Pecking and tradeoff theory

24

-

Upload

abdul-wali-khan-university-mardan-pakistan -

Category

Business

-

view

341 -

download

1

Transcript of Pecking and tradeoff theory

CAPITAL STRUCTURE THEORIES

Pecking Theory and Trade off theory

By: Muhammad Owais Khan

Group Members

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Theory:

• Myers (1984) A firm is said to follow a pecking order if it prefers

internal to external financing and debt to equity

if external financing is used.

By: Muhammad Owais Khan

P e c k i n g t h e o r y

• Adverse Sect ion :

• The most common motivation for the pecking order is adverseselection developed by Myers and Majluf (1984) and Myers (1984). Thekey idea is that the owner-manager of the firm knows the true value ofthe firm’s assets and growth opportunities. Outside investors can onlyguess these values. If the manager offers to sell equity, then theoutside investor must ask why the manager is willing to do so. In manycases the manager of an overvalued firm will be happy to sell equity,while the manager of an undervalued firm will not.

By: Muhammad Owais Khan

P e c k i n g t h e o r y

• Agency Theory :

• The idea that managers prefer internal financing to external financingis, of course, old (e.g., Butters 1949). Traditionally the argument wasthat outside financing required managers to explain the projectdetails to outside investors, and expose themselves to investormonitoring. Managers dislike this process. Thus, managers have apreference for retained earnings over external financing but their is nodirect prediction about the relative use of debt versus equity whenseeking external financing. These ideas were subsequently developedinto agency theories with Jensen and Meckling (1976) being aprominent contribution.

By: Muhammad Owais Khan

P e c k i n g t h e o r y

• Agency Theory :

• A modern corporation is a team effort involving many players,including management, employees, share holders. The member of thiscorporate team are bound together by a series of formal and informalcontracts to ensure that they pull together.

• For a long time economists assumed that all players acted for thecommon good but in the last 20 years we have learn a lot about thepossible conflicts of interest and how companies try to overcome suchconflicts these ideas are collectively known as agency theory.

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Fund Raising Steps:

Internal Funds

New Debt

New Equity

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Over Price of Share:

Current price of equity

Company's performance

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Theory Detail :

Internal F inance i s preferred

Target Div idend Payout Rat io

l imi ted Internal cash generat ion

Requi rement of External F inance

I s su ing of New Shares

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Theory Detail Cont.:

Share Pr ice Reponses

Share Pr ice and bus iness level

Leverage has negat ive relat ion with prof i tabi l i ty

Actual debt rat io

By: Muhammad Owais Khan

P e c k i n g t h e o r y

Theory Detail Cont.:

Popular i ty of Internal F inance

Less prof i table f i rms have to borrow more

Leverage depend upon operat ing cash f lows and investment need over t ime

By: Muhammad Owais Khan

P e c k i n g t h e o r y

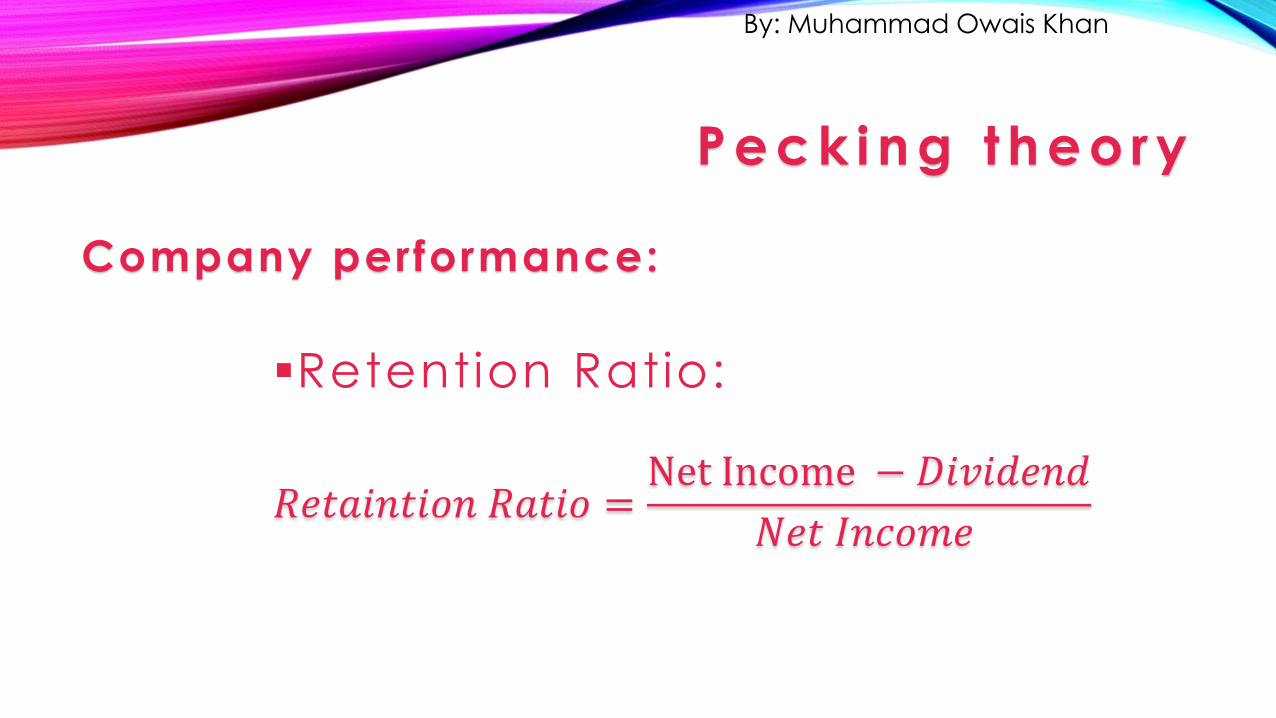

Company performance:

Retention Ratio:

𝑅𝑒𝑡𝑎𝑖𝑛𝑡𝑖𝑜𝑛 𝑅𝑎𝑡𝑖𝑜 =Net Income − 𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑

𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒

By: Muhammad Owais Khan

P e c k i n g t h e o r y

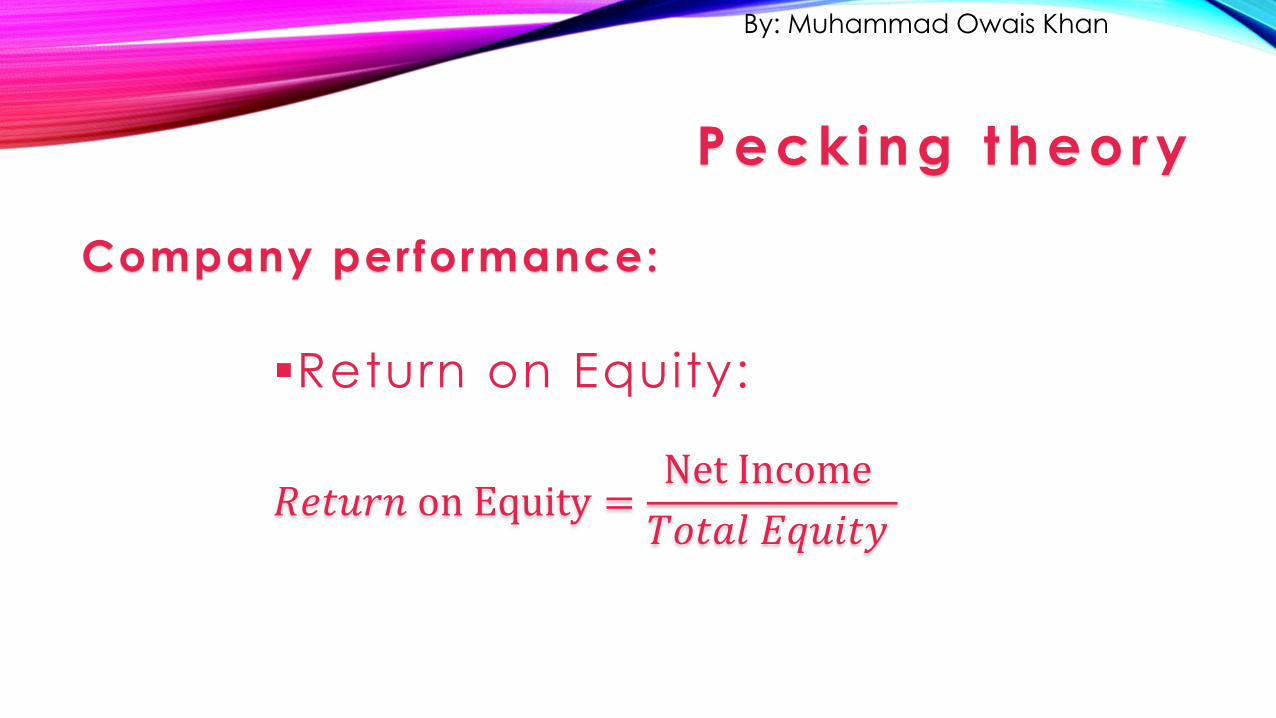

Company performance:

Return on Equity:

𝑅𝑒𝑡𝑢𝑟𝑛 on Equity =Net Income

𝑇𝑜𝑡𝑎𝑙 𝐸𝑞𝑢𝑖𝑡𝑦

By: Muhammad Owais Khan

P e c k i n g t h e o r y

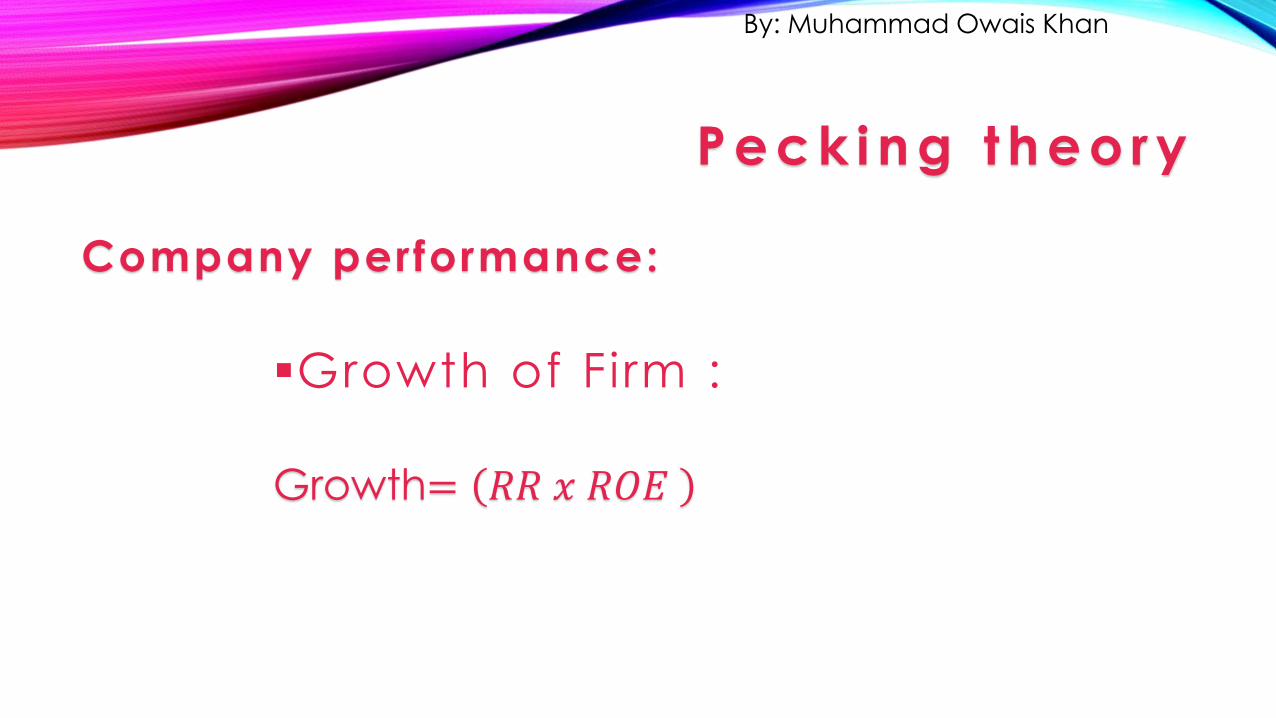

Company performance:

Growth of Firm :

Growth= 𝑅𝑅 𝑥 𝑅𝑂𝐸

By: Muhammad Owais Khan

P e c k i n g t h e o r y

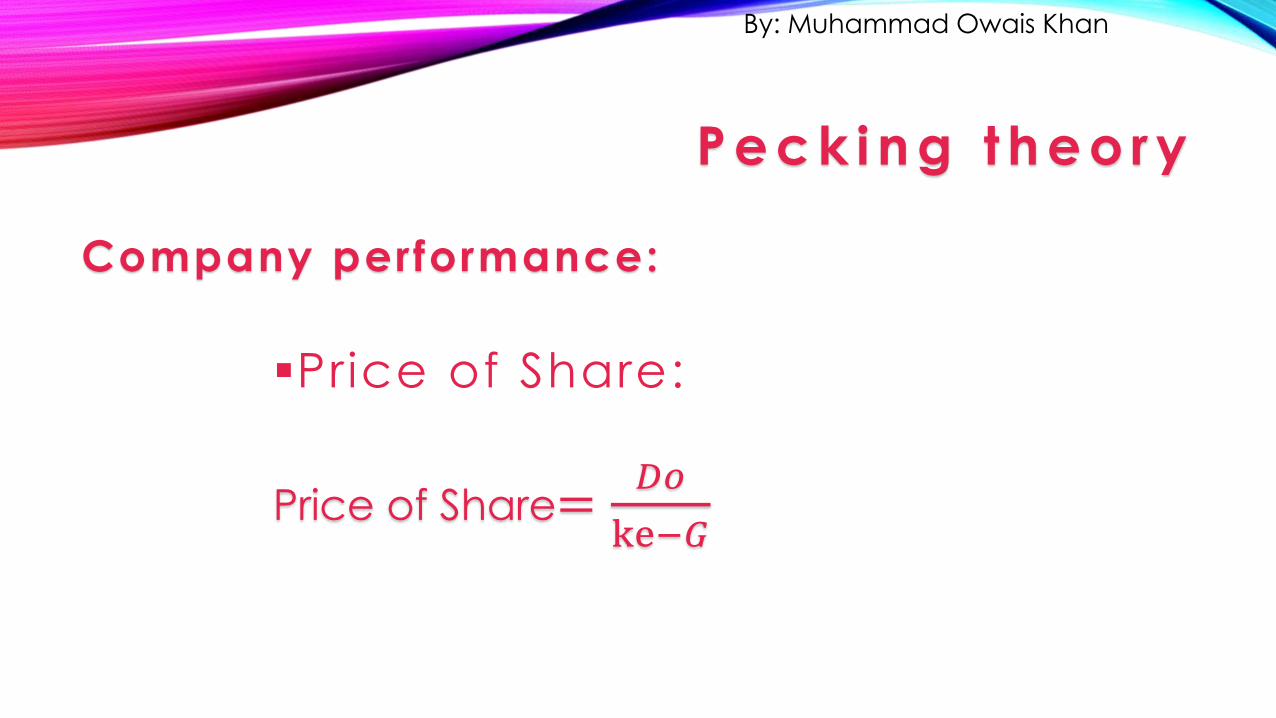

Company performance:

Price of Share:

Price of Share=𝐷𝑜

ke−𝐺

By: Muhammad Owais Khan

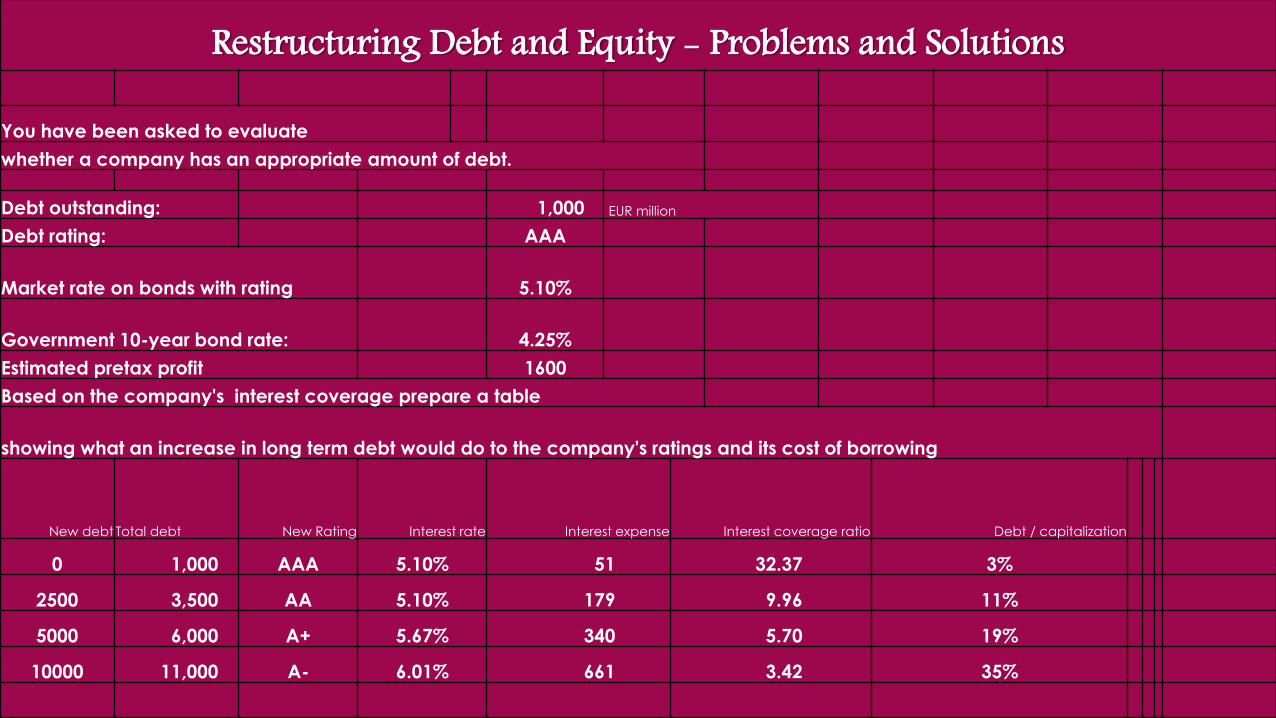

Restructuring Debt and Equity - Problems and Solutions

You have been asked to evaluate

whether a company has an appropriate amount of debt.

Debt outstanding: 1,000 EUR million

Debt rating: AAA

Market rate on bonds with rating 5.10%

Government 10-year bond rate: 4.25%

Estimated pretax profit 1600

Based on the company's interest coverage prepare a table

showing what an increase in long term debt would do to the company's ratings and its cost of borrowing

New debt Total debt New Rating Interest rate Interest expense Interest coverage ratio Debt / capitalization

