PEGAS NONWOVENS S.A. - CFA Institute Files/CFA Institute... · PEGAS NONWOVENS S.A. Team H January...

25

PEGAS NONWOVENS S.A. Team H January 28, 2015

Transcript of PEGAS NONWOVENS S.A. - CFA Institute Files/CFA Institute... · PEGAS NONWOVENS S.A. Team H January...

PEGAS NONWOVENS S.A.

Team H

January 28, 2015

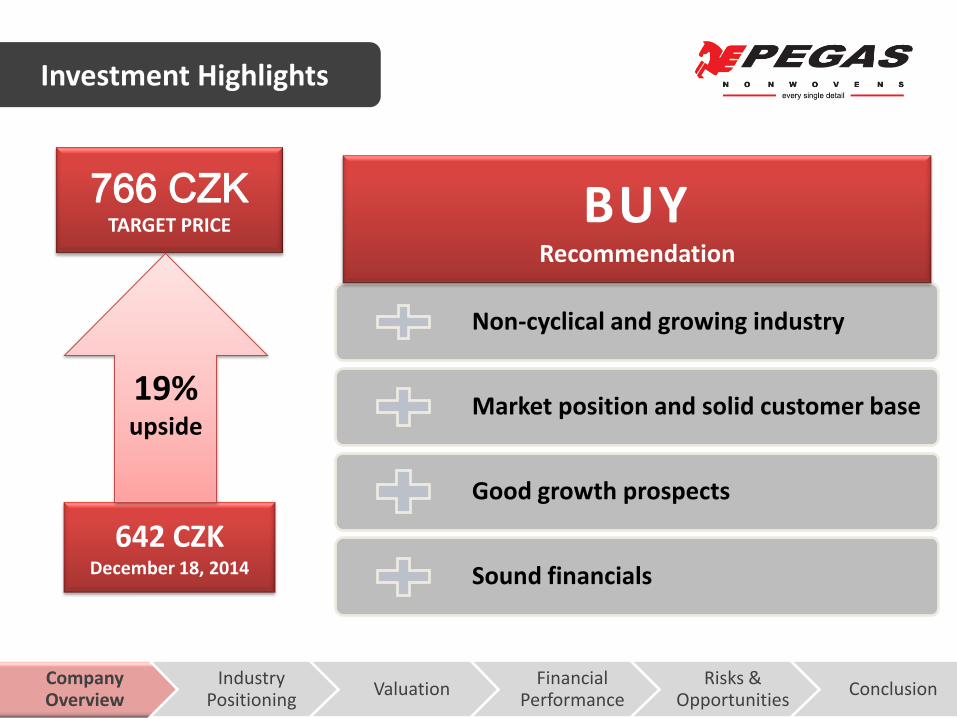

642 CZK December 18, 2014

766 CZK TARGET PRICE

19% upside

Non-cyclical and growing industry

Market position and solid customer base

Good growth prospects

Sound financials

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Investment Highlights

BUY Recommendation

Business Description

Introduction

Revenue Breakdown by Product (% of sales 2013)

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Hygiene Commodity

Hygiene – Technologically Advanced

Non-hygiene

Leading nonwoven textile producer in the

Europe, Middle East and Africa market

Market Profile (ticker PGSNsp.PR)

