Part I Pearson SETTING THE SCENEcatalogue.pearsoned.co.uk/.../samplechapter/0273763792.pdf · 1.5.2...

54

Part I SETTING THE SCENE Proofs: File not for distribution without prior permission from Pearson Education

Transcript of Part I Pearson SETTING THE SCENEcatalogue.pearsoned.co.uk/.../samplechapter/0273763792.pdf · 1.5.2...

..

Part I

SETTING THE SCENE

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 1

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

..

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 2

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

1

..

3

Introduction

CONTENTS

OBJECTIVES

1.1 Differences in financial reporting1.2 The global environment of accounting

1.2.1 Overview1.2.2 Accounting and world politics1.2.3 Economic globalization, international trade and foreign direct investment1.2.4 Globalization of stock markets1.2.5 Patterns of share ownership1.2.6 The international financial system

1.3 The nature and growth of MNEs1.4 Comparative and international aspects of accounting1.5 Structure of this book

1.5.1 An outline1.5.2 Setting the scene (Part I)1.5.3 Financial reporting by listed groups using IFRS or US GAAP (Part II)1.5.4 China and Japan (Part III)1.5.5 Financial reporting by individual companies (Part IV)1.5.6 Group accounting issues in reporting by MNEs (Part V)1.5.7 Enforcement and analysis (Part VI)

SummaryReferencesUseful websitesQuestions

After reading this chapter, you should be able to:

l explain why international differences in financial reporting persist, in spite of theadoption of international financial reporting standards (IFRS) by Australia, Canada,the member states of the European Union and many other countries;

l illustrate the ways in which accounting has been influenced by world politics, thegrowth of international trade and foreign direct investment, the globalization ofstock markets, varying patterns of share ownership, and the international monetarysystem;

l outline the nature and growth of multinational enterprises (MNEs);

l explain the historical, comparative and harmonization reasons for studyingcomparative international accounting.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 3

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

4

..

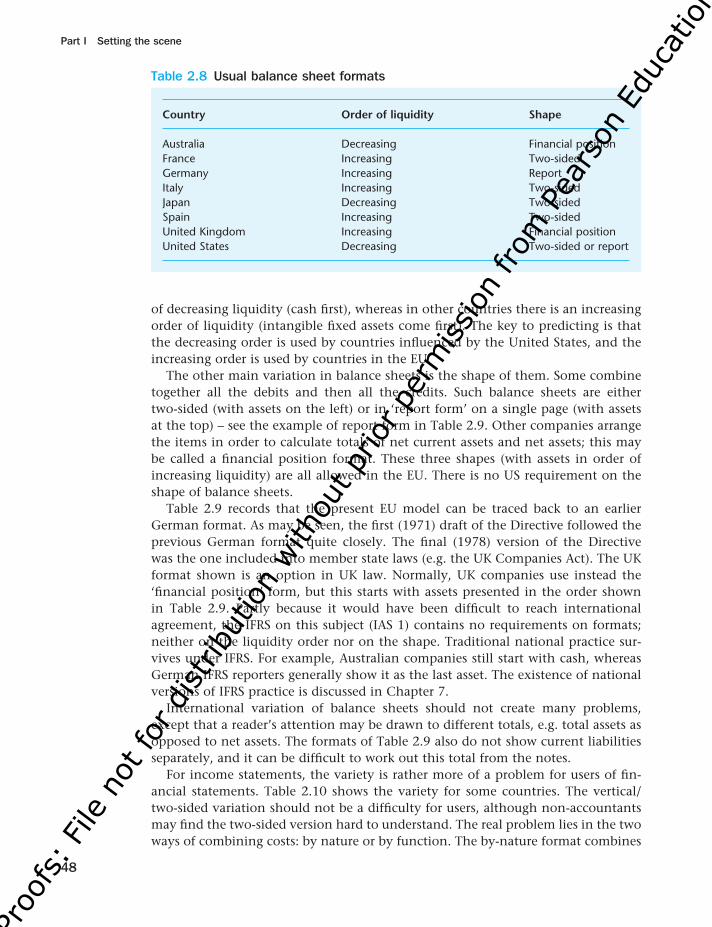

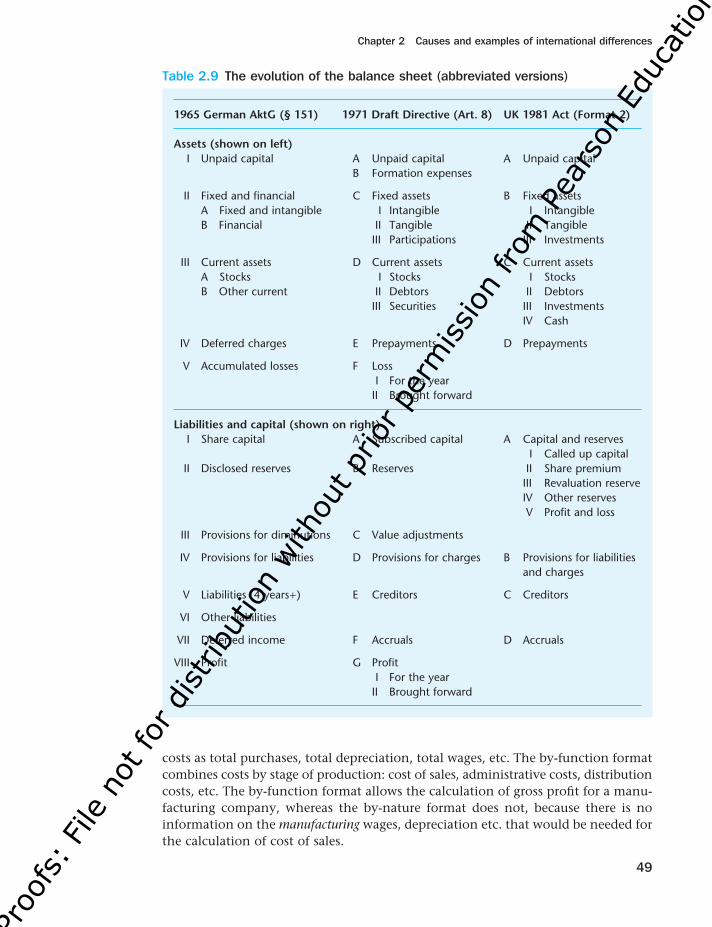

1.1 Differences in financial reporting

If a number of accountants from different countries, or even from one country, aregiven a set of transactions from which to prepare financial statements, they will not produce identical statements. There are several reasons for this. Although allaccountants will follow a set of rules, no set covers every eventuality or is prescrip-tive to the minutest detail. Thus there is always room for professional judgement, ajudgement that will depend in part on the accountants’ environments (e.g. whetheror not they see the tax authorities as the main users of the statements). Moreover,the accounting rules themselves may differ not just between countries but alsowithin countries. In particular the rules for company groups may differ from therules for individual companies. Multinational enterprises (MNEs) which operate as company groups in more than one country may find inter-country differencesparticularly irksome.

Awareness of these differences has led in recent decades to impressive attemptsto reduce them, in particular, by the International Accounting Standards Board(IASB) and by the European Union (EU). The IASB issues International FinancialReporting Standards (IFRS). The EU has issued Directives and Regulations onaccounting and financial reporting. The importance of American stock markets and US-based MNEs has meant that US generally accepted accounting principles(GAAP), the most detailed and best known of all national sets of rules, have greatlyinfluenced rule-making worldwide. The work of all these regulatory agencies hascertainly led to a lessening of international differences but, as this book will show,many still remain and some will always remain.

An example of the differences is provided by the record of GlaxoSmithKline(GSK) and its predecessor GlaxoWellcome (GW) since 1995 when GW was formedby a merger. In 2000, GW merged with SmithKlineBeecham to form GSK. It is listedin New York as well as on the London Stock Exchange, and in accordance withrequirements of the US Securities and Exchange Commission (SEC) it had to pro-vide up to 2006 a reconciliation to US GAAP of its earnings and shareholders’ equityas measured under UK rules (for 2005 and 2006 under IFRS). The differences as dis-closed in Tables 1.1 and 1.2 are startling. Data from other such reconciliations aregiven later in this book. Not all are as extreme as those of GSK, but it is clear thatthe differences can be very large and that no easy adjustment procedure can beused. One reason for this is that the differences depend not only on the differencesbetween two or more sets of rules, but also on the choices allowed to companieswithin those rules. The adoption by listed companies within the EU of IFRS from2005 onwards, and greater convergence between those standards and US GAAP, hasreduced, but not removed, these differences.

