Philip Chronican Chief Financial Officer · Philip Chronican Chief Financial Officer 21 March 2002....

28

CSFB Asian Investment Conference, March 2002 1 Delivering value Philip Chronican Chief Financial Officer 21 March 2002

Transcript of Philip Chronican Chief Financial Officer · Philip Chronican Chief Financial Officer 21 March 2002....

CS

FB A

sian Investment C

onference, March 2002

1

Delivering value

Philip ChronicanChief Financial Officer21 March 2002

CS

FB A

sian Investment C

onference, March 2002

2

Disclaimer

The material contained in the following presentation is intended to be general background information on Westpac Banking Corporation and its activities as at 21 March 2002.

The information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs.

CS

FB A

sian Investment C

onference, March 2002

3

l Westpac in context

l What’s topical

l Scoping the potential

l Points of differentiation

Today’s focus

CS

FB A

sian Investment C

onference, March 2002

4

Westpac

Established 1817 and one of four majorcommercial banks in Australia

l A$190 billion in assets (30 Sept 2001)

l Market capitalisation A$28 billion

l Within the world’s top 100 banks#

# euromoney June 2001

CS

FB A

sian Investment C

onference, March 2002

5

l MarketsØ Australia, New Zealand & near Pacific

l ProductsØ Full range of corporate, business and

consumer financial services

l CustomersØ 8.2 million

l OperationsØ Multi-channel integrated distribution networkØ Willing to partner/outsource

