Patent Valuation, Foreign Exchange Risk and Time Value of - Webs

18

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 401 MARCH 2013 VOL 4, NO 11 Patent Valuation, Foreign Exchange Risk and Time Value of Money Jonah, Udeme Inyang Msc Finance and Accounting (University of Wales, UK) Abstract The purpose of this paper is to critically value patent right by using real option theory (Black-Scholes-Merton Model) to determine the valuation of patent and the assumptions of Black and Scholes option pricing model, the second part will be on foreign exchange risk, participating forward contract, its advantages and disadvantages of participating in forward contract, foreign exchange risk hedging. The third part will be on time value of money, while the last part will be on advantages and disadvantages of high tech companies. This paper will provide critical understanding of international financial management topic. Conceptual grasp of issues, Analytical skills and techniques of international financial management. Furthermore, apply financial tools of risk analysis. Keywords: Patent Valuation, Foreign Exchange, Time Value of Money Introduction A patent is an intellectual property right granted by the Government of the United States of America to an inventor “to exclude others from making, using, offering for sale, or selling the invention throughout the United States or importing the invention into the United States” for a limited time in exchange for public disclosure of the invention when the patent is granted (Uspto, 2012). The term word patent originates from the Latin patere, which means "to lay open" (that is, to make available for public inspection) “A patent is a grant by the U.S. Patent and Trademark Office (USPTO) t hat allows the parent owner to maintain a monopoly for a limited period of time on the use development of an invention” ( Stim, 2012, p.17). The term patent usually refers to the right granted to anyone who invents any new or useful and non-obvious process, machine, article of manufacture, or composition of matter.

Transcript of Patent Valuation, Foreign Exchange Risk and Time Value of - Webs

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 401

MARCH 2013

VOL 4, NO 11

Patent Valuation, Foreign Exchange Risk and Time Value of Money

Jonah, Udeme Inyang

Msc Finance and Accounting (University of Wales, UK)

Abstract

The purpose of this paper is to critically value patent right by using real option theory (Black-Scholes-Merton

Model) to determine the valuation of patent and the assumptions of Black and Scholes option pricing model, the

second part will be on foreign exchange risk, participating forward contract, its advantages and disadvantages of

participating in forward contract, foreign exchange risk hedging. The third part will be on time value of money,

while the last part will be on advantages and disadvantages of high tech companies. This paper will provide critical

understanding of international financial management topic. Conceptual grasp of issues, Analytical skills and

techniques of international financial management. Furthermore, apply financial tools of risk analysis.

Keywords: Patent Valuation, Foreign Exchange, Time Value of Money

Introduction

A patent is an intellectual property right granted by the Government of the United States of America to an inventor

“to exclude others from making, using, offering for sale, or selling the invention throughout the United States or

importing the invention into the United States” for a limited time in exchange for public disclosure of the invention

when the patent is granted (Uspto, 2012).

The term word patent originates from the Latin patere, which means "to lay open" (that is, to make available for

public inspection)

“A patent is a grant by the U.S. Patent and Trademark Office (USPTO) that allows the parent owner to maintain a

monopoly for a limited period of time on the use development of an invention” (Stim, 2012, p.17).

The term patent usually refers to the right granted to anyone who invents any new or useful and non-obvious

process, machine, article of manufacture, or composition of matter.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 402

MARCH 2013

VOL 4, NO 11

VALUATION OF PATENT

The most common patent-valuation method is the economic-analysis method. But I‟m going to use the real option

theory (Black-Scholes-Merton model) to determine the valuation of the patent. The real option is also known as

option pricing.

Real options theory begins by drawing an analogy between real options and financial options. A financial option is a

derivative security whose value is derived from the worth and characteristics of another financial security, or the so-

called underlying asset. By definition, a financial option gives its holder the right, but not the obligation, to buy or

sell the underlying asset at a specified price in other words (the exercise price) on or before a given date that is (the

expiration date) (Tong and Reuer, 2007).

Financial economists Black and Scholes (1973) and Merton (1973) pioneered a formula for the valuation of a

financial option, and their methodology has opened up the subsequent research on the pricing of financial assets and

paved the way for the development of real options theory.

