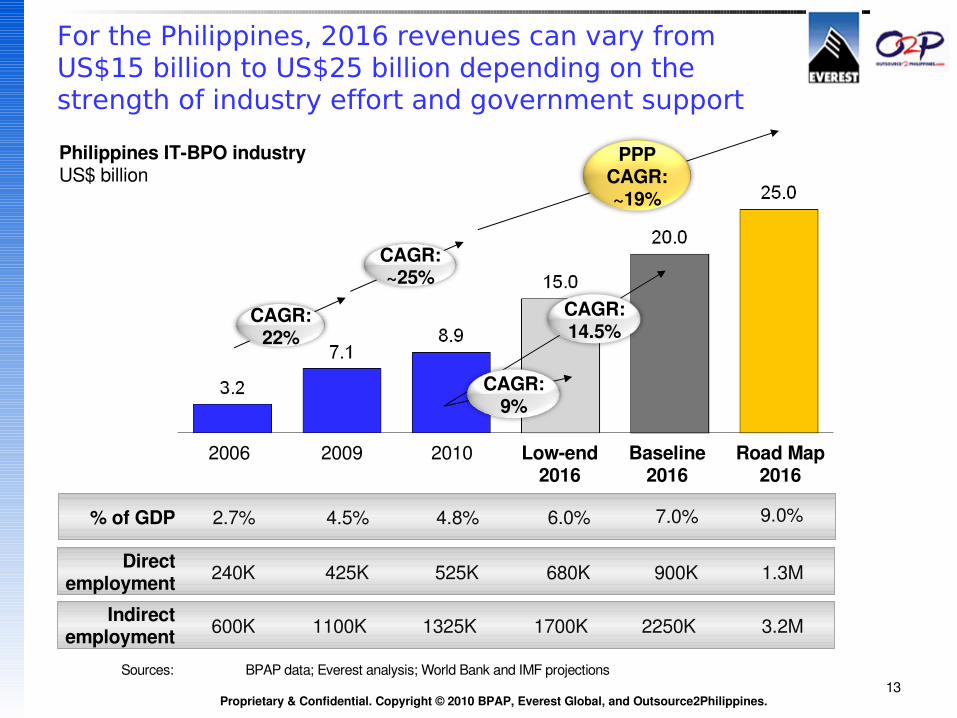

For the Philippines, 2016 revenues can vary from US$15 billion to US$25 billion depending on the strength of industry effort and government support

Philippines ITBPO industryUS$ billion

Sources: BPAP data; Everest analysis; World Bank and IMF projections

1325K 2250KIndirect employment 600K 1100K 3.2M

% of GDP 2.7% 4.8% 7.0%4.5% 9.0%

1700K

6.0%

2006 20102009 Road Map 2016

Baseline 2016

CAGR: 22%

CAGR: ~25%

CAGR: 14.5%

PPPCAGR: ~19%

Lowend 2016

CAGR: 9%

525K 900KDirect employment 240K 425K 1.3M680K

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.14

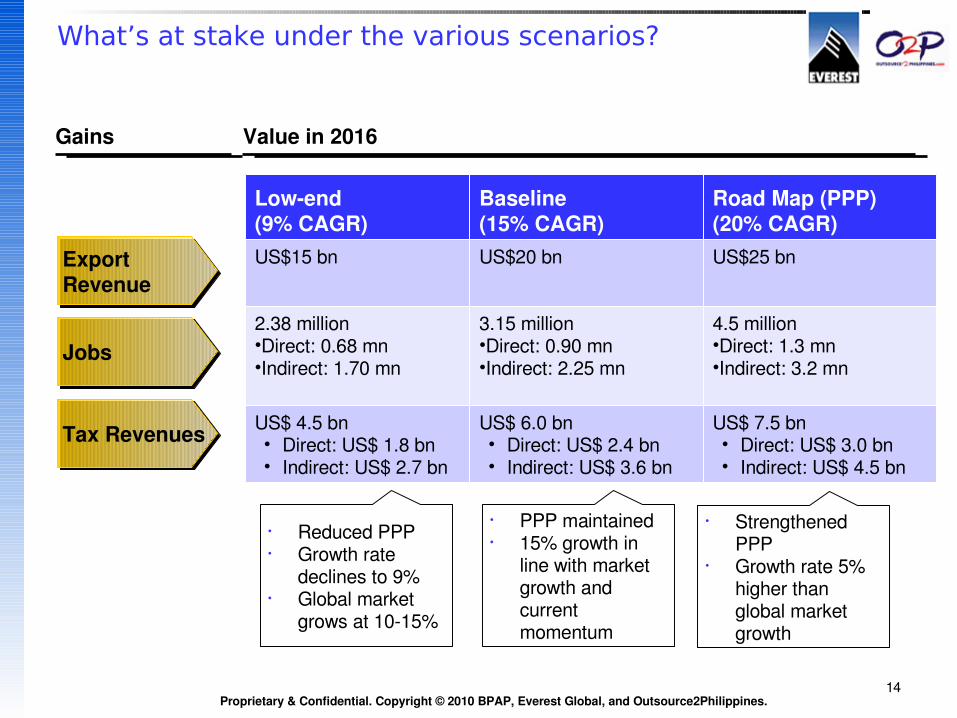

What’s at stake under the various scenarios?