Westpac in context

Meeting customers’ financial services needs

CS

FB A

sian Investment C

onference, March 2002

6

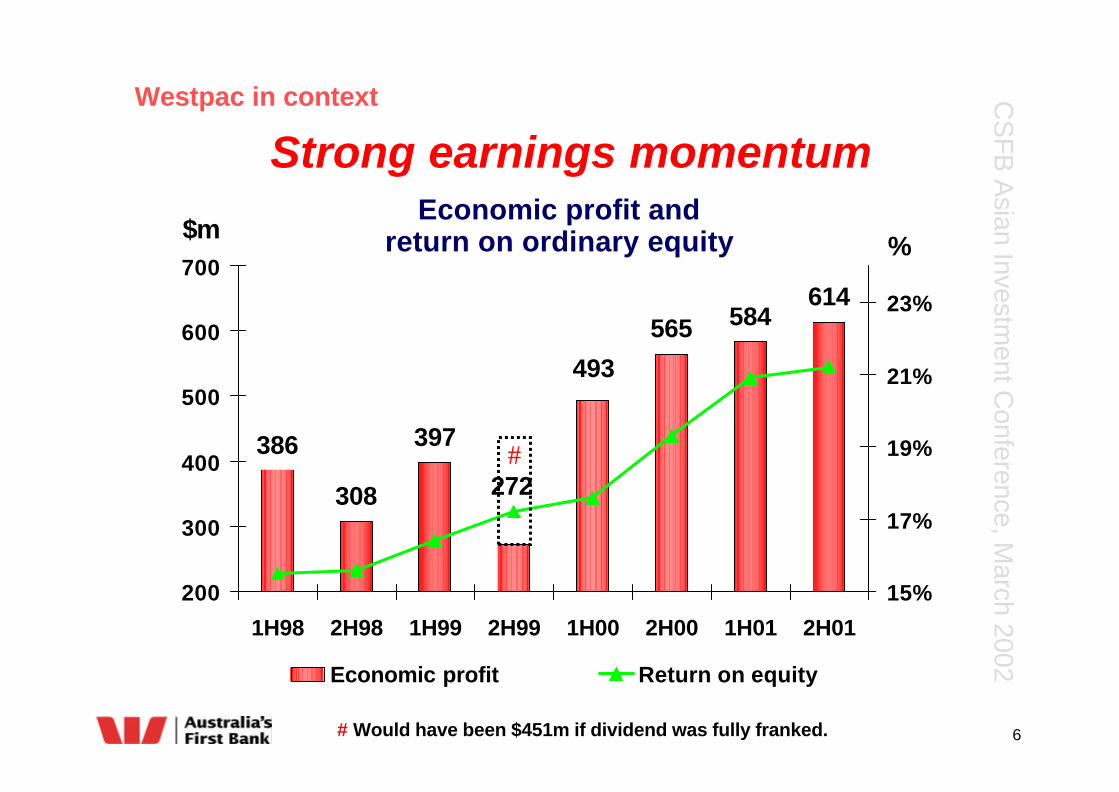

Strong earnings momentum

386

308

397

565 584614

272

493

200

300

400

500

600

700

1H98 2H98 1H99 2H99 1H00 2H00 1H01 2H01

15%

17%

19%

21%

23%

Economic profit Return on equity

Economic profit andreturn on ordinary equity %

$m

# Would have been $451m if dividend was fully franked.

#

Westpac in context

CS

FB A

sian Investment C

onference, March 2002

7

l Westpac in context

l What’s topicalØ Credit qualityØ Wealth managementØ Capital reviewØ Acquisition strategy

l Scoping the potential

l Points of differentiation

Today’s focus

CS

FB A

sian Investment C

onference, March 2002

8

Recent trends positive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

FY 94 FY 95 FY 96 FY 97 FY 98 FY 99 FY 00 1H 01 FY 01

Impaired 90 days past due well secured Watchlist & substandard

%

Stressed loans % of total commitments

Credit Quality

CS

FB A

sian Investment C

onference, March 2002

9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Sep-96 Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Dec-01

%

Mortgages Other consumer loans Business Banking *

90 day delinquencies

# Proportion of loans and acceptances* Data not available prior to 1998

7%

27%

49%

#

Credit Quality

CS

FB A

sian Investment C

onference, March 2002

10

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%C

BA

BK

WB

C

NA

B

PN

C

AN

Z

BA

C

WF

C

TD

WB

JPM

/Ch

ase

FB

F

RB

C

BM

O

CIB

C

ON

E

BN

S

Australian Peers US Peers Canadian Peers

Impaired assets also below peersImpaired Assets / Loans

(International Peer Comparison *)

