Petrobras Business and Management Plan 2013-2017 Webcast - March 19th

53

2013 – 2017 Business and Management Plan

-

Upload

petrobras -

Category

Investor Relations

-

view

15.655 -

download

0

Transcript of Petrobras Business and Management Plan 2013-2017 Webcast - March 19th

2013 – 2017

Business and Management Plan

March, 19th 2013

2013 – 2017

Business and Management Plan

Webcast

3

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future

events within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as

amended, that are not based on historical facts and are not assurances of

future results. Such forward-looking statements merely reflect the

Company’s current views and estimates of future economic

circumstances, industry conditions, company performance and financial

results. Such terms as "anticipate", "believe", "expect", "forecast", "intend",

"plan", "project", "seek", "should", along with similar or analogous

expressions, are used to identify such forward-looking statements.

Readers are cautioned that these statements are only projections and may

differ materially from actual future results or events. Readers are referred

to the documents filed by the Company with the SEC, specifically the

Company’s most recent Annual Report on Form 20-F, which identify

important risk factors that could cause actual results to differ from those

contained in the forward-looking statements, including, among other

things, risks relating to general economic and business conditions,

including crude oil and other commodity prices, refining margins and

prevailing exchange rates, uncertainties inherent in making estimates of

our oil and gas reserves including recently discovered oil and gas

reserves, international and Brazilian political, economic and social

developments, receipt of governmental approvals and licenses and our

ability to obtain financing.

We undertake no obligation to publicly update or revise any

forward-looking statements, whether as a result of new

information or future events or for any other reason. Figures for

2013 on are estimates or targets.

All forward-looking statements are expressly qualified in their

entirety by this cautionary statement, and you should not place

reliance on any forward-looking statement contained in this

presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas

resources, that we are not permitted to present in documents filed

with the United States Securities and Exchange Commission

(SEC) under new Subpart 1200 to Regulation S-K because such

terms do not qualify as proved, probable or possible reserves

under Rule 4-10(a) of Regulation S-X.

DISCLAIMER

4

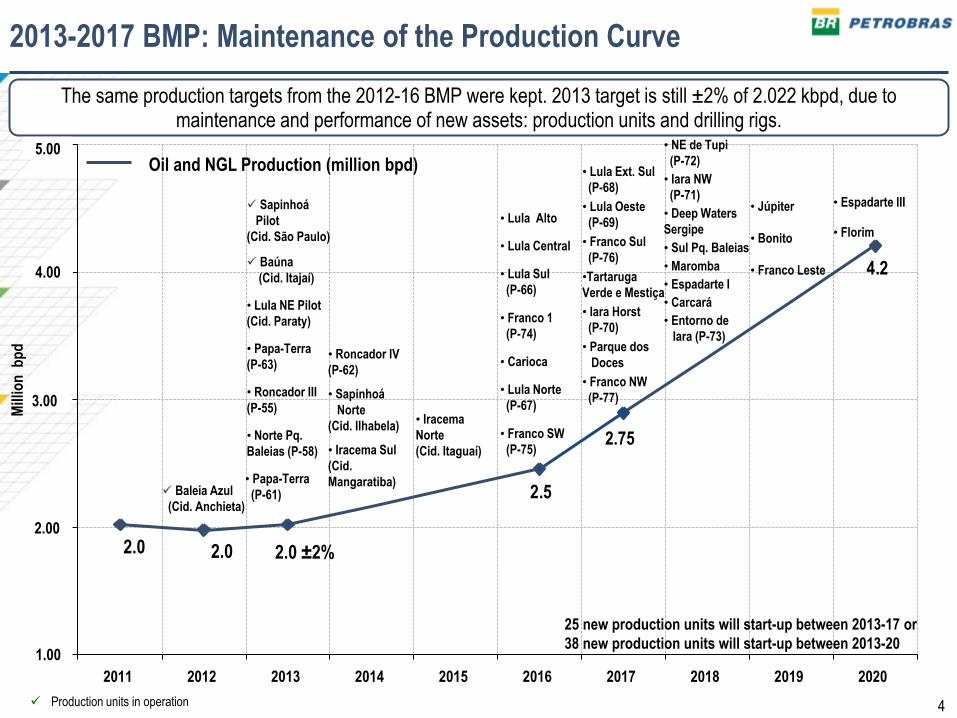

2.5

4.2

1,000

2,000

3,000

4,000

5,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2013-2017 BMP: Maintenance of the Production Curve

• Roncador III

(P-55) • Iracema

Norte

(Cid. Itaguaí)

• Norte Pq.

Baleias (P-58)

Baleia Azul

(Cid. Anchieta)

25 new production units will start-up between 2013-17 or

38 new production units will start-up between 2013-20

Sapinhoá

Pilot

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Lula NE Pilot

(Cid. Paraty)

• Papa-Terra

(P-63)

• Iracema Sul

(Cid.

Mangaratiba)

• Roncador IV

(P-62)

• Sapinhoá

Norte

(Cid. Ilhabela)

• Papa-Terra

(P-61)

2.0 2.0

The same production targets from the 2012-16 BMP were kept. 2013 target is still ±2% of 2.022 kbpd, due to maintenance and performance of new assets: production units and drilling rigs.

2.0 ±2%

• Florim

• Júpiter • Lula Alto

• Lula Central

• Lula Sul

(P-66)

• Franco 1

(P-74)

• Carioca

• Lula Norte

(P-67)

• Franco SW

(P-75)

• Lula Ext. Sul

(P-68)

• Lula Oeste

(P-69)

• Franco Sul

(P-76)

•Tartaruga

Verde e Mestiça

• Parque dos

Doces

• Maromba

• Iara Horst

(P-70)

• Franco NW

(P-77)

• Entorno de

Iara (P-73)

• NE de Tupi

(P-72)

• Iara NW

(P-71)

• Sul Pq. Baleias

• Espadarte I

• Deep Waters

Sergipe

• Carcará

• Bonito

• Franco Leste

• Espadarte III

Production units in operation

1,00

2,00

3,00

4,00

5,00

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2.75

5.00

4.00

3.00

2.00

1.00

Oil and NGL Production (million bpd)

Mill

ion

bp

d

5

001

002

003

004

005

006

1905ral 1905ral 1905ral 1905ral 1905ral 1905ral 1905ral 1905ral 1905ral 1905ral

2.0 2.0

Mill

ion

bo

ed

2.0 ±2%

4.2

1,00

2,00

3,00

4,00

5,00

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2.5

2.4 2.4

3.0

5.2

Oil and NGL Production (million bpd)

Oil, NGL and Natural Gas Production (million boe)

2.4 ±2%

2013-2017 BMP: Maintenance of the Production Curve

The same production targets from the 2012-16 BMP were kept. 2013 target is still ±2% of 2.022 kbpd, due to maintenance and performance of new assets: production units and drilling rigs.

6.00

5.00

4.00

3.00

2.00

1.00

2.75

3.4

6

Investments in 2012 totaled R$ 84.1 Billion, which represents 101% of the projected in the Plan

R$

Bill

ion

Annual Investment

Individual Physical and Financial Monitoring of 174 projects (S Curves): Average physical realization of 104.8% and financial realization of 110.6%.

+1%

2012 Accomplished

84.1

Projected 2012

2012-16 BMP

83.3

34%

51%

Biofuels

Distribution

Corporate

G&E

International

Downstream

E&P

6% 5%

2% 1,6%

0,4%

Investment by Area Main Projects

Investments and Physical and Financial Monitoring 2012: Alignment of Forecasts and Accomplishments: Physical Progress Tracking Financial Progress

E&P: Production Development Projects of Baleia

Azul (Cid. de Anchieta), Sapinhoá (Cid. de São

Paulo), Roncador Modules 3 and 4 (P-55 and P-62)

and Papa-Terra (P-61 and P-63).

Downstream: RNEST and Comperj.

G&P: UFN-III, Bahia Regasification Terminal and

UPGN Cabiúnas.

International: Production Development Projects of

Cascade and Saint-Malo.

