Performance Audits and Risk Assessments - Chapters Site · Presented By: Jim Godsey, Partner Mark...

27

Presented By: Jim Godsey, Partner Mark Cousineau, Senior Manager March 19, 2015 Performance Audits and Risk Assessments The Institute of Internal Auditors Beach Cities Chapter

Transcript of Performance Audits and Risk Assessments - Chapters Site · Presented By: Jim Godsey, Partner Mark...

Presented By: Jim Godsey, PartnerMark Cousineau, Senior Manager

March 19, 2015

Performance Audits and Risk Assessments

The Institute of Internal AuditorsBeach Cities Chapter

Agenda

• Introductions and Overview• What is a Performance Audit• Four Phase Approach• Risk Assessment• Fraud Overview

Purpose of Performance Audits

• Program Results• Need for Improved Performance

– Reduced Resources– Increased Service Demands– Diminished Reserves

1

Four-Phase Process

• Startup / Management• Fact Finding• Analysis• Reporting

2

Start-up and Management

• Identify key issues• Finalize audit plan• Develop interview list• Request documents• Define progress reporting and deliverables

3

Fact Finding – Document Review

• Gain breadth and depth of coverage• Ensure confidential conversations• Utilize standard questions and let

discussions evolve naturally• Build rapport with the interviewees

4

Fact Finding – Interviews

• Review historical performance and policy and political environment to understand how organization got to where it is today

• Document recent changes and impact on delivery

• Define service delivery requirements• Identify relevant best practices and

industry trends

5

Fact Finding – Walkthroughs

• Understanding the processes• Document information flow• Identify internal controls• Identify relevant regulations, policies, and

procedures• Conduct sampling and testing• Look for opportunities to streamline

6

Fact Finding – Surveys

• Confidential• Online• Broad participation• Low cost• Easy to administer

7

Analysis

• Assess economy, efficiency, and effectiveness

• Compare to best practices• Perform gap analysis• Identify alternatives• Define costs and benefits• Prepare findings and recommendations

8

Reporting

• Prepare draft report• Prepare final report• Develop implementation plan• Incorporate management response• Present to leadership and stakeholders

9

Risk Assessment Process

Risk Assessment – Internal Control

• What is an Internal Control?:“Internal control is a process, effected by an entity’s board of directors, management, and other personnel, designed to provide reasonable assurance regarding the achievement of objectives relating to:

• Operations• Reporting • Compliance”

10

Source: COSO Internal Control Framework

Risk Assessment – Optimal Risk TakingEx

pect

ed E

nter

pris

e Va

lue

Risk Level

Insufficient Optimal ExcessiveRisk-Taking Risk-Taking Risk-Taking

“Sweet Spot”

