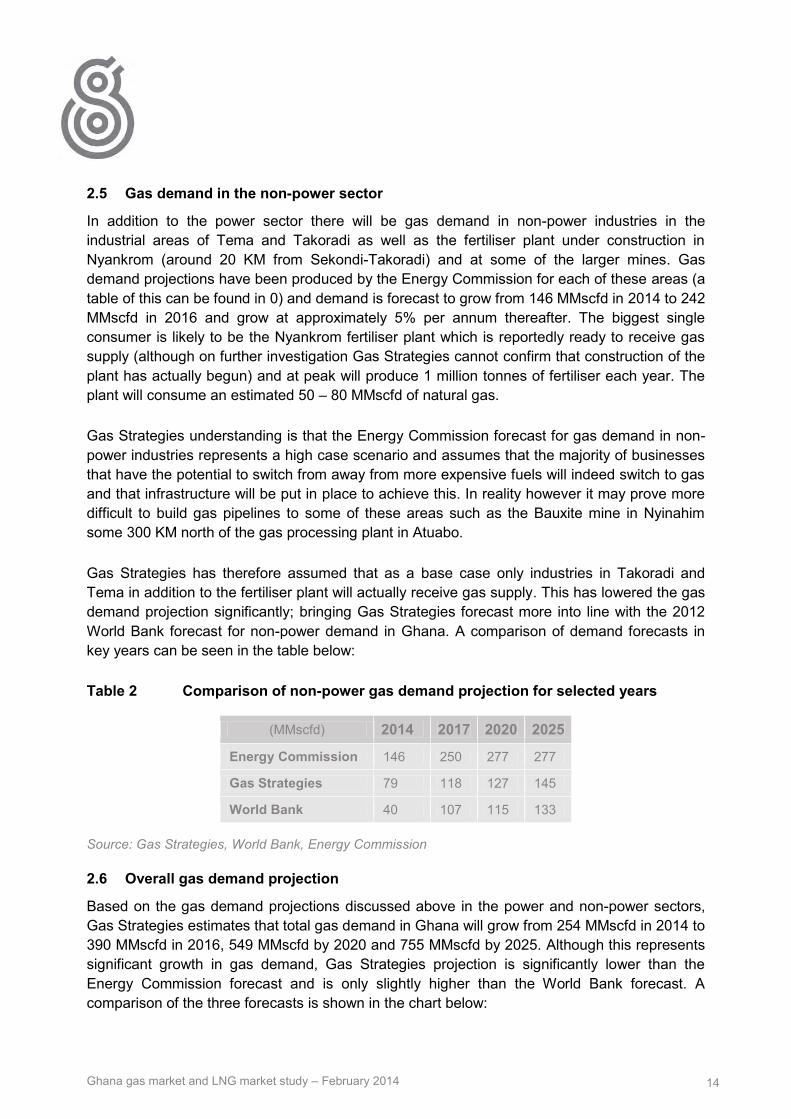

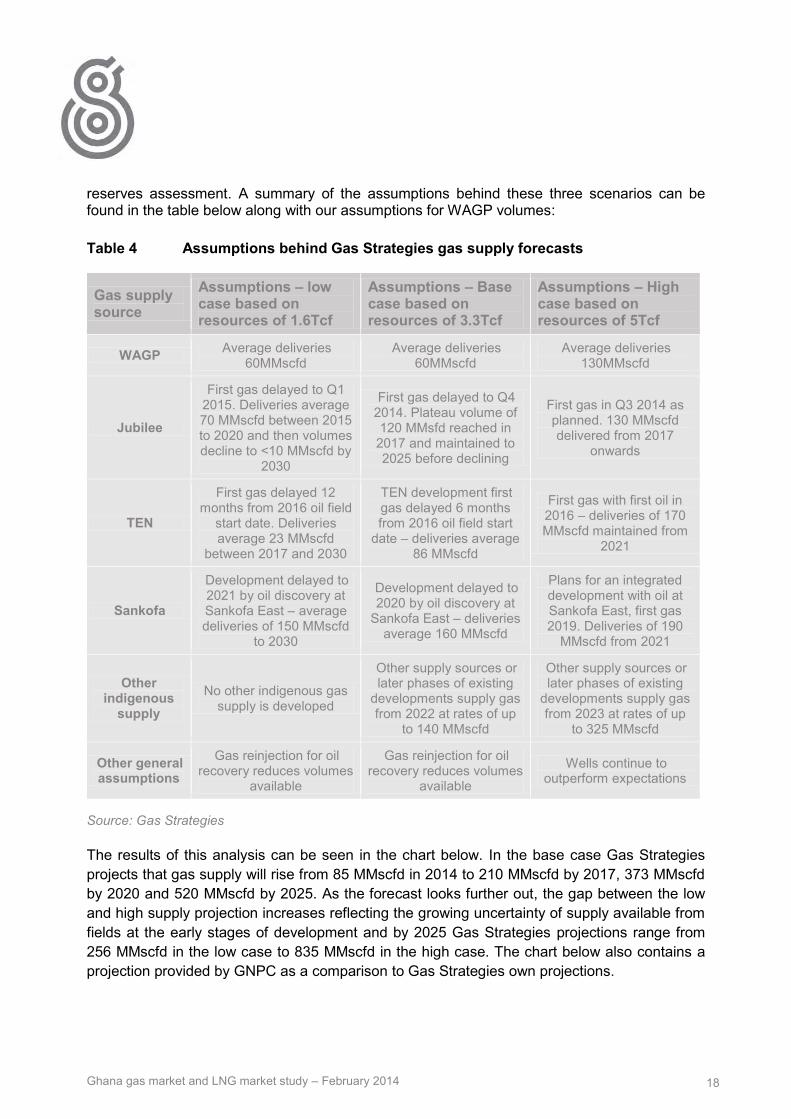

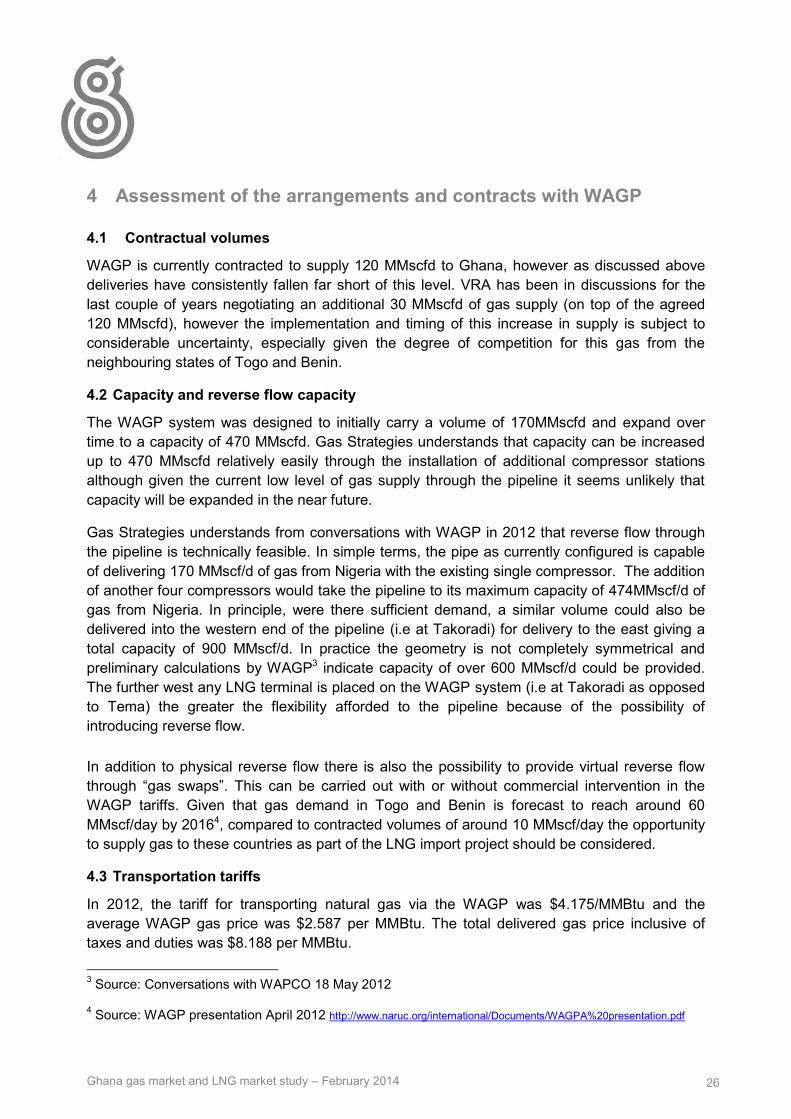

GHANA LIQUID NATURAL GAS STUDIES AND...

284

GHANA LIQUID NATURAL GAS STUDIES AND DESIGN SCREENING REPORT Prepared for: U.S. Army Corps of Engineers, Europe District U.S. ARMY CORPS OF ENGINEERS, EUROPE CONTRACT NUMBER: W912GB-12-D-0020, Order 0004 In Association with: The Millennium Challenge Corporation By: CH2MHill March 2014 The report was funded with the proceeds of a grant from The Millennium Challenge Corporation to the Government of Ghana for the preparation of a compact, issued under Section 609(g) of the Millennium Challenge Act of 2003. The use of the information in the report is subject to the following: 252.227-7022 Government Rights (Unlimited) MAR 1979 The Government shall have unlimited rights, in all drawings, designs, specifications, notes and other works developed in the performance of this contract, including the right to use same on any other Government design or construction without additional compensation to the Contractor. The Contractor hereby grants to the Government a paid-up license throughout the world to all such works to which he may assert or establish any claim under design patent or copyright laws. The Contractor for a period of three (3) years after completion of the project agrees to furnish the original or copies of all such works on the request of the Contracting Officer. 252.227-7023 Drawings and Other Data to become Property of Government MAR 1979 All designs, drawings, specifications, notes and other works developed in the performance of this contract shall become the sole property of the Government and may be used on any other design or construction without additional compensation to the Contractor. [The term "Government" above refers to the US Government.]