„The Black-Scholes model is one of the most outstanding models in financial economics. The Black-Scholes Option

Pricing Models based on stochastic calculus‟ (Sudarsanam et al. 2006, p.299).

Real options allow for flexibility to exist in investment decisions. They provide options to defer, time to build, alter

operating scales, abandon, switch, grow, and so on (Chang et al. 2005).

The Black and Scholes option pricing model (OPM) was developed in 1973, helped give rise to the rapid growth in

option trading. This model, which has even been programmed into some handheld and web-based calculators, is

widely used by option trader (Ehrhardt and Brigham, 2010).

Strengths and drawback of Merton (1974) model for default risky bonds and swaps

According to Ali (2004) the model is simple to implement, but the drawback is that it requires inputs from value of

the firm, it Default occurs only at the maturity of the debt. Furthermore, the Information in the history of defaults

and credit rating changes cannot be used.

DETERMINATION OF PATENT

The inputs to the option price model are as follows;

Value of the underlying asset = PV of inflows (current) = $1 billion.

Exercise price = PV of cost of the developing product = $1.5 billion.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 403

MARCH 2013

VOL 4, NO 11

Time to expiration = life of patent = 20 years

Variance in the value of the underlying asset = Variance in PV of inflows = 0.03

Risk-less rate = 10 %

Dividend yield = = = 0.05

Based on the input Black and Scholes model provides the following value for the call which are; d1 = 1.1548, N(d1)

= 0.8759, d2 = 0.3802, N(d2) = 0.6481

Cash value = $1billion exp(-0.05)(20)(0.8759) - $ 1.5 billion exp(-0.10)(20)(0.6481) = $190.66 billion

The cash value is $190.66 billion

However

Value of the call option

Where;

Where;

T= time to expiration

N= (.)- Cumulative normal probability

C = fair value of the option

S = the current price of the stock

R = the risk free rate of interest

X = exercise price of the option

= annualised standard deviation of the stock

Continues dividend rate on the stock

Therefore

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 404

MARCH 2013

VOL 4, NO 11

d1 = 1.15483958

429105

From the normal distribution, by using excel we will have the following below

N(d1) = 0.875921937

N(d2) = 0.648117445

0.875921937 0.648117445

While for the put options

NB: From the normal distribution, by using excel

N(-d1) = 0.124078063

N(-d2) = 0.351882555

Now we can now calculate how put option

P = 0.07143318787 – 0.04564576848

P = 0.02578741939

P = $25,787,419.39

COMMENT

From the calculation above the call option is $1,906,639,357 while for the put option is $2,578,741,939.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 405

MARCH 2013

VOL 4, NO 11

However, the dividend yield shows the return of the business which is 0.05 which gives the yearly return, the black

and schools model do not take consideration of dividend yield. Generally the Merton model can only be applied to

European option. Thus, there are some limitations of Merton model.

Limitation of Merton model

Firstly, how will you price the bond that is not been sold, secondly the riskless bond and borrowing is impossible

and the future dividend cannot be accurate which is impossible because sales might go up or down and the variance

cannot be fixed in the riskless bond. Finally difference between high tech and patent valuation, because innovation is

been increased every year.

OPTION PRICING MODEL ASSUMPTIONS

According to Ehrhardt & Brigham (2010), in deriving their option pricing model, Fischer Black and Myron Scholes

made the following assumptions.

1. The stock underlying the call option provides no dividends or other distributions during the life of the

options.

2. There are no transaction cost for buying and selling either the stock or the options

3. The short-term, risk-free interest rate is known and is constant during the life of the options.

4. Any purchaser of a security may borrow any fraction of the purchase price at the short-term, risk-free

interest rate.

5. Short selling is permitted, and the short seller will receive immediately the full cash proceeds of today‟s

price for a secure sold short.

6. The call option can be exercised only on its expiration dated

7. Trading in all securities takes place contentiously, and the stock price moves randomly

CRITICISM OF REAL OPTION MODEL

Real Option Models has its limitations when applied to the real world. Patents contain “adverse rights” which run

counter to the notion of “having an option”. Furthermore, the option value of a patent can be reduced or eliminated

by a third party filing and contesting the claim (Chang et al. 2005).

