PFM in Africa : The role of Accountancy Profession and ... in Africa : The role of Accountancy...

28

PFM in Africa : The role of Accountancy Profession and Independent Oversight Institutions Ms. Asmaa Resmouki PAFA President ICPAK Seminar - May 18 th 2016

Transcript of PFM in Africa : The role of Accountancy Profession and ... in Africa : The role of Accountancy...

PFM in Africa : The role of

Accountancy Profession

and Independent Oversight

Institutions

Ms. Asmaa Resmouki

PAFA President

ICPAK Seminar - May 18th 2016

CONTENT

Presentation to: XXXXXX Date: xx xx xxxx

1. WHY IS PFM REFORM IMPORTANT IN AFRICA?

2. ROLE OF ACCOUNTING PROFESSION IN PFM

REFORM

3. ROLE OF OVERSIGHT INSTITUTIONS AS MAIN

STAKEHOLDERS IN PFM REFORM

4. MAIN TAKEAWAYS AND THE WAY FORWARD

FOR THE ACCOUNTING PROFESSION

1. WHY IS PFM IMPORTANT IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

1.1 Definition of PFM and Impact on

governance

1.2 Status and trends of PFM Reform

in Africa

1.1 DEFINITON OF PFM

Presentation to: XXXXXX Date: xx xx xxxx

• PFM is the system by which financial

resources are planned, directed and

controlled to enable and influence the

efficient and effective delivery of public

service goals

1.1 IMPACT OF PFM REFORM ON GOVERNANCE

Good

Accounting

Good

GovernancePFM

REFORM

Accountability

1.1 FACTORS MILITATING FOR PFM REFORM

Presentation to: XXXXXX Date: xx xx xxxx

• Strong demand for financial transparency from government

debt holders

• Politicians becoming more accountable on the utilization of

taxpayers’ money

• Public sector financial statements reflecting the full

economic impact of political decisions

• Growth prospects in Africa leading to higher expectations on

governments

1.2 WORLD BANK ASSESSMENT OF PFM REFORM IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

• World Bank monitors PFM through 5 components : Budgeting

Accounting

Internal control

Financial reporting

Auditing

• World Bank measures PFM performance through

PEFA assessments (Public Expenditure and

Financial Accountability)

1.2 WORLD BANK PEFA SCORES IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

1.2 WORLD BANK PEFA SCORES IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

More specifically, the continent is lagging behind in the

following indicators :

Budget control

Quality of accounts

Efficiency of external audit

Parliamentary oversight

1.2 TRENDS OF PFM REFORM IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

• Increasing trend to move to accrual accounting, and

more specifically to IPSAS

• PwC research (2015) : In 5 years time, the biggest

shift to accrual accounting is expected in Africa and

Latin America, followed by Asia

2. ROLE OF ACCOUNTING PROFESSION IN PFM REFORM

Presentation to: XXXXXX Date: xx xx xxxx

2.1 Landscape of Accounting Profession in Africa

2.2 Role of Accounting Profession at PAO level

2.3 Role of Accounting Profession at Regional level

2.4 Status of Accounting reform in some African

countries

2.1 LANDSCAPE OF ACCOUNTING PROFESSION IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

• Members of PAFA : 46 PAOs from 38 countries, covering about

100,000 professionals

• 8 African countries without PAOs

• IFAC membership : 18 nations in Africa without a PAO sufficiently

developed, that have not yet joined IFAC as Members or Associates

Need for Capacity building : Main challenge in Africa

2.1 IFAC MEMBERSHIP LANDSCAPE WORLDWIDE

Presentation to: XXXXXX Date: xx xx xxxx

IFAC Member Bodies

IFAC Associates

No PAO or PAO is

not IFAC

member/Associate

2.2 AT PAO AND PROFESSIONELS’ LEVEL

Presentation to: XXXXXX Date: xx xx xxxx

• Accountants and Auditors in public sector : Important links in the financial reporting chain

Major role in Protection of public interest

• Advocates for PFM reform

• Trusted advisors and Capacity builders in : Transition to accrual accounting

Implementation of IPSAS

Internal and external auditing

Internal control procedures

• Education and training

2.3 AT REGIONAL LEVEL - PAFA

Presentation to: XXXXXX Date: xx xx xxxx

• Advocacy role / Capacity building / Sharing experiences among PAFA

members

• Adoption of International Standards (among which IPSAS) by PAFA in

2012

• ‘Improved Public Sector Reporting’ is one of the 5 Strategic initiatives

of PAFA’s strategy : Tools, materials, and resources to engage political leadership