7

Physical and Financial Performance: RNEST

RNEST Construction – 33 years after the last refinery (1980)

Suape Industrial Complex (PE) – Feb/13

Accumulated Physical Realization: 70.6%

Accumulated Financial Realization: US$ 11.7 Billion

RNEST: Physical Monitoring Curve

RNEST: Financial Monitoring Curve

8

RNEST: Physical Monitoring Curve

RNEST: Financial Monitoring Curve

Northeast Refinery (RNEST) Physical and Financial Monitoring of the Project: Planning Fullfilled

dez

/12

2012

Accomplished: R$ 4.9 bi*

2012-16 BMP: R$ 5.0 bi

2012

Accomplished: 19.9%

2012-16 BMP: 19.7%

dez

/12

dez

/11

Dec

/12

Dec

/11

Mar

/12

Jun

/12

Sep

/12

Mar

/13

dez

/12

dez

/11

Dec

/12

Dec

/11

Mar

/12

Jun

/12

Sep

/12

Mar

/13

* Considers R$ 100 Million of claims

already negotiated

9

Seeking convergence with international prices. In the last 9 months: 4 Diesel price readjustments, totaling +21.9%, and 2 Gasoline readjustments (+14.9%).

(*) considers Diesel, Gasoline, LPG, Jet Fuel and Fuel Oil. (**) USGC price with domestic market prices.

Parity: Seeking convergence with International Prices 9 months: +21.9% in Diesel and +14.9% in Gasoline

Jan/

13

Jan/

12

Jan/

10

Jan/

09

Jan/

11

Imp

orted

Vo

lum

es (Th

ou

sand

bb

l / d)

Pri

ces

(R$/

bb

l)

Gasoline Imports

Diesel Imports

ARP USGC (w/ volumes sold in Brazil)

ARP Brazil

Average Brazil Price* x Average USGC Price**

Mar

/13

0

100

200

300

400

500

600

700

800

900

0

20

40

60

80

100

120

140

160

180

200

220

240

260

Losses

Gains

2009 2010 2011 2012 2013 2008

Nov

/08

10

Jan/

13

Jan/

12

Jan/

10

Jan/

09

Jan/

11

Imp

orted

Vo

lum

es (Th

ou

sand

bb

l / d)

Pri

ces

(R$/

bb

l)

Gasoline Imports

Diesel Imports

ARP USGC (w/ volumes sold in Brazil)

ARP Brazil

Average Brazil Price* x Average USGC Price**

Mar

/13

0

100

200

300

400

500

600

700

800

900

0

20

40

60

80

100

120

140

160

180

200

220

240

260

Losses

Gains

2009 2010 2011 2012 2013 2008

Nov

/08

1Q12 1Q13

Brent (US$/bbl):

FX Rate (R$/US$):

105

1.67

113

1.99 +19%

(*) considers Diesel, Gasoline, LPG, Jet Fuel and Fuel Oil. (**) USGC price with domestic market prices.

Parity: Seeking convergence with International Prices 9 months: +21.9% in Diesel and +14.9% in Gasoline

Seeking convergence with international prices. In the last 9 months: 4 Diesel price readjustments, totaling +21.9%, and 2 Gasoline readjustments (+14.9%).

11

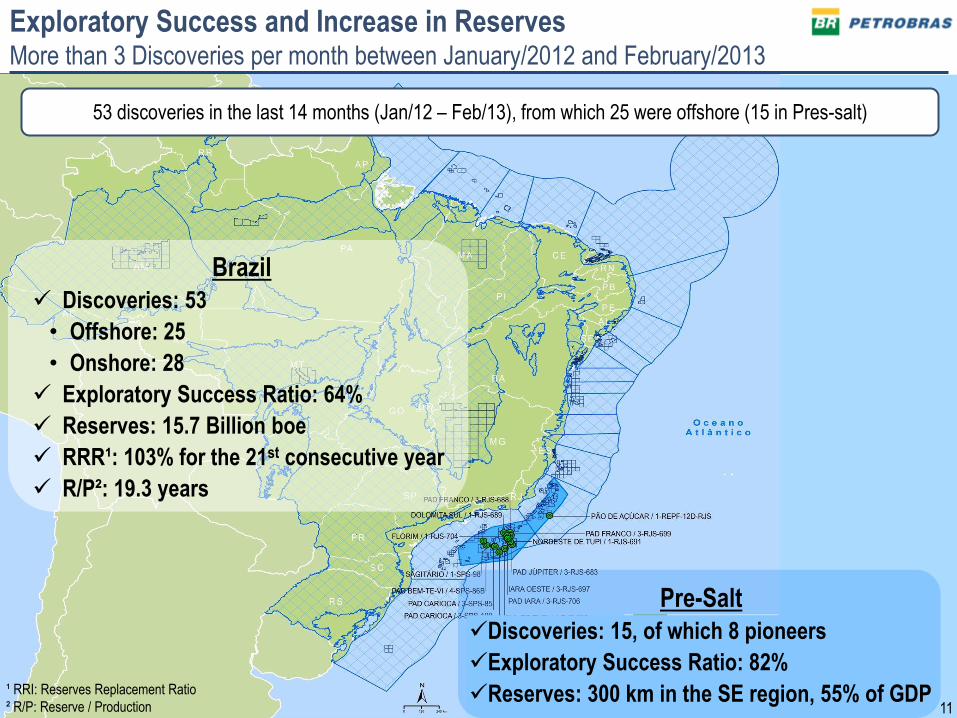

Exploratory Success and Increase in Reserves More than 3 Discoveries per month between January/2012 and February/2013

53 discoveries in the last 14 months (Jan/12 – Feb/13), from which 25 were offshore (15 in Pres-salt)

¹ RRI: Reserves Replacement Ratio

² R/P: Reserve / Production

Pre-Salt

Discoveries: 15, of which 8 pioneers

Exploratory Success Ratio: 82%

Reserves: 300 km in the SE region, 55% of GDP

Brazil

Discoveries: 53

• Offshore: 25

• Onshore: 28

Exploratory Success Ratio: 64%

Reserves: 15.7 Billion boe

RRR¹: 103% for the 21st consecutive year

R/P²: 19.3 years

11

12

Pre-Salt Production is a Reality Production reached 300 thousand barrels of oil per day in Feb/20/2013

Pre-Salt Production Data

Oil Production reached 300 kbpd (of which 249 kbpd

is Petrobras’ stake), 43% in Santos Basin and 57% in

Campos Basin;

This level was reached with only 17 producing wells, 6

in Campos Basin and 11 in Campos Basin;

Level reached only 7 years after discovery:

• Campos Basin: 11 years

• US Gulf of Mexico: 17 years

• North Sea: 9 years

Production of 1 million bpd operated by Petrobras will

be reached by 2017 and the 2.1 million bpd threshold

will be reached by 2020.

Technological Challenges Surmounted

High Resolution Seismic: higher exploratory

success

Geological and numerical modelling: better

production behaviour forecast

Reduction of well construction time from 134

days in 2006 to 70 day in 2012: lower costs

Selection of new materials: lower costs

Qualification of new systems for production

gathering: higher competitiveness

Separation of CO2 from natural gas in deep

waters and reinjection: lower emissions and

increase in recovery factor

13

Refining in Brazil: Oil Products Output

Oil Products output increases every year and will continue to grow with the start-up of the new refineries. Successive records in oil processing have been broken.

96% 93% 93% 93% 92%

• RNEST

Phase 1

Nov/14

• RNEST

Phase 2

May/15

• Comperj

Phase 1

Apr/15

• Premium I

Phase 1

Oct/17

• Premium II

Dec/17

• Comperj

Phase 2

Jan/18

• Premium I

Phase 2

Oct/20

Refineries in Operation Refineries under Construction Refineries in Design Phase

Oil Products Output in Brazil (Million bbl / day)

2.10 MMbpd

(Aug)

2.11 MMbpd

(Jan)

2.12 MMbpd

(Mar)

Daily Oil Processing records

Utilization Factor

3.5

3.0

2.5

2.0

1.5

1.0

14

Thermo power generation, Petrobras and Third Parties¹, above the 10,000 MW threshold in October/2012. We had successive power generation records in 2012 and 2013.