Closing price 18/12/2014 (CZK) 642

52-week price range (CZK) 588.50 – 659.80

Average daily volume 6,191

As % of shares outstanding 0.0671%

Free float 100%

Market capitalization (CZK mil) 5,999.110

Hygiene sector: baby diapers, feminine and adult incontinence products

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

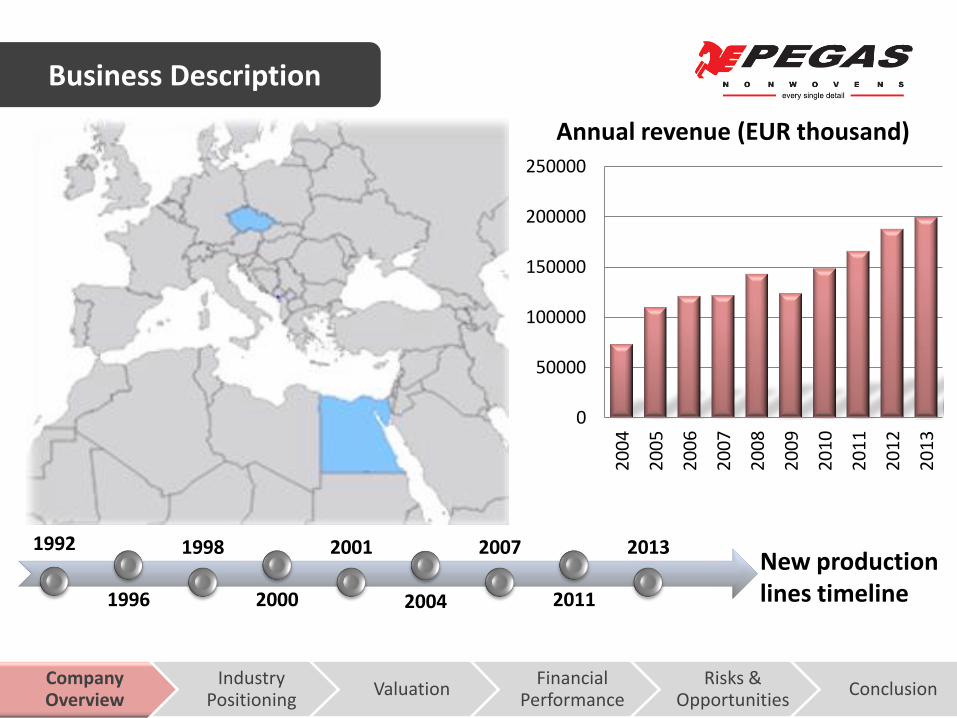

Business Description

Annual revenue (EUR thousand)