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 406

MARCH 2013

VOL 4, NO 11

The principal deficiency in using the Black–Scholes–Merton model to value executive stock options is that the

model assumes that the option is liquid while executive stock options are essentially illiquid. Models that account

for liquidity are typically based on utility functions and require personal information about the executive (Chance

and Yang, 2007).

The problem in option theory is to estimate the option price when the strike price, as well as several other

parameters, is given. For a business project, irreversible fixed investment is determined at the beginning of a project.

The problem in project investment is to estimate variable costs when fixed costs as well as other factors are given.

Mathematically speaking, the problem in option theory is to solve a backward equation derived from a lognormal

process for option prices with a known end condition – the strike price. The problem in project investment is to

solve a forward equation derived from a lognormal process for variable costs with a known initial condition – the

fixed investment. The similarity between these two problems explains why option theory becomes so important in

understanding project investment and other economic problems (Chen, 2006).

Introduction

Foreign exchange is the process were two more parties do business from one country to another. Thus foreign

exchange is also called forex. Forex is a process of conversion of one country‟s currency into another country‟s

currency. A currency‟s value can be pegged to another country‟s currency.

Examples of this were seen during the financial crisis in Asia during the year 1997, when the Chinese renminbi and

the Malaysian Ringgit were able to come out of critical financial crises. The Chinese renminbi fixed its rate and the

Malaysian Ringgit pegged itself to the US dollar, which helped revive its economic fortunes (Economy watch,

2010).

The market force do determined the value of the currency at any particular time.

ADVANTAGES AND DISADVANTAGES OF FOREIGN EXCHANGE RATE

Advantages

According to Carbaugh (2010) foreign exchange rate advantages are as follows;

Simplicity and clarity of exchange rate target

Automatic rule for the conduct of monetary policy

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 407

MARCH 2013

VOL 4, NO 11

keeps inflation under control

Continuous adjustment in the balance of payments

Operate under simplified institutional arrangement

Allows governments and fiscal policies.

Disadvantages

According Carbaugh (2010) disadvantages of foreign exchange rate are as follows;

Loss of independent monetary policy

Vulnerable to speculative attacks

Conducive to price inflation

Disorderly exchange markets can disrupt trade and investment patterns

Encourage reckless financial policies on the part of the government.

Forward Contract

A forward contract or forward outright is a transaction executed today in which one currency is bought or sold

against another for delivery on a specified date that is not the spot date, for example three month from the

commencement date (Shamah, n.d).

Foreign Exchange Risk

Foreign exchange risk is the risk that an entity will be required to pay more (or less) than expected as a result of

fluctuations in the exchange rate between its currency and the foreign currency in which payment must be made

(Abor, 2005).

Foreign exchange risk is commonly defined as the additional variability experienced by a multinational corporation

in its worldwide consolidated earnings that results from unexpected currency fluctuations. It is generally understood

that this considerable earnings variability can be eliminated partially or fully at a cost, the cost of foreign exchange

risk management (Jacque, 1981).

Foreign exchange risk is also known as exchange rate risk or currency risk is a financial risk posed by an exposure

to unanticipated changes in the exchange rate between two currencies (Levi 2005; Moffett et al, 2009)

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 408

MARCH 2013

VOL 4, NO 11

Investors and multinational businesses exporting or importing goods and services or making foreign

investments throughout the global economy are faced with an exchange rate risk which can have

severe financial consequences if not managed appropriately Homaifar (2004), Moosa (2003).

FOREIGN EXCHANGE HEDGE

Many firm attempts to manage their currency exposure through hedging. Hedging is the tacking of a position either

acquiring a cash flow, an asset or contracts (including a forward contract) that will rise (or fall) in the value and off

set a fall (or rise) in the value of an existing position (Eiteman et al, 2010).

This is a process which companies use to eliminate or hedge foreign exchange risk. There are methods used in

hedging. This is fair value method or cash flow method.

Hedging protect the owner exiting asset from loss. And the reasons for hedging is to reduce risk in the future

Forward Market Hedge

A forward market hedge involves a forward (or futures) contract and sources of funds to fulfil that contract. The

forward contract is entered into at the time transaction exposure is created (Eiteman et al, 2010).