Transcript of GHANA LIQUID NATURAL GAS STUDIES AND...

GHANA LIQUID NATURAL GAS STUDIES AND DESIGN SCREENING REPORT

Prepared for: U.S. Army Corps of Engineers, Europe District U.S. ARMY CORPS OF ENGINEERS, EUROPE CONTRACT NUMBER: W912GB-12-D-0020, Order 0004 In Association with: The Millennium Challenge Corporation By: CH2MHill March 2014 The report was funded with the proceeds of a grant from The Millennium Challenge Corporation to the Government of Ghana for the preparation of a compact, issued under Section 609(g) of the Millennium Challenge Act of 2003. The use of the information in the report is subject to the following: 252.227-7022 Government Rights (Unlimited) MAR 1979 The Government shall have unlimited rights, in all drawings, designs, specifications, notes and other works developed in the performance of this contract, including the right to use same on any other Government design or construction without additional compensation to the Contractor. The Contractor hereby grants to the Government a paid-up license throughout the world to all such works to which he may assert or establish any claim under design patent or copyright laws. The Contractor for a period of three (3) years after completion of the project agrees to furnish the original or copies of all such works on the request of the Contracting Officer. 252.227-7023 Drawings and Other Data to become Property of Government MAR 1979 All designs, drawings, specifications, notes and other works developed in the performance of this contract shall become the sole property of the Government and may be used on any other design or construction without additional compensation to the Contractor. [The term "Government" above refers to the US Government.]

F i na l

Ghana Liquid Natural Gas Studies and Design

Screening Report

Prepared for

U.S. Army Corps of Engineers, Europe District U.S. ARMY CORPS OF ENGINEERS, EUROPE CONTRACT NUMBER: W912GB-12-D-0020, Order 0004

In Association with

The Millennium Challenge Corporation

March 2014

Englewood, CO

Contents Acronyms and Abbreviations ................................................................................................................. VII

1 Introduction ............................................................................................................................. 1-1 1.1 Scope ...................................................................................................................................... 1-1 1.2 Proposed Project .................................................................................................................... 1-1 1.3 Assignment Objectives ........................................................................................................... 1-2 1.4 Structure of this Report ......................................................................................................... 1-2

2 Gas Supply and Demand in Ghana ............................................................................................. 2-1 2.1 Introduction ........................................................................................................................... 2-1 2.2 Gas Infrastructure in Ghana ................................................................................................... 2-1

2.2.1 Existing Facilities ....................................................................................................... 2-1 2.2.2 Facilities Under Construction .................................................................................... 2-2 2.2.3 Proposed Facilities .................................................................................................... 2-2 2.2.4 Capacity of Existing Infrastructure ............................................................................ 2-3

2.3 Gas Supply and Demand Forecasts ........................................................................................ 2-3

3 Overview of Port and Marine Facilities ...................................................................................... 3-1 3.1.1 Existing Facilities ....................................................................................................... 3-1 3.1.2 Proposed Facilities .................................................................................................... 3-1

4 Sites under Consideration ......................................................................................................... 4-1 4.1 Domunli .................................................................................................................................. 4-1

4.1.1 Site Description ......................................................................................................... 4-1 4.1.2 Proposed Concept ..................................................................................................... 4-1

4.2 Atuabo.................................................................................................................................... 4-2 4.2.1 Site Description ......................................................................................................... 4-2 4.2.2 Proposed Concept ..................................................................................................... 4-2

4.3 Esiama .................................................................................................................................... 4-2 4.3.1 Site Description ......................................................................................................... 4-2 4.3.2 Proposed Concept ..................................................................................................... 4-2

4.4 Takoradi ................................................................................................................................. 4-3 4.4.1 Site Description ......................................................................................................... 4-3 4.4.2 Proposed Concept ..................................................................................................... 4-3

4.5 Sekondi................................................................................................................................... 4-4 4.5.1 Site Description ......................................................................................................... 4-4 4.5.2 Proposed Concept ..................................................................................................... 4-4

4.6 Aboadze ................................................................................................................................. 4-4 4.6.1 Site Description ......................................................................................................... 4-4 4.6.2 Proposed Concept ..................................................................................................... 4-5

4.7 Tema ...................................................................................................................................... 4-5 4.7.1 Site Description ......................................................................................................... 4-5 4.7.2 Proposed Concept ..................................................................................................... 4-5

4.8 Summary of Options .............................................................................................................. 4-5

5 Metocean Conditions ................................................................................................................ 5-1 5.1 Introduction ........................................................................................................................... 5-1 5.2 Available Metocean Data Sources ......................................................................................... 5-1

5.2.1 NOAA WWIII Wind and Wave Hindcast .................................................................... 5-1

ES020414102958WDC III COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

CONTENTS

5.2.2 Other Data Sources ................................................................................................... 5-3 5.3 Water Levels ........................................................................................................................... 5-4

5.3.1 Tides .......................................................................................................................... 5-4 5.3.2 Surge .......................................................................................................................... 5-4 5.3.3 Sea Level Rise ............................................................................................................ 5-4

5.4 Wind ....................................................................................................................................... 5-4 5.5 Waves ..................................................................................................................................... 5-8 5.6 Currents ................................................................................................................................ 5-13 5.7 Preliminary Conclusions for Metocean Conditions .............................................................. 5-14

6 Marine Facilities ....................................................................................................................... 6-1 6.1 Floating Storage and Regasification Unit ............................................................................... 6-1 6.2 Fixed Berth with Breakwater .................................................................................................. 6-3 6.3 Offshore Mooring ................................................................................................................... 6-3

6.3.1 Types of Moorings ..................................................................................................... 6-3 6.3.2 Environmental Forces ................................................................................................ 6-4 6.3.3 Transfer of High-Pressure Gas to Shore .................................................................... 6-4 6.3.4 Mooring an LNG Tanker to an FSRU .......................................................................... 6-7 6.3.5 Navigational Safety of the LNG Tanker ..................................................................... 6-8 6.3.6 Possible Offshore Mooring Concepts ........................................................................ 6-8

7 Considerations for Conceptual Design ....................................................................................... 7-1 7.1 Introduction ............................................................................................................................ 7-1 7.2 Design Life .............................................................................................................................. 7-1 7.3 FSRU Characteristics ............................................................................................................... 7-1 7.4 LNG Tanker Size ...................................................................................................................... 7-2 7.5 Water Depth Requirements ................................................................................................... 7-2

7.5.1 Fixed Sheltered Berth ................................................................................................ 7-2 7.5.2 Offshore Mooring ...................................................................................................... 7-3

7.6 Exclusion Zones ...................................................................................................................... 7-3 7.7 Operational Limits .................................................................................................................. 7-3 7.8 Vessel Calling Frequency ........................................................................................................ 7-4 7.9 Loading and Unloading Operations ........................................................................................ 7-4 7.10 Tugs and Other Support Services ........................................................................................... 7-4

