Peru: Economic Outlook - mef.gob.pe · PDF filePeru: Economic Outlook Luis Miguel Castilla...

20

Peru: Economic Outlook Luis Miguel Castilla Minister of Economy and Finance May, 2013

Transcript of Peru: Economic Outlook - mef.gob.pe · PDF filePeru: Economic Outlook Luis Miguel Castilla...

Peru: Economic Outlook

Luis Miguel Castilla Minister of Economy and Finance

May, 2013

2

Peru is among the fastest growing economies with lowest inflation

• Peru’s story of success is based on: Sound economic policies

Sustained increases in productivity Private investment as the engine for growth Trade integration with the World

• Economic growth has led to a sustained reduction in poverty and an increase of the middle class.

Peru’s macroeconomic performance over the past decade has been exceptional

3

LATAM: Real GDP Growth and Inflation (2002-2012)

Source: MEF, IMF

LATAM: GDP Growth and Inflation (Average % change)

During 2002-2012, Real GDP grew at an average annual rate of 6.4 percent (the highest in Latin America), and the annual inflation rate fell to 2.8 percent on average (the lowest in Latin America).

GDP Inflation

Peru 6.4 2.8

Chile 4.4 3.3

Mexico 2.3 4.4

Colombia 4.5 4.8

Brazil 3.6 6.4

Argentina 5.6 11.5

0

2

4

6

8

10

12

14

0 1 2 3 4 5 6 7

Avera

ge In

flatio

n r

ate

(%

)

Average Real GDP Growth (%)

Peru

Argentina

Chile

Colombia

Brazil

Mexico

Economic growth has reduced poverty

Source: INEI, MTPE.

More adequate employment (Metropolitan Lima,% of total employment)

2012 2002

Reduction of Poverty and Extreme Poverty

(% of population)

More Decentralized Jobs (Urban Peru firms with 10 or more employees)

(Accumulated% change Jan-Dec. 2012 / Jan-Dec. 2002)

0

20

40

60

80

100

120

Caja

marc

a

Pucallp

a

Pis

co

Iquito

s

Chin

cha

Tacna

Chic

layo

Cusco

Metr

. Lim

a

Tara

po

to

Huancayo

Are

quip

a

Puno

Ica

Tru

jillo

Piu

ra

Peru:average growth 61.4%

39

61

Adequate employment

Underemployment59

41Adequate

employmentUnderemployment

58.755.6

49.1

42.4

37.333.5

30.827.8

25.8

16.4 15.813.8

11.2 10.9 9.57.6 6.3 6.0

0

10

20

30

40

50

60

70

2004 2005 2006 2007 2008 2009 2010 2011 2012

Total poverty Extreme poverty

4

Risk factors

5

• Intensification of the Eurozone crisis.

• Slowdown in China’s economic performance.

• Weaker U.S. growth.

• Plummeting commodity prices (60% of total exports).

• Less private investment due to a deterioration in expectations.

