Peck, Shaffer & Williams LLP 1 Federal Income Tax Issues Matthias Edrich Erick Stowe January 30,...

34

Peck, Shaffer & Williams LLP 1 Federal Income Tax Issues Matthias Edrich Erick Stowe January 30, 2009

-

Upload

elmer-anthony -

Category

Documents

-

view

220 -

download

3

Transcript of Peck, Shaffer & Williams LLP 1 Federal Income Tax Issues Matthias Edrich Erick Stowe January 30,...

Peck, Shaffer & Williams LLP

1

Federal Income Tax Issues

Matthias Edrich

Erick StoweJanuary 30, 2009

Peck, Shaffer & Williams LLP

2

Presenters

• Matthias Edrich, is a second year associate of Peck Shaffer with a focus on transaction structure, documents, disclosure and tax matters

• Erick Stowe, more than 30 years’ practice in public finance, partner at Peck Shaffer with a focus on tax matters

Peck, Shaffer & Williams LLP

3

Basic Tax Rule

Interest on debt of a state or political subdivision is excluded from federal gross income unless the debt is a private activity bond (that is not a qualified private activity bond) and unless the debt is an arbitrage bond.

There are also some technical rules that must be met.

Peck, Shaffer & Williams LLP

4

Issuers

• State or Local Governmental Issuer– State, D.C., Possession or Political Subdivision– On Behalf Of/Constituted Authority– 63-20 Issuers– Indian Tribal Governments– Other

Peck, Shaffer & Williams LLP

5

Debt

– Valid Exercise of Borrowing Power– Nonrecourse, Conduit or Revenue Financings– Debt Must Be Incurred– May be Lease or Installment Sale in Form --

Interest Must Be Separately Stated

Peck, Shaffer & Williams LLP

6

Private Activity Bonds

• Use of Proceeds– Governmental Bond– Qualified Private Activity Bond

• Private Business Use Test

• Private Loan Test

Peck, Shaffer & Williams LLP

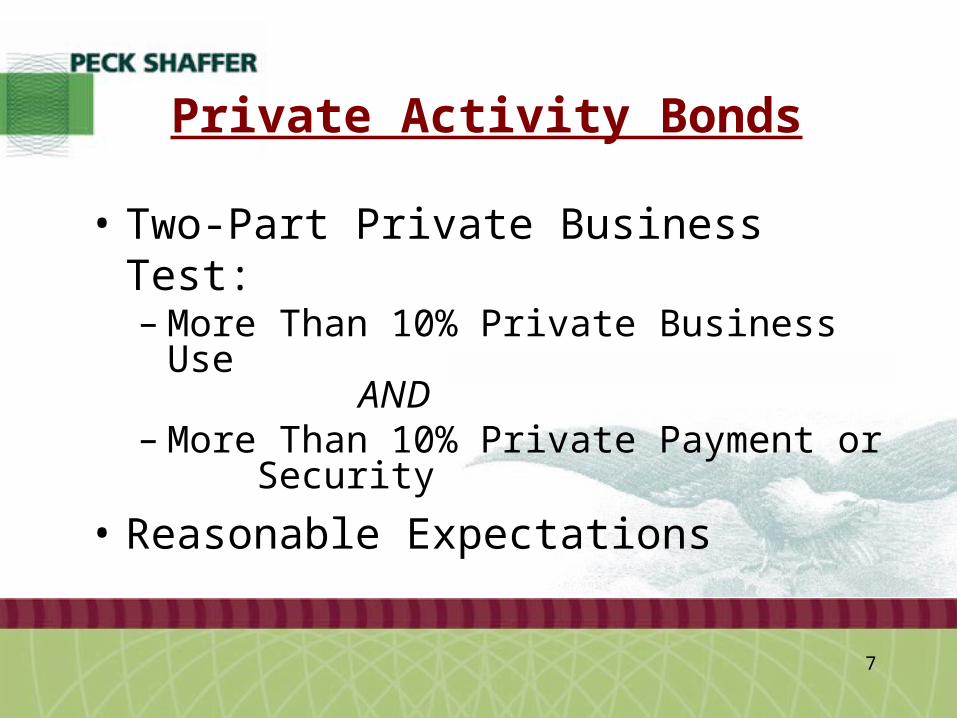

7

Private Activity Bonds

• Two-Part Private Business Test:– More Than 10% Private Business Use

AND– More Than 10% Private Payment or Security

• Reasonable Expectations

Peck, Shaffer & Williams LLP

8

Private Business Use?

