Debt and (not much) deleveraging - World Bank in debt-to-GDP ratio,1 2007 –14 Percentage points...

30

WORKING DRAFT Last Modified 5/19/2015 9:06 AM Malay Peninsula Standard Time Printed 3/12/2015 1:48 PM Eastern Standard Time Debt and (not much) deleveraging

Transcript of Debt and (not much) deleveraging - World Bank in debt-to-GDP ratio,1 2007 –14 Percentage points...

WORKING DRAFT

Last Modified 5/19/2015 9:06 AM Malay Peninsula Standard Time

Printed 3/12/2015 1:48 PM Eastern Standard Time

Debt and (not much)

deleveraging

11

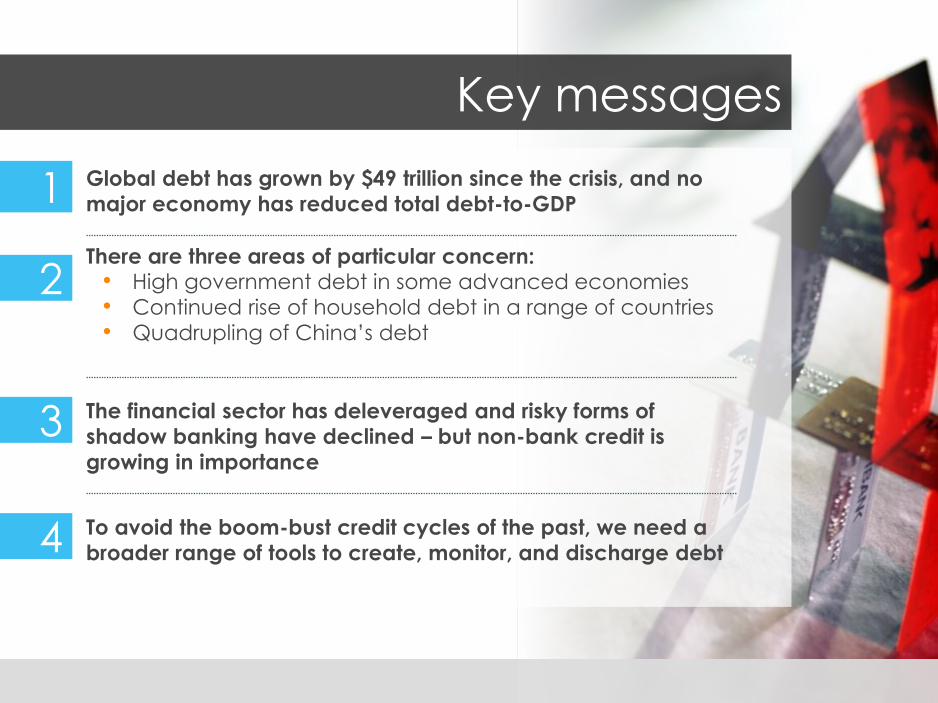

Global debt has grown by $49 trillion since the crisis, and no

major economy has reduced total debt-to-GDP

There are three areas of particular concern: • High government debt in some advanced economies

• Continued rise of household debt in a range of countries

• Quadrupling of China’s debt

The financial sector has deleveraged and risky forms of

shadow banking have declined – but non-bank credit is

growing in importance

1

2

3

To avoid the boom-bust credit cycles of the past, we need a

broader range of tools to create, monitor, and discharge debt4

Key messages

22

What happened to deleveraging?

33

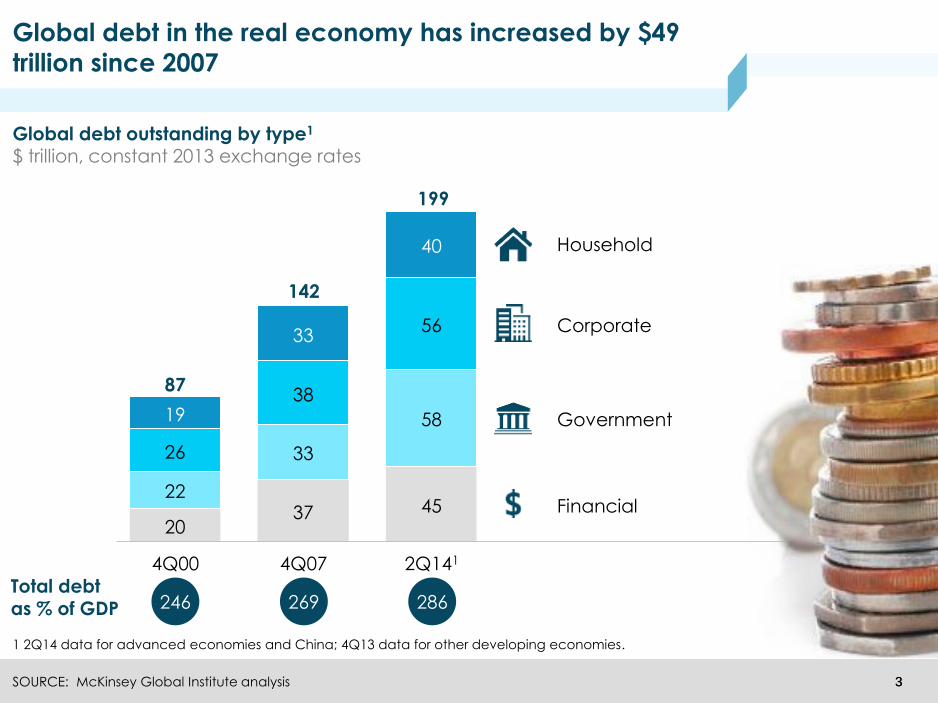

2037 45 Financial

Global debt outstanding by type1

$ trillion, constant 2013 exchange rates

SOURCE: McKinsey Global Institute analysis

1 2Q14 data for advanced economies and China; 4Q13 data for other developing economies.

199

87

142

4Q00 4Q07 2Q141

Global debt in the real economy has increased by $49

trillion since 2007

26

38

56 Corporate

22

33

58 Government19

33

40 Household

269246 286

87

142

199

Total debt as % of GDP

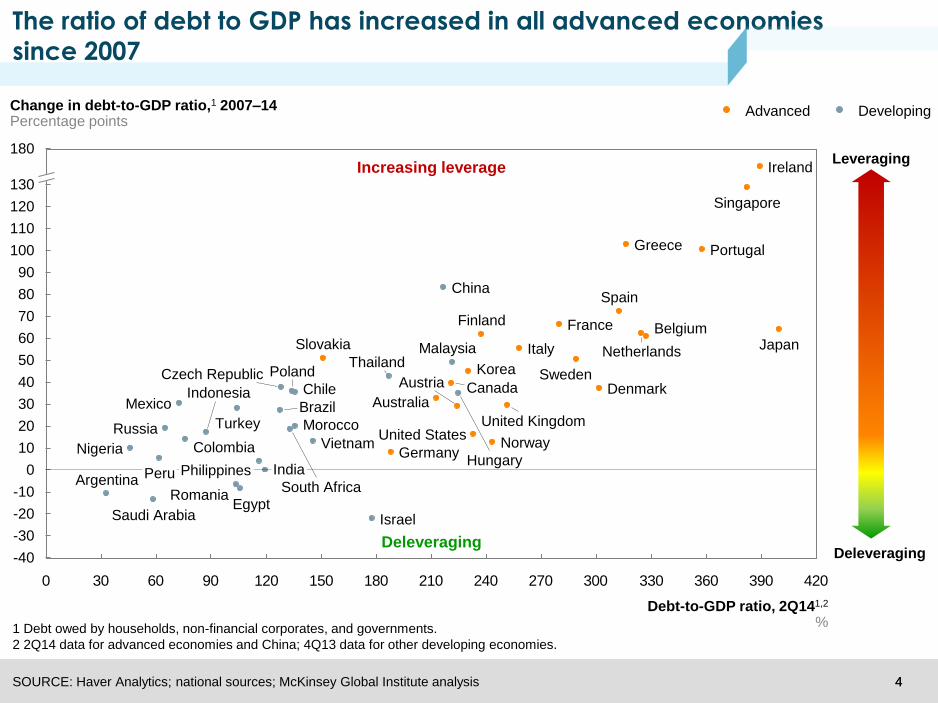

44

0 30 60 90 120 150 180 210 240 270 300 330 360 390 420

-30

-40

-10

0

10

180

-20

100

80

50

40

70

20

30

120

60

110

90

130

France

CanadaAustralia

Germany

Greece

Finland

DenmarkAustria

Belgium

Ireland

United States

Sweden

United Kingdom

Spain

Slovakia

Singapore

Portugal

JapanNetherlands

Korea

Italy

Change in debt-to-GDP ratio,1 2007–14Percentage points

Norway

Debt-to-GDP ratio, 2Q141,2

%

Thailand

Turkey

Vietnam

Saudi Arabia

Russia

South Africa

Morocco

Peru

Nigeria

Romania

Philippines

Poland

Indonesia

Malaysia

Israel

Mexico

ArgentinaIndia

Brazil

Chile

Egypt

Colombia

China

Czech Republic

Hungary

1 Debt owed by households, non-financial corporates, and governments.

2 2Q14 data for advanced economies and China; 4Q13 data for other developing economies.

