Pareto Oil & Offshore Conference 2013 - KrisEnergy Corporate Presentation... · Pareto Oil &...

18

Pareto Oil & Offshore Conference 2013 KrisEnergy’s IPO was sponsored by CLSA Singapore Pte Ltd and Merrill Lynch (Singapore) Pte. Ltd. (the “Joint Issue Managers, Global Coordinators, Bookrunners and Underwriters”) as joint issue managers, global coordinators, bookrunners and underwriters of the Offering. The Joint Issue Managers, Global Coordinators, Bookrunners and Underwriters assume no responsibility for the contents of this presentation.

Transcript of Pareto Oil & Offshore Conference 2013 - KrisEnergy Corporate Presentation... · Pareto Oil &...

Pareto Oil & Offshore Conference 2013 KrisEnergy’s IPO was sponsored by CLSA Singapore Pte Ltd and Merrill Lynch

(Singapore) Pte. Ltd. (the “Joint Issue Managers, Global Coordinators,

Bookrunners and Underwriters”) as joint issue managers, global coordinators,

bookrunners and underwriters of the Offering. The Joint Issue Managers, Global

Coordinators, Bookrunners and Underwriters assume no responsibility for the

contents of this presentation.

DISCLAIMER

The information in this document is in summary form and should not be relied upon as a complete and accurate representation of any

matters that a potential investor should consider in evaluating KrisEnergy Ltd (the “Company”). While management has taken every effort

to ensure the accuracy of the material in the presentation, neither the Company nor its advisers has verified the accuracy or

completeness of the information, or any statements and opinions contained in this presentation. This presentation is provided for

information purposes only, and to the maximum extent permitted by law, the Company, its officers and management exclude and disclaim

any liability in respect of the authenticity, validity, accuracy, suitability or completeness of, or any errors in or omission from, any

information, statement or opinion contained in this presentation or anything done in reliance on the presentation.

This presentation may contain forward looking statements. The words 'anticipate', 'believe', 'expect', 'project', 'forecast', 'estimate', 'likely',

'intend', 'should', 'could', 'may', 'target', 'plan‘ and other similar expressions are intended to identify forward-looking statements. Indications

of, and guidance on, future earnings and financial position and performance are also forward-looking statements. Forward-looking

statements are subject to risk factors associated with the Company’s business, many of which are beyond the control of the Company. It

is believed that the expectations reflected in these statements are reasonable but they may be affected by a variety of variables and

changes in underlying assumptions which could cause actual results or trends to differ materially from those expressed or implied in such

statements. There can be no assurance that actual outcomes will not differ materially from these statements. You should not place undue

reliance on forward-looking statements and neither KrisEnergy Ltd. nor any of its directors, employees, servants, advisers or agents

assume any obligation to update such information.

The Company is an exploration and development company and must continue to fund its exploration, feasibility and possibly development

programs through its cash reserves, equity capital or debt. Therefore the viability of the Company is dependent upon the Company’s

access to further capital through debt, equity or otherwise. There can be no guarantee that the Company will be able to successfully raise

such finance.

This presentation should not be considered as an offer or invitation to subscribe or purchase any securities in the Company or as an

inducement to make an offer or invitation with respect to those securities. No agreement to subscribe for securities in the Company will be

entered into on the basis of this presentation. You should not act and refrain from acting in reliance on this presentation material. Nothing

contained in this presentation constitutes investment, legal, tax or other advice. This overview of KrisEnergy Ltd. does not purport to be

all inclusive or to contain all information which its recipients may require in order to make an informed assessment of the Company’s

prospects. Before making an investment decision, you should conduct, with the assistance of your broker or other financial or

professional adviser, your own investigation in light of your particular investment needs, objectives and financial circumstances and

perform your own analysis in order to satisfy yourself as to the accuracy and completeness of the information, statements and opinions

contained in this presentation and making any investment decision.

2

© 2013 KrisEnergy Limited

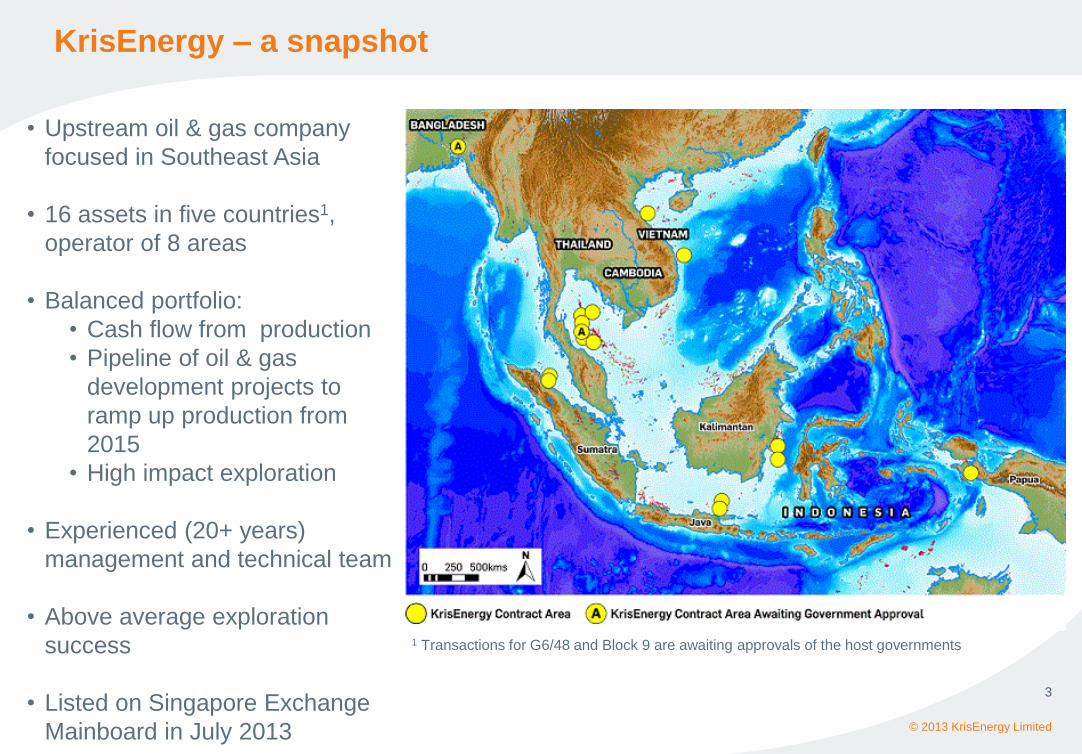

KrisEnergy – a snapshot

© 2013 KrisEnergy Limited

3

• Upstream oil & gas company

focused in Southeast Asia

• 16 assets in five countries1,

operator of 8 areas

• Balanced portfolio:

