Pension - Pre 2004 Hires

44

Pension Benefits ❑ How to request a package ❑ Optional forms of pension payment ❑ Timing of retirement (early, postponed) ❑ Pension calculation ❑ COLA ❑ Sunset of MRP

Transcript of Pension - Pre 2004 Hires

Pension Benefits

❑ How to request a package❑ Optional forms of pension payment❑ Timing of retirement (early, postponed)❑ Pension calculation❑ COLA❑ Sunset of MRP

From PSC Home Page - Click on My Retirement and Pension

From My Retirement - Click on More to options to go to the Retirement

Modeler or run Pension Estimates

The Retirement Modeler can also be reached from the My Retirement banner on the PSC Home Page

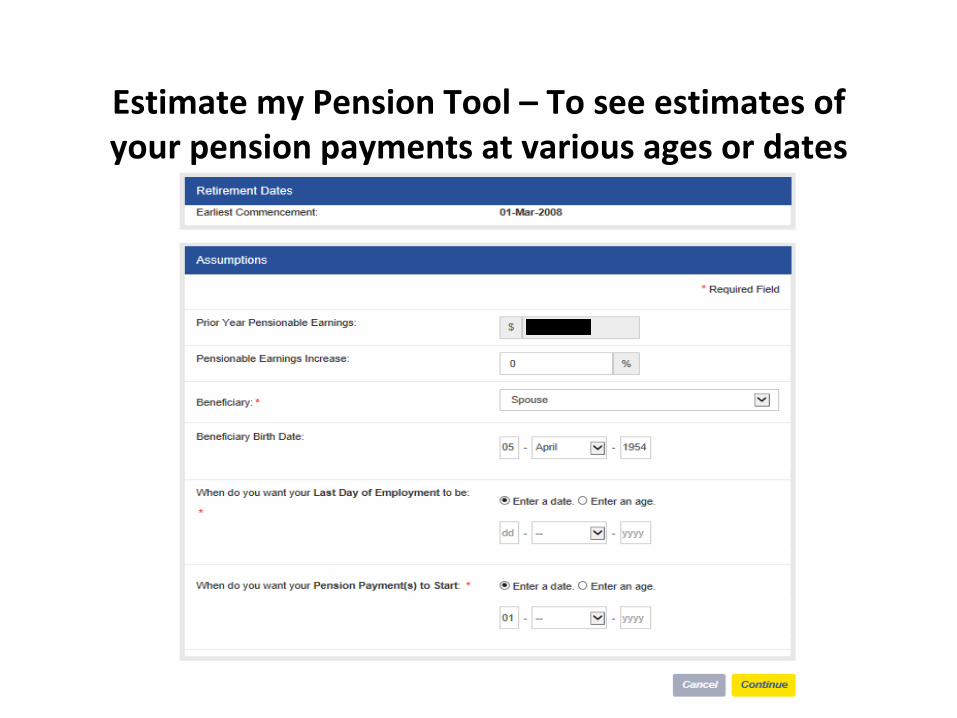

Estimate my Pension Tool – To see estimates of your pension payments at various ages or dates

Displays Estimates of Payment amounts for all Forms of Payment you are eligible for - based on

your inputs from prior screen!