Jobs

Export Revenue

Tax Revenues

Lowend(9% CAGR)

Baseline(15% CAGR)

Road Map (PPP)(20% CAGR)

US$15 bn US$20 bn US$25 bn

2.38 million•Direct: 0.68 mn•Indirect: 1.70 mn

3.15 million•Direct: 0.90 mn•Indirect: 2.25 mn

4.5 million•Direct: 1.3 mn•Indirect: 3.2 mn

US$ 4.5 bn • Direct: US$ 1.8 bn• Indirect: US$ 2.7 bn

US$ 6.0 bn• Direct: US$ 2.4 bn• Indirect: US$ 3.6 bn

US$ 7.5 bn• Direct: US$ 3.0 bn • Indirect: US$ 4.5 bn

Gains Value in 2016

• Reduced PPP• Growth rate

declines to 9%• Global market

grows at 1015%

• PPP maintained • 15% growth in

line with market growth and current momentum

• Strengthened PPP

• Growth rate 5% higher than global market growth

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.15

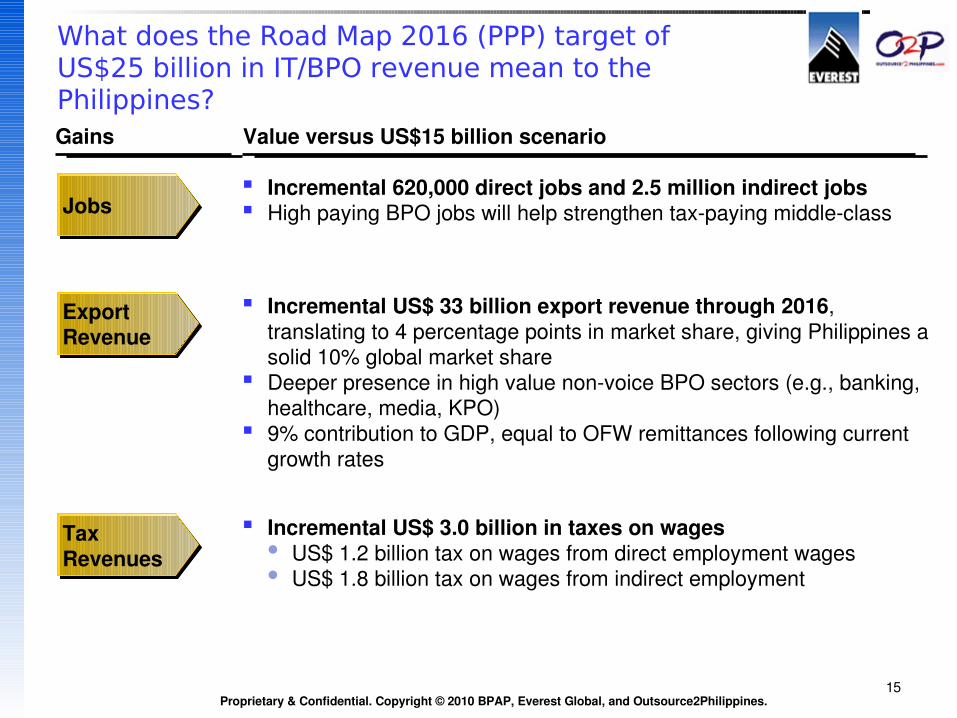

What does the Road Map 2016 (PPP) target of US$25 billion in IT/BPO revenue mean to the Philippines?

Jobs

Export Revenue

Tax Revenues

Gains Value versus US$15 billion scenario

Incremental 620,000 direct jobs and 2.5 million indirect jobs High paying BPO jobs will help strengthen taxpaying middleclass

Incremental US$ 33 billion export revenue through 2016, translating to 4 percentage points in market share, giving Philippines a solid 10% global market share

Deeper presence in high value nonvoice BPO sectors (e.g., banking, healthcare, media, KPO)

9% contribution to GDP, equal to OFW remittances following current growth rates

Incremental US$ 3.0 billion in taxes on wages US$ 1.2 billion tax on wages from direct employment wages US$ 1.8 billion tax on wages from indirect employment