Understanding why there have been differences in financial reporting in the past,why they continue in the present, and will not disappear in the future, is one of themain themes of comparative international accounting. In the next two sections ofthis chapter we look at the global environment of accounting and financial report-ing, and in particular at the nature and growth of multinational enterprises. Wethen explore in more depth the reasons for studying comparative internationalaccounting. In the last section we explain the structure of the book.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 4

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

5

..

Table 1.1 GlaxoSmithKline reconciliations of earnings to US GAAP

UK IFRS US Difference£m £m £m (% change)

1995 717 296 −591996 1,997 979 −511997 1,850 952 −491998 1,836 1,010 −451999 1,811 913 −502000 4,106 (5,228) −2272001 3,053 (143) −1052002 3,915 503 −872003 4,484 2,420 −462004 4,302 2,732 −362005 4,816 3,336 −312006 5,498 4,465 −19

Table 1.2 GlaxoSmithKline reconciliations of shareholders’ equity to US GAAP

UK IFRS US Difference £m £m £m (% change)

1995 91 8,168 +8,8761996 1,225 8,153 +5661997 1,843 7,882 +3281998 2,702 8,007 +1961999 3,142 7,230 +1302000 7,517 44,995 +4992001 7,390 40,107 +4432002 6,581 34,992 +4322003 5,059 34,116 +5742004 5,925 34,042 +4752005 7,570 34,282 +3532006 9,648 34,653 +259

1.2 The global environment of accounting

1.2.1 Overview

Accounting is a technology which is practiced within varying political, economic,and social contexts. These have always been international as well as national.Certainly since the last quarter of the twentieth century, the globalization ofaccounting rules and practices has become so important that narrowly nationalviews of accounting and financial reporting can no longer be sustained.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 5

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

6

..

Particularly important parts of the context have been:

l major political issues, such as the dominance of the United States and the expan-sion of the European Union;

l economic globalization, including the liberalization of, and dramatic increasesin, international trade and foreign direct investment;

l the emergence of global financial markets;

l patterns of share ownership, including the influence of privatization;

l changes in the international financial system; and

l the growth of MNEs.

These developments are interrelated and all have affected financial reporting andthe transfer of accounting technology from one country to another. They are nowexamined in turn.

1.2.2 Accounting and world politics

Important political events since the end of the Second World War in 1945 haveincluded: the emergence of the United States and the Soviet Union as the world’stwo superpowers, followed by the collapse of Soviet power at the end of the 1980s;the break-up of the British and continental European overseas empires; and the creation of the European Union, which has expanded from its original core of sixcountries to include, among others, the UK and many former communist countries.More detail on the consequences that these events have had for accounting is givenin later chapters. The following illustrations may suffice for the moment:

l US ideas on accounting and financial reporting have been for many decades, andremain, the most influential in the world. The collapse of the US energy tradingcompany, Enron, in 2001 and the demise of its auditor, Andersen, had repercus-sions in all major economies.

l The development of international accounting standards (at first of little interestin the US) owes more to accountants from former member countries of theBritish Empire than to any other source. The International Accounting StandardsCommittee (IASC) and its successor, the IASB, are based in London; the drivingforce behind the foundation of the IASC, Lord Benson, was a British accountantborn in South Africa.

l Accounting in developing countries is still strongly influenced by the formercolonial powers. Former British colonies tend to have Institutes of CharteredAccountants (set up after the independence of these countries, not before),Companies Acts and private sector accounting standard-setting bodies. FormerFrench colonies tend to have detailed governmental instructions, on everythingfrom double entry to published financial statements, that are set out in nationalaccounting plans and commercial codes.

l Accounting throughout Europe has been greatly influenced by the harmoniza-tion programme of the EU, especially its Directives on accounting and, more

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 6

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

7

..

recently, its adoption of IFRS for the consolidated financial statements of listedcompanies.

l The collapse of communism in Central and Eastern Europe led to a transforma-tion of accounting and auditing in many former communist countries. Thereunification of Germany put strains on the German economy such that largeGerman companies needed to raise capital outside Germany and to change theirfinancial reporting in order to be able to do so.

1.2.3 Economic globalization, international trade and foreign direct investment

A notable feature of the world economy since the Second World War has been theglobalization of economic activity. This has meant the spreading round the worldnot just of goods and services but also of people, technologies and concepts. Thenumber of professionally qualified accountants has greatly increased. Member bodiesof the International Federation of Accountants (IFAC) currently have well over twomillion members. Accountants in all major countries have been exposed to rules,practices and ideas previously alien to them.

Much has been written about globalization and from many different and con-trasting points of view. One attractive approach is the ‘globalization index’ pub-lished annually in the journal Foreign Policy. This attempts to quantify the conceptby ranking countries in terms of their degree of globalization. The components ofthe index are: political engagement (measured, inter alia, by memberships of inter-national organizations); technological connectivity (measured by internet use); personal contact (measured, inter alia, by travel and tourism and telephone traffic);and economic integration (measured, inter alia, by international trade and foreigndirect investment). The compilers of the index acknowledge that not everythingcan be quantified; for example, they do not include cultural exchanges. The rankingof countries varies from year to year but the most globalized countries according tothe index are small open economies such as Singapore, Switzerland and Ireland.Small size is not the only factor, however, and the top 20 typically also include theUS, the UK and Germany. A possible inference from the rankings is that measuresof globalization are affected by national boundaries. How different would the list be if the EU were one country and/or the states of the US were treated as separatecountries?

From the point of view of financial reporting, the two most important aspects ofglobalization are international trade and foreign direct investment (FDI) (i.e. equityinterest in a foreign enterprise held with the intention of acquiring control orsignificant influence). Table 1.3 illustrates one measure of the liberalization andgrowth of international trade: merchandise exports as a percentage of gross domesticproduct (GDP). Worldwide, the percentage has more than trebled since the end ofthe Second World War. The importance of international trade to member states ofthe EU is particularly apparent; much of this is intra-EU trade. At the regional level,economic integration and freer trade have been encouraged through the EU andthrough institutions such as the North American Free Trade Area (NAFTA) (the US,Canada and Mexico). The liberalization has also been due to the dismantling of

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 7

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

8

..

trade barriers through ‘rounds’ of talks under the aegis of the General Agreement onTariffs and Trade (GATT) and its successor the World Trade Organization (WTO).However, trade was under threat in 2008–9 for two connected reasons: the ‘creditcrunch’ and falling demand reduced trade; and rising unemployment led to calls fordomestic industries to be protected against foreign imports.

One area in which trade is insufficiently liberalized is agricultural products, leading to the criticism that liberalization has benefited developed rather thandeveloping countries. For a discussion of both the positive and negative aspects ofinternational trade, see Finn (1996).

The importance of foreign direct investment is illustrated in Table 1.4, which ranksthe 10 leading MNEs by the size of their foreign assets. It also shows the percentagesof their assets, sales and employees that are foreign, and a simple transnationalityindex (TNI), calculated as the average of the percentages. The home countries ofthese MNEs are the UK (three MNEs), France (two), the US (two), Germany,Luxembourg and Japan (one each). The industries represented are electrical equip-ment, oil, motor vehicles, telecommunications, electricity and stores. The UK com-panies, BP and Vodafone, have the highest transnationality indices. Of course, thevery nature of an MNE means that the concept of a ‘home country’ can be ambigu-ous. For example, in Table 1.4, we follow the source of the data by showing RoyalDutch Shell plc as a UK company. Here are some facts about the company:

l it is incorporated in England and Wales;

l its head office is in the Netherlands, as is its tax residency;

l it is listed on stock exchanges in Amsterdam, London and New York;

l it presents its financial statements in US dollars; and

l it has operations in 90 countries and shareholders all over the world.

Table 1.3 Merchandise exports as a percentage of gross domestic product at1990 prices (selected countries, 1950–98)

1950 1973 1998

France 7.7 15.2 28.7Germany 6.2 23.8 38.9Netherlands 12.2 40.7 61.2United Kingdom 11.3 14.0 25.0Spain 3.0 5.0 23.5United States 3.0 4.9 10.1Mexico 3.0 1.9 10.7Brazil 3.9 2.5 5.4China 2.6 1.5 4.9India 2.9 2.0 2.4Japan 2.2 7.7 13.4World 5.5 10.5 17.2

Source: Prepared from Maddison, A. (2001) The World Economy: A Millennial Perspective. Organisation for EconomicCo-operation and Development (OECD), Paris.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 8

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

9

..