Thermo Power Generation in the National Grid System 10,000 MW: Petrobras Supplies Fuel for 16% of the System Needs

MW

avg

¹ Where Petrobras has a stake or supplies fuel

0

2.000

4.000

6.000

8.000

10.000

12.000

01

-Ja

n-1

02

1-J

an

-10

10

-Fe

b-1

00

2-M

ar-

10

22

-Ma

r-1

01

1-A

pr-

10

01

-Ma

y-1

02

1-M

ay-

10

10

-Ju

n-1

03

0-J

un

-10

20

-Ju

l-1

00

9-A

ug

-10

29

-Au

g-1

01

8-S

ep

-10

08

-Oct

-10

28

-Oct

-10

17

-No

v-1

00

7-D

ec-

10

27

-De

c-1

01

6-J

an

-11

05

-Fe

b-1

12

5-F

eb

-11

17

-Ma

r-1

10

6-A

pr-

11

26

-Ap

r-1

11

6-M

ay-

11

05

-Ju

n-1

12

5-J

un

-11

15

-Ju

l-1

10

4-A

ug

-11

24

-Au

g-1

11

3-S

ep

-11

03

-Oct

-11

23

-Oct

-11

12

-No

v-1

10

2-D

ec-

11

22

-De

c-1

11

1-J

an

-12

31

-Ja

n-1

22

0-F

eb

-12

11

-Ma

r-1

23

1-M

ar-

12

20

-Ap

r-1

21

0-M

ay-

12

30

-Ma

y-1

21

9-J

un

-12

09

-Ju

l-1

22

9-J

ul-

12

18

-Au

g-1

20

7-S

ep

-12

27

-Se

p-1

21

7-O

ct-1

20

6-N

ov-

12

26

-No

v-1

21

6-D

ec-

12

05

-Ja

n-1

32

5-J

an

-13

14

-Fe

b-1

30

6-M

ar-

13

Petrobras - Gas Third Parties - Gas Petrobras - Oil Third Parties - Oil

2011 2012 2010 2013

10,485 MWavg

(Feb/06) 10,149 MWavg

(Nov/23)

12,000

10,000

8,000

4,000

2,000

0

6,000

15

2013-17 Business and Management Plan Fundamentals

• Management

focused on

reaching

physical and

financial targets

of each project

PERFORMANCE

• Guarantee the

expansion of

the business

with solid

financial

indicators

CAPITAL

DISCIPLINE

• Priority for

oil and

natural gas

exploration &

production

projects in

Brazil

PRIORITY

2013 2017

Financiability Assumptions

• Investment Grade rating maintenance

• No new equity issuance

• Convergence with International Prices (Oil Products)

• Divestments in Brazil and, mainly, abroad

16

2013-2017 BMP Investments: Approved by Petrobras’ Board of Directors in 03/15/13

2013-2017 Period

US$ 236.7 Billion

• Investment Grade Rating maintenance:

− Leverage lower than 35%

− Net Debt/EBITDA lower than 2.5x

• No new equity issuance

• Convergence with International Prices (Oil

Products)

• Divestments in Brazil and, mainly, abroad

* Pbio = Petrobras Biofuel │ETM = Engineering, Technology and Materials │Other Areas = Financial, Strategy and Corporate

Financiability Assumptions

28%

International ETM* Other Areas* Pbio* E&P Distribuition Downstream G&E

E&P 62.3%

(US$ 147.5 bi)

27.4% (US$ 64.8 bi)

1.0% (US$ 2.3 bi)

1.4% (US$ 3.2 bi)

1.1% (US$ 2.9 bi)

2.2% (US$ 5.1 bi)

4.2% (US$ 9.9 bi)

0.4% (US$ 1.0 bi)

17

2013-2017 BMP Investments: Implementation x Evaluation

Under Implementation

US$ 207.1 Billion

Under Evaluation

US$ 29.6 Billion

+ = Total

US$ 236.7 Billion

All E&P projects in Brazil and projects of the

remaining segments in phase IV

Projects for the remaining segments,

excluding E&P, currently in phase I, II and III.

770 projects 177 projects 947 projects

62.3%

(US$ 147.5 Billion) 27.4%

(US$ 64.8 Billion)

1.0%

(US$ 2.3 Billion)

1.4%

(US$ 3.2 Billion)

1.1%

(US$ 2.9 Billion)

2.2%

(US$ 5.1 Billion)

4.2%

(US$ 9.9 Billion)

0.4%

(US$ 1.0 Billion)

71.2%

(US$ 147.5 Billion) 20.9%

(US$ 43.2 Billion)

1.1%

(US$ 2.3 Billion)

1.4%

(US$ 2.9 Billion)

0.5%

(US$ 1.1 Billion)

1.5%

(US$ 3.2 Billion)

2.9%

(US$ 5.9 Billion)

0.5%

(US$ 1.0 Bililon)

73.0%

(US$ 21.6 Billion)

1.0%

(US$ 0.3 Billion)

13.5%

(US$ 4.0 Billion)

6.4%

(US$ 1.9 Billion)

6.1%

(US$ 1.8 Billion)

Phase I: Opportunity Identification; Phase II: Conceptual Project; Phase III: Basic Project ; Phase IV: Execution

* Pbio = Petrobras Biofuel │ETM = Engineering, Technology and Materials │Other Areas = Financial, Strategy and Corporate

International ETM* Other Areas* Pbio* E&P Distribuition Downstream G&E

18

INVESTMENTS UNDER IMPLEMENTATION

INVESTMENTS UNDER EVALUATION

* US$ 207.1 Billion include ETM (US$ 2,3 bi) and Other Areas (US$ 1,0 bi) investments

2013-2017 Business and Management Plan : Project Portfolio Management

Implementation of

Projects under

Evaluations contingent

on:

Results of Technical-

Economical Feasibility

studies;

Availability of Resources

(financiability);

Competition for available

resources.

US$ 147.5 Billion

E&P

US$ 43.2 Billion

Downstream

US$ 5.9 Billion

Gas & Energy

US$ 3.2 Billion

International

US$ 2.9 Billion

Distribution

US$ 1.1 Billion

Biofuels

-

E&P

US$ 21.6 Billion

Downstream

US$ 4.0 Billion

Gas & Energy

US$ 1.9 Billion

International

US$ 0.3 Billion

Distribution

US$ 1.8 Billion

Biofuels

US$

207.1 bi*

US$

29.6 bi*

19

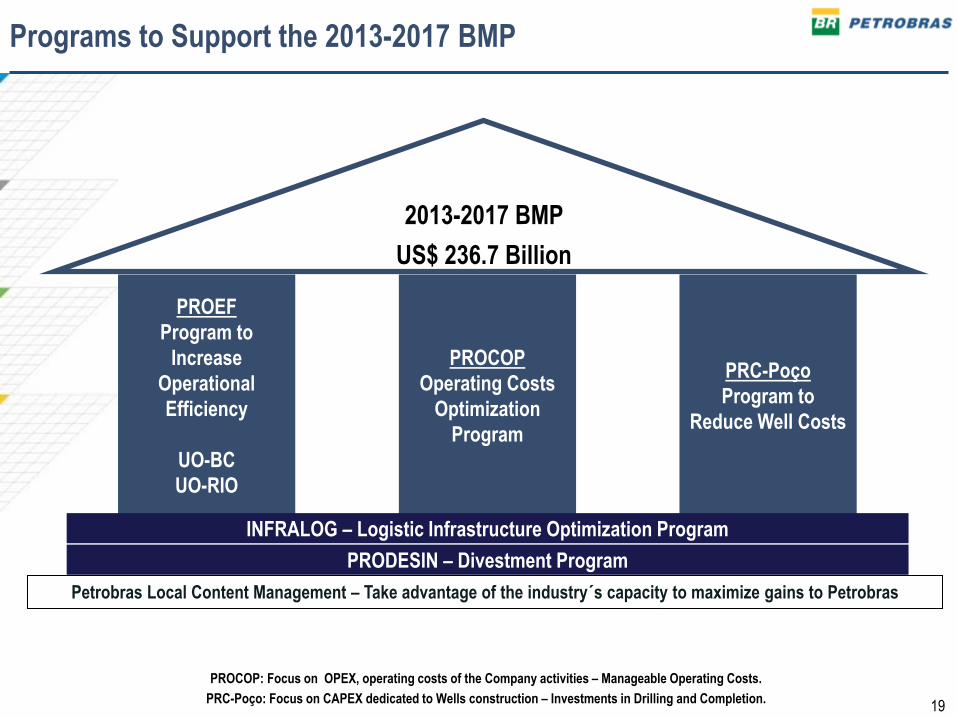

Programs to Support the 2013-2017 BMP

2013-2017 BMP

US$ 236.7 Billion

PRC-Poço

Program to

Reduce Well Costs

PROEF

Program to

Increase

Operational

Efficiency

UO-BC

UO-RIO

PROCOP

Operating Costs

Optimization

Program

INFRALOG – Logistic Infrastructure Optimization Program

PRODESIN – Divestment Program

PROCOP: Focus on OPEX, operating costs of the Company activities – Manageable Operating Costs.

PRC-Poço: Focus on CAPEX dedicated to Wells construction – Investments in Drilling and Completion.

