![Who’s Your Average Mutual Fund Investor? [INFOGRAPHIC]](https://static.fdocuments.in/doc/165x107/53f192df8d7f72e94b8b49a8/whos-your-average-mutual-fund-investor-infographic.jpg)

PERCEPTION OF INVESTOR IN MUTUAL FUND: INDIAN …

12

Volume:01, Number:04, August-2011 Page 24 www.theinternationaljournal.org PERCEPTION OF INVESTOR IN MUTUAL FUND: INDIAN PERSPECTIVE Peeyush Bangur- M.B.A (Financial Administration) Lecturer, Shri Vaishnav Institute of Management, Indore. Madhya Pradesh Pratima Jain- MBA (Finance) Reader, Shri Vaishnav Institute of Management, Indore. Madhya Pradesh. Niraj Vijayvargiya, MBA (Finance) Reader, Shri Vaishnav Institute of Management, Indore. Madhya Pradesh ABSTRACT: - Domestic saving and investment is the best tool to cure recession and it leads to the growth of our domestic financial market. The present study is comprise of mutual fund industry along with its history with all ups and down happened to it .The main aim of study is to analyses the perception and awareness of different investors and also one who invest in the mutual fund.

Transcript of PERCEPTION OF INVESTOR IN MUTUAL FUND: INDIAN …

Volume:01, Number:04, August-2011 Page 24 www.theinternationaljournal.org

PERCEPTION OF INVESTOR IN MUTUAL FUND:

INDIAN PERSPECTIVE

Peeyush Bangur- M.B.A (Financial Administration)

Lecturer, Shri Vaishnav Institute of Management,

Indore. Madhya Pradesh

Pratima Jain- MBA (Finance)

Reader, Shri Vaishnav Institute of Management,

Indore. Madhya Pradesh.

Niraj Vijayvargiya, MBA (Finance)

Reader, Shri Vaishnav Institute of Management,

Indore. Madhya Pradesh

ABSTRACT: -

Domestic saving and investment is the best tool to cure recession and it leads to the growth of

our domestic financial market.

The present study is comprise of mutual fund industry along with its history with all ups and

down happened to it .The main aim of study is to analyses the perception and awareness of

different investors and also one who invest in the mutual fund.

