PBGP Disallowances An insight of the Indian Tax Laws · PDF fileIncome-tax Act, 1961 PBGP...

46

Income-tax Act, 1961 PBGP Disallowances An insight of the Indian Tax Laws

-

Upload

nguyendien -

Category

Documents

-

view

225 -

download

6

Transcript of PBGP Disallowances An insight of the Indian Tax Laws · PDF fileIncome-tax Act, 1961 PBGP...

Income-tax Act, 1961

PBGP Disallowances

An insight of the Indian Tax Laws

Income-tax Act, 1961

Contents

Slide 2May 2014PGBP Disallowances

Income-tax Act, 1961

Introduction

Slide 3May 2014PGBP Disallowances

Income-tax Act, 1961

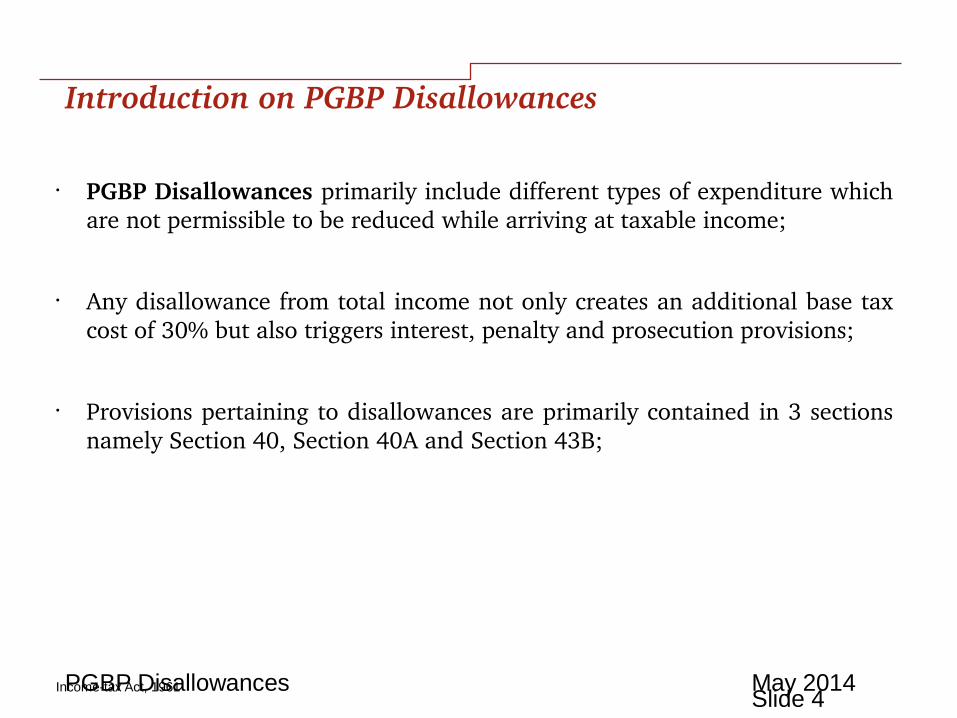

Introduction on PGBP Disallowances

• PGBP Disallowances primarily include different types of expenditure which are not permissible to be reduced while arriving at taxable income;

• Any disallowance from total income not only creates an additional base tax cost of 30% but also triggers interest, penalty and prosecution provisions;

• Provisions pertaining to disallowances are primarily contained in 3 sections namely Section 40, Section 40A and Section 43B;

Slide 4May 2014PGBP Disallowances

Income-tax Act, 1961

Analysis of the provisions with relevant jurisprudence

Slide 5May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 – Amounts not deductible

Slide 6May 2014PGBP Disallowances

Income-tax Act, 1961

Analysis of Section 40

Ø Section 40 imposes restrictions on the allowability of certain expenses and is in the nature of an exception to sections 30 to 38 – It overrides the provisions of sections 30 to 38;

Ø Introduced with a view to bring together provisions regarding certain inadmissible items;

Ø Clause (a) of this section applies to all assessees; Clause (b) applies to firms; Clause (ba) to association of persons or body to individuals.

