Petrobras and The Tanker Future in Brazil. - Intertanko · PETROBRAS Distribuidora S.A. (BR) Retail...

27

Elizio Araújo Neto Executive Manager for Transpetro Fleet Modernization and Expansion Program - PROMEF Petrobras and The Tanker Future in Brazil. INTERTANKO 2012 31/10/2012

Transcript of Petrobras and The Tanker Future in Brazil. - Intertanko · PETROBRAS Distribuidora S.A. (BR) Retail...

Elizio Araújo Neto

Executive Manager for Transpetro Fleet Modernization and Expansion Program -PROMEF

Petrobras and The Tanker Future in Brazil.

INTERTANKO 2012

31/10/2012

PETROBRAS

BOARD OF DIRECTORS

FISCAL COUNCIL

GENERAL OMBUDSMAN`S OFFICE

INTERNAL AUDITORS

EXECUTIVE BOARD

CEOBUSINESS STRATEGY AND PERFORMANCE

NEW BUSINESS

HUMAN RESOURCES

MANAGEMENT SYSTEM DEVELOPMENT

LEGAL

INSTITUCIONAL COMMUNICATION

BUSINESS COMMITTEE

CEO CABINET GENERAL SECRETARIAT

PETROBRAS

Finance Gas & Energy E&P (Upstream) Downstream International Services

CorporateFinancial Planning & RiskManagement

Finances

Tax

InvestorRelations

Corporate

Marketing &Trading

Natural GasLogistics andParticipations

EnergyDevelopment

Corporate

ProductionEngineering

Services

Exploration

North-Northeast

Corporate

Logistics

Refining

Marketing & TradingPetrochemicals& Fertilizers

Corporate

TechnicalBusiness Support

BusinessDevelopment

South Cone

Americas, Africa & Eurasia

Safety, Environment & Health

Procurement

Research & Development(Cenpes)

Engineering

Informationtechnology

South-Southeast

EnergyOperationsandParticipations

SharedServicesTRANSPETRO

(49 new ships) 2

EBNs(39 new ships)

Main Subsidiaries

Company ActivityPETROBRAS Distribuidora

S.A. (BR) Retail distribution and marketing of oil byproducts.

PETROBRAS Energia Participaciones S.A.

(PESA)

Holds several activities in Argentina, Venezuela, Peru, Bolivia and Ecuador.

PETROBRAS Quimica S.A. (PETROQUISA) Operates in the petrochemical industry.

PETROBRAS Gás S.A. (GASPETRO) Responsible for trading Brazilian and imported natural gas.

PETROBRAS Transporte S.A. (TRANSPETRO) Builds and operates our transportation network.

PETROBRAS Americas Inc. Participates in the exploitation of oil fields in the Gulf of Mexico and owns 50% of the Pasadena Refinery, in Texas.

PETROBRAS International Finance Company (PIFCo) Int

finermediary between PETROBRAS and oil suppliers, obtains ancings facilitating commercial operations

PETROBRAS Bio Fuels Responsible for the biofuels programmes.

Independent companies

with their own executive

boards, linked to the head

office.