1992

1996

1998

2000

2001

2004

2007

2011

2013

0

50000

100000

150000

200000

250000

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

New production lines timeline

Industry Overview & Competitive Positioning

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

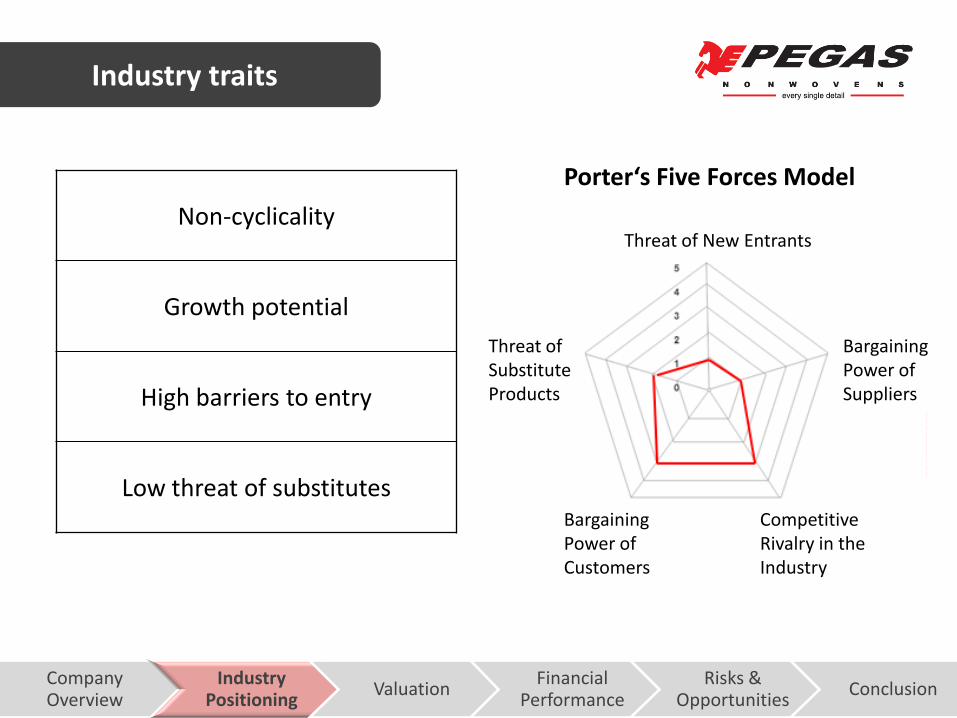

Industry traits

Threat of New Entrants

Threat of Substitute Products

Bargaining Power of Customers

Bargaining Power of Suppliers