• Cash flow from production

• Pipeline of oil & gas

development projects to

ramp up production from

2015

• High impact exploration

• Experienced (20+ years)

management and technical team

• Above average exploration

success

• Listed on Singapore Exchange

Mainboard in July 2013

1 Transactions for G6/48 and Block 9 are awaiting approvals of the host governments

Experienced team with track record of success

4

The majority of our management and senior technical team have worked together for over 15

years and have established a reputation for value creation

• Co-founder

• >35 years of O&G experience, > 25 in SEA

• Former co-founder and CEO of Pearl

Keith Cameron

CEO

Chris Gibson-

Robinson

Director E&P

Richard Lorentz

Director Business

Development

• Co-founder

• >30 years of upstream O&G experience, >25

in SEA

• Former co-founder and Chief TO of Pearl

• Co-founder • >30 years of upstream O&G experience, >25

in SEA • Former co-founder and Chief BDO of Pearl

Kiran Raj

Chief Financial

Officer

• >19 years corporate finance experience

• Qualified Chartered Accountant with ICAA

• Former Director of IB CLSA and CEO of BCA

Stephen Clifford

Chief Strategy

Officer / VP Treasury

• >20 years O&G experience

• Former Financial Controller for Pearl

• Chartered Certified Accountant and Certified

Compliance Officer

• >13 years legal experience

• Former GC for Aabar and Pearl

• Member of Association of International

Petroleum Negotiators

Kelvin Tang

VP Legal

James Parkin

VP Exploration

Tim Kelly

VP Engineering

• >30 years of O&G experience, >25 in SEA

• Former Regional VP SEA for Pearl and Senior

Geologist and Team Leader East Java at Gulf

Indonesia/ Conoco/ ConocoPhilips

• >30 years O&G experience, >23 in SEA

• Former Corp. Petroleum Eng. Manager, Pearl

and DST Specialist with ExxonMobil

Chris Wilson

VP Business

Development

Michael Whibley

VP Technical

John Bujnoch

VP Drilling

Brian Helyer

VP Operations

Tanya Pang

General Manager

Investor Relations

• >19 years corporate finance & business

development experience in Asia

• Former financial advisor with Pearl Energy

• Member of AIPN

• >30 years of E&P technical and business

development experience, >20 in SEA

• Technical roles in Pearl, Aabar, Amerada

• >40 years offshore O&G experience

• >30 years drilling and operations in UK, US,

Middle East, SEA

• >30 years offshore O&G experience

• Prior roles with Petrofac in SEA, UK and

Tunisia

• 20 years media/IR in energy sector

• IR Manager for Pearl Energy

• Senior management with Reuters

2002 2005 2006 2008 Track Record of Value

Creation Since Pearl

Energy Pearl Energy

Established

Pearl Energy Listed

on SGX-ST with

US$240m market cap

Aabar Petroleum

acquired Pearl Energy

for >US$500m

Mubadala acquired

Pearl Energy for

US$833m

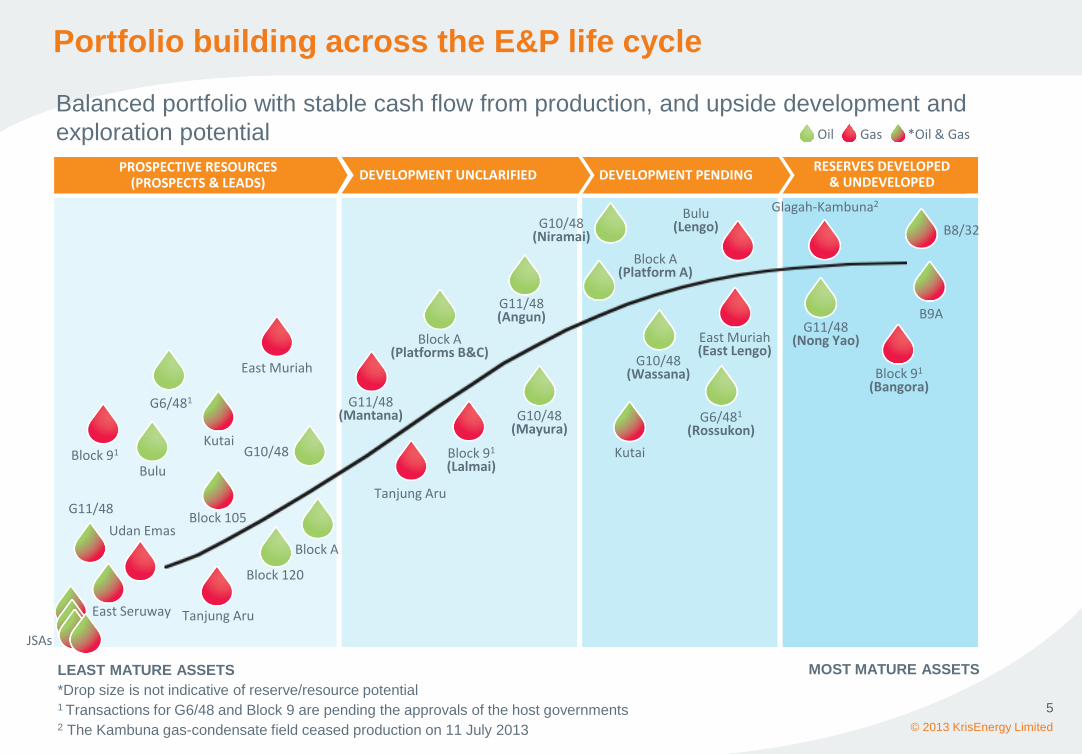

Portfolio building across the E&P life cycle

© 2013 KrisEnergy Limited

5

Balanced portfolio with stable cash flow from production, and upside development and

exploration potential

PROSPECTIVE RESOURCES (PROSPECTS & LEADS)

DEVELOPMENT UNCLARIFIED DEVELOPMENT PENDING RESERVES DEVELOPED

& UNDEVELOPED

Oil Gas *Oil & Gas

B9A

B8/32

Glagah-Kambuna2

G11/48 (Nong Yao) East Muriah

(East Lengo)

Bulu (Lengo)

Block A (Platform A)

G10/48 (Niramai)

G11/48 (Angun)

Block A (Platforms B&C)

G11/48 (Mantana)

East Muriah

Tanjung Aru

Kutai

Block 120

Block A

G10/48 Kutai

Block 105

Tanjung Aru East Seruway

Udan Emas

JSAs

G11/48

G10/48 (Mayura)

G10/48 (Wassana)

G6/481

(Rossukon)

Bulu

LEAST MATURE ASSETS

*Drop size is not indicative of reserve/resource potential 1 Transactions for G6/48 and Block 9 are pending the approvals of the host governments 2 The Kambuna gas-condensate field ceased production on 11 July 2013