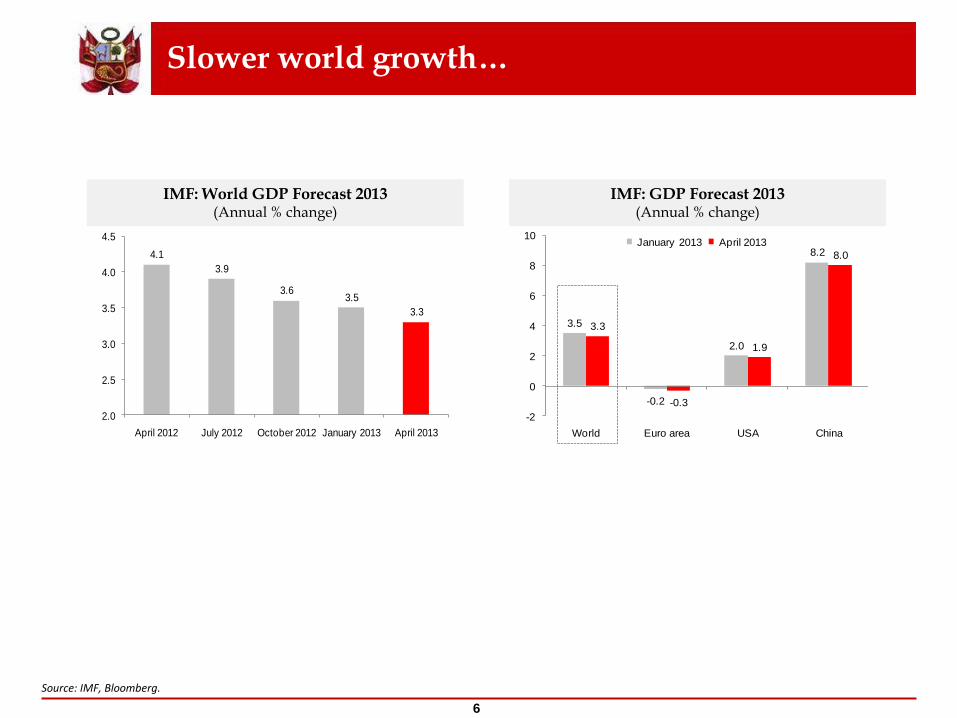

Slower world growth…

Source: IMF, Bloomberg.

IMF: GDP Forecast 2013 (Annual % change)

IMF: World GDP Forecast 2013 (Annual % change)

3.5

-0.2

2.0

8.2

3.3

-0.3

1.9

8.0

-2

0

2

4

6

8

10

World Euro area USA China

January 2013 April 20134.1

3.9

3.63.5

3.3

2.0

2.5

3.0

3.5

4.0

4.5

April 2012 July 2012 October 2012 January 2013 April 2013

6

... is affecting the economic performance of Latin America

Source: IMF, Bloomberg.

7

Chile and Mexico: GDP (Annual % change)

Brazil and Colombia: Industrial Production (Annual % change)

-11.5

-20

-15

-10

-5

0

5

10

15

20

25

M-09 M-10 M-11 M-12 M-13

Brazil Colombia

-3.3

Peru: GDP (Annual % change)

4.1

0.8

-10

-5

0

5

10

06Q1 07Q1 08Q1 09Q1 10Q1 11Q1 12Q1 13Q1

Chile Mexico

-2

0

2

4

6

8

10

12

06Q1 07Q1 08Q1 09Q1 10Q1 11Q1 12Q1 13Q1

4.8

Metals: Prices record strong downward corrections in short periods

1/ Prices updated to May 22, 2013. Source: Bloomberg.

8

Copper Price (US$ cents/pound)

Gold Price (US$/troy ounce)

Metal Prices (Prices, % change)

300

340

380

420

460

500

E-11 A-11 M-12 O-12 M-13

Prices fell 9.8% between 10 and

23 April

1,300

1,400

1,500

1,600

1,700

1,800

1,900

E-11 A-11 M-12 O-12 M-13

Prices fell 12.4% between 10 and

16 April

Closing Price % change % change

22.05.13 vs. 31.12.12 vs. 22.05.12

Copper US$ cents/pound 339 -5.5 -3.8

Gold US$/troy ounce 1,409 -15.0 -11.0

Lead US$ cents/pound 93 -12.2 6.5

Zinc US$ cents/pound 83 -9.5 -3.1

Silver US$/troy ounce 22 -26.5 -20.9

The share of commodities in economic activity and fiscal revenues is less than in other peer countries

9

Sources: IMF, 2012, “Fiscal Frameworks for Resource Rich Developing Countries”, May. IDB, 2013, “Rethinking reforms, How Latin America and the Caribbean Can Escape Suppressed World Growth”, March.

Commodity Revenue (% of total GDP, Average 2006-2010)

Estimated impact on total revenue caused by a fall of 25% in commodity prices

19

17

11

8

7

6

4

Venezuela

Trinidad & Tobago

Bolivia

Mexico

Ecuador

Chile

Peru

-4,5 -4,0 -3,5 -3,0 -2,5 -2,0 -1,5 -1,0 -0,5 0,0

Argentina

Colombia

Peru

Chile

Mexico

Venezuela

Trinidad & Tobago

Bolivia

Ecuador

Percent of potential GDP

411

18 20 2327

33

44

6875

82 8690

0

20

40

60

80

100

Saud

i A

rab

ia

Chile

United

Ara

b

Em

irate

s

Peru

Chin

a

Austr

alia

Co

lom

bia

Mexic

o

Bra

zil

Isra

el

Germ

any

Canad

a

United

Kin

gd

om

Peru has strong economic fundamentals to face external shocks

Peru: Overall Balance of Non-Financial Public Sector (% of GDP)