• Use By a “Nongovernmental Person”– Federal Government– Section 501(c)(3) Organization– Other Private Entity (Corporation, Partnership,

LLC)

Peck, Shaffer & Williams LLP

9

Private Business Use?

• Use Includes– Ownership– Lease/Sublease– Certain Management/Services Contracts– Certain Sponsored Research Agreements– Certain Output Contracts– “Special Legal Entitlement”– “Special Economic Benefit”

Peck, Shaffer & Williams LLP

10

Private Business Use?

• Exceptions– “General Public Use”– Short, Incidental and Temporary Use

• Measuring Private Business Use– Generally Measured Over Time– Allocation for Mixed Use Facilities

Peck, Shaffer & Williams LLP

11

Private Payment Test

• Measure Private Payments– Present Value (PV) of all Private Payments

over Term of Bonds– All private Payments Benefiting Issuer– Limited to the Amount of Private Use– Excludes Operating Expenses – Generally applicable taxes are not private

payments

Peck, Shaffer & Williams LLP

12

Private Loan

• Alternative to Private Business Test• Measure Loans

– In Amounts More Than the Lesser of• 5% of the Bond Proceeds or• $5 million

• Used to Make or Finance Loans to Nongovernmental Persons

• Tax Assessment Exception

Peck, Shaffer & Williams LLP

13

Qualified Private Activity Bonds• 501(c)(3) Bonds• Small Issue (Maximum $10 million) for

Manufacturing and 1st Time Farmers• Acquisition of Non-Government Output Facility

Bonds• Student Loan Bonds• Qualified Redevelopment Bonds• Low- and Moderate-Income Single Family

Mortgage Bonds• Exempt Facilities

Peck, Shaffer & Williams LLP

14

PABs – Exempt Facility Bonds• Airports

Docks and WharvesMass CommutingEnvironmental Enhancement of Hydroelectric Facilities

• Residential Rental FacilitiesWater FurnishingSewage FacilitiesSolid Waste FacilitiesLocal Furnishing of gas or electricityLocal District Heating or CoolingQualified Hazardous Waste FacilitiesHigh Speed Intercity Rail FacilitiesPublic Educational FacilitiesEnterprise Zone Facilities

Peck, Shaffer & Williams LLP

15

Requirements For All Bonds

• Reimbursement Rules– Declaration of Official Intent By Issuer of

Bonds (or 501(c)(3) Organization) Specifying Project and Principal Amount

– Can Reimburse Costs Paid No More Than 60 Days Before Declaration of Intent (Exceptions for Preliminary Expenditures and De Minimis Amount)

Peck, Shaffer & Williams LLP

16

Requirements For All Bonds

• Reimbursement Rules– Reimbursement Within 18 Months of Later of

Date Expenditure Paid or Project Placed In Service (Overall 3 Year Limit From Date Expenditure Paid)

Peck, Shaffer & Williams LLP

17

Requirements For All Bonds

• Bonds Must Be In Registered Form• Federal Guarantee Restriction

– Exceptions For Housing Bonds, Refunding Escrows, Certain Agency Guarantees

• Information Reporting– Form 8038, Form 8038-G, Form 8038-GC– Filing Deadlines, Late Filing– Source of Information

Peck, Shaffer & Williams LLP

18

Arbitrage – Basic Rule

• Proceeds of an issue cannot be invested at above the yield on the bonds except during temporary periods, as part of a reasonable reserve, as part of a minor portion, and arbitrage earnings must generally be rebated.