PARTICIPATING FORWARD CONTRACT

Participating forward is also called a zero cost ratio option and forward participation agreement is an option

contribution that allows the hedger to share in potential upside movement while providing option based downside

protection, all at a zero net premiums (Eiteman et al, 2010).

ADVANTAGES AND DISAVANTAGES OF PARTICIPATING FORWARD

CONTRACT

Advantages

The followings are advantages of participating forward according to Qfinance, (2010);

Total protection against currency falls

No premium

A guaranteed worst-case rate

A practical benefit from currency gains

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 409

MARCH 2013

VOL 4, NO 11

Disadvantages

The followings are disadvantages of participating forward according to Qfinance, (2010);

If the currency weakens the rate will not as good as the forward exchange contract

The spot rate will be better if there is a positive move in currency.

Foreign exchange calculation

Investment amount = SF 1,000,000 which is payable in six month

Forward rate = SF 1.2100 / $ for six month

Foreign exchange broker rate = SF 1.1600 / $

Option1.

For instance if the US dollars strengthen to SF 1.1600 we will buy half at SF 1.1600 / $ and the remaining at the

prevailing market price which is SF 1.2500 / $

From the option we look at the benefit or otherwise of buying the whole contract at the broke rate

Option to buy from the broker = = $862,068.9655

GoodPharma will have to buy entire contract at $862,068.9655 under a normal forward contract. But GoodPharma is

involved in participating forward contract which will allow them to enjoy the benefit of spot rate.

Option to buy half from the broker before the completion = = $431,034.4828

Option to buy from the market after completion = = $400,000

GoodPharma will pay $431,034.4828 + $400,000 = $831,034.4828

Option 2

Buy all at the broker rate = = $862,068.9655

The broker rate is high than the forward rate, because if GoodPharma do not enter the contract they will save

$62,068.9655 which will be better for the company.

The Participating forward contract provides full protection against downside. Rather than apply the 50 – 50 rule as

below:

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 410

MARCH 2013

VOL 4, NO 11

Buying half from the broker = $431,034.4828

Buying half at Spot rate = $434,782.6087

The total will be $431,034.4828 + $434,782.6087 = $865,817.0915

By the participating forward contract and buying at broker rate of SF1.16 the savings will be $865,817.0915 ‒

$862,068.9655 = $3,748.126

Introduction

The time value of money approaches that will be used are NPV and IRR. For better understanding we will need to

know the basic terms which are as follows;

Double Taxation Agreement

This is an agreement which concluded between to state in order to prevent a person who is fully liable tax in one of

the States (or sometimes in both states) from being taxed on the same income (or capital) in both States (Rasmussen,

2011).

Tax Holiday

Tax holiday is an exclusion or elimination or reduction temporary from tax. It‟s a way of creating an incentive for

business investment. Which is called tax subside

Capital allowance

According to Venture line (n.d) corporation tax refers to direct taxes charged by various jurisdictions on the profits

made by companies or associations. As a general principle, this varies substantially between jurisdictions. In

particular allowances for capital expenditure and the amount of interest payments that can be deducted from gross

profits when working out the tax liability vary substantially. Also, tax rates may vary depending on whether profits

have been distributed to shareholders or not.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 411

MARCH 2013

VOL 4, NO 11

Withholding tax

Withholding tax is an amount withheld by the party making payment to another (payee) and paid to the taxation

authorities. The amount the payer deducts may vary, depending on the nature of the product or service being paid for

(Withholding tax, 2012).