The ratio of debt to GDP has increased in all advanced economies

since 2007

Increasing leverage

SOURCE: Haver Analytics; national sources; McKinsey Global Institute analysis

Deleveraging

Leveraging

Deleveraging

DevelopingAdvanced

55

Continued risks ahead

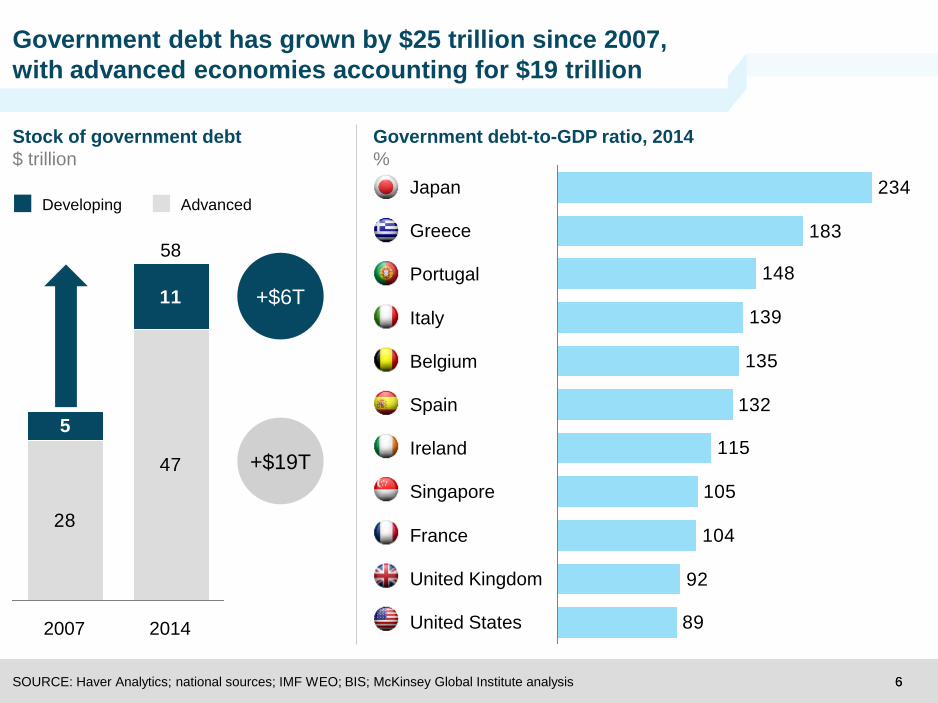

Government debt

66

28

47

5

11

58

20142007

33

89

92

104

105

115

132

135

139

148

183

234

France

Spain

Singapore

United Kingdom

Ireland

Belgium

Japan

Italy

Greece

Portugal

United States

Government debt has grown by $25 trillion since 2007,

with advanced economies accounting for $19 trillion

SOURCE: Haver Analytics; national sources; IMF WEO; BIS; McKinsey Global Institute analysis

AdvancedDeveloping

Government debt-to-GDP ratio, 2014

%

Stock of government debt

$ trillion

+$19T

+$6T

77

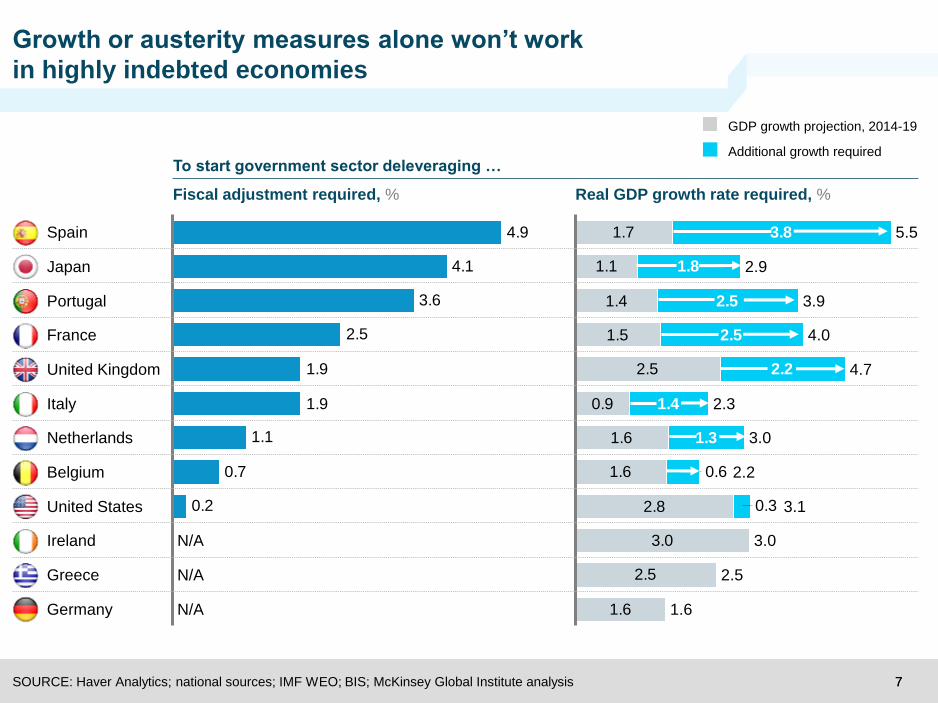

Growth or austerity measures alone won’t work

in highly indebted economies

SOURCE: Haver Analytics; national sources; IMF WEO; BIS; McKinsey Global Institute analysis