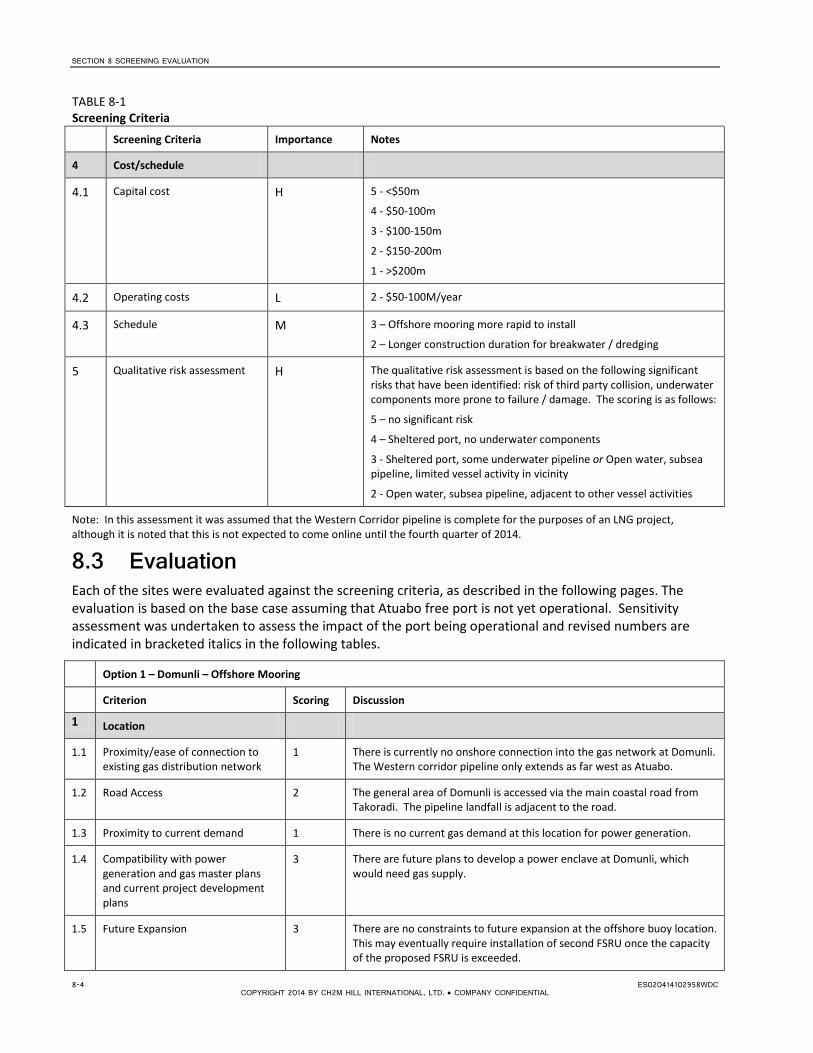

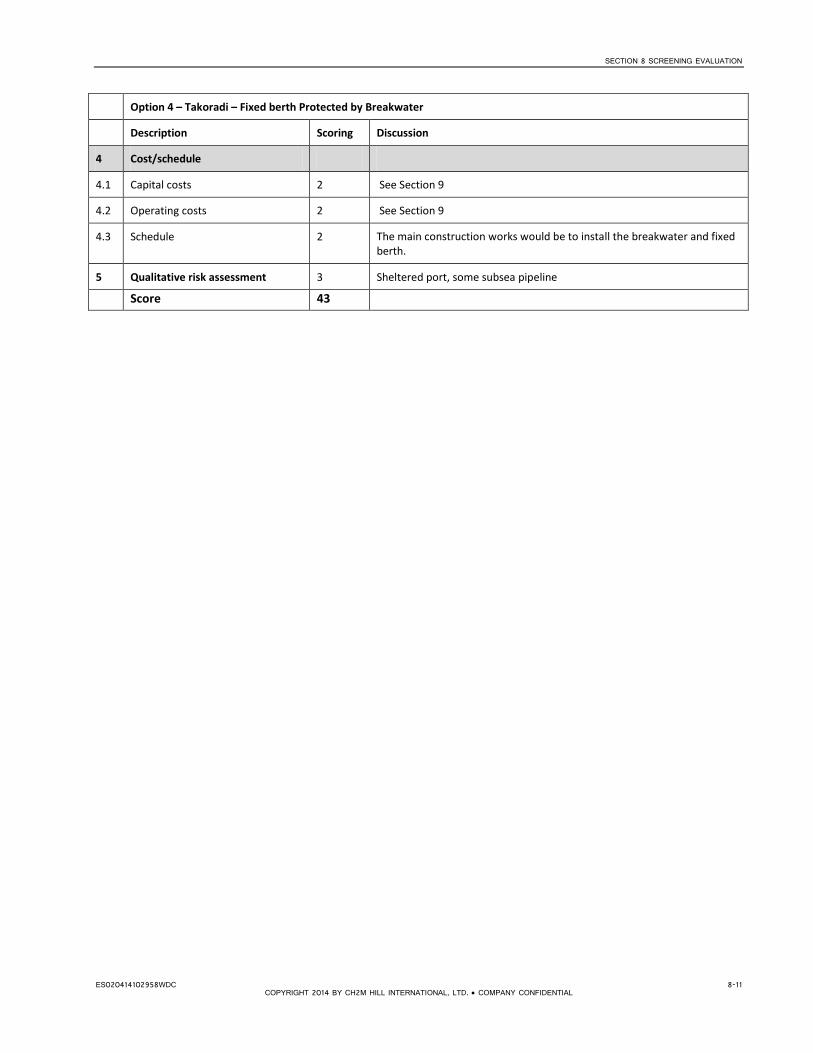

8 Screening Evaluation ................................................................................................................. 8-1 8.1 Screening Criteria ................................................................................................................... 8-1 8.2 Basis of Scoring/Weighting ..................................................................................................... 8-1 8.3 Evaluation ............................................................................................................................... 8-4 8.4 Screening Results.................................................................................................................. 8-14

9 Cost Estimate ............................................................................................................................ 9-1 9.1 Estimate Classification and Methodology .............................................................................. 9-1 9.2 Basis of Estimate .................................................................................................................... 9-2

9.2.1 Basis Documents ....................................................................................................... 9-2 9.2.2 Key Assumptions ....................................................................................................... 9-2 9.2.3 Estimate Methodology .............................................................................................. 9-2 9.2.4 Scope of Work ........................................................................................................... 9-2 9.2.5 Exclusions .................................................................................................................. 9-3 9.2.6 Allowances and Unit Cost Basis ................................................................................. 9-3 9.2.7 Project Delivery Schedule and Methodology ............................................................ 9-4 9.2.8 Labor, Materials, Subcontracts and Other Direct Costs ............................................ 9-4

IV ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

CONTENTS

9.2.9 Markups, Taxes and Other Indirect Costs ................................................................. 9-4 9.2.10 Market Conditions .................................................................................................... 9-5 9.2.11 Escalation Costs ........................................................................................................ 9-5 9.2.12 Cost Resources .......................................................................................................... 9-5 9.2.13 Estimate Validity ....................................................................................................... 9-6 9.2.14 Disclaimer ................................................................................................................. 9-6

9.3 Capital Cost Estimate ............................................................................................................. 9-6 9.4 Operational Cost Estimate ..................................................................................................... 9-6

10 Environmental and Social Review ............................................................................................ 10-1 10.1 Overview .............................................................................................................................. 10-1 10.2 Offshore Impacts ................................................................................................................. 10-1

10.2.1 Dredging and Trenching Impacts to Benthic Habitat and Water Quality ............... 10-1 10.2.2 Operational Impacts to Marine Water Quality ....................................................... 10-1 10.2.3 Loss of Marine Biodiversity ..................................................................................... 10-2 10.2.4 Impacts to Marine Mammals .................................................................................. 10-2 10.2.5 Impacts to Turtle Nesting Beach Sites .................................................................... 10-2 10.2.6 Impacts to Other Protected Marine Species .......................................................... 10-2

10.3 Onshore Impacts .................................................................................................................. 10-3 10.3.1 Noise and Air Emissions .......................................................................................... 10-3 10.3.2 Shoreline Impacts ................................................................................................... 10-3 10.3.3 Impacts to Onshore Water Quality ......................................................................... 10-3 10.3.4 Impacts to Sensitive Habitats ................................................................................. 10-3 10.3.5 Impacts to Legally Protected and Internationally Recognized Areas ..................... 10-4 10.3.6 Impacts to Onshore Aquatic, Wetland or Terrestrial Biodiversity.......................... 10-4 10.3.7 Disturbance or Loss of Other Protected Onshore Species...................................... 10-4

10.4 Socioeconomic impacts ....................................................................................................... 10-4 10.4.1 Impacts to Cultural Heritage, Resources and Sacred Groves ................................. 10-4 10.4.2 Explosion or Fire Hazard to Communities .............................................................. 10-4 10.4.3 Noise, Dust, Traffic, Debris and Safety ................................................................... 10-5 10.4.4 Resettlement: Physical Displacement .................................................................... 10-5 10.4.5 Economic Displacement .......................................................................................... 10-5 10.4.6 Reduction in Artisanal Fishing Access ..................................................................... 10-5

11 Conclusions and Recommendations......................................................................................... 11-1 11.1 Situation Assessment ........................................................................................................... 11-1 11.2 Project Screening ................................................................................................................. 11-1 11.3 Indicative Costs .................................................................................................................... 11-2 11.4 Environmental and Social Review ........................................................................................ 11-2 11.5 Recommendations ............................................................................................................... 11-2

12 References .............................................................................................................................. 12-1

Appendixes

A Ghana Gas Market and LNG Market Study B Metocean Data Tables C Option Sketches D Environmental and Social Review

Tables

2-1 Existing Gas-fired Power Plants in Ghana ........................................................................................... 2-1

ES020414102958WDC V COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

CONTENTS

2-2 LNG Demand under Different Scenarios for Selected Years ............................................................... 2-3

4-1 Summary of Sites and Mooring Options Considered .......................................................................... 4-6

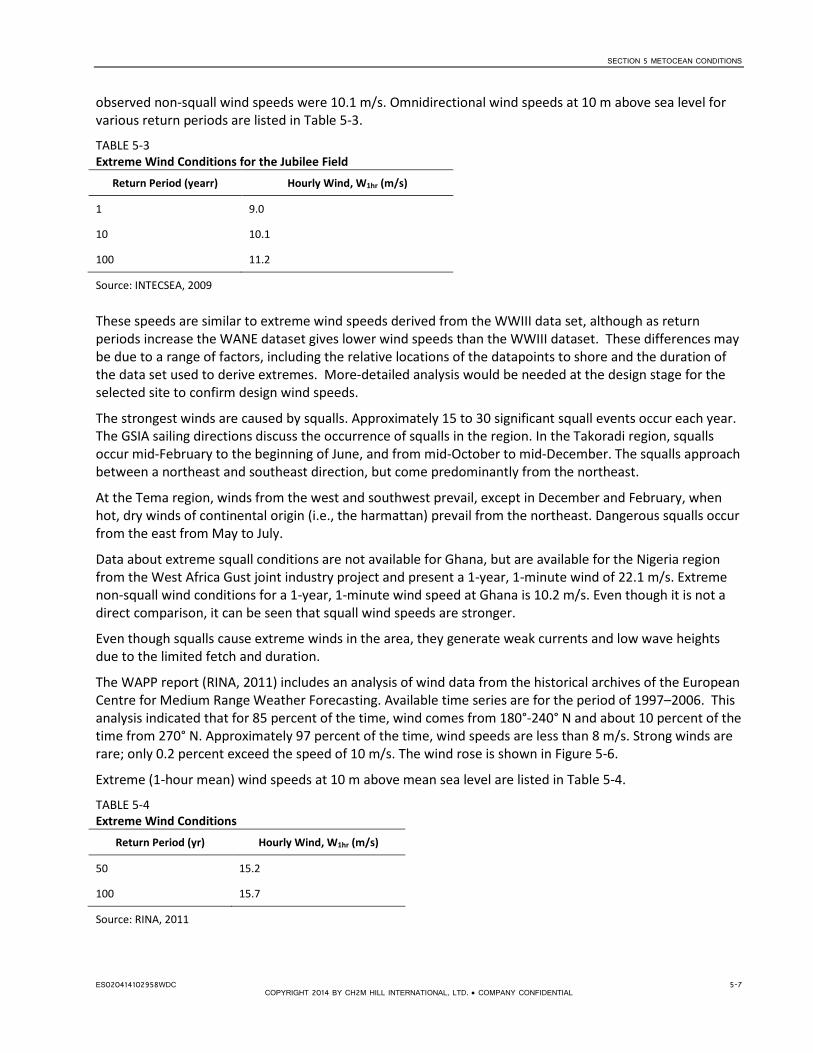

5-1 Tidal Levels at Takoradi and Tema Ports ............................................................................................. 5-4 5-2 Estimated Wind Speed Extremes ........................................................................................................ 5-6 5-3 Extreme Wind Conditions for the Jubilee Field ................................................................................... 5-7 5-4 Extreme Wind Conditions .................................................................................................................... 5-7 5-5 EVA Estimated Extreme Significant Wave Heights ............................................................................ 5-10 5-6 Percentage Exceedance for a Range of Wave Height Thresholds ..................................................... 5-11 5-7 Offshore Directional Waves from WANE Data .................................................................................. 5-11 5-8 1-year Return Period Directional Currents ........................................................................................ 5-14 5-9 Metocean Conditions at WWIII Data Points...................................................................................... 5-14