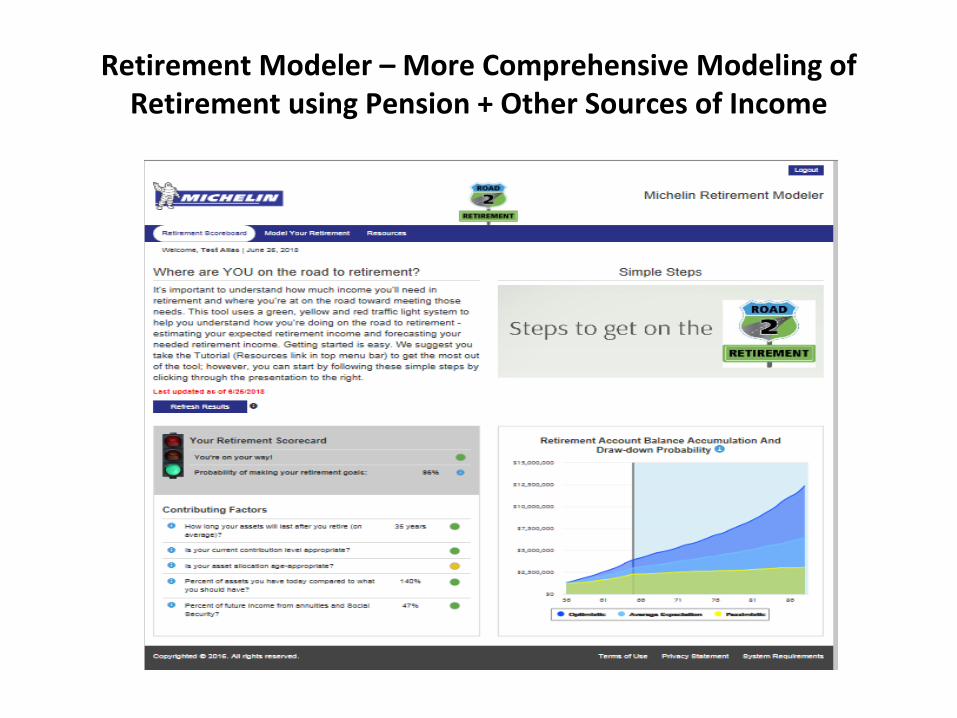

Retirement Modeler – More Comprehensive Modeling of Retirement using Pension + Other Sources of Income

Ready to Retire?

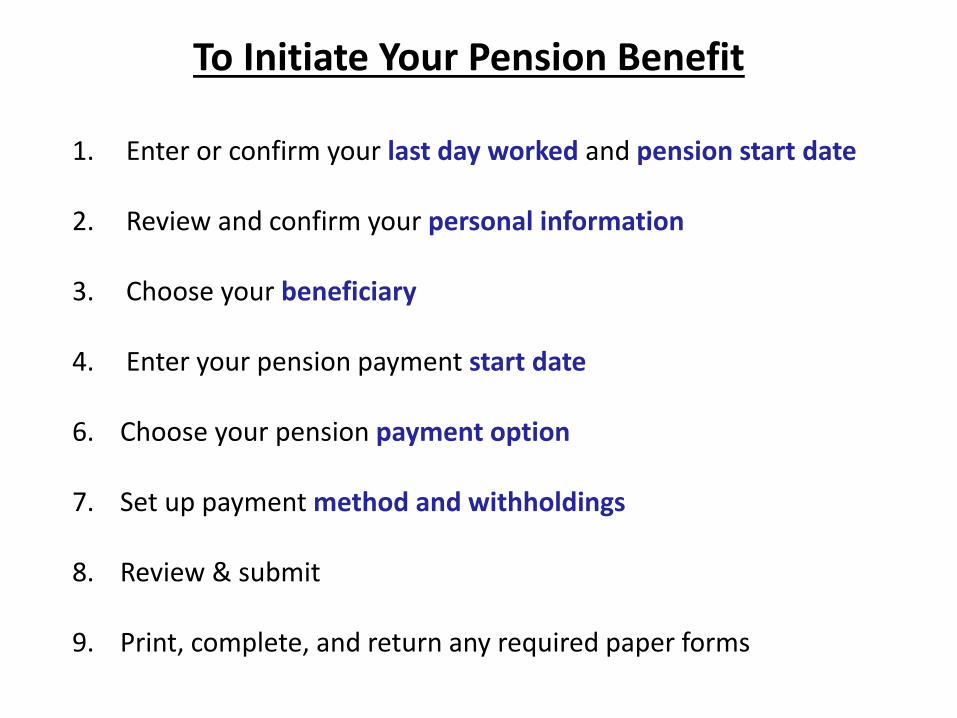

To Initiate Your Pension Benefit

1. Enter or confirm your last day worked and pension start date

2. Review and confirm your personal information

3. Choose your beneficiary

4. Enter your pension payment start date

6. Choose your pension payment option

7. Set up payment method and withholdings

8. Review & submit

9. Print, complete, and return any required paper forms

Please note when Commencing

• You must be terminated in InTouch before your retirement can be processed and your first pension payment be issued.

• Therefore, there may be a delay in receiving your first pension payment if your commencement date closely follows your last day worked

• For example if you work until June 30 and commence on July 1, your first payment will not be made on July 1. It

will likely be paid between mid-July and August 1.

Please note when Commencing - Tips

• Your paperwork must be 100% accurate, complete and submitted to the PSC in enough time for it to be processed prior to commencement.

• Problems with paperwork will delay processing & payments:

– Signatures are missing

– Spousal consents are missing

– Information is not complete

• Incomplete paperwork will not be accepted!