Westpac

*Based on most recent published results

Credit Quality

CS

FB A

sian Investment C

onference, March 2002

11

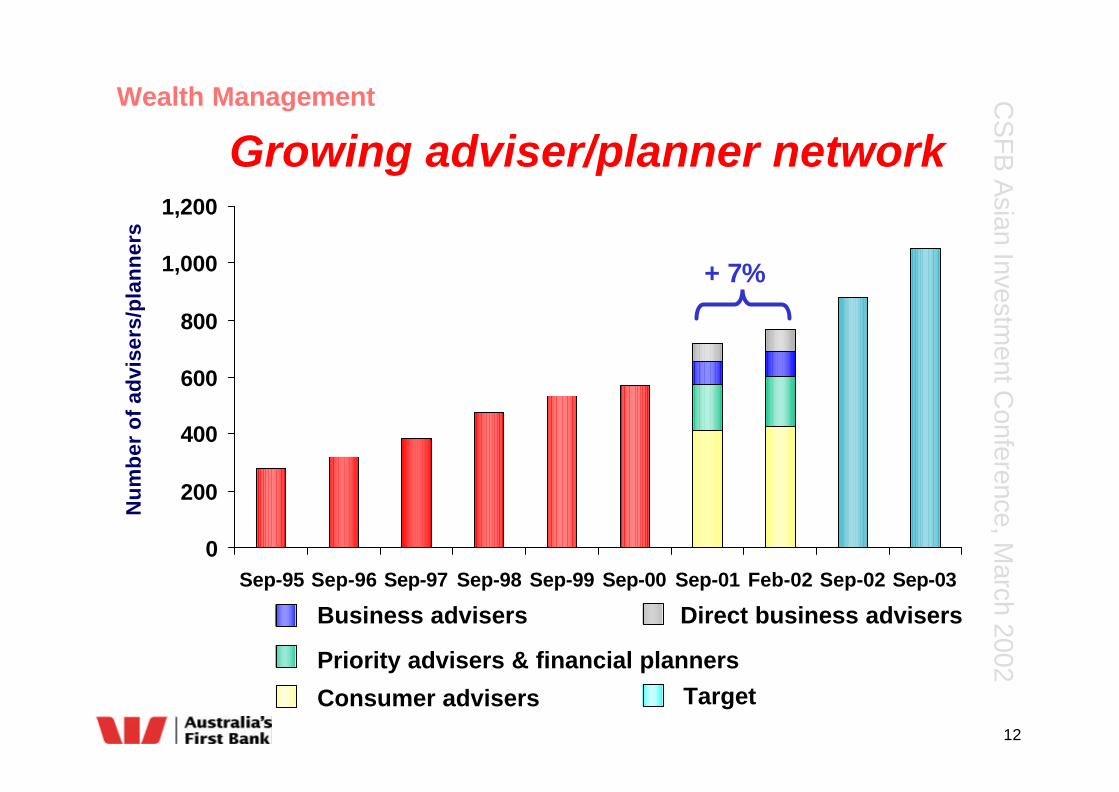

Seeking to increase customer penetration

l Leverage comparative advantageØ large customer baseØ understanding of customer needs

l Expand distribution size and capability

l Access and integrate ‘best of breed’ products

l Balance growth and profitable returns

Wealth Management

CS

FB A

sian Investment C

onference, March 2002

12

Growing adviser/planner network

0

200

400

600

800

1,000

1,200

Sep-95 Sep-96 Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Feb-02 Sep-02 Sep-03

Nu

mb

er o

f ad

vise

rs/p

lan

ner

s

Consumer advisers

Priority advisers & financial planners

Business advisers

Target

Direct business advisers

+ 7%

Wealth Management

CS

FB A

sian Investment C

onference, March 2002

13

6.7

7.2

6.3

6.66.3

6.1

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

TOE / RAA Tier 1 ratio1999 2000 2001

Ratios at top end of target range

%

* Target range

6.5%6.0%*

5.8%5.6%*

Capital

CS

FB A

sian Investment C

onference, March 2002

14

Acquisition strategy

l No particular requirement to acquire customers

l Focused on filling strategic gaps and enhancing capabilitiesØ Wealth management - predominantly distribution