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.16

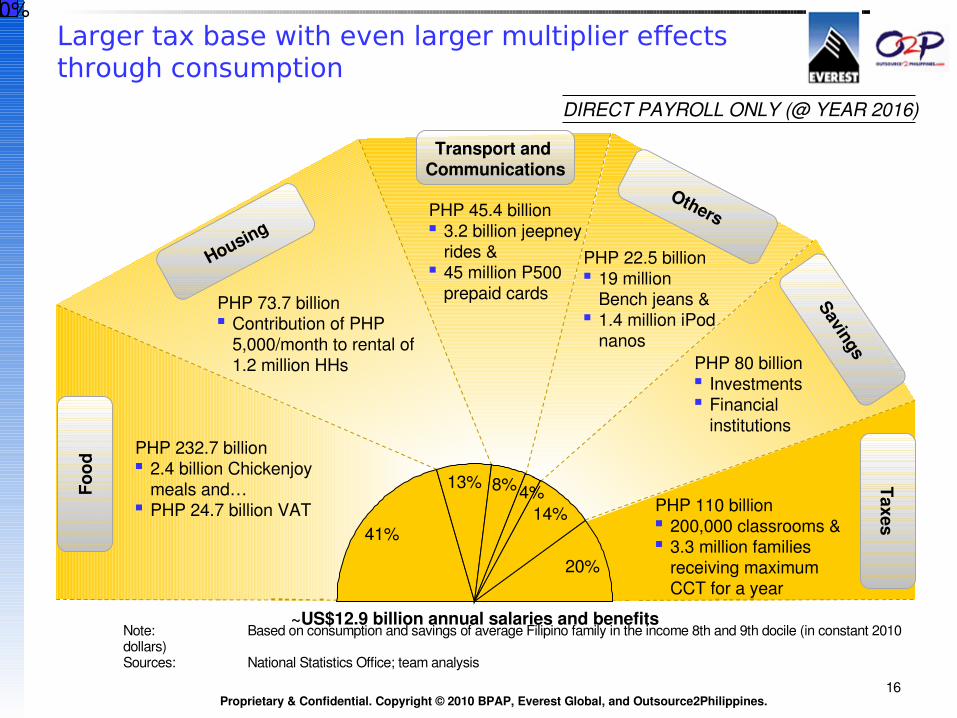

10%Larger tax base with even larger multiplier effects through consumption

Food

Housing

Transport and Communications

Others

Savings

Taxes

PHP 22.5 billion 19 million

Bench jeans & 1.4 million iPod

nanosPHP 80 billion Investments Financial

institutions

PHP 73.7 billion Contribution of PHP

5,000/month to rental of 1.2 million HHs

PHP 232.7 billion 2.4 billion Chickenjoy

meals and… PHP 24.7 billion VAT PHP 110 billion

200,000 classrooms & 3.3 million families

receiving maximum CCT for a year

PHP 45.4 billion 3.2 billion jeepney

rides & 45 million P500

prepaid cards

Note: Based on consumption and savings of average Filipino family in the income 8th and 9th docile (in constant 2010 dollars) Sources: National Statistics Office; team analysis

~US$12.9 billion annual salaries and benefits

DIRECT PAYROLL ONLY (@ YEAR 2016)

41%

13% 8%4%14%

20%

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.17

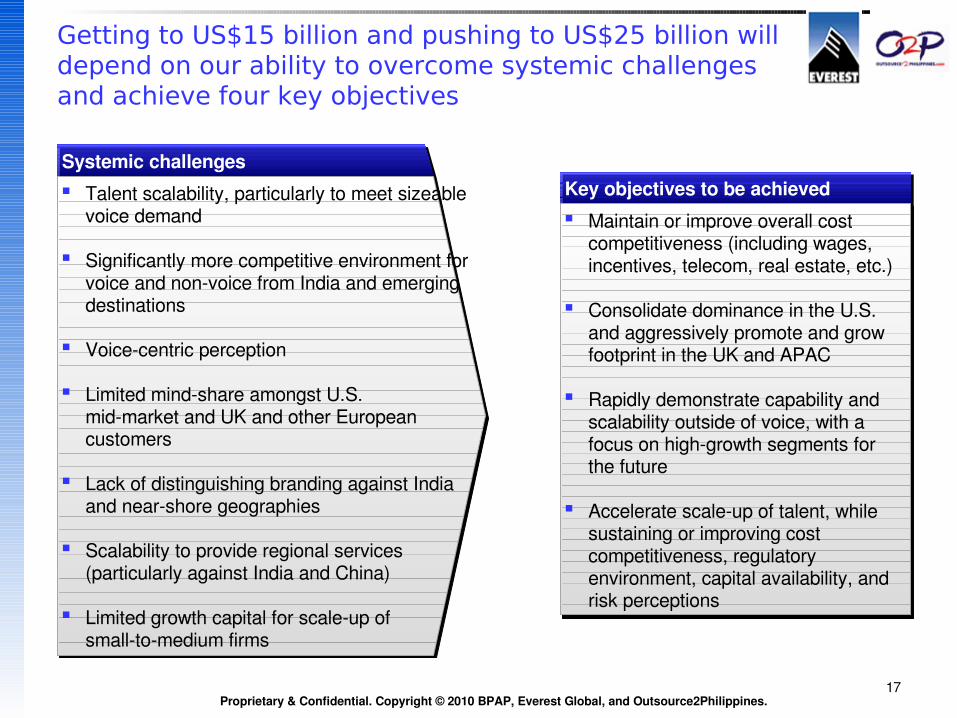

Getting to US$15 billion and pushing to US$25 billion will depend on our ability to overcome systemic challenges and achieve four key objectives

Systemic challengesKey objectives to be achieved Talent scalability, particularly to meet sizeable

voice demand

Significantly more competitive environment for voice and nonvoice from India and emerging destinations

Voicecentric perception

Limited mindshare amongst U.S.midmarket and UK and other European customers

Lack of distinguishing branding against India and nearshore geographies

Scalability to provide regional services (particularly against India and China)

Limited growth capital for scaleup of smalltomedium firms

Maintain or improve overall cost competitiveness (including wages, incentives, telecom, real estate, etc.)