Volume:01, Number:04, August-2011 Page 25 www.theinternationaljournal.org

INTRODUCTION

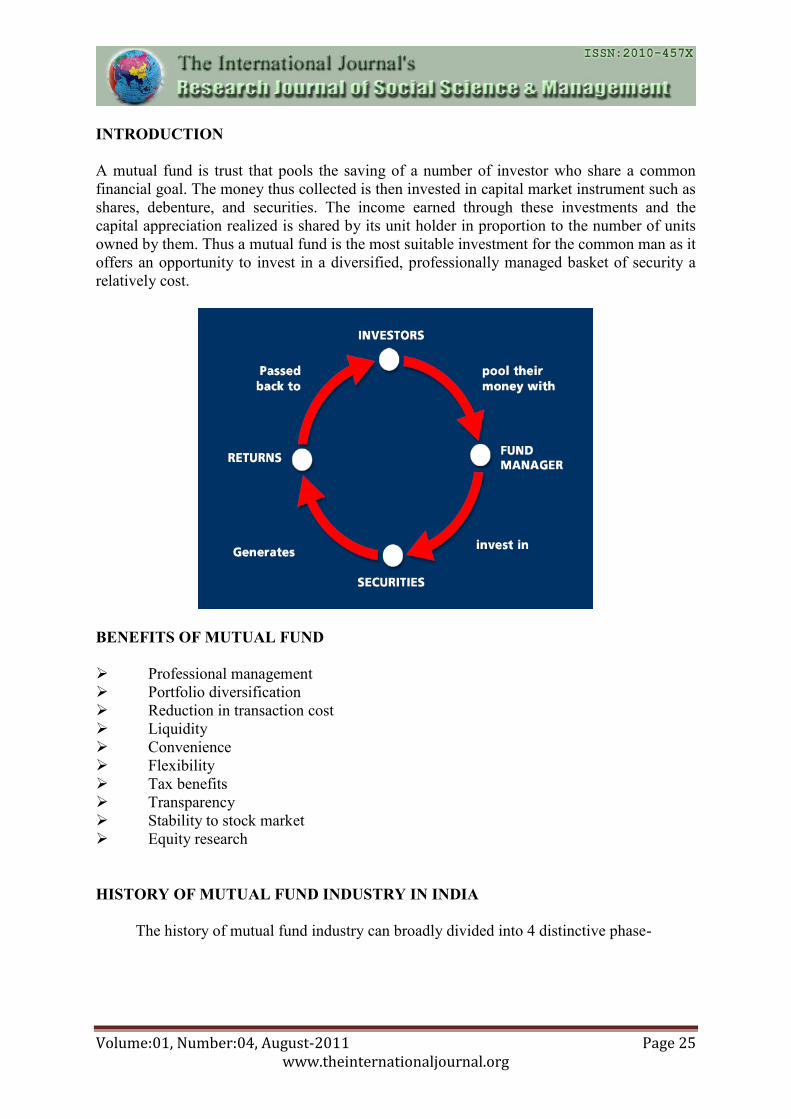

A mutual fund is trust that pools the saving of a number of investor who share a common

financial goal. The money thus collected is then invested in capital market instrument such as

shares, debenture, and securities. The income earned through these investments and the

capital appreciation realized is shared by its unit holder in proportion to the number of units

owned by them. Thus a mutual fund is the most suitable investment for the common man as it

offers an opportunity to invest in a diversified, professionally managed basket of security a

relatively cost.

BENEFITS OF MUTUAL FUND

Professional management

Portfolio diversification

Reduction in transaction cost

Liquidity

Convenience

Flexibility

Tax benefits

Transparency

Stability to stock market

Equity research

HISTORY OF MUTUAL FUND INDUSTRY IN INDIA

The history of mutual fund industry can broadly divided into 4 distinctive phase-

Volume:01, Number:04, August-2011 Page 26 www.theinternationaljournal.org

PHASE 1ST

1964-87

The Indian mutual fund industry were incepted in 1964 by UTI (unit trust of India)

under the UTI act 1963 (a special act of parliament). UTI was a set up by the Reserve Bank

Of India and functioned under the regulatory and administrative control of RBI. In 1978 UTI

was unlinked from RBI, and the Industrial development bank of India (IDBI) took over the

regulatory and administrative control in place of RBI. UTI acted as sole player from 1963-87

and it maintained its monopoly and experienced a consistent growth till 1987. Although the

growth of mutual fund industry was slow but it becomes intensive after 1987 when non UTI

companies were entered in the industry.

PHASE 2nd

1987-93 (entry of public sector fund)

In 1987, SBI mutual fund (June), and Can bank M.F.(December), were set up as trusts

under the Indian trust act 1982. These circumstances were followed by PNB mf (aug-89),

Indian bank mf (nov-89), Bank of India (june-90), BOB mf (oct-92). The two nationalized

giant LIC(june-89) and GIC(dec-90), set up their mutual fund.

At the end of 1993 AUM(asset under management) was of Rs. 47004 Crs.

PHASE 3rd

1993-2003jan.(entry of private sectors)

With the entry of private sector funds in 1993, new era were started in mutual fund

industry. Also 1993 was the year in which 1st mutual fund regulation incipient, under which

all MF, except UTI were registered and governed.

The Kothari Pioneer (now merged with Franklin Templeton) was first private sector

MF registered in July 1993. The number of mutual fund houses went on increasing with

many foreign mutual fund setting up funds in India and also the industry has witness several

mergers and acquisition. As at the end of January 2003, there were 33 MFs with total asset of

Rs. 121805 Crs. The UTI with 44541 Crs. Of AUM was way ahead of other MF.