• Please note that it can take up to 30 days from the date you elect your pension payment to begin and the actual pension payment start date. If your actual pension payment start date is later than your requested pension payment start date, you will receive retroactive payments back to your requested pension payment start date

Think about when you want you last day of work to be…

Intent to Retire

Make sure your personal information is correct. If a correction is needed, please do so via InTouch

Select the individual who should serve as your pension beneficiary for the purpose of determining your Joint & Survivor benefit

Your pension payment start date cannot be more than 90 days after the date of submitting Intent to Retire event

Next you see a list of optional forms of payment of your pension benefit with amounts calculated based on your previous inputs.

For option explanations, click here

“55 & 30”

Special Early Retirement Supplement

Special Early Retirement Supplement of $500 per month if:• Leave at age 55 or older• Have at least 30 years of vested service; and• Start receiving your benefit before the age when you are eligible to

receive 80% of your unreduced Social Security benefit.

Package will be mailed to your home within two weeks

Retirement Counselor

Key Resources Once You Receive Your Package

• Retirement Counselor (RC)

• Walk through retirement paperwork one on one and

answer questions/assist completion of paperwork

.

Retirement Case Administrator

Key Resources Once You Receive Your Package

• Retirement Case Administrator (RCA)

• Point of contact for any questions from now till payment commences

• Once completed paperwork is received they will reach out and confirm receipt, set payment up and set expectations of first payment date

.

Retirement Payment Options• Lump Sum for MRAP participants

– Full lump sum, or

– Half lump sum and half annuity

• Life Annuity

• 10 Year Certain and Life

• Joint and Survivor

• 50%

• 75%

• 100%

• Social Security Equalization

• Social Security Equalization w/ 50% J&S

Decision is irrevocable.*

* You cannot change either your retirement option or your beneficiary in retirement.

Lump Sum Option

• If elected the MRAP in 2004 or 2007, can take MRP as a Lump Sum when leave the company.

• Lump Sum will be calculated using the segmented discount rates for that particular year.

Choose retirement date wisely

Lower discount rate = higher lump sum*

• MRP Lump Sums can be rolled into MRAP accounts at retirement.

* Typically, not always! Mortality table also comes into play.

Minimum Present Value Segment Rates

Year First Segment: Retirement Age + 5 Years

Second Segment: Next 15 Years of Retirement

Third Segment: Remaining Years

2021 0.52 2.22 3.03

2022 0.66 2.50 3.12

Which rates are lower? 2021

Which rates result in higher lump sum?

It depends…

To use 2021 rates, what is required by Dec. 30, 2021?

• End employment

• Elect lump sum option

• Sign and return your retirement paperwork

How to Calculate a Lump Sum (example)

6/30/2007

1,222.83

1,222.83

0.855

1,045.52

500.00

How to Calculate a Lump Sum

• Use COLA-eligible life annuity lump sum table

• Employee is 61 & 0 months at retirement date

• Employee is COLA eligible

Age-Months

0 1 2 3 4 5 6 7 8 9 10 11

55 331.613431 330.881606 330.149782 329.417957 328.686132 327.954308 327.222483 326.490658 325.758834 325.027009 324.295184 323.563360

s 56 322.831535 322.100780 321.370026 320.639271 319.908516 319.177762 318.447007 317.716252 316.985498 316.254743 315.523988 314.793234

r 57 314.062479 313.331134 312.599789 311.868444 311.137099 310.405754 309.674409 308.943063 308.211718 307.480373 306.749028 306.017683

a 58 305.286338 304.554790 303.823241 303.091693 302.360144 301.628596 300.897047 300.165499 299.433950 298.702402 297.970853 297.239305

e 59 296.507756 295.776446 295.045135 294.313825 293.582515 292.851204 292.119894 291.388584 290.657273 289.925963 289.194653 288.463342

Y 60 287.732032 287.001847 286.271661 285.541476 284.811291 284.081105 283.350920 282.620735 281.890549 281.160364 280.430179 279.699993

- 61 278.969808 278.241976 277.514144 276.786311 276.058479 275.330647 274.602815 273.874982 273.147150 272.419318 271.691486 270.963653

e 62 270.235821 269.510768 268.785715 268.060662 267.335609 266.610556 265.885503 265.160449 264.435396 263.710343 262.985290 262.260237

g 63 261.535184 260.813901 260.092619 259.371336 258.650054 257.928771 257.207489 256.486206 255.764923 255.043641 254.322358 253.601076