Petrobras Local Content Management – Take advantage of the industry´s capacity to maximize gains to Petrobras

20

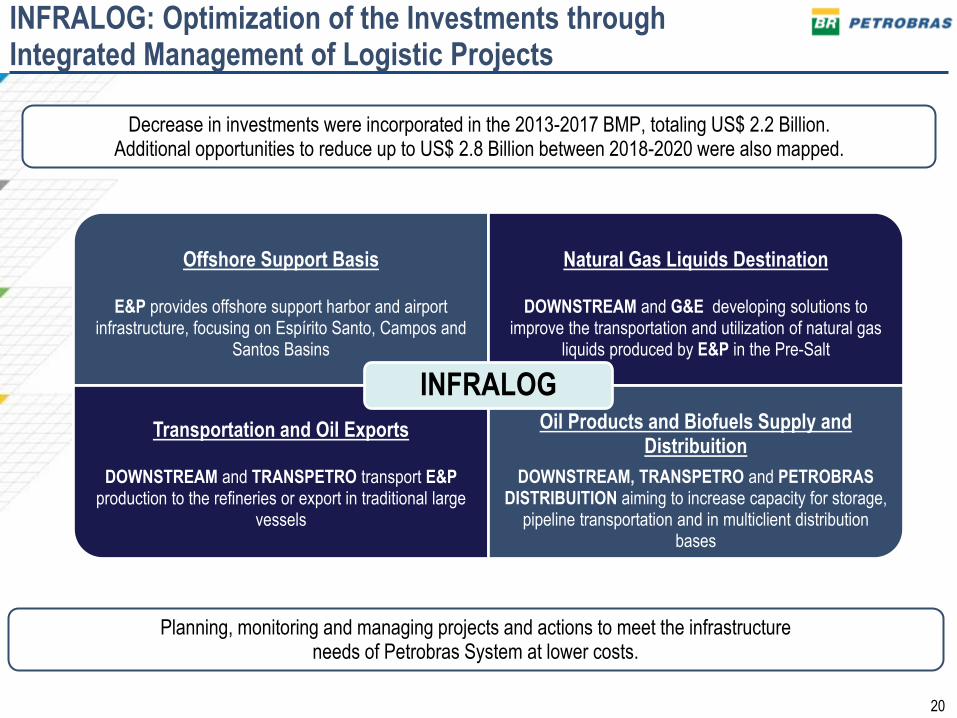

INFRALOG: Optimization of the Investments through Integrated Management of Logistic Projects

Planning, monitoring and managing projects and actions to meet the infrastructure needs of Petrobras System at lower costs.

Offshore Support Basis

E&P provides offshore support harbor and airport infrastructure, focusing on Espírito Santo, Campos and

Santos Basins

Natural Gas Liquids Destination

DOWNSTREAM and G&E developing solutions to improve the transportation and utilization of natural gas

liquids produced by E&P in the Pre-Salt

Transportation and Oil Exports

DOWNSTREAM and TRANSPETRO transport E&P production to the refineries or export in traditional large

vessels

Oil Products and Biofuels Supply and

Distribuition

DOWNSTREAM, TRANSPETRO and PETROBRAS DISTRIBUITION aiming to increase capacity for storage,

pipeline transportation and in multiclient distribution bases

INFRALOG

Decrease in investments were incorporated in the 2013-2017 BMP, totaling US$ 2.2 Billion. Additional opportunities to reduce up to US$ 2.8 Billion between 2018-2020 were also mapped.

21

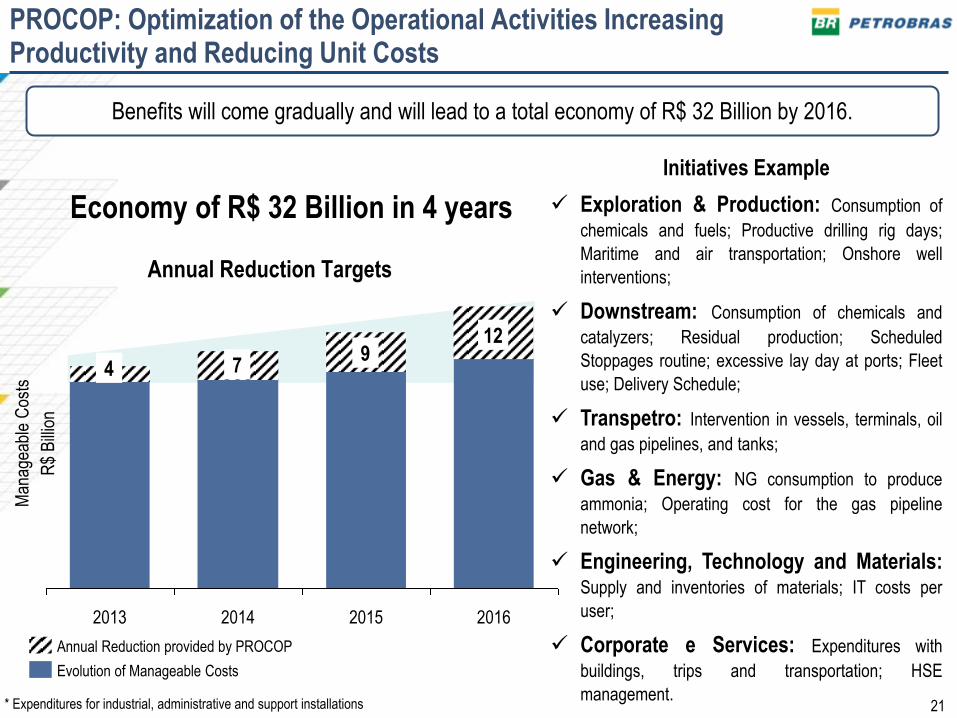

2014 2013 2016 2015

Annual Reduction Targets

Economy of R$ 32 Billion in 4 years

Benefits will come gradually and will lead to a total economy of R$ 32 Billion by 2016.

4 7 9

12

PROCOP: Optimization of the Operational Activities Increasing Productivity and Reducing Unit Costs

Initiatives Example

Exploration & Production: Consumption of

chemicals and fuels; Productive drilling rig days;

Maritime and air transportation; Onshore well

interventions;

Downstream: Consumption of chemicals and

catalyzers; Residual production; Scheduled

Stoppages routine; excessive lay day at ports; Fleet

use; Delivery Schedule;

Transpetro: Intervention in vessels, terminals, oil

and gas pipelines, and tanks;

Gas & Energy: NG consumption to produce

ammonia; Operating cost for the gas pipeline

network;

Engineering, Technology and Materials: Supply and inventories of materials; IT costs per

user;

Corporate e Services: Expenditures with

buildings, trips and transportation; HSE

management.

* Expenditures for industrial, administrative and support installations

Annual Reduction provided by PROCOP

Evolution of Manageable Costs

Man

agea

ble

Cos

ts

R$

Bill

ion

22

16%

(24.3) 73%

(106.9) 11%

(16.3)

Infrastructure and Support

Exploration

Production Development

2013-2017 Period US$ 147.5 Billion

22

Exploration & Production

23

E&P Investments

25%

(26.2)

43%

(46.4)

32%

(34.3)

Production Development

US$ 106.9 Billion

70%

(17.1)

24%

(5.8)

6%

(1.4)

Post-Salt

Pre-Salt

Transfer of Rights

Exploration

US$ 24.3 Billion

2013-2017 Period

Aside from Exploration and Production Development, E&P infrastructure investments total US$ 16.3 Billion.

24

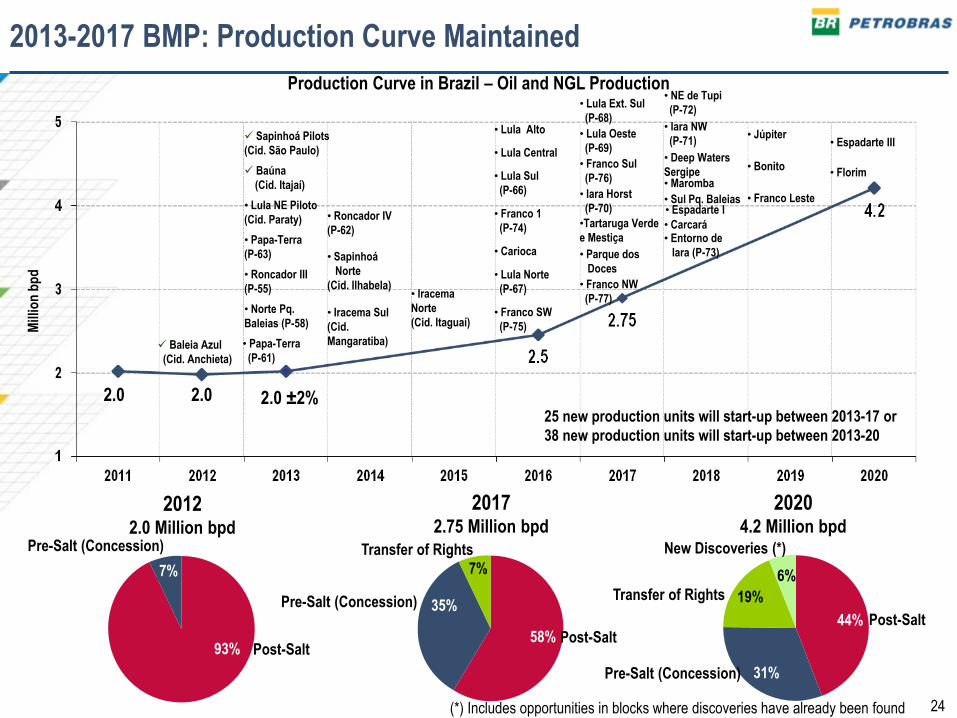

2013-2017 BMP: Production Curve Maintained

Production Curve in Brazil – Oil and NGL Production

• Roncador III

(P-55) • Iracema

Norte

(Cid. Itaguaí)

• Florim

• Júpiter

• Norte Pq.