Ø Longer term growth options

l Disciplined approachØ Aligned with strategic direction

Ø Strict valuation criteria

Ø Minimal franchise stress

CS

FB A

sian Investment C

onference, March 2002

15

l Westpac in context

l What’s topical

l Scoping the potential

ØCustomer base

ØEfficiency improvements

l Points of differentiation

Today’s focus

CS

FB A

sian Investment C

onference, March 2002

16

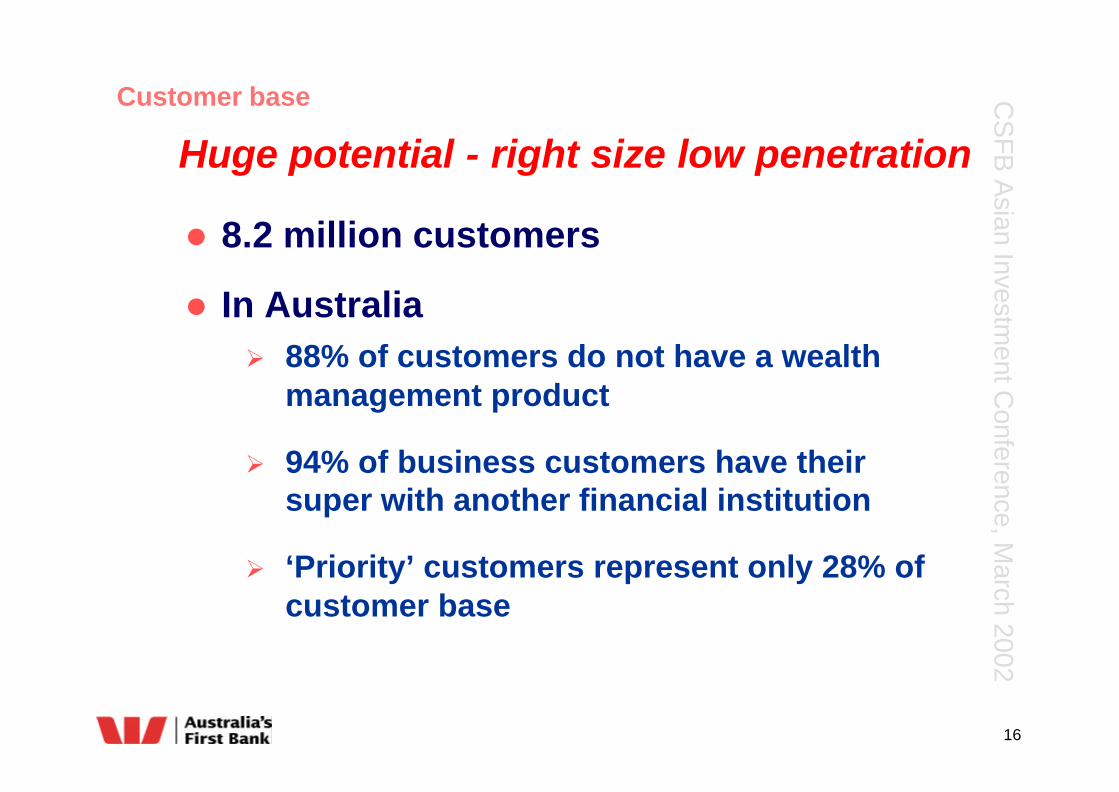

Huge potential - right size low penetration

l 8.2 million customers

l In AustraliaØ 88% of customers do not have a wealth

management product

Ø 94% of business customers have their super with another financial institution

Ø ‘Priority’ customers represent only 28% of customer base

Customer base

CS

FB A

sian Investment C

onference, March 2002

17

11

9

8

6

14

10

0 20 40 60 80 100

Total

Middle Business

Small Business

Private Bank

Priority

Personal

Financial Services penetration

Source : Westpac data and analysis, September 2001

Consum

erB

usin

ess

Customer base

CS

FB A

sian Investment C

onference, March 2002

18

45

50

55

60

65

1997 1998 1999 2000 2001 2H2001

WBC Peer Average

Expense to income ratio*

%

* Excludes goodwill

50.9%

Efficiency improvements

Major efficiency gains

CS

FB A

sian Investment C

onference, March 2002

19

l Westpac in context

l What’s topical

l Scoping the potential

l Points of differentiation

Ø Customer centric focus

Ø Sustainability

Ø Performance culture

Today’s focus

CS

FB A

sian Investment C

onference, March 2002

20

Customer focus

l Segmented customer base

l Doubled number of priority customers between 1998 and 2001

l Major improvement in customer response times

l Leader in customer satisfactionØ Top rated against peers in Consumer, business

middle markets and small business#

# Roy Morgan (consumer) and Greenwich Associates (business) –2001 Surveys – rank against four major Australian banks

CS

FB A

sian Investment C

onference, March 2002

21

Proactive social and environmental agenda...

l Board Social Responsibility Committee

l One of 10 banks globally developing Triple Bottom Line industry reporting standards

l UNEP Financial Institutions working committee for environmental management and reporting

l Active member of Australian Government sustainability finance sector Round Table

Sustainability

CS

FB A

sian Investment C

onference, March 2002

22

l Dow Jones Sustainability IndexØ Rated in top 3 banks worldwide Ø One of only 11 Australian companies in index

l Australian Good Reputation IndexØ 1st in top 100 publicly listed companies

l Corporate Monitor Sustainability RatingsØ Only top 150 listed company with a 5-star social and

environmental rating

Sustainability

Enhancing brand and customer loyalty

CS

FB A

sian Investment C

onference, March 2002

23

Changing behaviours

l Economic profit is the driverØ Incentives and motivational leversØ Alignment to common goals and strategy

l Right people, right job and ‘consequence’ management

l Internal and external benchmarking

l Strong planning, control and accountability

l Simplified structure and autonomy of operation

Performance culture

CS

FB A

sian Investment C

onference, March 2002

24

CUSTOMERSATISFACTION

Flowing through to the bottom line

RETURNS

Incentives / rewards

EMPLOYEE COMMITMENT

Employee Satisfaction

People systems

Sustainability

Simplification

Image & reputation

CS

FB A

sian Investment C

onference, March 2002

25* Westpac internal rolling morale index.