Slide 7May 2014PGBP Disallowances

Income-tax Act, 1961

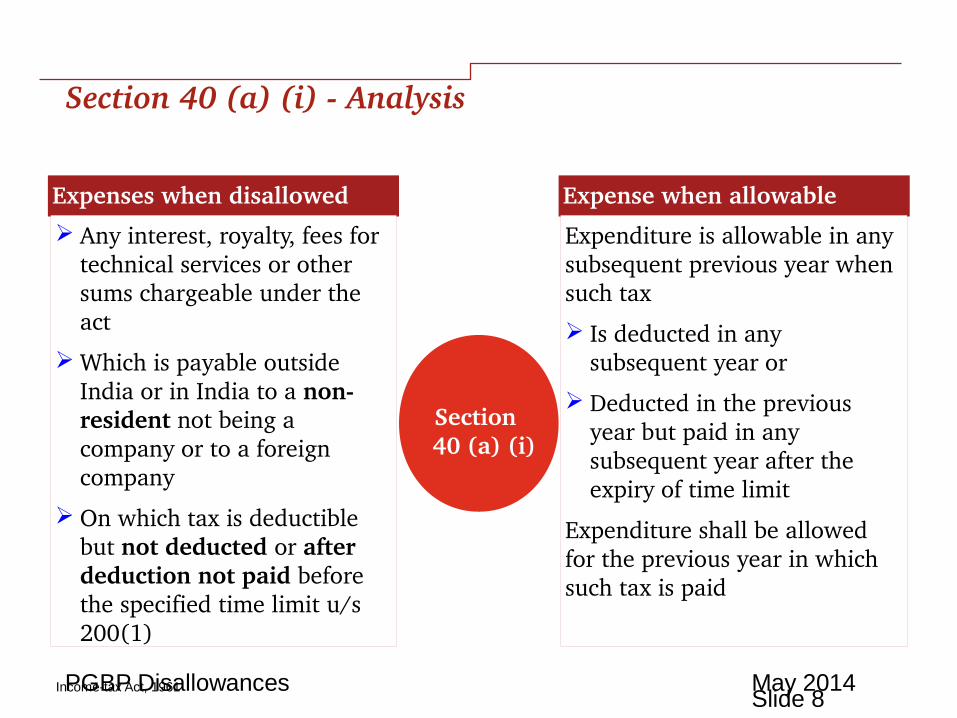

Section 40 (a) (i) Analysis

Expenses when disallowed

Ø Any interest, royalty, fees for technical services or other sums chargeable under the act

Ø Which is payable outside India or in India to a nonresident not being a company or to a foreign company

Ø On which tax is deductible but not deducted or after deduction not paid before the specified time limit u/s 200(1)

Expense when allowable

Expenditure is allowable in any subsequent previous year when such tax

Ø Is deducted in any subsequent year or

Ø Deducted in the previous year but paid in any subsequent year after the expiry of time limit

Expenditure shall be allowed for the previous year in which such tax is paid

Section 40 (a) (i)

Slide 8May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (i) Judicial Precedents

Ø DIT ( IT). v.Cargil TSF PTE Ltd. (2013) 212 Taxman 16 (Delhi) (HC)

Discount charges earned by assessee (financial service provider) by way of discounting bill of exchange and promissory notes in favor of Indian companies is to be treated as business income, and not as interest income, hence provisions of section 40(a) (i) cannot be applied.

Ø ACIT .v. Bank of India (2013) 59 SOT 102 (Mum.)(Trib.)

Assessee claimed deduction for fees paid to Master Card International outside India which was disallowed on ground that no tax had been deducted at source. The assessee claimed that payee had paid tax on said payment and accordingly, deduction should be allowed. However, in the absence of any evidence that payee had paid taxes on amount received from assessee, deduction could not be allowed.

Slide 9May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (i) Judicial PrecedentsSu

bsid

iary

I. Co. [Taxpayer]

Ø C.U. Inspections (I) Pvt. Ltd .v. DCIT (2013)142 ITD 761/156 TTJ 690 (Mum.)(Trib.)

The Tribunal held that § Reimbursement of expenses to

holding company Not an income under the Act and hence not chargeable to tax.

§ Expenses routed through holding company for payment to third party Not in the nature of reimbursement of expenses and liable to withholding as if assessee has made payment to such independent third party.

Slide 10March 2014

F. Co. [Netherlands]

Made following payments without deducting tax Ø Payments incurred by F.

Co. on behalf of tax payer

Ø Payments for training services availed by I. Co. from independent third party, routed through parent Co.

PGBP Disallowances

Income-tax Act, 1961

• Disallowance of amount paid/payable

•Sikandarkhan N. Tunvar [2013] 357 ITR 312 (Gujarat HC)

• Crescent Export Syndicate [2013] 262 CTR 525 (Calcutta HC)

• CBDT Circular No. 1/2014 dated 13th January 2014

Disallowance of amount payable

•Vector Shipping Services Pvt. Ltd. [2013] 357 ITR 642 (Allahabad HC)

• Merilyn Shipping & Transports [2012] 16 ITR(T) [Visakhapatnam Trib. (SB)]

Section 40 (a) (i) Judicial Precedents

Slide 11May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (ia) Analysis

Expenses when disallowed

Ø Any sum payable to a resident assessee in the nature of interest, commission, brokerage, rent, royalty, fees for technical services and fees for professional services or

Ø Amounts payable to a resident contractor or sub contractor

Ø On which tax is deductible but not deducted or after deduction not paid before the due date for filing return u/s 139 (1)

Expense when allowable

Expenditure is allowable in any subsequent previous year when such tax

Ø Is deducted in any subsequent year or

Ø Deducted in the previous year but paid in any subsequent year after the expiry of time limit

Expenditure shall be allowed for the previous year in which such tax is paid

Section 40 (a) (ia)

Slide 12May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (ia) – Judicial Precedents

May 2014PGBP DisallowancesSlide 13

No disallowanceØ CIT v. S K Tekriwal [TS902

HC2012(Cal)]Ø DCIT v. M/s Chandabhoy &

Jassobhoy [2012] 49 SOT 448 (Mum Trib.)