Table 1.4 World’s top ten non-financial multinationals ranked by foreign assets, 2008

Foreign % that is foreign ofassets

Company Country Industry (US $bn) Assets Sales Employees TNI

General Electric US Electrical 401 50 53 53 52Royal Dutch Shell UK Oil 222 78 57 83 73Vodafone UK Telecoms 202 92 86 87 89BP UK Oil 189 83 78 82 81Toyota Motor Japan Motors 170 57 64 38 53Exxon Mobil US Oil 161 71 70 63 68Total France Oil 141 85 76 61 75E.On Germany Energy 141 64 42 61 56Electricité de France France Electricity 133 49 47 32 42Arcelor Mittal Luxembourg Steel 127 95 90 76 87

Note: TNI = transnationality index, calculated as an average of the assets, sales and employees percentages.Source: Compiled from data in UNCTAD (2010) World Investment Report 2010. Copyright © United Nations 2010. Reproduced with permission.

Despite this interesting mix, its choice of the UK as country of incorporation hassome major effects, such as:

l the annual report is presented under UK law;

l the auditors (pwc, London) are appointed under UK law;

l the calculation of distributable profit is done under UK law; and

l the UK corporate governance code is followed.

1.2.4 Globalization of stock markets

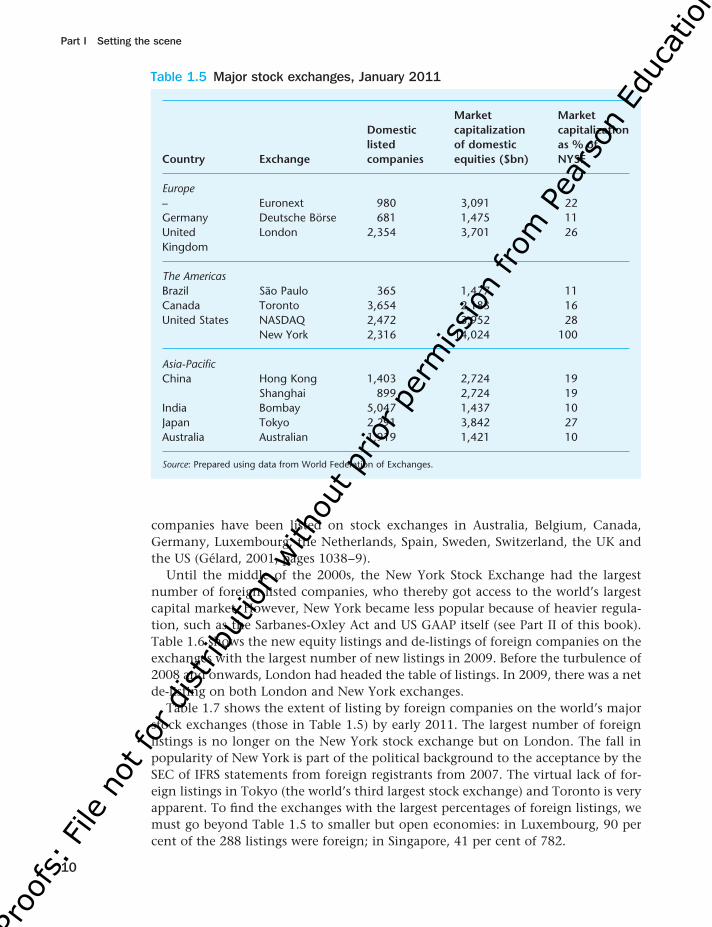

At the same time as international trade and FDI have increased, capital mar-kets have become increasingly globalized. This has been made possible by thederegulation of the leading national financial markets (e.g. the ‘Big Bang’ on theLondon Stock Exchange in 1986); the speed of financial innovation (involving newtrading techniques and new financial instruments of sometimes bewildering com-plexity); dramatic advances in the electronic technology of communications; andgrowing links between domestic and world financial markets. Table 1.5 lists thecountries where there are stock exchanges with more than 350 domestic listed com-panies and also a market capitalization (excluding investment funds) of more thanUS$1,400 billion.

Davis et al. (2003) examine the international nature of stock markets from thenineteenth century onwards, and chart the rise in listing requirements on theLondon, Berlin, Paris and New York exchanges. Michie (2008) also provides aninternational history of stock markets. Precise measures of the internationalizationof the world’s stock markets are hard to construct. Two crude measures are cross-border listings and the extent to which companies translate their annual reportsinto other languages for the benefit of foreign investors. For example, French

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 9

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

10

..

companies have been listed on stock exchanges in Australia, Belgium, Canada,Germany, Luxembourg, the Netherlands, Spain, Sweden, Switzerland, the UK andthe US (Gélard, 2001, pages 1038–9).

Until the middle of the 2000s, the New York Stock Exchange had the largestnumber of foreign listed companies, who thereby got access to the world’s largestcapital market. However, New York became less popular because of heavier regula-tion, such as the Sarbanes-Oxley Act and US GAAP itself (see Part II of this book).Table 1.6 shows the new equity listings and de-listings of foreign companies on theexchanges with the largest number of new listings in 2009. Before the turbulence of2008 and onwards, London had headed the table of listings. In 2009, there was a netde-listing on both London and New York exchanges.

Table 1.7 shows the extent of listing by foreign companies on the world’s majorstock exchanges (those in Table 1.5) by early 2011. The largest number of foreignlistings is no longer on the New York stock exchange but on London. The fall inpopularity of New York is part of the political background to the acceptance by theSEC of IFRS statements from foreign registrants from 2007. The virtual lack of for-eign listings in Tokyo (the world’s third largest stock exchange) and Toronto is veryapparent. To find the exchanges with the largest percentages of foreign listings, wemust go beyond Table 1.5 to smaller but open economies: in Luxembourg, 90 percent of the 288 listings were foreign; in Singapore, 41 per cent of 782.

Table 1.5 Major stock exchanges, January 2011

Market MarketDomestic capitalization capitalizationlisted of domestic as % of

Country Exchange companies equities ($bn) NYSE

Europe– Euronext 980 3,091 22Germany Deutsche Börse 681 1,475 11United London 2,354 3,701 26Kingdom

The AmericasBrazil São Paulo 365 1,477 11Canada Toronto 3,654 2,183 16United States NASDAQ 2,472 3,952 28

New York 2,316 14,024 100

Asia-PacificChina Hong Kong 1,403 2,724 19

Shanghai 899 2,724 19India Bombay 5,047 1,437 10Japan Tokyo 2,291 3,842 27Australia Australian 1,919 1,421 10

Source: Prepared using data from World Federation of Exchanges.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 10

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

11

..

Any particular company might be listed on many exchanges. For example, the2000 annual report of Volvo, the Swedish commercial vehicle company, discloseslistings on the exchanges of five foreign countries; but in 2007 there was only one:the US (the NASDAQ); and by the 2008 annual report the NASDAQ and the Swedishexchange (OMX) had merged, so there was only one listing. Norsk Hydro, theNorwegian power company, reveals listing on seven foreign exchanges in 2000,reduced to the US, UK, Euronext and Germany in 2008; and then to only Londonby 2011.

Table 1.6 Top twelve exchanges for new equity listings in 2009

Listings De-listings

Mexican 42 9New York 36 43London 26 98Luxembourg 26 21NASDAQ 17 33Singapore 10 12Taiwan 10 0Australian 7 7Korean 6 0Toronto 5 12Euronext 5 9Johannesburg 5 4

Source: Compiled from the 2009 Annual Statistics of the World Federation of Exchanges.

Table 1.7 Foreign company listings on major stock exchanges, January 2011

No. As % of total listings

London 600 20New York 520 22NASDAQ 299 11Euronext 153 14Toronto 89 2Australia 88 4Germany 79 10Hong Kong 17 1Tokyo 12 0Brazil 8 2Bombay 0 0Shanghai 0 0

Source: Prepared using data from World Federation of Exchanges.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 11

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

12

..

