Petroleum Project 2003

15

Organizations are developed to maximize profit and minimize the loss and to give strength to country economy (Home & Host Country). Organizations actions have direct affects on the economy. Organizations plan there action according to information they gather from organizational members. Trade organizations relates from the demand of their customers that can be international and local. The project relates from Petroleum Accounting. Petroleum demand is increasing day by day. Crude Oil is the major part which gives strength to the country economy. There demand is driven by multiple factors including world supply, product markets, refinery capacity, technological changers and the prevailing economy. Accounting is used for organization to take decision because it records all the information which relates from production till end user in which currency is involves. To understand the overall accountants should be aware of nature and treatment of exploration, development and production costs and the agreements on which joint venture formed and international best accounting practices. The word Petroleum is derived from the Latin terms Petra (rock) and oleum (oil). Petroleum refers not only crude oil but also natural gas which found underground rock formation. Petroleum refers to the hydrocarbon compound of the Crude Oil. Crude Oil is measured in barrels (bbl) which equates to 42 U.S. gallons and natural gas is measured in two ways, and both are important in petroleum accounting. Amount of energy is expressed in million British thermal units (MMbtu). By volume, this is expressed in:

-

Upload

muhammadusama92 -

Category

Documents

-

view

216 -

download

0

description

Petroleum Project 2003

Transcript of Petroleum Project 2003

Organizations are developed to maximize profit and minimize the loss and to give strength to country economy (Home & Host Country). Organizations actions have direct affects on the economy. Organizations plan there action according to information they gather from organizational members. Trade organizations relates from the demand of their customers that can be international and local.

The project relates from Petroleum Accounting. Petroleum demand is increasing day by day. Crude Oil is the major part which gives strength to the country economy. There demand is driven by multiple factors including world supply, product markets, refinery capacity, technological changers and the prevailing economy.

Accounting is used for organization to take decision because it records all the information which relates from production till end user in which currency is involves. To understand the overall accountants should be aware of nature and treatment of exploration, development and production costs and the agreements on which joint venture formed and international best accounting practices.

The word Petroleum is derived from the Latin terms Petra (rock) and oleum (oil). Petroleum refers not only crude oil but also natural gas which found underground rock formation. Petroleum refers to the hydrocarbon compound of the Crude Oil.

Crude Oil is measured in barrels (bbl) which equates to 42 U.S. gallons and natural gas is measured in two ways, and both are important in petroleum accounting.

Amount of energy is expressed in million British thermal units (MMbtu).

By volume, this is expressed in:

Mcf (thousand cubic feet) MMcf (million cubic feet) Bcf (billion cubic feet) Tcf (trillion cubic feet)\

Hydrocarbon is expressed in Barrels of Oil Equivalent (BOE) & gas volumes in Mcf are converted to barrels on the basis of energy content or sales value. Approximately 5.6 Mcf of dry gas has the same MMBtu energy (5.8 MMBtu) as an average U.S. barrel of Oil.

We have three types of petroleum industry.

1. Upstream2. Midstream3. Downstream

1. Upstream : A complex and capital intensive business including preliminary exploration (2D & 3D seismic), drilling of wells, development and production of hydrocarbon.

2. Midstream : Midstream gathering and transmission pipelines are a major part of midstream petroleum industry.

3. Downstream : Downstream operations include oil refineries, petro-chemical plants, fuel products distributers and retail outlets.

(In this project we discuss only upstream companies.)

Accounting is used by upstream companies consists of four folds:

1. Joint Venture Accounting as per Joint Operating Agreement (JOA) of Petroleum Concession Agreement (PCA) or Production Sharing Accounting (PSA).

2. Financial Accounting in each partners’ books of Accounts reflection of JV Accounting.3. Revenue Accounting.4. Tax Accounting.

Joint Venture Accounting as per Joint Operating Agreement (JOA) of Petroleum Concession Agreement (PCA) or Production Sharing Accounting (PSA)

A joint venture is an agreement whereby two or more parties (the ventures) jointly control a specific business undertaking and contribute resources towards its accomplishment. We can say joint venture is executed by Exploration & Production Companies in Pakistan. Joint Operating Agreement of Petroleum Concession Agreement signed by Government of Pakistan with Licensee. Accountants should be aware of the block system and award of exploration license (signing of Petroleum Concession Agreement) with Exploration Company (Licensee) in Pakistan by Government of Pakistan.