11

Source: COSO Risk Assessment in Practice

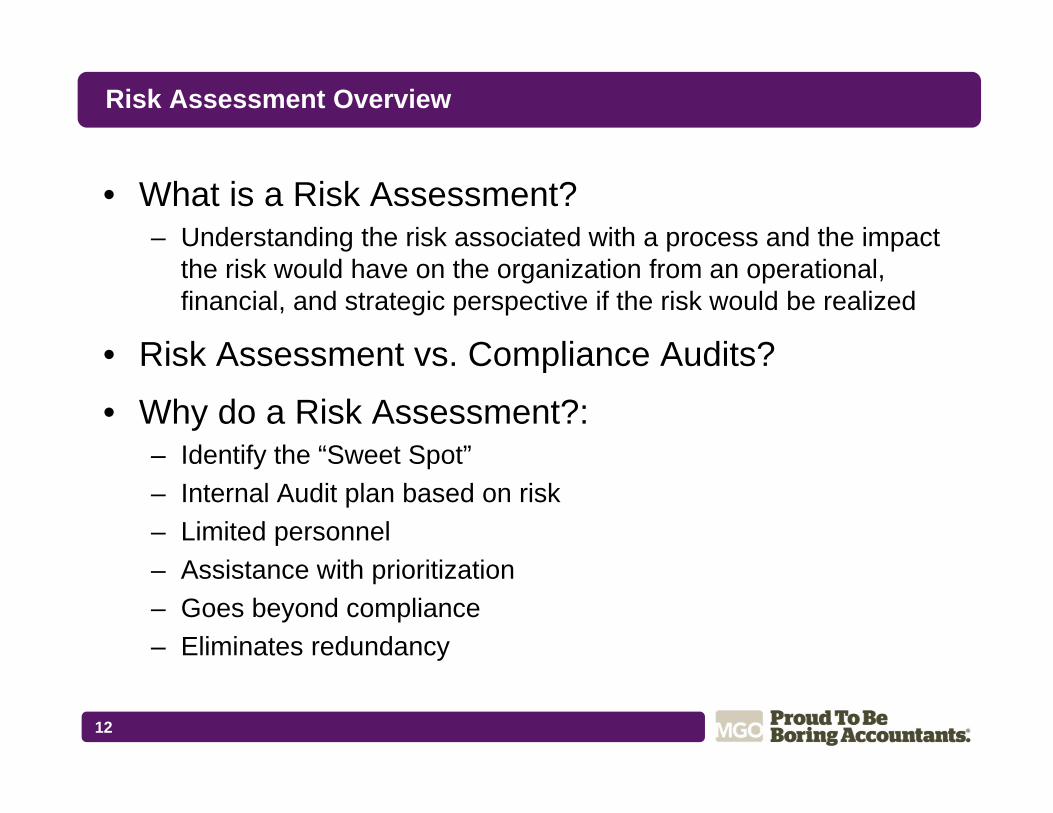

Risk Assessment Overview

• What is a Risk Assessment? – Understanding the risk associated with a process and the impact

the risk would have on the organization from an operational, financial, and strategic perspective if the risk would be realized

• Risk Assessment vs. Compliance Audits?

• Why do a Risk Assessment?:– Identify the “Sweet Spot”– Internal Audit plan based on risk– Limited personnel – Assistance with prioritization– Goes beyond compliance – Eliminates redundancy