The above two are very large companies based in rather small countries, whichsuggests one of the main reasons for foreign listing: to attract extra investors and widen the pool of shareholders. For example, Norsk Hydro reports in 2011 that9 per cent of its shares are owned by US shareholders and 6 per cent by UK shareholders. Gray et al. (1994) look at foreign listings of several large Europeancompanies. Saudagaran (1988) found evidence that a company’s size relative to itsdomestic exchange helps to explain foreign listings.

Another reason for foreign listing is that the company wishes to raise its profilein a foreign country among potential customers, employees or regulators. The firstlisting of a German company on a US exchange (Daimler-Benz in 1993) was relatedto the setting up of factories in the US and the expansion of sales. Radebaugh et al.(1995) look in more detail at this particular case. It was followed by a takeover ofthe US car company, Chrysler, that was presented as a ‘merger of equals’ for publicrelations and accounting reasons (see Section 8.7.2).

Of course, as well as potential benefits from foreign listing, there are also costs.These include the expenses of initially satisfying the accounting and other require-ments of the foreign exchange or its regulator, and then the continuing need toprovide extra or different accounting compared to domestic requirements. Biddleand Saudagaran (1989) found evidence of the resistance to extra disclosures byMNEs from eight countries (including the UK), although Gray and Roberts (1997)found no such evidence for UK companies. The world’s largest equity markets arebased in New York, including the New York Stock Exchange and NASDAQ. Theseexchanges have their own requirements but the major problem for companies wishing to list on them is to satisfy the requirement of the Securities and ExchangeCommission (SEC), including the onerous auditing and corporate governancerequirements of the Sarbanes-Oxley Act. Foreign registrants could present full-scaleUS GAAP annual reports but generally they choose instead to file Form 20-F thatcontains many of the normal SEC disclosure requirements but allows non-USaccounting with numerical reconciliations to US GAAP for equity and income.From 2007, if IFRS (as issued by the IASB) is used, a reconciliation is not necessary.

If a non-US company wishes to gain access to US markets without so much cost,it can arrange for its shares to be traded ‘over the counter’ (not fully listed) throughAmerican Depositary Receipts (ADRs). The ADRs (which contain a package of shares)are traded, rather than the shares themselves. The SEC then accepts domesticannual reports without reconciliation to US GAAP. It is also possible to arrange forADRs to be traded on an exchange but then reconciliation is necessary.

Some companies publish their annual reports in more than one language. Themost important reason for this is the need for large MNEs to raise money and havetheir shares traded in the US and the UK. This explains why English is the mostcommon secondary reporting language. Jeanjean et al. (2010) examine various reasons that explain why translation into English is more common in some countriesthan in others.

Other reasons for using more than one language are that the MNE is based in acountry with more than one official language, that the MNE has headquarters inmore than one country or that it has substantial commercial operations in severalcountries. For example, the Finnish telecommunications company, Nokia, pub-lished its annual report and financial statements not only in Finnish and Swedish

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 12

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

13

..

(the two official languages of Finland) but also in English. The Business Review section of the report was also available in French, German, Italian, Portuguese,Spanish, Chinese and Japanese (Parker, 2001b). Evans (2004) discusses the problemsof translating accounting terms from one language to another. Baskerville andEvans (2011) report on the difficulties of translating IFRS, as discovered by con-ducting a survey of translators.

A more sophisticated measure of internationalization is the extent to which stockmarkets have become ‘integrated’, in the sense that securities are priced accordingto international rather than domestic factors (Wheatley, 1988). Froot and Dabora(1999) show that domestic factors are still important even for such Anglo-Dutch‘twin’ stocks as Unilever NV/PLC.

National stock exchange regulators not only operate in their domestic marketsbut also are, through the international bodies to which they belong, such as theInternational Organization of Securities Commissions (IOSCO) and the Committeeof European Securities Regulators (CESR), playing increasingly important roles inthe internationalization of accounting rules (see Chapter 4).

1.2.5 Patterns of share ownership

The globalization of stock markets does not mean uniformity of investor behavioraround the world. Patterns and trends in share ownership differ markedly fromcountry to country. The nature of the investors in listed companies has implicationsfor styles of financial reporting. The greater the split between the owners and man-agers of these companies, the greater the need for publicly available and indepen-dently audited financial statements. La Porta et al. (1999) distinguish companieswhose shares are widely held from those that are family controlled, state controlled,controlled by a widely held financial corporation or controlled by a widely heldnon-financial corporation. According to their data, which cover 27 countries (notincluding China, India and Eastern Europe) in the mid-1990s, 36 per cent of thecompanies in the world were widely held, 30 per cent were family controlled and18 per cent were state controlled. The countries whose largest 20 companies weremost widely held were, in descending order, the UK, Japan, the US, Australia,Ireland, Canada, France and Switzerland. The countries with most family controlwere Mexico, Hong Kong and Argentina. The countries with most state control wereAustria, Singapore, Israel, Italy, Finland and Norway. The countries with companiesheld 15 per cent or more by a widely held financial corporation were Belgium,Germany, Portugal and Sweden.

More up-to-date data are available from surveys of share ownership. These showdifferent trends in different countries. In the US the percentage of householdsinvesting in shares and bonds directly or indirectly grew rapidly from 1989onwards, peaking at 50 per cent in 2001, but falling to 47 per cent by 2008(Investment Company Institute et al., 2008). In the UK at the end of 2006, foreigninvestors held 40 per cent of shares, insurance companies 15 per cent, pensionfunds 13 per cent, individuals 13 per cent, other financial institutions 10 per centand banks 3 per cent. The percentage held by foreign investors has been steadilyincreasing (National Statistics, 2007). Some reasons for this are: international mergerswhere new companies are listed in the UK; the flotation of UK subsidiaries of

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 13

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

14

..

foreign companies in which the foreign parent retains a significant stake; and companies moving their domicile to the UK.

Privatization, i.e. the selling-off of state-owned businesses, has greatly expandedthe private sector in many countries. In the UK, for example, the privatization of public utilities and other publicly owned enterprises from the 1980s onwardsbrought several very large organizations within the ambit of company law andaccounting standards. In the short run this increased the number of shares held bypersons, but many of them later sold out and some companies have deliberatelytried to reduce the number of their small shareholders. Privatization opened com-panies up to foreign ownership, thus stimulating the growth of FDI, and facilitatingtheir expansion into foreign markets. Privatization has been most dramatic in theformer communist countries of Central and Eastern Europe. In some cases, notablyin Russia, privatization has transferred the ownership of large companies from thestate to a small group of so-called ‘oligarchs’. In 2008, many governments around theworld reluctantly bought shares in financial institutions in order to rescue them. So, privatization went, at least temporarily, into reverse.

Having looked above at why a company might seek foreign investors, we nowlook at why an investor might seek foreign opportunities to invest. It is easy, look-ing backwards, to identify countries where shares have risen more rapidly than inone’s own country over the last one, five or ten years. This would argue for overseasinvestment if the past were a good predictor of the future. Even if it is not, a largeinvestor might wish to diversify among several countries because share price move-ments in different regions of the world are not strongly correlated. Gross annualpurchases by foreigners of US securities in 2000 amounted to $7 trillion; and pur-chases by US residents of foreign securities were about half that. These figures hadgrown by about ten times over the previous ten years (Griever et al., 2001).

Nevertheless, Lewis (1999) reports that investors in Europe, Japan and the US putonly about 10 per cent of their investments into foreign shares, which is far belowwhat one would expect if they considered foreign shares to be perfect substitutes fordomestic ones. Choi and Levich (1990) looked at investors from the US, Japan andEurope and found that many were dissuaded from foreign investment by concernabout different accounting practices. Others were put to extra expense in order toadjust the foreign statements. Later, Choi and Levich (1996) found that only abouta quarter of European investors were restrained by international accounting differ-ences. Miles and Nobes (1998) found that London-based investors did not generallyadjust for the accounting differences.

Other reasons for home country bias could include currency risk, political risk,language barriers, transaction costs and taxation. Coval and Moskovitz (1999) foundthat investment managers show regional preferences even within the United States.On a related matter, Helliwell (1998) reported that Canadians are more than tentimes more likely to trade with each other than with the US.

1.2.6 The international financial system

From 1945 to 1972, the international monetary system under the Bretton WoodsAgreement was based on fixed exchange rates with periodic devaluations. From1973, major currencies have floated against each other and exchange rates have

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 14

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

15

..

been very volatile (as illustrated in Table 17.1). Within the EU, however, mostnational currencies, with the notable exception of the pound sterling, were replacedby a single currency, the euro, in 1999. Accounting standard-setters have beenmuch concerned with hedging activities and other transactions in foreign currency.There is discussion of these issues in Chapters 9 and 17.