PHASE 4th

Since Feb 2003

In February 2003, following the repeal of the UTI act 1963, UTI was bifurcated into

two separate entities, One is specified undertaking of the UTI with the AUM of Rs 29835

Crs. As at the end of January 2003 representing broadly, the asset of US 64 scheme, assured

return and certain their scheme. The specified undertaking UTI, functioning under the rules

framed by government of India and does not come under the purview of the MF regulation.

The second is UTI MF Ltd. Sponsored by SBI, PNB, BOB, and LIC. It is registered

under SEBI and function under MF regulation.

Volume:01, Number:04, August-2011 Page 27 www.theinternationaljournal.org

Different type of Mutual Fund scheme present in India

So many schemes exist in MF industry which fulfill the desire of Investor and provide them

safety, different type of mutual fund scheme are as follows,

Functional type Portfolio type Geographical type Other

Open-ended Income fund Domestic sectoral

Close ended Growth fund Offshore Tax saving

Interval schemes Balanced fund Gilt fund

Money market MF Load fund

index fund

ELSS

1. Functional classification

Open Ended scheme- Open ended scheme do not have fixed Corpus, and is not closed for

public subscription. Investor can Enter and Exit the scheme any time during the life of the

fund. The corpus of the fund Increase or decrease, depending on the purchase or redemption

by the investors, there is no such period of maturity. It is not listed in stock exchange,

liquidity is main feature of this scheme.

Close Ended scheme- This scheme are open for a limited period (30-45 days), this scheme

has stipulated maturity period from 5-7 years. This is transected at the stock exchange.

Interval scheme- This schemes combine the feature of open and close ended scheme. They

are open for the sale or redemption during predetermined intervals at net asset value (NAV)

related prices.

2. Portfolio classification-

Income fund- Main objective of this scheme is to provide a safety of investment and regular

income to investor, Investment are made in debt instrument viz. bond, debenture, and

government securities. Risk and returns are lower in this scheme.

Growth fund- Main objective of this scheme is capital appreciation, rather than regular

income, Investment are mainly done in equity share and small portion in money market

instruments. Risk are higher in this schemes.

Balance fund- Aim is both distributing regular income and providing capital appreciation to

the investor by balancing the investment of corpus between high growth equity shares and

income earning securities, risk is moderate.

Money market mutual fund- Investment done in money market instruments viz. treasury bills

and certificate of deposits, risk is of low rate.

Volume:01, Number:04, August-2011 Page 28 www.theinternationaljournal.org

3. Geographical classification-

Domestic fund- Investment done in one’s own country are domestic funds. The market is

limited and confined to boundaries of nation in which fund operates.

Offshore fund-These funds attract foreign capital for investment in country of issuing

company. They facilitates cross border fund flow which leads to an increase in foreign

currency and foreign exchange reserve.

4. Others-

Sectoral- Investment of funds in different sector such as I.T., pharmaceuticals, life science

etc. having aim of growth in capital and income generation.

Tax saving schemes- These scheme offer tax rebate on investment made in the equity shares,

under section 88 of income tax,1961.Income may also be periodically distributed depending

upon distributable surplus, subscription made up to Rs. 100000 in an assessment year are

eligible for tax rebate.

Equity linked saving scheme- The scheme controlled by government to encourage the

investor to invest in equity market which is followed by7 tax concession.

Gilt fund- This fund seeks to generate return through investment in gilts. Under this scheme

funds are invested only in central and state government securities, repo and reverse repo

rather than equity and corporate debt securities.

Load fund- mutual fund incurs certain expenses such as brokerage, marketing expenses and

communication expenses are known as load fund. These expense are known as load and

recovered by the fund when it sales the unit to investor or repurchase the units from

withholder. Load is of two types-

1. Front end load – or sale load, is that charge collect at the same time when an investor

enters into the scheme.

