PCAOB Audit Alert #11: New Internal Control Testing Standards & Excel

PCAOB Inspection FindingsPCAOB Audit Committee Dialogue

Auditor Assessment Toolkit

Doug MorallySenior Audit ManagerSeptember 14, 2015

2

Overview• PCAOB Inspection Findings

• PCAOB Audit Committee Dialogue

• Auditor Assessment Toolkit

3

PCAOB Inspection Findings• Inspections of over 650 audit firms• Annually inspect the largest firms

– BDO USA, LLP – Crowe Horwath LLP – Deloitte & Touche LLP – Ernst & Young LLP – Grant Thornton LLP – KPMG LLP – Malone Bailey, LLP– Marcum LLP – McGladrey LLP – PricewaterhouseCoopers LLP

4

Summary of DeficienciesBIG 4 vs. BIG 4

2015 2014Total Audits Inspected 213 213Total Audits with Deficiencies 70 79

33% 37%

AS-5Integrated audit of ICFR and Financial Statements 30% 31%

AU 342 Auditing Accounting Estimates 14% 8%AS-13 Auditors' Response to the RMM 13% 16%

AU 328Auditing FV Measurement and Disclosures 11% 8%

AS-14 Evaluating Audit Results 9% 8%AU 350 Audit Sampling 7% 9%AS-15 Audit Evidence 6% 4%

AU 329 Substantive Analytical Procedures 4% 6%Various Various 4% 6%AU 322 Auditors' Consideration of Internal Audit 1% 4%

5

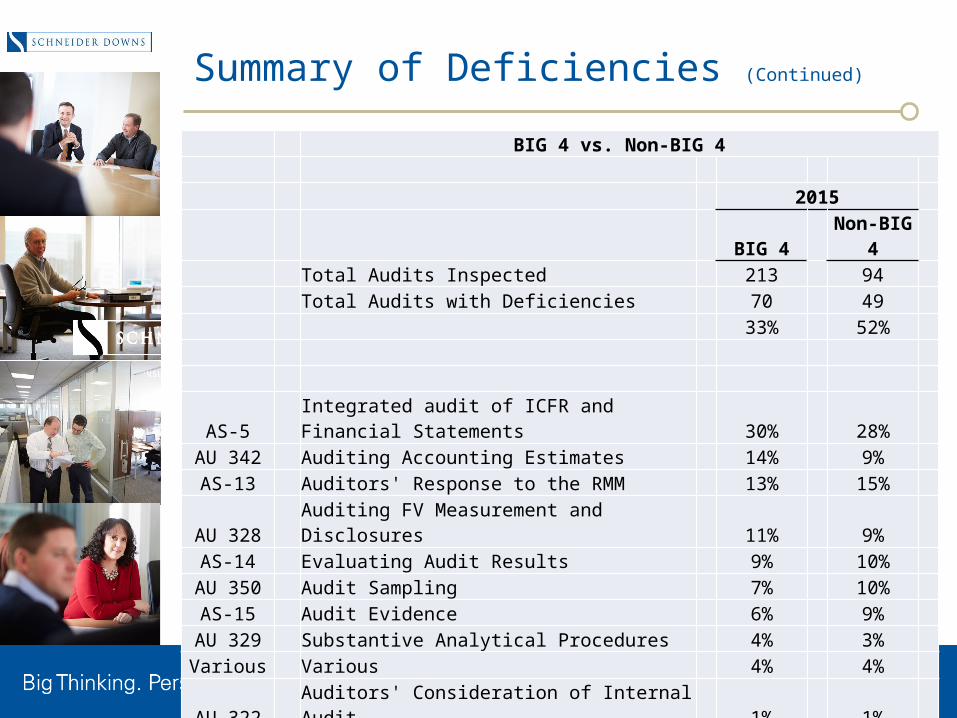

Summary of Deficiencies (Continued)

BIG 4 vs. Non-BIG 4

2015

BIG 4Non-BIG

4Total Audits Inspected 213 94Total Audits with Deficiencies 70 49

33% 52%

AS-5Integrated audit of ICFR and Financial Statements 30% 28%

AU 342 Auditing Accounting Estimates 14% 9%AS-13 Auditors' Response to the RMM 13% 15%

AU 328Auditing FV Measurement and Disclosures 11% 9%

AS-14 Evaluating Audit Results 9% 10%AU 350 Audit Sampling 7% 10%AS-15 Audit Evidence 6% 9%

AU 329 Substantive Analytical Procedures 4% 3%Various Various 4% 4%AU 322 Auditors' Consideration of Internal Audit 1% 1%

6

PCAOB Audit Committee Dialogue

• Inspectors consider two broad questions:– What recurring audit concerns identified

in past inspections are expected are expected to continue to be significant?