Competitive Rivalry in the Industry

Porter‘s Five Forces Model

Non-cyclicality

Growth potential

High barriers to entry

Low threat of substitutes

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

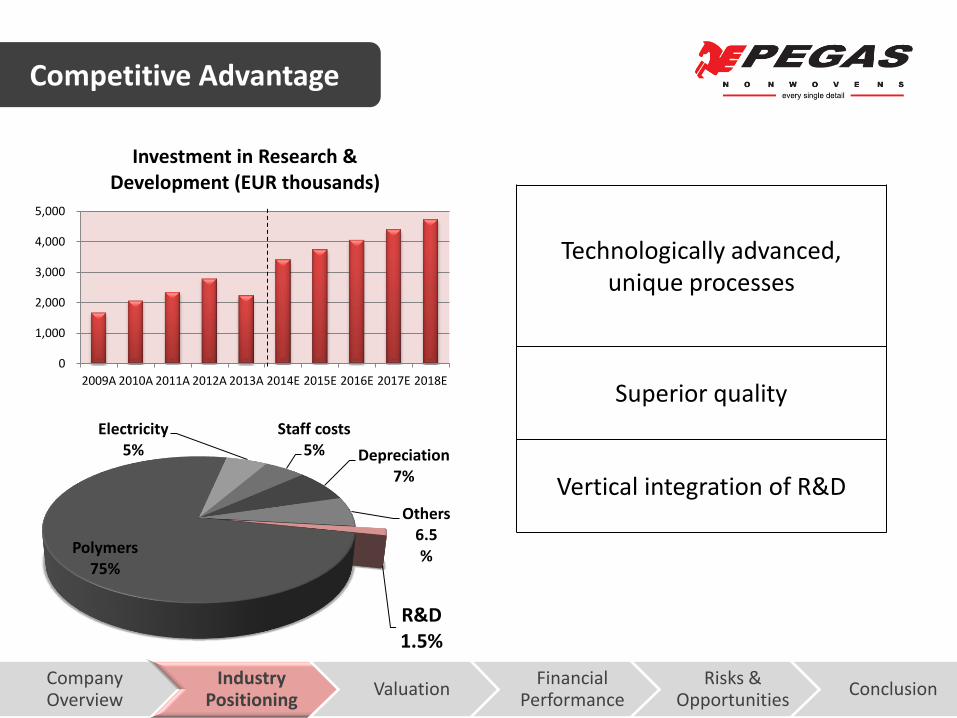

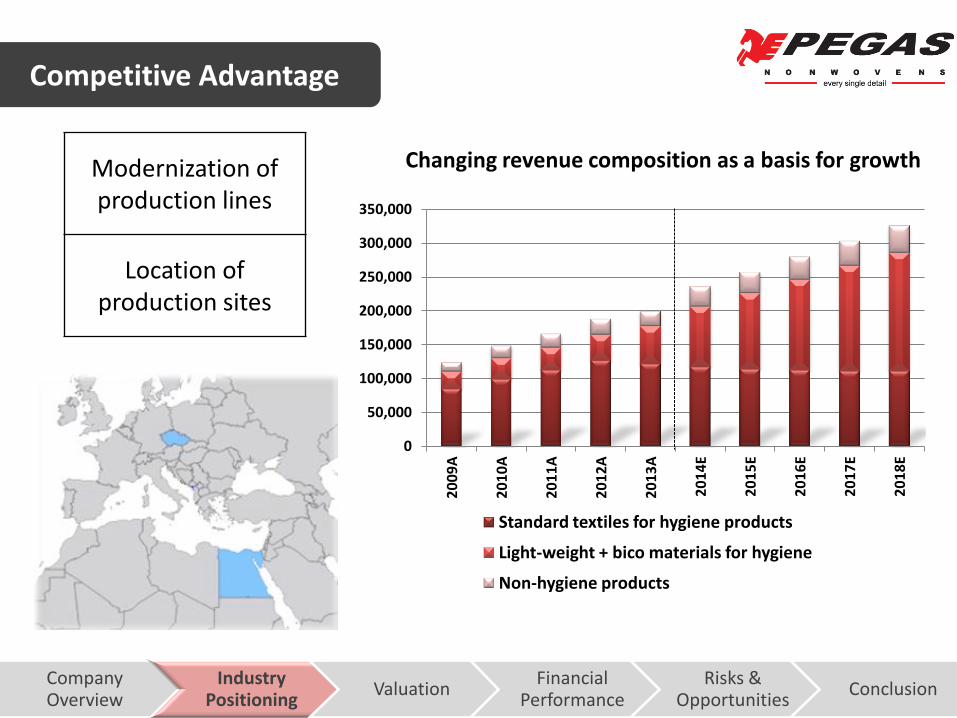

Competitive Advantage

0

1,000

2,000

3,000

4,000

5,000

2009A 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Investment in Research & Development (EUR thousands)