Influencing IAESB to include Public Sector subjects in the accountancy

qualification framework

Research on topical PFM areas to influence PFM reforms at countries’ level

Public sector programs of mutual interests with other institutions (AFROSAI,

ESAAG …)

2.4 STATUS OF ACCOUNTING REFORM IN SOME AFRICAN COUNTRIES

Presentation to: XXXXXX Date: xx xx xxxx

FRANCOPHONE COUNTRIES

• Laws exist + Close timelines to shifting to Accrual basis + PFM

reforms are part of governments’ agendas

But implementation lagging behind

• Main challenge : Involvement of PAOs and Accounting

Professionals in Public Sector - Business models of Francophone

PAOs – Political will

• Call for Action : PFM Conference in Senegal – October 2015 -

Organised by PAFA/IFAC/FIDEF/WB/AfdB

2.4 STATUS OF ACCOUNTING REFORM IN SOME AFRICAN COUNTRIES

Presentation to: XXXXXX Date: xx xx xxxx

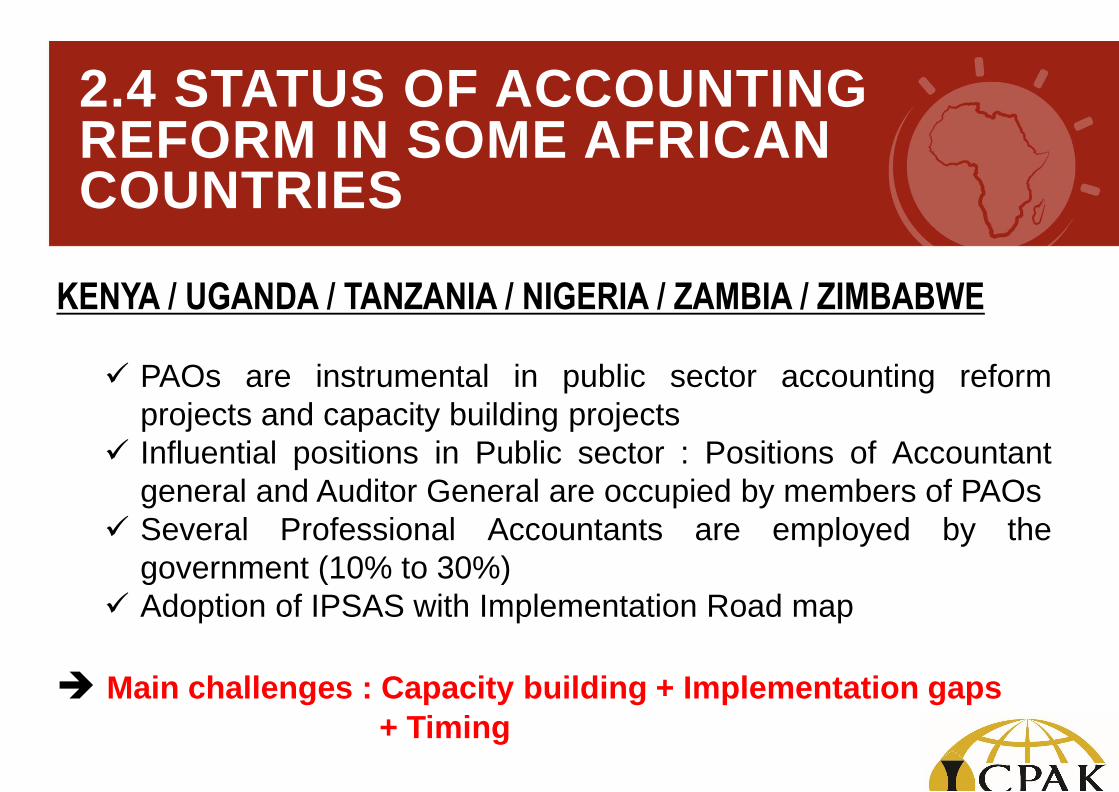

KENYA / UGANDA / TANZANIA / NIGERIA / ZAMBIA / ZIMBABWE

PAOs are instrumental in public sector accounting reform

projects and capacity building projects

Influential positions in Public sector : Positions of Accountant

general and Auditor General are occupied by members of PAOs

Several Professional Accountants are employed by the

government (10% to 30%)

