Paper and Paperboard Quarterly Special report€¦ · 9Globally, paper industry remained marginally...

26

Paper and Paperboard Quarterly Special report June 2014 June 2014 1

Transcript of Paper and Paperboard Quarterly Special report€¦ · 9Globally, paper industry remained marginally...

Paper and Paperboard Quarterly Special report

June 2014June 2014

1

Price Trends – Kraft Paper

Ruby Macons (22 BF 150 GSM) Siddeshwari (22 BF 150 GSM)

DateBasic rate Change Net change, Basic rate Change Net change,Date

(INR per kg)g

(M-o-M)g ,

since Jan’14 (INR per kg)g

(M-o-M)g ,

since Jan’14

Dec'13 31.70 -0.75 NA 30.00 -0.50 NA

Jan'14 31.70 0.00 0.00 30.00 0.00 0.00

Feb'14 31.70 0.00 0.00 30.50 0.50 0.50

Mar'14 31.70 0.00 0.00 30.50 0.00 0.50

Apr'14 33.20 1.50 1.50 32.50 2.00 2.50

May'14 33.20 0.00 1.50 32.50 0.00 2.50

Jun'14 33.20 0.00 1.50 32.50 0.00 2.50

Driven by the higher cost of production due to ongoing power crisis paper pricesDriven by the higher cost of production due to ongoing power crisis, paper pricesremained in firm tone.

Paper prices dependent on wood pulp have been supported by the due to steady risein its costs and lower supply

© TransGraph Consulting Pvt Ltd Slide 2

in its costs and lower supply

Weaker INR vs USD keeping raw material import prices higher.

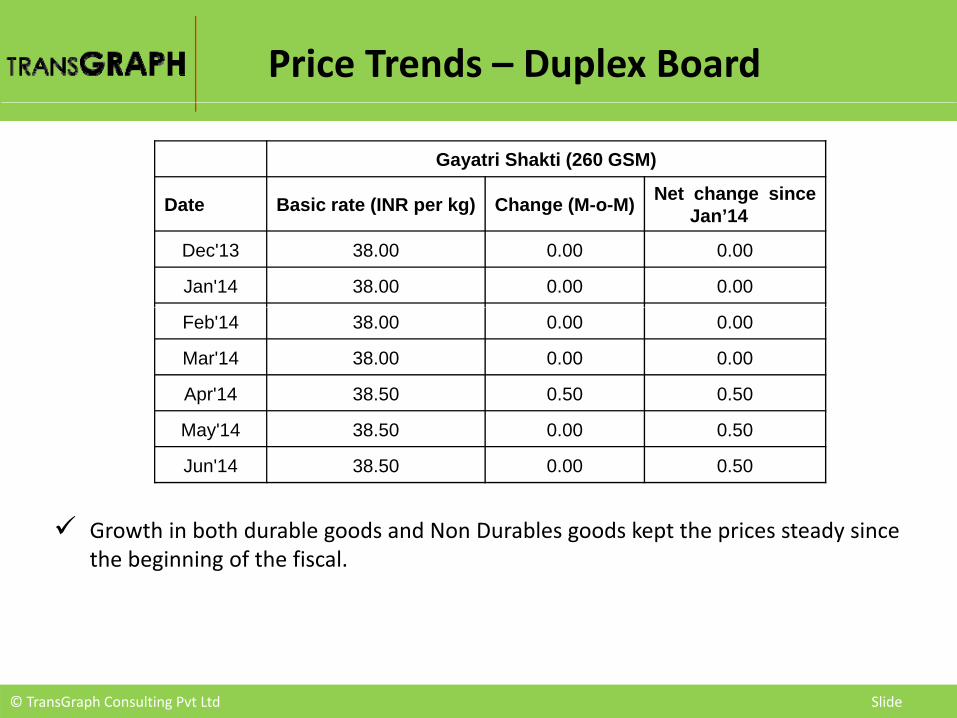

Price Trends – Duplex Board

Gayatri Shakti (260 GSM)

Date Basic rate (INR per kg) Change (M-o-M) Net change sinceDate Basic rate (INR per kg) Change (M-o-M) Jan’14

Dec'13 38.00 0.00 0.00

Jan'14 38.00 0.00 0.00

Feb'14 38.00 0.00 0.00

Mar'14 38.00 0.00 0.00

Apr'14 38.50 0.50 0.50

May'14 38.50 0.00 0.50

Jun'14 38.50 0.00 0.50

Growth in both durable goods and Non Durables goods kept the prices steady sincethe beginning of the fiscal.

© TransGraph Consulting Pvt Ltd Slide

Factors affecting pulp and paper prices in April – June 2014p

Globally, paper industry remained marginally weak due to weather condition stilldisturbed paper industry production and deliveries in North America. Shipments in andto the developing countries continued to grow due to muted demand in Europeto the developing countries continued to grow due to muted demand in Europe

Recycled paper global demand has seen a decline in recent past amidst slowdown inChinese economy. Prices for bulk grades of RCF paper have been pretty much flat inNorth America and Western Europe, the largest two recovered paper suppliers to ChinaNorth America and Western Europe, the largest two recovered paper suppliers to China

In softwood, prices remained high due to the shortages in the volumes of softwoodcompared to demand. However, hardwood prices remained lower due to higherinventories and demand concerns

At the Indian front, sharp rise in raw material prices due to supply shortage of sugarbagasse and wheat straw which climbed to year high level have made paper prices torise in major Mills in India

Free trade agreements with south‐east countries like Thailand, Malaysia and Indonesiahave been impacting the profitability of the Indian paper industry significantly. Duty‐freeimport of paper from these Southeast Asian countries, which are around Rs 3000 per tonh tti I di fi hi h h b bl t hik i

© TransGraph Consulting Pvt Ltd Slide 4

cheaper, putting pressure on Indian paper firms which have been unable to hike pricesthough they have been incurring losses due to high input costs

Economy updates

US

After recording 10 quarters of consecutive economic growth, contraction in Q1 wasaggravated by the harsh winter this year. Q2 numbers such as IP, employment and retailsales indicate close to 3% growth and the US economy remains on firm foot among thedeveloped economies at present.