6-1 Inventory of FSRUs .............................................................................................................................. 6-2

7-1 FSRU Typical Characteristics ................................................................................................................ 7-1 7-2 Typical LNG Tanker Characteristics ..................................................................................................... 7-2

8-1 Screening Criteria ................................................................................................................................ 8-2 8-2 Screening Results ............................................................................................................................... 8-15

9-1 AACE Cost Estimate Classes ................................................................................................................. 9-1 9-2 Capital Cost Estimate ........................................................................................................................... 9-6 9-3 Operational Cost Estimate................................................................................................................... 9-7 Figures

2-1 Gas Supply and Demand Forecast, Base Case Estimate (MMscfd) ..................................................... 2-4 2-2 Gas Supply and Demand Forecast, Base Case Estimate, Western Region (MMscfd) ......................... 2-5 2-3 Gas Supply and Demand Forecast, Base Case Estimate, Tema (MMscfd) .......................................... 2-5

3-1 Atuabo Free Port ................................................................................................................................. 3-2

4-1 Sites Considered in Screening Study ................................................................................................... 4-1

5-1 Available Data from WWIII Hindcast Data for the Area of Interest .................................................... 5-2 5-2 Wind Rose Plots of WWIII data ........................................................................................................... 5-4 5-3 Exceedance Probability versus Wind Speed for Point N4.5, W2.5 ...................................................... 5-5 5-4 Exceedance Probability versus Wind Speed for Point N4.5, W1.5 ...................................................... 5-5 5-5 Exceedance Probability versus Wind Speed for Point N5, W0 ............................................................ 5-6 5-6 Wind Rose ............................................................................................................................................ 5-8 5-7 Wave Rose Plots from NOAA Data ...................................................................................................... 5-8 5-8 Exceedance Probability versus the Significant Wave Height for Point N4.5, W2.5 ............................ 5-9 5-9 Exceedance Probability versus the Significant Wave Height for Point N4.5, W1.5 ............................ 5-9 5-10 Exceedance Probability versus the Significant Wave Height for Point N5, W0 ................................ 5-10 5-11 Offshore Swell Wave Rose ................................................................................................................ 5-12 5-12 Offshore Wind-sea Wave Rose .......................................................................................................... 5-13

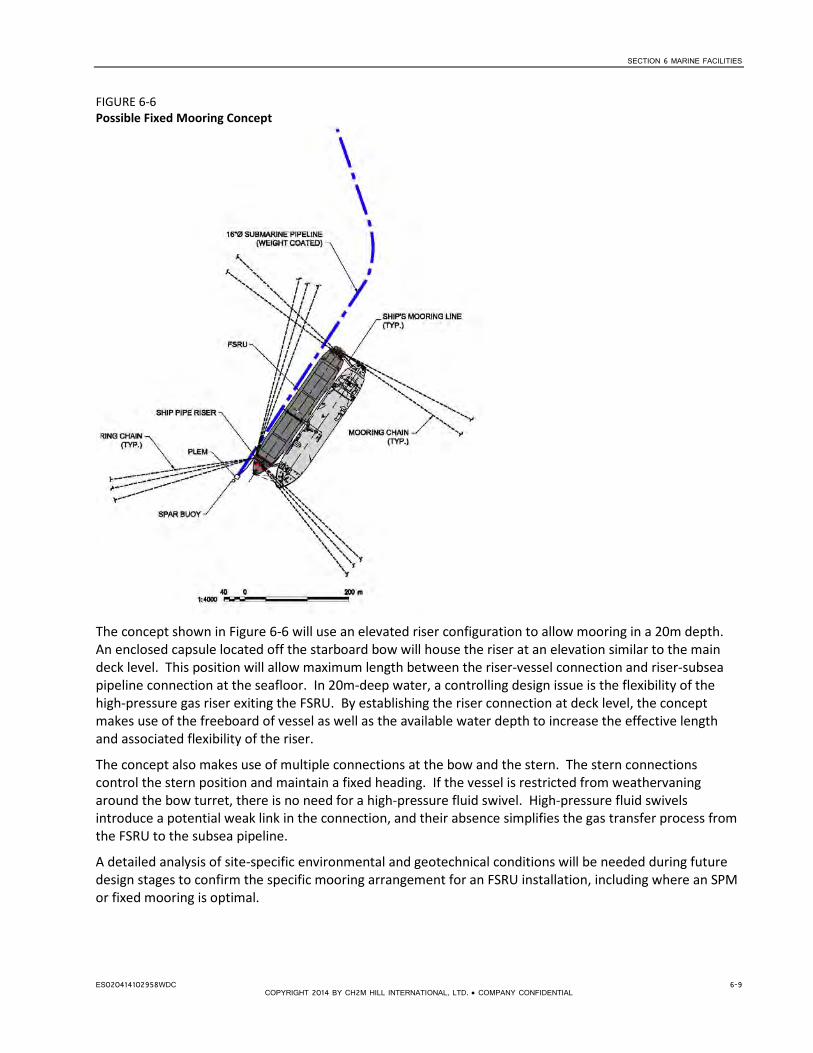

6-1 FSU in Covenas .................................................................................................................................... 6-5 6-2 Sanha FPSO in Angola .......................................................................................................................... 6-5 6-3 FPSO with SPM Turret Mooring .......................................................................................................... 6-6 6-4 STL System ........................................................................................................................................... 6-6 6-5 Fixed Moored FPSO Offshore of Brazil ................................................................................................ 6-7 6-6 Possible Fixed Mooring Concept ......................................................................................................... 6-9

VI ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

Acronyms and Abbreviations AIS Atuabo Initial Station

BLV block valve station

EVA extreme value analysis

FEED Front End Engineering Design FPSO Floating Production Storage and Offload FSRU Floating Storage and Regasification Unit FSI Floating Storage Units

GNGC Ghana National Gas Company GoG Government of Ghana GSIA (National) Geospatial-Intelligence Agency (U.S.)

Hm0 (m) significant wave height Hs significant wave height

IFC International Finance Corporation IPP independent power producer

km kilometer(s) kW kilowatt(s)

LNG liquefied natural gas

m meter(s) m3 cubic meter(s) m/s meter(s) per second MCC Millennium Challenge Corporation MMscfd million standard cubic feet per day MW megawatts

NOAA National Oceanic and Atmospheric Administration (U.S.)

OWI Oceanweather, Inc.

R&M regulation and metering

s second(s) SPM single-point mooring STL submerged turret loading

USACE U.S. Army Corps of Engineers

VRA Volta River Authority

WAGP West African Gas Pipeline WANE West Africa Normals and Extremes WAPP West African Power Pool WWIII WaveWatch III

ES020414102958WDC VII COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

Executive Summary As part of a grant to be provided to the Government of Ghana (GoG) under the authority of Section 609(g) of the Millennium Challenge Act of 2003, the Millennium Challenge Corporation (MCC) engaged U.S. Army Corps of Engineers (USACE)/CH2M HILL, on behalf of GoG, to undertake screening, feasibility, and engineering studies for the introduction of liquefied natural gas (LNG) to Ghana.

A three-phased program of study is planned including screening, feasibility, and Front End Engineering Design (FEED) and preparation of procurement documentation leading to an Engineering, Procurement, Construction, and Commissioning (EPCC) contract for the full scope of the works.

This report documents the Phase I screening studies that focused on the screening for site selection and mode of delivery for re-gasified natural gas from a floating storage and regasification unit (FSRU) to Ghana’s natural gas pipeline network.

The scope of the Phase I studies was as follows:

• Task 1 – Situation Assessment. Evaluation of the Ghana gas supply and LNG markets in order to establish some baseline conditions and key performance indicators for the project.

• Task 2 – Project Screening. Screening of alternative sites for an LNG import facility, taking into account key technical issues, potential environmental and social risks and impacts, and operational and cost considerations.

• Task 3 – Development of Indicative Costs. Development of Level 5 cost estimate for both capital investment and operational costs.

• Task 4 – Environmental and Social Review. Environmental and social review to characterize existing site conditions and identify potential environmental and social risks based on MCC environmental guidelines, which take into account International Finance Corporation (IFC) performance standards and applicable Ghanaian regulatory requirements.

• Screening Report. Preparation of this report documenting the methodology and results of the screening analysis and presenting recommendations for the preferred option for LNG import.

Situation Assessment • An evaluation of gas infrastructure in Ghana was undertaken, including an assessment of supply and

demand.

• Current gas demand is primarily for power generation and is focused around power plants at Aboadze and Tema. Industrial demand is also concentrated in these areas. Future power generation plans include expansion and new projects at these sites and also new projects at Atuabo, Esiama and Domunli.

• The current gas supply to Ghana is via the West African Gas Pipeline (WAGP). The contracted volume is 120 MMscfd, but this has not been achieved to date with average volumes closer to 60 MMscfd. The shortfall in fuel for power generation is made up by import of light crude oil via SPMs located at Aboadze and Tema.

• There has been significant investment in the Western Corridor infrastructure project which will import gas from the Jubilee field via a subsea pipeline at Atuabo to a gas processing plant. Natural gas will then be transported via pipeline to the power plants at Aboadze. This project is not yet operational and first gas for power generation is currently estimated to be available in the fourth quarter of 2014. Other offshore gas reserves have been identified and these are anticipated to come on stream from 2016 onwards.