Consolidate dominance in the U.S. and aggressively promote and grow footprint in the UK and APAC

Rapidly demonstrate capability and scalability outside of voice, with a focus on highgrowth segments for the future

Accelerate scaleup of talent, while sustaining or improving cost competitiveness, regulatory environment, capital availability, and risk perceptions

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.18

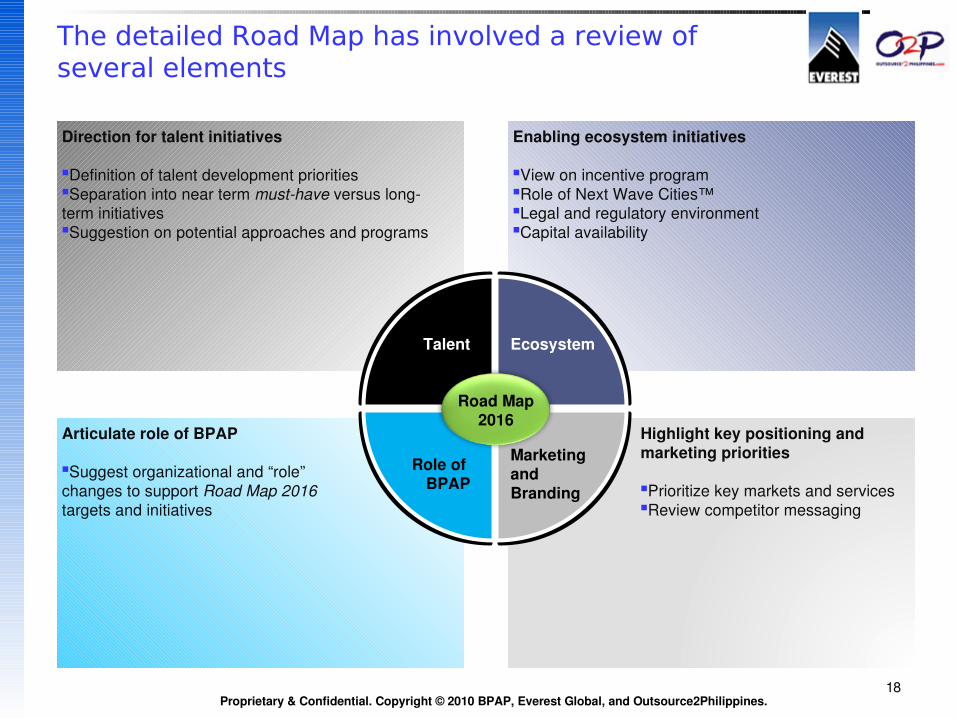

The detailed Road Map has involved a review of several elements

Direction for talent initiatives

Definition of talent development prioritiesSeparation into near term musthave versus long term initiativesSuggestion on potential approaches and programs

Articulate role of BPAP

Suggest organizational and “role” changes to support Road Map 2016 targets and initiatives

Enabling ecosystem initiatives

View on incentive programRole of Next Wave Cities™Legal and regulatory environmentCapital availability

Road Map2016

Highlight key positioning and marketing priorities

Prioritize key markets and servicesReview competitor messaging

Role of BPAP

Ecosystem

Marketing and Branding

Talent

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.19

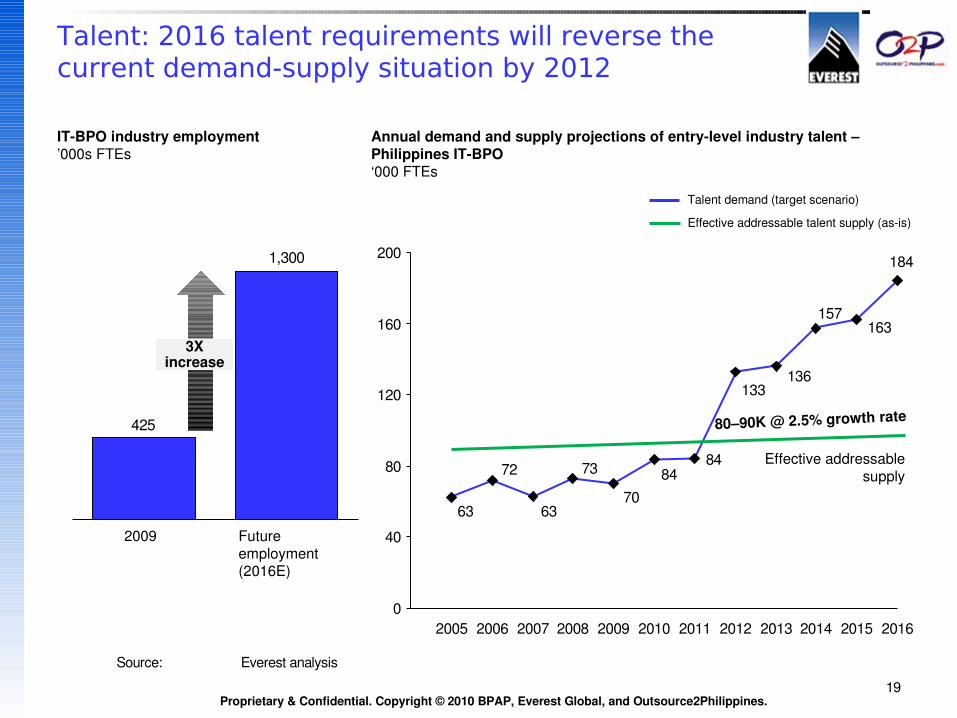

Talent: 2016 talent requirements will reverse the current demand-supply situation by 2012