12

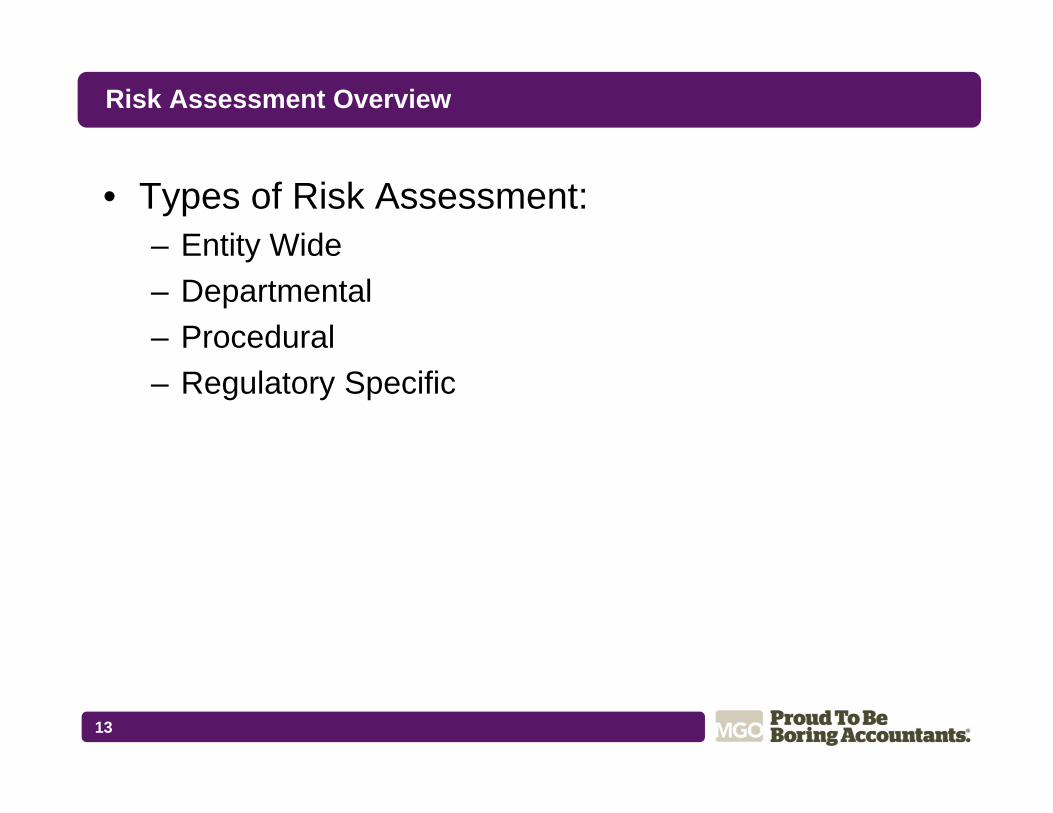

Risk Assessment Overview

• Types of Risk Assessment:– Entity Wide– Departmental – Procedural – Regulatory Specific