ES020414102958WDC IX COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

EXECUTIVE SUMMARY

• Supply and demand assessment has been undertaken which indicates a base case demand for additional gas of approximately 250 MMscfd out to 2025. There is considerable uncertainty associated with this estimate, primarily due to uncertainties in timing of new power plant developments and in the timing and volume of indigenous gas supplies and of volumes via the WAGP. Thus demand may be greater than this. There is also a possibility that demand could be less if power plant projects are delayed, WAGP contract volumes are delivered and indigenous supplies are greater than estimated in the base case.

Project Screening Seven sites were identified in the Scope of Work and preliminary site visits. Tema is located in the East and the other six are located in the Western Region of Ghana. The sites are as follows:

• Domunli – an undeveloped site approximately 115 km north west of Takoradi. There are future power generation and gas processing developments planned here.

• Atuabo – approximately 90 km north west of Takoradi. A gas processing plant is under construction here, fed by gas from the Jubilee offshore field. The pipeline from the Jubilee field makes landfall here and it is also the most westerly point on the Western Corridor pipeline which extends to Aboadze.

• Esiama – approximately 70 km north west of Takoradi. There is a distribution center on the Western corridor pipeline and a lateral extending north to Prestea,

• Takoradi – there is an existing port at Takoradi

• Sekondi – site of an existing naval facility

• Aboadze – site of the Takoradi power plants T1, T2 and T3, the most easterly point on the Western Corridor pipeline and also the most westerly point on the West African Gas Pipeline, delivering gas from Nigeria. Projects are currently underway to increase generation capacity at this location and further power generation plants are also being considered.

• Tema – site of numerous power plants, some of which have future expansion plans. A lateral from the West African Gas Pipeline makes landfall here.

The proposed LNG facility will make use of an FSRU. This offers a number of benefits over a land-based regasification facility, including lower capital cost and speed of implementation. Two alternative concepts for the associated marine facilities have been considered:

• A conventional fixed berth adjacent to an existing port facility. This would require construction of a breakwater for protection and a jetty against which the FSRU would be permanently moored.

• An offshore mooring, to be either a single point mooring or a fixed multi-point mooring.

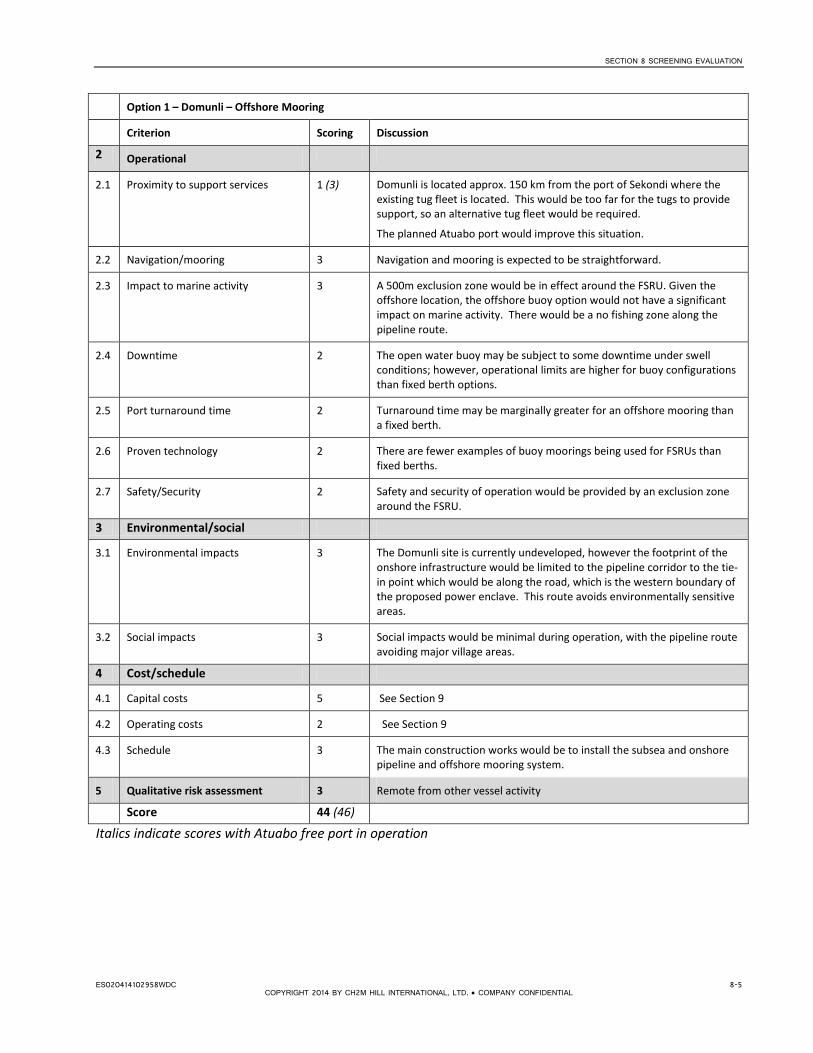

Fixed berth options were considered for Sekondi and Takoradi. All other options considered offshore moorings.

A screening evaluation of the sites was undertaken. Screening criteria were selected that addressed location, operations, social and environmental impacts and cost. The criteria included assessment of proximity to gas demand and to supporting infrastructure for transport of gas and marine operations.

Indicative Costs Preliminary cost estimates indicate that capital costs for the offshore mooring are in the order of $30-40M, whereas fixed breakwater / breakwater options are in the region of US$195-270M.

X ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

EXECUTIVE SUMMARY

Environmental and Social Review Potential environmental and social issues were evaluated for each of the seven sites. Both offshore and onshore environmental and social impacts associated with the construction and operation of the berthing facilities, FSRU, and offshore and onshore pipelines were evaluated based on existing baseline information and the project descriptions for each site option.

The five site options with offshore moorings were found to have similar environmental impacts with the single most important issue being the impacts associated with the chilled water discharge from the regasification process. The full impact of the chilled water discharge is expected to be fairly localized around the FSRU, the full extent of which will be determined through thermal plume modeling conducted as part of Phase II. The two sites utilizing fixed berth technology, Takoradi and Sekondi were found to have greater environmental impacts because of their location near to the shoreline and sensitive habitats. The sites utilizing the fixed berth technology are expected to have somewhat greater impacts associated with their discharge of chilled water into shallower waters near shore.

Socioeconomic impacts associated with construction and operation of the sites with offshore moorings will all be minimal because of the distance between the mooring sites and the coastline and because construction activities, including the housing of workers, will be done for ships and floating work platforms. The two sites utilizing fixed berth technology will have additional socioeconomic impacts because of the need for quarrying and transportation of rock for construction of the breakwaters and housing of construction workers on shore within the existing population. All site options will require an exclusion zone around the FSRU that will have a small impact on artisanal fishing. The onshore natural gas pipelines associated with the various site options have differing lengths and different impact levels depending upon the characteristics of the areas crossed. In general, socioeconomic impacts associated with the offshore mooring options were found to be less than those associated with the fixed berth options because of the length of the onshore pipelines and density of residential and commercial development in the Takoradi and Sekondi areas.

Conclusions Screening identified Aboadze as the preferred site for the FSRU, primarily due to the proximity to current and future gas demand and to the Western Corridor pipeline. The sites of Tema, Atuabo and Esiama also scored highly and present viable options for location of the facility. Domunli scored lower due to the lack of current demand and infrastructure at this location.

From a marine operations perspective those options located furthest from the established ports of Tema, Sekondi and Takoradi present the greatest challenges in terms of accessibility to support services including tugs and workboats. This could change if the plans to develop a new port at Atuabo are executed and it is available at the time the FSRU facility goes into operation. The offshore mooring options scored more favorably than the fixed berth options due to cost and also because the options at Takoradi and Sekondi present challenges in terms of the onshore connection to the gas distribution network.

ES020414102958WDC XI COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 1

Introduction

1.1 Scope As part of a grant to be provided to the Government of Ghana (GoG) under the authority of Section 609(g) of the Millennium Challenge Act of 2003, the Millennium Challenge Corporation (MCC) engaged U.S. Army Corps of Engineers (USACE)/CH2M HILL, on behalf of GoG, to undertake screening, feasibility, and engineering studies for the introduction of liquefied natural gas (LNG) to Ghana.

A phased program of study is planned as follows:

1. Phase I: Screening for site selection and mode of delivery for regasified natural gas from a Floating Storage and Regasification Unit (FSRU) to Ghana’s natural gas pipeline network

2. Phase II: Feasibility study of selected options and related environmental, social, and economic studies

3. Phase III: Front End Engineering Design (FEED) and preparation of procurement documentation leading to an Engineering, Procurement, Construction, and Commissioning (EPCC) contract for the full scope of the works

This report documents the Phase I studies. The scope of the Phase I studies was as follows:

• Task 1 – Situation Assessment. Evaluation of the Ghana gas supply and LNG markets in order to establish some baseline conditions and key performance indicators for the project.

• Task 2 – Project Screening. Screening of alternative sites for an LNG import facility, taking into account key technical issues, potential environmental and social risks and impacts, and operational and cost considerations.

• Task 3 – Development of Indicative Costs. Development of Level 5 cost estimate for both capital investment and operational costs for two recommended options.

• Task 4 – Environmental and Social Review. Environmental and social review to characterize existing site conditions and identify potential environmental and social risks based on MCC environmental guidelines, which take into account International Finance Corporation (IFC) performance standards and applicable Ghanaian regulatory requirements.

• Screening Report. Preparation of this report documenting the methodology and results of the screening analysis and presenting recommendations for the preferred option for LNG import.

Currently, only Phase I has been authorized. Factors that will influence MCC’s decision to take up all three phases of study and design include the results of Phase I and further consultation with GoG. In addition, the current situation in the power sector in Ghana is very dynamic; governmental entities, donors and private companies are sponsoring various studies and projects. A decision to proceed will depend on coordination among numerous stakeholders, the timing of award and completion of other studies, and reaching mutual agreement about who will take lead responsibility for delivery of certain power sector activities and supporting studies.

The studies reported in this document have been undertaken by CH2M Hill with input from Gas Strategies on the situation assessment and ESL on the environmental and social review.

