Duke University NROTC 04 March 2014 Personal Financial Management.

Upload

datherine-cooperCategory

view

27download

2description

Personal Financial Management

Semester 2 2008 – 2009

Gareth Myles [email protected]

Paul Collier [email protected]

Reading

Callaghan: Chapter 4McRae: Chapter 8

Interest and Interest Rates

Some basic information on interest rates Bank of England base rate

Set by Monetary Policy Committee Provides a basis for other rates No-one can trade at a lower rate (arbitrage)

Objectives of the MPC To control the rate of inflation (target band)

Increase in interest rate reduces demand Reduction in interest rate stimulates demand

Base decisions on economic data

Other Important Rates

LIBOR: London Interbank Offered Rate The rate at which banks are willing to lend to each

other The basis for many financial calculations

Mortgage rates Mortgages are the safest form of lending to

individual so have lowest interest rates Market rate is determined by competition between

lenders

Other Important Rates

Personal loans Loans for purchases other than property (more risk) Higher interest rate than mortgages More variation in interest rates than for mortgages

Collateral Secured loan: an asset is held as collateral Unsecured loan: no collateral Interest rate is lower on a secured loan

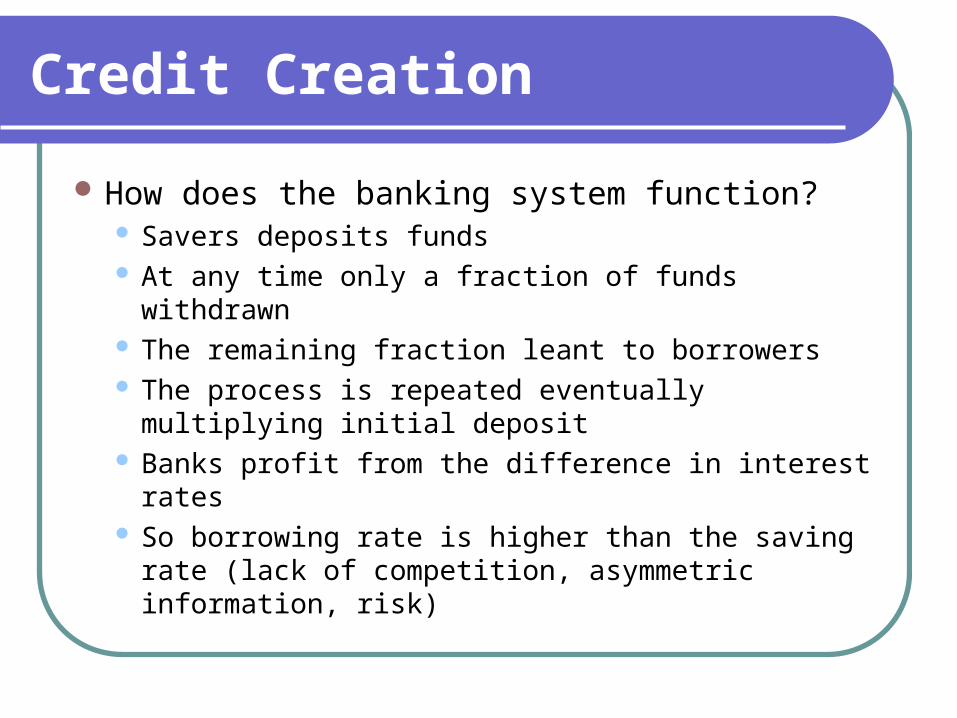

Credit Creation

How does the banking system function? Savers deposits funds At any time only a fraction of funds withdrawn The remaining fraction leant to borrowers The process is repeated eventually multiplying

initial deposit Banks profit from the difference in interest rates So borrowing rate is higher than the saving rate

(lack of competition, asymmetric information, risk)

Loans

Open-ended An upper limit is agreed, borrower has flexibility

Specific For the purchase of a defined item, with a clear

payment schedule What determines the interest rate?