13

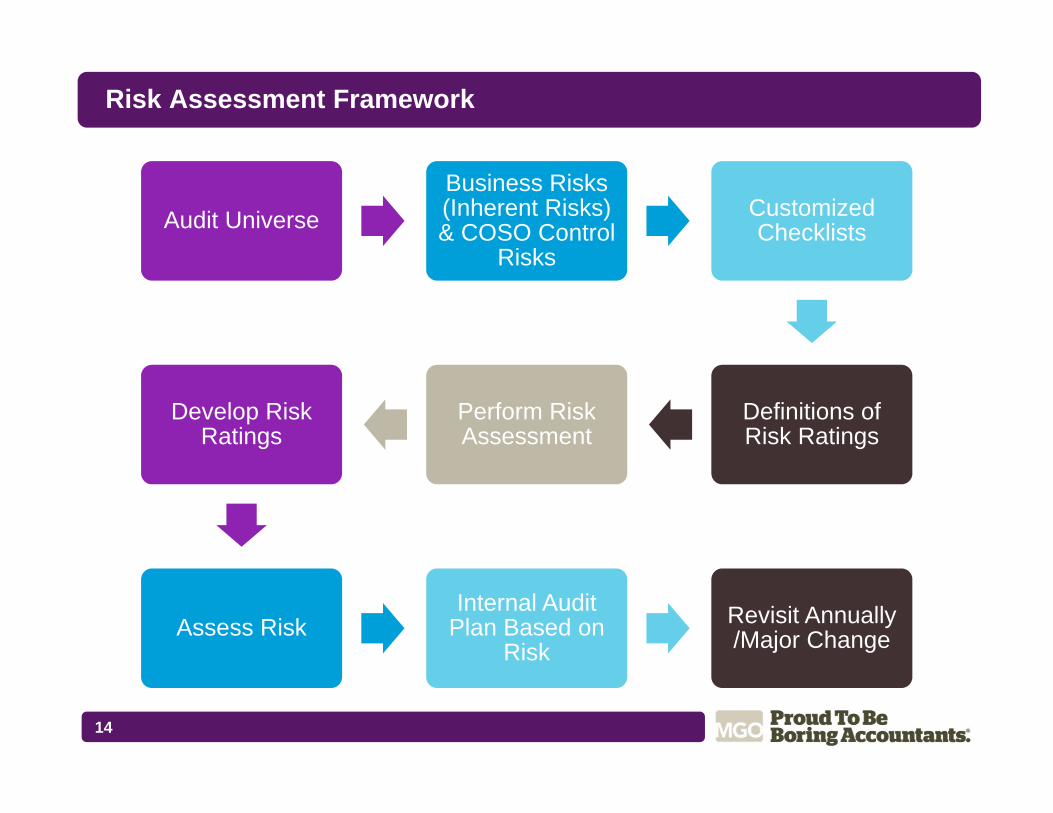

Risk Assessment Framework

14

Audit UniverseBusiness Risks (Inherent Risks) & COSO Control

Risks

Customized Checklists

Definitions of Risk Ratings

Perform Risk Assessment

Develop Risk Ratings

Assess Risk Internal Audit

Plan Based on Risk

Revisit Annually /Major Change

Risk Assessment Heat Map

15

Department /Process

Publi

cRep

utatio

n

Finan

cial

Oper

ation

al

Lega

l /Reg

ulator

y

Stra

tegic

Tech

nolog

y /Sy

stems

Peop

le /C

ultur

e

Frau

d

Inhe

rent

Risk

Rat

ing

2

Contr

olEn

viron

ment

Risk

Asse

ssme

nt

Contr

ol Ac

tivitie

s

Infor

matio

n & C

ommu

nicati

on

Monit

oring

COSO

Con

trol R

atin

g

ProcurementL H H L M H H H 88 0 W W W W M 96

Department /Process

Publi

cRep

utatio

n

Finan

cial

Oper

ation

al

Lega

l /Reg

ulator

y

Stra

tegic

Tech

nolog

y /Sy

stems

Peop

le /C

ultur

e

Frau

d

Inhe

rent

Risk

Rat

ing

2

Contr

olEn

viron

ment

Risk

Asse

ssme

nt

Contr

ol Ac

tivitie

s

Infor

matio

n & C

ommu

nicati

on

Monit

oring

COSO

Con

trol R

atin

g

Human Resources L M M M H M M M 75 0 S S S M M 58

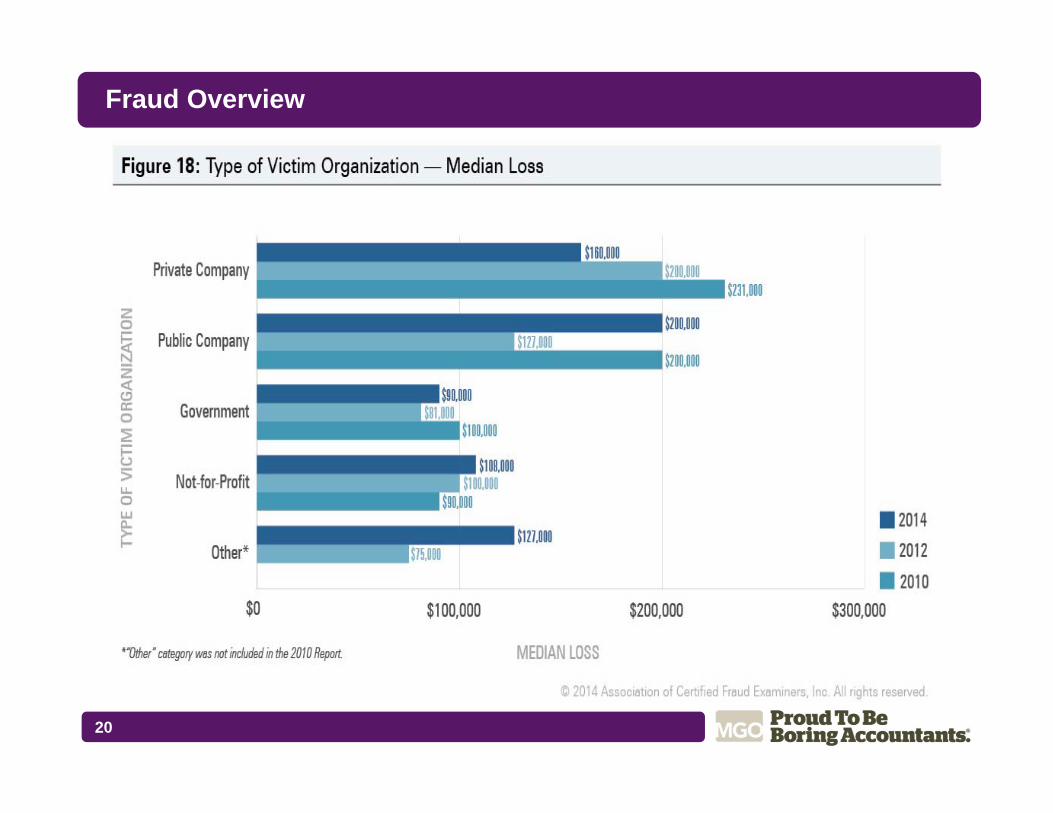

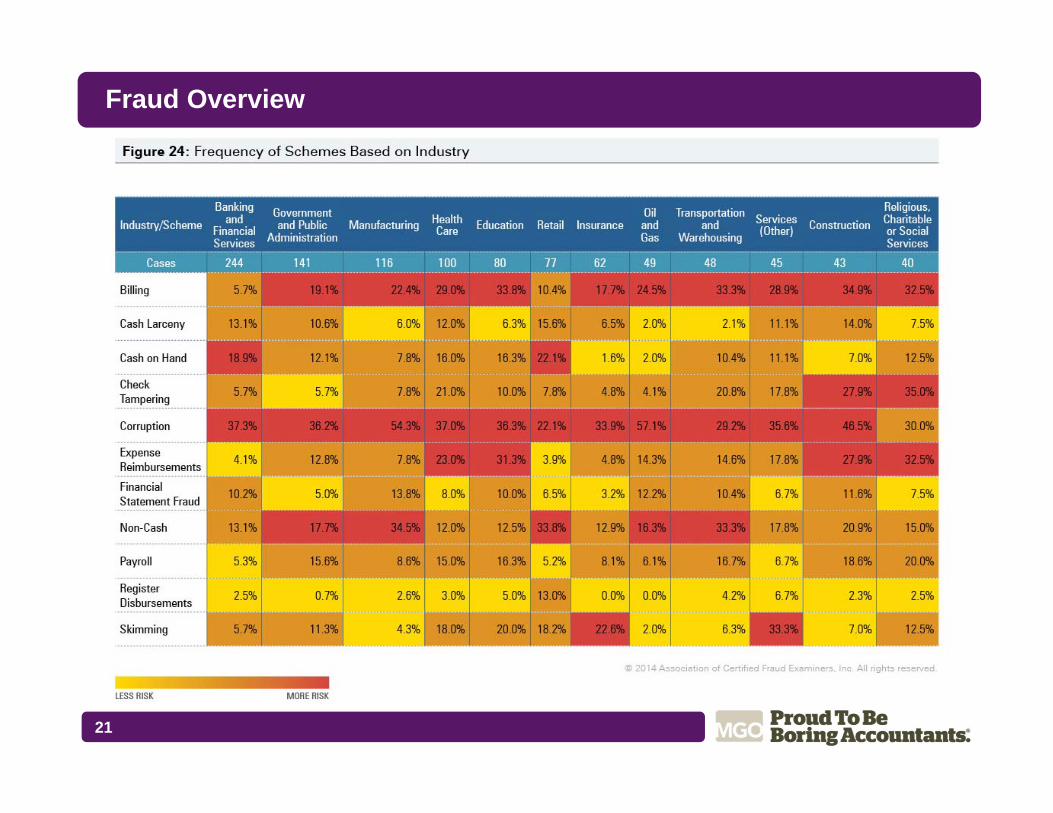

Fraud Overview