6 years of fiscal surpluses in the last 9 years

Peru: Net International Reserves (NIR)1

(US$ Million)

Country Risk2 (Basis points, average from May 1st to May 22nd, 2013)

Public Debt

(% of GDP)

8,180

17,275

67,060

0

20,000

40,000

60,000

80,000

2000 2006 2013

NIR for 20 months of imports

8 times

34% of GDP

1/ Updated on May 17th, 2013. 2/ Credit Rating by Moody’s. Source: BCRP,MEF, Bloomberg.

-0.3

2.3

2.9

2.4

-1.3

-0.3

1.92.2

0.7

-2.0

0.0

2.0

4.0

2005 2006 2007 2008 2009 2010 2011 2012 2013e

10

123

125

128

135

135

148

152

168

172

268

341

Peru (Baa2)

Philippines (Ba1)

Colombia (Baa3)

Chile (Aa3)

Mexico (Baa1)

China (Aa3)

Russia (Baa1)

Brazil (Baa2)

Indonesia (Baa3)

Emerging Economies

Latin America

0

1

2

3

4

5

6

7

8

9

10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 F 2014 F 2015 F 2016 F

Peru can grow around its potential: 6.0-6.5%

11

Gross Domestic Product (Annual % change)

F: Forecast Source: BCRP, MEF.

Average Growth 2002-2012 6.4%

Ample potential for further economic growth and diversification

0

5

10

15

20

25

30

35

40

45

Peru Chile

0

2

4

6

8

10

Peru Chile Brazil

0

2

4

6

8

10

Peru Chile

0

1

2

3

4

5

6

Peru Colombia Chile Argentina

0

5

10

15

20

25

30

35

40

45

Peru Chile Argentina Brazil

0

10

20

30

40

50

60

Peru Chile Brazil Argentina

Exports of Wood and Paper 2012 (US$ Billion)

Exports of Copper 2012 (US$ Billion)

Agricultural Exports 2012 (US$ Billion)

Exports of Services 2012 (US$ Billion)

Tourist Arrivals 2012 (Million of people)

High-technology Exports 20111

(US$ per capita)

1 / According to the World Bank, high-technology exports are products with high R&D intensity, such as in aerospace, computers, pharmaceuticals, scientific instruments and electrical machinery. Source: SUNAT, BCRP, ministries of commerce of countries, World Bank.

12

There are important investment projects that will reach maturity in the short and medium term

Source: BCRP, MINEM, MTC, PROINVERSION, OSINERGMIN, Apoyo Consultoria.

13

Mining Region Las Bambas – Cu (Xstrata Copper) Apurimac Cerro Verde extension – Cu (Freeport-MacMoran Copper) Arequipa Toromocho – Cu (Chinalco) Junin Constancia – Cu (Hudbay) Cusco Marcona extension – Fe (Shougang) Ica Hydrocarbons Energy security and southern gas pipeline (Called) Cusco, Arequipa, Moquegua Block 58 (Petrobras) Cusco NGL & gas pipeline extension (TGP) Cusco Block 56 & 88 extension (Pluspetrol) Cusco Block 57 (Repsol & Petrobras) Junin, Cusco, Ucayali Block 67 (Perenco & PetroVietman) Loreto Block Z1 (BPZ, Pacific Rubiales Energy) Tumbes, Piura Electricity Chaglla Hydroelectric – 406MW (Odebrecht) Huanuco Cerro del Águila Hydroelectric – 402MW (Inkia Energy) Huancavelica Molloco Hydroelectric – 300MW (Corsan /Engevix/Enex) Arequipa Cheves Hydroelectric – 168 MW (SN Power) Lima Quitaracsa I Hydroelectric – 112MW (GDF Suez) Ancash Ilo Thermoelectric – 569MW (GDF Suez) Moquegua 220 kV Moyobamba – Iquitos transmission line and

associated substations (Called) Loreto, San Martin

Infrastructure Metro of Lima & Callao – Section 2 (Called) Lima Vía Parque Rimac (OAS S.R.L.) Lima Muelle Norte port modernization (APM Terminals) Lima Paita port extension (Tertir Terminais/Cosmos/Translei) Piura Longitudinal de la Sierra road – Section 2 (Called) Cajamarca, La Libertad WWTP & Outfall La Chira (Acciona Agua, GYM) Lima IIRSA Centro Road – Section II (Deviandes) Lima, Junin, Pasco Yurimaguas port terminal (Hidalgo e Hidalgo) Loreto