Baleias (P-58)

Baleia Azul

(Cid. Anchieta)

Sapinhoá Pilots

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Lula NE Piloto

(Cid. Paraty)

• Papa-Terra

(P-63)

• Iracema Sul

(Cid.

Mangaratiba)

• Roncador IV

(P-62)

• Sapinhoá

Norte

(Cid. Ilhabela)

• Lula Alto

• Lula Central

• Lula Sul

(P-66)

• Franco 1

(P-74)

• Carioca

• Lula Norte

(P-67)

• Franco SW

(P-75)

• Lula Ext. Sul

(P-68)

• Lula Oeste

(P-69)

• Franco Sul

(P-76)

•Tartaruga Verde

e Mestiça

• Parque dos

Doces

• Maromba • Iara Horst

(P-70)

• Franco NW

(P-77)

• Entorno de

Iara (P-73)

• NE de Tupi

(P-72)

• Iara NW

(P-71)

• Sul Pq. Baleias • Espadarte I

• Deep Waters

Sergipe

• Carcará

• Bonito

• Franco Leste

• Espadarte III

• Papa-Terra

(P-61)

2.0 ±2% 2.0 2.0

Mill

ion

bp

d

2012 2.0 Million bpd

2017 2.75 Million bpd

2020 4.2 Million bpd

Pre-Salt (Concession)

7%

93%

Transfer of Rights

7%

Pre-Salt (Concession) 35%

Post-Salt 58%

New Discoveries (*)

6%

Transfer of Rights 19%

Pre-Salt (Concession) 31%

Post-Salt 44%

Post-Salt

(*) Includes opportunities in blocks where discoveries have already been found

25 new production units will start-up between 2013-17 or

38 new production units will start-up between 2013-20

25

Production Curve in Brazil – Oil and NGL Production

2013

• Roncador III

(P-55) • Iracema

Norte

(Cid. Itaguaí)

• Florim • Júpiter

• Norte Pq.

Baleias (P-58)

Baleia Azul

(Cid. Anchieta)

Sapinhoá Pilot

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Lula NE Pilot

(Cid. Paraty)

• Papa-Terra

(P-63)

• Iracema Sul

(Cid.

Mangaratiba)

• Roncador IV

(P-62)

• Sapinhoá

Norte

(Cid. Ilhabela)

• Lula Alto

• Lula Central

• Lula Sul

(P-66)

• Franco 1

(P-74)

• Carioca

• Lula Norte

(P-67)

• Franco SW

(P-75)

• Bonito

• Franco Leste

• Espadarte III

• Papa-Terra

(P-61)

2.0 ±2% 2.0 2.0

Mill

ion

bp

d

2013-2017 BMP: Production Curve Maintained

25 new production units will start-up between 2013-17 or

38 new production units will start-up between 2013-20

• Lula Ext. Sul

(P-68)

• Lula Oeste

(P-69)

• Franco Sul

(P-76)

•Tartaruga Verde

e Mestiça

• Parque dos

Doces

• Maromba

• Iara Horst

(P-70)

• Franco NW

(P-77)

• Entorno de

Iara (P-73)

• NE de Tupi

(P-72)

• Iara NW

(P-71)

• Sul Pq. Baleias

• Espadarte I

• Deep Waters

Sergipe

• Carcará

Production units in operation

26

Sapinhoá Pilot Project: Drilling, completion and interconnection of 13 wells to a chartered FPSO from Schahin/Modec with capacity to process120 kbpd

of oil and 5 million m3/d of natural gas.

Sapinhoá Pilot Project: Operating since January 5th, 2013 FPSO Cidade de São Paulo: 120 kbpd

FPSO Cidade de São Paulo anchored in field – Mar/13 TOTAL PHYSICAL COMPLETION - Forecast: 59.9% / Accomplished: 54.0%

TOTAL LOCAL CONTENT – Commitment with ANP: 30% / Planned: 57%

26

27

Baúna Project: Drilling, completion and interconnection of 13 submarine well to chartered FPSO Cidade de Itajaí, with capacity to process 80 kbpd of oil and

2 million m3/d of gas.

Baúna Project: Operating since February 16th, 2013 FPSO Cidade de Itajaí: 80 kbpd

FPSO Cidade de Itajaí anchored in field - Jan/13 TOTAL PHYSICAL COMPLETION - Forecast: 69.8% / Accomplished: 53.5%

TOTAL LOCAL CONTENT – Commitment with ANP: 60%

27

28

Lula NE Pilot Project – 1st Oil on May 28th, 2013 FPSO Cidade de Paraty: 120 kbpd Lula NE Pilot Project: Drilling, completion and interconnection of 14 wells to a FPSO chartered from QGOG/SBM with capacity to process 120 kbpd of oil

and 5 million m3/d of gas.

FPSO Cidade de Paraty Integration at BrasFELS Shipyard, Angra dos Reis/RJ, Mar/13.

UNIT's PHYSICAL COMPLETION - Forecast: 99.0% / Accomplished: 97.8%

UNIT's LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 30% / Planned: 60%

28

29 P-63 Integration at Honório Bicalho Shipyard, in Rio Grande (RS) – Feb/2013

Papa-Terra Project: 1st Oil of P-63 on July 15th, 2013 FPSO P-63: 140 kbpd

Papa-Terra Project: Drilling, completion and interconnection of 30 wells to P-61 TLWP (Tension Leg Wellhead Plataform) and P-63 (FPSO) with capacity to

produce 140 kbpd and 1 MM m2/day of gas.

UNIT’s PHYSICAL COMPLETION - Forecast: 98.5% / Accomplished: 94.1%

UNIT’s LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 0% / Planned: 46%

29

30

Roncador Project Module III - 1st Oil on September 30th, 2013 SS P-55: 180 kbpd Roncador Project Module III: Drilling, completion and interconnection of 17 wells to SS P-55 with capacity to process 180 kbpd of oil and 6 million m3/d of

gas.

SS P-55 Integration at ERG1 Shipyard in Rio Grande/RS – Feb/2013

UNIT’s PHYSICAL COMPLETION - Forecast: 87.5% / Accomplished: 89.2%

UNIT’s LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 0% / Planned : 50%

30

31

Parque das Baleias Project: Drilling, completion and interconnection of 24 wells to FPSO P-58, with a processing capacity of 180 kbpd of oil and 6 MM

m³/d of gas.

FPSO P-58 Integration at Honório Bicalho Shipyard , in Rio Grande/RS – Mar/2013

Parque das Baleias Project: 1st Oil on November 30th, 2013 FPSO P-58: 180 kbpd

UNIT’s PHYSICAL COMPLETION – Forecast: 86.0% / Accomplished: 90.6%

UNIT’s LOCAL CONTENT – Planned: 62%

TOTAL LOCAL CONTENT – Commitment with ANP: 0% / Planned : 58%

31

32

Papa-Terra Project: 1st Oil of P-61 on December 31st, 2013 TLWP P-61 Papa-Terra Project: Drilling, completion and interconnection of 30 wells to P-61 – TLWP (Tension Leg Wellhead Plataform) and to P-63 (FPSO) with capacity

to process 140 kbpd and 1 MM m³/day of gas.

Topside and hull of P-61 at BrasFELS Shipyard (RJ) – Jan/2013

UNIT’s PHYSICAL COMPLETION – Forecast: 94.9% / Accomplished: 76.2%

UNIT’s LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 0% / Planned : 46%

32

33

2013-2017 BMP: Production Curve Maintained

Production Curve in Brazil – Oil and NGL Production

2014

• Roncador III

(P-55)

• Norte Pq.