Lowest when secured on a safe asset Highest when unsecured and open Depends also on credit worthiness of borrower

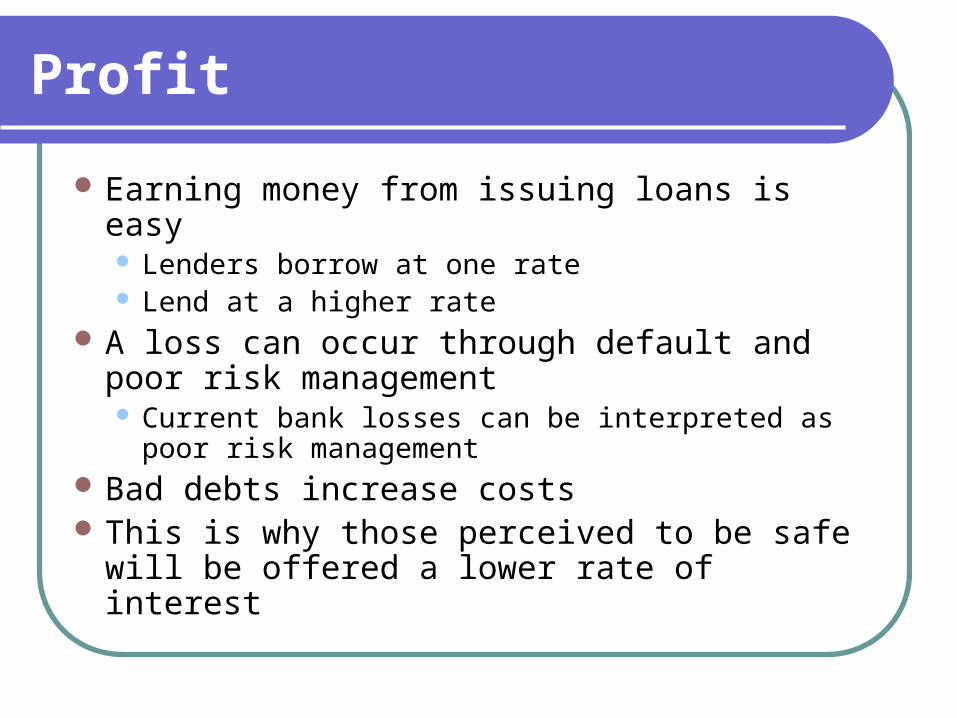

Profit

Earning money from issuing loans is easy Lenders borrow at one rate Lend at a higher rate

A loss can occur through default and poor risk management Current bank losses can be interpreted as poor risk

management Bad debts increase costs This is why those perceived to be safe will be

offered a lower rate of interest

Credit Rating Agencies

Hold data on borrowers to advise lenders of previous history

Can make mistakes For example assigning bad risk to an address

If refused credit Can ask whether because of a credit agency report Can then contact agency to correct any false

information

Credit Cards

Credit Cards: offer free credit if repaid monthly, but otherwise incur a very high interest rate Table of Rates Strategy: carry debt from card to card to take

advantage of introductory offers

Store Cards: usually an even higher rate Store Card The only reason to hold these is to benefit from