2. Back end load- or repurchase load, is that charge collected when the investor gets out of

scheme.

Index fund- This type of mutual fund invest in the securities in the index on which it is based

BSE sensex or S and P CNX Nifty.

NET ASSET VALUE- The performance of a particular scheme of a mutual fund is denoted

by NAV. The NAV per unit is the market value of securities of a scheme divided by the total

number of units of the scheme divided by the total number of units of the scheme, on any

particular date. In simple words, NAV is the market value of the security held by the scheme.

Volume:01, Number:04, August-2011 Page 29 www.theinternationaljournal.org

Organization:

Source: AMFIINDIA.com

Sponsor- The sponsor means any person who, acting alone or in combination with the

another body corporate establishes a mutual fund. A mutual fund is set up after certificate of

registration is issued by SEBI some eligibility criteria should be fulfilled by sponsor.

Trustee- A mutual fund in India is constituted in the form of a public trust created under the

Indian trust act, 1882. The sponsor forms the trust and registers it with SEBI. The fund

sponsor appoints a trustee to held the asset of trust for benefits of units holder, who are

beneficiaries of Trust.

Asset management company- The trustee appoints the asset management company (AMC)

with prior approval of SEBI. The AMC is a company formed and register under companies

act 1956, to manage affairs of mutual fund and operates the scheme of mutual fund the AMC

should have a net worth of net less than 10 crores.

Growth of Mutual Funds: Indian Perspective: The Mutual Fund industry had shown a

colossal growth and climatic improvement in last decade. AUM crossed Rs. 1 Lac Crore

during March 2000. This showed a growth of 65% comparison to previous year. However in

subsequent year i.e. March 2001 AUM sharply declined by 20% to Rs. 90587 Cr. Due to

extreme volatility & depressed equity condition. There was turnaround in year March 2002

the AUM grew by 11% to Rs. 100594 Cr. Again the Mutual Fund Industry had shown a sharp

decline in the year 2003, due to bifurcation of UTI into UTI Mutual Fund and specified

undertaking of UTI, effective from Feb 2003.

From 2003 Mutual Fund Industry shown a rapid and consistent growth AUM crossed

1.5 Lac Cr. In 2005, 2 Lac in 2006 which were followed by 3 Lac in March 2007. Presently

AUM is 505152 by ending of March 31st

Volume:01, Number:04, August-2011 Page 30 www.theinternationaljournal.org

Table & Graph unveils the growth of M.F. Industry

Year 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Total AUM 68984 68472 113005 90587 100594 79464 139616 149554 231668 326388 505152

Growth % (0.75%)

65.03% (19.8%) 11.05% (21%) 75.6% 7.1% 55.03% 40.7% 54.8%

Growth %

RoundOff

(1%) 65% (20%) 11% (21%) 76% 7% 55% 41% 55%

Source: Amfindia.com

Year Ending 31st March i.e. 68984 were total AUM in 31

st March, 1998 Growth %

calculated on the previous year basis

GROWTH IN ASSETS UNDER MANAGEMENT

Volume:01, Number:04, August-2011 Page 31 www.theinternationaljournal.org

Objective of Study: To determine the cognizance of the people & to make aware them

regarding to mutual fund.

Procedure of Research Methodology: 1. A proper questionnaire was prepared which contains the 6 question regarding Mutual

Fund.

2. A survey were shaped among 154 people which belongs to the region of

Madhyapradesh(Indore) and Rajasthan(Jaipur & Ajmer)

3. Data (obtained from survey) were collected in very systemic way.

4. Data were arranged properly

5. Different mathematical tool viz. mean, percentage, & chi square test were applied as

per requirements data relied on primary data.

Analysis of Research: Research analysis is the analysis of different questions which were

asked in survey.