To start government sector deleveraging …

Fiscal adjustment required, % Real GDP growth rate required, %

0.2

0.7

1.1

1.9

1.9

2.5

3.6

4.1

4.9

N/A

United States

Belgium

Netherlands

Italy

United Kingdom

Germany N/A

Greece N/A

Ireland

France

Portugal

Japan

Spain 1.7

1.1

1.4

1.5

2.5

0.9

1.6

1.6

2.8

3.0

2.5

1.6

3.8

1.8

2.5

2.5

2.2

1.4

1.3

0.3

0.6

2.5

3.0

3.1

2.2

3.0

2.3

4.7

4.0

3.9

2.9

5.5

1.6

GDP growth projection, 2014-19

Additional growth required

88

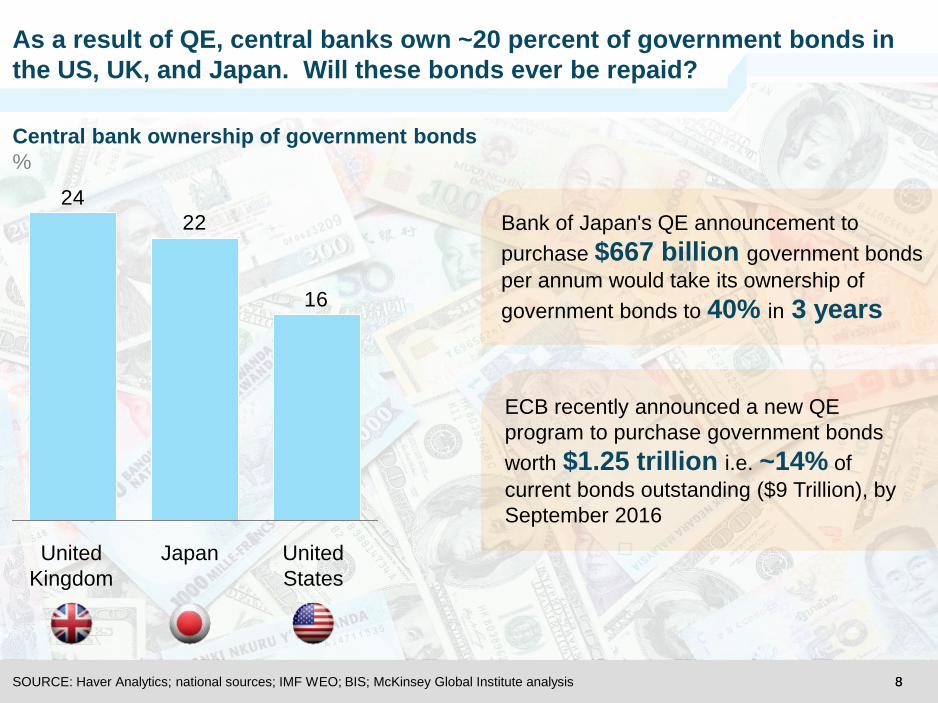

As a result of QE, central banks own ~20 percent of government bonds in

the US, UK, and Japan. Will these bonds ever be repaid?

SOURCE: Haver Analytics; national sources; IMF WEO; BIS; McKinsey Global Institute analysis

Central bank ownership of government bonds

%

ECB recently announced a new QE

program to purchase government bonds

worth $1.25 trillion i.e. ~14% of

current bonds outstanding ($9 Trillion), by

September 2016

United

States

United

Kingdom

Japan

Bank of Japan's QE announcement to

purchase $667 billion government bonds

per annum would take its ownership of

government bonds to 40% in 3 years16

22

24

99

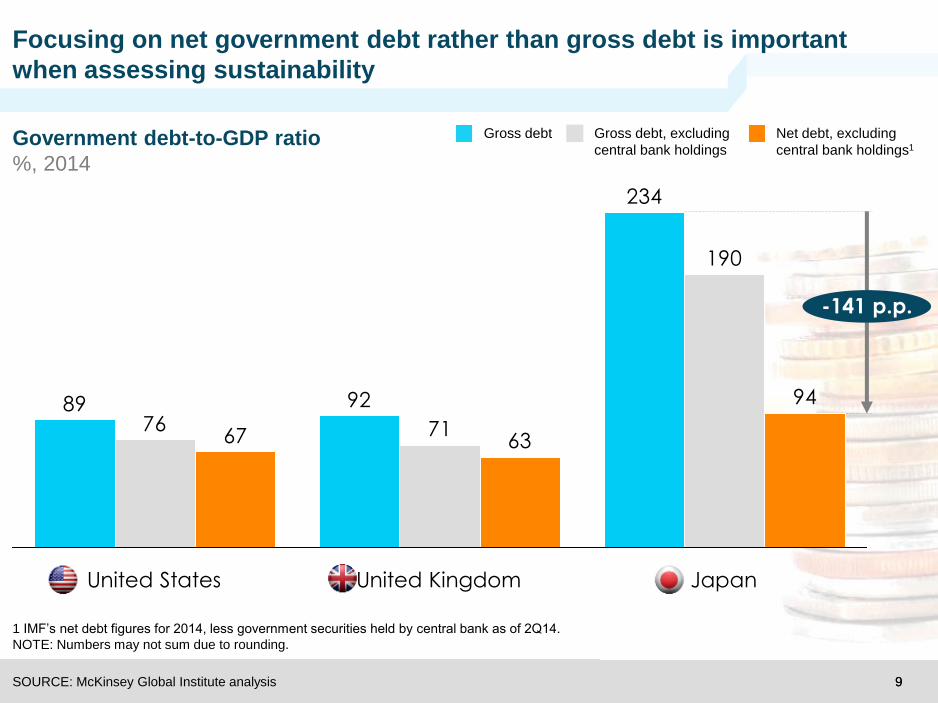

Focusing on net government debt rather than gross debt is important

when assessing sustainability

SOURCE: McKinsey Global Institute analysis

Government debt-to-GDP ratio

%, 2014

1 IMF’s net debt figures for 2014, less government securities held by central bank as of 2Q14.

NOTE: Numbers may not sum due to rounding.

Net debt, excluding

central bank holdings1

Gross debt, excluding

central bank holdings

Gross debt

234

9289

190

7176

94

6367

-141 p.p.

JapanUnited KingdomUnited States

1010

Hidden time bomb?