3

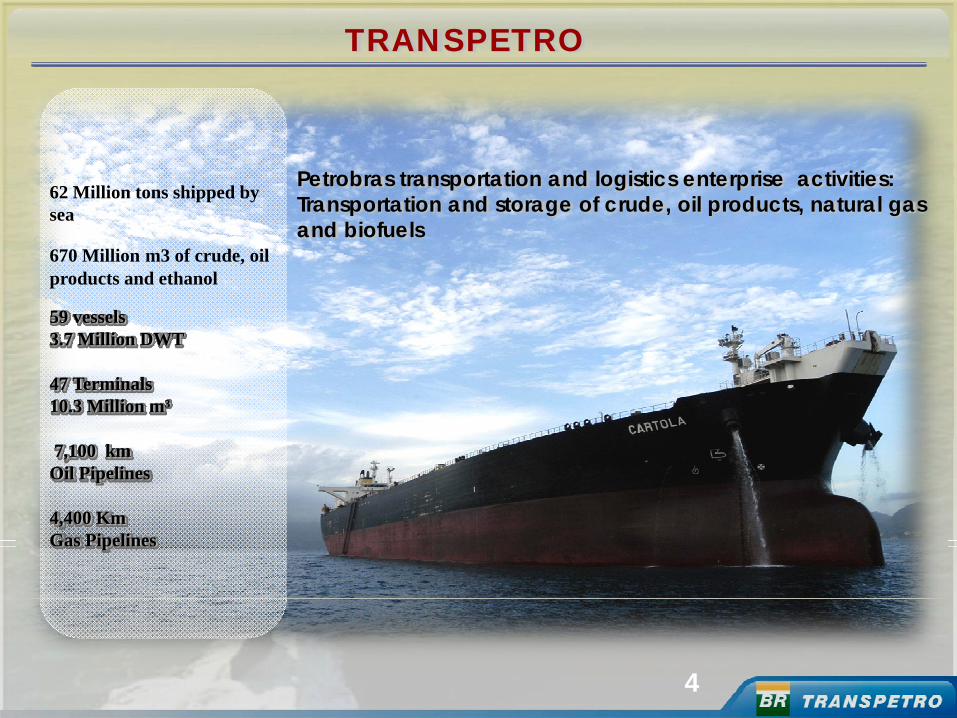

TRANSPETRO

Petrobras transportation and logistics enterprise activities: Transportation and storage of crude, oil products, natural gas and biofuels

62 Million tons shipped by sea

670 Million m3 of crude, oil products and ethanol

59 vessels3.7 Million DWT

47 Terminals10.3 Million m³

7,100 km Oil Pipelines

4,400 Km Gas Pipelines

4

TRANSPETROFISCAL COUNCIL

EXECUTIVE BOARD

BOARD OF DIRECTORS

INTERNAL AUDITORS

CEO

NATURAL GAS TERMINALS and PIPELINES MARITIME TRANSPORT FINANCIAL and ADMINISTRATIVE

CEO CABINET OMBUDSMAN OFFICE

Terminals

Pipelines

Natural Gas

HES

Maritime Transportation

HES

Financial

Accounting

Logistics and Operations

Commercial

HES

Logistics and Operations

Commercial

Commercial Administrative Services

Studies and Performance

INSTITUCIONALCOMMUNICATIONS

LEGAL

Studies and Performance

Studies and Performance

SERVICES AND ENGENEERING

CORPORATE

GENERAL SECRETARIAT

HUMAN RESOURCES

Vetting and Inspection

Pipeline Emergency Repairs

Compliance

Compliance

FLEET MODERNIZATION PROGRAM

FRONAPEINTERNATIONAL CO. - FIC

PROMEF

5

TRANSPETRO Fleet Challenges (2003)

Modernize and expand the TRANSPETRO fleet of tankers, reaching 100% of coastal shipping and 50% of ocean going transportation.

Tasks and challenges

• To reconstruct Brazil’s shipbuilding industry on competitive bases.

• To re-shape the logic underpinning Brazil’s transportation matrix.

• Almost 60% of Brazil’s transportation matrix is road-based, which is twice

as expensive as rail transportation, and four times dearer than maritime

transportation.

• New vessels required for coastal shipping and ocean going

transportation.

• Qualify the work force.

• Lack of seamen to the new ships. (They must be Brazilian by law)

6

PROMEF

To modernize and expand the TRANSPETRO fleet of tankers, reaching 100% of coastal shipping and 50% of ocean going transportation.