Sustained high private investment is key to ensure a GDP growth of about 6% per year

14

Source: MEF, Apoyo Consultoría, BCRP, SUNAT, INEI.

Total Investment: 2012 (% of GDP)

21.2

24.4 24.6 2526.7

0

5

10

15

20

25

30

Brazil Chile Colombia Mexico Peru

-1.6

6.2

11.6

-4

-2

0

2

4

6

8

10

12

1982-1991 1992-2001 2002-2012

Private Investment (Average % change )

Private Investment (Annual % change)

GDP (Annual % change )

11.6

0

2

4

6

8

10

12

14

Average2002-2012

t t+1 t+2

Baseline Stress

6.4

2

3

4

5

6

7

Average2002-2012

t t+1 t+2

Baseline Stress

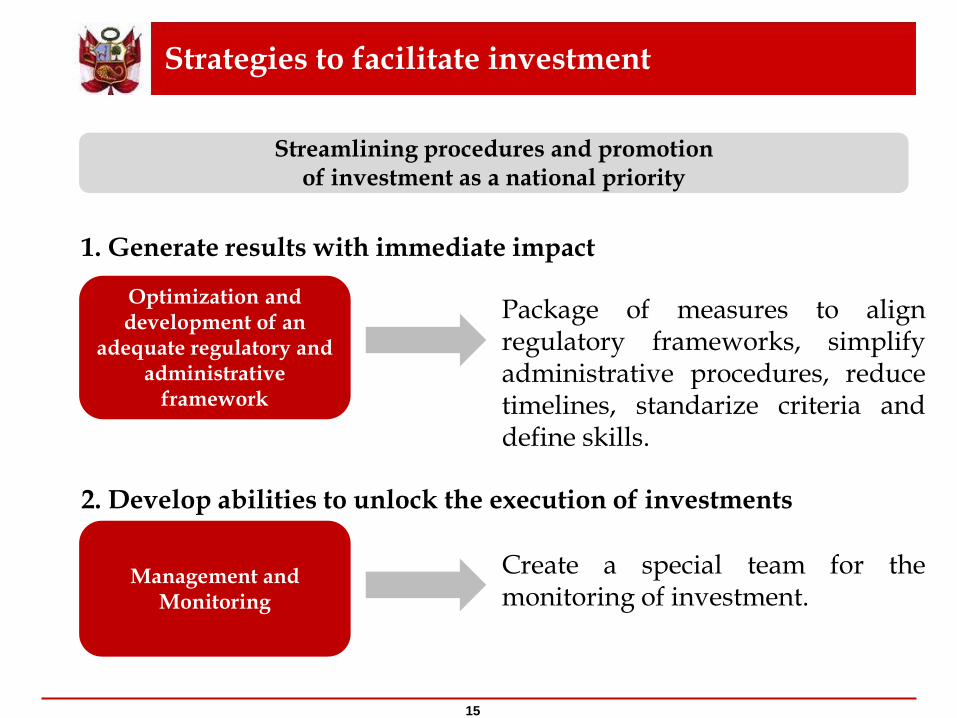

Strategies to facilitate investment

15

Package of measures to align

regulatory frameworks, simplify administrative procedures, reduce timelines, standarize criteria and define skills.

Create a special team for the

monitoring of investment.