Investment A

The initial investment was $200,000 the unit of sales is $60,000×3=$180,000 is the revenue. The asset is value at

$200,000/10= $20,000 which is the depreciable value $20,000. The operating expense of $80,000, the EBIT is the

summation of revenue, operating expenses and depreciation which is $80,000. Tax was charge at 34 % which is

$27,200. The profit after tax is $52,800 the depreciation was added back which is $20,000. The working capital was

added back only at year 10 which is $ 10,000, the net cash flow for year 1 to year 9 is $72,800, while year 10 was

$82,800, because of the working capital that was added back. Using excel the NPV is $234,909 and the IRR of 33%

Table 1: Project A

YEARS ZERO ONE TWO THREE FOUR FIVE SIX SEVEN EIGHT NINE TEN

$ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000)

CAPITAL INVESTMENT 200.00-

WORKING CAPITAL 10.00-

REVENUE ($3*60,000) 180 180 180 180 180 180 180 180 180 180

OPERATING EXPENSES -80 -80 -80 -80 -80 -80 -80 -80 -80 -80

DPRECIATION -20 -20 -20 -20 -20 -20 -20 -20 -20 -20

EBT 80 80 80 80 80 80 80 80 80 80

TAX -27.2 -27.2 -27.2 -27.2 -27.2 -27.2 -27.2 -27.2 -27.2 -27.2

PAT 52.8 52.8 52.8 52.8 52.8 52.8 52.8 52.8 52.8 52.8

WORKING CAPITAL 10

ADD BACK DEPRECIATION 20 20 20 20 20 20 20 20 20 20

NET CASH INFLOW 210.00- 72.8 72.8 72.8 72.8 72.8 72.8 72.8 72.8 72.8 82.8

NPV= (1+r)^-n 66.18 60.17 54.70 49.72 45.20 41.09 37.36 33.96 30.87 31.92

IRR 33%

NPV OF INVESTMENT 210.00- 66.18 60.17 54.70 49.72 45.20 41.09 37.36 33.96 30.87 31.92

NPV OF INVESTMENT 241.18

NPV OF INVESTMENT($) 241,179.92

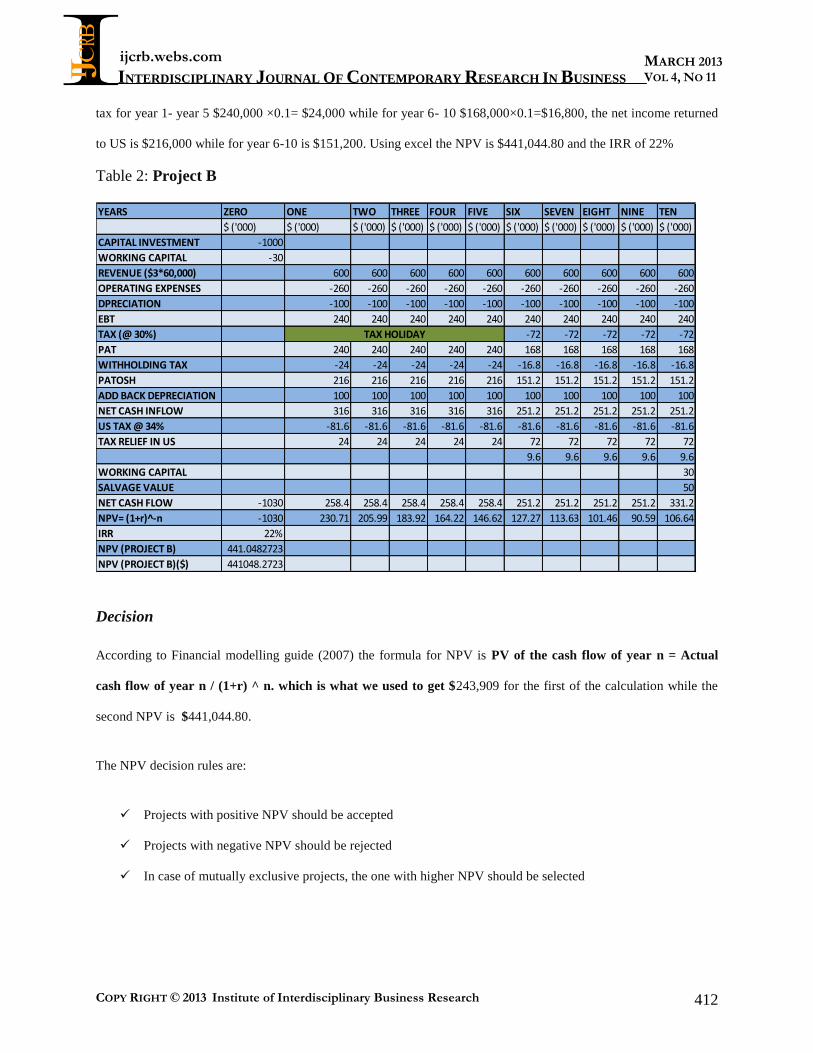

Investment B

The capital invested was $1,000,000 and working capital of $30,000, the revenue of $600,000, operating expenses