Ø UE Trade Corp. (India) Ltd. v. DCIT [2012] 54 SOT 596 (Delhi Trib.)

Disallowance/ Proportionate disallowanceØ Frontier Offshore Exploration (India) Ltd. v. DCIT [2009] (118 ITD 494) [Chennai Trib.]Ø Position taken by Revenue in many cases at assessment stage

Ø Absence of the expression “the whole or any part of the tax” in section 40 as used in section 201 – mandate under section 40 is deduction of taxØThe view to be accepted if the shortfall is due to any difference of opinion as to which TDS provision would get triggered [bonafide reasons]

ØSection 40 uses the expression “tax deductible under Chapter XVIIB” which would include section 201 Ø The view to be accepted when short deduction occurs for non bonafide reasons

Short deduction of tax

Income-tax Act, 1961

Consequences for non deduction of tax at source

May 2014PGBP DisallowancesSlide 14

Income-tax Act, 1961

Amendment by Finance Act 2012

Relaxation of Disallowance u/s 40 (a) (ia)

Ø Where the assessee fails to deduct whole or part of the tax

Ø On any such sum but is not deemed to be an assessee in default under first proviso to 201(1), then

Ø For the purpose of 40 (a) (ia), it shall be deemed that assessee has deducted and paid the tax on the date of furnishing ROI by the resident payee referred to in the said proviso

Deemed Compliance of section 201 (1)

Ø Any person [payer] who fails to deduct whole or part of the tax on the sum paid/credited to a resident payee,

Ø Shall not be deemed to be an assessee in default if such resident [payee]: Has furnished ROI u/s 139 Has considered such sum for computing his income Has paid tax due on the income declared Furnishes a certificate to this effect from an accountant

The benefit does not apply to Nonresident payments u/s 40 (a)(i) or 40(a)(iii)

Amendment by Finance Act 2012 : Effective from AY 201314

Slide 15May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (ic)/(ii)/(iia) Analysis

Section 40 (a)(ic)

Any sum paid on account of Fringe Benefit Tax

#Fringe Benefit tax has been withdrawn with effect from AY 201011

Section 40 (a) (ii)

Rates or taxes levied onprofits or gains of any business or profession.

Taxes not deductible Incometax Other payments under the Act like Interest Foreign Incometax

Taxes which are deductible Excise duty Sales tax Service tax

Section 40 (a)(iia)

Wealth Tax paid under the Wealth Tax Act and Tax of similar nature chargeable in any foreigncountry

# Interest under the Wealthtax Act is required to be paid by an assessee on account of delayed payment on the demand of wealth tax and partakes the character of the wealth tax itself.

Slide 16May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (iib) – Inserted by Finance Act 2013

Any amountØ Being royalty, licence fee, service fee, privilege fee, service charge or any other fee or

charge by whatever name called, which is levied exclusively on; orØ Which is appropriated, directly or indirectly, from,

a State Government undertaking by the State Government

A State Government undertaking includes

i. Corporation established by or under any Act of the State Government [‘SG’];

ii. A company in which more than 50% of the paidup equity capital is held by the SG;

iii. A company in which more than 50% of the paidup equity capital is held by the entity referred to in clause (i) or clause (ii) [whether singly or taken together];

iv. A company /corporation in which the SG has the right to appoint the majority of directors/control management/policy decisions, directly/indirectly inc. by virtue of its management rights, shareholding, etc

v. An authority, a board or an institution or a body established or constituted by or under any Act of the SG or owned/controlled by the SG