1.2 Proposed Project The proposed LNG project consists of a number of activities. These include purchasing and delivering LNG on behalf of end users, procuring or leasing an FSRU to store and regasify LNG for transport to end users in ES020414102958WDC 1-1

COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 1 INTRODUCTION

Ghana, procuring and installing offshore and onshore infrastructure connecting the FSRU to Ghana’s existing network of natural gas pipelines, and assessing any impact on the downstream pipeline network.

1.3 Assignment Objectives The overall objective of the work (Phases I to III) will be to recommend the most appropriate technical option, to establish the costs and schedule of the development, and define the basis for Engineering, Procurement, Construction and Commissioning contracts to develop and build the necessary LNG infrastructure facilities. In parallel with the technical work being done by CH2M HILL, other consultants to the GoG, MCC, and USACE are addressing other aspects of the LNG project such as:

• Reviewing and verifying/validating natural gas supply and demand

• Conducting a legal and commercial review to identify any barriers to project implementation and a project structure involving private sector participation

• Structuring and establishing a special purpose company or companies for purchasing LNG, leasing or owning and operating an FSRU, owning and operating the infrastructure for transporting regasified natural gas from the FSRU to Ghana’s network of natural gas pipelines (West African Gas Pipeline (WAGP), Ghana’s on-shore network)

• Developing an LNG purchasing strategy

• Establishing a credit-worthy natural gas off-taker

• Addressing project financing and other implementation considerations

The studies that CH2M HILL will produce (during Phases I to III), as well as the additional studies by the GoG and the US Government will:

• Select a site for location of the FSRU and method of interconnection with Ghana’s natural gas pipeline network

• Develop a project design

• Develop cost estimates for the project

• Perform economic and financial analyses

• Perform environmental and social impact assessment, including resettlement screening

• Evaluate the project’s social and gender impacts

• Develop a technical bid package for turnkey implementation of the project, as may be defined.

1.4 Structure of this Report Following this introductory section, this report is structured as follows:

Section 2 gives an overview of existing and proposed gas infrastructure in Ghana that might influence the siting of an LNG facility. It also gives an overview of the supply and demand analysis undertaken by Gas Strategies and presented in more detail in Appendix A. Appendix A also gives an overview of the LNG market. Section 3 summarizes existing marine facilities in Ghana.

Section 4 discusses the sites that have been considered for the FSRU facility and describes the selected option at each site that has been considered in the screening. Sketches showing the conceptual layouts are presented in Appendix C.

1-2 ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 1 INTRODUCTION

The metocean conditions that might affect the design and operation of an FSRU are summarized in Section 5. Section 6 describes in more detail the types of marine facilities that are considered. Other design considerations are covered in Section 7.

The screening evaluation methodology and results are presented in Section 8. Preliminary cost estimates are presented in Section 9. A summary of the environmental and social review that was undertaken is presented in Section 10, supported by a more detailed environmental and social review in Appendix D. Conclusions are recommendations for future works stages are given in Section 11.

ES020414102958WDC 1-3 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 2

Gas Supply and Demand in Ghana

2.1 Introduction Certain aspects of the situation assessment were undertaken as part of the Phase I LNG screening study scope of work. Specifically, this work included the following tasks:

• Ghana Fuel Supply. Review of fuel supply options for thermal power generation in Ghana, encompassing the gas supply infrastructure in Ghana, including the West African Gas Pipeline (WAGP), arrangements and contracts with WAGP, the Jubilee, Sankofa and TEN fields and any implications there may be for new LNG project development. The assessment examined the current state of existing processing facilities, pipelines, and related infrastructure and future development plans.

• Gas Demand. Assessment of future power generation plant proposals and the likely gas demand for power generation. Assessment of future non-power demand.

• LNG Markets. Appraisal of the international market for LNG: the value chain, including liquefaction plants, vessels, and receiving regasification terminals, both shore-side and floating; sources of supply, size of market, and the main participants; recent developments and outlook; and typical size of projects. Gas specifications that are normal for LNG projects: limits on impurities content and minimum acceptable calorific value.

This work was undertaken by Gas Strategies and is included in a standalone report provided as Appendix A to this report.

This section of the report provides a summary of the gas supply and demand assessment undertaken by Gas Strategies, as well as an overview of the key infrastructure with Ghana that influences that supply and demand, and future plans because these are all key factors that influence the screening assessment.

2.2 Gas Infrastructure in Ghana A detailed review of gas supply infrastructure is presented in Section 3 of the Gas Strategies report in Appendix A. The key components are summarized here, focusing on how they may influence the siting of an LNG facility.

2.2.1 Existing Facilities The primary means of gas supply to Ghana is currently via the WAGP, which makes landfall at Tema and Aboadze. It is contracted to supply 120 million standard cubic feet per day (MMscfd), but actual volumes delivered have been around 60MMscfd, dropping to 30 MMscfd in January 2014.

Most of Ghana’s gas supply is used for power generation. There are currently two main centers of thermal power generation—at Tema and Aboadze—where multiple power plants are located. The details of the power plants at these locations are summarized in Table 2-1.

TABLE 2-1 Existing Gas-fired Power Plants in Ghana

Tema Capacity

Volta River Authority (VRA) Tema Thermal 1 110

VRA Tema Thermal 2 49.5

Mines Reserve Plant 80

ES020414102958WDC 2-1 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 2 GAS SUPPLY AND DEMAND IN GHANA

TABLE 2-1 Existing Gas-fired Power Plants in Ghana

Tema Capacity

Sunon Asogli* 200

Cenit power plant 110

Total 549.5 megawatts (MW)

Aboadze Capacity

Takoradi Thermal (TAPCo) 330

Takoradi Thermal (TICo) T2** 220

Takoradi Thermal 3 132

Total 682 MW

Source: Gas Strategies

*Gas-fired only; all others are also fueled by light crude oil.

** Currently under expansion to 330MW

2.2.2 Facilities Under Construction The Western Corridor project will provide key gas infrastructure to western Ghana. It will be undertaken in two phases. Phase 1 is currently under construction and comprises the following key components:

• A 12-inch-diameter, 45-kilometer (km) offshore pipeline from the Jubilee field to Atuabo, where the pipeline comes ashore

• A gas processing plant at Atuabo, which processes the gas from the Jubilee field, with an initial capacity of 150 MMscfd

• A 20–inch-diameter, 100km onshore gas pipeline from the gas processing plant at Atuabo to Aboadze, with a capacity of 400 MMscfd. This pipeline will transport natural gas to the Takoradi power plants at Aboadze.

• Atuabo Initial Station - (AIS) located at the gas processing plant

• Esiama Distribution Station - north of Esiama and the start of the branch line, distributing gas to Prestea

• Takoradi Metering and Regulating Station - north of the Takoradi thermal power plant at Aboadze, in the vicinity of the existing WAGP Company regulating and metering stations. This will be the custody metering facility for the onshore pipeline from Atuabo to Takoradi.

• Block Valve Stations (BLVs) – these are minimum facilities to provide pipeline isolation. They are located 55km (BLV1) and 87km (BLV2) from the AIS at Atuabo.

Current indications (February 2014) are that first gas will flow via this system to Aboadze in the fourth quarter of 2014.

2.2.3 Proposed Facilities There are numerous plans for future power generation, including proposals for the existing power generation sites at Takoradi and Tema, as well as at Domunli, Atuabo, Esiama and Prestea. Projects have been proposed by the GoG and by independent power producers (IPPs). Numerous projects have been granted provisional licenses by the Energy Commission.

2-2 ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 2 GAS SUPPLY AND DEMAND IN GHANA

Phase 2 of the Western Corridor project would increase capacity at the Atuabo gas processing plant to 300 MMscfd. This would also include a natural gas liquids plant and export facility at Domunli and a new pipeline connecting the two sites.

2.2.4 Capacity of Existing Infrastructure A key factor for siting an LNG import facility will be ensuring that the gas and power can be readily transported to demand centers.

The Western Corridor pipeline from Atuabo to Aboadze has a capacity of 400 MMscfd. This pipeline will receive a 150 MMscfd natural gas output from the processing plant. Thus at the outset there will be spare capacity of at least 250 MMscfd in the pipeline. After the Phase 2 expansion, the plant capacity will increase to 300 MMscfd. This will leave at least 100 MMscfd spare capacity in the pipeline without the need for additional compressor capacity. The spare capacity is expected to be more than this, depending on the make-up of the supply gas and how much natural gas is output from the processing plant.

The Gas Strategies report (see Appendix A) discusses the WAGP in some detail. It notes that the pipeline has an initial capacity of 170 MMscfd and that it can be expanded over time to a capacity of 470 MMscfd, relatively easily by installing additional compressor stations. However, given the current low level of planned to be transported through the pipeline, it seems unlikely that capacity will be expanded in the near future.

It is understood that reverse flow through the pipeline is technically feasible, allowing gas to also be delivered into the western end of the pipeline (at Takoradi) for delivery to the east. It is understood that this could increase capacity to more than 600 MMscf/d by introducing reverse flow.

Generated power is evacuated via transmission lines owned by GRIDco from locations near Tema and Aboadze. It is understood that parts of this network are in the process of being upgraded. Although not part of this study, it is assumed that there will be sufficient capacity to evacuate current and future power generation.

2.3 Gas Supply and Demand Forecasts Ghana’s gas demand has been evaluated by Gas Strategies in the report presented in Appendix A. The report provides a range of estimates, but notes a high degree of uncertainty in the forecasts, based on the following key factors:

• Uncertainty in the timescale of power plant project developments • Uncertainty in supply from the WAGP • Uncertainty as to the start-up date of the Jubilee pipeline

The range of demand scenarios presented by Gas Strategies is summarized in Table 2-2.