Polymers 75%

Electricity 5%

Staff costs 5% Depreciation

7%

Others 6.5 %

R&D 1.5%

Technologically advanced, unique processes

Superior quality

Vertical integration of R&D

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Competitive Advantage

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

20

09

A

20

10

A

20

11

A

20

12

A

20

13

A

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

Standard textiles for hygiene products

Light-weight + bico materials for hygiene

Non-hygiene products

Modernization of production lines

Location of production sites

Changing revenue composition as a basis for growth

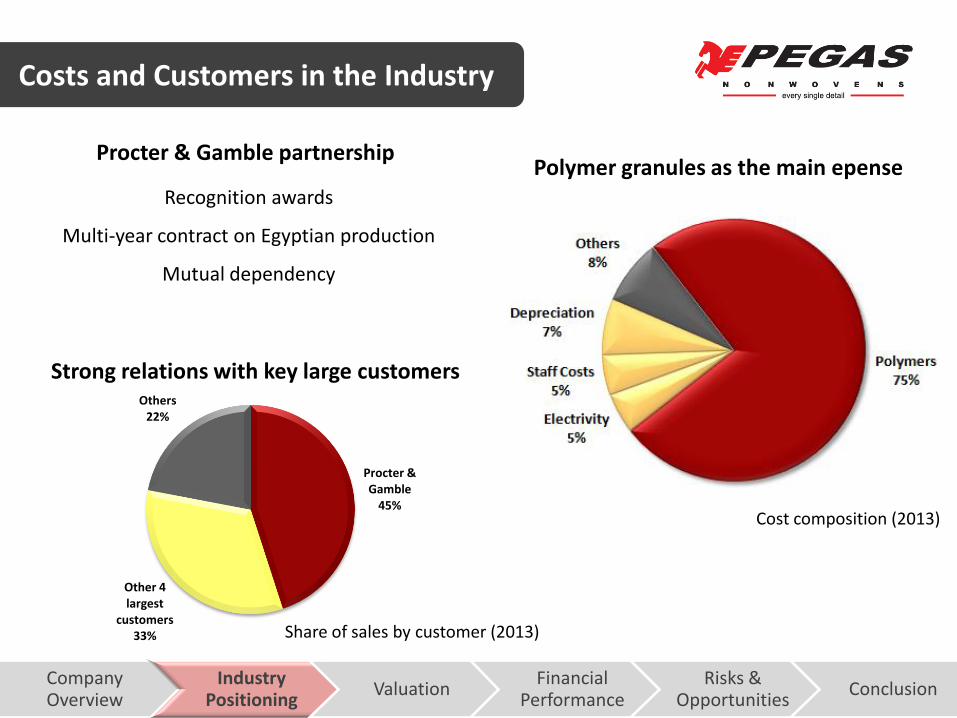

Procter & Gamble partnership

Cost composition (2013)

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Costs and Customers in the Industry

Procter & Gamble

45%

Other 4 largest

customers 33%

Others 22%

Polymer granules as the main epense

Share of sales by customer (2013)

Strong relations with key large customers

Recognition awards

Multi-year contract on Egyptian production

Mutual dependency

Valuation

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

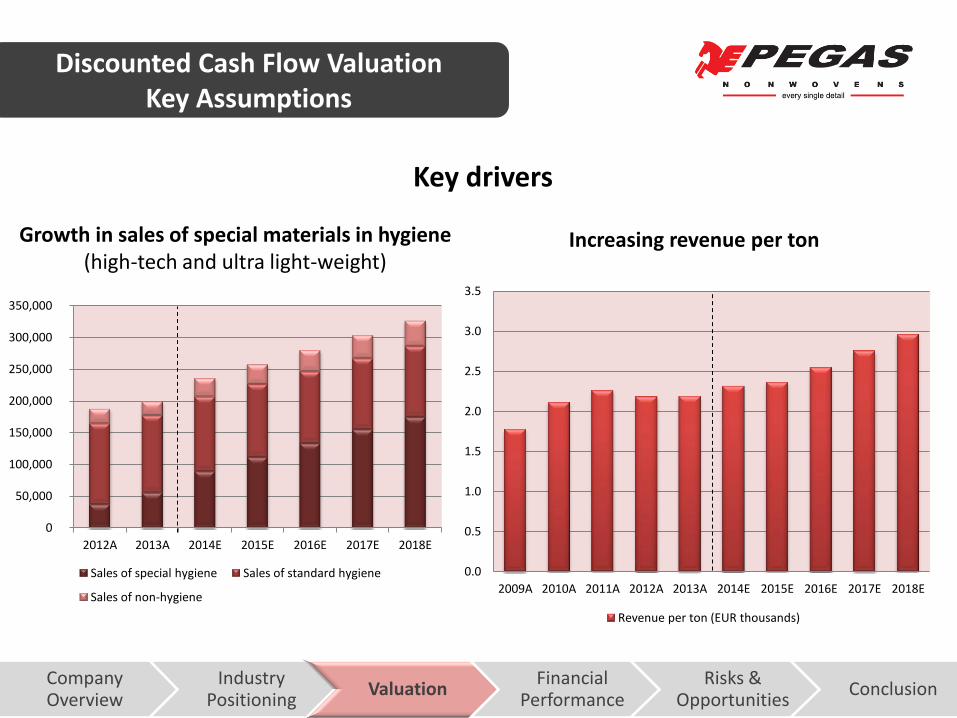

Discounted Cash Flow Valuation Key Assumptions

Key drivers

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2009A 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Increasing revenue per ton

Revenue per ton (EUR thousands)

Growth in sales of special materials in hygiene (high-tech and ultra light-weight)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2012A 2013A 2014E 2015E 2016E 2017E 2018E