0 1,000 AAA 5.10% 51 32.37 3%

2500 3,500 AA 5.10% 179 9.96 11%

5000 6,000 A+ 5.67% 340 5.70 19%

10000 11,000 A- 6.01% 661 3.42 35%

T r a d e - o f f t h e o r y

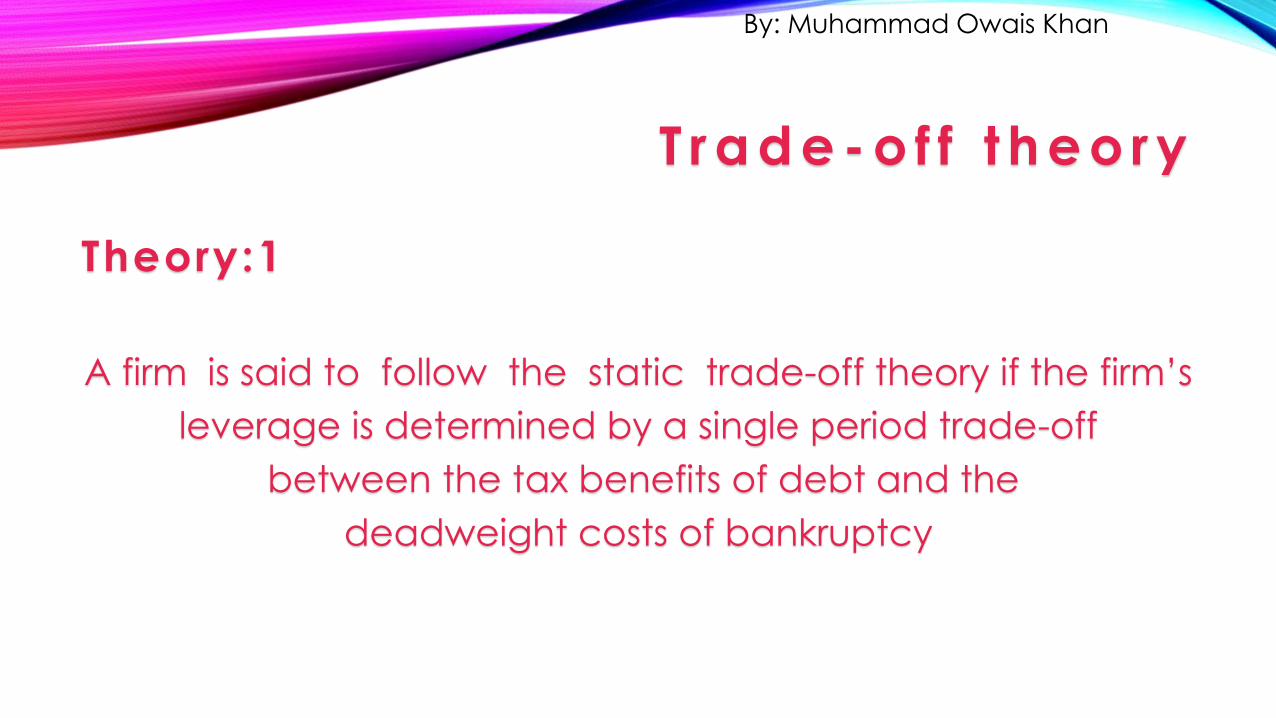

Theory:1

A firm is said to follow the static trade-off theory if the firm’s

leverage is determined by a single period trade-off

between the tax benefits of debt and the

deadweight costs of bankruptcy

By: Muhammad Owais Khan

T r a d e - o f f t h e o r y

Theory:2

A firm is said to exhibit target adjustment behavior

If the firm has a target level of leverage and

the deviation from that target are

Gradually removed over time

By: Muhammad Owais Khan

T r a d e - o f f t h e o r y

Theory Detail :