The Block System

The onshore/ offshore areas are divided into blocks. It is based on exploration/ appraisal costs and risks of discoveries blocks are distributed into Zones. Calculation of Oil & Gas prices are linked with Zones which is also a detail part of Petroleum Policies.

Grant of License

To grant a license Director General Petroleum Concession (DGPC) has established a two-tier pre-qualification system for grant of license. The first tier is based on the technical competences of application and the second tier concerns with the financial strength of the application and its commitment to invest in the upstream sector. Pre-qualified applicants are eligible for participating in building for grant of a license as Operator or Non-Operator. Applicant companies

that seek to become Operator in an onshore and/or offshore area meet the following benchmarks as per criteria laid down:

Technical Capacity. Operational Capacity Legal and Compliance with Residential Requirement. Financial Capacity.

DGPC operate a “balanced scorecard system” to check company’s performance. Pre-qualified companies and/ or consortia are evaluated under the following bid criteria under the Petroleum Policy 2007.

1. Gas Price Gradient (GPG) for when the Reference Crude Price (RCP) is above USD45/ bbl; with a minimum GPG set at 0.2 and maximum GPG allowed set at 1.0. No application company will bid GPG at less than 0.2 or more than 1.0 unless instructed to by DGPC to a rebid.

2. Firm Work Units for Phase I of the initial term ordered at the time of bidding.

DGPC numerically rank bids by candidate companies with regards to each individual category as per balance scorecard. The bid with the highest weighted average score will be declared the winner.

Accounting Procedure of JOA which describes how funds are generated and nature of expenditure chargeable to Joint Account, Accountants must be aware that Joint Accounts maintained by operator for Joint Operations are nothing but a receipts and payment register concluded with each partners’ under/ over advance balance at month end which is represented by cash, bank, debtors and creditors. Classification of expenditure under Exploration, appraisal (Extend Well Test), Development and production phases are maintained in joint venture books due to:

This information are required by each partner to account for it share of cost in its books of accounts.

To calculate accounting as well as taxable profit, different treatments are used for exploration, appraisal (Extend Well Test), and Development and production expenditure.

Joint venture has no ability to submit tax return.

Accounting Procedure

a) Funds ManagementUpon approval of work program and budget, the Operator has a right on a current basis only, to make monthly advance cash calls to all WIOs for the period covered by such work program and budget. The Operator shall restrict the funds held in the bank account

for Joint Operation to a level consistent with that required for the conduct of Joint Operation.

b) Charges to the Joint Accounts1) Allocable Charges

In the event any of operator’s employees of field camps, sub-offices or other facilities serve properties in addition to joint Property and costs cannot be identified, such cost shall be pro-rated or charged on an equitable basis (E&P companies charged on tie writing basis) to be approved by the Operating Committee

2) Direct ChargesDirect charges are those which have a direct affect on the cost of product. All payments to the Government (other than tax and royalty payments). Fields offices, camps, warehouses, supply bases, offices and other facilities to serving the license or lease.

Itemize detail of direct charges are:i.) Labor

Labor costs like their salaries, allowances etc. are included.ii.) Material

Material costs, equipment, purchases of goods (locally & importing, duties, surcharges, license fees) are all included.

iii.) TransportationTransportation of employees, materials, costs of package, insurance and other related costs.

iv.) ServicesServices charges like consultants, contract services, utilities and other services.

v.) Working Interest Owners Exclusively Owned Equipment & FacilitiesCharged on the basis of actual usage at rates commensurate with the cost of ownership and operation.

vi.) Damages of Losses to PropertyDamages which are not covered by insurance like fire, flood, storm, accident etc.

vii.) Litigation ExpensesThese are the protection expenses of the Working Interest Owners interest.

viii.) InsurancePremium insurance is charged to joint Account.

ix.) Other ExpenditureAny other expenditure incurred will be included.

3) Indirect Charges Included in Overhead

Expenses relate to legal, treasury, tax (excluding corporate income tax), and employee relation. Overhead is determined total annual expenditure incurred for joint operation less payment to Government, litigation expenses, and damages and losses to property.i.) Exploration 3% of Expenditures or a minimum of USD 5,000 P/ M.ii.) Development and Production Expenditures

From USD 0 to USD 5,000,000 = 2%From USD 5,000,000 to USD 30,000,000 = 1%Above USD 30,000,000 = 0.25%

All the transactions related to sales in made with the consent of WIOs and the amount will be collected by the purchaser. Any sales return will be deducted by the purchaser and add to the material organization already have.