of $260,000. The EBIT of $240,000, Tax (Brazil tax exempt 30%) which is $240,000×0.30=$72,000 it was charge

at year 6 –year 10. The profit after tax for year 1- 5 is $240,000 while for year 6-10 is $168,000. The withholding

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 412

MARCH 2013

VOL 4, NO 11

tax for year 1- year 5 $240,000 ×0.1= $24,000 while for year 6- 10 $168,000×0.1=$16,800, the net income returned

to US is $216,000 while for year 6-10 is $151,200. Using excel the NPV is $441,044.80 and the IRR of 22%

Table 2: Project B

YEARS ZERO ONE TWO THREE FOUR FIVE SIX SEVEN EIGHT NINE TEN

$ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000) $ ('000)

CAPITAL INVESTMENT -1000

WORKING CAPITAL -30

REVENUE ($3*60,000) 600 600 600 600 600 600 600 600 600 600

OPERATING EXPENSES -260 -260 -260 -260 -260 -260 -260 -260 -260 -260

DPRECIATION -100 -100 -100 -100 -100 -100 -100 -100 -100 -100

EBT 240 240 240 240 240 240 240 240 240 240

TAX (@ 30%) -72 -72 -72 -72 -72

PAT 240 240 240 240 240 168 168 168 168 168

WITHHOLDING TAX -24 -24 -24 -24 -24 -16.8 -16.8 -16.8 -16.8 -16.8

PATOSH 216 216 216 216 216 151.2 151.2 151.2 151.2 151.2

ADD BACK DEPRECIATION 100 100 100 100 100 100 100 100 100 100

NET CASH INFLOW 316 316 316 316 316 251.2 251.2 251.2 251.2 251.2

US TAX @ 34% -81.6 -81.6 -81.6 -81.6 -81.6 -81.6 -81.6 -81.6 -81.6 -81.6

TAX RELIEF IN US 24 24 24 24 24 72 72 72 72 72

9.6 9.6 9.6 9.6 9.6

WORKING CAPITAL 30

SALVAGE VALUE 50

NET CASH FLOW -1030 258.4 258.4 258.4 258.4 258.4 251.2 251.2 251.2 251.2 331.2

NPV= (1+r)^-n -1030 230.71 205.99 183.92 164.22 146.62 127.27 113.63 101.46 90.59 106.64

IRR 22%

NPV (PROJECT B) 441.0482723

NPV (PROJECT B)($) 441048.2723

TAX HOLIDAY

Decision

According to Financial modelling guide (2007) the formula for NPV is PV of the cash flow of year n = Actual

cash flow of year n / (1+r) ^ n. which is what we used to get $243,909 for the first of the calculation while the

second NPV is $441,044.80.

The NPV decision rules are:

Projects with positive NPV should be accepted

Projects with negative NPV should be rejected

In case of mutually exclusive projects, the one with higher NPV should be selected

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 413

MARCH 2013

VOL 4, NO 11

However, when the project NPV is zero, the rate at that point of time is considered to be its Internal Rate of Return

(IRR). A rule of the IRR also state that accept the project with higher IRR but that where NPV and IRR conflicts,

NPV should be the decision criteria.

Since we are dealing with two projects, we will use the mutually exclusive project. So project B is chosen as it has

the higher NPV of 441,044.80.

Limitations of NPV Analysis

The main limitation of net present value analysis is the difficulty of accurately forecasting future costs and benefits.

In particular, benefits are often non tangible (but real) improvements to the community. Programs can have

unanticipated costs or generate less revenue than expected. Another limitation of net present value analysis is that

there is no universal discount rate or standard method of setting a discount rate. Because there is no standard in this

area, net present value analysis is vulnerable to manipulation through selecting a high or low discount rate; however,

both of these weaknesses may be addressed by conducting a sensitivity analysis (Michel, 2001).