Baleias (P-58)

Baleia Azul

(Cid. Anchieta)

Sapinhoá Pilot

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Lula NE Pilot

(Cid. Paraty)

• Papa-Terra

(P-63)

• Papa-Terra

(P-61)

2.0 ±2% 2.0 2.0

Mill

ion

bp

d

• Iracema

Norte

(Cid. Itaguaí)

• Iracema Sul

(Cid.

Mangaratiba)

• Roncador IV

(P-62)

• Sapinhoá

Norte

(Cid. Ilhabela)

• Florim • Júpiter • Lula Alto

• Lula Central

• Lula Sul

(P-66)

• Franco 1

(P-74)

• Carioca

• Lula Norte

(P-67)

• Franco SW

(P-75)

• Bonito

• Franco Leste

• Espadarte III

• Lula Ext. Sul

(P-68)

• Lula Oeste

(P-69)

• Franco Sul

(P-76)

•Tartaruga Verde

e Mestiça

• Parque dos

Doces

• Maromba

• Iara Horst

(P-70)

• Franco NW

(P-77)

• Entorno de

Iara (P-73)

• NE de Tupi

(P-72)

• Iara NW

(P-71)

• Sul Pq. Baleias

• Espadarte I

• Deep Waters

Sergipe

• Carcará

Production units in operation

34 P-62 Integration at Atlântico Sul Shipyard, Ipojuca (PE) – Jan/2013

Roncador Project Module IV: Drilling, completion and interconnection of 17 wells to FPSO P-62 with a processing capacity of 180 kbpd of oil and 6 MM

m³/d of gas.

Roncador Project Module IV – 1st Oil on March/2014 FPSO P-62: 180 kbpd

UNIT’s PHYSICAL COMPLETION – Forecast: 70.5% / Accomplished: 88.4%

UNIT’s LOCAL CONTENT – Planned: 64%

TOTAL LOCAL CONTENT – Commitment with ANP: 0% / Planned : 56%

34

35

Sapinhoá Norte Project: 1st Oil on September/2014 FPSO Cidade de Ilhabela: 150 kbpd Sapinhoá Norte Project: Drilling, completion and interconnection of 15 wells to a production unit chartered from QGOG/SBM with processing capacity of 150

kbpd of oil and compression of 6 MM m³/day of gas.

FPSO Cidade de Ilhabela’s Hull Conversion at CSSC Shipyard, in China - Feb/2013

UNIT’s PHYSICAL COMPLETION – Forecast: 41% / Accomplished: 62%

UNIT’s LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 30% / Planned : 56.3%

35

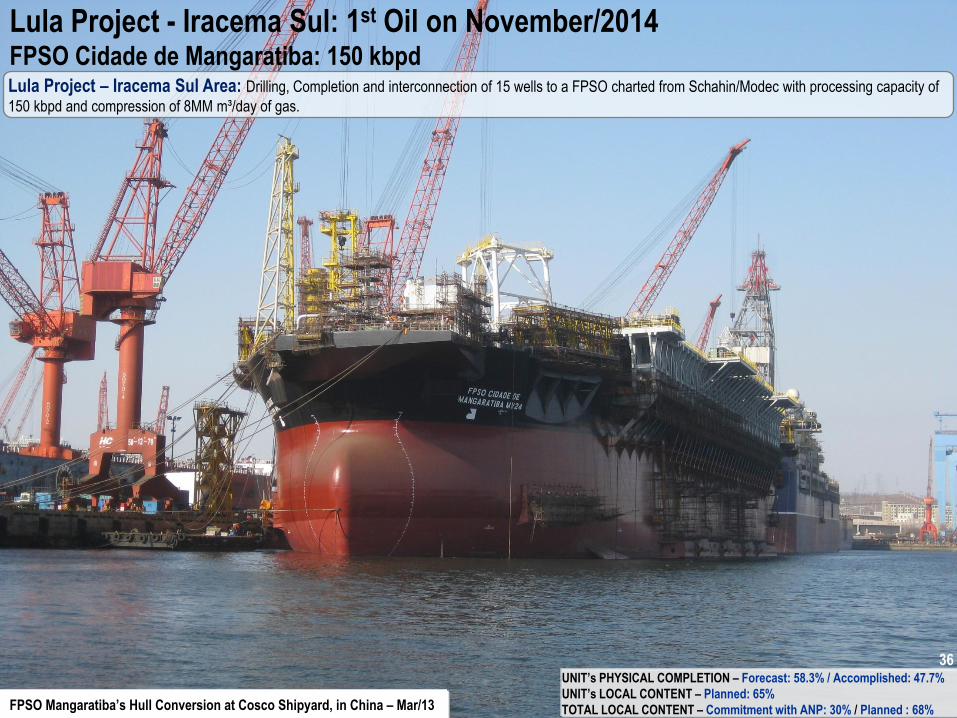

36

Lula Project - Iracema Sul: 1st Oil on November/2014 FPSO Cidade de Mangaratiba: 150 kbpd Lula Project – Iracema Sul Area: Drilling, Completion and interconnection of 15 wells to a FPSO charted from Schahin/Modec with processing capacity of

150 kbpd and compression of 8MM m³/day of gas.

FPSO Mangaratiba’s Hull Conversion at Cosco Shipyard, in China – Mar/13

UNIT’s PHYSICAL COMPLETION – Forecast: 58.3% / Accomplished: 47.7%

UNIT’s LOCAL CONTENT – Planned: 65%

TOTAL LOCAL CONTENT – Commitment with ANP: 30% / Planned : 68%

36

37

2013-2017 BMP: 24 Contracted Units and 15 to Be Contracted between 2013-17

Production Curve in Brazil – Oil and LGN Production

• Roncador III

(P-55) • Iracema

Norte

(Cid. Itaguaí)

• Florim • Júpiter

• Norte Pq.

Baleias (P-58)

Baleia Azul

(Cid. Anchieta)

Sapinhoá Pilot

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Lula NE Pilot

(Cid. Paraty)

• Papa-Terra

(P-63)

• Iracema Sul

(Cid.

Mangaratiba)

• Roncador IV

(P-62)

• Sapinhoá

Norte

(Cid. Ilhabela)

• Bonito

• Franco Leste

• Espadarte III

• Papa-Terra

(P-61)

2.0 ±2% 2.0 2.0

Mill

ion

bp

d

• Lula Alto (*)

• Lula Central (*)

• Lula Sul

(P-66) (**)

• Franco 1

(P-74) (***)

• Carioca

• Lula Norte

(P-67) (**)

• Franco SW

(P-75) (***)

• Lula Ext. Sul

(P-68) (**)

• Lula Oeste

(P-69) (**)

• Franco Sul

(P-76) (***)

•Tartaruga

Verde e Mestiça

• Parque dos

Doces

• Maromba

• Iara Horst

(P-70) (**)

• Franco NW

(P-77) (***)

• Entorno de

Iara (P-73) (**)

• NE de Tupi

(P-72) (**)

• Iara NW

(P-71) (**)

• Sul Pq. Baleias

• Espadarte I

• Deep Waters

Sergipe

• Carcará

Production units in operation (*) Units in final contraction phase

• 24 Production Units contracted, 3 already in operation (**) Hull being built in Rio Grande Shipyard (RS)

(***) Hull being converted in Inhaúma Shipyard (RJ)

• 15 new Production Units to be contracted between 2013-17

38

Exploration Investments in Brazil Target: Keep R/P > 12 Minimizing Dry-Well Risks

Transfer

of Rights

24%

(5.8)

Pre-Salt

70%

(17.1) Post-Salt

Consolidation and delimitation of Pre-Salt and Transfer of Rights areas, besides Post-Salt Sergipe-Alagoas and Espirito Santo basins.

Selective investments in New Frontiers: Equatorial and East Margin.