Peck, Shaffer & Williams LLP

19

Arbitrage – Basic Questions

• Arbitrage- - Can you earn it?– Temporary Periods– Minor Portion ($100,000)– Invested at yield not materially higher

Peck, Shaffer & Williams LLP

20

Arbitrage

• Definition of Gross Proceeds– Sale Proceeds– Investment Proceeds– Replacement Funds (Sinking Fund, Pledged

Fund, Negative Pledge)– Transferred Proceeds

Peck, Shaffer & Williams LLP

21

Arbitrage

• Temporary Periods– Construction or Other Capital Projects (3-Year)

• Must expect to satisfy “Expenditure Test”

– Bona Fide Debt Service Fund

Peck, Shaffer & Williams LLP

22

Arbitrage

• Temporary Periods– Construction (3 years)– Refunding Escrow (30 days)– Investment Income (1 Year)– Replacement Proceeds (30 Days)– Working Capital (13 Months)

Peck, Shaffer & Williams LLP

23

Arbitrage• Yield

– General Calculation Method– Initial Offering Price

– Guarantee Fees– Costs of Issuance

• Materially Higher

– Generally 1/8 of 1%

– Acquired Program Investment 1.5%

– Replacement Proceeds and Restricted Escrows 1/1000 of 1%

Peck, Shaffer & Williams LLP

24

Reasonably Required Reserve Fund

• Sizing Limits– MADS, 125% AADS, 10% issue– Funding limit: 10% of issue

• “Reasonably Required”

Peck, Shaffer & Williams LLP

25

Rebate – Basic Rules

• Rebate- - Can you keep it?– Small Issuer Exception– 6 month Exception (includes refundings)– 18 Month Exception– 2-Year Construction Exception

• Calculation Periods

• Yield Reduction Payments

Peck, Shaffer & Williams LLP

26

Rebate – Basic Rules

• Rebate- - Can you keep it?– Small Issuer Exception– 6 month Exception (includes refundings)– 18 Month Exception– 2-Year Construction Exception

• Calculation Periods

• Yield Reduction Payments

Peck, Shaffer & Williams LLP

27

Voluntary Closing Agreement Program

• If ongoing post-issuance compliance efforts have not prevented violation of rules applicable to qualified 501(c)(3) bonds, voluntary closing agreement program (“VCAP”) is available in some situations

Peck, Shaffer & Williams LLP

28

CONCLUSION

Where Do We Go From Here?

Peck, Shaffer & Williams LLP

29

A. Take Stock of Existing Bond Financings and Potential Issues ► May involve an outside consultant

B. Addressing of Issues Discovered

I. Bond Audit

Peck, Shaffer & Williams LLP

30

A. Designate Responsibility for Monitoring Compliance with Conditions Required to Maintain Tax Exemption of Interest on Bonds ► May be internal responsibility, external responsibility or combination

► Centralized responsibility

II. Ongoing Compliance Program

Peck, Shaffer & Williams LLP

31

B. Rebate/Spend-Down Monitoring

C. Tracking of Bond Proceeds

► Must know how bond proceeds were spent, what portions of facilities bond-financed

Peck, Shaffer & Williams LLP

32

D. Review of Management Contracts/Research Agreements by Bond Counsel to Ensure Compliance with Qualified Management Contract Rule

E. Special Care for Investment of Bond Proceeds to Address IRS Concerns With Yield-Burning

► Involve Bond Counsel in process of bidding GICs

Peck, Shaffer & Williams LLP

33

F. Keep Records With Respect to Expenditures and Investment of Bond Proceeds Until 3-6 Years Following Retirement of Bonds

► Don’t rely on others for record-keeping

Peck, Shaffer & Williams LLP

34

Matthias Edrich and Erick Stowe

Presenters’ Information

Peck, Shaffer & Williams LLPSuite 17001801 BroadwayDenver, Colorado 80202

(303) 296-3996 Main(877) 296-0333 WATTS (Toll Free)(303) 296-0344 Facsimile

www.peckshaffer.com