Household debt

1111

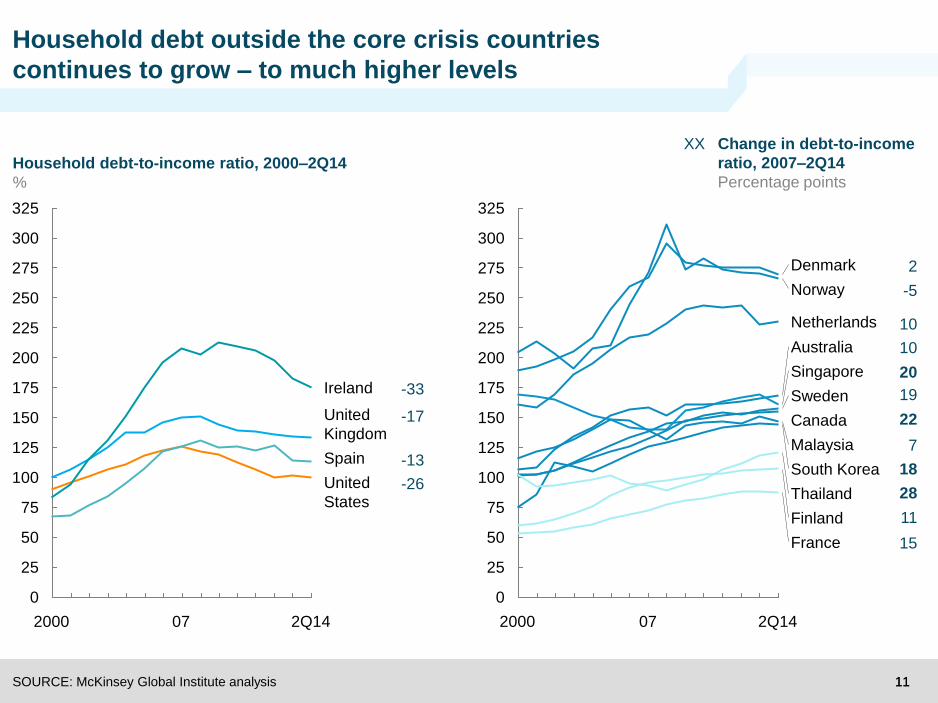

Household debt outside the core crisis countries

continues to grow – to much higher levels

Household debt-to-income ratio, 2000–2Q14

%

SOURCE: McKinsey Global Institute analysis

0

25

50

75

100

125

150

175

200

225

250

275

300

325

Ireland

United

Kingdom

Spain

United

States

2000 07 2Q14

0

25

50

75

100

125

150

175

200

225

250

275

300

325

Singapore

Australia

Finland

Netherlands

Sweden

Canada

Malaysia

South Korea

Thailand

France

Denmark

Norway

2000 07 2Q14

-33

-17

-13

-26

10

19

22

11

10

18

15

2

-5

Change in debt-to-income

ratio, 2007–2Q14

Percentage points

XX

7

28

20

1212

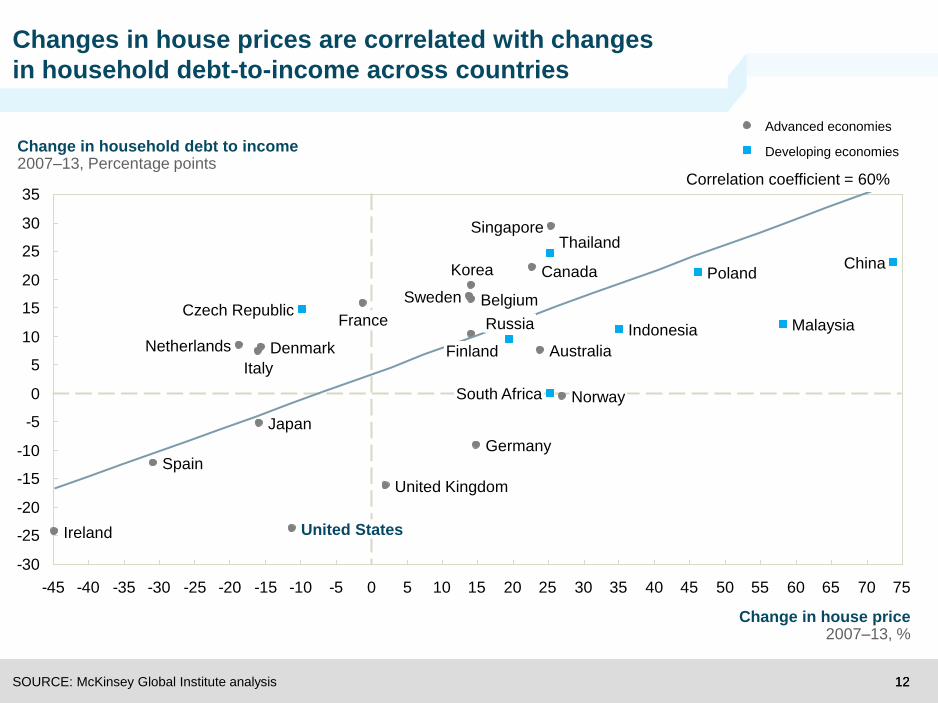

Changes in house prices are correlated with changes

in household debt-to-income across countries

SOURCE: McKinsey Global Institute analysis

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

-45 -40 -35 -30 -25 -20 -15 -10 -5 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75

Change in household debt to income2007–13, Percentage points

Change in house price2007–13, %

ThailandSingapore

Russia

PolandKorea

IndonesiaFrance

Czech Republic

ChinaCanada

Belgium

South Africa

Finland

Malaysia

Sweden

AustraliaNetherlands

Italy

Germany

Japan

United States

Spain

United Kingdom

Ireland

Norway

Denmark

Advanced economies

Developing economies

Correlation coefficient = 60%

1313

138115

135 125 116 104

60–80 80–90

157

194 196

40–60

192

20–40

140

<20

178

55 5280

160

216 23179

117

20–40

74

<20

280

80–90

263

60–80

205

40–60

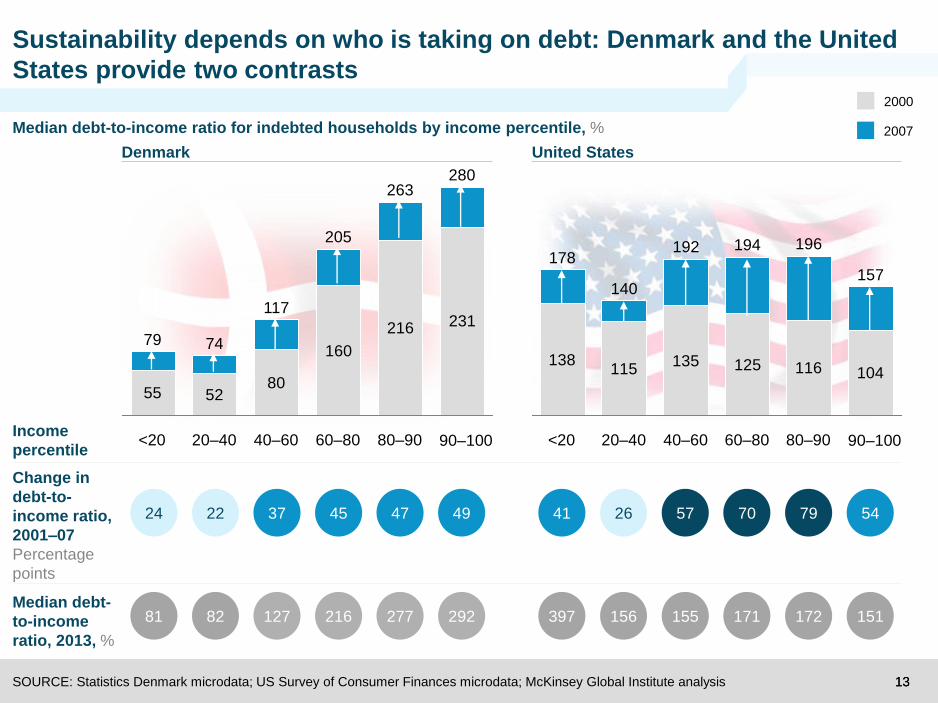

Sustainability depends on who is taking on debt: Denmark and the United

States provide two contrasts

Median debt-to-income ratio for indebted households by income percentile, %

SOURCE: Statistics Denmark microdata; US Survey of Consumer Finances microdata; McKinsey Global Institute analysis

Change in

debt-to-

income ratio,

2001–07

Percentage

points

2224 37 45 47 26 57 797041 5449

90–100

Denmark United States

Median debt-

to-income

ratio, 2013, %

8281 127 216 277 156 155 172171397 151292

2000

2007

90–100Income

percentile

1414SOURCE: McKinsey Global Institute analysis

Highest

Lowest

Country

Netherlands

South Korea

Canada

Sweden

Denmark

Norway

Australia

Malaysia

Thailand

Ireland

Belgium

Finland

UK

Spain

Portugal

China

France

Brazil

Russia

United States

Germany

Italy

Debt-to-income ratio,

2Q14, %

230

144

155

157

269

266

168

146

121

175

93

106

133

113

115

57

87

41

27

99

83

62

10

18

22

19

2

-5

10

7

28

-33

16

11

-17

-13

-9

22

15

14

9

-26

-11

7

Debt servicing ratio,1

2013, %

-18

15

28

18

-13

30

28

62

27

-43

15

14

9

-31

-2

86

-2

178

20

-9

18

-18

House price increase,

2007–2Q14, %

Change in debt-to-

income ratio,

2007–2Q14, p.p.