Ser

gip

e-A

lag

oas

, E

spír

ito

San

to,

New

Fro

nti

ers

Co

nso

lidatio

n an

d

Delim

itation

1.96

1.561.15

0.760.640.58

2007 2008 2009 2010 2011 2012

Finding Cost (US$ / boe)

Petrobras Costs Lower than Majors'

Majors (2007-2011): US$ 3.2 to 4.5 / boe

Equatorial

Margin

East

Margin

US$ 24.3 Billion

6%

(1.4)

Concession Areas March, 2012

Petrobras

Other Companies

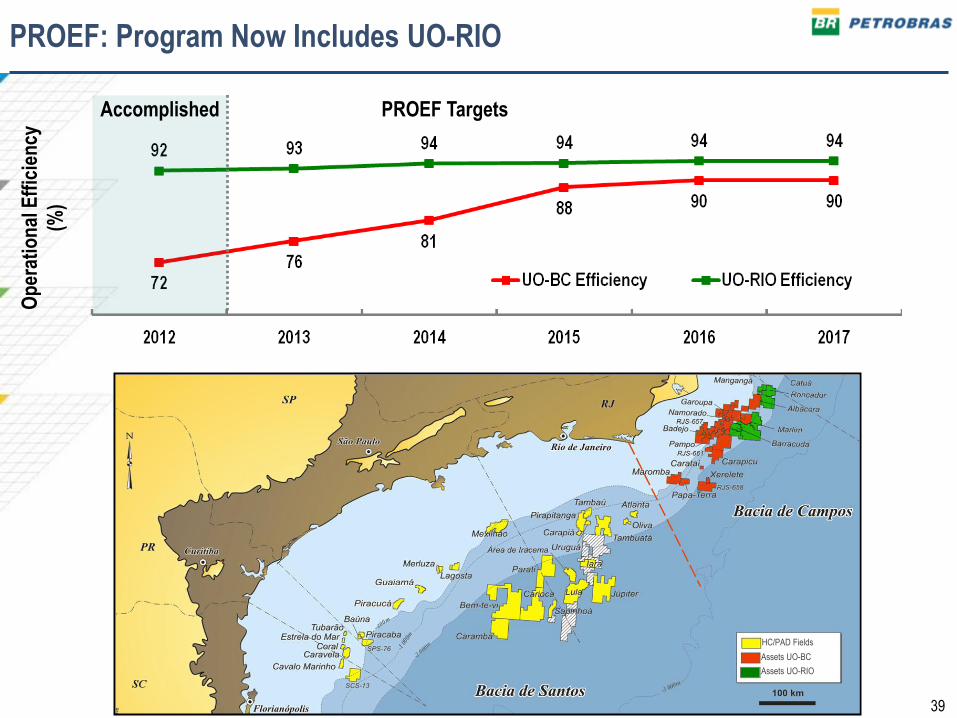

39

Op

erat

ion

al E

ffic

ien

cy

(%)

Accomplished PROEF Targets

PROEF: Program Now Includes UO-RIO

Assets UO-RIO

Assets UO-BC

HC/PAD Fields

40

PRC-Poço: Program to Reduce Well Costs Well Construction is a Relevant Portion in Investments

Exploratory and Production

Development Well Investments

total US$ 75 billion

2013-2017 BMP

Investments

E&P

Other Areas 89.2

147.5

236.7

147.5

106.9

24.3

Infra-structure and Support 16.3

Exploration

Production Development

Brazil E&P

Investments

Increase of drilling rigs fleet and logistic resources

• Petrobras currently has 69 floating drilling rigs for well construction and maintenance in Brazil

Well construction represents:

• 32% of Petrobras investments in 2013-2017 BMP

• 51% of Brazil E&P Investments

41

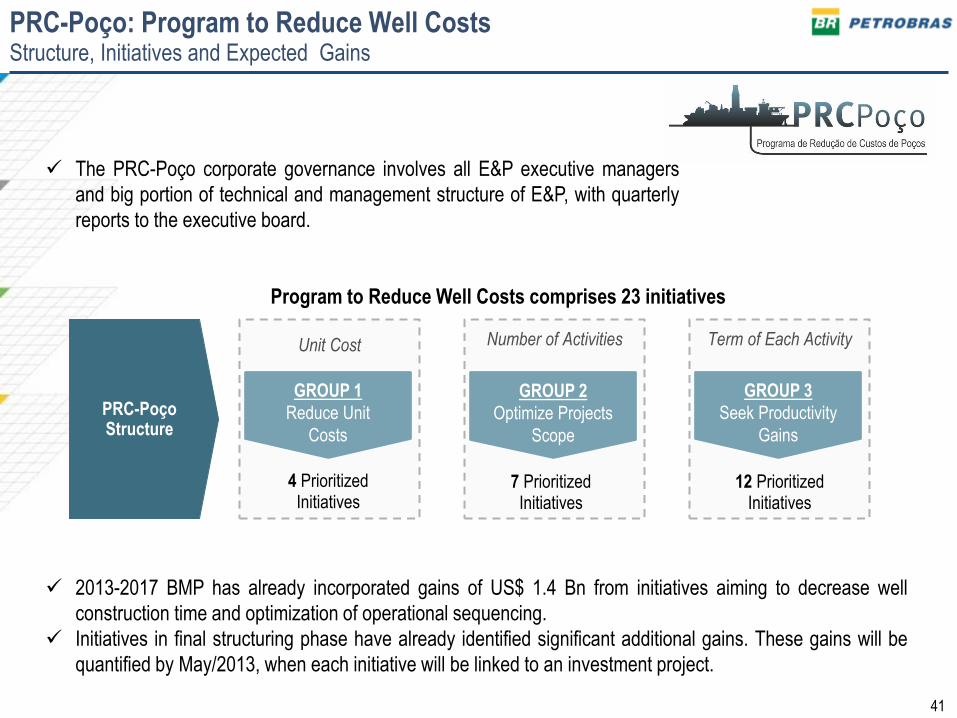

PRC-Poço: Program to Reduce Well Costs Structure, Initiatives and Expected Gains

PRC-Poço Structure

4 Prioritized Initiatives

7 Prioritized Initiatives

12 Prioritized Initiatives

GROUP 1

Reduce Unit

Costs

GROUP 2

Optimize Projects

Scope

GROUP 3

Seek Productivity

Gains

Term of Each Activity Unit Cost Number of Activities

Program to Reduce Well Costs comprises 23 initiatives

2013-2017 BMP has already incorporated gains of US$ 1.4 Bn from initiatives aiming to decrease well

construction time and optimization of operational sequencing.

Initiatives in final structuring phase have already identified significant additional gains. These gains will be

quantified by May/2013, when each initiative will be linked to an investment project.

The PRC-Poço corporate governance involves all E&P executive managers

and big portion of technical and management structure of E&P, with quarterly

reports to the executive board.

42

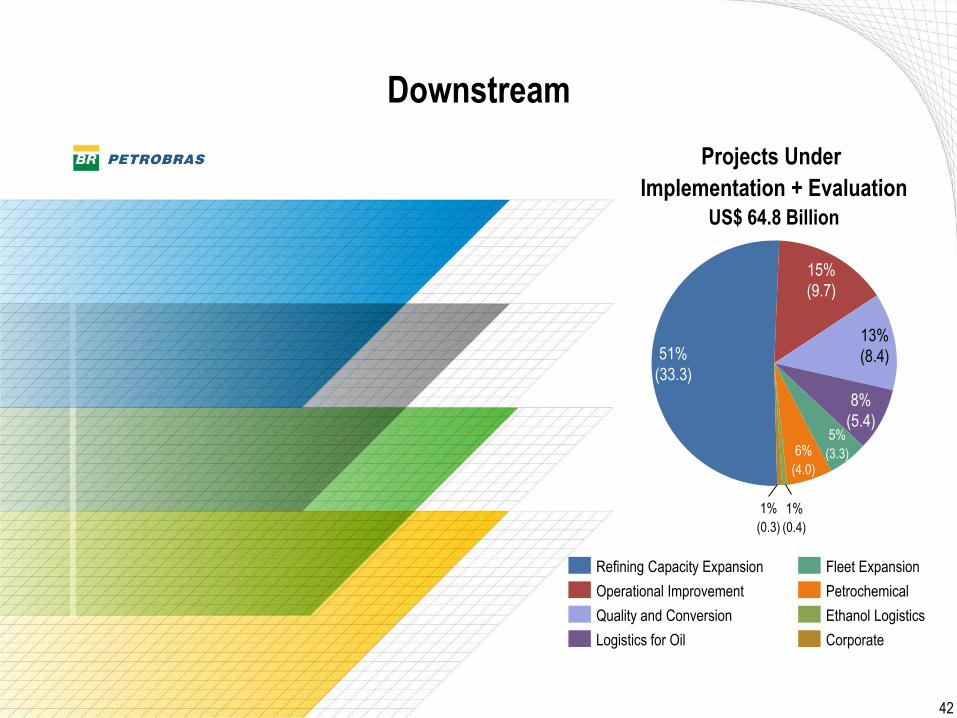

Downstream

8%

(5.4)

13%

(8.4)

15%

(9.7)

51%

(33.3)