In 2008 and 2009, the world’s financial system was under exceptional stress. Thecollapse of financial institutions and whole economies led to calls for a new versionof Bretton Woods. It also put the regulation of stock markets in the spotlight. Theuse of market values in accounting was criticized, partly because values were falling(causing losses to be revealed) and partly because markets were not operating sothat a market price was difficult to determine. Academic writers conclude thataccounting is not to blame (André et al., 2009; Barth and Landsman, 2010).

1.3 The nature and growth of MNEs

MNEs may be broadly defined as those companies that produce a good or a servicein two or more countries. ‘MNE’ is an economic category, not a legal one. The sizeof most MNEs is such that they need to raise external finance and hence to be incor-porated companies listed on stock exchanges. As listed companies (i.e. whose sharesare publicly traded), their financial reporting is subject to special regulations thatare discussed at length in Part II of this book. The existence of MNEs brought a new dimension to areas such as auditing, which already existed at the domesticlevel (see Chapter 20). Issues such as the translation of the financial statements offoreign subsidiaries for the preparation of consolidated statements (see Chapter 17)are peculiar to multinational companies. Most of the world’s MNEs produce con-solidated financial statements in accordance with either US GAAP, IFRS or approxi-mations thereto.

The above definition of MNEs is broad enough to include early fourteenth-centuryenterprises such as the Gallerani company, a Sienese firm of merchants that hadbranches in London and elsewhere and whose surviving accounts provide one ofthe earliest extant examples of double entry (Nobes, 1982). From the late sixteenthcentury onwards, chartered land and trading companies – notably the English,Dutch and French East India Companies – were early examples of ‘resource-seeking’MNEs, i.e. those whose object is to gain access to natural resources that are notavailable in the home country. The origins of the modern MNE are to be found inthe period 1870 to 1914, when European people and European investment wereexported on a large scale to the rest of the world and when the United Statesemerged as an industrial power. On the eve of the First World War, the stock ofaccumulated FDI was greatest in, by order of magnitude, the United Kingdom, theUnited States, Germany, France and the Netherlands. Two world wars decreased the relative economic importance of European countries and increased that of the United States. Table 1.8 shows how the rankings changed from 1914 to 2009.After the Second World War, the United States became, as it remains, the world’slargest exporter of FDI. More recently, however, Europe-based multinationals haveregained some of their relative importance and both US and European MNEs were

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 15

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

16

..

challenged, at least for a time, by those of Japan. All these countries are major recipi-ents of FDI as well as providers of it. A few other European countries are now alsoimportant holders of FDI.

MNEs can be classified according to their major activity. Most nineteenth-centuryand earlier multinationals were ‘resource-seeking’. In the twentieth century othertypes have developed. Some MNEs are ‘market-seeking’, i.e. they establish subsidiarieswhose main function is to produce goods to supply the markets of the countries in which they are located. Other MNEs are ‘efficiency-seeking’, i.e. each subsidiaryspecializes in a small part of a much wider product range, or in discrete stages in the production of a particular product. Manufacturing MNEs have also developedsubsidiaries that specialize in trade and distribution, or in providing services such

Table 1.8 Percentage shares of estimated stock of accumulated foreign directinvestment by country of origin, 1914–2009 (%)

1914 1938 1980 1990 2000 2009

United Kingdom 45 40 15 13 14 9United States 14 28 42 24 20 23Germany 14 1 8 8 8 7France 11 9 5 6 7 9Netherlands 5 10 8 6 5 4Japan – – 4 11 4 4

Sources: Based on Dunning (1992) and UNCTC (2010).

Table 1.9 Accumulated stock of outward foreign direct investment as apercentage of GDP in 2005 (selected countries)

Country %

Norway 123Switzerland 107Belgium 104Netherlands 103Sweden 57United Kingdom 56France 41Canada 35Germany 35Italy 17United States 16Japan 9World 24

Source: United Nations Conference on Trade and Development (UNCTAD) (2007) World Investment Report 2007:Transnational Companies, Extractive Industries and Development. Geneva, UNCTAD. Copyright © United Nations2007. Reproduced with permission.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 16

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

17

..

as insurance, banking or finance. Some MNEs, such as the larger banks and accoun-tancy firms, provide services on a global basis. Improvements in technology haveled to the creation of overseas subsidiaries specializing in information transfer.

The extent to which the production of goods and services has been internation-alized varies between countries and industries. The United States has the world’shighest absolute value of FDI, but the size of its economy is such that investmentoverseas is relatively less important for the United States than for many Europeancountries, although it is higher in percentage terms than that of Japan (see Table 1.9).Table 1.10 demonstrates the extent to which the headquarters of the largest MNEsare located in the European Union, US and Japan. However, the number for Chinaincreased from 29 to 46 in two years.

Economists and others have sought to explain why MNEs exist. The most favored explanation is Dunning’s eclectic paradigm, which states that the propensityfor firms of a particular country to engage in, or to increase, overseas production is

Table 1.10 Share of the world’s top 500 MNEs by revenues, 2010

France 39Germany 37United Kingdom 29Netherlands 13Spain 10Italy 11Sweden 5Belgium 5Austria 3Denmark 2Finland 1Ireland 2Belgium/Netherlands 1UK/Netherlands 1Other EU 1Total EU 160United States 139Japan 71China 46Switzerland 15South Korea 10Canada 11Australia 8India 8Taiwan 8Brazil 7Russia 6Mexico 2Singapore 2Other countries (one each) 7

500

Source: Prepared from Fortune Global 500 (2010).

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 17

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

18

..

determined by three interrelated conditions. These are the extent to which theenterprises possess, or can gain privileged access to, assets that provide them with a competitive advantage over local firms; the extent to which relative transactioncosts make it appropriate for the enterprises to use such advantages themselvesrather than to license or franchise them to other firms; and the extent to which rel-evant costs and government policies push enterprises towards locating productionoverseas rather than towards meeting demand by exports from the home country.An important consequence of the growth of multinational enterprise is that muchof the world’s trade takes place within firms as well as between countries. The pricesat which the transactions take place are internal transfer prices, which are often notthe same as open market prices. This has important implications for taxation, man-agement control and the relationships between MNEs and their host countries.

The rise of the MNE is one of the main factors responsible for the international-ization of the accountancy profession. Accountancy firms have followed their clientsaround the world, setting up new offices overseas and/or merging with overseasfirms. The audit of MNEs is considered further in Chapter 20.

1.4 Comparative and international aspects of accounting

Given the global context set out above, there are clearly strong arguments for study-ing international accounting. Moreover, there are at least three reasons why a com-parative approach is appropriate. First, it serves as a reminder that the US and otherAnglo-Saxon1 countries are not the only contributors to accounting as it is practicedtoday. Secondly, it demonstrates that the preparers, users and regulators of finan-cial reports in different countries can learn from each others’ ideas and experiences.Thirdly, it explains why the international harmonization of accounting has beendeemed desirable but has proved difficult to achieve (Parker, 1983). These three reasons are now looked at in more detail.

Historically, a number of countries have made important contributions to thedevelopment of accounting. The Romans had forms of bookkeeping and the calcu-lation of profit, although not double entry. In the Muslim world, while ChristianEurope was in the Dark Ages, developments in arithmetic and bookkeeping pavedthe way for later progress. In the fourteenth and fifteenth centuries, the Italian citystates were the leaders in commerce, and therefore in accounting. The ‘Italianmethod’ of bookkeeping by double entry spread first to the rest of Europe and even-tually round the whole world. One lasting result of this dominance is the numberof accounting and financial words in English and other languages that are of Italianorigin. Some examples in English are bank, capital, cash, debit, credit, folio andjournal.

