PDF 8.01 MB

24

Lumwana Site Visit P tI O ti R i 1 PartI – Operations Review February 5-6, 2014 Agenda 1 SAFETY IMPROVEMENTS 2 OVERVIEW OF COPPER GROUP 1. SAFETY IMPROVEMENTS 2. OVERVIEW OF COPPER GROUP 3. SITE OVERVIEW 4. TURNAROUND PROGRESS TO DATE 2

Transcript of PDF 8.01 MB

Lumwana Site VisitP t I O ti R i

1

Part I – Operations ReviewFebruary 5-6, 2014

Agenda

1 SAFETY IMPROVEMENTS

2 OVERVIEW OF COPPER GROUP

1. SAFETY IMPROVEMENTS

2. OVERVIEW OF COPPER GROUP

3. SITE OVERVIEW

4. TURNAROUND PROGRESS TO DATE

2

Agenda

1 SAFETY IMPROVEMENTS

2 OVERVIEW OF COPPER GROUP

1. SAFETY IMPROVEMENTS

2. OVERVIEW OF COPPER GROUP

3. SITE OVERVIEW

4. TURNAROUND PROGRESS TO DATE

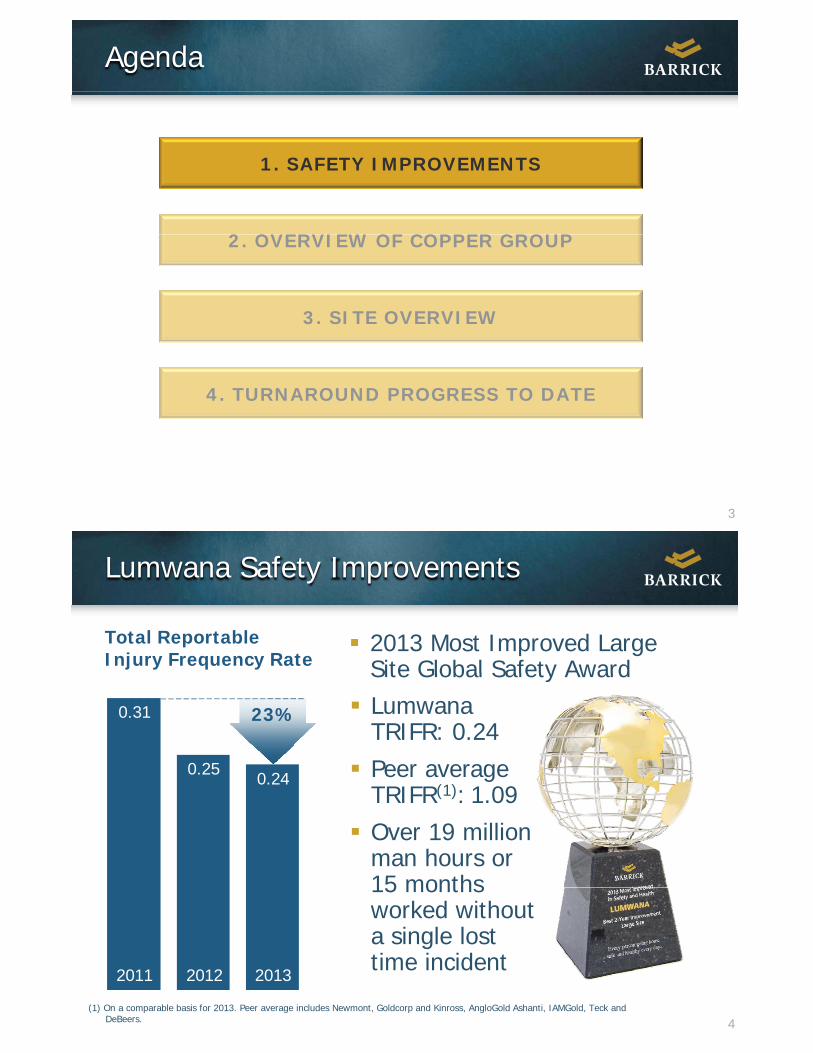

3

Lumwana Safety Improvements

2013 Most Improved Large Site Global Safety Award

Total Reportable Injury Frequency Rate Site Global Safety Award

23%0.31 Lumwana TRIFR: 0.24

0.25 0.24 Peer average TRIFR(1): 1.09Over 19 million man hours or 15 months15 monthsworked without a single lost time incident

4

2011 2012 2013

(1) On a comparable basis for 2013. Peer average includes Newmont, Goldcorp and Kinross, AngloGold Ashanti, IAMGold, Teck and DeBeers.

time incident

Agenda

1 SAFETY IMPROVEMENTS

2 OVERVIEW OF COPPER GROUP

1. SAFETY IMPROVEMENTS

2. OVERVIEW OF COPPER GROUP

3. SITE OVERVIEW

4. TURNAROUND PROGRESS TO DATE

5

Global Copper Group

A dedicated senior leadership team was appointed in late 2012in late 2012

Small company approach, lean, clarity of roles

Focused exclusively on optimizing copper assets to maximize free cash flow and risk adjusted returns

Zaldívar Lumwana Jabal Sayid

66

Copper Group Leadership Team

Mark Fisher: President

Jon Douglas: CFOJon Douglas: CFO

David Elliott: Vice President

Brian Grebenc: Director of Operations, Africa & Middle Eastp ,

Bill MacNevin: General Manager, Lumwana

77

Agenda

1 SAFETY IMPROVEMENTS

2 OVERVIEW OF COPPER GROUP

1. SAFETY IMPROVEMENTS

2. OVERVIEW OF COPPER GROUP

3. SITE OVERVIEW

4. TURNAROUND PROGRESS TO DATE

8

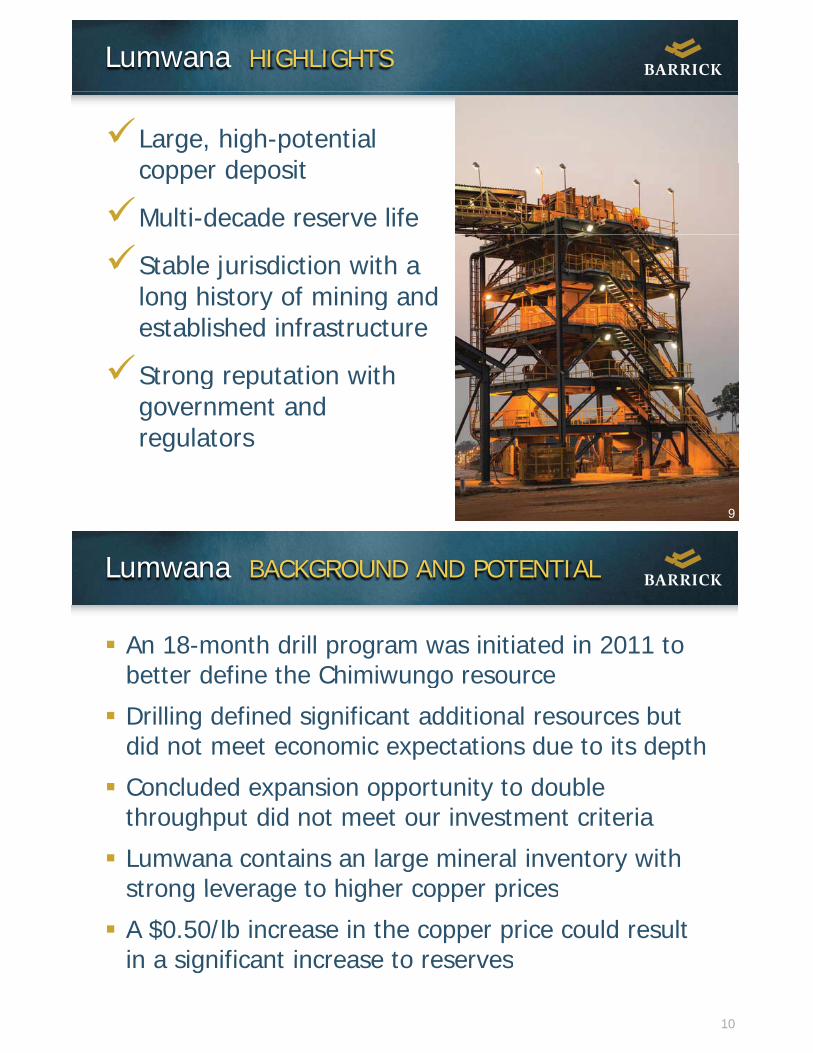

Lumwana HIGHLIGHTS

Large, high-potential d itcopper deposit

Multi-decade reserve life

Stable jurisdiction with a long history of mining and g y gestablished infrastructure