A 64 252.879793 252.160611 251.441430 250.722248 250.003067 249.283885 248.564704 247.845522 247.126340 246.407159 245.687977 244.968796

65 244.249614 243.532520 242.815427 242.098333 241.381239 240.664146 239.947052 239.229958 238.512865 237.795771 237.078677 236.361584

COLA: 2.23% Intrateapprox Beginning Immediately

Lump Sum Equivalency Factors

Annuity Form: Life Annuity

Multiply Monthly Benefit by Factor Below to Derive Lump Sum Value

Payment at Beginning of Month

Mortality: Retiree - 417E2022

Interest: Segments: 0.66%, 2.50%, 3.12%

How to Calculate a Lump Sum

Monthly accrued pension benefit after early retirement adjustment

$1,045.52

Lump sum factor from COLA-eligible life annuity lump sum table

278.969

$291,668

Lump sum factor from temporary annuity lump sum table

37.328

$500

$18,664

$310,332Total Michelin Qualified Plan Lump Sum

Michelin qualified plan lump sum

Early retirement supplement

Supplement Lump Sum

--------------------------------------------------------------------------------

--------------------------------------------------------------------------------

Half Lump Sum and Half Annuity

• Combination 50% lump sum and 50% annuity option. Note: This results in a lower lump sum and a smaller annuity.

• Annuity portion of this new option available as either a Life Annuity or 75% Joint and Survivor Annuity

• Maybe/maybe not?

Life Annuity

• The maximum monthly amount you could receive from the Plan.

• Will receive a monthly benefit for your lifetime only.

• Payments will stop at the time of your death.

If married at the time of your retirement, your spouse must agree in writing to this selection.

10 Year Certain and Life Annuity

• Receive reduced monthly benefits for your lifetime.

• If you die within 10 years of retiring, your beneficiary would receive monthly payments for the balance of the 10 years.

• At the end of the 10 years, or if you were to die after at least 10 years of retirement, your beneficiary would not receive any additional payments.

1 2 3 4 5 6 7 8 9 10

Joint and Survivor Options

• Receive reduced monthly benefits for your life

• After your death, survivor benefits would be paid to your beneficiary (not necessarily your spouse) for the remainder of the survivor’s life.

• Survivor benefits can equal 50%, 75%, or 100% of your reduced monthly benefit.

Your spouse would have to approve in writing should you not name them as your beneficiary with this option.

Social Security Equalization• If retire before age 62, can increase your annuity payment

from retirement date until age 62 (Social Security eligible)

• When reach age that you can begin to receive a reduced benefit from Social Security, benefit from the Plan reduced

• “Pulling forward” pension to create steady income steam

There are no survivor benefits with this option so your spouse would have to agree in writing.

$3,053.97

Pensio

n

Pensio

n

Pensio

n

Pensio

n

Pensio

n

Pensio

n

Social Secu

rity

Social Secu

rity

$1,308.97

Pensio

n

Pensio

n

Age 56 57 58 59 60 61 62 63+

Social Security Equalizationw/ 50% Joint & Survivor

• The same as the regular Social Security Equalization option, except this option offers a 50% Joint and Survivor benefit.

• At the time of your death, your beneficiary would begin to receive 50% of your benefit (reducing down at the point you would have been eligible for Social Security).

Types of Retirement

1. Normal: First day of the month after you reach age 65, or your 65th birthday if it falls on the 1st of the month

2. Early: First day of any month between ages 55 and 65, if you have at least 10 years of service

3. Postponed: If you continue to work past age 65, your accrued benefit may be actuarially adjusted to reflect a retirement date past age 65.