TABLE 2-2 LNG Demand under Different Scenarios for Selected Years

Scenario

Demand from LNG (MMscfd)

2016 2020 2025

Base case supply – Base case demand (Gas Strategies 2014 demand forecast) 230 176 235

Low case supply – high case demand (Energy Commission demand forecast) 434 795 909

High case supply – low case demand (World Bank demand forecast) 139 7 -182

Source: Gas Strategies; see Appendix A. ES020414102958WDC 2-3

COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 2 GAS SUPPLY AND DEMAND IN GHANA

The base case supply and demand data from Gas Strategies is summarized in Figure 2-1. This indicates a fairly constant deficit of around 230 MMscfd, with some reduction around 2020-2022, based on the assumptions made regarding when indigenous supply comes online. There is then a steady increase as additional power generation capacity comes online.

FIGURE 2-1 Gas Supply and Demand Forecast, Base Case Estimate (MMscfd)

Data source: Gas Strategies; see Appendix A.

This can be further broken down by region, based on the regional demand data given in Appendix C of the Gas Strategies report. This is illustrated for the Western Region and Tema in Figures 2-2 and 2-3.

The figures indicate that in the longer term the bulk of the demand is in the Western region.

Assuming the domestic demand is met by the indigenous gas supply and that all WAGP gas goes to Tema, this indicates a deficit in the Western region of up to 100 MMscfd out to 2019, gradually decreasing to a small regional surplus around 2022, then increasing as more power demand comes online and yield from indigenous supplies reduces.

In the case of Tema, assuming that only 60 MMscfd is available from the WAGP, this indicates an average deficit of around 100MMscfd out to 2020, with some increase beyond that.

There is significant uncertainty around these values and the base case values used here are for illustrative purposes to show the regional split in supply and demand. In the short term, there is a fairly even split, between the two regions. The uncertainties identified above in terms of timing of the increase in generation capacity, and of indigenous supply indicate that a flexible approach that could balance shortfall between the two regions may be preferred. This would have to make use of the WAGP. Further study would be required to confirm technical feasibility and to determine if acceptable contract arrangements could be agreed with WAGP for use of the pipeline for transport.

2-4 ES020414102958WDC COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 2 GAS SUPPLY AND DEMAND IN GHANA

FIGURE 2-2 Gas Supply and Demand Forecast, Base Case Estimate, Western Region (MMscfd)

Data source: Gas Strategies; see Appendix A.

FIGURE 2-3 Gas Supply and Demand Forecast, Base Case Estimate, Tema (MMscfd)

Data source: Gas Strategies; see Appendix A.

ES020414102958WDC 2-5 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 3

Overview of Port and Marine Facilities An FSRU facility will require marine support services, including tugs, workboats, security and a berth for loading equipment on tugs and workboats. This section discusses port and marine facilities that exist or are planned in the region because these may provide support services for the FSRU facility. Specific requirements for supporting the FSRU are discussed in Section 7.10.

3.1.1 Existing Facilities Takoradi

The existing port at Takoradi handles bulk exports, including manganese, bauxite, bulk and bagged cocoa beans, and forest products. A variety of bulk and containerized products are also imported. The port is served by a rail line that delivers bulk materials to the berths. Vessels supporting offshore oil and gas exploration and production also call at the port. Channel depth at the port entrance is 11.5 meters (m). The port is protected by a rubble mound breakwater with a roadway along the crest.

The port is currently undergoing expansion with construction of a 1,100m breakwater extension, and dredging and reclamation to create additional berths.

Two 40 ton bollard pull tugs are available as standard at the port. Tugs of up to 1,250 horsepower are available by special request.

Sekondi

The port at Sekondi is a naval facility, located to the northeast of Takoradi. It has a SMIT Lamnalco tug that currently services the single-point mooring (SPM) at Aboadze. Water depths at the harbor entrance are 8 to 9 m, too shallow for LNG carriers.

Tema

Tema is the largest port in Ghana and receives container vessels, general cargo vessels, tankers, Ro-Ro, and cruise vessels, amongst many others. The port has a dry dock facility. The port authority operates four tugs: two of 1,866 kilowatts (kW), one of 1,860 kW, and one of 1,644 kW. These tugs have a capacity of 20-25t bollard pull. All tugs are fitted with pumps and monitors for fire-fighting.

The port is currently dredged to a water depth of 12.5m. Expansion plans indicate deepening to 16m to accommodate larger-draft vessels.

3.1.2 Proposed Facilities Atuabo Free Port

There is a proposal by LonRho for an Oil Services Terminal at Atuabo, to be called the Atuabo Free Port. This facility would comprise the following:

• Harbor, turning basin, and access channel – The harbor is protected by breakwaters. The turning basin and access channel would be dredged to provide sufficient water depth for vessels that would use the facility.

• Sheltered Waiting Area – Temporary anchorage for vessels and rigs within the harbor, with a water depth of 12.5m.

ES020414102958WDC 3-1 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 3 OVERVIEW OF PORT AND MARINE FACILITIES

• A number of quays to allow vessels to berth, and load and unload personnel and cargo. This would

include a naval logistics base and berths as follows:

− Berth 1: Marine offshore supply base (300m length)

− Berth 2: Storage and supply of liquid bulk products (200m length)

− Berth 3: Rig repair facilities (400m length)

− Multi-purpose vessel berth (200m length)

− 50m pier for mooring of various service vessels in a water depth of 6m. This would provide berths for seven general service vessels, including tugs, pilot vessels and a mooring launch.

This facility could potentially provide a tug support facility for an FSRU located at the sites under consideration west of Takoradi.

The project was given parliamentary approval to proceed in February 2014, and indications are that work will begin in the second quarter of 2014. Timescales of 18 to 25 months are suggested for completion, indicating the facility would be operational by late 2016.

The proposed layout for the Atuabo Free Port, shown in Figure 3-1 appears to overlap with the as-constructed route of the gas pipeline from the Jubilee field, which is shown to be much closer to the adjacent village to the east. It is therefore expected that there may be some reconfiguration of the port layout to accommodate the pipeline.

FIGURE 3-1 Atuabo Free Port

Source: Ghana Oil Services Terminal, Environmental and Social Impact Assessment (ERM, 2012) 3-2 ES020414102958WDC

COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4

Sites under Consideration The sites that are have been considered as potential locations for an FSRU are indicated in Figure 4-1. Key design criteria and characteristics are summarized in Section 7.

FIGURE 4-1 Sites Considered in Screening Study

The key characteristics of each of the sites in terms of the proposed LNG facility are discussed in this section. A more-detailed environmental and social review of each site is provided in Appendix B. Sketches for each of the sites are included in Appendix C.

4.1 Domunli 4.1.1 Site Description Domunli is located approximately 37 km east of the border with Cote D’Ivoire. It is currently an undeveloped site. There are plans for power plant and gas processing plant developments to the north of this site, and a pipeline connection to the gas processing plant at Atuabo for natural gas liquids (NGLs). A 19 km2 area has been identified by Ghana National Gas Company (GNGC) as a power enclave, and VRA has plans to develop a 6 km2 area for power generation. Some site clearance work has commenced in relation to these developments. A tidal lagoon extends between the proposed power enclave area and the shoreline. Currently there is no connection into the gas pipeline network at this location.

The shoreline consists of broad sandy beaches, coconut palms, lagoons, mangroves, and other wetland and upland habitats. The immediate area is relatively undeveloped and is used primarily for artisanal fishing and coconut farming. Several small villages are located with the general area. Further detailed discussion on the site is provided in the Environmental and Social Review (Appendix D).

4.1.2 Proposed Concept The proposed concept is an offshore mooring at this location (see sketch SK-1). To minimize environmental impact, an onshore pipeline corridor is placed immediately adjacent to the roadway at the west of the site. The tie-in point would be at the future VRA/GNGC power generation sites.

ES020414102958WDC 4-1 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4 SITES UNDER CONSIDERATION

4.2 Atuabo 4.2.1 Site Description Atuabo is the site of a gas processing plant being constructed by SINOPEC contractors for GNGC. The gas processing plant will receive raw gas from the Jubilee field via a 12–inch-diameter pipeline that makes landfall at this location. The plant will produce various gas products, and natural gas will be transported via the Western Corridor pipeline to feed the Takoradi power plants at Aboadze.

The shoreline consists of a broad sandy beach with an area of coconut palms extending inland from the beach for a distance of approximately 225 m. A broad right-of-way has been cleared for the gas pipeline through the coconut palms from the shoreline to the gas processing plant. There are scattered residents and other land uses in the general area. Further detailed discussion on the site is provided in the Environmental and Social Review (Appendix D).

4.2.2 Proposed Concept An offshore mooring is considered at Atuabo (see sketch SK-2). It is assumed that the pipeline landfall would use the same corridor as the Jubilee pipeline. The pipeline would then tie in to the Western Corridor pipeline at the Atuabo Initial Station (AIS) on the downstream side of the processing plant (to the east of the plant).

The proposed FSRU would be located outside the “Area to be Avoided” around the Jubilee pipeline. The nearshore section of the pipeline would fall within this zone. Adequate distance from the existing pipeline would need to be maintained during construction.

A proposal for an oil services terminal at the Atuabo Free Port was recently approved by the GoG. This port would provide support services for an FSRU at this location, including tugs and other support facilities. The screening assessment has been undertaken assuming a base case excluding the port development. A sensitivity check has assumed the project is fully executed and in operation.

The presence of the port could make a fixed berth an option for consideration at this site, most likely by constructing a new sheltered berth outside the perimeter of the port. The harbor basin and turning circle will be dredged to -16.5mCD. The approach channel will be dredged to -17.5mCD. There would be additional complexities in the planning and integration of such a berth because the oil services terminal is not yet constructed, although there could be opportunities to optimize the design of both facilities if the projects are executed in parallel.

4.3 Esiama 4.3.1 Site Description Esiama, approximately 30 km east of Atuabo, is the location of a distribution station on the Western Corridor pipeline from Atuabo to Aboadze. It connects to a lateral line running north to Prestea and would be a possible tie-in point for gas from the FSRU. The town of Esiama lies between the shore and the GNGC pipeline, and the distribution station is approximately 1.7 km inland, to the north of the town.