– What emerging risks might require increased focus by auditors and audit committees in the future?

• Key Recurring Areas of Concern• New Risks PCAOB is Monitoring

7

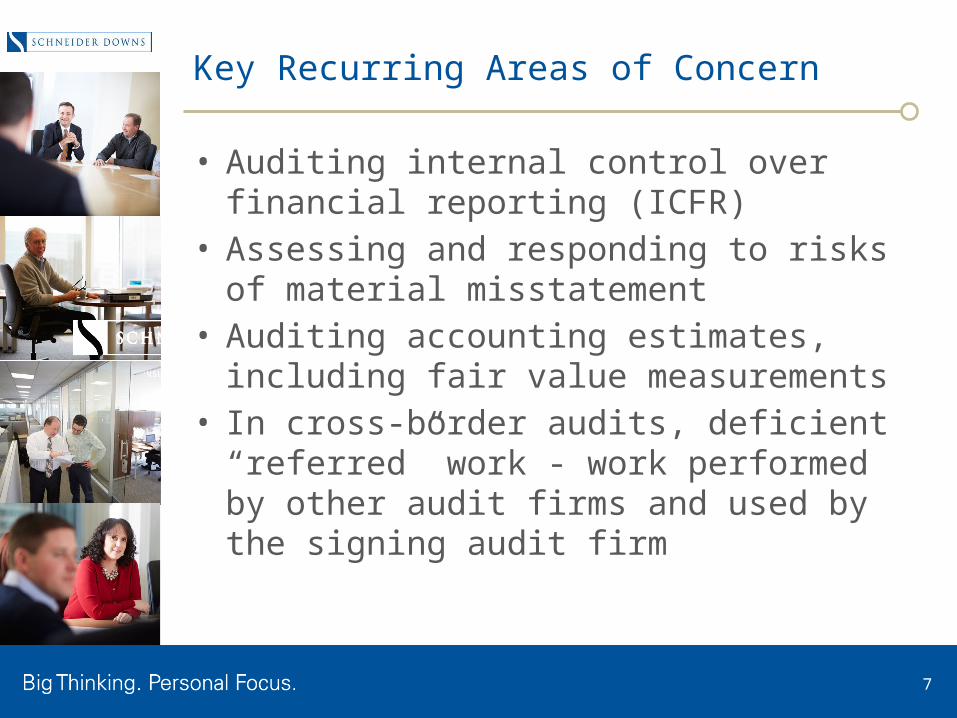

Key Recurring Areas of Concern• Auditing internal control over

financial reporting (ICFR)• Assessing and responding to risks of

material misstatement• Auditing accounting estimates,

including fair value measurements• In cross-border audits, deficient

“referred” work - work performed by other audit firms and used by the signing audit firm