In the nineteenth century, Britain took the lead in accounting matters, to be fol-lowed in the twentieth century by the United States. As a result, English has become

1 This expression is used in this book with its common European meaning, i.e. the UK, the US and other mainlyEnglish-speaking countries such as Canada, Australia and New Zealand.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 18

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

19

..

established as the world’s language of accounting (Parker, 2000, 2001a). Table 1.11,which gives details of some members of IFAC, shows, inter alia, that the modernaccountancy profession developed first in Scotland and England. The table alsoshows that some countries (e.g. Australia, Canada and the UK) have more than one

Table 1.11 Age and size of some members of IFAC

Approx. membersCountry Body Founding date∗ 2010 (000s)

Australia CPA Australia 1952 (1886) 132

Institute of Chartered Accountants in Australia 1928 (1885) 54

Brazil Conselho Federal de Contabilidade 1946 292

Canada Canadian Institute of Chartered

Accountants 1902 (1880) 78

China Chinese Institute of Certified

Public Accountants 1988 140+†

France Ordre des Experts Comptables 1942 19

Germany Institut der Wirtschaftsprüfer 1932 13

India Institute of Chartered Accountants of India 1949 162

Japan Japanese Institute of Certified Public Accountants 1948 (1927) 20‡

Netherlands Koninklijk Nederlands Instituut van Registeraccountants 1967 (1895) 14

New Zealand Institute of Chartered Accountants of New Zealand 1909 (1894) 32

United Kingdom Institute of Chartered Accountants in and Ireland England and Wales 1880 (1870) 136

Institute of Chartered Accountants of Scotland 1951 (1854) 19

Association of Chartered Certified Accountants 1939 (1891) 140

Chartered Institute of Management Accountants 1919 83

Institute of Chartered Accountants in Ireland 1888 20

United States American Institute of Certified

Public Accountants 1887 348

∗ Dates of earliest predecessor bodies in brackets. The names of some of the bodies have changed from time to time.† The website of the CICPA in March 2011 refers to 140,000 members in May 2006.‡ Excluding junior CPAs.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 19

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

20

..

important accountancy body. A multiplicity of bodies has been the norm in Anglo-Saxon countries. The largest body is the American Institute of Certified PublicAccountants.

Table 1.11 does not show rates of growth; the Chinese Institute of CertifiedPublic Accountants has grown in recent years to become the fourth largest in theworld. The table also does not show the extent to which bodies have worldwide andnot just national membership. Two UK-based bodies, the ACCA and the CIMA,have been notably active and successful in this regard. A look at the table also sug-gests that some countries have far more accountants per head of population thanothers: compare, for example, France (population 60 million; accountants 19,000)and New Zealand (population 4 million; accountants 32,000). Of course, compari-sons such as these depend in part on how the term ‘accountant’ is defined in eachcountry. There is further discussion of the accountancy profession in Chapter 2.

Table 1.12 demonstrates the overwhelmingly British and American origins of thelargest international accountancy firms. Accounting techniques, institutions andconcepts have been imported and exported around the world. Britain, for example,not only has imported double entry from Italy and exported professional accoun-tancy to the rest of the world, but also has exported the concept of a true and fairview, first to the other countries of the British Commonwealth and, more recently,to the other member states of the European Union (Parker, 1989; Nobes, 1993). Theconcepts and practices of management accounting throughout the industrializedworld owe much to American initiatives. In the second half of the twentieth century, Japan contributed to management accounting and control. Carnegie andNapier (2002) make a persuasive case for the study of comparative internationalaccounting history.

The second reason for taking a comparative approach is that it allows one tolearn from both the achievements and failures of others and to avoid the perils ofaccounting ethnocentrism. It is possible for a country to improve its own accountingby observing how other countries react to problems that, especially in industrializednations, may not differ markedly from those of the observer’s home country. It isalso possible to examine whether, where accounting methods differ, the differencesare justified by differences in the economic, legal and social environment and arenot merely the accidents of history. Such accidents may not impede harmonization(see Section 2.6), whereas more fundamental differences are likely to be much moredifficult to deal with.

Table 1.12 Leading international accountancy firms, 2012

Main countries of origin

Deloitte UK, USA, Canada, Japan

Ernst & Young USA, UK

KPMG Netherlands, UK, USA, Germany

PricewaterhouseCoopers UK, USA

Note: The names given above are those of the international firms. National firms may have different names.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 20

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

21

..

A feature of recent decades has been the extent to which countries have beenwilling to adopt and adapt accounting methods and institutions from other coun-tries. Examples will be found in many of the chapters of this book. The UK acceptedcontinental European ideas about greater uniformity in the layout of financial state-ments. France and Germany accepted US and UK approaches to consolidated state-ments. The Netherlands accepted a much greater degree of regulation of companyaccounting and auditing than previously. France and Australia set up their own versions of the US Securities and Exchange Commission (SEC). Germany, whereenforcement of accounting standards had been weak, adopted a compromisebetween the SEC and the UK Financial Reporting Review Panel. Even the US, shakenby accounting scandals from 2001 onwards, is showing itself willing to consider thevirtues of the principles approach to accounting standard setting espoused in theUK and by the IASB.

The third reason for taking a comparative approach is better to understand harmonization, a process that has grown steadily in importance since the 1970s.The arguments for and against are considered in Chapter 4. At this point it may be noted that, as is demonstrated later in this book, major problems such as leaseaccounting, consolidation accounting and foreign currency translation have beentackled in different countries in significantly different ways, although a pattern maysometimes be discerned. Solutions devised by the Financial Accounting StandardsBoard (FASB) in the US – the world’s most powerful national accounting standard-setting body – have been very influential but have not always been accepted.Indeed, one reason for the acceptance by many countries and companies of inter-national standards is that they are not US GAAP.

The growing strength of the IASB and the adoption of its standards by the EU (in part in order to prevent EU-based MNEs adopting US GAAP) can be seen as a process of regulatory competition (Esty and Geradin, 2001), with the IASB and theFASB competing in a ‘race to the top’. The process of harmonization within the EUmeant that all the major countries had their own regulatory solutions challengedand had to accept compromises of both a technical and a political nature. It is clearthat any attempt to harmonize financial reporting touches on wider issues thanaccounting. In Chapter 2 we look at some of the underlying reasons for the differ-ences that exist. Before that, we explain the structure of this book.

1.5 Structure of this book

1.5.1 An outline

The book is divided into six parts. Part I sets the context, covering the causes andnature of differences in financial reporting, classification of accounting systems,and an introduction to international harmonization. Part II deals with financialreporting by listed groups, which is dominated worldwide by IFRS and US GAAP.Part III looks at financial reporting in China and Japan. Part IV covers the financialreporting (particularly that by individual legal enterprises in Europe) that continuesto be governed by sets of national rules, some of which differ considerably from

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 21

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

22

..

IFRS and US GAAP. Part V examines some major technical accounting issues relatedto group reporting by MNEs. Part VI examines some international issues of enforce-ment and analysis.

The chapters in the six parts of the book are described in more detail below.

1.5.2 Setting the scene (Part I)

The adoption of IFRS by the European Union and the convergence of IFRS and USGAAP, both formally agreed in 2002, have not removed the differences in financialreporting among countries. This is partly because IFRS is used in many countriesonly for consolidated statements, and partly because different national versions of IFRS practice exist. The causes and nature of these differences are discussed inChapter 2. Several writers on international accounting have attempted classificationsof financial reporting. These are discussed and evaluated in Chapter 3. Most classi-fications have been of countries, which are explicitly or implicitly assumed to have homogeneous financial reporting. More recently the emphasis has shifted to‘accounting systems’, in recognition of the fact that countries (and even companies)can use more than one type of accounting. In this book we discuss differencesbetween countries, between systems and between companies. This examination ofinternational differences and patterns in them leads to Chapter 4, which discussesinternational harmonization, explaining why and how the need for this has grownin recent decades. We particularly look at the extent to which it has been met bythe establishment of the IASC and its successor the IASB.

1.5.3 Financial reporting by listed groups using IFRS or US GAAP (Part II)

Chapter 5 follows on from the material of Chapter 4 by exploring the relationshipbetween international and national standards, including ‘competition’ and ‘con-vergence’ between IFRS and the most influential set of national standards, USGAAP. The chapter also introduces the analysis of financial statements in an inter-national context. The requirements of IFRS are summarized in Chapter 6, first interms of topics (conceptual framework, assets, liabilities, group accounting, disclos-ures) and secondly in the numerical order of extant standards. Chapter 7 examinesthe possible motives and opportunities for different national versions of IFRS practice. Chapter 8 describes and analyzes corporate financial reporting and itsenvironment in the US, and includes a comparison of US rules with internationalrules. The plans for the replacement of US GAAP with IFRS are discussed. Chapter 9examines some major topics of financial reporting by comparing IFRS and USGAAP. We leave issues specifically related to consolidation for later (Chapter 16).The setting of accounting rules is in part a political issue, and Chapter 10 thereforeexamines the politicization of accounting and particularly political lobbying by pre-parers of financial statements.