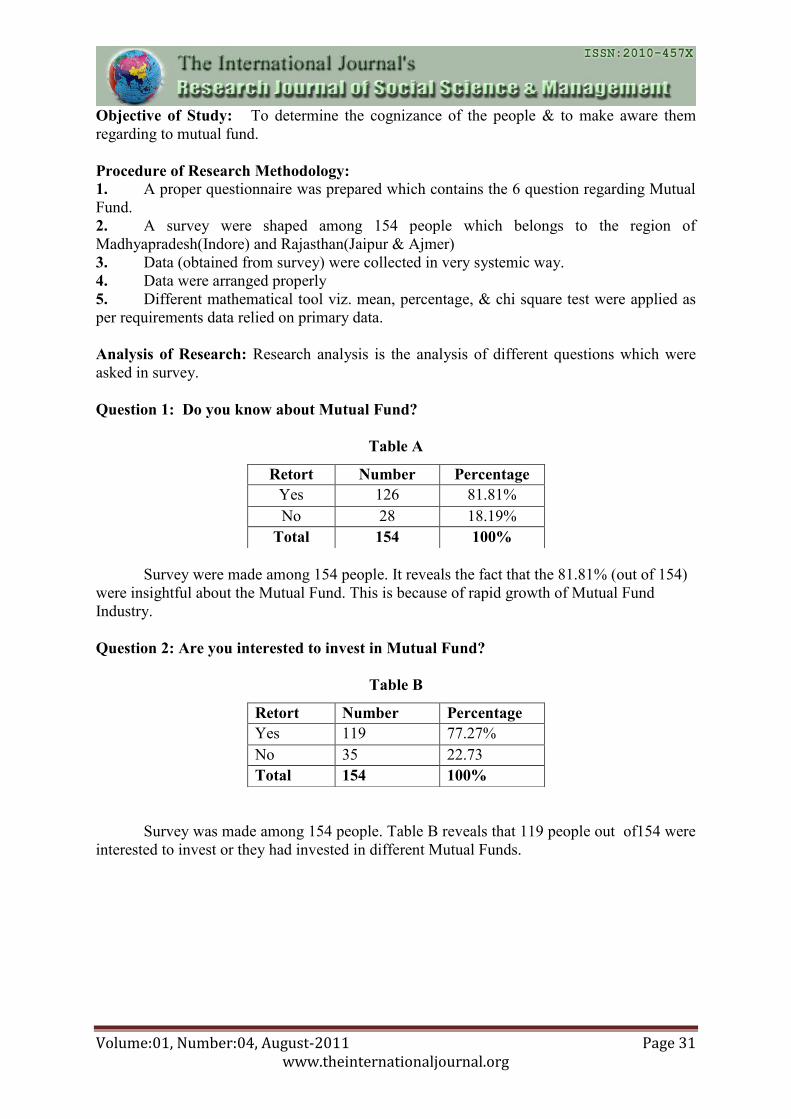

Question 1: Do you know about Mutual Fund?

Table A

Survey were made among 154 people. It reveals the fact that the 81.81% (out of 154)

were insightful about the Mutual Fund. This is because of rapid growth of Mutual Fund

Industry.

Question 2: Are you interested to invest in Mutual Fund?

Table B

Survey was made among 154 people. Table B reveals that 119 people out of154 were

interested to invest or they had invested in different Mutual Funds.