8

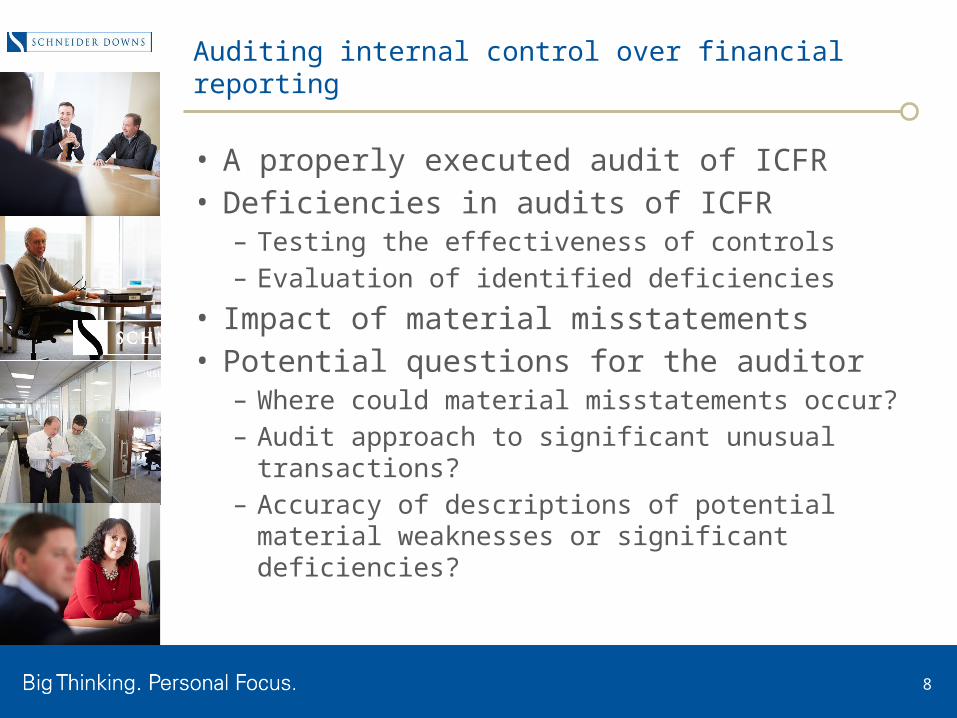

Auditing internal control over financial reporting

• A properly executed audit of ICFR• Deficiencies in audits of ICFR

– Testing the effectiveness of controls– Evaluation of identified deficiencies

• Impact of material misstatements• Potential questions for the auditor

– Where could material misstatements occur?– Audit approach to significant unusual

transactions?– Accuracy of descriptions of potential material

weaknesses or significant deficiencies?

9

Assessing and responding to risks of material misstatement

• Identification of risks or responding effectively to existing risks

• PCAOB insights based on experience of deficiencies identified:– When risks change, audit plans should change– Insufficient audit procedures at certain locations or

business segments• Potential questions for the auditor

– Significant audit areas with risks of material misstatement?

– How have risk areas changes since the prior year?– Address the risks in a multi-location environment?– Identification of specific risks in countries

experiencing political instability?

10

Auditing estimates, including fair value measurements, and disclosures

• Audit deficiencies identified in areas such as revenue, inventory reserves, fair value measurements and tax-related estimates

• Identification and evaluation of indicators of asset impairments

• Potential questions for the auditor– What is the auditors’ approach to auditing

critical estimates?– Assessment of all separate intangible assets

when assessing goodwill for possible impairment?

– Will the engagement team use the firm’s in-house valuation specialists?

11

Referenced work in cross-border audits

• Quality of the referred work• PCAOB found significant problems in

over 40% of referred work engagements at non-US member firms

• Potential questions for the auditor– How does the engagement partner assess

the quality of the audit work performed in other jurisdictions?

– Were the firms participating in the audit recently inspected by the PCAOB?

– How does your auditor review the work?

12

New Risks the PCAOB is Monitoring

• Increase in mergers & acquisitions• Falling oil prices• Undistributed foreign earnings• Maintaining audit quality while

growing other businesses

13

Auditor Assessment Toolkit• Role of the audit committee• Assessment Process– Draw upon prior experience– Observations from management and

internal audit– Private meetings between committee

chair and engagement partner– Review of regulator inspection reports

and peer review findings– Communication of process with

shareholders

14

Evaluation of the auditor• Quality of services and sufficiency of

resources provided by the auditor• Communication and interaction with

the auditor• Auditor independence, objectivity,

and professional skepticism• Obtaining input from company

personnel about the external auditor

15

Quality of services and sufficiency of resources provided by the auditor

• Assessment of the primary members of the audit engagement team– Demonstrated skills and experience to address

financial reporting risk– Access to appropriate specialists– Provide a sound risk assessment at the onset of

the audit– Demonstrated a good understanding of the

company’s business, industry and economic environment

– Audit responses to auditing and accounting issues• Quality of the audit in various domestic

locations or in other countries

16

Quality of services and sufficiency of resources provided by the auditor (continued)

• Firm’s relevant industry expertise• Geographical reach necessary to

serve the company• Results of the firms’ most recent

inspection results of the PCAOB and peer review

17

Communication and interaction with the auditor

• Quality of communications• Frequency of discussions• Communications should focus on

accounting and auditing issues• Required communications under

PCAOB standards and SEC rules• Communications held with

management present or in executive session

18

Auditor independence, objectivity, and professional skepticism

• Communication to the committee that the auditor is independent

• Auditor’s evaluation of the methods and assumptions used by management

• Auditor’s responses to open-ended questions from the committee– Financial reporting challenges of the

company– Changes in accounting methods– Key assumptions underlying critical estimates– Accounting issues discussed with

management

19

Obtaining input from company personnel about the external auditor

• Responsiveness and communicative

• Proactively identifies opportunities and risks

• Delivers value for the money• Assigned sufficient resources to

complete work in a timely manner• Forthright in dealing with difficult

situations

20

Contact InformationDouglas J. Morally, CPASenior Audit ManagerSchneider Downs & Co., Inc.One PPG Place, Suite 1700Pittsburgh, PA 15222-5416

Direct Phone: 412.697.5389

Email: [email protected]

21

Questions?