1.5.4 China and Japan (Part III)

Chapter 11 compares and contrasts financial reporting in the two major economiesof East Asia: China and Japan. Both have been and still are subjected to a variety of

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 22

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

23

..

outside influences, but both retain their own special national characteristics. Thechapter examines accounting by both listed and unlisted companies, and account-ing for both individual companies and groups.

1.5.5 Financial reporting by individual companies (Part IV)

Financial reporting by individual business enterprises is much more diverse thanthat of listed company groups. Chapter 12 explains why this is the case, with spe-cial emphasis on the information needs of tax authorities and the determination ofdistributable profit. This chapter also examines the IFRS for SMEs. Chapter 13 looksat the attempts that have been made to harmonize the great variety of financialreporting that exists within the EU, as part of a more general aim of eliminating economic barriers. The chapter explains the initial difficulties of reconcilingContinental European and Anglo-Saxon approaches, and the more recent problemsof the accession to the EU of many economies which have had to make a transitionfrom communist to market-based accounting. Chapter 14 analyzes the differentways of rule-making that have evolved in Europe (accounting plans, legal codes,statutes, standards) and assesses their usefulness. Chapter 15 explains how theaccounting rules applicable to individual business enterprises may differ from IFRSor US GAAP, with particular reference to France, Germany and the UK.

1.5.6 Group accounting issues in reporting by MNEs (Part V)

Accounting standards are always in a state of change and those contained withinIFRS and US GAAP are no exception. It is never sufficient merely to learn thedetailed content of standards at a particular date. All standards are compromisesand this is especially so when they have to be agreed at an international level.Chapters 16 to 18 examine three problems which relate especially to MNEs: con-solidated financial statements, foreign currency translation and segment reporting,with comparisons of the solutions arrived at in IFRS and US GAAP.

1.5.7 Enforcement and analysis (Part VI)

This Part looks at the final stages in the process that leads from transactions tobookkeeping to financial reporting to monitoring/enforcement and eventually tointerpretation of the financial statements. Chapter 19 discusses how the applicationof IFRS and US GAAP to the financial statements of listed groups is governed andenforced in the US, in leading member states of the EU (UK, France and Germany),and in other important countries such as Australia, China and Japan. A major com-ponent of monitoring and enforcement is external auditing. Chapter 20 explainshow auditing has been internationalized, with particular reference to the role ofMNEs, international capital markets, international accounting firms and IFRS. Itlooks at international standards on auditing (ISAs), the international audit processin practice and the audit expectations gap in an international context. Chapter 21arrives at the final goal. It examines the problems faced by readers and analysts offinancial statements in an international context. These problems have been lessenedbut not removed by the increasing use of IFRS.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 23

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

24

..

SUMMARY

l The scale of international differences in corporate financial reporting remains large,despite the adoption of IFRS for listed companies within the EU and elsewhere.

l Financial reporting since the Second World War has taken place within a globalcontext which has been characterized by: vast changes in world politics; dramaticgrowth in international trade and foreign direct investment (FDI); the globaliza-tion of stock markets; varying patterns of share ownership; an unstable interna-tional monetary system; and the rise of MNEs, which are the main exporters andimporters of FDI and a major factor in the internationalization of the accoun-tancy profession.

l Historically, several countries have made important contributions to the develop-ment of accounting and financial reporting.

l The comparison of accounting rules and practices between countries is a strongantidote to accounting ethnocentrism. Successful innovations in one country arebeing copied in others.

l Harmonization is taking place at both regional and international levels.

l This book is arranged into six parts: setting the scene; financial reporting by listedgroups using IFRS or US GAAP; China and Japan; financial reporting by individualcompanies; major issues for MNEs; and enforcement and analysis.

André, P., Cazavan-Jeny, A., Dick, W., Richard, C. and Walton, P. (2009) ‘Fair value account-ing and the banking crisis in 2008: shooting the messenger’, Accounting in Europe, Vol. 6,No. 1, pp. 3–24.

Barth, M. and Landsman, W. (2010) ‘How did financial reporting contribute to the financialcrisis?’, European Accounting Review, Vol. 19, No. 3, pp. 399–423.

Baskerville, R. and Evans, L. (2011) The Darkening Glass: Issues for Translation of IFRS, Instituteof Chartered Accountants of Scotland, Edinburgh.

Biddle, G.C. and Saudagaran, S.M. (1989) ‘The effect of financial disclosure levels on firms’choices among alternative foreign stock exchange listings’, Journal of International FinancialManagement and Accounting, Vol. 1, No. 1.

Carnegie, G.D. and Napier, C.J. (2002) ‘Exploring comparative international accounting history’, Accounting, Auditing & Accountability Journal, Vol. 15, No. 5.

Choi, F.D.S. and Levich, R.M. (1990) The Capital Market Effects of International AccountingDiversity, Dow Jones-Irwin, Homewood.

Choi, F.D.S. and Levich, R.M. (1996) ‘Accounting diversity’, in B. Steil (ed.) The EuropeanEquity Markets, Royal Institute of International Affairs, London.

Coval, J.D. and Moskovitz, T.J. (1999) ‘Home bias at home: local equity preferences in domes-tic portfolios’, Review of Financial Studies, Vol. 7, No. 1, pp. 2045–73.

Davis, L., Neal, L. and White, E.N. (2003) ‘How it all began: the rise of listing requirementson the London, Berlin, Paris, and New York Stock Exchanges’, International Journal ofAccounting, Vol. 38, No. 2.

Dunning, J.H. (1992) Multinational Enterprises and the Global Economy, Addison-Wesley,Wokingham.

Esty, D.C. and Geradin, D. (eds) (2001) Regulatory Competition and Economic Integration, OxfordUniversity Press, Oxford.

References

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 24

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 1 Introduction

25

..

Evans, L. (2004) ‘Language, translation and the problem of international accounting com-munication’, Accounting, Auditing & Accountability Journal, Vol. 17, No. 2.

Finn, D. (1996) Just Trading. On the Ethics and Economics of International Trade, Abingdon Press,Nashville.

Froot, K.A. and Dabora, E.M. (1999) ‘How are stock prices affected by the location of trade?’,Journal of Financial Economics, August.

Gélard, G. (2001) ‘France – individual accounts’, in D. Ordelheide and KPMG, TransnationalAccounting, Vol. 2, Palgrave Publishers, Basingstoke.

Gray, S.J., Meek, G.K. and Roberts, C.B. (1994) ‘Financial deregulation, stock exchange listingchoice, and the development of a European capital market’, in Zimmerman, V.K. (ed.) TheNew Europe: Recent Political and Economic Implications for Accountants and Accounting, Centerfor International Education and Research in Accounting, University of Illinois.

Gray, S.J. and Roberts, C.B. (1997) ‘Foreign company listings on the London Stock Exchange:Listing patterns and influential factors’, in T.E. Cooke and C.W. Nobes (eds) TheDevelopment of Accounting in an International Context, Routledge, London.

Griever, W.L., Lee, G.A. and Warnock, F.E. (2001) ‘The U.S. system for measuring cross-borderinvestment in securities: a primer with a discussion of recent developments’, Federal ReserveBulletin, Vol. 87, No. 10, pp. 634–50.

Helliwell, J. (1998) How Much Do National Borders Matter?, Brookings Institution, Washington, DC.Investment Company Institute and the Securities Industry and Financial Markets Association

(2008) Equity and Bond Ownership in America. 2008. Available at www.ici.org/statements.Jeanjean, T., Lesage, C. and Stolowy, H. (2010) ‘Why do you speak English (in your annual

report)?’, International Journal of Accounting, Vol. 45, No. 2, pp. 220–23.La Porta, R., Lopez-de-Silanes, F. and Shleifer, A. (1999) ‘Corporate ownership around the world’,

Journal of Finance, April.Lewis, K.K. (1999) ‘Trying to explain home bias in equities and consumption’, Journal of

Economic Literature, Vol. 37, pp. 571–608.Maddison, A. (2001) The World Economy. A Millennial Perspective, OECD, Paris.Michie, R. (2008) The Global Securities Market. A History, Oxford University Press, Oxford.Miles, S. and Nobes, C.W. (1998) ‘The use of foreign accounting data in UK financial institu-

tions’, Journal of Business Finance and Accounting, Vol. 25, Nos. 3 & 4.National Statistics (2007) Share Ownership 2006. Available at www.statistics.gov.uk.Nobes, C.W. (1982) ‘The Gallerani account book of 1305–8’, Accounting Review, April.Nobes, C.W. (1993) ‘The true and fair view requirement: impact on and of the Fourth Directive’,

Accounting and Business Research, Winter.Parker, R.H. (1983) ‘Some international aspects of accounting’, in S.J. Gray (ed.) International

Accounting and Transnational Decision, Butterworths, London.Parker, R.H. (1989) ‘Importing and exporting accounting: the British experience’, in A.G.