card-holder discounts

Interest Rate Calculations

To understand interest rates, need to go some through some basic calculations

Interest is compounded at a specified intervalThe interval can make a difference

Assume interval is one year Then borrowing £100 at a rate of 10% for one year

implies a total repayment of

110£1.1100£1100£ r

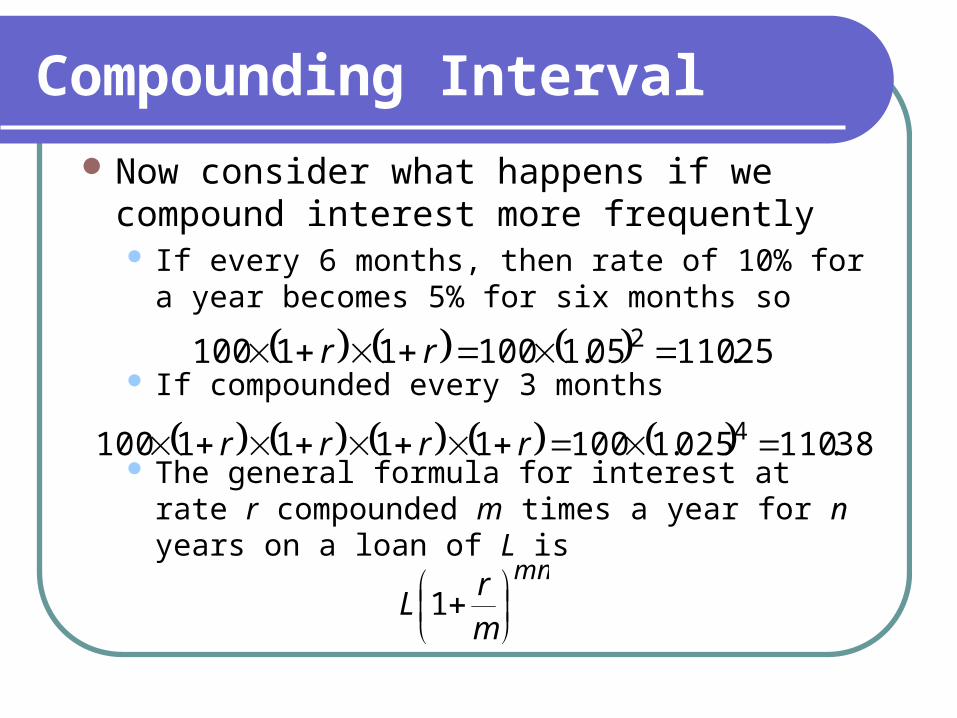

Compounding Interval

Now consider what happens if we compound interest more frequently If every 6 months, then rate of 10% for a year

becomes 5% for six months so

If compounded every 3 months

The general formula for interest at rate r compounded m times a year for n years on a loan of L is