84

184

163

63

72

63

73

7084

133136

157

0

40

80

120

160

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

80–90K @ 2.5% growth rate

Effective addressable supply

425

1,300

2009 Future employment (2016E)

3Xincrease

ITBPO industry employment’000s FTEs

Annual demand and supply projections of entrylevel industry talent – Philippines ITBPO ‘000 FTEs

Talent demand (target scenario)

Effective addressable talent supply (asis)

Source: Everest analysis

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.20

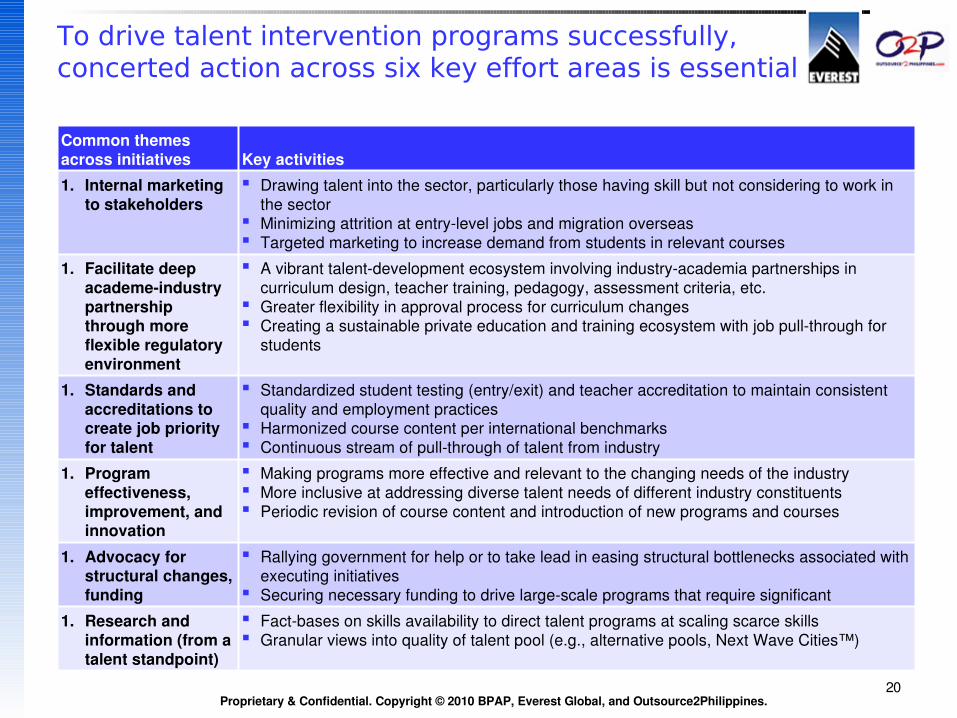

To drive talent intervention programs successfully, concerted action across six key effort areas is essential

Common themes across initiatives Key activities

1. Internal marketing to stakeholders

Drawing talent into the sector, particularly those having skill but not considering to work in the sector

Minimizing attrition at entrylevel jobs and migration overseas Targeted marketing to increase demand from students in relevant courses

1. Facilitate deep academeindustry partnership through more flexible regulatory environment

A vibrant talentdevelopment ecosystem involving industryacademia partnerships in curriculum design, teacher training, pedagogy, assessment criteria, etc.

Greater flexibility in approval process for curriculum changes Creating a sustainable private education and training ecosystem with job pullthrough for

students

1. Standards and accreditations to create job priority for talent

Standardized student testing (entry/exit) and teacher accreditation to maintain consistent quality and employment practices

Harmonized course content per international benchmarks Continuous stream of pullthrough of talent from industry

1. Program effectiveness, improvement, and innovation

Making programs more effective and relevant to the changing needs of the industry More inclusive at addressing diverse talent needs of different industry constituents Periodic revision of course content and introduction of new programs and courses

1. Advocacy for structural changes, funding

Rallying government for help or to take lead in easing structural bottlenecks associated with executing initiatives

Securing necessary funding to drive largescale programs that require significant investment 1. Research and

information (from a talent standpoint)

Factbases on skills availability to direct talent programs at scaling scarce skills Granular views into quality of talent pool (e.g., alternative pools, Next Wave Cities™)