23

22

8

15

24

19

26

44

19

20

22

10

16

25

21

8

18

22

20

10

13

10

Singapore 161 20 2329

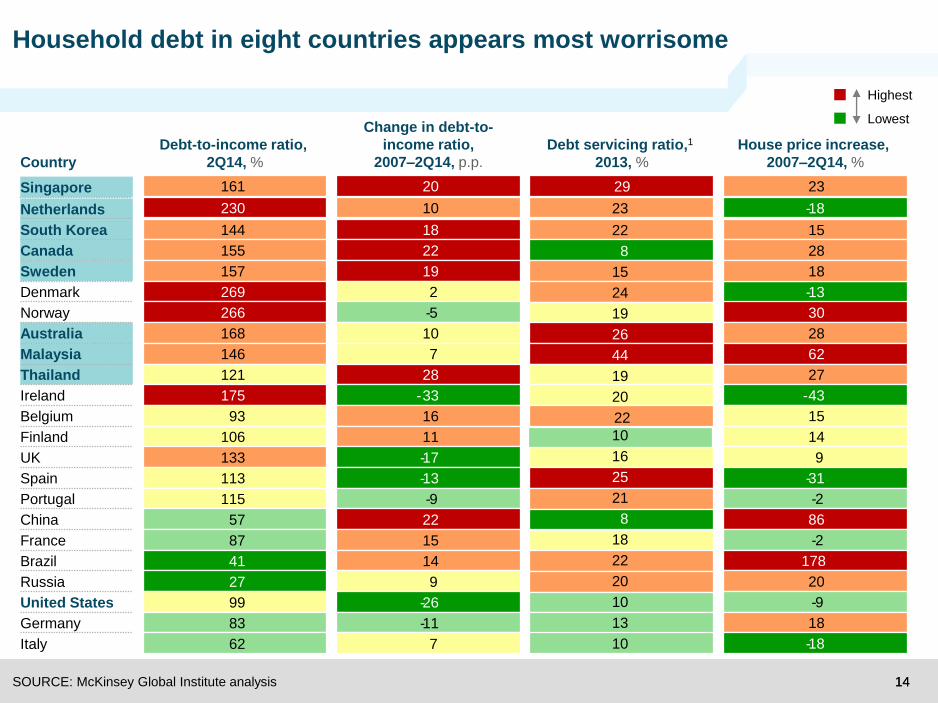

Household debt in eight countries appears most worrisome

1515

Three risks to watch

China’s soaring

debt

1616

55

31

89

80

70

125

69

67

54

60

38

113

77

54

92

65

61

36

70

25

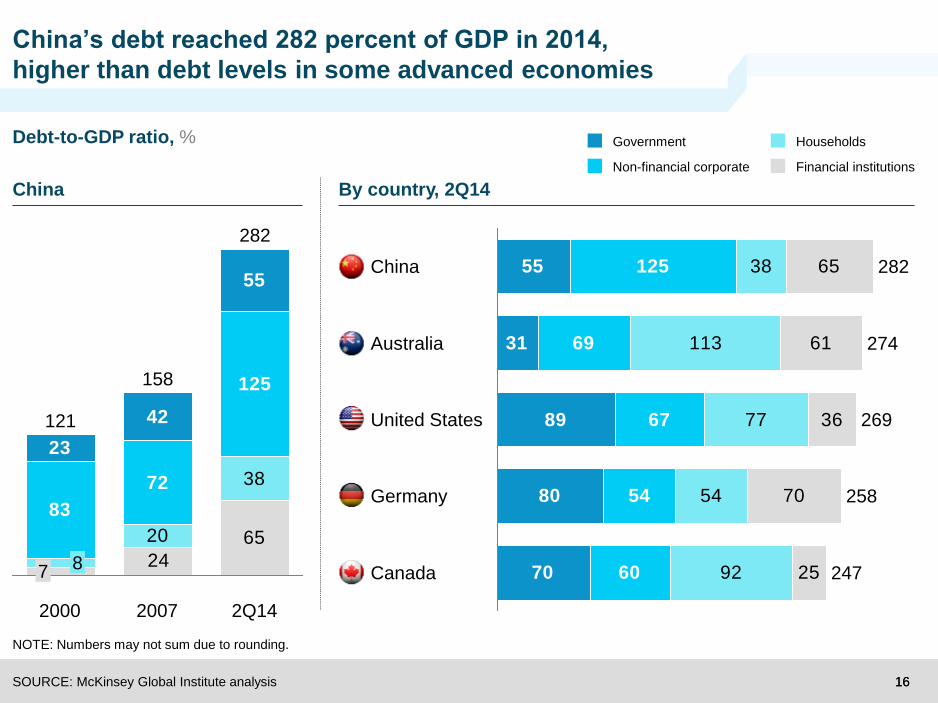

China 282

Australia

United States

274

Germany 258

269

247Canada

China’s debt reached 282 percent of GDP in 2014,

higher than debt levels in some advanced economies

SOURCE: McKinsey Global Institute analysis

NOTE: Numbers may not sum due to rounding.

Debt-to-GDP ratio, %

China By country, 2Q14

6520

38

83

72

125

23

42

24

55

8

2000

7

2007

158

282

2Q14

121

Financial institutions

Government Households

Non-financial corporate

1717

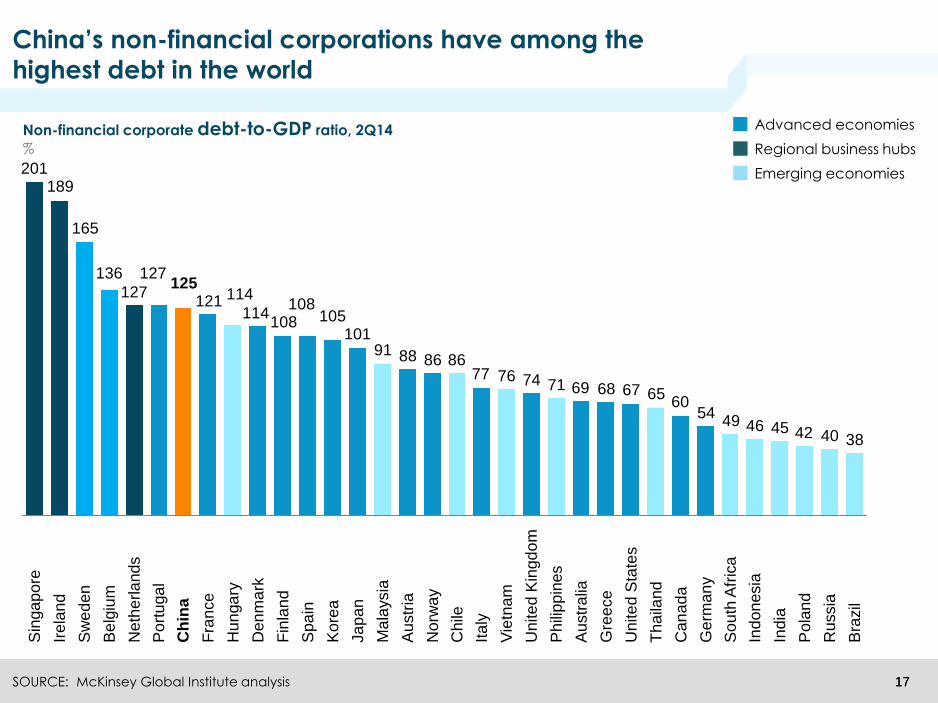

China’s non-financial corporations have among the

highest debt in the world

Non-financial corporate debt-to-GDP ratio, 2Q14

%

38404245464954

606567686971747677

86868891101

105108

108114

114121125

127

127

136

165

189201

Ru

ssia

Po

lan

d

Bra

zil

Un

ite

d S

tate

s

Au

str

alia

Ind

ia

Ph

ilipp

ines

Ca

na

da

So

uth

Afr

ica

Ind

on

esia

Ge

rma

ny

Th

aila

nd

Gre

ece

Fra

nce

Sp

ain

Au

str

ia

Ja

pa

n

Hu

nga

ry

Ita

ly

Ch

ile

De

nm

ark

Ma

laysia

Ko

rea

Un

ite

d K

ingd

om

Vie

tna

m

No

rwa

y

Fin

lan

d

Ch

ina

Po

rtu

ga

l

Sw

ed

en

Ne

the

rla

nds

Sin

ga

po

re

Be

lgiu

m

Ire

lan

d

Advanced economies

Regional business hubs

Emerging economies

SOURCE: McKinsey Global Institute analysis

1818

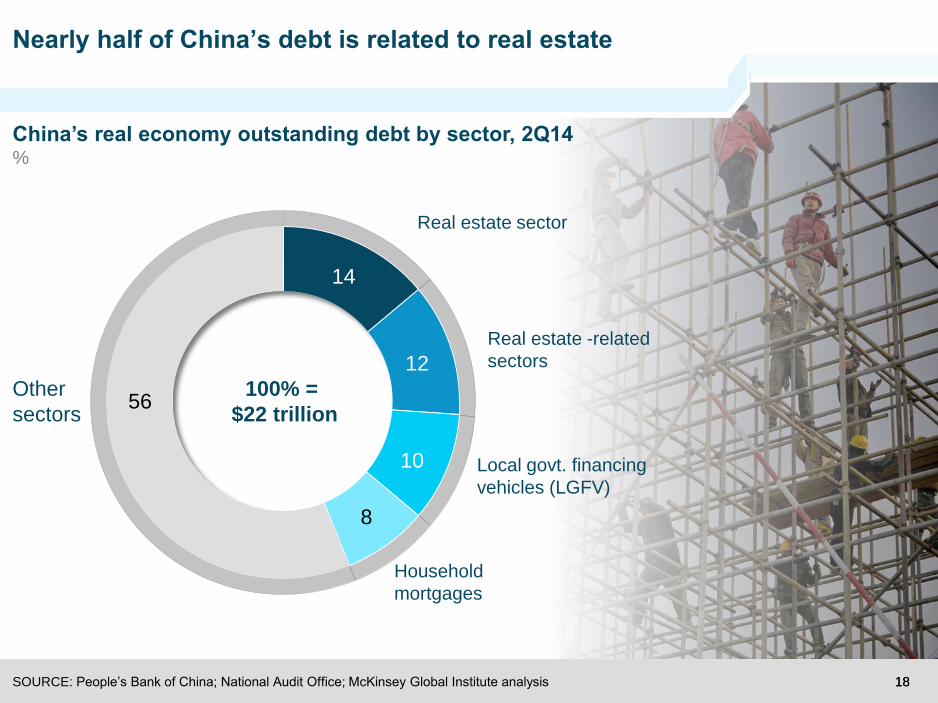

Nearly half of China’s debt is related to real estate

SOURCE: People’s Bank of China; National Audit Office; McKinsey Global Institute analysis