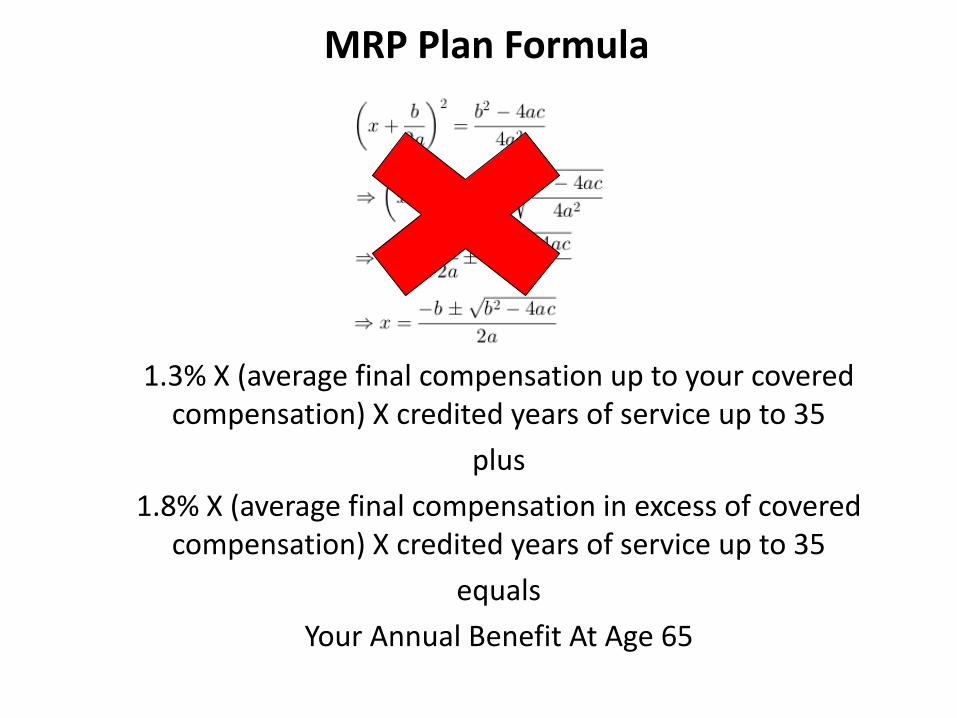

MRP Plan Formula

1.3% X (average final compensation up to your covered compensation) X credited years of service up to 35

plus

1.8% X (average final compensation in excess of covered compensation) X credited years of service up to 35

equals

Your Annual Benefit At Age 65

Formula Components

• Average Final Compensation: average of your eligible earnings during the 5 full, consecutive, highest paid calendar years of the last ten calendar years while you were covered under the MRP (through 2016)

• Covered Compensation: average of the Social Security Wage Bases over the 35 year period ending when you reach full Social Security retirement age.

• Credited Years of Service: total number of years that you worked for Michelin and were covered under the MRP up to 2016 and a maximum of 35 years

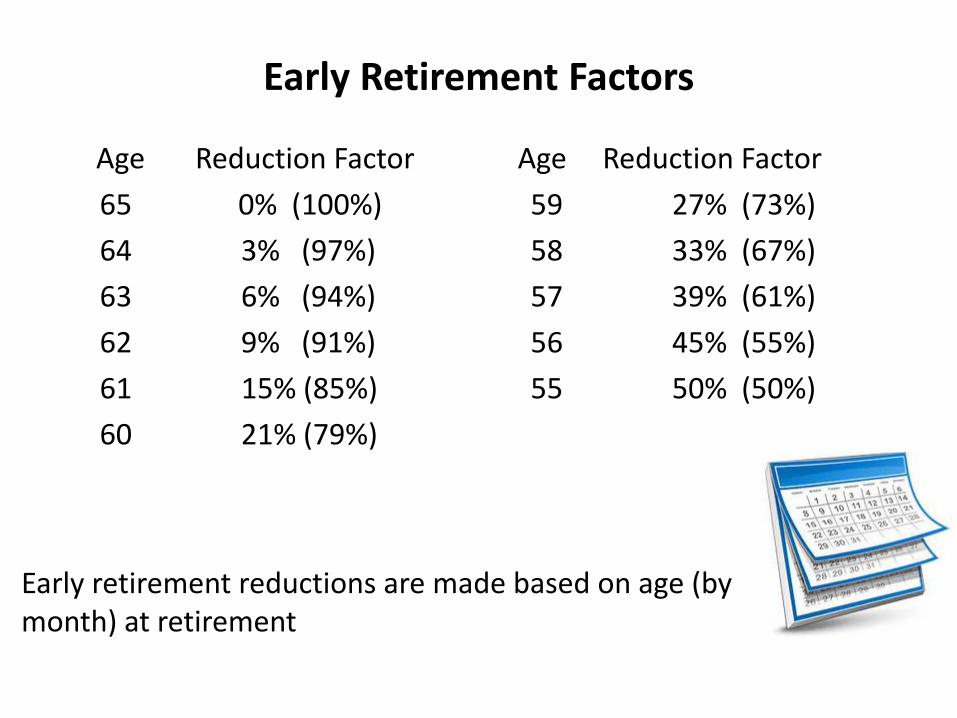

Early Retirement Factors

Age Reduction Factor

65 0% (100%)

64 3% (97%)

63 6% (94%)

62 9% (91%)

61 15% (85%)

60 21% (79%)

Age Reduction Factor

59 27% (73%)

58 33% (67%)

57 39% (61%)

56 45% (55%)

55 50% (50%)

Early retirement reductions are made based on age (by month) at retirement

Delayed Retirement Factors

The MRP plan requires you to commence payment at the later of age 65 and date of termination. If you continue working after age 65 your MRP Benefit will be increased by a factor related to your delayed retirement. Actual delayed retirement factors (DRFs) are calculated by month. Above are sample factors from Sub-Plan 851.