IRR decision rules are:

Projects with an IRR which is better than that of the firm should be accepted

Projects with an IRR which is less than that of the firm should be rejected

According to Clayman, et al (2012) for mutually exclusive project, if the project with the

Highest NPV should be accepted

Project B is a foreign direct investment

Foreign direct investment (FDI) is a term used to denote the acquisition abroad of physical asset, such as plant and

equipment, with operational control ultimately residing with the parent company in the home country (Buckley,

2004).

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 414

MARCH 2013

VOL 4, NO 11

The economy of Brazil is the world's sixth largest by nominal GDP and is expected to become fifth by the end of

2012 (Cia, 2007).

Brazil has moderately free market and an inward-oriented economy. Its economy is the largest in Latin

American nations and the second largest in the western hemisphere (Forbes, 2010).

A tax haven is a state or a country or territory where certain taxes are levied at a low rate or not at all while

offering due process, good governance and a low corruption rate (Dharmapala and Hines, 2009).

The Advantages of Foreign Direct Investment

Location advantages

Location advantages is defined as „benefits arsing from host country‟s corporative advantages accrued to foreign

direct investors‟ (Shenkar and Luo, 2008 p.63). On the other hand, because of some specific resources at lower real

costs, also benefits resulting from economic liberation.

Expands the market

Foreign direct investment expands the market domain in which a multinational economy (MNE) capitalise on its

core competencies, generating more income from existing resources capabilities or knowledge (Shenkar and Luo,

2008).

Organisation learning

Foreign direct investment is also a vehicle for organisational learning. Being actively involved in foreign direct

investment grants the multinational enterprise (MNE) learning opportunities that would not have been available to

otherwise (Shenkar and Luo, 2008).

Cost factors

Foreign direct investment „Reduced transport cost, scale economies, host government incentives, reduced packaging

cost, tariff and duties elimination access to resources‟ (Bradley, 2005 P.277).

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 415

MARCH 2013

VOL 4, NO 11

The Disadvantages of Foreign Direct Investment

Product-Market factors

The product market factors are one of the disadvantages of foreign direct investment which are „Management

constraints, loss of flexibility, increased marketing, complexity‟ (Bradley, 2005 P.277).

Cost factors

This is another disadvantage of foreign direct investment. High initial capital investment for example project B

capital investment is £1,000,000 which is higher than project A. high information and search cost not nationalisation

or expropriation (Bradley, 2005).

ADVANTAGES AND DISAVANTAGES OF OFFSHORE MANUFACTURING

ADVANTAGES

Large size and economic of scare

Lower input costs

Brand image and good will

DISADVANTAGES

Host country regulation/political

Natural risk

BENEFITS OF OFFSHORE MANUFACTURING

The primary factor which attracts manufacturers to outsource manufacturing offshore is the reduction in their cost of

production. There are various key factors which have led the growing trend of offshore manufacturing. For instance,

lack of well experienced and skilled labour available in domestic market or availability of cheap labour in

international markets forces the manufacturers to outsource their manufacturing to the other countries to keep their

costs of manufacturing within their budgets (Allbestarticles, 1987).

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 416

MARCH 2013

VOL 4, NO 11

Conclusion

From the calculation above in part A. we can the patent valuation and the limitation for part B. we can see the

calculation about foreign exchange. Part C, the mutually exclusive investment. Finally we could say it‟s safer to

manufacturing in an offshore location.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 417

MARCH 2013

VOL 4, NO 11

References

Abor, J. (2005) Managing foreign exchange risk among Ghanaian firms. The Journal of Risk Finance, 6 (4).

Ali, A. (2004) Credit Risk Modeling: An introduction to credit risk modeling. Risk International.

Allbestarticles.com (1987) Benefits of offshore manufacturing. [online] Available at:

http://www.allbestarticles.com/business/specialized-manufacturer/benefits-of

Offshore-manufacturing.html [Accessed: 25 Jul 2012].

Black, F. and Scholes, M. (1973) the pricing of options and corporate liabilities. Journal of Political Economy,

81 (3).

Bradley, F. (2005) International Marketing Strategy. 5th ed. Essex: Pearson Education Limited, p.277.