Sales of special hygiene Sales of standard hygiene

Sales of non-hygiene

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

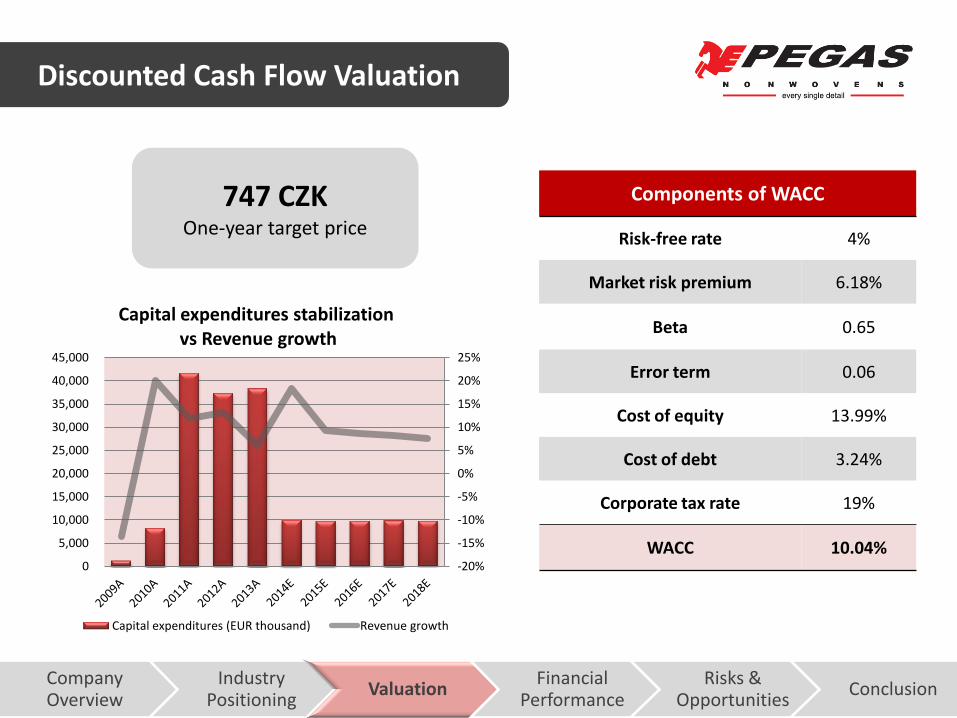

Discounted Cash Flow Valuation

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Capital expenditures stabilization vs Revenue growth