Adoption of IPSAS with Implementation Road map

Main challenges : Capacity building + Implementation gaps

+ Timing

3. ROLE OF OVERSIGHT INSTITUTIONS AS MAIN STAKEHOLDERS IN PFM REFORM

Presentation to: XXXXXX Date: xx xx xxxx

3.1 Main stakeholders in Oversight

3.2 Major Audit models of SAIs in Africa

3.3 Status of Oversight in African countries:

Areas requiring further development

3.1 MAIN STAKEHOLDERS IN OVERSHIGHT

MINISTRY OF

FINANCE

SUPREME

AUDIT

INSTITUTION

Parliament /

Public

Accounts

Committees

PFM cannot function properly without proper

oversight and control

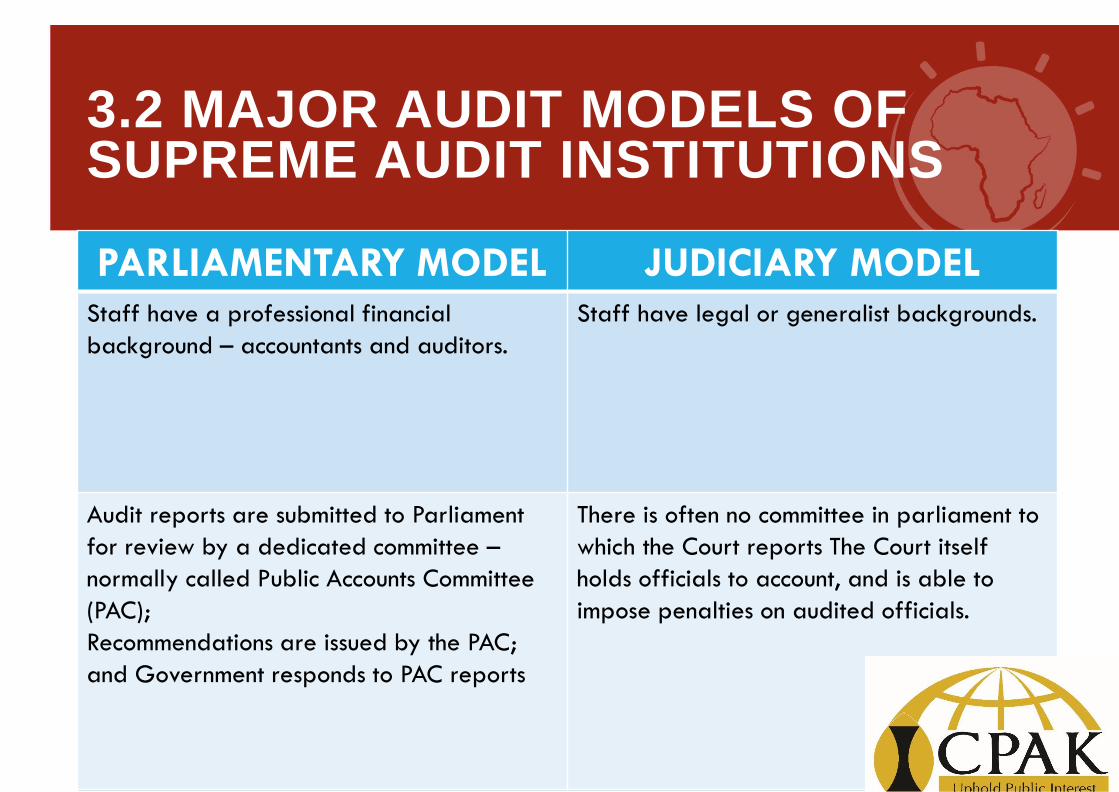

3.2 MAJOR AUDIT MODELS OF SAI IN AFRICA

Presentation to: XXXXXX Date: xx xx xxxx

PARLIAMENTARY MODEL JUDICIARY MODELThe work of the SAI is linked closely to the

system of parliamentary accountability

The SAI is an integral part of the judicial

system

NATIONAL AUDIT OFFICE

All rights, powers and responsibilities vested

in the Auditor general personally

COURT OF ACCOUNTS (OR AUDIT)