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.21

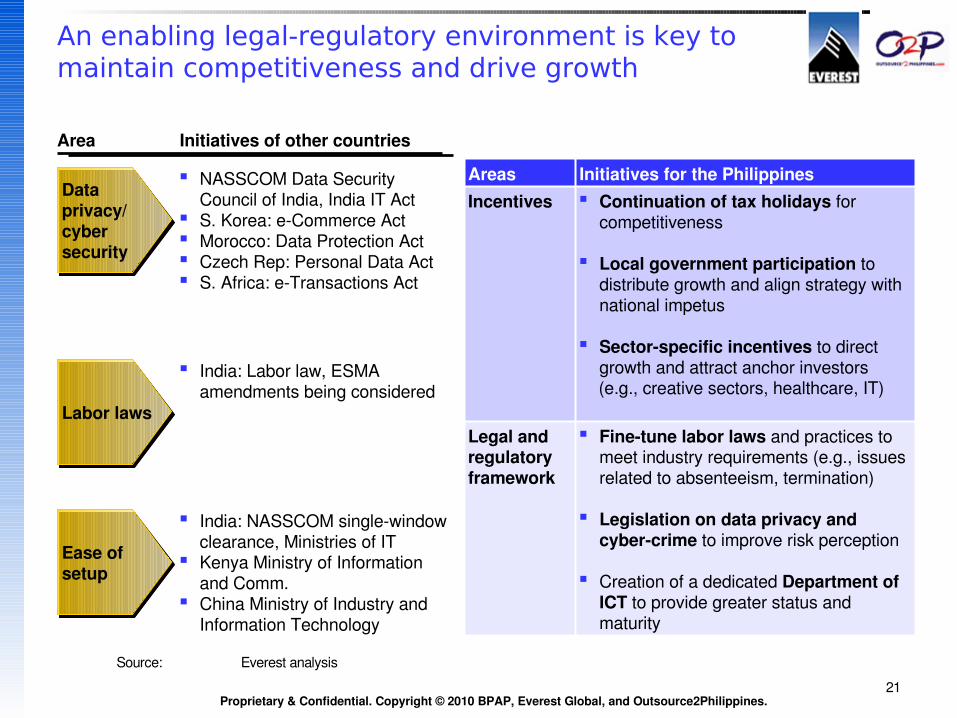

An enabling legal-regulatory environment is key to maintain competitiveness and drive growth

Initiatives of other countries

Data privacy/ cyber security

NASSCOM Data Security Council of India, India IT Act

S. Korea: eCommerce Act Morocco: Data Protection Act Czech Rep: Personal Data Act S. Africa: eTransactions Act

India: Labor law, ESMA amendments being considered

India: NASSCOM singlewindow clearance, Ministries of IT

Kenya Ministry of Information and Comm.

China Ministry of Industry and Information Technology

Labor laws

Ease of setup

Area

Source: Everest analysis

Areas Initiatives for the PhilippinesIncentives Continuation of tax holidays for

competitiveness

Local government participation to distribute growth and align strategy with national impetus

Sectorspecific incentives to direct growth and attract anchor investors

(e.g., creative sectors, healthcare, IT)

Legal and regulatory framework

Finetune labor laws and practices to meet industry requirements (e.g., issues related to absenteeism, termination)

Legislation on data privacy and cybercrime to improve risk perception

Creation of a dedicated Department of ICT to provide greater status and maturity

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.22

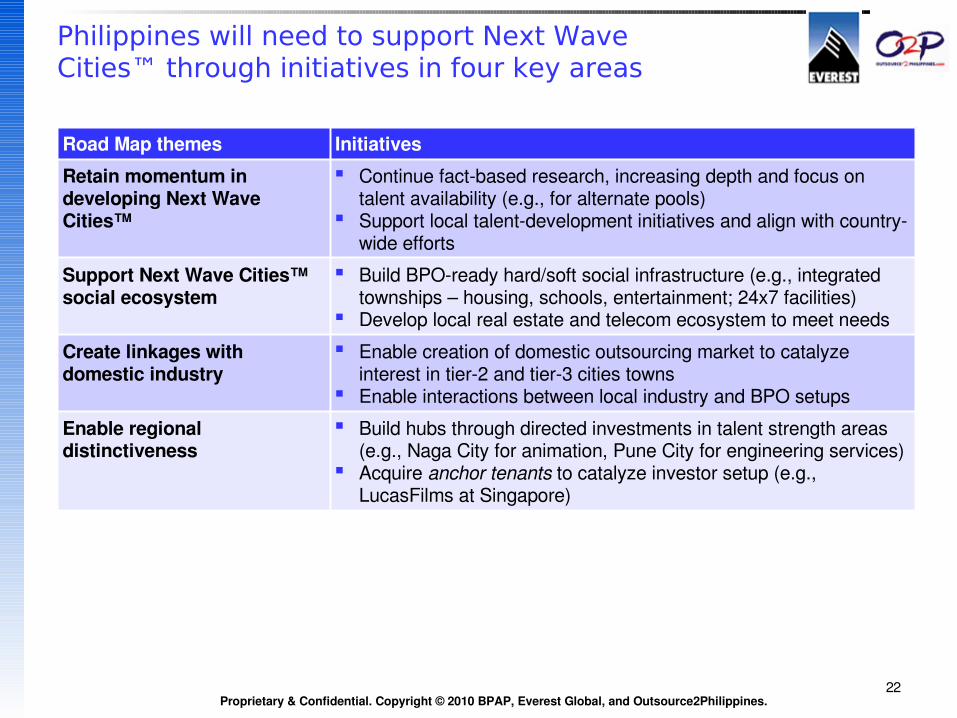

Philippines will need to support Next WaveCities™ through initiatives in four key areas