• SCOPE: construction of 49 vessels

• PROGRAM PHASES:

PHASE 1: construction of 26 vessels (10 Suezmax, 5 Aframax, 4

Panamax, 4 Products and 3 LPG)

PHASE 2: construction of 23 vessels (4 Suezmax DP, 3 Aframax DP, 8

Products, 5 LPG and 3 Bunker)

• 40,000 direct jobs

7

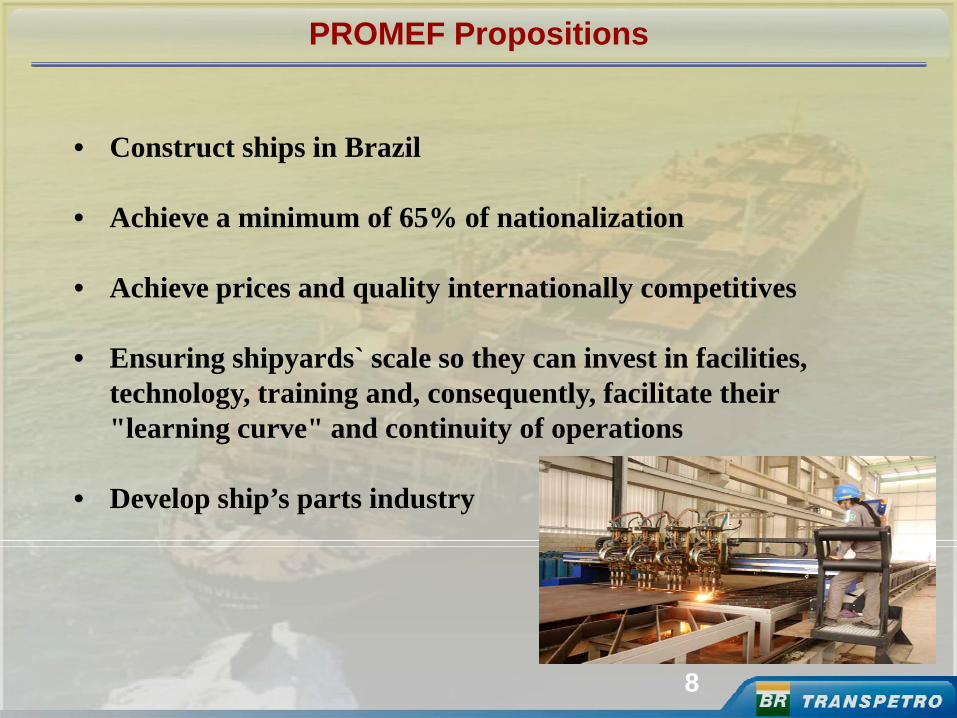

PROMEF Propositions

• Construct ships in Brazil

• Achieve a minimum of 65% of nationalization

• Achieve prices and quality internationally competitives

• Ensuring shipyards` scale so they can invest in facilities, technology, training and, consequently, facilitate their "learning curve" and continuity of operations

• Develop ship’s parts industry

8

• Integrates Petrobras Strategic Plan on the development of logistics for biofuels;

• Modal ethanol logistics system that will integrate BR Distribuidora trucks and wagons, Petrobras pipelines and terminals and Transpetro convoys;

• Construction of 20 riverine convoys, each composed of 4 barges and 1 pusher tugboat to sail through the watershed of biofuels by the Tietê-Paraná rivers and its tributaries;

PROMEF Waterway

9

Araçatuba

Anhembi

PR

SP

MS

Senador Canedo

REPLAN

Ilha D’ água

REDUC

Ribeirão Preto

Uberaba

MG

RJ

São Sebastião

TaubatéPres. Epitácio

REVAP

Logistic Integrated System

10

PETROBRAS EBNs Program

11

EBN – Empresa brasileira de navegação (Brazilian Shipping Company)

Hiring, by Petrobras, a 15 years TCP contract to any Brazilian Shipping Company interested in the construction of listed ships in Brazilian Shipyards.