China’s real economy outstanding debt by sector, 2Q14%

Real estate sector

Real estate -related

sectors

Local govt. financing

vehicles (LGFV)

Household

mortgages

14

12

10

8

56100% =

$22 trillion

Other

sectors

1919

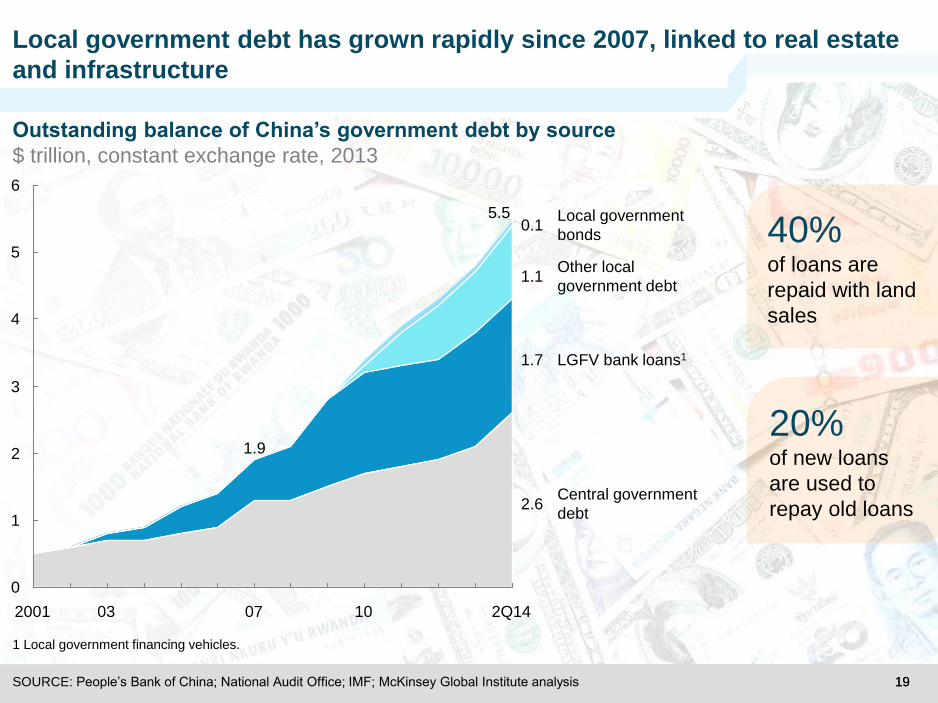

Local government debt has grown rapidly since 2007, linked to real estate

and infrastructure

SOURCE: People’s Bank of China; National Audit Office; IMF; McKinsey Global Institute analysis

Outstanding balance of China’s government debt by source

$ trillion, constant exchange rate, 2013

1 Local government financing vehicles.

0.1Local government

bonds

1.1Other local

government debt

1.7 LGFV bank loans1

2.6Central government

debt

20% of new loans

are used to

repay old loans

40%of loans are

repaid with land

sales

0

1

2

3

4

5

6

2Q14

5.5

1007

1.9

032001

2020

53%

13%

30.0%

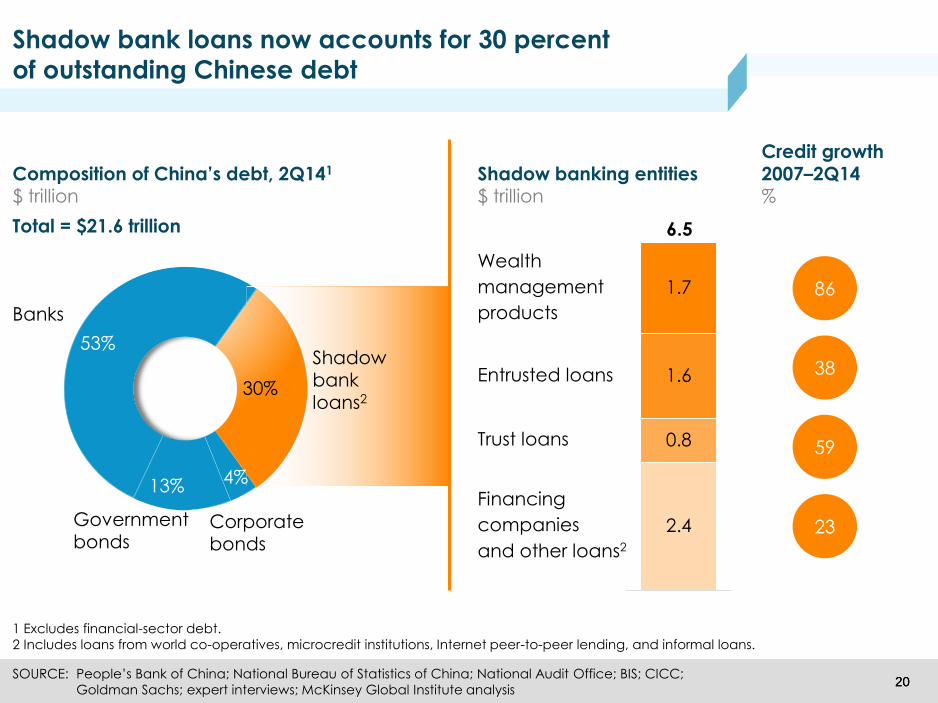

Shadow bank loans now accounts for 30 percent

of outstanding Chinese debt

1 Excludes financial-sector debt.

2 Includes loans from world co-operatives, microcredit institutions, Internet peer-to-peer lending, and informal loans.

SOURCE: People’s Bank of China; National Bureau of Statistics of China; National Audit Office; BIS; CICC;

Goldman Sachs; expert interviews; McKinsey Global Institute analysis

Banks

Corporatebonds

Governmentbonds

Total = $21.6 trillion

Composition of China’s debt, 2Q141

$ trillion

86

38

59

23

Credit growth 2007–2Q14%

Shadow banking entities$ trillion

Entrusted loans

Wealth

management

products

2.4

0.8

1.6

1.7

Financing

companies

and other loans2

Trust loans

6.5

Shadowbankloans2

30%

4%

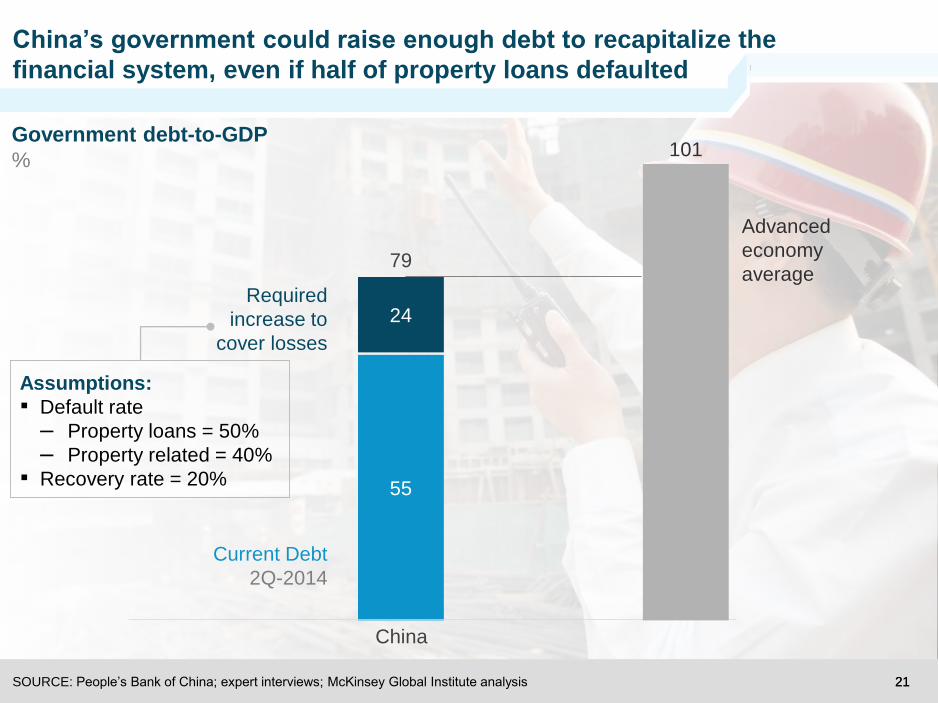

2121SOURCE: People’s Bank of China; expert interviews; McKinsey Global Institute analysis