25.11005.110011100 2 rr

38.110025.11001111100 4 rrrr

mn

mr

L

1

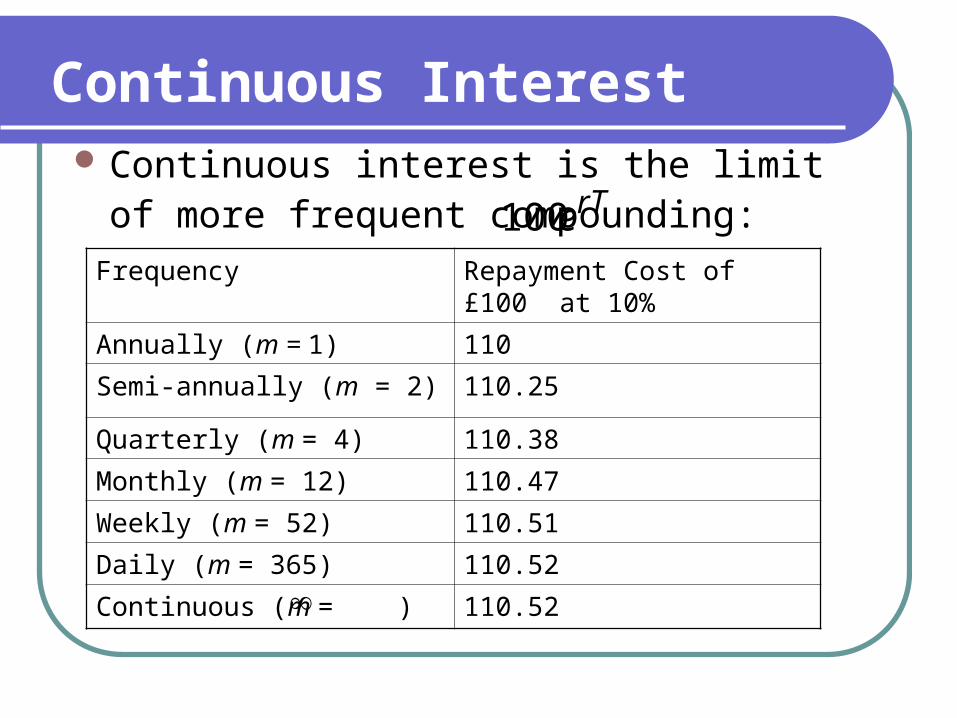

Continuous Interest Continuous interest is the limit of more

frequent compounding: Frequency Repayment Cost of £100 at

10%

Annually (m = 1) 110

Semi-annually (m = 2) 110.25

Quarterly (m = 4) 110.38

Monthly (m = 12) 110.47

Weekly (m = 52) 110.51

Daily (m = 365) 110.52

Continuous (m = ) 110.52

rTe100

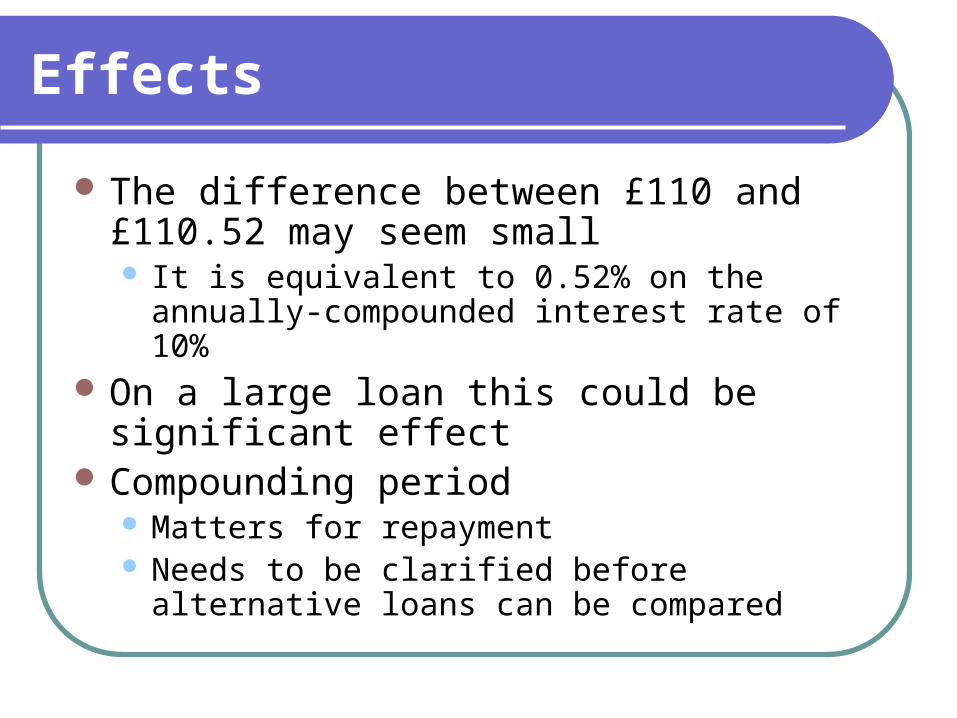

Effects

The difference between £110 and £110.52 may seem small It is equivalent to 0.52% on the annually-

compounded interest rate of 10% On a large loan this could be significant effect Compounding period

Matters for repayment Needs to be clarified before alternative loans can

be compared

Flat Rate Interest

Interest can also be quoted as a flat rate Consider £100 borrowed for 5 years, with a flat

rate of interest of 10% This means £10 of interest is paid per year

Over 5 years the total payments on the loan are

£10+£10+£10+£10+£10+£100 = £150 The repayment structure is 5 payments of £30 This is equivalent to an APR of 15.2% (see

later or use mortgage calculation)