Capital expenditures (EUR thousand) Revenue growth

747 CZK One-year target price

Components of WACC

Risk-free rate 4%

Market risk premium 6.18%

Beta 0.65

Error term 0.06

Cost of equity 13.99%

Cost of debt 3.24%

Corporate tax rate 19%

WACC 10.04%

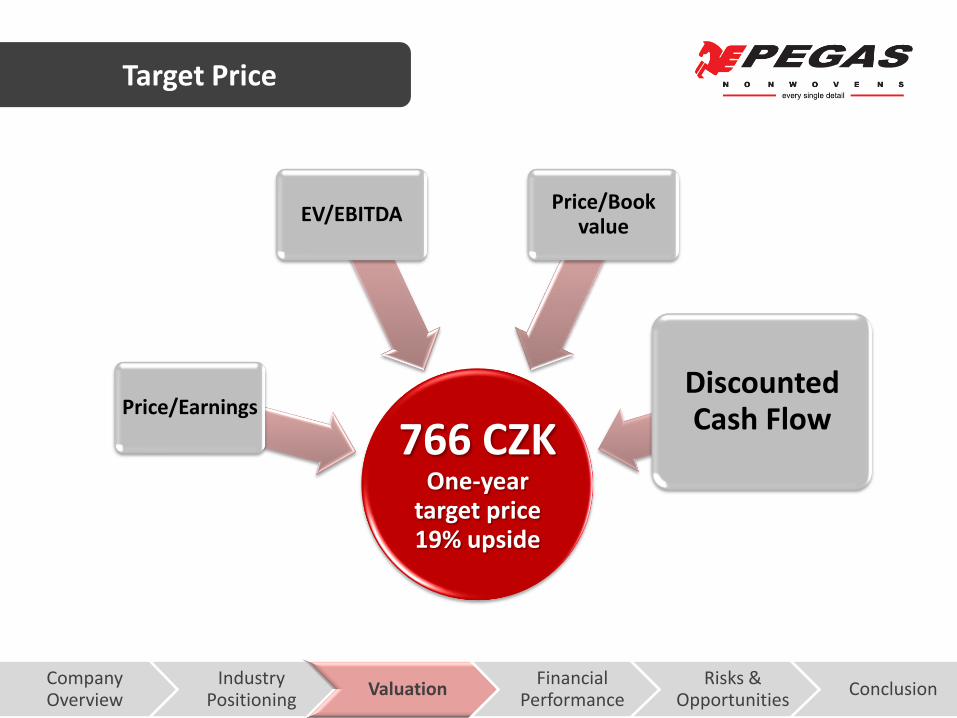

Price/Earnings EV/EBITDA Price/Book

value

13.2 9.0 1.85

890 CZK 778 CZK 764 CZK

Multiples Valuation

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

766 CZK One-year

target price 19% upside

Price/Earnings

EV/EBITDA Price/Book

value

Discounted Cash Flow

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Target Price

Financial Performance

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

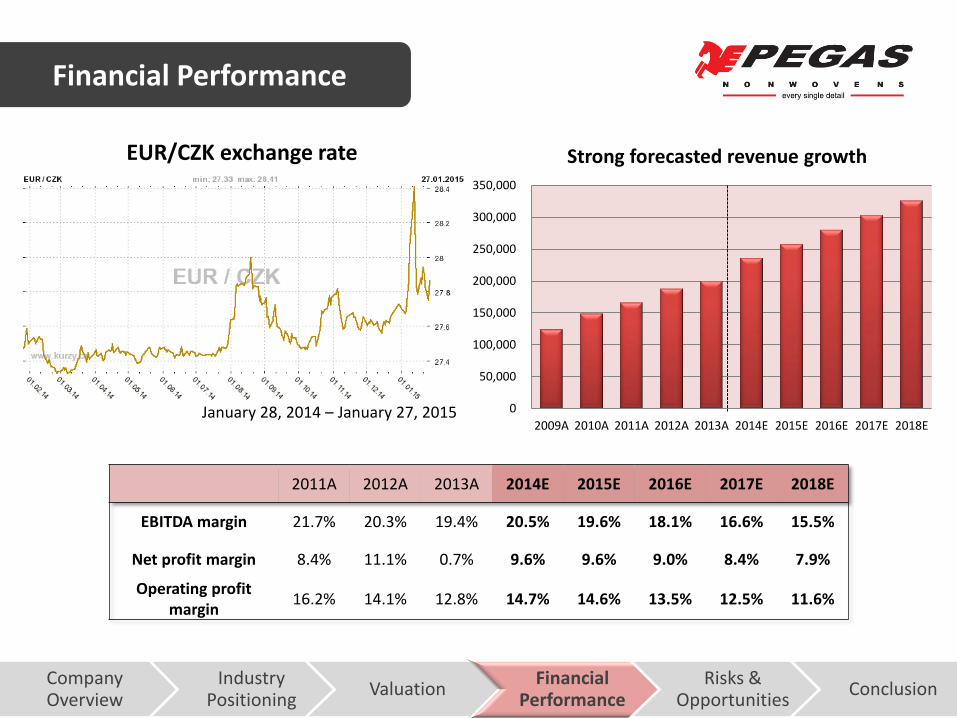

Financial Performance

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2009A 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Strong forecasted revenue growth EUR/CZK exchange rate