• SCOPE: construction of 39 vessels

• PROGRAM PHASES:

EBN 1: construction of 19 vessels (10 Products, 3 LPGs and 5 Bunkers)

EBN 2: construction of 20 vessels (6 Panamax, 10 Products and 4 LPGs)

PETROBRAS EBNs Program

12

PETROBRAS EBNs Program

13

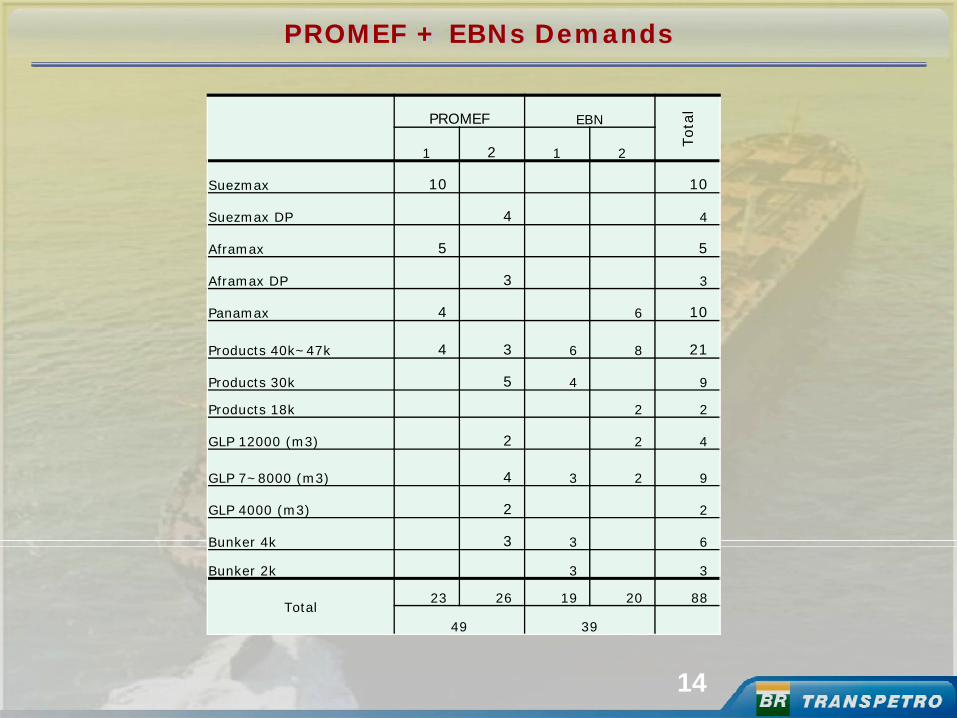

PROMEF + EBNs Demands

PROMEF EBN

Tota

l

1 2 1 2

Suezmax 10 10

Suezmax DP 4 4

Aframax 5 5

Aframax DP 3 3

Panamax 4 6 10

Products 40k~47k 4 3 6 8 21

Products 30k 5 4 9

Products 18k 2 2

GLP 12000 (m3) 2 2 4

GLP 7~8000 (m3) 4 3 2 9

GLP 4000 (m3) 2 2

Bunker 4k 3 3 6

Bunker 2k 3 3

Total23 26 19 20 88

49 39

14

Brazilian E&P Profile

PETROBRAS Records in Deep Water

Around 65% of thearea of PETROBRASoffshore explorationblocks is in waterdepths of more than400 meters.

Consequently, in recent years the company has increased its exploration drilling activities in increasingly deep water.

15

The Brazilian pre-salt reservoirs are formed by carbonatic rocks about whichvery little is known. Additionally, the biggest hydrocarbon accumulationsfound in the Santos Basin are located in ultra-deep waters, under a thicklayer of salt which, in certain places, is more than 2,000 meters deep. Thesecharacteristics represent an unprecedented technological challenge in theindustry.

All of these obstacles show it will be necessary to make a major effort to createthe technological solutions that will allow for production to be developedeconomically in this new province. In a scenario in which discoveries of thistype are becoming increasingly rare, developing new solutions and findingways to make the best use of them is what makes the difference.

Pre-salt Fields Overview

16

Pre-salt Fields Overview

The discovery of the biggest domestic oil province was the most significant factof 2007, one that has the potential to rank Brazil among the countries with thebiggest oil and gas reserves in the world. The called pre-salt layer, spreadsthrough the Santos, Campos and Espírito Santo Basins, ranging from the coast ofSanta Catarina to the coast of Espírito Santo, measuring 800km in length and200km in width.