Buckley, A. (2004) Multinational Finance. 5th ed. Essex: Pearson Education Limited, p.363.

Carbaugh, R. (2010) International Economics. 13th ed. Cengage learning, p.468.

Chance, D. and Yang, T. (2007) Advances in Financial Economics. Emerald Group Publishing Limited.

Chang, J. et al. (2005) Valuation of intellectual property: A real option approach. Journal of Intellectual

Capital, 6 (3), p.341.

Chen, J. (2006) An analytical theory of project investment: a comparison with real option theory. International

Journal of Managerial Finance, 2 (4), p.357.

Cia.gov (2007) CIA Site Redirect — Central Intelligence Agency. [online] Available at:

http://www.cia.gov/library/publications/the-world-factbook/geos/br.html [Accessed: 25 Jul 2012].

Clayman, M. et al. (2012) Corporate Finance: A Practical Approach. 2nd ed. New Jersey: John Wiley & Sons,

p.82.

Dhammika, D. and Hines, J. (2009) which countries become tax havens. Journal of public Economics, 39 (9-

10).

Economywatch.com (2010) Fixed Exchange Rate | Economy Watch. [online] Available at:

http://www.economywatch.com/exchange-rate/fixed.html [Accessed: 7 Jul 2012].

Eiteman, D. et al. (2010) Multinational business finance. 12th ed. Pearson Education Limited.

Erhardt , and Brigham, E. (2010) Financial management; theory and practice. 13th ed. mason: South western

Cengage learning, p.319.

Forbes.com (2010) Is Brazil's Economy Getting Too Hot? - Forbes. [online] Available at:

http://www.forbes.com/sites/kerenblankfeld/2010/12/13/is-brazils-economy-getting-too-hot/ [Accessed: 25 Jul

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 418

MARCH 2013

VOL 4, NO 11

2012].

Homaifar, G. (2004) Managing Global Financial and Foreign Exchange Risk. Hoboken: John Wiley & Sons.

Jacque, L. (1981) Management of foreign exchange risk: a review article. Journal of International Business

Studies, 12 (1).

Levi, M. (2005) International Finance. 4th ed. New York: Routledge.

Michel, G. (2001) Net Present Value Analysis: A Primer for Finance Officers. Government Finance Review.

Moffett, M. et al. (2009) Fundamentals of Multinational Finance. 3rd ed. Boston: Addison-Wesley.

Mossa, I. (2003) International Financial Operations: Arbitrage, Hedging, Speculation, Financing and

Investment. New York: Palgrave Macmillan.

Qfinance.com (2010) Hedging Foreign Exchange Risk—Case Studies and Strategies- QFINANCE. [online]

Available at: http://www.qfinance.com/financial-risk-management-checklists/hedging-foreign-exchange-

riskcase-studies-and-strategies [Accessed: 7 Jul 2012].

Rasmussen, M. (2011) International Double Taxation. Kluwer Law International.

Shamah, S. (n.d.) A Foreign Exchange Primer. 2nd ed. John Wiley and Sons.

Shenkar, O. and Lou, Y. (2008) International Business. 2nd ed. California: Sage Publication , p.63.

Stim, R. (2012) Patent, Copyright & Trademark: An Intellectual Property Desk Reference. 12th ed. Nolo and

Richard Stim, p.17.

Sudarsanam, S. et al. (2006) Real options and the impact of intellectual capital on corporate value. Journal of

Intellectual Capital, 7 (3), p.299.

Tong, T. and Reuer, J. (2007) Real Options Theory (Advances in Strategic Management, Volume 24). Emerald

Group Publishing Limited, p.5.

Uspto.gov (2012) Patents. [online] Available at: http://www.uspto.gov/patents/index.jsp [Accessed: 5 Jul 2012].

Ventureline.com (n.d.) CORPORATION TAX DEFINITION. [online] Available at:

http://www.ventureline.com/accounting-glossary/C/corporation-tax-definition/ [Accessed: 24 Jul 2012].

Withholdingtax.org (2012) Withholding Tax. [online] Available at: http://www.withholdingtax.org/ [Accessed:

24 Jul 2012