Its Members are judges and are typically

appointed for an unlimited term, with one

Member selected to act as its President

A strong focus on financial audit and on the

value for money

Major attention paid until recently to verify

the legality of the transactions

3.2 MAJOR AUDIT MODELS OF SUPREME AUDIT INSTITUTIONS

Presentation to: XXXXXX Date: xx xx xxxx

PARLIAMENTARY MODEL JUDICIARY MODELStaff have a professional financial

background – accountants and auditors.

Staff have legal or generalist backgrounds.

Audit reports are submitted to Parliament

for review by a dedicated committee –

normally called Public Accounts Committee

(PAC);

Recommendations are issued by the PAC;

and Government responds to PAC reports

There is often no committee in parliament to

which the Court reports The Court itself

holds officials to account, and is able to

impose penalties on audited officials.

3.3 STATUS OF OVERSIGHT IN AFRICAN COUNTRIES

Presentation to: XXXXXX Date: xx xx xxxx

• Study performed by AFROSAI-E based on self

assessment tool of its 25 Members

• Progress made but still weak areas requiring further

development

3.3 STATUS OF OVERSIGHT IN AFRICAN COUNTRIES

Presentation to: XXXXXX Date: xx xx xxxx

AREAS REQUIRING FURTHER DEVELOPMENT

• Independence and legal framework of SAIs

• Financial Resourcing of SAIs

• Communications and stakeholder management

3.3 STATUS OF OVERSIGHT IN AFRICAN COUNTRIES

Presentation to: XXXXXX Date: xx xx xxxx

AREAS REQUIRING FURTHER DEVELOPMENT

• Strategies for planning and managing financial and

Human Resources

• Development of quality assurance strategies

• Timeliness and audit coverage

4. MAIN TAKEAWAYS AND THE WAY FORWARD

Presentation to: XXXXXX Date: xx xx xxxx

4.1 Main Takeaways

4.2 The way forward for the

accounting profession

4.1 MAIN TAKEAWAYS

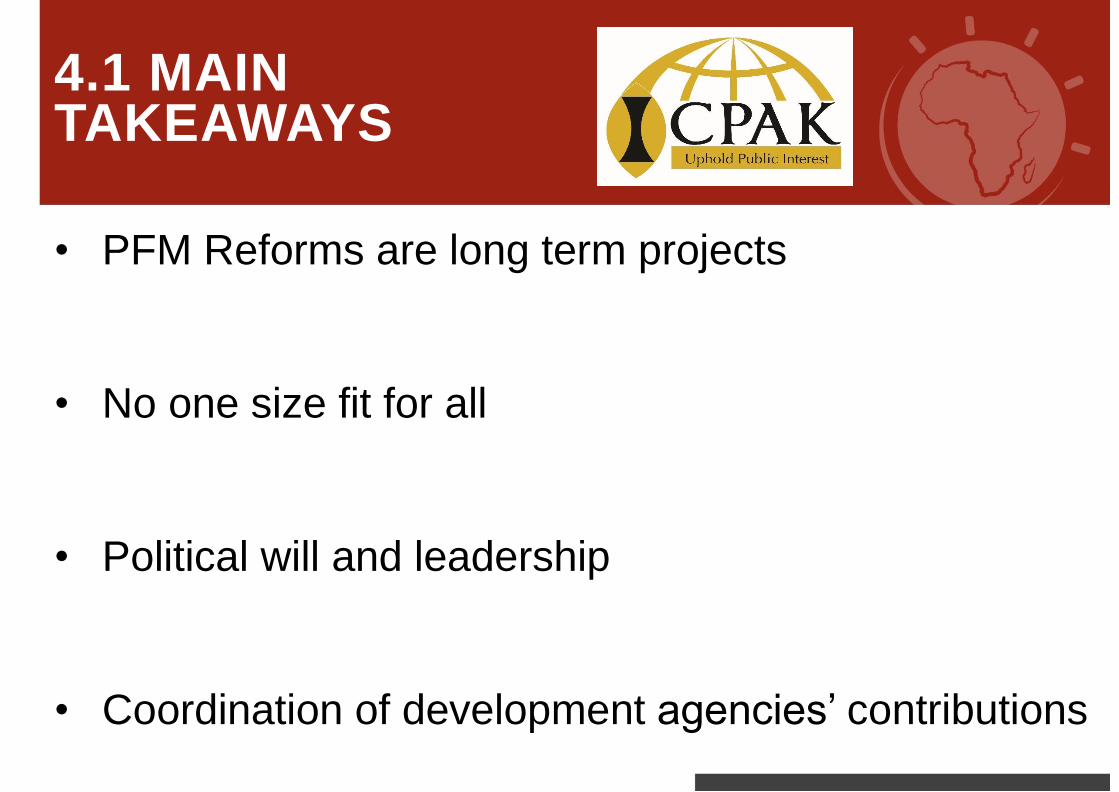

• PFM Reforms are long term projects

• No one size fit for all

• Political will and leadership

• Coordination of development agencies’ contributions

4.2 WAY FORWARD FOR THE ACCOUNTING PROFESSION

Presentation to: XXXXXX Date: xx xx xxxx

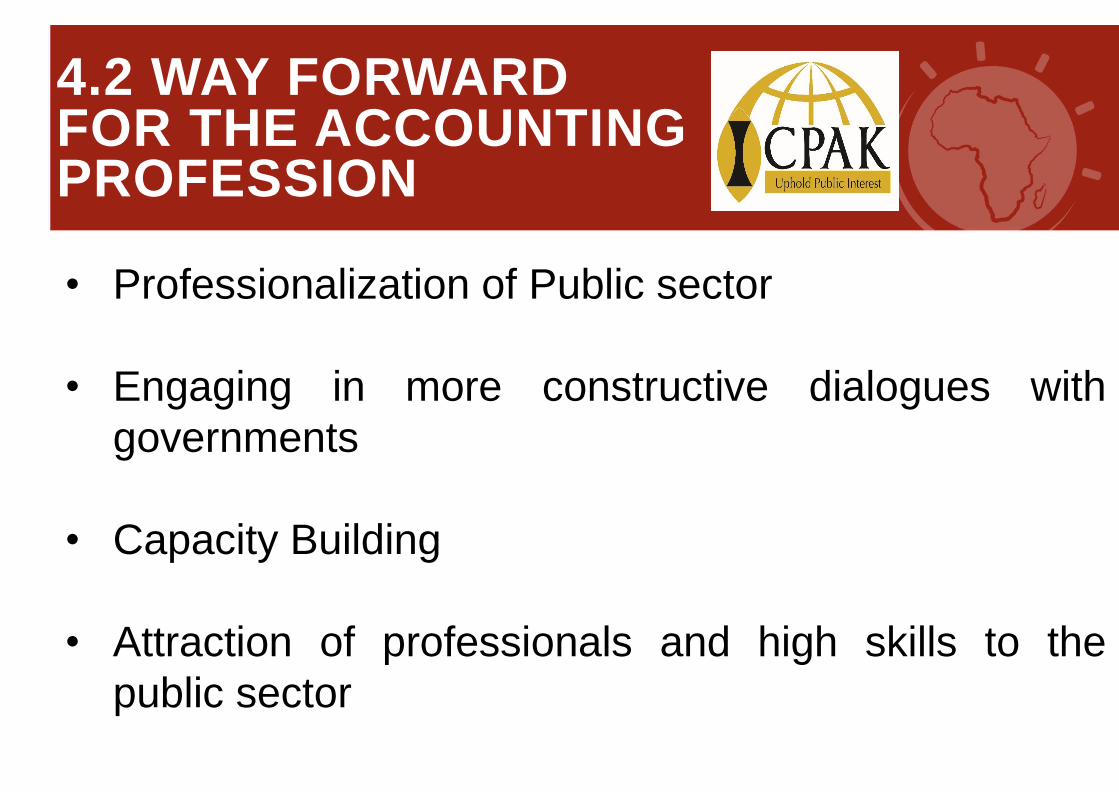

• Professionalization of Public sector

• Engaging in more constructive dialogues with

governments

• Capacity Building

• Attraction of professionals and high skills to the

public sector

Presentation to: XXXXXX Date: xx xx xxxx

THANK YOU