Slide 17May 2014PGBP Disallowances

Income-tax Act, 1961

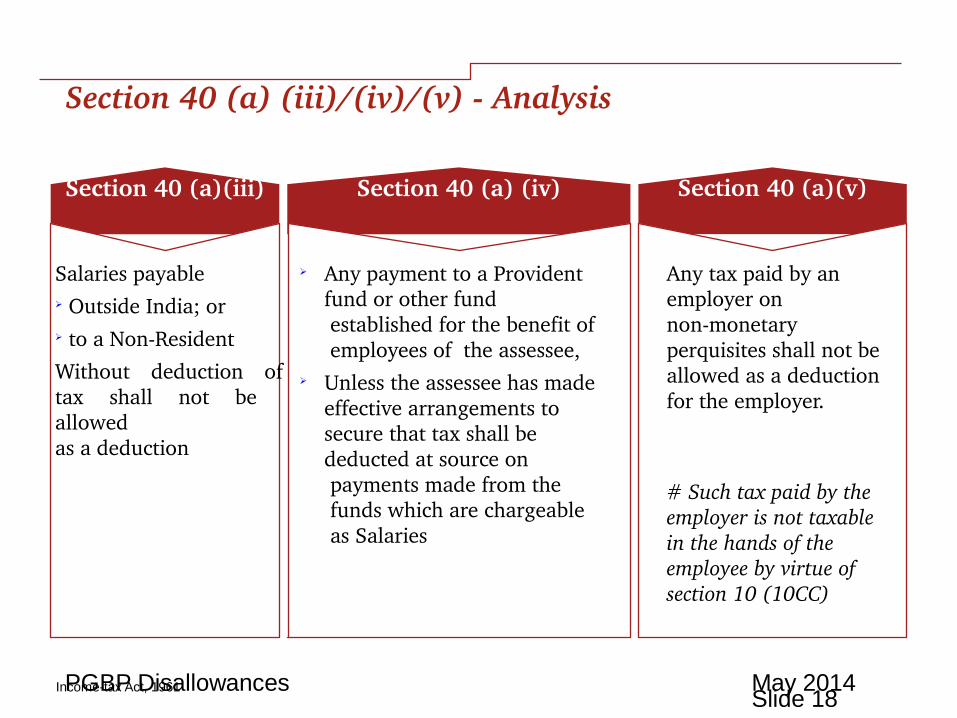

Section 40 (a) (iii)/(iv)/(v) Analysis

Section 40 (a)(iii)

Salaries payable Ø Outside India; orØ to a NonResident

Without deduction oftax shall not be allowedas a deduction

Section 40 (a) (iv)

Ø Any payment to a Provident fund or other fund established for the benefit of employees of the assessee,

Ø Unless the assessee has made effective arrangements to secure that tax shall be deducted at source on payments made from the funds which are chargeable as Salaries

Section 40 (a)(v)

Any tax paid by an employer on nonmonetary perquisites shall not be allowed as a deductionfor the employer.

# Such tax paid by the employer is not taxablein the hands of the employee by virtue of section 10 (10CC)

Slide 18May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (a) (iii) – Judicial Precedents

Ø Tianjin Tianshi India (P.) Ltd. v. ITO (2013) 59 SOT 111 (Delhi)(Trib.)

Where tax deducted at source on salary payable outside India is paid on or before due date for filing return specified under section 139(1), it cannot be disallowed under section 40(a)(iii). Where tax deducted at source is paid after due date specified under section 139(1), such sum shall be allowed as deduction in previous year in which such tax has been paid. (AY.200708)

Slide 19May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (b) Analysis

Payment of Interest and Remuneration to partners of a Firm

• Remuneration or salary to a nonworkingpartner shall not be allowed as a deduction

• Remuneration to workingpartners & interest to any partner shall beallowed only if it isauthorised by the partnership deed

• Remuneration/interest paid for a period prior to the date of authorization by the deed shall not be allowable

Remuneration/Interest Limits

Ø Maximum interest on partner’s capital shall be restricted to 12%. However if the rate as per deed is less, then interest shall be allowed to such extent

Ø Remuneration to working partners shall be subject to following limits:

The limit u/s 40(b) provide for the maximum allowable remuneration and interest.

If the remuneration as per books is lower than 40(b) limit, such lower amount shall be regarded as allowable deduction. Inother words allowable remuneration/ interest shall be lower of:

Ø Remuneration/interest as per books

Ø Limits as per section 40(b)

Book Profit Maximum Limit

First 3 lacs of book profit

Rs. 1,50,000 or 90% of book profit, whichever is higher

Balance of book profit

60% of book profit

Slide 20May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (b) – Other points

Key Notes

Interest paid to representative partners

Where an individual (say A) ia a partner in a firm on behalf of and for the benefit of any other person (say B), then:Ø Interest paid to the representative partner

(A) in his individual capacity (i.e. not in the capacity of a representative partner) shall not be considered for the purpose of 40(b)

Ø However, interest paid to the representative partner (A) in his capacity as such and to the person so represented (B) shall be covered for 40(b)

Ø Where an individual partner (say C) receives interest on behalf and for the benefit of any other person, restriction u/s 40(b) shall not operate provided the representative (C) is not a partner in his individual capacity

Ø Working partners refers to an individual partner actively engaged in conducting the affairs of the business/profession of the firm

Ø Partnership deed must specify the amount of remuneration to be allowed or the manner in which remuneration is to be computed, for it to be allowed as a deductible expense

Ø Book Profit :Net Profit computed as per Chapter IV D(+) Remuneration paid/payable to partners(if already deducted while computing Net Profit)

Slide 21May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (b) – Judicial Precedents

Ø CIT v. Great City Manufacturing Co. (2013) 351 ITR (All) (HC)

While considering the provisions of section 40(b) (v) read with section 40A(2) (a), the Court held that the Assessing Officer is only required to see whether the partners are the working partners mentioned in the partnership deed, the terms and conditions of the partnership deed provide for payment of remuneration to the working partners and whether the remuneration provided is within the limits prescribed under section 40(b) (v). If all the conditions are fulfilled he cannot disallow any part of the remuneration on the ground that it is excessive.