Accounting In Each Partners’ Books of Accounts

Books of Accounts record all the transactions. It raises Financial reporting issues. Petroleum exploration and production raises numerous issues of accounts. Some of these challenges includes, but are not limited to:

Should wells costs be treated as Assets or Expenses? Should the cost of a dry hole well be capitalized as a cost of finding oil and gas reserves or expected?

Will the amount of oil and gas reflects assets in financial statements because there prices fluctuates?

If production decline over time and productive life varies by property, how should capitalized costs be amortize and depreciated?

Should the gain/ loss be recognized on the sale if the company forms a joint venture and sells portions of the lease to its venture partners?

Upstream petroleum companies follow one of two financial accounting method for Petroleum E&P activities.

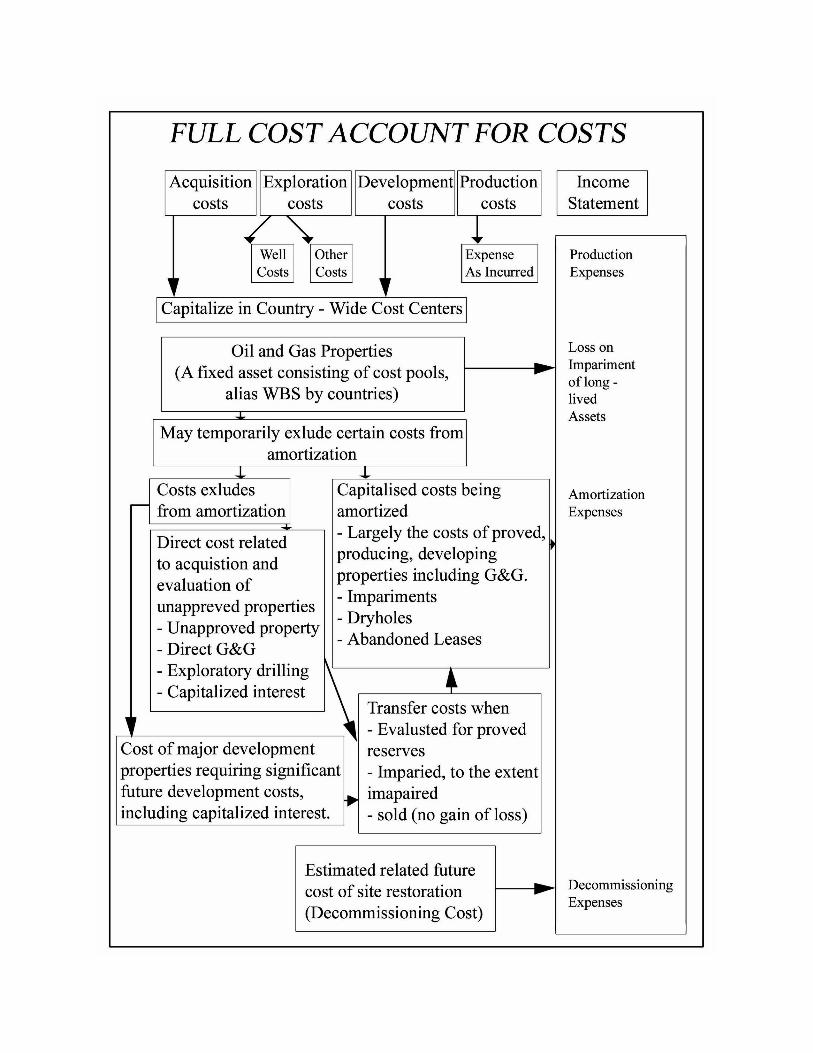

1. Successful Efforts.2. Full Cost.

The methods are different as how the costs are accounted for development and its impact on profit & loss.

Cost of exploratory dry hole and other property carrying costs are charged to expenses in the year incurred. Costs of successful exploratory well and all development costs are capitalized. Net of unamortized capital costs are amortized using unit of production calculations.

Fixed Assets capitalized all property acquisition, exploration and development costs, even dry hole costs.

Classification of Costs Incurred

In oil and gas producing activities costs are classified into four categories.

1. Property acquisition costs.2. Exploration costs.3. Development costs.4. Production costs.

1. Property Acquisition Costs.Nature

Acquisition costs include the costs incurred to purchase lease or otherwise acquire property or mineral right.