MOST MATURE ASSETS

Block 91

(Bangora)

Block 91

(Lalmai)

G6/481

Block 91

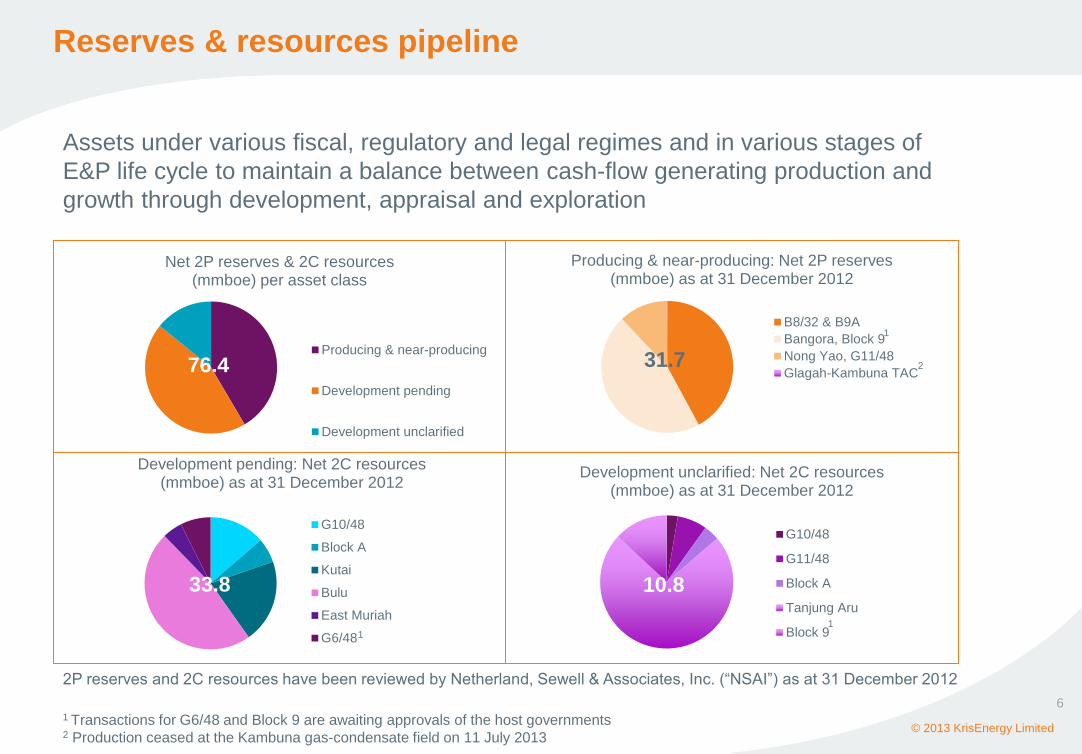

Reserves & resources pipeline

Net 2P reserves & 2C resources (mmboe) per asset class

Producing & near-producing

Development pending

Development unclarified

76.4

Producing & near-producing: Net 2P reserves (mmboe) as at 31 December 2012

B8/32 & B9A

Bangora, Block 9

Nong Yao, G11/48

Glagah-Kambuna TAC

1

2 31.7

Development pending: Net 2C resources (mmboe) as at 31 December 2012

G10/48

Block A

Kutai

Bulu

East Muriah

G6/48

33.8

6

© 2013 KrisEnergy Limited

Development unclarified: Net 2C resources (mmboe) as at 31 December 2012

G10/48

G11/48

Block A

Tanjung Aru

Block 91

10.8

Assets under various fiscal, regulatory and legal regimes and in various stages of

E&P life cycle to maintain a balance between cash-flow generating production and

growth through development, appraisal and exploration

1

1 Transactions for G6/48 and Block 9 are awaiting approvals of the host governments 2 Production ceased at the Kambuna gas-condensate field on 11 July 2013

2P reserves and 2C resources have been reviewed by Netherland, Sewell & Associates, Inc. (“NSAI”) as at 31 December 2012

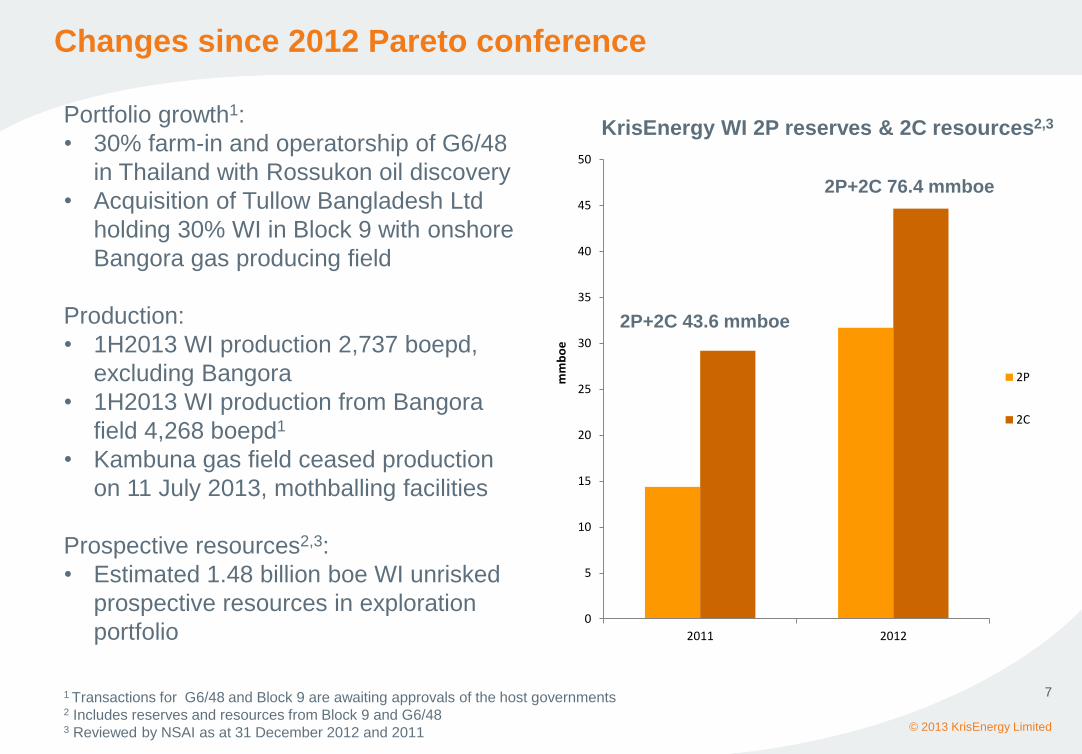

Changes since 2012 Pareto conference

© 2013 KrisEnergy Limited

7

Portfolio growth1:

• 30% farm-in and operatorship of G6/48

in Thailand with Rossukon oil discovery

• Acquisition of Tullow Bangladesh Ltd

holding 30% WI in Block 9 with onshore

Bangora gas producing field

Production:

• 1H2013 WI production 2,737 boepd,

excluding Bangora

• 1H2013 WI production from Bangora

field 4,268 boepd1

• Kambuna gas field ceased production

on 11 July 2013, mothballing facilities

Prospective resources2,3:

• Estimated 1.48 billion boe WI unrisked

prospective resources in exploration

portfolio

1 Transactions for G6/48 and Block 9 are awaiting approvals of the host governments 2 Includes reserves and resources from Block 9 and G6/48 3 Reviewed by NSAI as at 31 December 2012 and 2011

0

5

10

15

20

25

30

35

40

45

50

2011 2012

mm

bo

e

2P

2C

KrisEnergy WI 2P reserves & 2C resources2,3

2P+2C 43.6 mmboe

2P+2C 76.4 mmboe

Changes since 2012 Pareto conference/2

© 2013 KrisEnergy Limited

8

Operations:

• FID approved for Nong Yao oil field

development in G11/48, Gulf of Thailand

Drilling:

• Successful Lengo-2 appraisal well in

Bulu PSC, Indonesia. Drafting plan of

development

• Tayum-1 exploration well in Kutai PSC,

Indonesia, encountered gas. Moving into

development planning

• Commenced drilling of Cua Lo-1 high-

impact exploration well offshore Vietnam

Exploration:

• Completed 948 km 2D seismic program

in East Seruway PSC

• Completed 270 sq km 3D seismic

program in G6/48

IPO:

• Listed on SGX Mainboard on 19 July 2013

• Total offering 246,154,000 new shares,

23.5% enlarged share capital

• Issue price S$1.10/share

• Institutional demand >6x subscribed; retail

offer 22.9x

• Net proceeds US$203 million

• First Reserve holds 45.2%, Keppel Corp

holds 31.6%

Financial:

• Successful US$35 million tap of 2016

Senior Guaranteed Secured Bond to

US$120 million

• Increased revolving credit facility by

US$12.5 million to US$42.5 million

• Unused sources of liquidity at 30 June 2013

were US$167.6 million

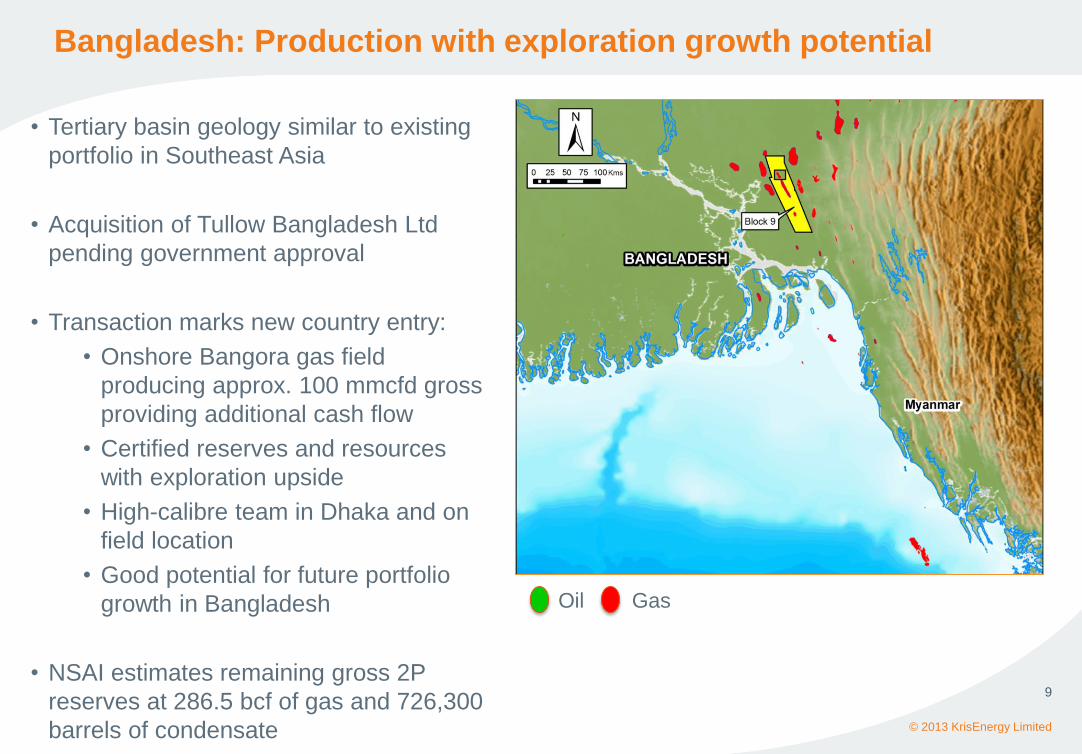

Bangladesh: Production with exploration growth potential

© 2013 KrisEnergy Limited

9

• Tertiary basin geology similar to existing

portfolio in Southeast Asia

• Acquisition of Tullow Bangladesh Ltd

pending government approval

• Transaction marks new country entry:

• Onshore Bangora gas field

producing approx. 100 mmcfd gross

providing additional cash flow

• Certified reserves and resources

with exploration upside

• High-calibre team in Dhaka and on

field location

• Good potential for future portfolio

growth in Bangladesh

• NSAI estimates remaining gross 2P

reserves at 286.5 bcf of gas and 726,300

barrels of condensate

Oil Gas

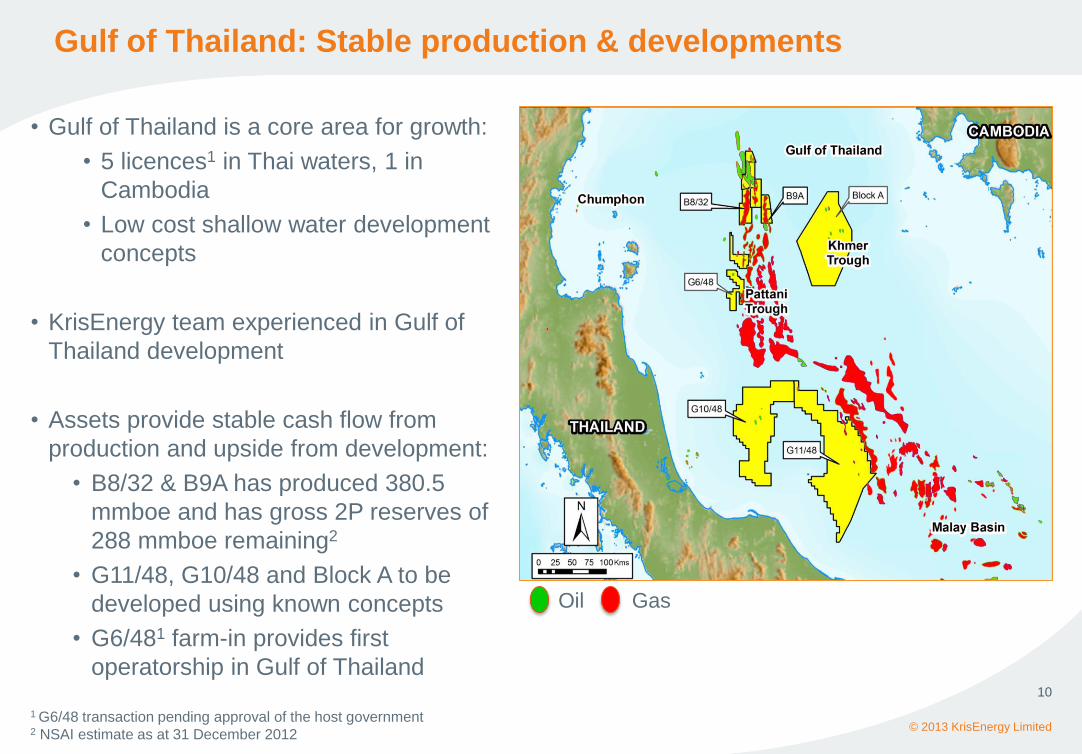

Gulf of Thailand: Stable production & developments

© 2013 KrisEnergy Limited

10

• Gulf of Thailand is a core area for growth:

• 5 licences1 in Thai waters, 1 in

Cambodia

• Low cost shallow water development

concepts

• KrisEnergy team experienced in Gulf of

Thailand development

• Assets provide stable cash flow from

production and upside from development:

• B8/32 & B9A has produced 380.5

mmboe and has gross 2P reserves of

288 mmboe remaining2

• G11/48, G10/48 and Block A to be

developed using known concepts

• G6/481 farm-in provides first

operatorship in Gulf of Thailand

1 G6/48 transaction pending approval of the host government 2 NSAI estimate as at 31 December 2012

Oil Gas

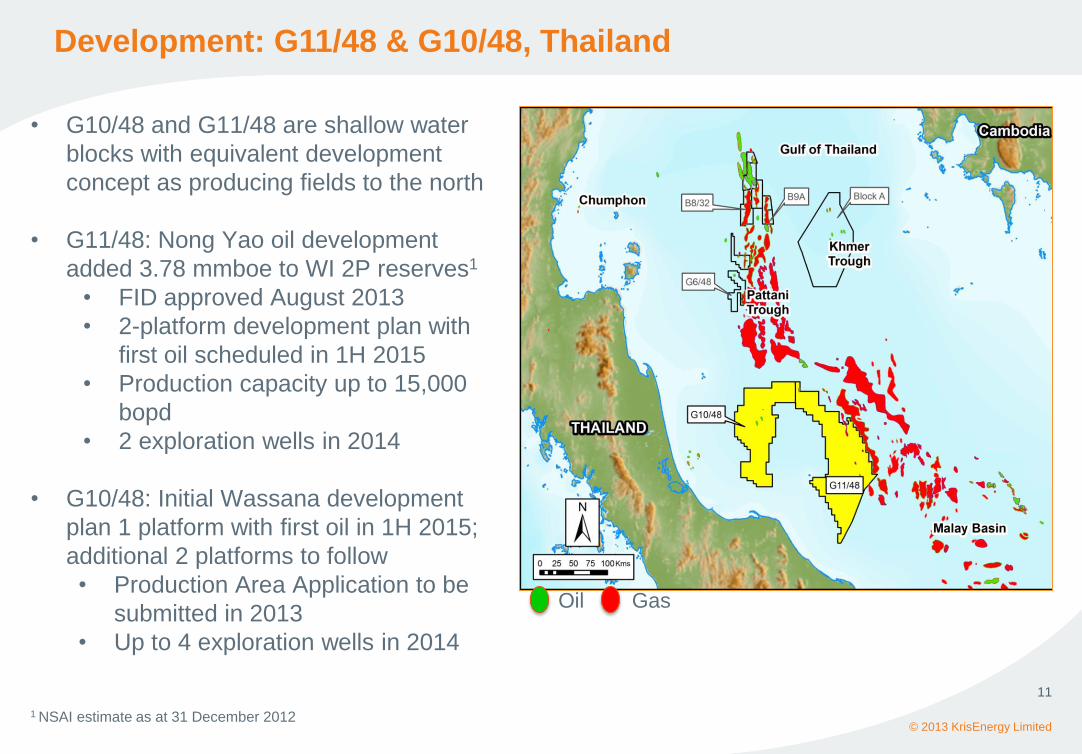

Development: G11/48 & G10/48, Thailand

© 2013 KrisEnergy Limited

11

• G10/48 and G11/48 are shallow water

blocks with equivalent development

concept as producing fields to the north

• G11/48: Nong Yao oil development

added 3.78 mmboe to WI 2P reserves1

• FID approved August 2013

• 2-platform development plan with

first oil scheduled in 1H 2015

• Production capacity up to 15,000

bopd

• 2 exploration wells in 2014

• G10/48: Initial Wassana development

plan 1 platform with first oil in 1H 2015;