Slide 22May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (b) – Judicial Precedents

ØSood Brij & Associates vs. CIT [2011] 15 taxmann.com 76 (DELHI)

Partnership Deed must quantify or lay down the manner of quantifying remuneration to partners. Where the deed stated that the working partners would be paid such remuneration as may be mutually agreed upon subject to the ―provisions of the Act, it was held that the deed did not specifically provide for remuneration and hence no remuneration is allowable u/s 40(b)

However, a converse rationale was upheld in the case of Durga Dass Devki Nandan vs. ITO [2011] 12taxmann.com 156 (HP) where it was held that a provision in the deed that “remuneration would be as per the Act” was sufficient for section 40(b)(v)

Slide 23May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40 (ba) Analysis

Slide 24May 2014PGBP Disallowances

Income-tax Act, 1961

Section 4oA– Expenses or payments not deductible in certain circumstances

Slide 25May 2014PGBP Disallowances

Income-tax Act, 1961

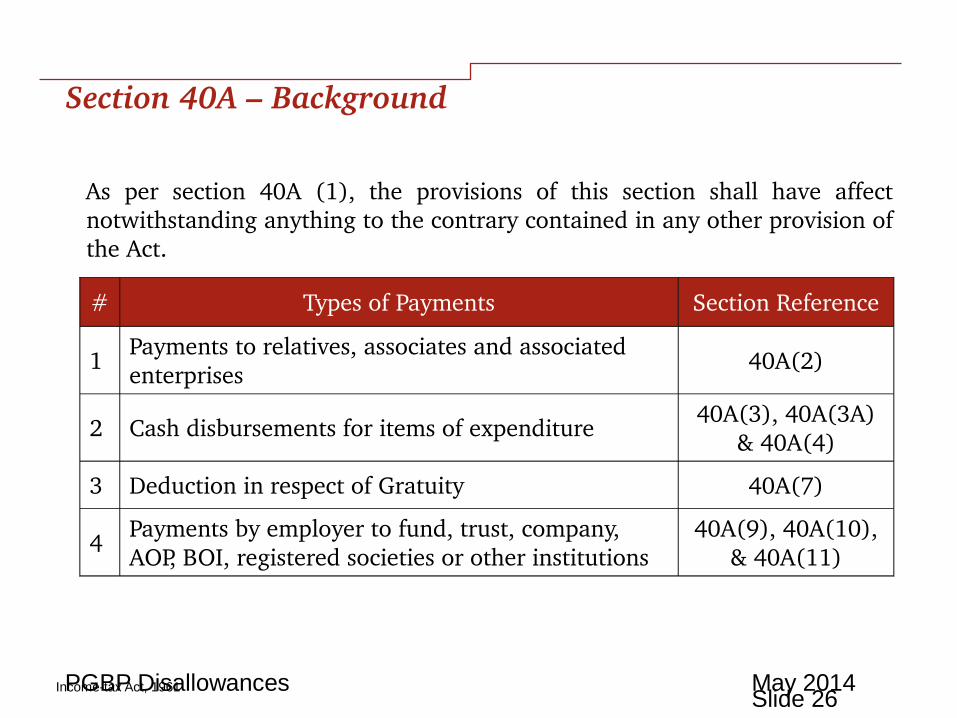

Section 40A – Background

As per section 40A (1), the provisions of this section shall have affect notwithstanding anything to the contrary contained in any other provision of the Act.

# Types of Payments Section Reference

1Payments to relatives, associates and associated enterprises 40A(2)

2 Cash disbursements for items of expenditure40A(3), 40A(3A)

& 40A(4)

3 Deduction in respect of Gratuity 40A(7)

4 Payments by employer to fund, trust, company, AOP, BOI, registered societies or other institutions

40A(9), 40A(10), & 40A(11)

Slide 26May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(2)(a) Analysis

ØFair market value of the goods/services/facilities, orØLegitimate needs of the business/profession, orØBenefit derived/accruing from such expenditure

The AO shall disallow so much of the expenditure as is considered by him to be excessive or unreasonable