Strong reputation withStrong reputation withgovernment and regulators

9

g

9

Lumwana BACKGROUND AND POTENTIAL

An 18-month drill program was initiated in 2011 to better define the Chimiwungo resourcebetter define the Chimiwungo resource

Drilling defined significant additional resources but did not meet economic expectations due to its depthdid not meet economic expectations due to its depth

Concluded expansion opportunity to double throughput did not meet our investment criteriathroughput did not meet our investment criteria

Lumwana contains an large mineral inventory with strong leverage to higher copper pricesstrong leverage to higher copper prices

A $0.50/lb increase in the copper price could result in a significant increase to reserves

10

in a significant increase to reserves

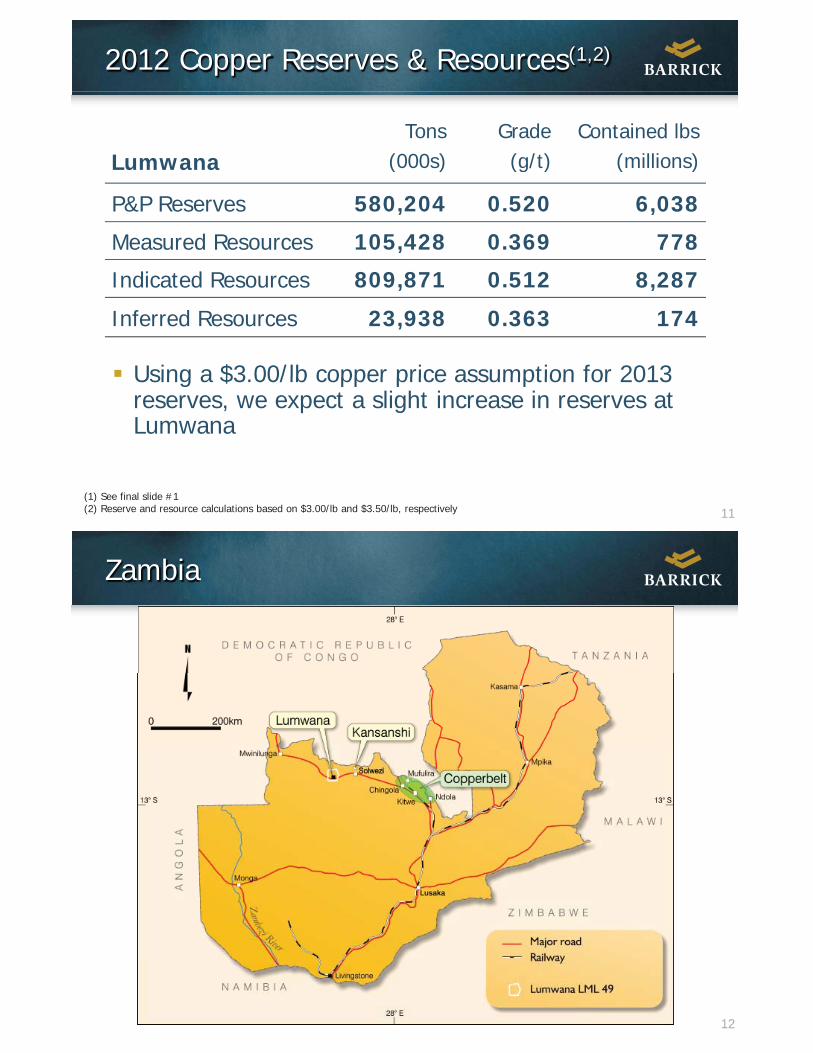

2012 Copper Reserves & Resources(1,2)

Tons Grade Contained lbsLumwana (000s) (g/t) (millions)Lumwana (000s) (g/t) (millions)

P&P Reserves 580,204 0.520 6,038

M d R 105 428 0 369 778Measured Resources 105,428 0.369 778

Indicated Resources 809,871 0.512 8,287

Inferred Resources 23,938 0.363 174

Using a $3 00/lb copper price assumption for 2013Using a $3.00/lb copper price assumption for 2013reserves, we expect a slight increase in reserves at Lumwana

11(1) See final slide #1(2) Reserve and resource calculations based on $3.00/lb and $3.50/lb, respectively

Zambia

12

Zambian Copper Belt

D R CTenke

Kamoto

Z A M B I A

A N G O L A

KansanshiSentinel

A N G O L A

Z A M B I AKonkola

Nchanga

LUMWANA

Z A M B I A NchangaChambishi

MufuliraNkana

1,265 km2

Equinox Tenement

Upper & Lower Roan

13

0 200kmBasement Inlier

Undiff Kundelunga

13

Lumwana Land Package

14

Lumwana Plan View

Malundwe Lumwana

Tailings Storage Facility

MalundweWasteDumpMalundwe

Main Pit

LumwanaTownship

LumwanaDam

ROM Pad & Crusher

Diversion Channel

Plant

Township

CampChimi Dam

LightIndustrial

Area

Admin Office

Chimi ngo

ChimiwungoEast Pit

ChimiwungoMain Pit

ChimiEast

Waste

Chimiwungo South Waste

ChimiwungoMain Waste

15

ChimiwungoSouth Pit

Solwezi 65 km 15

Open Pit Mining

Open pit – truck/shovel Chimiwungo expected toChimiwungo expected toprovide ~70% of ore feed in 2014 Malundwe