Cost and Benef i ts

Trade off between debt and equi ty

Tax saving

Dist ress cost

Bus iness r i sk and leverage

By: Muhammad Owais Khan

T r a d e - o f f t h e o r y

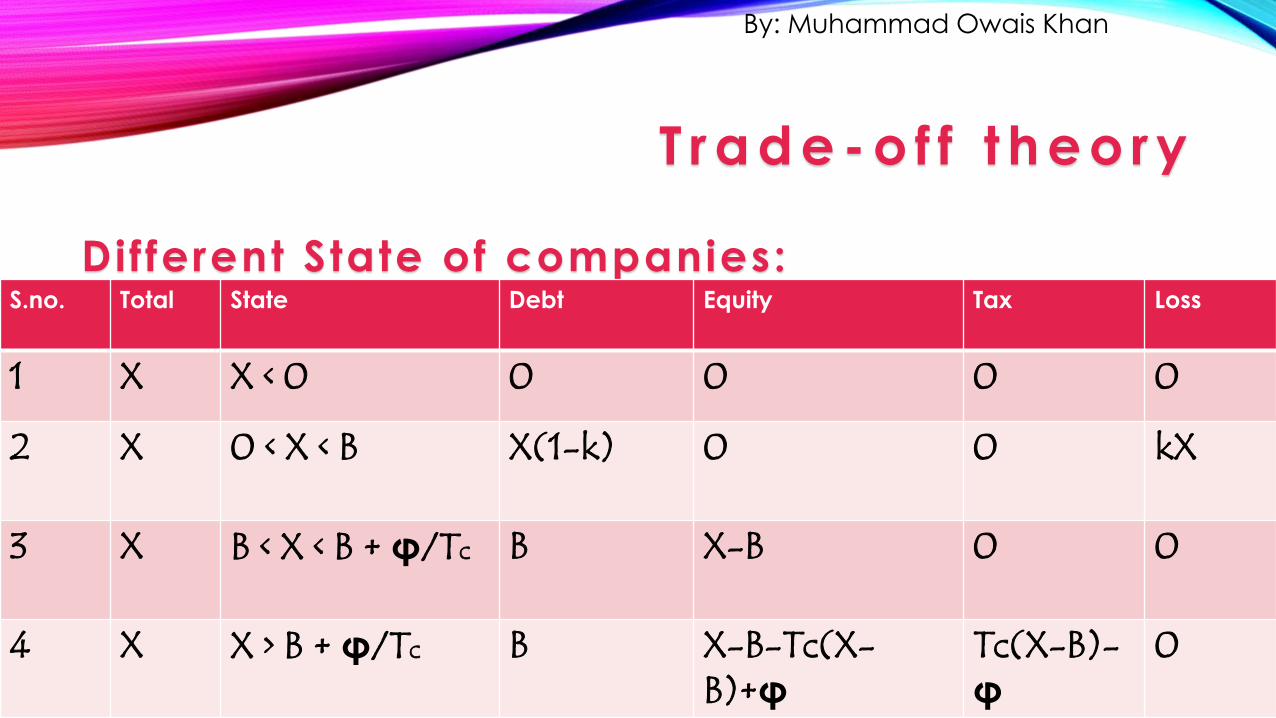

Different State of companies:S.no. Total State Debt Equity Tax Loss

1 X X < 0 0 0 0 0

2 X 0 < X < B X(1-k) 0 0 kX

3 X B < X < B + φ/Tc B X-B 0 0

4 X X > B + φ/Tc B X-B-Tc(X-B)+φ

Tc(X-B)-φ

0

By: Muhammad Owais Khan

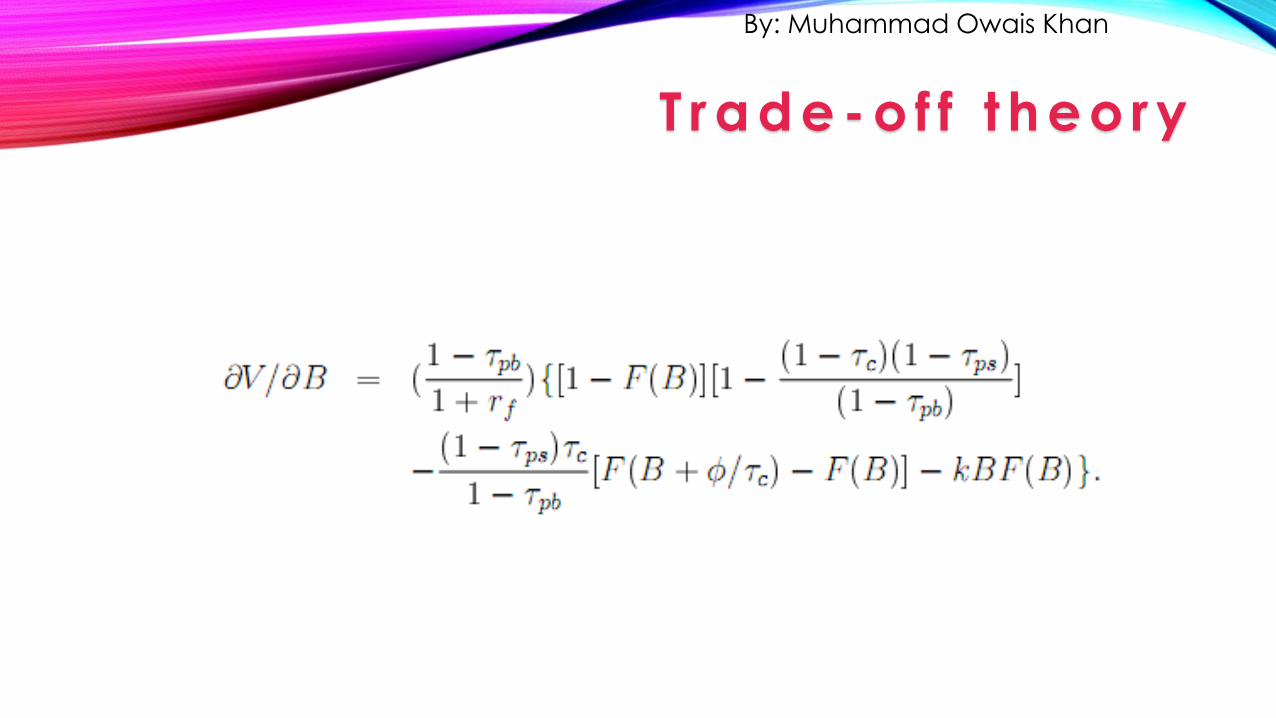

T r a d e - o f f t h e o r y