• Internal controls are only as good as the personnel performing the activities.

16

Fraud Overview

25%

49%

25%

1%Never

Would ifthey couldLooking

Stealing

Source: ACFE

Fraud Overview

• 2014 ACFE Report To The Nations – Organizations lose approximately 5% of revenue due

to fraud • Asset Misappropriation – 85.4% with median loss of

$130,000• Corruption – 36.8% with median loss of $200,000 • Financial Statements – 9.0% with median of $1 million

– Fraud duration 18 months – Men (66.8%) vs. Women (33.2%) – 40% of cases were detected via Tip /Hotline

17

22

Fraud Overview

18

23

Fraud Overview

19

24

Fraud Overview

20

25

Fraud Overview

21

26

Fraud Overview

22

Jim Godsey, Partner777 S. Figueroa Street, Ste 2500Los Angeles, CA 90017P: 213.408.8666 E: [email protected]

Questions?Mark Cousineau, Senior Manager777 S. Figueroa Street, Ste 2500Los Angeles, CA 90017P: 213.408.8674E: [email protected]

![Internal Audits and Assessments with help of Enterprise …itq.ch/pdf/Slides_PISA_wallmuellerV11-140510-1[1].ppt.pdf · Internal Audits and Assessments with help of Enterprise SPiCE](https://static.fdocuments.in/doc/165x107/5aa235257f8b9a436d8ca62b/internal-audits-and-assessments-with-help-of-enterprise-itqchpdfslidespisawallmuellerv11-140510-11pptpdfinternal.jpg)