The shoreline consists of a broad sandy beach with an area of coconut palms. The town of Esiama is characterized by fairly dense residential and commercial structures and covers an area of approximately 0.75 km east-to-west, with areas of palm plantation, native vegetation, and dispersed housing extending beyond either side of the town. Further detailed discussion on the site is provided in the Environmental and Social Review (Appendix D).

4.3.2 Proposed Concept An offshore mooring is proposed at Esiama (see sketch SK-3), with the offshore pipeline making landfall to the west of the town. The pipeline would follow a route to the north where it would meet the Western 4-2 ES020414102958WDC

COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4 SITES UNDER CONSIDERATION

Corridor pipeline route and run parallel to this to the east, where it would connect at the distribution station.

4.4 Takoradi 4.4.1 Site Description The existing port at Takoradi handles bulk exports, including manganese, bauxite, bulk and bagged cocoa beans, and forest products. A variety of bulk and containerized products are also imported. The port is served by a rail line that delivers bulk materials to the berths. Vessels supporting offshore oil and gas exploration and production currently also call at the port, although this may change in the future, given the recent approval of the Atuabo Free Port, which is planned to be a dedicated facility to serve this industry. Channel depth at the port entrance is 11.5m, which is too shallow for LNG vessels. Two 40-ton bollard pull tugs are available at the port.

The port is undergoing expansion and the first phase of the project has just been commissioned. Marine Contractor Jan de Nul is currently onsite undertaking the contract, which includes construction of a 1.1-km extension to the existing rubble mound breakwater, dredging, reclamation, and construction of a new 200-m section of quay wall. Rock for breakwater construction is sourced from a local quarry, Justmac, adjacent to the shore road between Takoradi and Sekondi. The dredging includes some rock removal to be undertaken with a cutter suction dredger. Future phases of port expansion are planned.

The immediate shoreline consists of port-related seawalls and rock. Beyond the port area, the coast is characterized as sandy beach habitat. The town Takoradi north of the port is characterized by a mixed land use of dense industrial, commercial, and residential areas.

4.4.2 Proposed Concept The existing port provides an opportunity to construct a conventional sheltered berth for the FSRU (see sketches SK-4a and 4b), which would be prohibitively expensive at a greenfield site, primarily due to the amount of dredging and breakwater construction required. The LNG tankers would be able to make use of the existing dredged approaches, although some deepening of the approach would be required to accommodate the LNG tankers.

The proposed berth would be on the outer face of the existing breakwater, with a new rubble mound breakwater constructed to protect the new berth. The breakwater would include a roadway to provide access to the berth. The footprint of the new breakwater would cover an area of shallow water extending eastwards from the western corner of the existing breakwater, to minimize rock volumes required for construction. Based on feedback from dredging activities as part of the port expansion project currently in progress, this concept is likely to require rock dredging. The current work at the sites is being undertaken using a cutter suction dredger, and blasting is not required, although geotechnical investigation would need to be undertaken to confirm this.

There are various challenges in terms of connecting the imported gas to demand at Takoradi. The Western Corridor pipeline runs approximately 10 miles inland, so a pipeline route would need to be established through or around the town of Takoradi. For the purposes of screening, a route has been identified that would run along the breakwater to shore, with a subsea section that would parallel the shore before making landfall to the west of the town.

There is no existing connection point to the Western Corridor pipeline at this location. There may be a need to interrupt operation of the pipeline while a connection is made, or it may be possible to hot-tap depend on the pipeline pressure. A Block Valve Station (BLV) at Kwekutsiakrom to the west of the proposed tie-in location could be used to isolate the section of pipeline to the regulation and metering (R&M) station if isolation is required.

ES020414102958WDC 4-3 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4 SITES UNDER CONSIDERATION

The section of subsea pipeline is likely to present construction challenges in the surf zone, and there may also be an impact on artisanal fishing in the area because an exclusion zone would need to be enforced.

4.5 Sekondi 4.5.1 Site Description Sekondi is a naval port located to the northeast of Takoradi port. Water depths at the harbor entrance are 8 to 9 m, too shallow for LNG carriers. A SMIT Lamnalco tug is based here (overall length 28 m) that services the SPM at Aboadze.

The immediate shoreline consists of port-related seawalls and rock. Beyond the port area, the coast is characterized as sandy beach habitat. The town of Sekondi north of the port is characterized by a mixed land use of dense industrial, commercial, and residential areas.

4.5.2 Proposed Concept Similar to the port at Takoradi, the port at Sekondi provides an opportunity to construct a conventional sheltered berth for the FSRU (see Sketches SK-5a and 5b), which would be prohibitively expensive at a greenfield site, primarily due to the amount of dredging and breakwater construction required. The LNG tankers would be able to make use of the existing dredged approaches, although some deepening of the approach would be required to accommodate the LNG tankers.

The proposed berth would be on the outer face of the existing breakwater, with a new rubble mound breakwater constructed to protect the new berth. The existing breakwater does not have a roadway, so one would need to be constructed to provide access to the berth.

Like the Takoradi site, connection to the onshore gas pipeline is challenging at this site. An indicative pipeline route has been identified that would run overland through the eastern outskirts of the town to connect with the Western Corridor pipeline. There may be a need to interrupt operation of the pipeline while a connection is made, or it may be possible to hot-tap depend on the pipeline pressure. A Block Valve Station (BLV) at Kwekutsiakrom to the west of the proposed tie-in location could be used to isolate the section of pipeline to the regulation and metering (R&M) station if isolation is required.

There are various challenges in terms of connecting the imported gas to demand at Sekondi. The Western Corridor pipeline runs approximately 10 miles inland, so a pipeline route would need to be established through or round the town of Takoradi-Sekondi. For the purposes of screening, a route has been identified that would run along the breakwater to shore, then toward the east north through the eastern outskirts of the town to connect with the Western Corridor pipeline.

The section of subsea pipeline is likely to present construction challenges in the surf zone, and there may also be an impact on artisanal fishing in the area because an exclusion zone would need to be enforced.

4.6 Aboadze 4.6.1 Site Description There are several power plants at Aboadze:

• T1 – 330MW combined cycle (owned and operated by VRA). The plant has dual fuel capacity (gas and crude oil).

• T2 – 220MW single cycle – joint venture between TAQA of Abu Dhabi (90 percent) and VRA (10 percent). This plant is currently being expanded to 330MW combined cycle. The engineering-procurement-construction contract is being carried out by a consortium of KEPCO E&C and Mitsui. The plant is fueled by gas or crude oil.

• T3 – 132MW combined cycle (gas- or diesel-fueled). 4-4 ES020414102958WDC

COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4 SITES UNDER CONSIDERATION

Another plant is proposed and is in the early stages of project development:

• T4 – 115MW combined cycle (gas- and crude oil-fueled)

Land to the west of the existing plants is available that could accommodate three to four 330MW plants. VRA is in the process of acquiring this land for joint venture or IPP projects. It is understood that there are three candidate IPPs who currently have provisional licenses from the Energy Commission.

The WAGP makes landfall at Aboadze and provides gas directly to the plants; however, supply from the pipeline currently falls below demand and was interrupted in 2012 due to damage to the pipeline, and crude oil is therefore used as a back-up fuel. This fuel is imported from an SPM located offshore of Aboadze and stored in three tanks onsite. These tanks were originally sized to support the T1 plant only and can provide about 3 weeks’ supply. Crude is currently delivered to the SPM in relatively small tankers (450,000 barrels).

The T2 power plant is being converted to once-through seawater cooling, and a submerged pipeline intake/outfall is under construction between the WAGP and the subsea pipeline from the SPM.

The shoreline consists of broad sandy beaches with mixed native vegetation and coconut palms to the north. A fairly large fishing village characterized by dense residential development is to the east of the power plant facilities. The area inland and west of the power plants is characterized by wetlands, native vegetation, and coconut palms. To the west, areas of residential and commercial development are approximately 2 km north of the coastline.

4.6.2 Proposed Concept An offshore mooring is proposed for Aboadze (See Sketch SK-06). The proposed location for the mooring is to the east of the WAGP exclusion zone and the existing SPM. The onshore pipeline would tie in to the Western Corridor R&M station approximately 1km north of the Takoradi Power Plants.

4.7 Tema 4.7.1 Site Description Tema is the most easterly of the sites being considered, located 30 km east of Accra. A lateral line from the WAGP makes landfall at Tema, east of the port, in the vicinity of a heavy industrial area where several power plants are located. An onshore metering station is a short distance inland. An 18-inch line serves a VRA power enclave at this location with various gas (and in some cases light crude oil) -fired plants located here, consisting of the Sunon Asogli plant, Cenit plant, and VRA Tema thermal power plant. An SPM is located offshore of Tema. When gas does not flow through the WAGP or when supply is deficient, crude oil imported from the SPM is used to fire the existing power plants, with the exception of Sunon Asogli plant, which is gas-fired only. Land available for expansion of the power generation enclave is limited, and evacuation of power is reportedly an issue here with the system at capacity.

The shoreline is characterized as a mixture of sandy and rocky habitats. The upland area along the coast contains a mixture of native vegetation mixed and small agricultural plots. Industrial, power generation, and residential land uses are present in the general area.

4.7.2 Proposed Concept The option proposed at Tema is an offshore mooring that would be located between the WAGP exclusion zone and the SPM. The onshore connection would be at the WAGP metering station.

4.8 Summary of Options The options considered are summarized in Table 4-1.

ES020414102958WDC 4-5 COPYRIGHT 2014 BY CH2M HILL INTERNATIONAL, LTD. • COMPANY CONFIDENTIAL

SECTION 4 SITES UNDER CONSIDERATION

TABLE 4-1 Summary of Sites and Mooring Options Considered

1 Domunli Offshore mooring

2 Atuabo Offshore mooring

3 Esiama Offshore mooring

4 Takoradi Fixed berth outside existing port, protected with breakwater

5 Sekondi Fixed berth outside existing port, protected with breakwater

6 Aboadze Offshore mooring

7 Tema Offshore mooring