By: Muhammad Owais Khan

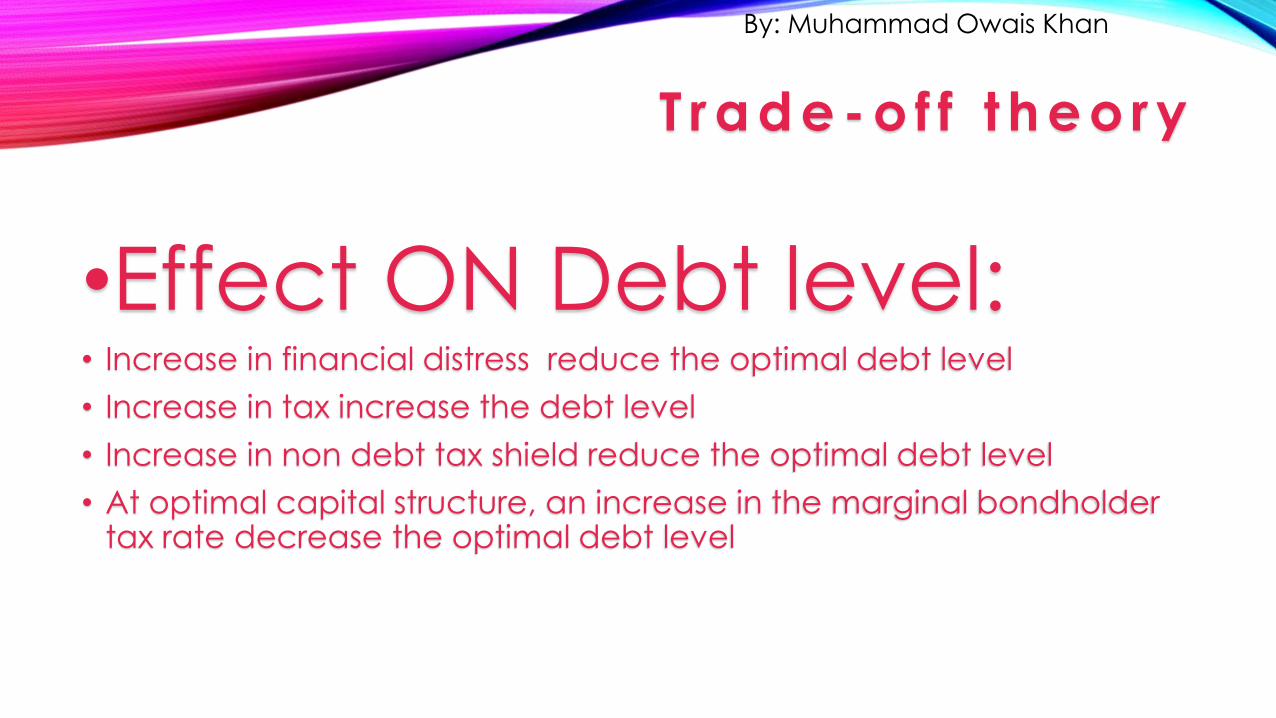

•Effect ON Debt level:• Increase in financial distress reduce the optimal debt level

• Increase in tax increase the debt level

• Increase in non debt tax shield reduce the optimal debt level

• At optimal capital structure, an increase in the marginal bondholder tax rate decrease the optimal debt level

T r a d e - o f f t h e o r y

By: Muhammad Owais Khan

THE ENDPecking Theory and Trade off theory

By: Muhammad Owais Khan