Optimization and development of an

adequate regulatory and administrative

framework

Management and Monitoring

Streamlining procedures and promotion of investment as a national priority

1. Generate results with immediate impact

2. Develop abilities to unlock the execution of investments

Effects of initial normative measures: the case of Environmental Impact Assessment (EIA)

16

ANA: Environmental management instruments assessed 2013Q1

(Number of records)

ANA: Investment of Environmental management instruments assessed 2013Q1

(US$ million)

166 projects

US$ 3,307 million

Source: MEF, ANA (National Agency for Water)

0

10

20

30

40

50

60

Aprobado Observado

GORE MEM-AAE MEM-AAM MINAG

MINCETUR MVCS PRODUCE

56

(34%)

110

(66%)

Approved Observed

The measures will double the execution of investment in the same period of time

9701148

633414

2091 31

0

300

600

900

1200

1500

1800

Aprobado Observado

MVCS MINCETUR MEM-AAM MEM-AAE

1,694

(51%)

1,613

(49%)

Approved Observed

Law 30025 to promote investment in infrastructure

17

Railway

Line 1 & 2 of the Basic Netw ork of the Metro of Lima and Callao.

Road

Highw ay of Sol (Trujillo - Chiclay o - Piura -Sullana).

Road sections multimodal ax is Northern Amazon of “Plan de accion para la integracion de

infraestructura regional sudamericana - IIRSA” .

Section Nº 1 South Interoceanic Highw ay Corridor, Peru Brazil (San Juan de Marcona -

Urcos).

Section Nº 2 South Interoceanic Highw ay Corridor, Peru Brazil (Urcos - Inambari).

Section Nº 4 South Interoceanic Highw ay Corridor, Peru Brazil (Inambari - Azangaro).

Section Nº 5 South Interoceanic Highw ay Corridor, Peru Brazil (Ilo - Puno - Juliaca,

Matarani - Juliaca- Azangaro).

Road IIRSA Centro - Section Nº 2 (Bridge Ricardo Palma- La Oroy a - Huancay o & La

Oroy a - Cerro de Pasco).

Road section Nuev o Mocupe - Cay alti - Oy otun -Puente Las Delicias.

Road section Chancay /Variante Pasamay o - Huaral - Acos.

Red Vial Nº 4: Section Pativ ilca - Santa - Trujillo & Puerto Salav erry - Empalme PN1N.

Red Vial Nº 5: Section Ancon - Huacho - Pativ ilca, North Pan-American Highw ay .

Red Vial Nº 6: Section Bridge Pucusana - Cerro Azul - Ica, South Pan-American Highw ay

Longitudinal de la Sierra road: Chiple -Cuterv o - Cochabamba - Chota - Bambamarca-

Hualgay oc - Yanacocha, Cajabamba -Sausacocha, Huamachuco - Shorey - Santiago de

Chuco - Pallasca - Cabana - Tauca, Huallanca- Caraz, Huallanca - La Union -

Huanuco, Izcuchaca - May occ - Huanta Ay acucho -Andahuay las - Abancay .

Road Huancav elica-Santa Inés-Castrov irrey na - Pampano & Santa Ines-Rumichaca.

Road Imperial - Pampas - May occ.

Road Huancav elica - Lircay .

Longitudinal de la Selv a road “Puente Integracion - San Ignacio - Perico, Juanjui -

Campanilla - Pizana - Tocache - Von Humboldt- Puerto Bermudez - Villa Rica - Puente

Reither- Satipo - Mazamari - Puerto Ocopa” .

Port

Paita Port Terminal

San Martin Port Terminal.

Tourism

Gondolas Sy stem of Kuelap.

Others

Fishing complex La Puntilla.

Road

Road Cusco - Quillabamba.

Road Trujillo - Shiran - Shorey .

Road Quinua - San Francisco.

Road Cajamarca - Celendin - Balzas, Soritor - La Calzada.

Road Pimentel - Chiclay o.

Road Lima - Canta - Huay llay - Vicco - Emp. PE-3N (Shelby ).

Ev itamiento Highw ay - Chimbote.

Road Chongoy ape - Cochabamba.

Road La Tina - La Tina - Cachaquito.

Road Quilca - Matarani - Ilo.

Road Cañete - Lunahuana, Roncha -Chupaca - Puente Pilcomay o.

Road Tarata - Mazocruz - Ilav e.

Road Huamachuco - Bridge Pallar – Abra Naranjillo.

Ev itamiento Highw ay - Urcos.

Road Imata - Oscollo - Negromay o - San Genaro - Descanso - Sicuani & Negro May o-

Ocoruro - Pallpata - Yauri.