55

24

79

Current Debt

2Q-2014

Required

increase to

cover losses

China

Government debt-to-GDP

%101

Advanced

economy

average

Assumptions:

▪ Default rate

– Property loans = 50%

– Property related = 40%

▪ Recovery rate = 20%

China’s government could raise enough debt to recapitalize the

financial system, even if half of property loans defaulted

2222

Out of the shadows

Shadow banking

2323

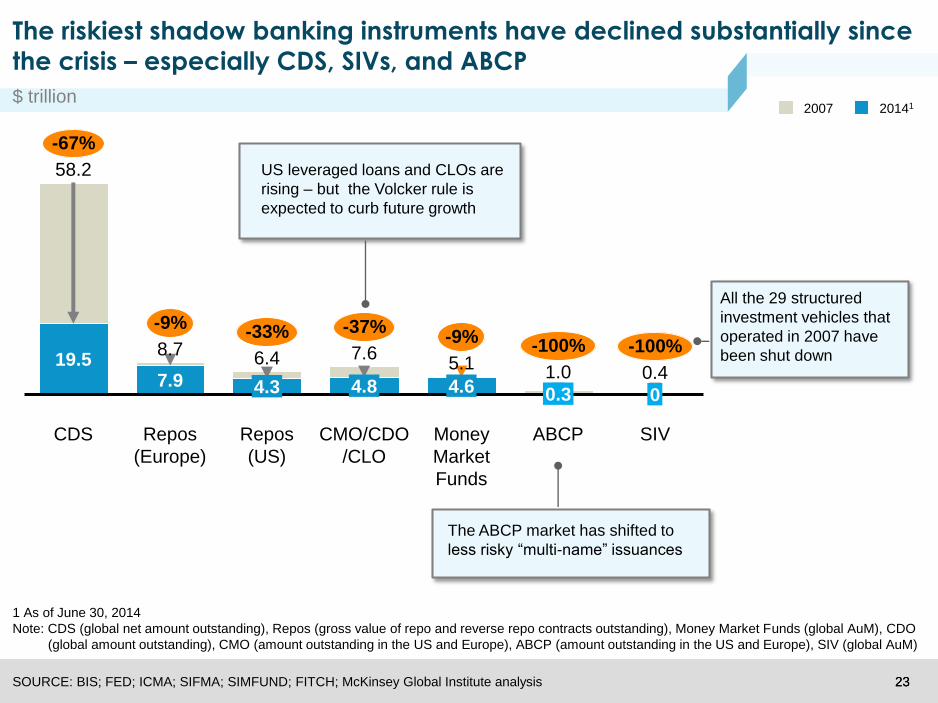

The riskiest shadow banking instruments have declined substantially since

the crisis – especially CDS, SIVs, and ABCP

5.11.0 0.4

-100%-9%

-100%

ABCPMoney

Market

Funds

-37%

6.4

-33%7.6

58.2

SIV

-9%

8.7

00.3

-67%

Repos

(US)

CDS

19.5

4.8 4.6

Repos

(Europe)

7.9

CMO/CDO

/CLO

4.3

2007 20141

All the 29 structured

investment vehicles that

operated in 2007 have

been shut down

US leveraged loans and CLOs are

rising – but the Volcker rule is

expected to curb future growth

The ABCP market has shifted to

less risky “multi-name” issuances

1 As of June 30, 2014

Note: CDS (global net amount outstanding), Repos (gross value of repo and reverse repo contracts outstanding), Money Market Funds (global AuM), CDO

(global amount outstanding), CMO (amount outstanding in the US and Europe), ABCP (amount outstanding in the US and Europe), SIV (global AuM)

SOURCE: BIS; FED; ICMA; SIFMA; SIMFUND; FITCH; McKinsey Global Institute analysis

$ trillion

2424

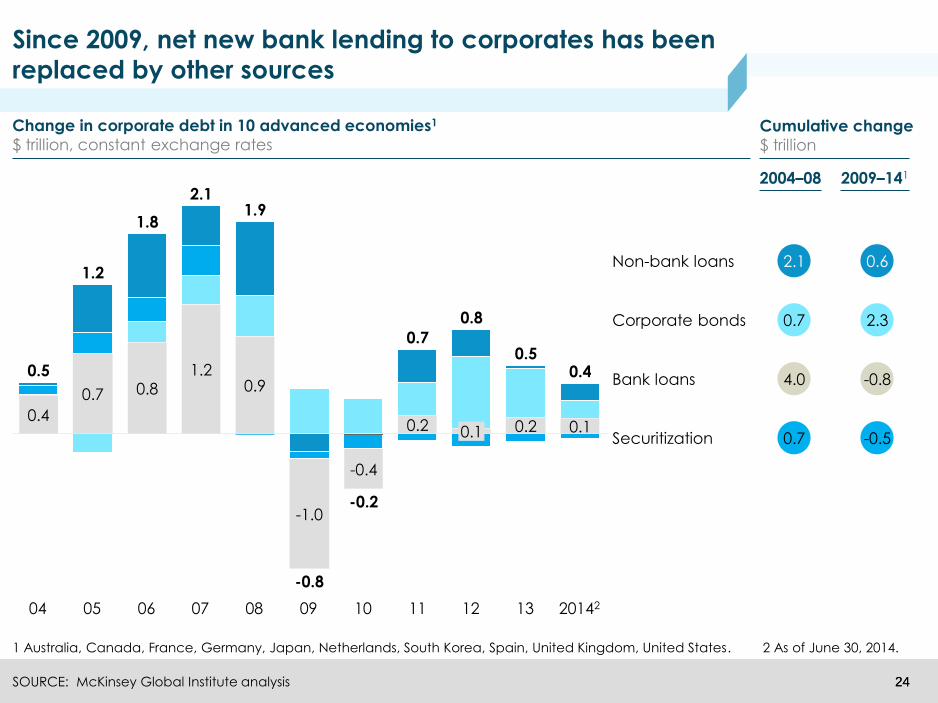

1 Australia, Canada, France, Germany, Japan, Netherlands, South Korea, Spain, United Kingdom, United States. 2 As of June 30, 2014.