2013E Malundwe Chimiwungo

Tonnes per 40k 210Kpday

Grade 0.68 % 0.46 %

Mining Cost $3.43 per $3.47 per

Chimi LOM strip ratio

Mining Cost $3.43 pertonne

$3.47 pertonne

16

Chimi LOM strip ratioexpected to be ~2.3:1

Chimiwungo16

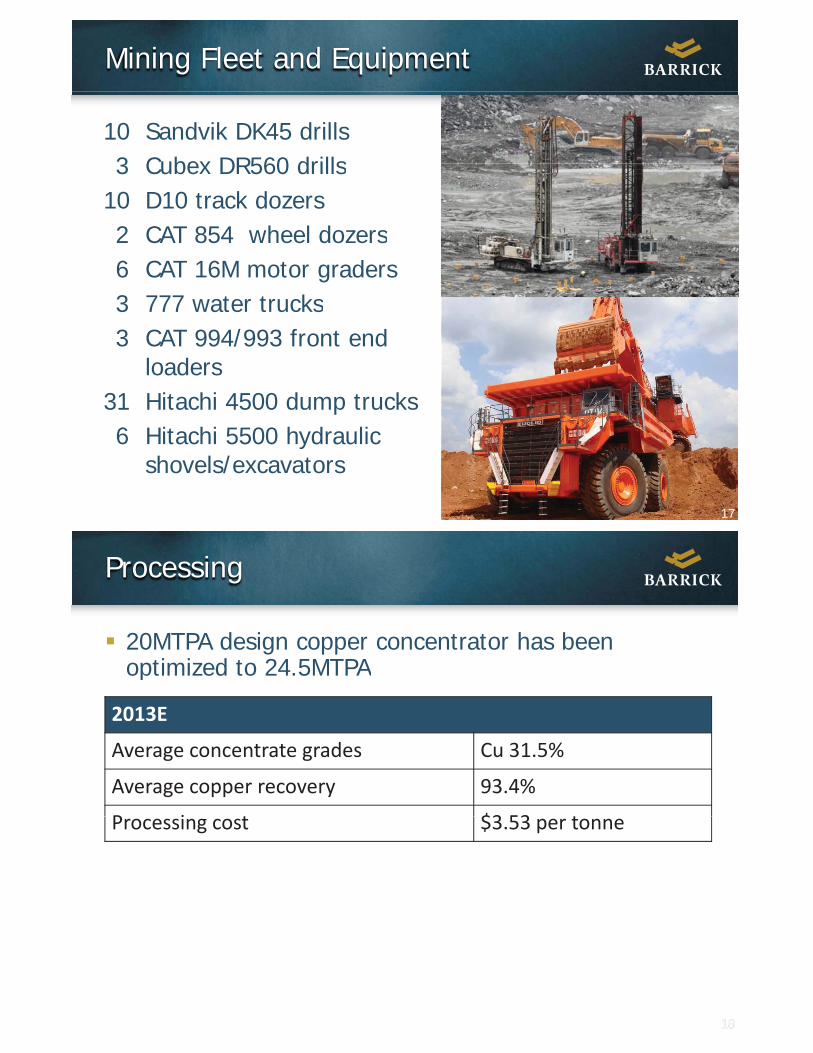

Mining Fleet and Equipment

10 Sandvik DK45 drills 3 Cubex DR560 drills3 Cubex DR560 drills

10 D10 track dozers2 CAT 854 wheel dozers2 CAT 854 wheel dozers6 CAT 16M motor graders3 777 water trucks3 777 water trucks3 CAT 994/993 front end

loaders31 Hitachi 4500 dump trucks6 Hitachi 5500 hydraulic

17

yshovels/excavators

17

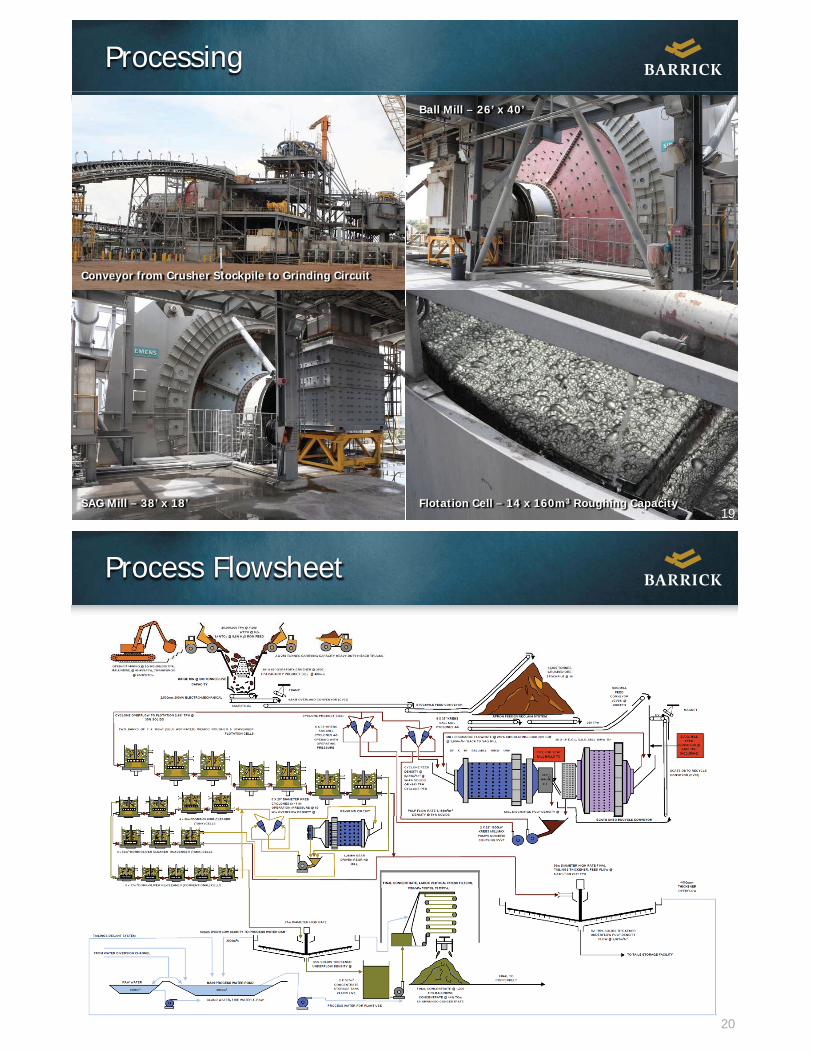

Processing

20MTPA design copper concentrator has been optimized to 24.5MTPAoptimized to 24.5MTPA

2013E

A t t d C 31 5%Average concentrate grades Cu 31.5%

Average copper recovery 93.4%

P i t $3 53 tProcessing cost $3.53 per tonne

1818

Processing

Ball Mill – 26’ x 40’

Conveyor from Crusher Stockpile to Grinding Circuit

19SAG Mill – 38’ x 18’ Flotation Cell – 14 x 160m3 Roughing Capacity

19

Process Flowsheet

20

Concentrate Marketing

Lumwana sells concentrate under long-term sales agreements to three smelters in Zambiaagreements to three smelters in Zambia– Chambishi Copper Smelter (CCS)– Konkola Copper Mines (KCM)Konkola Copper Mines (KCM)– Mopani

Concentrate is only sold domestically and is notConcentrate is only sold domestically and is notsubject to the 10% duty on all copper concentrate sold internationally (~$0.35/lb)

Smelter capacity not an issue as long-term agreements are in place that ensure our full