Corporate

Fleet Expansion

Ethanol Logistics

Petrochemical

Logistics for Oil

Quality and Conversion

Operational Improvement

Refining Capacity Expansion

Projects Under

Implementation + Evaluation

US$ 64.8 Billion

5%

(3.3) 6%

(4.0)

1%

(0.4)

1%

(0.3)

42

43

Downstream Investments

Refining capacity expansion on the Under

Implementation Portfolio: RNEST (Pernambuco)

and COMPERJ 1st Phase (Rio de Janeiro)

Refining capacity expansion in design phase:

Premium I (Maranhão), Premium II (Ceará) and

COMPERJ 2nd Phase (Rio de Janeiro)

Diesel and Gasoline Quality Portfolio: REPLAN,

RPBC, REGAP, REFAP and RLAM

Fleet expansion: PROMEF – 45

Oil and Oil Products transportation vessels

2013-2017 HIGHLIGHTS

Projects Under Implementation

US$ 43.2 billion

Corporate Ethanol Logistics Fleet Expansion Petrochemical

Logistics for Oil Quality and Conversion Operational Improvement Refining Capacity Expansion

11%

(4.9)

21%

(9.2)

45%

(19.4)

6%

(2,8)

6%

(2.4)

1%

(0.4)

1%

(0.3)

Projects Under Evaluation

US$ 21.6 billion

64%

(13.8)

16%

(3.5)

3%

(0.5)

7%

(1.5)

2%

(0.5)

6%

(2.8)

9%

(3.7)

8%

(1.7)

44

1

1

8

8

9

2

3

8

6

7

8

4 4

6

5

(1) Oil and oil products storage area; (2) Atmospheric distillation unit; (3) Power House; (4) Coking Unit; (5) Intermediary products tanks; (6) Contractors yard; (7) Acid water treatment

unit; (8) Pipelines; (9) Hydrotreatment units

6 6

6 6

7

Northeast Refinery (RNEST): Start-up on November/14 Processing capacity: 230 kbpd

RNEST construction – Feb/13 TOTAL PHYSICAL PROGRESS- Forecast: 70.3% / Accomplished: 70.6%

LOCAL CONTENT- Target: 75% / Planned: 86.5%

44

45

Relevance of refining capacity expansion for the oil product market supply and demand balance

(kbpd)

Demand for oil products in Brazil grows 4.2% p.a. between 2012 and 2020.

Without Premium I, Premium II and Comperj 2nd phase, Brazil will import 29% of its oil product demand

Brazil’s oil product market in 2020

New Refineries Under Implemantation

• Premium I – 1st Phase 300 kbpd - Oct/17

• Premium II - Trem 1 300 kbpd - Dec/17

• Premium I - 2nd Phase 300 kbpd - Oct/20

• Comperj – 2nd Phase

300 kbpd - Jan/18 • Comperj 1st phase: under

construction

165 kbpd - Apr/15

• RNEST: under construction

1st phase - 115 kbpd - Nov/14

2nd phase - 115 kbpd - May/15

New Refineries in Design Phase

Deficit

- 972

Demand

3380

Processing

capacity

2408

46

46%

(4.6)

8%

(0.8)

20%

(2.0)

25%

(2.5)

Gas-chemical plants

LNG

Network

Electric Energy

Projects Under Implementation

+ Under Evaluation

US$ 9.9 billlion

Gas & Energy

46

47

Gas & Energy Investments

Projects Under Implementation

US$ 5.9 billion

Conversion of Natural Gas into fertilizers and

other gas chemical products: UFN III at Três

Lagoas (Mato Grosso do Sul)

Natural gas processing and transportation:

NGPU Cabiúnas (Rio de Janeiro)

Electric energy generation: Thermal Power

Plant Baixada Fluminense (Rio de Janeiro)

LNG Regasification: Bahia Terminal (Bahia)

Units in Design Phase: UFN IV (Espírito Santo)

and UFN V (Minas Gerais)

2013-2017 HIGHLIGHTS

Gas-chemical plants

LNG

Network

Electric Energy

43%

(2.6)

32%

(1.9)

19%

(1.1)

6%

(0.3)

Projects Under Evaluation

US$ 4.0 billion

12%

(0.5)

34%

(1.4) 51%

(2.0)

3%

(0.1)

48

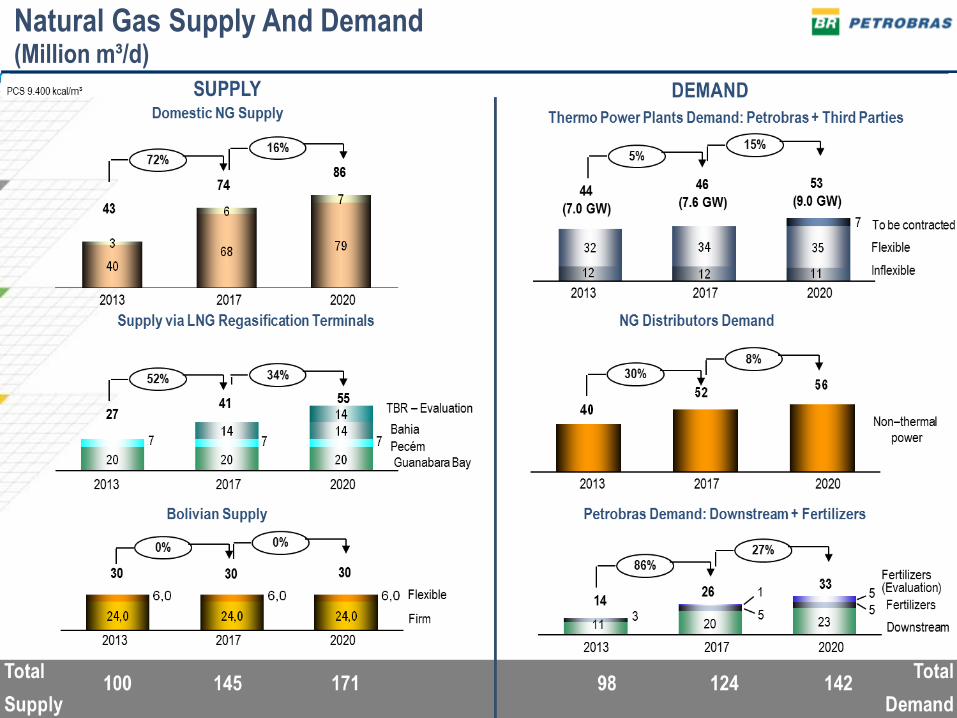

Natural Gas Supply And Demand (Million m³/d)

49

Financiability

49

50

Financial Planning Assumptions Financing analysis only incorporates projects under implementation

Main assumptions for cash flow generation and investment levels

2013-17 BMP is based on constant currencies from 2013.

Brent prices (US$/bbl) US$ 107 in 2013, declining to US$ 100 in the long term

Average exchange rate (R$/US$) R$ 2.00 in 2013, strengthening to R$ 1.85 in the long term

Leverage Limit: < 35% │ Maximum leverage in 2013 and 2014 (34%), declining after 2015

Net debt / EBITDA Limit : < 2.5x │ Limit will be surpassed in 2013 and will fall below 2.0x after 2015

Oil product prices in Brazil Convergence to international prices

Divestments US$ 9.9 billion

Returns on new E&P projects Pre-salt projects breakeven between US$ 40-45/barrel

Big post-salt projects have returns similar to pre-salt’s

No equity issuance Investment grade maintenance

51

Operating Cash Flow and Funding Needs

Divestments and restructurings

Cash utilization

Third-party resources (Debt)

Operating cash flow (after dividends)

Investments

Amortization

Additional financing needs will be funded exclusively through

new debt. No equity issuance is envisaged.

Free cash flow, before dividends, after 2015.

Annual borrowing needs (2013-2017)

Gross – US$ 12.3 billion │Net – US$ 4.3 billion

Net borrowing needs 50% below previous Plan due to:

• 2017 production, versus 2012, leading to higher

operating cash flows

• Declining downstream investments

• Long-term Brent prices (US$ 100 vs US$ 90 in the

previous Plan) and long-term F/X rate (R$ 1.85 vs R$

1.73)

US

$ B

illio

n

246.9

61.3

10.7 9.9

Fontes

165.0

Usos

207.1

39.8

246.9

52

Leverage

• Declining leverage, within the Company’s self-imposed limits

• Net Debt/EBITDA surpasses limit at some points in time, during the Plan period

BMP Target (< 35%)

2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Leverage Net Debt/EBITDA

BMP Target (< 2,5x)

53

The End