SOURCE: McKinsey Global Institute analysis

Since 2009, net new bank lending to corporates has been

replaced by other sources

0.7 -0.5Securitization

2.1 0.6Non-bank loans

Change in corporate debt in 10 advanced economies1

$ trillion, constant exchange rates

20142

0.4

13

0.5

12

0.8

11

0.7

10

-0.2

09

-0.8

08

1.9

07

2.1

06

1.8

05

1.2

04

0.5

2004–08

Cumulative change

$ trillion

2009–141

0.7 2.3Corporate bonds

4.0 -0.8Bank loans

0.2 0.10.2

-0.4

-1.0

0.91.2

0.80.7

0.40.1

2525

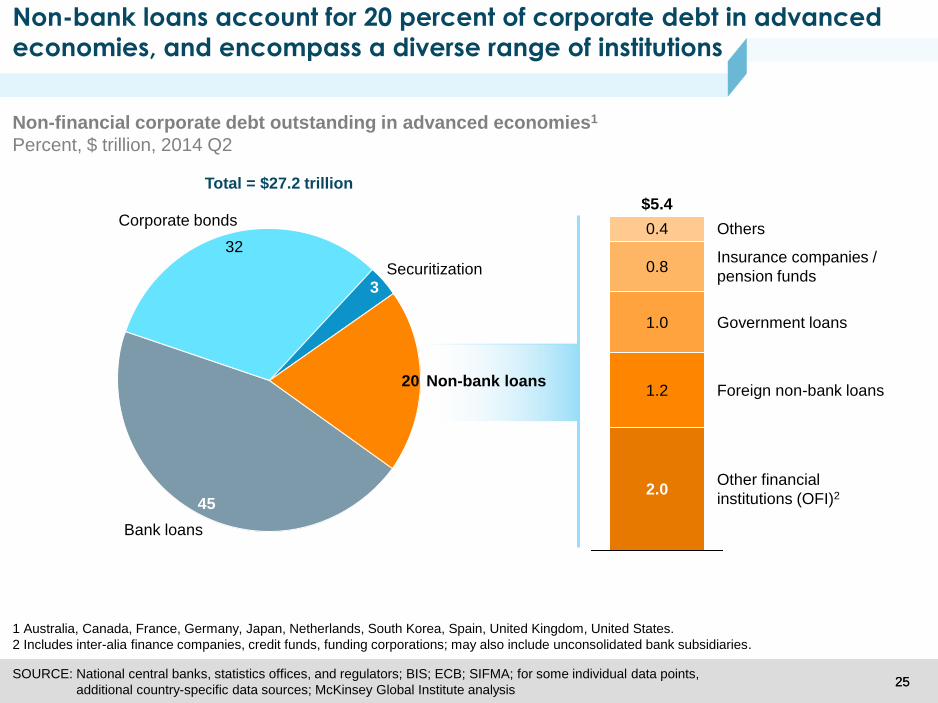

Non-bank loans account for 20 percent of corporate debt in advanced

economies, and encompass a diverse range of institutions

SOURCE: National central banks, statistics offices, and regulators; BIS; ECB; SIFMA; for some individual data points,

additional country-specific data sources; McKinsey Global Institute analysis

1 Australia, Canada, France, Germany, Japan, Netherlands, South Korea, Spain, United Kingdom, United States.

2 Includes inter-alia finance companies, credit funds, funding corporations; may also include unconsolidated bank subsidiaries.

Non-financial corporate debt outstanding in advanced economies1

Percent, $ trillion, 2014 Q2

32

45

Corporate bonds

Securitization3

20 Non-bank loans

Bank loans

Total = $27.2 trillion

Other financial

institutions (OFI)2

Foreign non-bank loans

Government loans

Insurance companies /

pension funds

$5.4

1.2

Others

2.0

1.0

0.8

0.4

2626

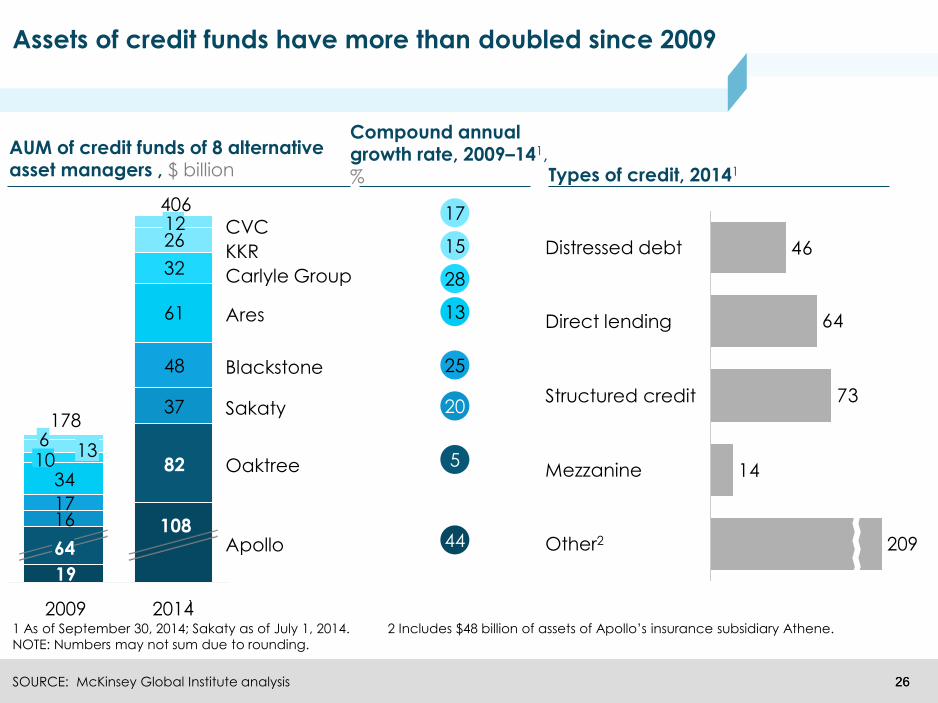

Assets of credit funds have more than doubled since 2009

SOURCE: McKinsey Global Institute analysis

1 As of September 30, 2014; Sakaty as of July 1, 2014. 2 Includes $48 billion of assets of Apollo’s insurance subsidiary Athene.

NOTE: Numbers may not sum due to rounding.

14

73

64

46

Structured credit

Direct lending

Distressed debt

209Other2

Mezzanine

AUM of credit funds of 8 alternative asset managers , $ billion

17

15

28

13

25

20

5

44

Compound annual growth rate, 2009–141, % Types of credit, 20141

82

48

61

19

37

1617

34

32

26

Ares

Carlyle Group

KKR

CVC

20141

406

108Apollo

Oaktree

Sakaty

Blackstone

12

2009

178

64

1013

6

2727

Finding stability in an indebted world

2828

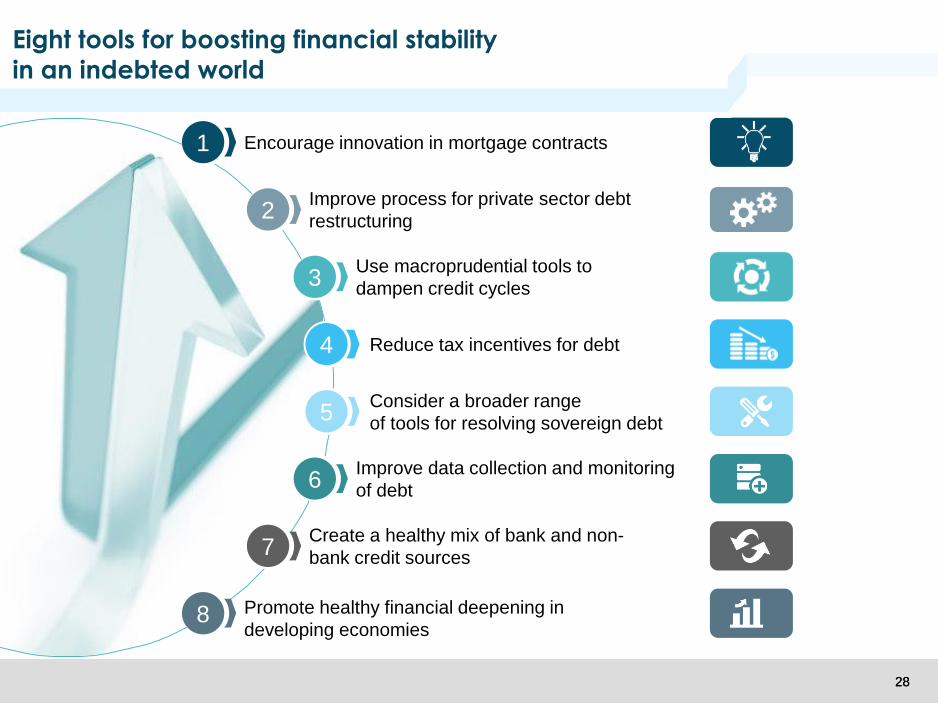

Eight tools for boosting financial stability

in an indebted world

Improve data collection and monitoring

of debt6

Create a healthy mix of bank and non-

bank credit sources7

Consider a broader range

of tools for resolving sovereign debt5

Promote healthy financial deepening in

developing economies8

Improve process for private sector debt

restructuring2

Use macroprudential tools to

dampen credit cycles3

Encourage innovation in mortgage contracts1

Reduce tax incentives for debt4

2929

Thank you

Follow us on Twitter:

www.mckinsey.com/mgi

Download McKinsey Global Institute reports:

@mckinsey_mgi