d ti b d

21

production can be processed

Agenda

1 SAFETY IMPROVEMENTS

2 OVERVIEW OF COPPER GROUP

1. SAFETY IMPROVEMENTS

2. OVERVIEW OF COPPER GROUP

3. SITE OVERVIEW

4. TURNAROUND PROGRESS TO DATE

22

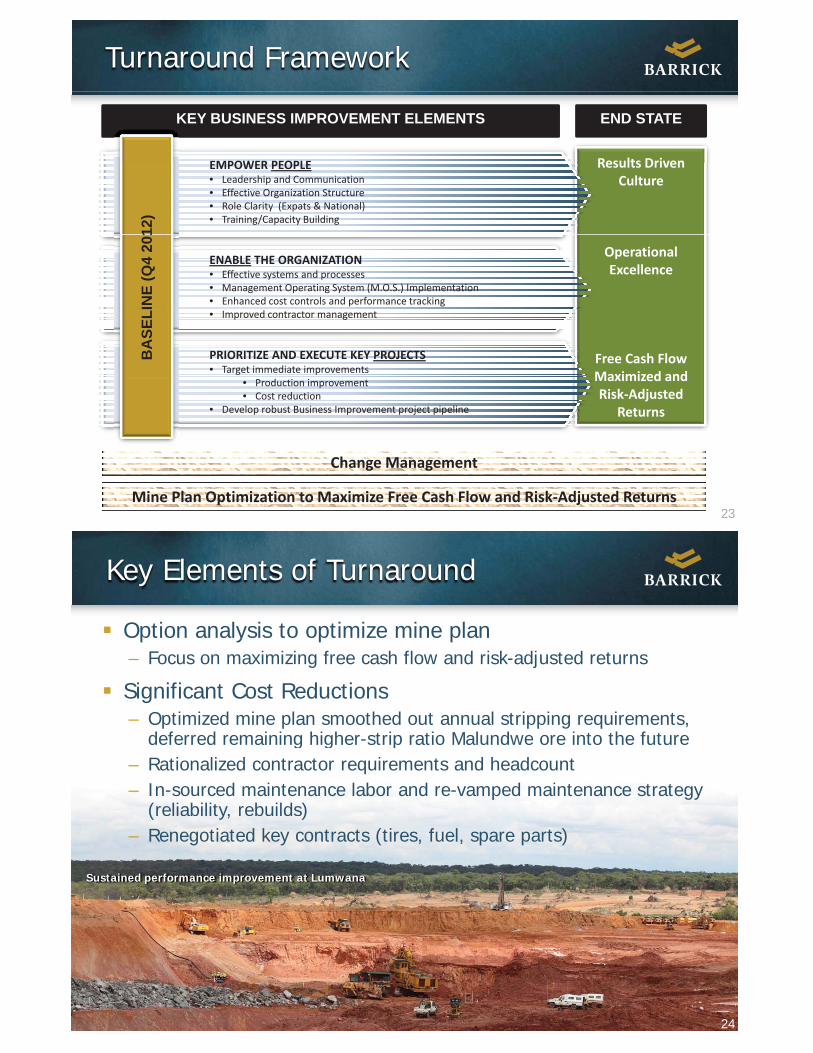

Turnaround Framework

Results Driven

KEY BUSINESS IMPROVEMENT ELEMENTS END STATE

EMPOWER PEOPLE Results DrivenCulture

EMPOWER PEOPLE• Leadership and Communication• Effective Organization Structure• Role Clarity (Expats & National)• Training/Capacity Building

12)

OperationalExcellence

ENABLE THE ORGANIZATION• Effective systems and processes• Management Operating System (M.O.S.) Implementation• Enhanced cost controls and performance trackingN

E (Q

4 20

1

Free Cash FlowMaximized and

p g• Improved contractor management

PRIORITIZE AND EXECUTE KEY PROJECTS• Target immediate improvements

BA

SELI

Maximized andRisk Adjusted

Returns

• Production improvement• Cost reduction

• Develop robust Business Improvement project pipeline

23Mine Plan Optimization to Maximize Free Cash Flow and Risk Adjusted Returns

Change Management

Key Elements of Turnaround

Option analysis to optimize mine plan – Focus on maximizing free cash flow and risk-adjusted returns

Significant Cost Reductions– Optimized mine plan smoothed out annual stripping requirements,

deferred remaining higher-strip ratio Malundwe ore into the futurede e ed e a g g e st p at o a u d e o e to t e utu e– Rationalized contractor requirements and headcount – In-sourced maintenance labor and re-vamped maintenance strategy

(reliability, rebuilds)

Sustained performance improvement at Lumwana

( y, )– Renegotiated key contracts (tires, fuel, spare parts)

2424

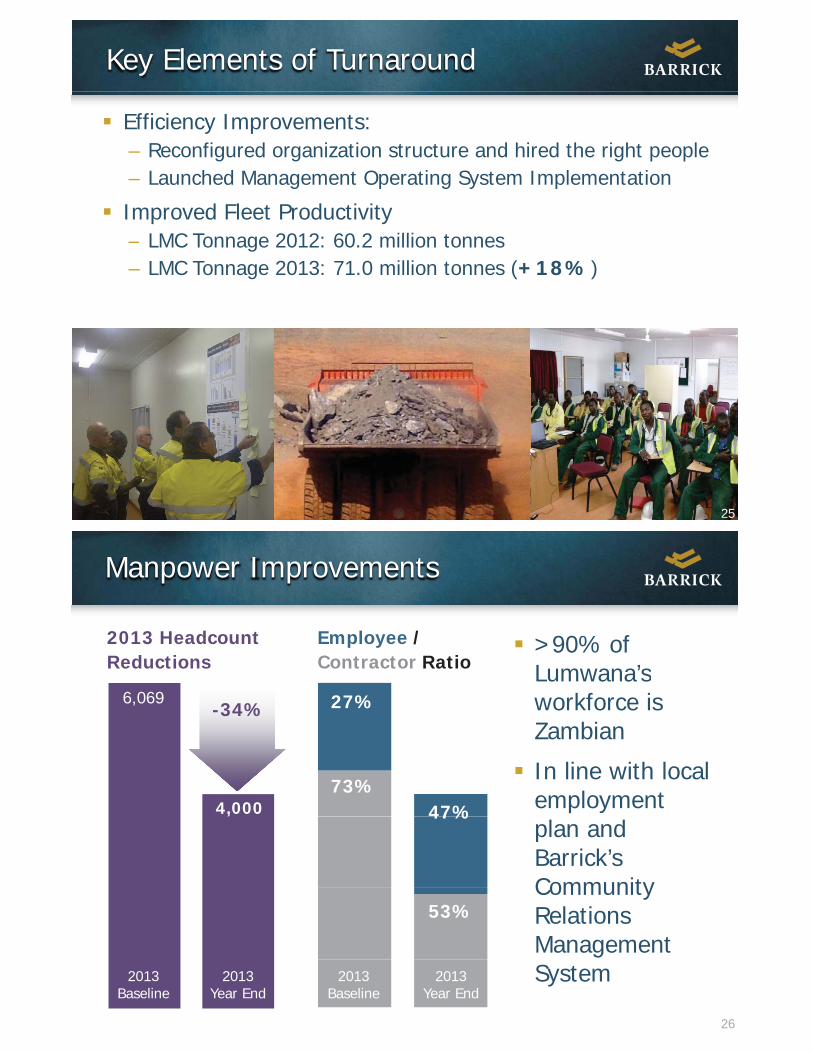

Key Elements of Turnaround

Efficiency Improvements: – Reconfigured organization structure and hired the right people– Launched Management Operating System Implementation

Improved Fleet Productivity LMC T 2012 60 2 illi t– LMC Tonnage 2012: 60.2 million tonnes

– LMC Tonnage 2013: 71.0 million tonnes (+18%)