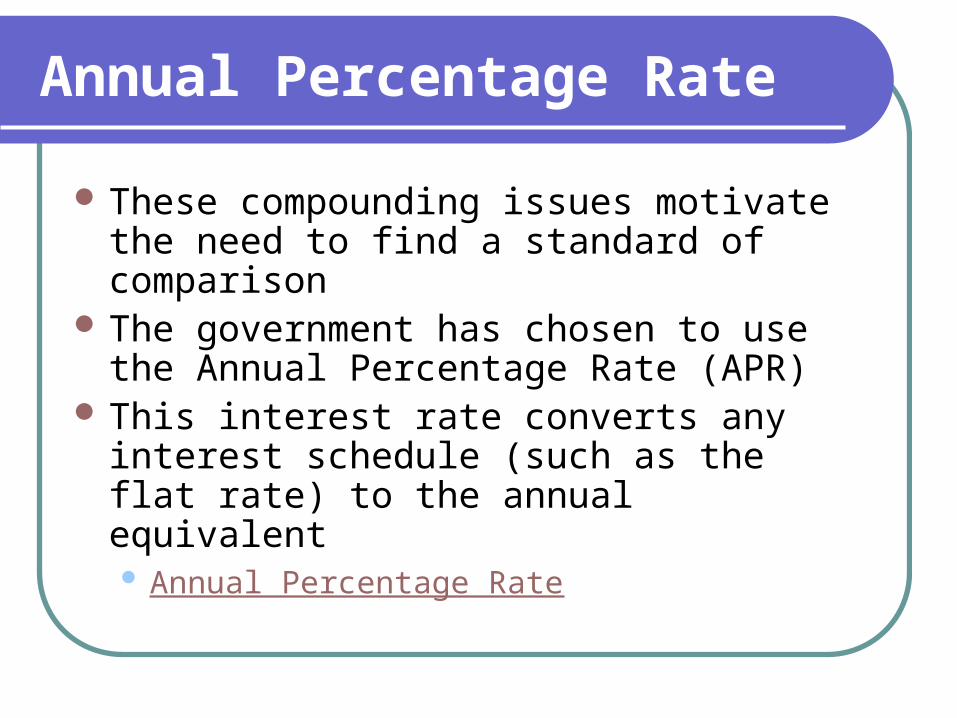

Annual Percentage Rate

These compounding issues motivate the need to find a standard of comparison

The government has chosen to use the Annual Percentage Rate (APR)

This interest rate converts any interest schedule (such as the flat rate) to the annual equivalent Annual Percentage Rate

Annual Percentage Rate

Consider receiving m payments Ak at times tk and making n payments Ak′ at times tk ′

The interest rate that makes the present discounted value of both flows equal solves

The solution r to this equation is the APR

n

kt

km

kt

k

kk r

A

r

A

1''

1 1

'