January 28, 2014 – January 27, 2015

2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

EBITDA margin 21.7% 20.3% 19.4% 20.5% 19.6% 18.1% 16.6% 15.5%

Net profit margin 8.4% 11.1% 0.7% 9.6% 9.6% 9.0% 8.4% 7.9%

Operating profit margin

16.2% 14.1% 12.8% 14.7% 14.6% 13.5% 12.5% 11.6%

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Financial Performance

0.00

0.50

1.00

1.50

2.00

2.50

2009A 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Progressive dividend policy

Gross dividend (EUR/share)

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

2012A 2013A 2014E 2015E 2016E 2017E 2018E

125,000

130,000

135,000

140,000

145,000

150,000

155,000

160,000

165,000

Decrease in long term debt levels

Long term debt Debt as % of EBITDA

Risk Analysis

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

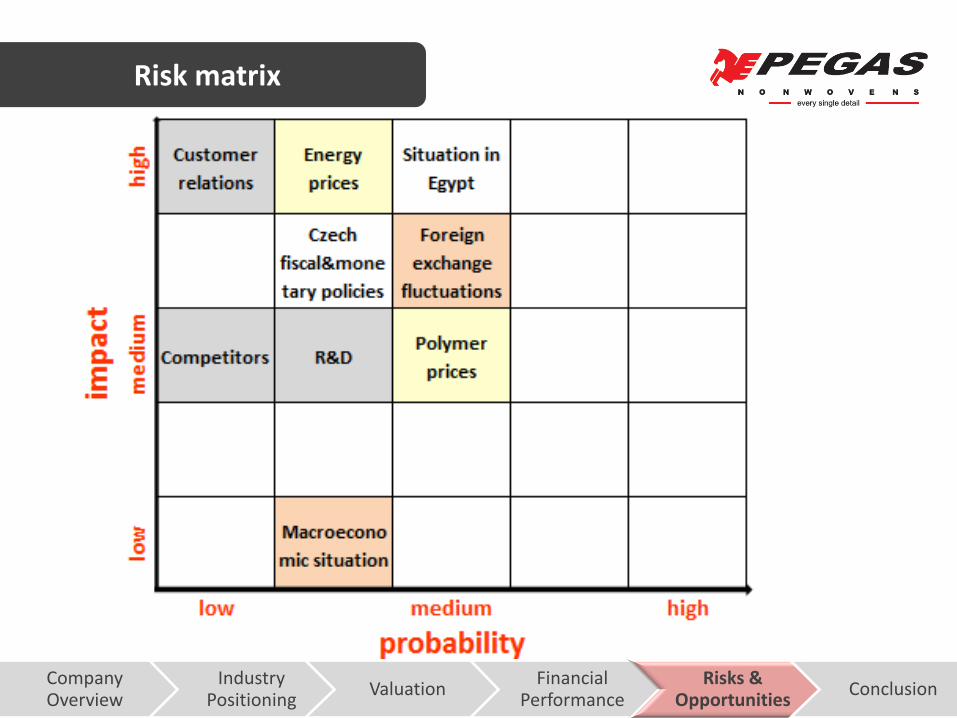

Risk matrix

100%

78%

45%

• all customers

• 5 customers

• 1 customer

Sensitivity of the target price to energy and staff costs

Composition of customers as % of sales (2013)

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Key Customers and Costs

Importance of the large corporate customers

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Expansion to Egypt: Upside Risk

642 CZK December 18, 2014

19% upside

827 CZK UPSIDE TARGET PRICE

766 CZK TARGET PRICE

29% upside

Upside scenario: annual revenue (EUR thousand)

Conclusion

BUY

Industry traits

non-cyclicality and growth

Competitive position

location of production sites, innovation and quality,

customer relations

Strong performance

financial performance, constant growth, dividend

payouts

Expansion in Egypt

Company Overview

Industry Positioning

Valuation Financial

Performance Risks &

Opportunities Conclusion

Conclusion

Thank you for your attention!

Team H

January 28, 2015