Slide 27May 2014PGBP Disallowances

Income-tax Act, 1961

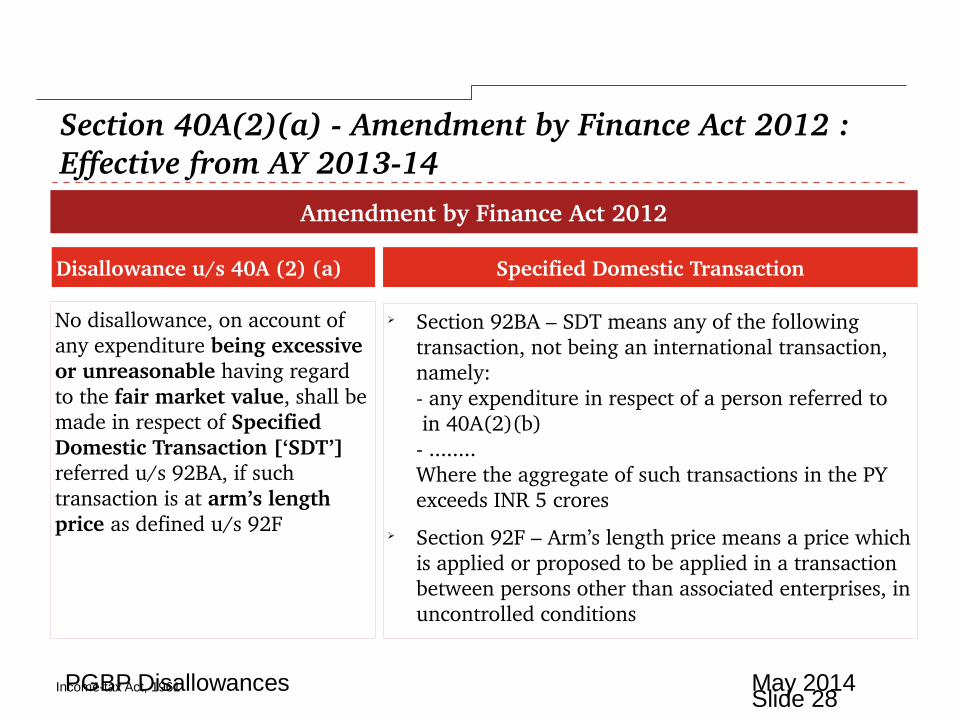

Amendment by Finance Act 2012

Disallowance u/s 40A (2) (a)

No disallowance, on account of any expenditure being excessive or unreasonable having regard to the fair market value, shall be made in respect of Specified Domestic Transaction [‘SDT’] referred u/s 92BA, if such transaction is at arm’s length price as defined u/s 92F

Specified Domestic Transaction

Ø Section 92BA – SDT means any of the following transaction, not being an international transaction, namely: any expenditure in respect of a person referred to in 40A(2)(b) ........Where the aggregate of such transactions in the PY exceeds INR 5 crores

Ø Section 92F – Arm’s length price means a price which is applied or proposed to be applied in a transaction between persons other than associated enterprises, in uncontrolled conditions

Section 40A(2)(a) Amendment by Finance Act 2012 : Effective from AY 201314

Slide 28May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(2)(a) Amendment by Finance Act 2012 : Effective from AY 201314

May 2014PGBP DisallowancesSlide 29

Mr. A purchases RM from his brother [specified person] for Rs. 10L

Income-tax Act, 1961

Section 40A(2)(b) Analysis

Assessee Specified Person – Section 40A(2)(b)

Individual

Ø Any relative of such individualØ Any person in whose business/profession, the individual or his

relatives have substantial interest

Note: Relatives includes spouse, brother, sister and lineal ascendant or descendant of the individual – section 2(41)

Company, Firm, AoP and HUF

Ø Any director of the company, partner of the firm, member of an AoP or family

Ø Any relative of such director, partner or memberØ Any person in whose business or profession the assessee or such

director, partner or member or any relative of such persons have substantial interest

Slide 30May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(2)(b) Analysis

Assessee Specified Person – Section 40A(2)(b)

All Assessees

Ø Any individual having substantial interest in the business or profession of the assessee

Ø Any relative of such individual

Ø Any company, firm , AoP or HUF§ One of whose directors/ members/ partners have

substantial interest in the business of the assessee§ any other director, member or partner§ any relative of such other director, member or partner

Ø Any company, firm, AoP or HUF§ Having substantial interest in the business or profession of

the assessee§ Any director, partner or member of such person§ Any relative of such director, partner or member

Slide 31May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(2)(b) – Amendment by Finance Act 2012

Slide 32May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(2)(b) – Analysis

Substantial Interest

In the case of a Company In any other Case

At least 20% of equity capital (share with voting rights, not entitled to fixed rate of dividend and with or without the right to participate in profits)

At least 20% of share in profits

Slide 33May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(3) read with rule 6DD – Disallowance of expenditure in excess of Rs. 20,000

Any expenditure Ø In respect of which payment in excess of Rs. 20,000 is made to a person in a dayØ Otherwise than by account payee cheque or account payee demand draft Ø Entire expenditure shall be disallowed

Rule 6DD Exceptions to the above general rule

i. Payments to Government / RBI;

ii. Payments by way of an arrangement•. Letters of credit through a bank•. Book adjustment between accounts in banks•. Bills of exchange payable to a bank•. Use of electronic clearing system through a bank account•. Book adjustment of a receivable and payable

iii. Payments required to be made on bank holiday / strike

iv. Payments made through agents who is required to make cash payments for goods and services purchased on behalf of such person.

Slide 34May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(7) Analysis

Slide 35May 2014PGBP Disallowances

Income-tax Act, 1961

Section 40A(9)/ (10)/ (11) Analysis

Section 40A(9)

§No deduction shall be allowed in respect of any sum paid by the assessee as an employer towards the setting up/formation /contribution to any fund, trust, company,AoP, BoI, society or institution for any purpose, except where such sum is paid for the followingpurposes : Approved superannuation fund§ recognized provident fund§Pension scheme [80CCD]§Approved gratuity fund

Section 40A(10)

Ø After disallowance u/s 40A(9) if the AO is satisfied that the fund, trust, etc has expended such sum wholly for the welfare of the employees, deduction shall be allowed to the assesseein the year in which such expenditure is made

Ø The section stands redundant as the section prescribes expenditure to be made by the fund, trust, etc before 1st March 1984.