1

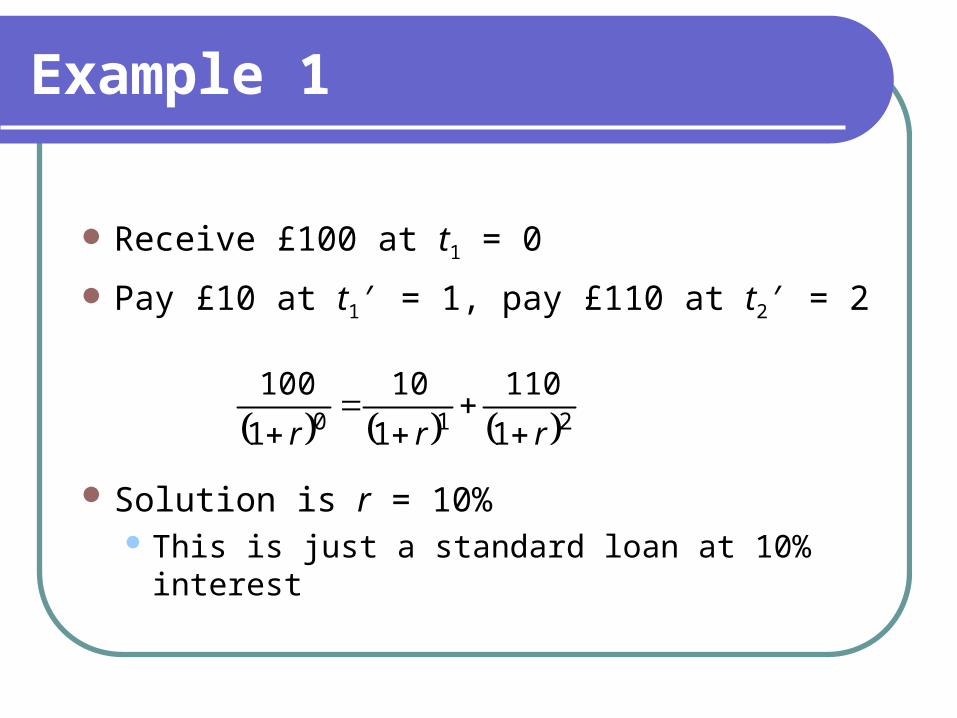

Example 1

Receive £100 at t1 = 0

Pay £10 at t1′ = 1, pay £110 at t2′ = 2

Solution is r = 10% This is just a standard loan at 10% interest

210 1

110

1

10

1

100

rrr

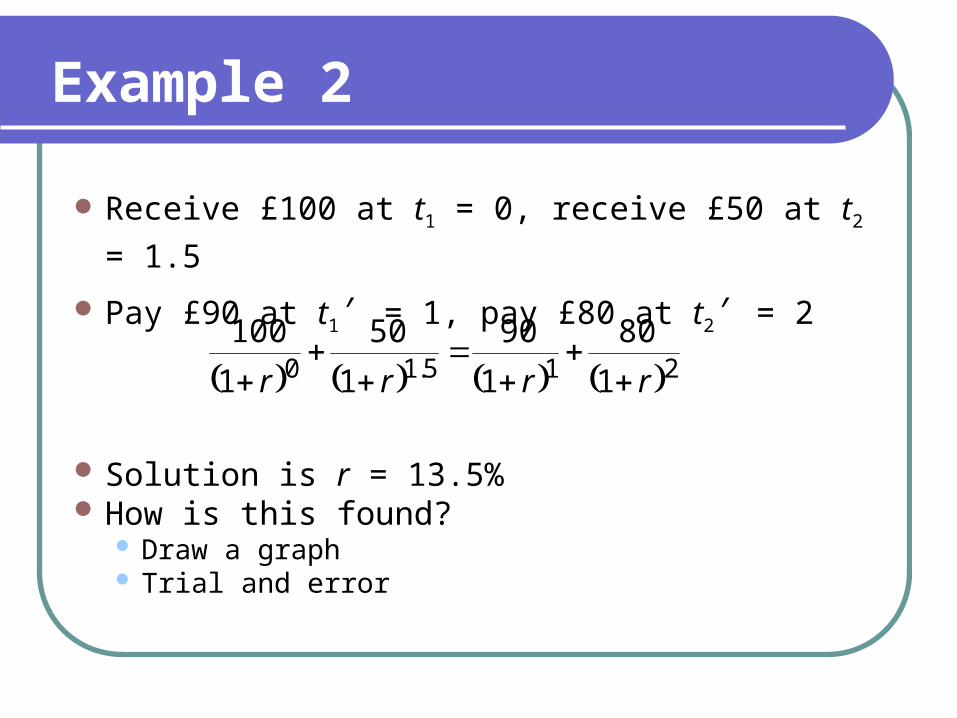

Example 2

Receive £100 at t1 = 0, receive £50 at t2 = 1.5

Pay £90 at t1′ = 1, pay £80 at t2′ = 2

Solution is r = 13.5% How is this found?