Road Map themes Initiatives

Retain momentum in developing Next Wave Cities™

Continue factbased research, increasing depth and focus on talent availability (e.g., for alternate pools)

Support local talentdevelopment initiatives and align with countrywide efforts

Support Next Wave Cities™ social ecosystem

Build BPOready hard/soft social infrastructure (e.g., integrated townships – housing, schools, entertainment; 24x7 facilities)

Develop local real estate and telecom ecosystem to meet needs

Create linkages with domestic industry

Enable creation of domestic outsourcing market to catalyze interest in tier2 and tier3 cities towns

Enable interactions between local industry and BPO setups

Enable regional distinctiveness

Build hubs through directed investments in talent strength areas (e.g., Naga City for animation, Pune City for engineering services)

Acquire anchor tenants to catalyze investor setup (e.g., LucasFilms at Singapore)

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.23

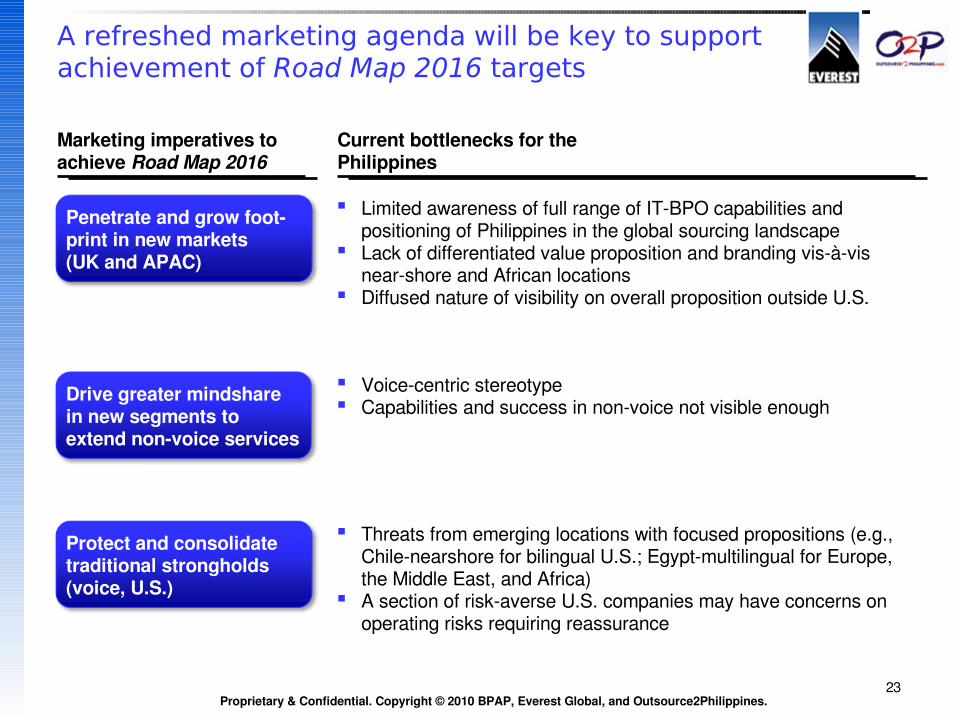

A refreshed marketing agenda will be key to support achievement of Road Map 2016 targets

Marketing imperatives to achieve Road Map 2016

Current bottlenecks for the Philippines

Penetrate and grow footprint in new markets (UK and APAC)

Limited awareness of full range of ITBPO capabilities and positioning of Philippines in the global sourcing landscape

Lack of differentiated value proposition and branding visàvis nearshore and African locations

Diffused nature of visibility on overall proposition outside U.S.

Voicecentric stereotype Capabilities and success in nonvoice not visible enough

Drive greater mindshare in new segments to extend nonvoice services

Protect and consolidate traditional strongholds (voice, U.S.)

Threats from emerging locations with focused propositions (e.g., Chilenearshore for bilingual U.S.; Egyptmultilingual for Europe, the Middle East, and Africa)

A section of riskaverse U.S. companies may have concerns on operating risks requiring reassurance