2525

Manpower Improvements

>90% of Lumwana’s

2013 Headcount Reductions

Employee /Contractor Ratio Lumwana s

workforce is Zambian

6,069-34% 27%

In line with local employment 4,000

73%47%

plan and Barrick’sCommunity

, 47%

CommunityRelations Management

53%

26

System2013Year End

2013Baseline

2013Baseline

2013Year End

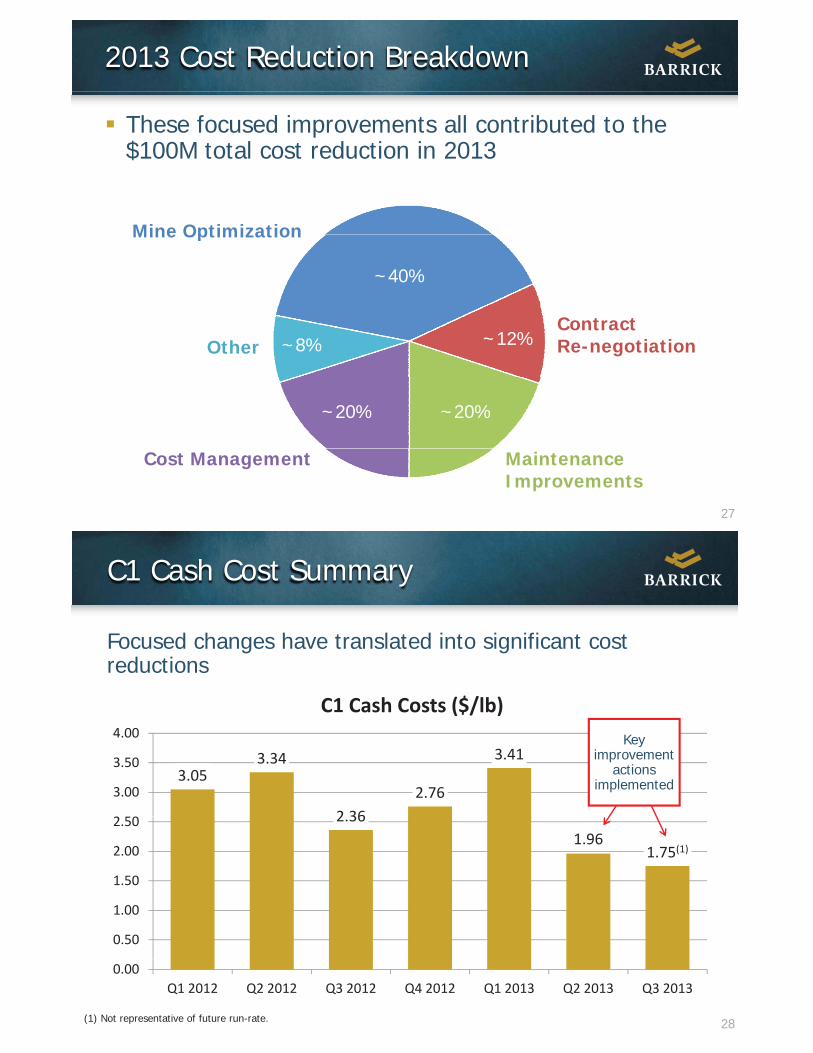

2013 Cost Reduction Breakdown

These focused improvements all contributed to the $100M total cost reduction in 2013

Mine OptimizationMine Optimization

~40%

ContractRe-negotiationOther ~8% ~12%

~20% ~20%

27

MaintenanceImprovements

Cost Management

C1 Cash Cost Summary

Focused changes have translated into significant cost reductions

4.00

C1 Cash Costs ($/lb)Key

3.053.34

2 362.76

3.41

3.00

3.50y

improvement actions

implemented

2.361.96

1.75(1)

1.50

2.00

2.50

0.50

1.00

28

0.00Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013

(1) Not representative of future run-rate.

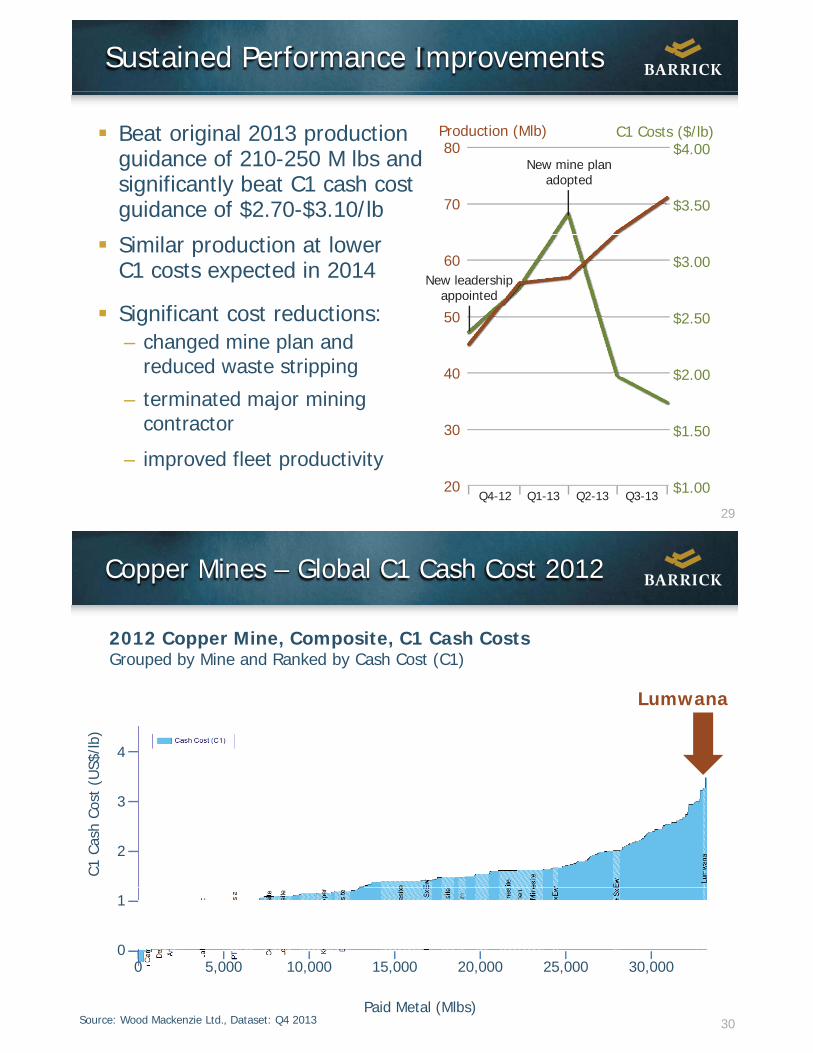

Sustained Performance Improvements

Beat original 2013 production guidance of 210-250 M lbs and $4.0080

C1 Costs ($/lb)Production (Mlb)

New mine planguidance of 210 250 M lbs andsignificantly beat C1 cash cost guidance of $2.70-$3.10/lb $3.5070

New mine planadopted

Similar production at lower C1 costs expected in 2014

Si ifi t t d ti

$3.0060New leadership

appointed

Significant cost reductions:– changed mine plan and

reduced waste stripping $2 00

$2.50

40

50

– terminated major mining contractor $1.50

$2.00

30

40

29

– improved fleet productivity$1.0020

Q4-12 Q1-13 Q2-13 Q3-13

Copper Mines – Global C1 Cash Cost 2012

2012 Copper Mine, Composite, C1 Cash CostsGrouped by Mine and Ranked by Cash Cost (C1)

b)

Lumwana

Cost

(U

S$/l

3

4

C1Ca

sh C

2

0

1

30Paid Metal (Mlbs)