Section 40A(11)

Where the assessee has, before 1st March 1984, paid any sum which remained unutilised, the assessee can claim the repayment of such sum from the fund, trust, etc or transfer of any asset acquired/ constructedout of the sum by the fund, trust, etc

Slide 36May 2014PGBP Disallowances

Income-tax Act, 1961

Section 43B– Certain deductions to be only on actual payment

Slide 37May 2014PGBP Disallowances

Income-tax Act, 1961

Section 43B Analysis

Expenses covered under section 43B

Notwithstanding anything contained in any other provision of this Act, a deduction otherwise allowable under the Act, shall be allowed when such sum is actually paid by the assessee

Time limit Specified

• During the previous year, or

• Before the due date for filing return

Any sum payable by way of tax, duty, cess or fee by whatever name called under any law

Any sum payable as Employers contribution to employee welfare fund like PF, Gratuity, SAF, etc

Any sum being Bonus or Commission payable to employees [i.e. sum referred to in 36 (1) (ii)

Any sum payable by an employer in lieu of any leave credit i.e. leave salary encashment

Scope of Section 43B

Any sum payable as Interest on loan borrowed from Scheduled banks and Financial Institutions

Slide 38May 2014PGBP Disallowances

Income-tax Act, 1961

Ø DCIT vs Sri Shanmugavel Mills Ltd. [2011] 14 taxmann.com 185 (MAD.)

Where provision made for labor welfare expenses was not for payment of bonus or any other payment in guise of bonus but it was to be paid as a part of wages being incentive for performance of workers, no disallowance could be made thereof.

Ø ACIT v Kaiser Industries Ltd (2011) 10 Taxmann.com 133 (Delhi).

When unexpired MODVAT credit is set off against excise duty payable and thereby liability has been extinguished or reduced, that settingoff of MODVAT credit is as good as duty paid

Ø Thanjavur Textiles Ltd. vs. JCIT [2012] 25 taxmann.com 544 (Mad.)

Depositing of bonus amounts payable to employees into a separate bank account does not amount to actual payment.

Section 43B – Judicial Precedents

Slide 39May 2014PGBP Disallowances

Income-tax Act, 1961

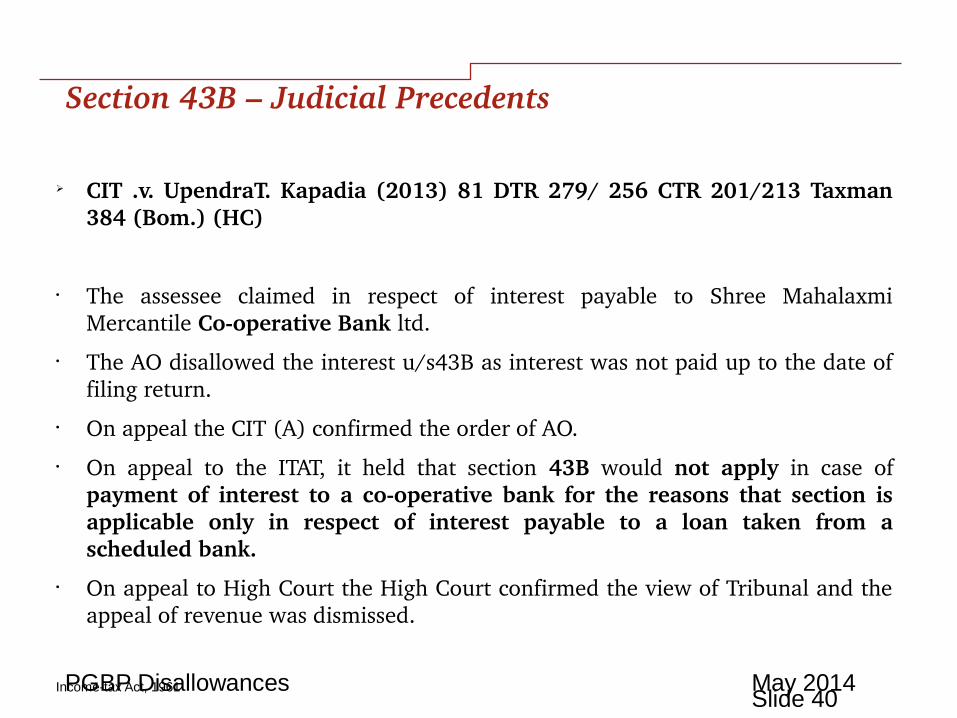

Ø CIT .v. UpendraT. Kapadia (2013) 81 DTR 279/ 256 CTR 201/213 Taxman 384 (Bom.) (HC)

• The assessee claimed in respect of interest payable to Shree Mahalaxmi Mercantile Cooperative Bank ltd.

• The AO disallowed the interest u/s43B as interest was not paid up to the date of filing return.

• On appeal the CIT (A) confirmed the order of AO. • On appeal to the ITAT, it held that section 43B would not apply in case of

payment of interest to a cooperative bank for the reasons that section is applicable only in respect of interest payable to a loan taken from a scheduled bank.

• On appeal to High Court the High Court confirmed the view of Tribunal and the appeal of revenue was dismissed.