Draw a graph Trial and error

215.10 1

80

1

90

1

50

1

100

rrrr

Example 2

-20

-15

-10

-5

0

5

0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2r

215.10 1

80

1

90

1

50

1

100

rrrr

Example 3

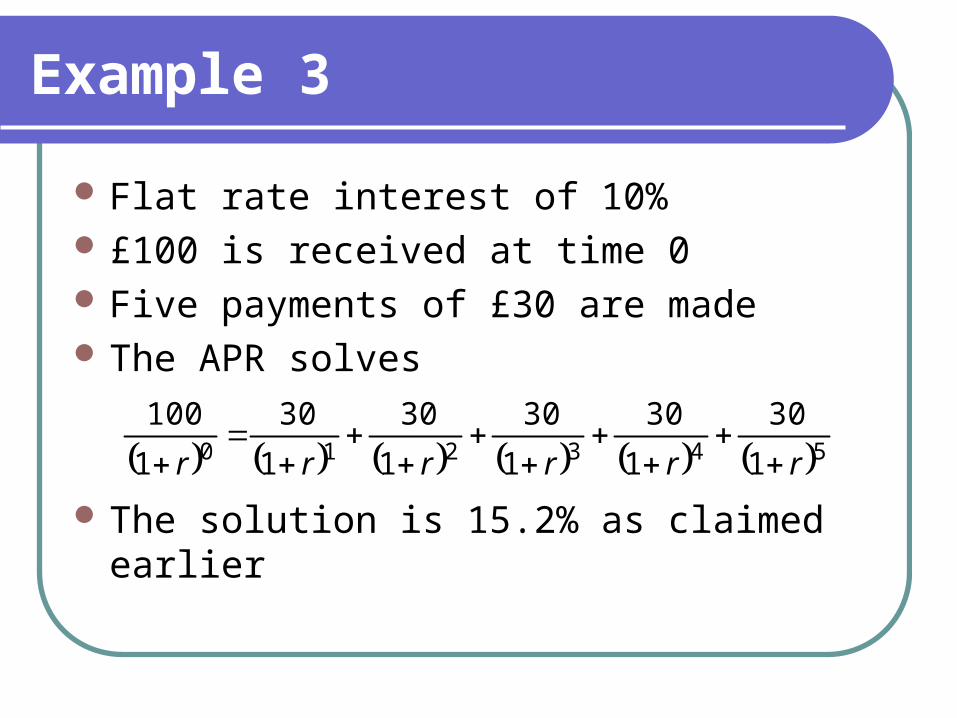

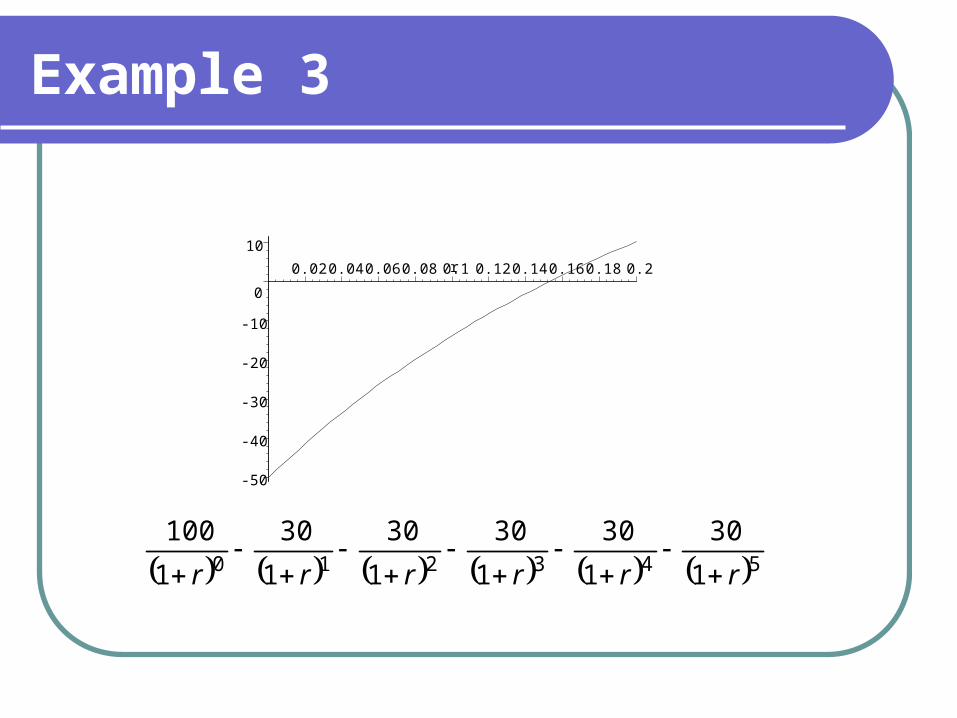

Flat rate interest of 10% £100 is received at time 0 Five payments of £30 are made The APR solves

The solution is 15.2% as claimed earlier

543210 1

30

1

30

1

30

1

30

1

30

1

100

rrrrrr

Example 3

-50

-40

-30

-20

-10

0

10

0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2r

543210 1

30

1

30

1

30

1

30

1

30

1

100

rrrrrr

Comparison

The APR is quoted with all adverts for loans It is a simple means of contrasting the rates on

loans with different structures