Source: Wood Mackenzie Ltd., Dataset: Q4 2013

30,00025,00020,00015,00010,0005,0000

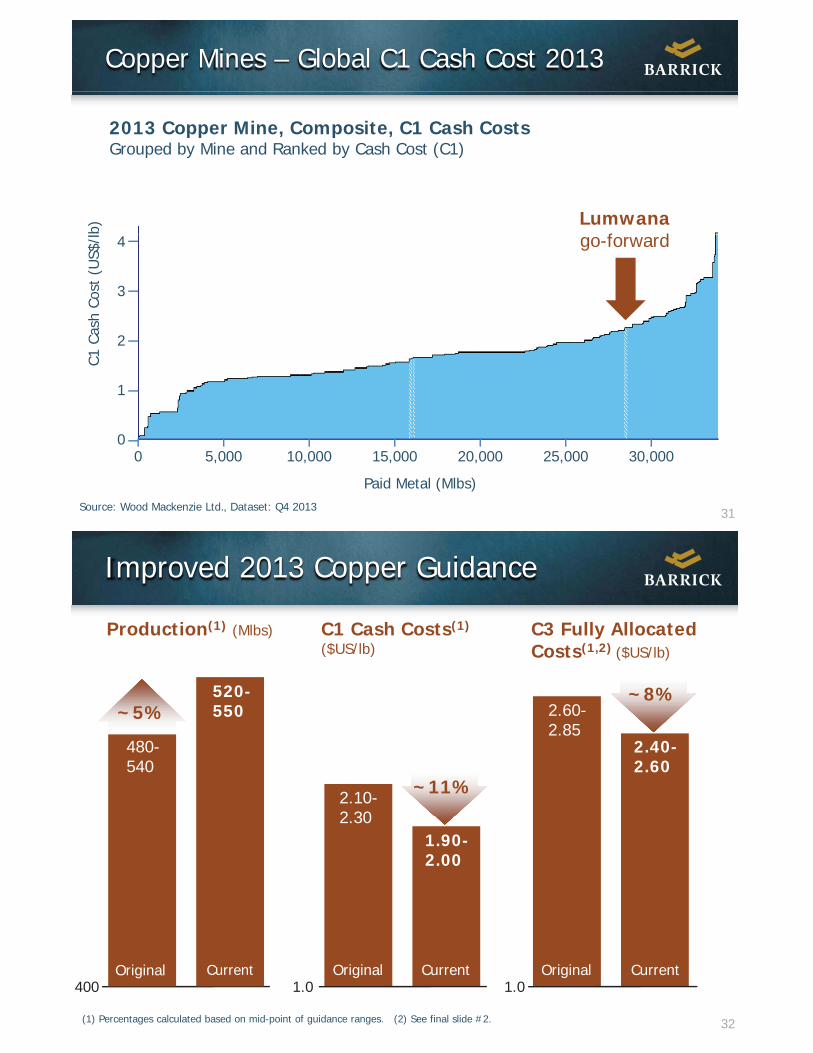

Copper Mines – Global C1 Cash Cost 2013

2013 Copper Mine, Composite, C1 Cash CostsGrouped by Mine and Ranked by Cash Cost (C1)

b)

Lumwanaf d

Cost

(U

S$/l

3

4 go-forward

C1Ca

sh C

2

0

1

31

Paid Metal (Mlbs)Source: Wood Mackenzie Ltd., Dataset: Q4 2013

30,00025,00020,00015,00010,0005,0000

Improved 2013 Copper Guidance

C1 Cash Costs(1)

($US/lb)C3 Fully Allocated Costs(1,2) ($US/lb)

Production(1) (Mlbs)

2 40

2.60-2.85

~8%520-550

480

~5%

2.10-2 30

~11%

2.40-2.60

480-540

1.90-2.00

2.30

32

1.0 1.0Original Current Original Current

400Original Current

(1) Percentages calculated based on mid-point of guidance ranges. (2) See final slide #2.

Lumwana Site Visit

33

Part II – Corporate Responsibility and Future OpportunitiesFebruary 5-6, 2014

Agenda

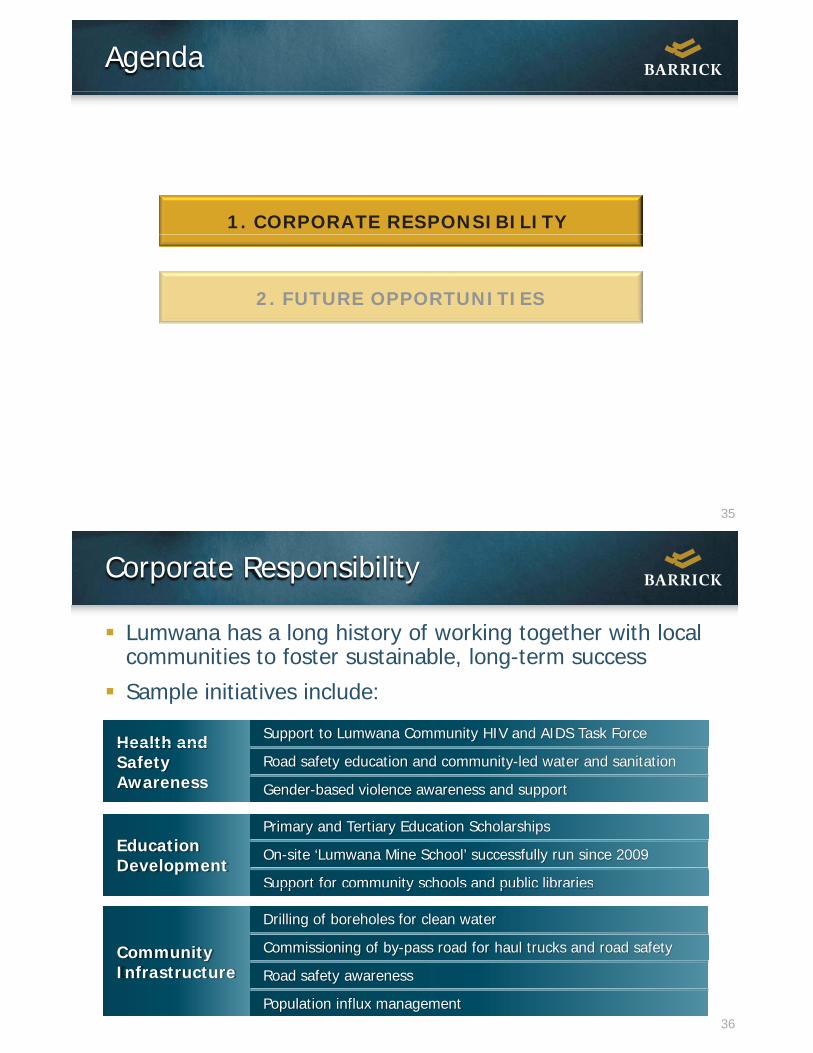

1. CORPORATE RESPONSIBILITY

2. FUTURE OPPORTUNITIES

34

Agenda

1. CORPORATE RESPONSIBILITY

2. FUTURE OPPORTUNITIES

35

Corporate Responsibility

Lumwana has a long history of working together with local communities to foster sustainable, long-term success

Sample initiatives include:

Health and Support to Lumwana Community HIV and AIDS Task ForceHealth andSafetyAwareness Gender-based violence awareness and support