Hopwood (ed.) International Pressures for Accounting Change, Prentice Hall, London.Parker, R.H. (2000) ‘Why English?’ Accountancy, August.Parker, R.H. (2001a) ‘European languages of account’, European Accounting Review, Vol. 10,

No. 1.Parker, R.H. (2001b) ‘Read with care’, Accountancy, June.Radebaugh, L.H., Gebhart, G. and Gray, S.J. (1995) ‘Foreign stock exchange listings: a case

study of Daimler-Benz’, Journal of International Financial Management and Accounting, Vol. 6,No. 2, pp. 158–92.

Saudagaran, S.M. (1988) ‘An empirical study of selected factors influencing the decision to listin foreign stock exchanges’, Journal of International Business Studies, Spring, pp. 101–27.

United Nations Center on Transnational Corporations (UNCTC) (2010) World Investment Report.Wheatley, S. (1988) ‘Some tests of international equity integration’, Journal of Financial

Economics, Vol. 21, No. 2.

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 25

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Useful websites

QUESTIONS

Part I Setting the scene

26

..

Accounting Education www.accountingeducation.com

British Accounting Association www.baa.group.shef.ac.uk

European Accounting Association www.eaa-online.org

International Accounting Standards Board www.ifrs.org

International Federation of Accountants www.ifac.org

United Nations Conference on Trade and Development www.unctad.org

World Bank www.worldbank.org

World Federation of Exchanges www.world-exchanges.org

World Trade Organization www.wto.org

Suggested answers to the asterisked questions are given at the end of the book.

1.1∗ What effects have the major political events in the world since the end of theSecond World War had on accounting and financial reporting?

1.2∗ Why have the major accounting firms become ‘international’? From what coun-tries have they mainly originated? Why?

1.3 What major contributions to accounting and its terminology have been made historically by the following countries: Italy, the United Kingdom, the UnitedStates, Japan?

1.4 Which are the top three countries in respect of each of:

(a) share of the world’s top 500 companies;(b) number of qualified accountants;(c) market capitalization of stock exchange?

Why is the answer not the same for all three questions?

1.5 What factors have made possible the ‘internationalization’ of the world’s stockmarkets?

1.6 What factors have led to the establishment of multinational enterprises?

1.7 Which countries historically have been the home countries of MNEs? Are they thesame countries from which international accounting firms have originated?

1.8 Why are there more accountants per head of population in New Zealand than inFrance?

1.9 Why are some EU companies listed on non-European (especially North American)stock exchanges?

1.10 Why is English the leading language of international corporate financial reporting?

C01_NOBE3796_12_SE_M01.qxd 18/1/12 8:55 Page 26

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

..

2 Causes and examples of international differences

CONTENTS

OBJECTIVES

2.1 Introduction2.2 Culture2.3 Legal systems2.4 Providers of finance2.5 Taxation2.6 Other external influences2.7 The profession2.8 Conclusion on the causes of international differences2.9 Some examples of differences

2.9.1 Conservatism and accruals2.9.2 Provisions and reserves2.9.3 Measurement of assets2.9.4 Financial statement formats

SummaryReferencesQuestions

After reading this chapter, you should be able to:

l discuss the degree to which international cultural differences might explainaccounting differences;

l outline the two main types of legal system to be found in the Western world andhow these are related to accounting differences;

l explain how the predominant methods of financing of companies can differinternationally and how this may affect the purpose and nature of accounting;

l illustrate the linkages between taxation and financial reporting, and show howthese are stronger in some countries than in others;

l outline the relationships between international accounting variations and differencesin the accountancy profession;

l synthesize all the above relationships to begin to explain international differences infinancial reporting;

l outline various ways in which accounting under German national rules is moreconservative than that under UK rules;

l explain the difference between a provision and a reserve, and show how thedefinition of provision is wider in some countries than in others;

l outline the main valuation bases used for assets in major countries;

l summarize the international differences in formats of financial statements.

27

C02_NOBE3796_12_SE_M02.qxd 18/1/12 9:14 Page 27

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Part I Setting the scene

28

..

2.1 Introduction

That there are major international differences in accounting practices is not obviousto all accountants, let alone to non-accountants. The latter may see accounting assynonymous with double entry, which is indeed similar universally. Much of thisbook investigates the major differences in accounting. Some examples are given in Section 2.9. As a prelude to this, we try to identify the likely causes of the differ-ences. It is not possible to be sure that the factors discussed below cause them, buta relationship can be established and reasonable deductions made.

A large list of possible causes of international differences can be found in the writings of previous researchers (e.g. Choi and Meek, 2008, Chapter 2; Radebaugh,Gray and Black, 2006, Chapter 3). Some researchers have used their estimates of suchcauses as a means of classifying countries by their accounting systems (see Chapter 3).Other researchers have studied whether perceived differences in accounting practicescorrelate with perceived causal factors (e.g. Frank, 1979; Doupnik and Salter, 1995).

Jaafar and McLeay (2007) examine whether accounting differences between com-panies are mainly influenced by a company’s country, size, sector or number ofstock exchange listings. They find that all these factors have some effect, but coun-try is far more important than all the other factors. Jaafar and McLeay’s research isset in the context of national accounting systems, before the widespread use of IFRS.The same applies to most of this chapter. However, we will see later (e.g. Chapters 3and 7) that the national influences still affect practices under IFRS.

Before going further, it is also important to define ‘accounting’. In this context,we mean published annual financial reporting by companies. By ‘accounting system’,we mean the set of financial reporting practices used by a particular company foran annual report. Different companies in a country may use different accountingsystems. The same applies to different purposes. For example, in many EU countries,consolidated statements are prepared using IFRS whereas unconsolidated statementsuse national rules. This chapter investigates why and how national systems differ.However, the ideas here can be used to explain why different countries might exhibitdifferent styles of IFRS practice, as explained further in Chapter 7.

Several factors that seem linked to the differences in accounting systems are nowexamined. These are not necessarily causes of the differences; they might be results,as will be discussed later.

2.2 Culture

Clearly, accounting is affected by its environment, including the culture of thecountry in which it operates. Hofstede (1980) develops a model of culture as the collective programming of the mind that distinguishes the members of one humangroup from another. Hofstede argues that, much as a computer operating systemcontains a set of rules that acts as a reference point and a set of constraints tohigher-level programs, so culture includes a set of societal values that drives institutional form and practice. As Gray (1988, page 5) notes:

C02_NOBE3796_12_SE_M02.qxd 18/1/12 9:14 Page 28

Proo

fs: File n

ot fo

r di

strib

ution

with

out p

rior pe

rmission

from

Pea

rson

Edu

catio

n

Chapter 2 Causes and examples of international differences

29

..

societal values are determined by ecological influences and modified by external factors. . . In turn, societal values have institutional consequences in the form of the legal system,political system, nature of capital markets, patterns of corporate ownership and so on.

Culture in any country contains the most basic values that an individual mayhold. It affects the way that individuals would like their society to be structured andhow they interact with its substructure. Accounting may be seen as one of thosesubstructures. As Gray (1988, page 5) explains:

the value systems or attitudes of accountants may be expected to be related to and derivedfrom societal values with special reference to work related values. Accounting ‘values’ willin turn impact on accounting systems.

To get some idea of the basic cultural patterns of various countries, we turn againto Hofstede. Based on a study of over 100,000 IBM employees in 39 countries,Hofstede (1984, pages 83, 84) defined and scored the following four basic dimensionsof culture, which can be summarized as follows:

1 Individualism versus collectivism. Individualism means a preference for a looselyknit social framework in society wherein individuals are supposed to take care ofthemselves and their immediate families only. The fundamental issue addressedby this dimension is the degree of interdependence that a society maintainsamong individuals.