Road Las Vegas - Tarma.

Road Rio Seco - El Ahorcado - Say an.

Road Mala - Calango - La Capilla.

Linea Amarilla.

Southern Highw ay Project.

New Highw ay Projects, Lima city .

Arequipa La Joy a Regional Road, Arequipa.

Construction of Trunk Road Interconectora: Miraflores, Alto Selv a Alegre, Yanahuara,

Cay ma & Cerro Colorado - Arequipa.

Integrated Transport Sy stem SIT, Arequipa.

Rehabilitation and pav ing of the National Route Highw ay Nº PE - 18, Section Oy on -

Yanahuanca - Ambo.

Airport

“Capitan FAP Pedro Canga Rodriguez” Airport, Zarumilla, Tumbes.

“Capitan FAP Guillermo Concha Iberico” Airport, Castilla, Piura.

“Capitan FAP Victor Montes” International Airport, Talara, Piura.

“Capitan FAP José Abelardo Quiñones Gonzalez” Airport, Chiclay o, Lambay eque.

“Capitan FAP Carlos Martinez Pinillos” Airport, Trujillo, La Libertad.

“May or General FAP Armando Rev oredo Iglesias” Airport, Baños del Inca, Cajamarca.

“Comandante FAP German Arias Graziani” Airport, Carhuaz, Ancash.

“Coronel FAP Francisco Secada Vignetta” International Airport, Iquitos city , Loreto.

“Cadete FAP Guillermo del Castillo Paredes” Airport, Tarapoto city , San Martin.

“Capitan FAP Dav id Abensur Rengifo” Airport, Pucallpa city , Ucay ali.

Pisco International Airport, Pisco city , Ica.

“ Inca Manco Capac” International Airport, Juliaca city , Puno.

“Alfredo Rodriguez Ballon” International Airport, Arequipa city .

“Coronel FAPAlfredo Mendiv il Duarte” Airport, Ay acucho city

“Padre Aldamiz” International Airport, Puerto Maldonado city , Madre de Dios.

“Coronel FAP Carlos Ciriani Santa Rosa” International Airport, Tacna city .

Aerodrome of Puerto May o - Pichari.

Border

Relocation, construction and equipment of the border crossing in Inapari (Peru-Brasil),

Madre de Dios.

Desaguadero Border Crossing (Peru-Boliv ia).

Construction and equipment of the border complex in Tilali-Puerto Acosta.

Construction and equipment of border complex in El Alamor.

Construction and equipment of border complex in Saramiriza-Loja.