Road safety education and community-led water and sanitation

EducationDevelopment

Primary and Tertiary Education Scholarships

Support for community schools and public libraries

On-site ‘Lumwana Mine School’ successfully run since 2009

Suppo t o co u ty sc oo s a d pub c b a es

Community

Drilling of boreholes for clean water

Commissioning of by-pass road for haul trucks and road safety

36

yInfrastructure Road safety awareness

Population influx management

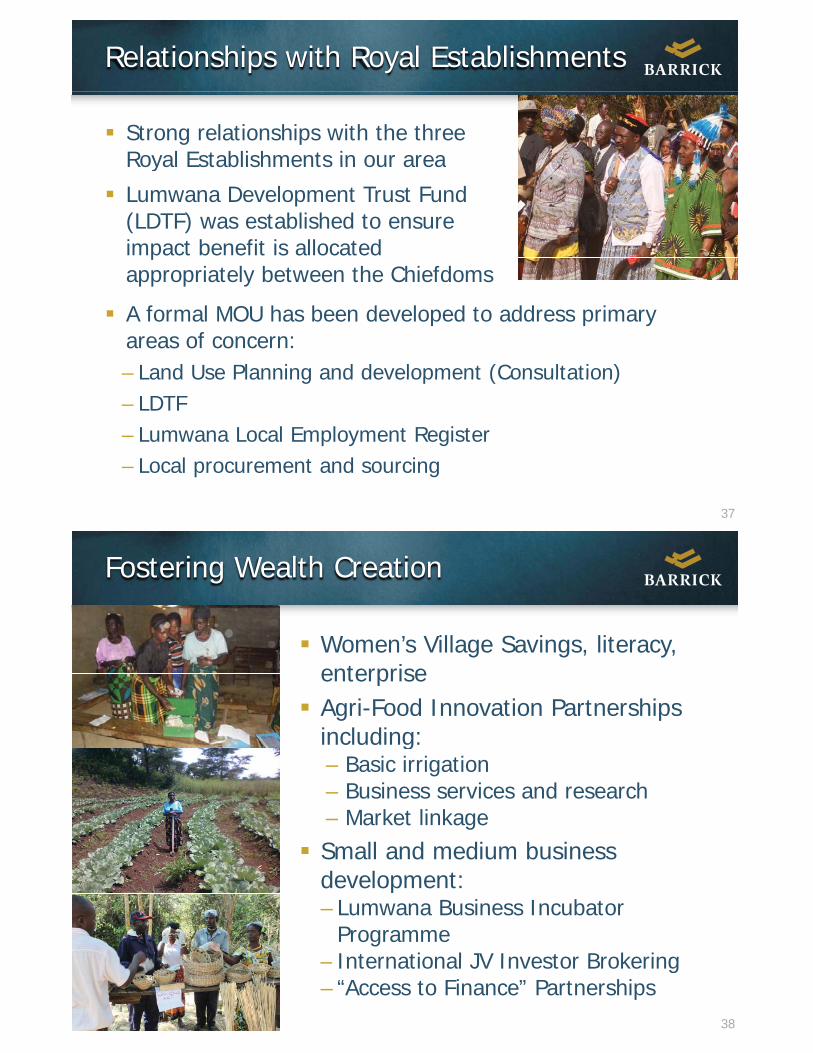

Relationships with Royal Establishments

Strong relationships with the three Royal Establishments in our areaRoyal Establishments in our area

Lumwana Development Trust Fund (LDTF) was established to ensure impact benefit is allocated appropriately between the Chiefdoms

A f l MOU h b d l d t dd iA formal MOU has been developed to address primaryareas of concern:– Land Use Planning and development (Consultation)Land Use Planning and development (Consultation)– LDTF– Lumwana Local Employment Register

37

– Local procurement and sourcing

Fostering Wealth Creation

Women’s Village Savings, literacy, enterpriseenterpriseAgri-Food Innovation Partnerships including:c ud g– Basic irrigation– Business services and research

Market linkage– Market linkageSmall and medium business development:development:– Lumwana Business Incubator