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.24

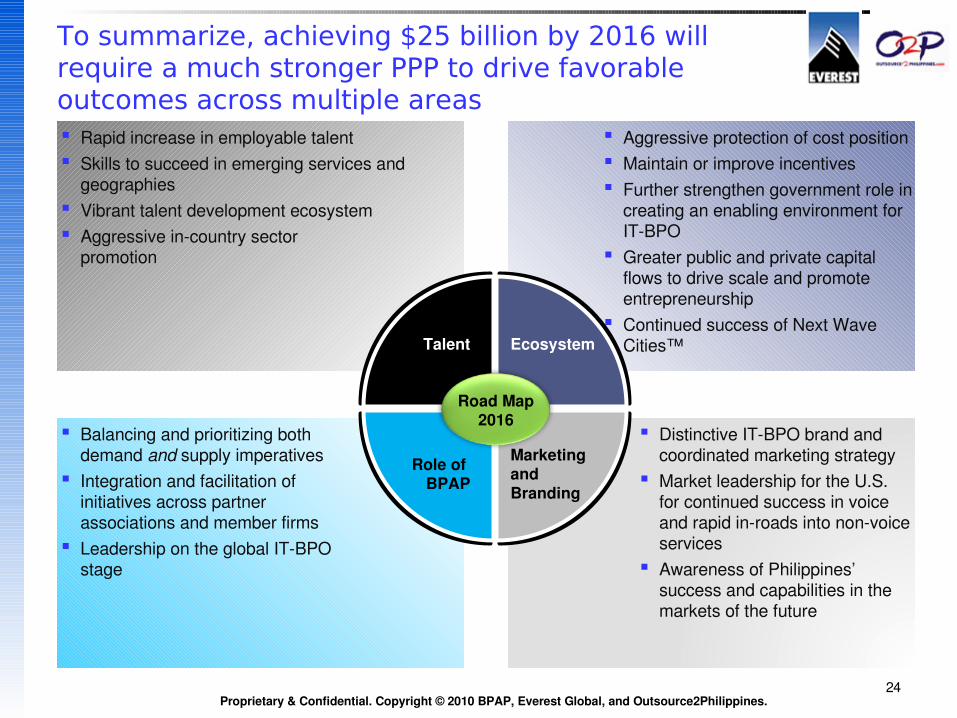

To summarize, achieving $25 billion by 2016 will require a much stronger PPP to drive favorable outcomes across multiple areas Rapid increase in employable talent Skills to succeed in emerging services and

geographies Vibrant talent development ecosystem Aggressive incountry sector

promotion

Balancing and prioritizing both demand and supply imperatives

Integration and facilitation of initiatives across partner associations and member firms

Leadership on the global ITBPO stage

Aggressive protection of cost position Maintain or improve incentives Further strengthen government role in

creating an enabling environment for ITBPO

Greater public and private capital flows to drive scale and promote entrepreneurship

Continued success of Next Wave Cities™

Road Map2016

Distinctive ITBPO brand and coordinated marketing strategy

Market leadership for the U.S. for continued success in voice and rapid inroads into nonvoice services

Awareness of Philippines’ success and capabilities in the markets of the future

Role of BPAP

Ecosystem

Marketing and Branding

Talent

Proprietary & Confidential. Copyright © 2010 BPAP, Everest Global, and Outsource2Philippines.25

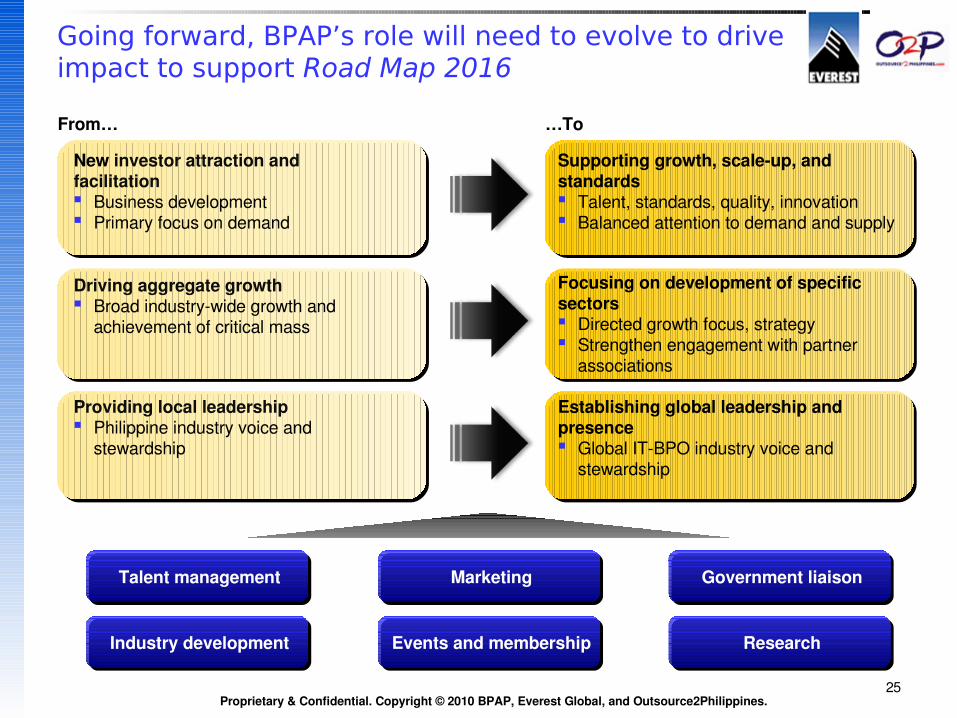

Going forward, BPAP’s role will need to evolve to drive impact to support Road Map 2016

ResearchEvents and membershipIndustry development

Marketing Government liaisonTalent management

From… …To

New investor attraction and facilitation Business development Primary focus on demand

Supporting growth, scaleup, and standards Talent, standards, quality, innovation Balanced attention to demand and supply

Driving aggregate growth Broad industrywide growth and

achievement of critical mass

Focusing on development of specific sectors Directed growth focus, strategy Strengthen engagement with partner

associations

Providing local leadership Philippine industry voice and

stewardship

Establishing global leadership and presence Global ITBPO industry voice and

stewardship