17

Perspectives

18

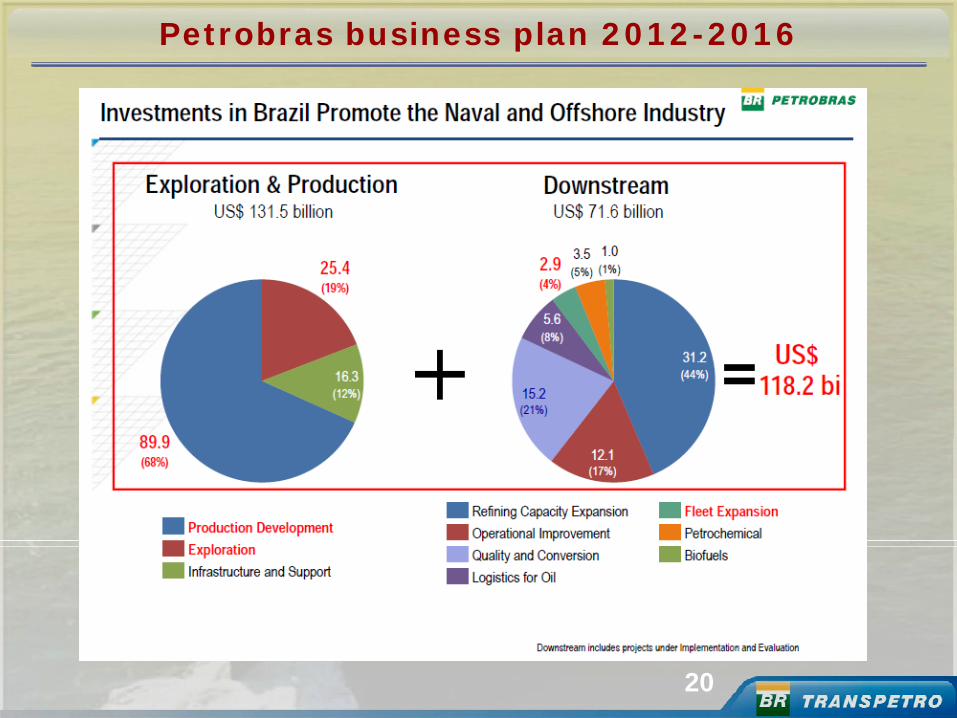

Petrobras business plan 2012-2016

19

Petrobras business plan 2012-2016

20

Petrobras needs to fulfill Presalt demands

21

PETROBRAS Needs Overview

Download a Petrobras CEO presentation from

www petrobras com br

Choose:1. English2. Investors3. Presentations4. 20/092012 - Apresentação Rio Oil and Gas / CEO Maria

das Graças Silva Foster

22

Brazilian Shipbuilding & Offshore Industry

23

Brazilian Opportunities Overview

• each year 4,600 ships sail along the

Brazilian coastline

Main maritime trades

COASTLINE AND MAIN RIVERS• 95% of its foreign trade depends on

maritime transportation

• 8,000 km (5,000 miles) of coastline

• 42,000 km (26,000 miles) of navigable rivers

24

BRAZILIAN OPPORTUNITIES OVERVIEW

The planned expansion are unable to respond in full to future demands prompted by Brazil’s pre-salt oilfields and the expansion of the biofuels market. So, we still need:

• To build new shipyards – vessels, rigs, semi-sub, FPSOs, FSOs, offshore support vessels will be needed.

• To build repair shipyards – there are a good number of vessels operating in Brazilian waters or passing by, with no modern repair facility currently available.

• To establish industries to supply equipment, parts, service and repair for shipyards and ship-owners.

• To establish support industries for shipbuilding – specialized contractors.

25

Brazil – An Attractive Investment Opportunity

Natural resources – oil, bio-fuels, grain, ore and minerals, water and land.

Economical stability – regulated bank andfinancing system, inflation and currencyunder control, sizeable internationalreserves with little net debt.

Social conditions – political stability, consolidated democractic institutions, social programs.

26

www.transpetro.com.br

Thank You !

27