ProgrammeInternational JV Investor Brokering

38

– International JV Investor Brokering– “Access to Finance” Partnerships

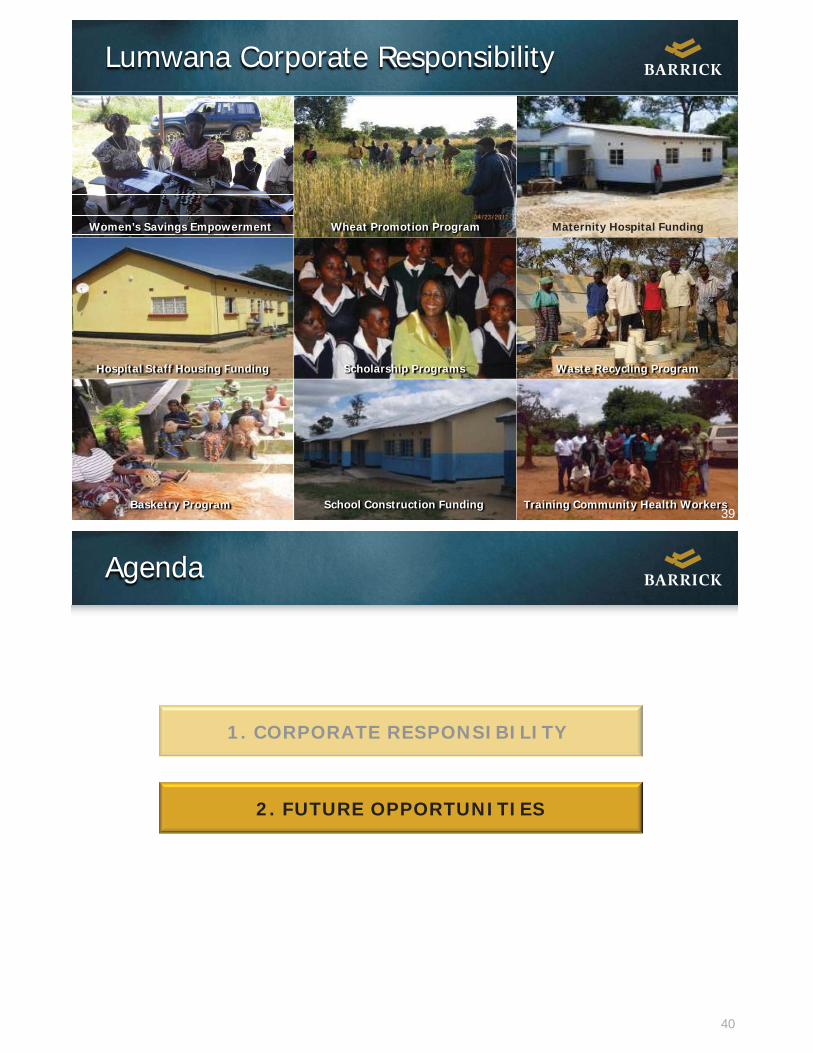

Lumwana Corporate Responsibility

Women’s Savings Empowerment Wheat Promotion Program Maternity Hospital Funding

Waste Recycling ProgramScholarship ProgramsHospital Staff Housing Funding

39Basketry Program School Construction Funding Training Community Health Workers

39

Agenda

1. CORPORATE RESPONSIBILITY

2. FUTURE OPPORTUNITIES

40

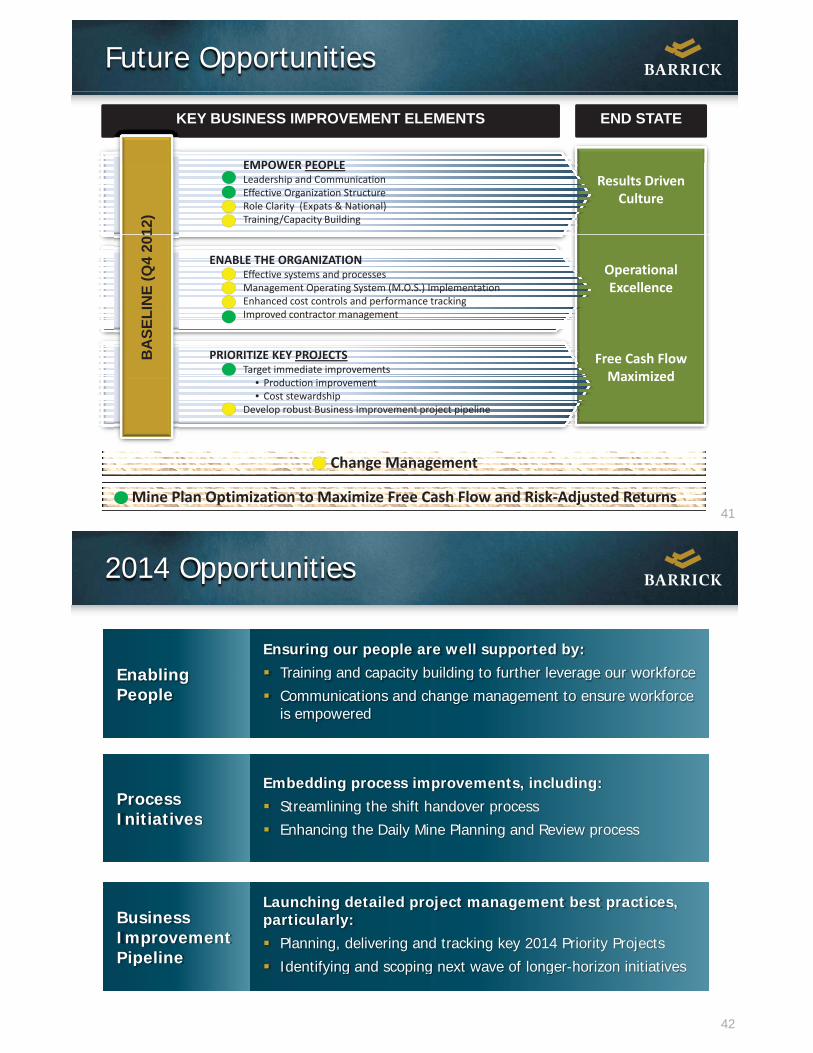

Future Opportunities

KEY BUSINESS IMPROVEMENT ELEMENTS END STATE

EMPOWER PEOPLEResults Driven

Culture

EMPOWER PEOPLELeadership and CommunicationEffective Organization StructureRole Clarity (Expats & National)Training/Capacity Building

12)

OperationalExcellence

ENABLE THE ORGANIZATIONEffective systems and processesManagement Operating System (M.O.S.) ImplementationEnhanced cost controls and performance trackingN

E (Q

4 20

1

Free Cash FlowMaximized

p gImproved contractor management

PRIORITIZE KEY PROJECTSTarget immediate improvements

BA

SELI

Maximized• Production improvement• Cost stewardship

Develop robust Business Improvement project pipeline

41Mine Plan Optimization to Maximize Free Cash Flow and Risk Adjusted Returns

Change Management

2014 Opportunities

EnablingEnsuring our people are well supported by:

Training and capacity building to further leverage our workforceEnablingPeople

Training and capacity building to further leverage our workforce

Communications and change management to ensure workforce is empowered

ProcessInitiatives

Embedding process improvements, including: Streamlining the shift handover process

InitiativesEnhancing the Daily Mine Planning and Review process

BusinessImprovementPipeline

Launching detailed project management best practices, particularly:

Planning, delivering and tracking key 2014 Priority Projects

42

Pipeline Identifying and scoping next wave of longer-horizon initiatives

Looking to the Future

Lumwana is a large deposit in a stable, mining-friendly jurisdictionfriendly jurisdiction

New mine plan maximizes free cash flow in the current price environment and preserves optionalityp p p y

Our goal is to continue to improve Lumwana’sproductivity and drive it further down the Global C1 p yCash Cost curve

The outlook for long term copper prices remains strong due to continued demand growth and supply-side challenges

43

Lumwana is very well positioned for the future

Appendix

COPPER MARKET OUTLOOK

44

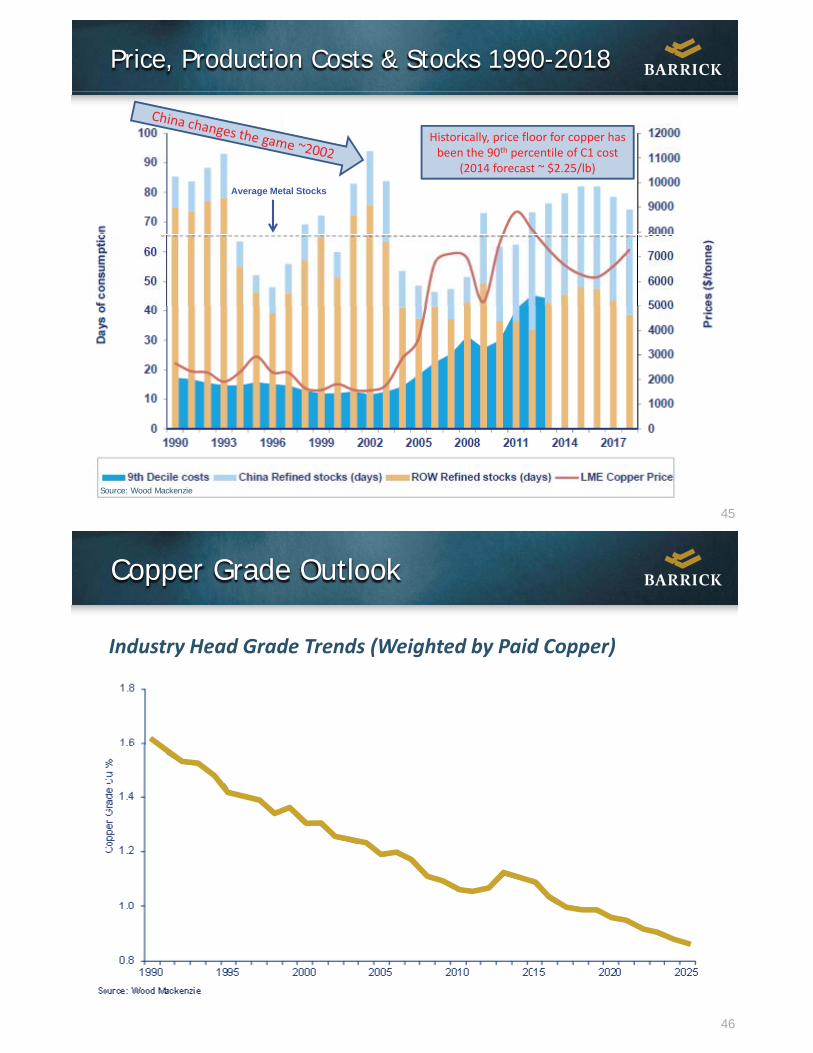

Price, Production Costs & Stocks 1990-2018

Historically, price floor for copper hasbeen the 90th percentile of C1 cost

( $ / )(2014 forecast ~ $2.25/lb)

Average Metal Stocks

45

Source: Wood Mackenzie

Copper Grade Outlook

Industry Head Grade Trends (Weighted by Paid Copper)

46

Positive Copper Outlook

Structural change in demand supported by urbanization of emerging markets, i.e. China/Indiaurbanization of emerging markets, i.e. China/IndiaIn the long term, the industry will be challenged to mount a sufficient supply response due to:– aging, lower grade mines and operational disruptions– dearth of new discoveries

project delays and development/permitting challenges– project delays and development/permitting challengeswith next generation of mines in riskier, more remote locations

Industry costs continue to rise– Chile produces 40% of the world’s copper and is

experiencing cost pressures for desalinated water energy

47

experiencing cost pressures for desalinated water, energyand labor

Footnotes

1. Calculated in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. For abreakdown of reserves and resources by category and additional information relating to reserves and resources, see pages25-35 of Barrick’s Form 40-F.

2. C1 cash costs per pound and C3 fully allocated cash costs per pound are non-GAAP financial performance measures with no t d di d d fi iti d IFRS S 44 49 f B i k’ Thi d Q t 2013 R tstandardized definition under IFRS. See pages 44-49 of Barrick’s Third Quarter 2013 Report.

48

![PDF [2.50 MB]](https://static.fdocuments.in/doc/165x107/586a8b9d1a28ab123a8b9c0a/pdf-250-mb.jpg)