Section 43B – Judicial Precedents

Slide 40May 2014PGBP Disallowances

Income-tax Act, 1961

Ø Spectrum Consultants India (P.) Ltd. v. CIT (2013) 215 Taxman 597 (Karn.)(HC)

• The assessee claimed deduction of employee’s contribution under the EPF Act, and ESI Act, which were remitted beyond the due dates prescribed under the statutes.

• AO disallowed the payment on the ground that section 43B(b) allowed payment of only employer’s contribution till due date of filing return.

• The assessee filed revision application under section 264, which was dismissed. • The assessee challenged the said order by filing writ petition. • Allowing the petition the Court held that where the assessee remitted employees'

contribution under EPF Act, and ESI Act after due dates prescribed under said statutes, but before extended due date for filing return u/s 139(1), deduction could not be disallowed.

Section 43B – Judicial Precedents

Slide 41May 2014PGBP Disallowances

Income-tax Act, 1961

Ø Gujarat State Road TransportCorporation [2014] 265 CTR 64 (Gujarat)

• Assessee, a State transport corporation collected a sum being provident fund contribution from its employees. However, it deposited lesser sum in provident fund account;

• Assessing Officer disallowed same under section 43B; • However, CIT (A) deleted disallowance on ground that employees contribution

was deposited before filing return ;• ITAT upheld the treatment adopted by CIT (A);• High Court held that where an employer has not credited sum received by it as

employees' contribution to employees' account in relevant fund on or before due date as prescribed in Explanation to section 36(1)(va), assessee shall not be entitled to deduction of such amount though he deposits same before due date prescribed under section 43B i.e., prior to filing of return under section 139(1).

Section 43B – Judicial Precedents

Slide 42May 2014PGBP Disallowances

Income-tax Act, 1961

Section 43B – Recent Judgments on Employees Contribution

• Recently, different High Courts [‘HC’] have taken different view with respect to deductibility of Employee’s Contribution to any Fund and application of section 43B.

• One view as taken by Karnataka HC and Rajasthan HC – Employees Contribution is covered by 43B and hence if payments are made after expiry of due date under respective statutes but before ROI filing due date, such expenditure should be allowed

• The other view as taken by Gujarat HC – 43B covers only Employer’s Contribution. Employees contribution is covered by section 36(1)(va) and for the expenditure to be allowed, it has to be deposited within the due date as prescribed in the respective statue. Benefit of depositing the same till the return filing due date is not available for Employees Contribution.

Employee C

ontribution covered by 43B

Employee C

ontribution – not covered by 43B

Slide 43May 2014PGBP Disallowances

Q & A

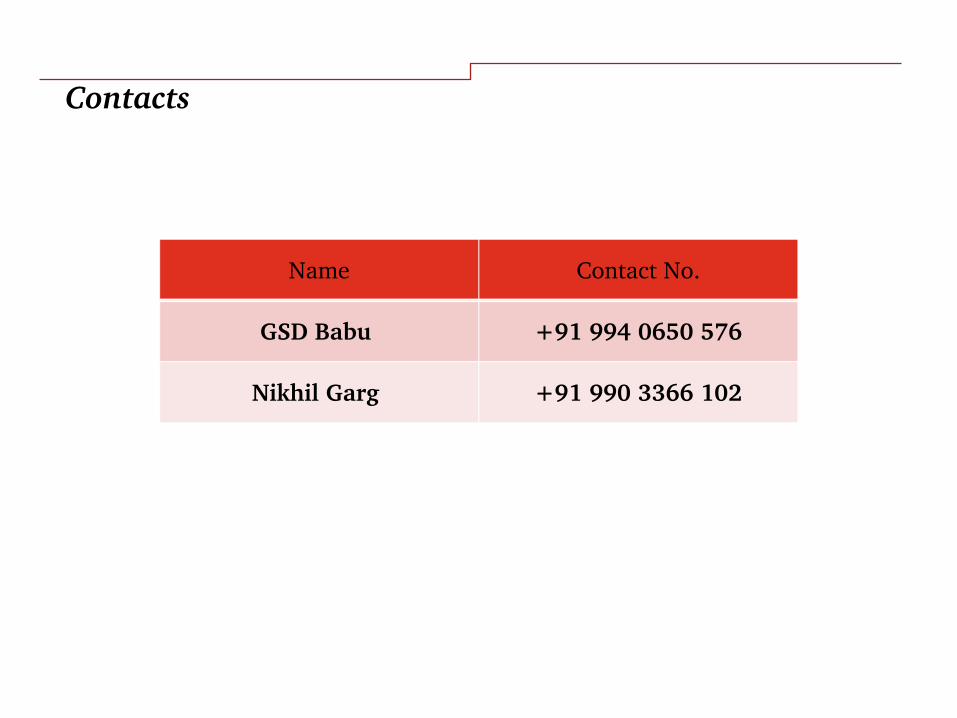

Contacts

Name Contact No.

GSD Babu +91 994 0650 576

Nikhil Garg +91 990 3366 102

Thank you!