Age DRF Age DRF

65 1.000 69 1.592

66 1.125 70 1.800

67 1.259 71 2.044

68 1.413 72 2.331

COLA Eligibility

• Employees hired by Michelin prior to 12/31/1990 have a cost-of-living (COLA) component to their retirement.

• Adjusts when inflation has moved 5% or more since their retirement/ last COLA date.

• In a normal inflationary environment, eligible retirees can expect to see a COLA increase every 2 to 3 years.

Employees originally hired by Uniroyal, BFG, or Uniroyal Goodrich are not eligible to receive any COLA adjustments

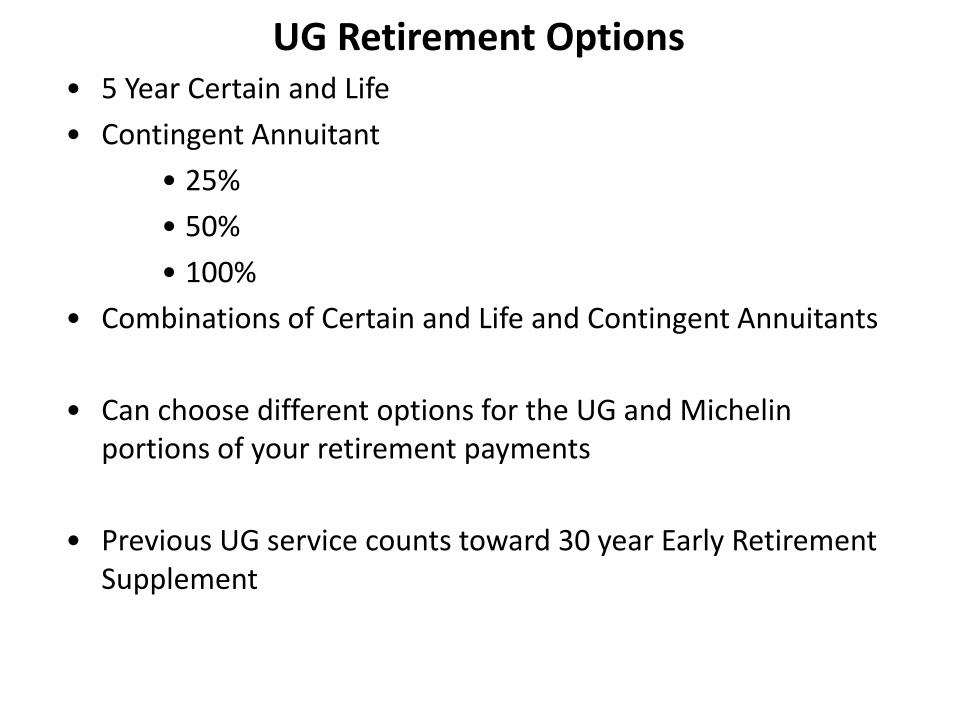

UG Retirement Options• 5 Year Certain and Life

• Contingent Annuitant

• 25%

• 50%

• 100%

• Combinations of Certain and Life and Contingent Annuitants

• Can choose different options for the UG and Michelin portions of your retirement payments

• Previous UG service counts toward 30 year Early Retirement Supplement

Moving to MRAP

• As of 01/01/2017, those individuals who finished in the MRP on 12/31/2016 began to accrue a new benefit in the MRAP.

• What that means:

• An account at Vanguard

• Account owners can invest in the same options that are available in the 401(k).

• Company contributions are made annually (typically in February) for the prior year.

Thinking About Retiring?

• If within 3 months, request a package! Caution as Lump Sum Rates Change ~ October each year

• Make copies of your birth certificate(s) and marriage license

• Call the PSC to request a retirement counseling session.

• Return paperwork to the PSCabout 1 month before retirement

• Once entered into the system, Northern Trust will provide lump sumor monthly retirement payments