additional 2 platforms to follow

• Production Area Application to be

submitted in 2013

• Up to 4 exploration wells in 2014

Oil Gas

1 NSAI estimate as at 31 December 2012

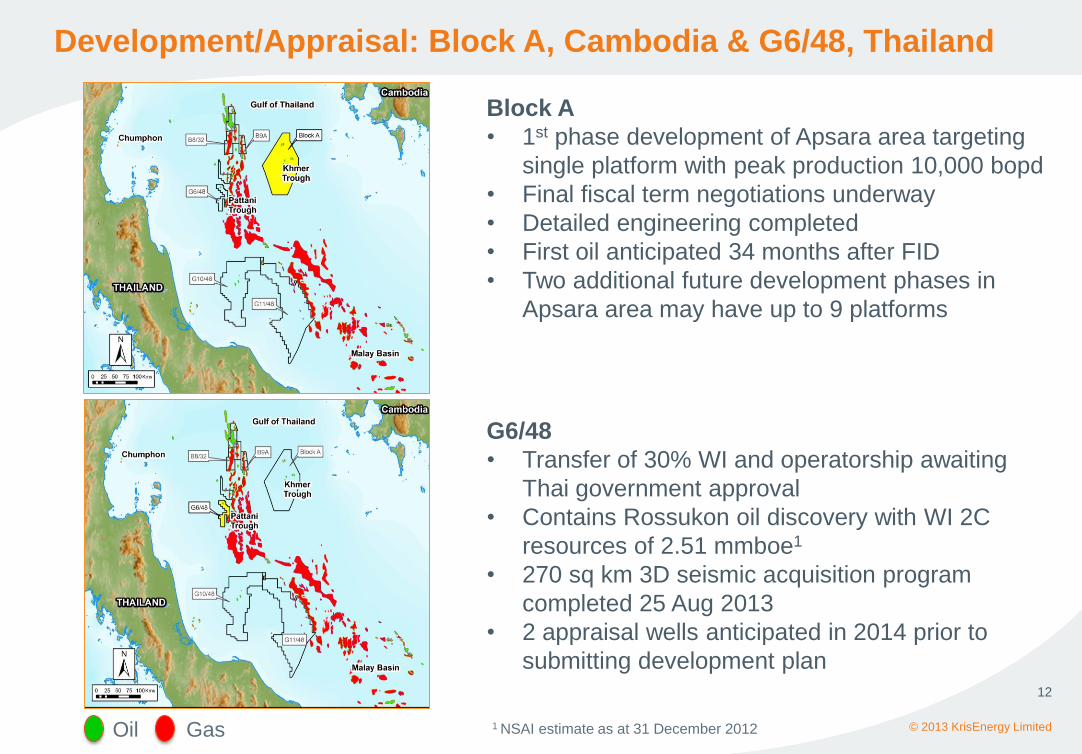

Development/Appraisal: Block A, Cambodia & G6/48, Thailand

© 2013 KrisEnergy Limited

12

Block A

• 1st phase development of Apsara area targeting

single platform with peak production 10,000 bopd

• Final fiscal term negotiations underway

• Detailed engineering completed

• First oil anticipated 34 months after FID

• Two additional future development phases in

Apsara area may have up to 9 platforms

G6/48

• Transfer of 30% WI and operatorship awaiting

Thai government approval

• Contains Rossukon oil discovery with WI 2C

resources of 2.51 mmboe1

• 270 sq km 3D seismic acquisition program

completed 25 Aug 2013

• 2 appraisal wells anticipated in 2014 prior to

submitting development plan

Oil Gas 1 NSAI estimate as at 31 December 2012

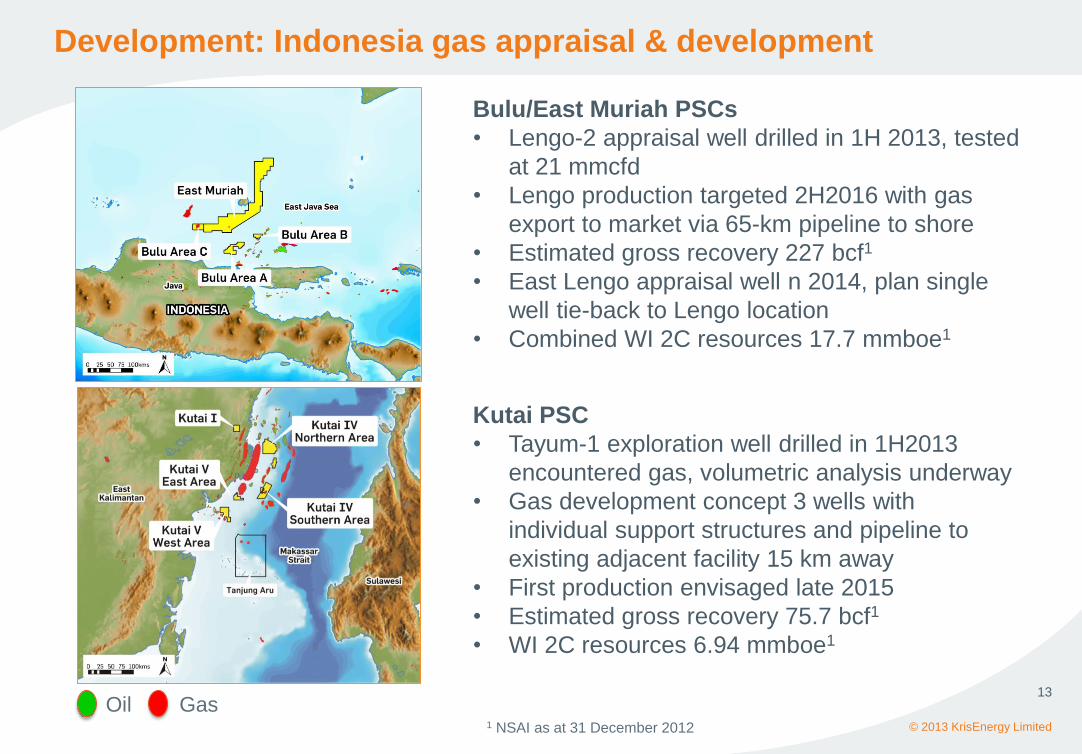

Development: Indonesia gas appraisal & development

© 2013 KrisEnergy Limited

13

Bulu/East Muriah PSCs

• Lengo-2 appraisal well drilled in 1H 2013, tested

at 21 mmcfd

• Lengo production targeted 2H2016 with gas

export to market via 65-km pipeline to shore

• Estimated gross recovery 227 bcf1

• East Lengo appraisal well n 2014, plan single

well tie-back to Lengo location

• Combined WI 2C resources 17.7 mmboe1