Strong staff morale

Industry Norms75th Percentile

50th Percentile

Staff morale index*Business and Consumer Banking

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Jan-

00M

ar-0

0M

ay-0

0Ju

l-00

Sep-

00No

v-00

Jan-

01M

ar-0

1M

ay-0

1Ju

l-01

Sep-

01No

v-01

Jan-

02

CS

FB A

sian Investment C

onference, March 2002

26

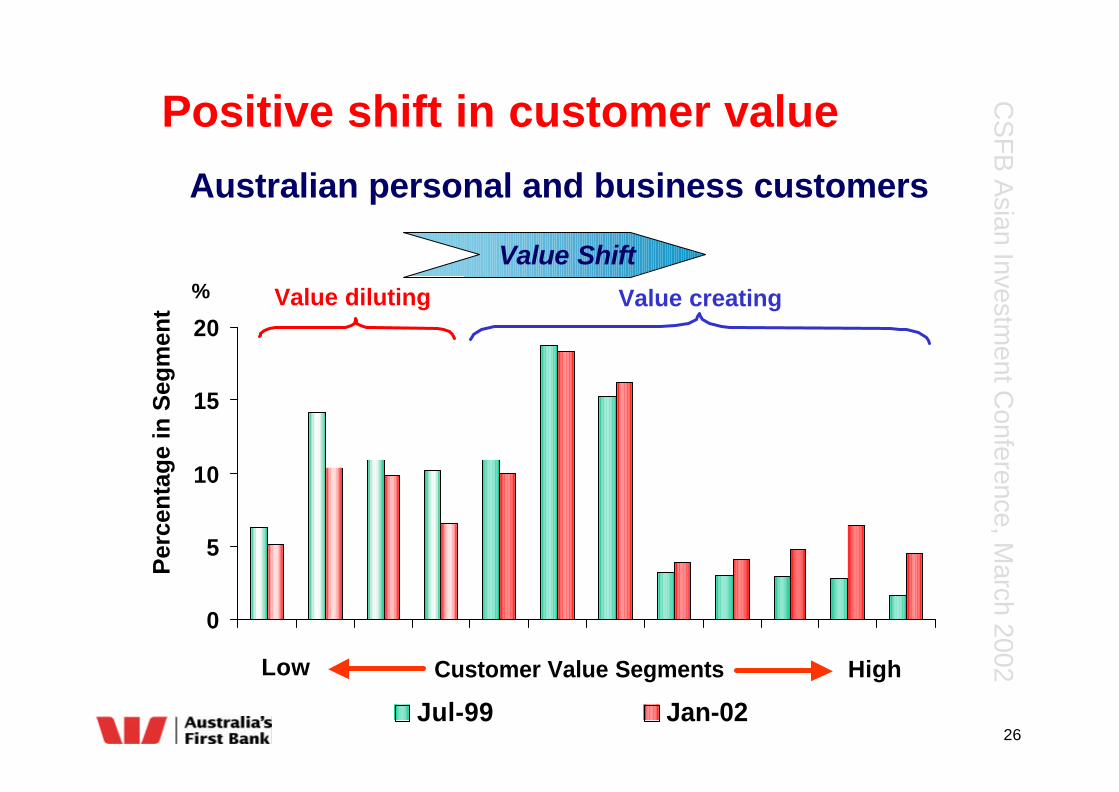

0

5

10

15

20

Customer Value Segments

Jul-99 Jan-02

Positive shift in customer value

Low High

%

Per

cen

tag

e in

Seg

men

tAustralian personal and business customers

Value diluting Value creating

Value Shift

CS

FB A

sian Investment C

onference, March 2002

27

Summary of key driversMedium Term Outlook

Revenue growth 5.5% - 6.5%

Expense growth 0% - 2%

UP growth 11%-13%

Bad debts 25 - 35 bps

Tax rate 29% - 31%

NPAT growth 8% - 13%

Surplus capital growth 3% - 4%

Double digit EPS growth without stretching assumptions

CS

FB A

sian Investment C

onference, March 2002

28