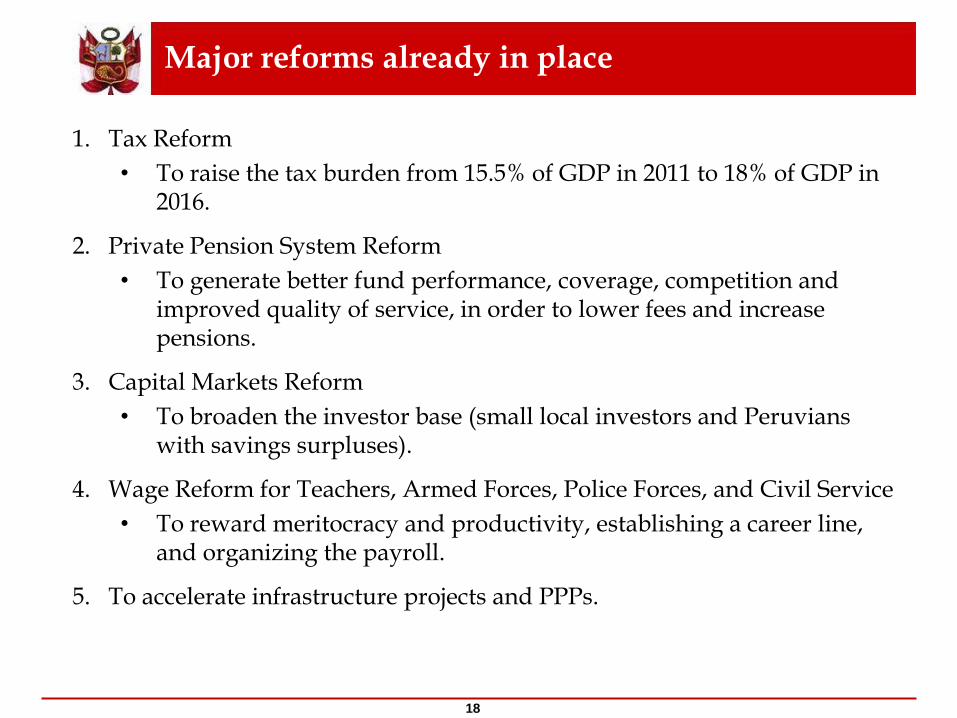

Major reforms already in place

1. Tax Reform

• To raise the tax burden from 15.5% of GDP in 2011 to 18% of GDP in 2016.

2. Private Pension System Reform

• To generate better fund performance, coverage, competition and improved quality of service, in order to lower fees and increase pensions.

3. Capital Markets Reform

• To broaden the investor base (small local investors and Peruvians with savings surpluses).

4. Wage Reform for Teachers, Armed Forces, Police Forces, and Civil Service

• To reward meritocracy and productivity, establishing a career line, and organizing the payroll.

5. To accelerate infrastructure projects and PPPs.

18

19

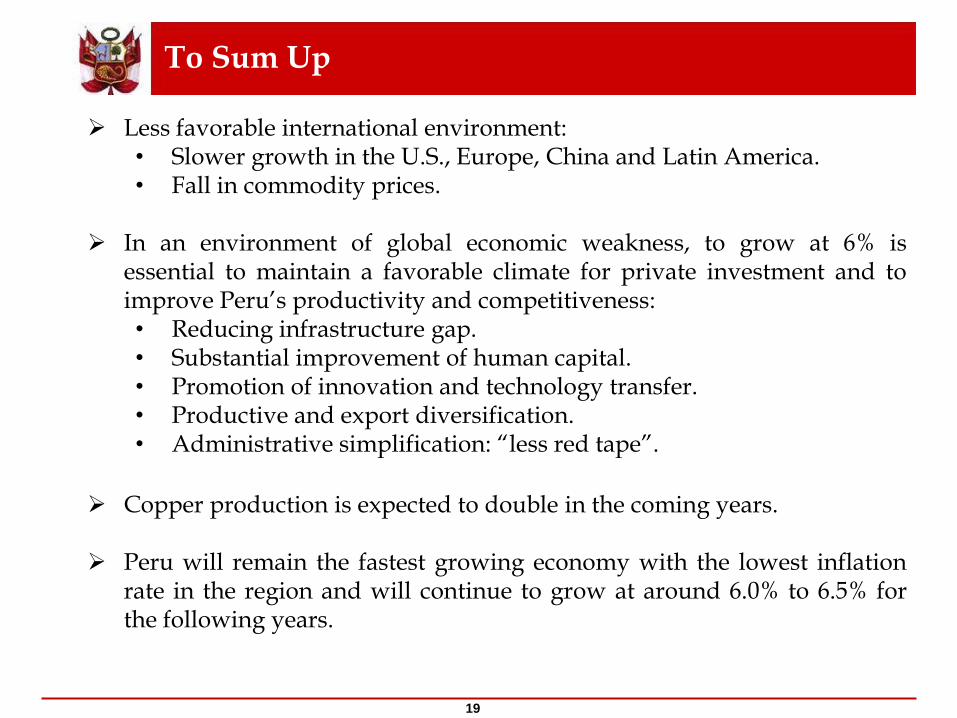

Less favorable international environment: • Slower growth in the U.S., Europe, China and Latin America. • Fall in commodity prices.

In an environment of global economic weakness, to grow at 6% is

essential to maintain a favorable climate for private investment and to improve Peru’s productivity and competitiveness: • Reducing infrastructure gap. • Substantial improvement of human capital. • Promotion of innovation and technology transfer. • Productive and export diversification. • Administrative simplification: “less red tape”.

Copper production is expected to double in the coming years.

Peru will remain the fastest growing economy with the lowest inflation

rate in the region and will continue to grow at around 6.0% to 6.5% for the following years.

To Sum Up

www.mef.gob.pe