Retort Number Percentage

Yes 126 81.81%

No 28 18.19%

Total 154 100%

Retort Number Percentage

Yes 119 77.27%

No 35 22.73

Total 154 100%

Volume:01, Number:04, August-2011 Page 32 www.theinternationaljournal.org

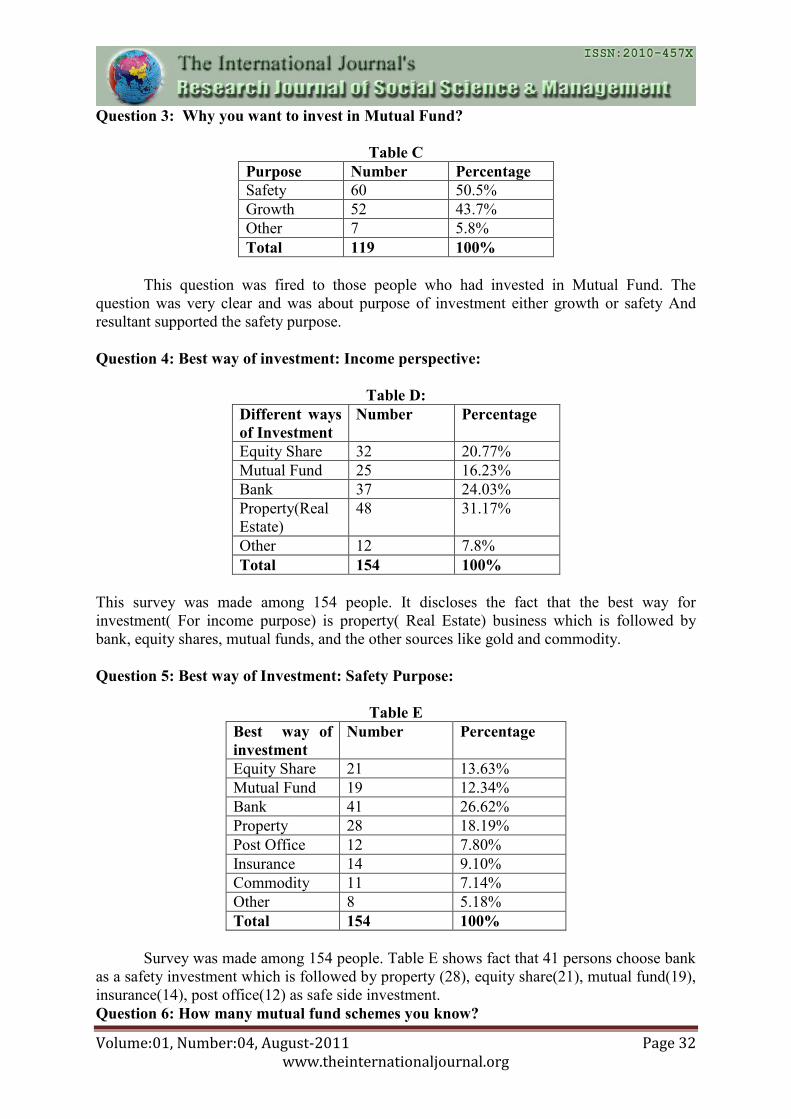

Question 3: Why you want to invest in Mutual Fund?

Table C

Purpose Number Percentage

Safety 60 50.5%

Growth 52 43.7%

Other 7 5.8%

Total 119 100%

This question was fired to those people who had invested in Mutual Fund. The

question was very clear and was about purpose of investment either growth or safety And

resultant supported the safety purpose.

Question 4: Best way of investment: Income perspective:

Table D:

Different ways

of Investment

Number Percentage

Equity Share 32 20.77%

Mutual Fund 25 16.23%

Bank 37 24.03%

Property(Real

Estate)

48 31.17%

Other 12 7.8%

Total 154 100%

This survey was made among 154 people. It discloses the fact that the best way for

investment( For income purpose) is property( Real Estate) business which is followed by

bank, equity shares, mutual funds, and the other sources like gold and commodity.

Question 5: Best way of Investment: Safety Purpose:

Table E

Best way of

investment

Number Percentage

Equity Share 21 13.63%

Mutual Fund 19 12.34%

Bank 41 26.62%

Property 28 18.19%

Post Office 12 7.80%

Insurance 14 9.10%

Commodity 11 7.14%

Other 8 5.18%

Total 154 100%

Survey was made among 154 people. Table E shows fact that 41 persons choose bank

as a safety investment which is followed by property (28), equity share(21), mutual fund(19),

insurance(14), post office(12) as safe side investment.

Question 6: How many mutual fund schemes you know?