Lease bonuses. Option to purchase or lease properties. Broker fees, recoding costs and legal expenses. Misc costs incurred in obtaining mineral right.

Treatment

Successful Effort Method: Costs are expensed out as incurred in the same financial year.

Full Cost Method: Cost is capitalized. Only loss on impairment of long lived assets is expensed out.

Exploration Costs

Nature

Costs incurred on areas that are considered to have prospects of containing oil and gas reserves including costs of drilling exploratory and stratigraphic test wells.

Exploratory costs are of two types.

a. Geology and GeophysicsGeology is the science that studies the planet earth and geophysics studies the earth by quantities the earth by quantitative physical methods, is used in conjunction with geology in the exploration for oil and gas.

Treatment

I. Successful Effort Method: Except the cost of wells, all exploration cost are correctly expense incurred.

II. Full Cost Method: Cost must be capitalized is capitalized.

b. Drilling CostWhen subsurface formations point to the presence of hydrocarbon, detailed planning in conducted including decision on a drilling method and choice of contractor to drill and exploratory well as per the committed work program.

Exploratory Well: An exploratory well is any well that is not a developed well.Developed Well: A well drilled within the proved area of an oil or gas reservoir to the depth of a stratigraphic horizon known to be productive.Strategic Test Well: A drilling effort, geologically directed, to obtain information pertaining to a specific geologic condition. Such wells customary are drilled without the intention of being completed for hydrocarbon production. This classification also includes tests identified as core tests and all types of expendable holes related to hydrocarbon exploration. Stratigraphic tests wells are classified as (a) exploratory – type, if not drilled in a proved area or (b) development – type, if drilled in a proved area.

Treatmenta) Successful Effort Method: Exploratory drilling costs are deferred (kept in

CWIP) until the outcome of the well is known. If an exploratory well finds proved reserves, the deferred costs are capitalized. Absent proved reserve, the deferred costs of the well are expensed out.

b) Full Cost Method: All drilling and equipment costs that are incurred are capitalized.

Disclosure for each annual period and Income Statement is presented, as follows:

Capitalized exploratory well costs including (1) additions to capitalized exploratory well costs that are pending the determination of proved reserves; (2) capitalized exploratory well costs that were reclassified to well, equipment and facilities and (3) capitalized exploratory well costs that were charged to expense.

Exploratory well costs that greater than one year after the completion of drilling.

A description of the project and activities undertaken in order to evaluate the reserves and projects, including the remaining activities necessary to make the determination of proved reserves for each exploratory well or project that continue to be capitalized for a period greater than one year.

Post Balance Sheet Event

Information at the end of the organization period covered by financial statement but before those financial statements are issued shall be taken into account in evaluation conditions that exists at the balance sheets date.

Development Costs

Including depreciation and applicable operating costs of support equipment and facilities and other costs of development activities are costs incurred to:

Drilling sites, clearing ground, drilling road, building and relocating public roads, gas lines and power lines.

Including casing, tubing, pumping equipment and wellhead assembly. Acquire, construct and install production such as lease flow lines, separator, treaters,

manifolds, measuring devices and production storage tanks. Provide improved recovery system.

Treatment

Development costs are capitalized and depreciation, depletion and amortization (DD&A) charged as follows. Basic unit of production computation.

Production Costs

Costs incurred to operate and maintain wells and related equipment and facilities, including depreciation and applicable operating costs of support equipment and facilities and other costs of operating and maintaining those wells and related equipment and facilities. They become part of the cost of oil and gas produced.

I. Costs of labor to operate the wells and related equipment and facilities.II. Repair and maintenance.

III. Materials, supplies, fuel consumed in operating the wells and related equipment and facilities.

Treatment

Production costs are generally expensed as incurred under both methods.

I. Petroleum Policy 2007.II. Petroleum Concession Agreements.

III. IFRS 6.IV. Petroleum Accounting 6th Edition by ICAEW.V. Industry Best Practices.

![Petroleum Products Amendment Act [No. 58 of 2003] · 8 No. 26293 GOVERNMENT GAZETTE, 26 APRIL 2004 Act No. 58,2003 PETROLEUM PRODUCTS AMENDMENT ACT, 2003 (a) Promoting an efficient](https://static.fdocuments.in/doc/165x107/5af47fc77f8b9a9e598ccbba/petroleum-products-amendment-act-no-58-of-2003-no-26293-government-gazette.jpg)