Kutai PSC

• Tayum-1 exploration well drilled in 1H2013

encountered gas, volumetric analysis underway

• Gas development concept 3 wells with

individual support structures and pipeline to

existing adjacent facility 15 km away

• First production envisaged late 2015

• Estimated gross recovery 75.7 bcf1

• WI 2C resources 6.94 mmboe1

1 NSAI as at 31 December 2012

Oil Gas

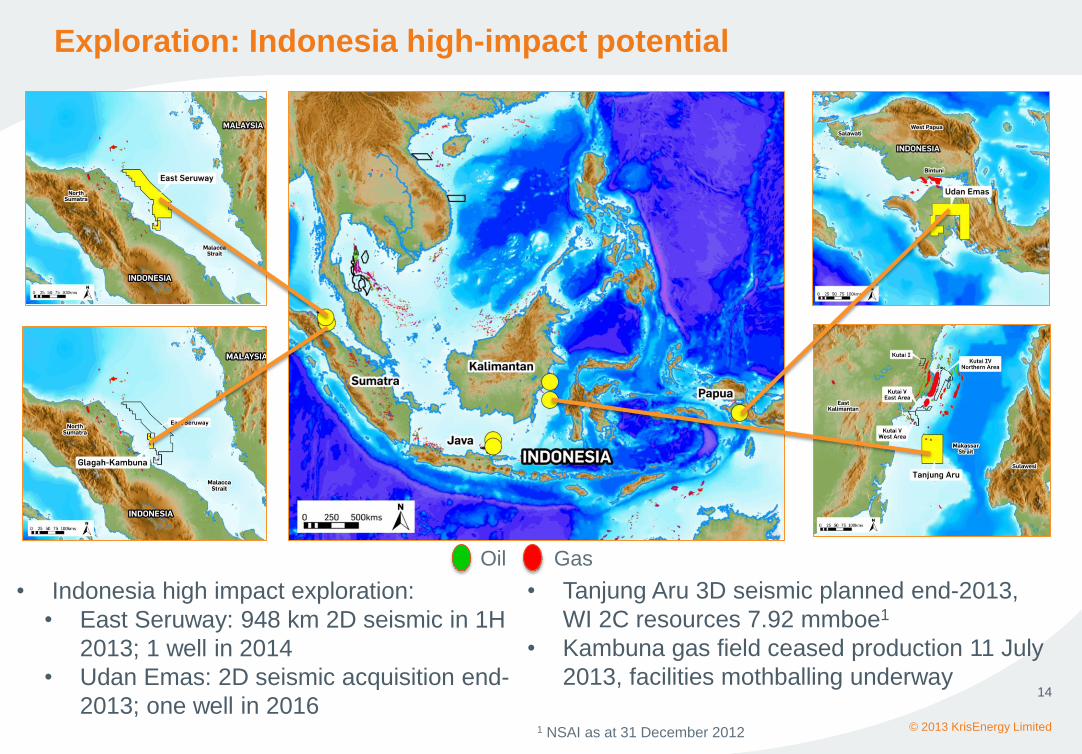

Exploration: Indonesia high-impact potential

© 2013 KrisEnergy Limited

14

Oil Gas

• Indonesia high impact exploration:

• East Seruway: 948 km 2D seismic in 1H

2013; 1 well in 2014

• Udan Emas: 2D seismic acquisition end-

2013; one well in 2016

• Tanjung Aru 3D seismic planned end-2013,

WI 2C resources 7.92 mmboe1

• Kambuna gas field ceased production 11 July

2013, facilities mothballing underway

1 NSAI as at 31 December 2012

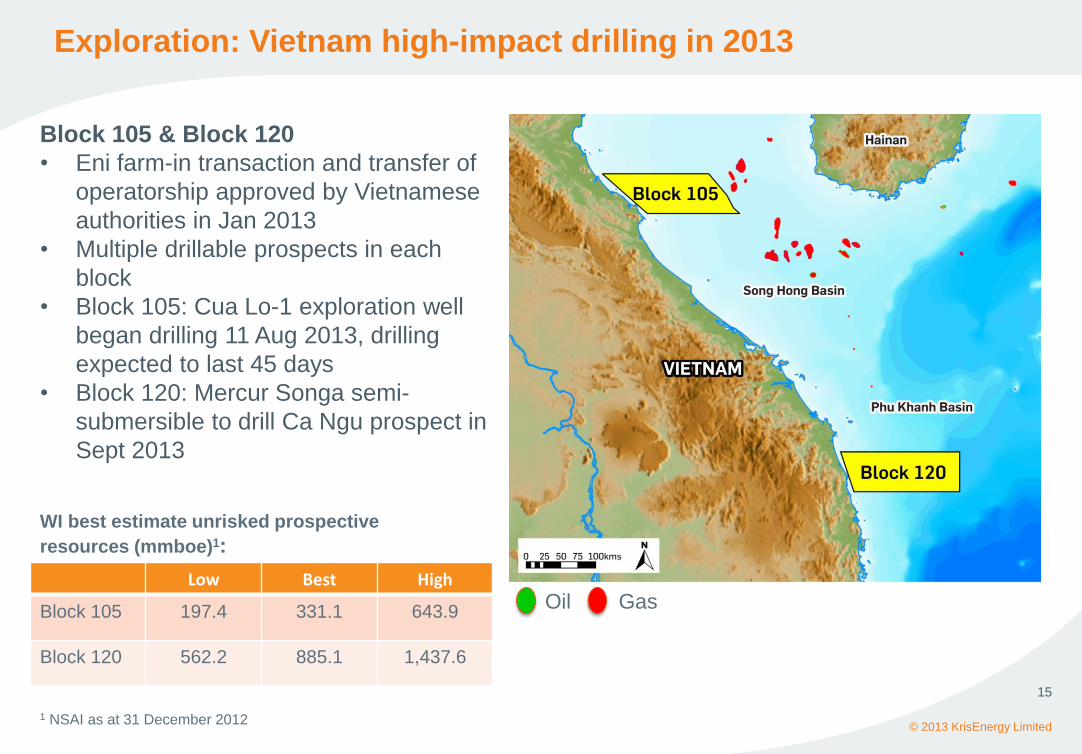

Exploration: Vietnam high-impact drilling in 2013

© 2013 KrisEnergy Limited

15

Oil Gas

Block 105 & Block 120

• Eni farm-in transaction and transfer of

operatorship approved by Vietnamese

authorities in Jan 2013

• Multiple drillable prospects in each

block

• Block 105: Cua Lo-1 exploration well

began drilling 11 Aug 2013, drilling

expected to last 45 days

• Block 120: Mercur Songa semi-

submersible to drill Ca Ngu prospect in

Sept 2013

WI best estimate unrisked prospective

resources (mmboe)1:

Low Best High

Block 105 197.4 331.1 643.9

Block 120 562.2 885.1 1,437.6

1 NSAI as at 31 December 2012

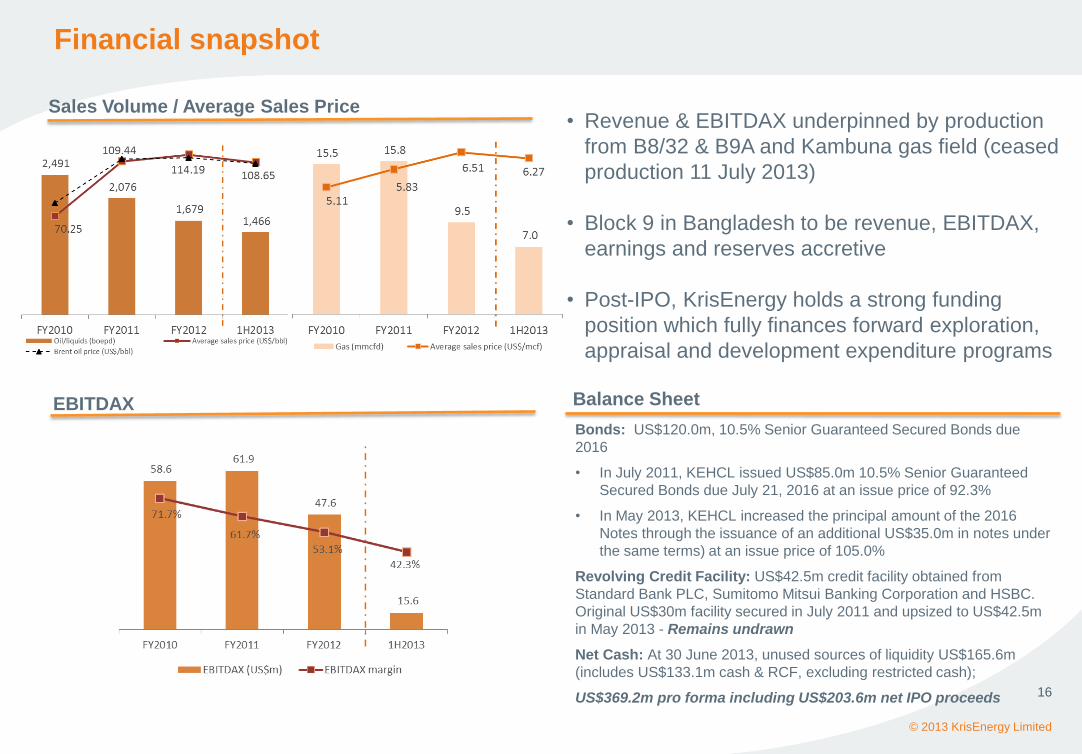

Financial snapshot

© 2013 KrisEnergy Limited

16

Sales Volume / Average Sales Price

EBITDAX

• Revenue & EBITDAX underpinned by production

from B8/32 & B9A and Kambuna gas field (ceased

production 11 July 2013)

• Block 9 in Bangladesh to be revenue, EBITDAX,

earnings and reserves accretive

• Post-IPO, KrisEnergy holds a strong funding

position which fully finances forward exploration,

appraisal and development expenditure programs

Balance Sheet

Bonds: US$120.0m, 10.5% Senior Guaranteed Secured Bonds due

2016

• In July 2011, KEHCL issued US$85.0m 10.5% Senior Guaranteed

Secured Bonds due July 21, 2016 at an issue price of 92.3%

• In May 2013, KEHCL increased the principal amount of the 2016

Notes through the issuance of an additional US$35.0m in notes under

the same terms) at an issue price of 105.0%

Revolving Credit Facility: US$42.5m credit facility obtained from

Standard Bank PLC, Sumitomo Mitsui Banking Corporation and HSBC.

Original US$30m facility secured in July 2011 and upsized to US$42.5m

in May 2013 - Remains undrawn

Net Cash: At 30 June 2013, unused sources of liquidity US$165.6m

(includes US$133.1m cash & RCF, excluding restricted cash);

US$369.2m pro forma including US$203.6m net IPO proceeds

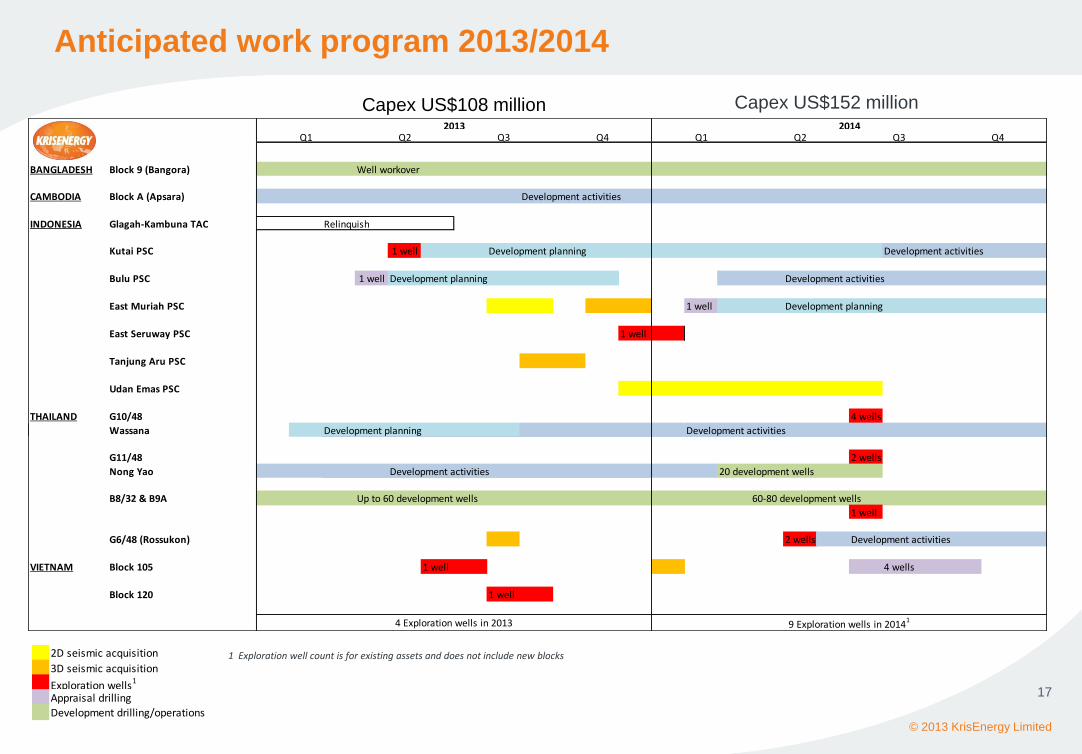

Anticipated work program 2013/2014

© 2013 KrisEnergy Limited

17

2D seismic acquisition

3D seismic acquisition

Exploration wells1

Appraisal drillingDevelopment drilling/operations

1 Exploration well count is for existing assets and does not include new blocks

BANGLADESH Block 9 (Bangora) Well workover

CAMBODIA Block A (Apsara) Development activities

INDONESIA Glagah-Kambuna TAC Relinquish

Kutai PSC 1 well Development planning Development activities

Bulu PSC 1 well Development planning Development activities

East Muriah PSC 1 well Development planning

East Seruway PSC 1 well

Tanjung Aru PSC

Udan Emas PSC

THAILAND G10/48 4 wells

Wassana Development planning Development activities

G11/48 2 wells

Nong Yao Development activities 20 development wells

B8/32 & B9A Up to 60 development wells 60-80 development wells

1 well

G6/48 (Rossukon) 2 wells Development activities

VIETNAM Block 105 1 well 4 wells

Block 120 1 well

20142013Q1 Q3 Q4 Q1 Q2 Q3 Q4Q2

4 Exploration wells in 2013 9 Exploration wells in 20141

Capex US$108 million Capex US$152 million

Thank you!