Volume:01, Number:04, August-2011 Page 33 www.theinternationaljournal.org

Table F

Scheme Number Percentage

Open 39 32.77%

Closed 32 26.89%

Growth 12 10.08%

Income 16 13.45%

Gilt 8 6.72%

Others 12 10.09%

Total 119 100%

This question was asked to only those people which were interested to invest in

Mutual Fund, and hence survey was made among 119 people.

Question 7: Which is the best Mutual fund for investment purpose?

This Question was asked to study that the investors is biased or unbiased towards

investment in all mutual fund. For this Chi Square test have been applied.

H0 : Investor is unbiased towards invest in all mutual funds.

H1 : Investor is biased towards invest in all mutual funds.

S.

No.

Different

Mutual F.

O E (O-E) 2 (O-E)

2

E

1. Reliance 35 19.33 230.03 11.9

2. LIC 11 19.33 69.44 3.6

3. UTI 13 19.33 46.69 2.41

4. TATA 29 19.33 84.02 4.23

5. ICICI 15 19.33 23.36 1.178

6. Other 16 19.33 14.69 0.74

Total 119 24.05

Where:

O : Observer Frequency

E : Expected Frequency

Level Of Significance = 5%

X 2

=Sigma (O-E) 2

= 24.05

E

Critical Value: The table value at 5% level of significance and for 6-1 =5 degree of

freedom is Y2

0.055 = 11.070

Decision : since calculated value of Y2

=24.05 is > Y2

0.055 = 11.07 null hypothesis is

rejected.

Research analysis based on personal attributes:- this research is very interesting part of

Volume:01, Number:04, August-2011 Page 34 www.theinternationaljournal.org

our whole research paper after completion of this research some outstanding facts comes out

Research analysis based on personal feature viz. occupation, age, gender,

salary, marital status, of investor for this purpose questionnaire of 5 question were prepared

and it was fired to those who were interested invest in mutual fund.

Question 1: Tell us about your occupation

Table A

Question 2: May we know about your salary package

Table B

Question 3: What is your age ?

Table C

Age Number Percentage

0-25 29 24.36%

25-50 62 52.10%

50-75 25 21.02%

75&above 3 2.52%

Total 119 100%

Question 4: Gender and Marital status

Table D

Occupation Number Percent

Student 10 8.40%

Business class 80 67.23%

Service class 24 20.16%

Other 5 4.21%

Total 119 100%

Salary Number Percentage

0-10000 2 1.68%

10000-25000 14 11.76%

25000-50000 45 37.81%

50000-100000 43 36.13%

100000&above 15 12.62%

Total 119 100%

Volume:01, Number:04, August-2011 Page 35 www.theinternationaljournal.org

Result and Discussion:

No stone remain unturned for the completion of research analysis and finally we concluded

that: about 80% people are cognizant about mutual fund (table A), out of these 80% people

are invested in mutual fund(table B), out of these about 51% investors invest for safety

purpose (table C).

In our analysis some facts were revealed are as follows:

Investors thought that Real Estate is a most appropriate source of income, probably

you will get 2-3 times return and it may go up to 6 times.

Investors thought that Bank deposits are the safest source of investment.

Mutual fund industry is male dominant

Most of the investor is rely on business class.

Most of the investors are rely between the salary packages of 25000-100000.

References:-

1 Varshney P.N.; Mittal D. K.; (2005); Indian Financial system; Sultan Chand hand & sons;

New Delhi

2. Khan M. Y.; (2007); Indian Financial system; Tata McGraw hill; New Delhi

3. Pathak B. V.; (2004); Indian Financial system; Pearson education; Delhi

4. www.amfiindia .com

5. www.sebi.com

6. Module 2; Securities Laws and Compliances ;company secretaries of India, 413-448.

Gender Number Percentage

Male 105 88.24

Female 14 11.76

Marital

status

Number Percentage

Married 69 57.98

Unmarried 50 42.02