St l t th f 200 th d th d l i t f QEStrong employment growth of over 200 thousand a month and low impact of QEtapering (indicated by increase in inflation to 2.1% against target of 2%) indicatingeconomy withstanding tightening monetary policy.

Although US Fed is likely to increase interest rates by next year – comments from FedAlthough, US Fed is likely to increase interest rates by next year – comments from FedChairwoman and US treasury yields signals a prolonged period of loose monetary policy.

EUEU

Mixed picture of growth

Recent business surveys and PMI numbers point to improvement in business conditionsh

© TransGraph Consulting Pvt Ltd Slide 5

across the region.

Nascent recovery remains uneven with growing threat of deflation.

Economy updates

China

China represents a large portion of global demand for several key energy, metals, andi lt l ditiagricultural commodities.

Credit crisis‐induced China slowdown would have a sizeable negative impact on demandfor commodities and the (mostly emerging market) economies that produce them.

India

High foreign funds inflow (USD 12.7 bn) in AMJ 2014 and election results helped in rupeeappreciation during AMJ 2014. FII’s poured in USD 12.7 billion with USD 5.3 billion in debtsegment and USD 7.4 billion in equities. This is comparable to USD 5.5 billion in debt andUSD 3.8 billion in equity during JFM 2014 indicating strong equity driven INRappreciationappreciation.

Fiscal spending remains key post budget for the new government and is likely to keeprupee appreciation limited from the current levels.

Rising Crude oil and gold prices pose a threat of renewal of CAD concerns in the short

© TransGraph Consulting Pvt Ltd Slide 6

Rising Crude oil and gold prices pose a threat of renewal of CAD concerns in the short‐term.

US Economic Indicators – at a glance

Quarterly Forecasts for Economic Indicators

Real GDP (%) Unemployment Payrolls Consumer Price Real GDP (%) Rate (%) (000s/month) Index (%)Previous (Mar‐14)

New (Jun‐14) Previous New Previous New Previous New

2014:Q2 3.0 3.2 6.6 6.4 193.5 232.0 1.7 1.9

2014:Q3 2.8 3.5 6.4 6.3 195.2 214.7 1.9 1.9

2014:Q4 2.7 2.7 6.3 6.2 215.0 197.9 2.0 2.0Q

Source: Federal Reserve Bank of Philadelphia and TG Estimates

The outlook for growth over the next three quarters looks stronger now than it did threemonths ago according to the Federal Reserve Bank of Philadelphiamonths ago according to the Federal Reserve Bank of Philadelphia.

Improved outlook for unemployment and inflation are likely to fuel volatility and mightalso alter the Forward Guidance by the Federal Reserve.

R i i i fl ti i ht l h i ht d l d t ti i ti f f t

© TransGraph Consulting Pvt Ltd Slide 7

Reviving inflationary concerns might also heighten and lead to anticipation of fasterincrease in interest rates by mid 2015.

US economy remains on firm foot of recoveryy

4.10%

3.20% 3.50%

US GDP growth (Q-o-Q annualized)After witnessing a first quarter lag, US GDP isexpected to grow by 3.2% in AMJ‐14 backed by

2.60%3.20%

2.70% reviving fixed asset investments and healing labormarket.

In 2014, US GDP is forecasted to grow by 2.4% in

-1.00%Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

line with the Fed, IMF and the World Bank’sexpectations.

Improving personal income and spending backed

17.2

8.510

17

24Gross Private Domestic Investment (%

Change Q/Q)by gradual fall in business inventories should signaluptick in economic activity.

Private investments are expected to peak in theJAS 14 t b k d b F d2.5 4.6 3.9

-11

-4

3

10 JAS‐14 quarter backed by concerns over Fedraising interest rates.

Concisely, the US economy is likely to witnessstable economic growth but concerns of inflation

© TransGraph Consulting Pvt Ltd Slide 8

-11.7-18

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

stable economic growth but concerns of inflationand Fed increasing rates might dent confidence.

Euro‐zone – gradually overcoming headwinds

The recovery in the Euro zone is ongoing and it is

progressing at varying speeds and strength across1 1%

1.4%1 2%

EU GDP growth (% Change Y/Y)

the region.

Although private credit growth remained anemic,0.6%

0.9%1.1% 1.2%

recent rate cut by the ECB and targeted long term

refinancing operation is likely to broaden GDP

growth in H2 2014.

-0.3%Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

0.8%

1.0% 1.0%EU CPI (% Change Y/Y)

Inflation is also likely to pick up gradually but is

expected to remain well below the ECB’s long term

f

0.2% 0.2%

target of 2%.

Consumption and investments will increase,

making the Euro zone recovery less dependent on

© TransGraph Consulting Pvt Ltd Slide 9

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

g y p

international markets.

China – a tough balancing act

7.8%7.7%

China GDP growth (% Change Y/Y) Shift of the economic growth engine from

export based to consumption based is likely7.7%

7.4%7.3%

7.6%

7.4%

export based to consumption based is likely

to weigh on Chinese GDP in 2014.

Economic slowdown continues to raise

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

doubt over the Government’s policies and

pro‐growth reforms might shrug‐off any

0.4%

0.1%0.3%

0.2%

China CPI (% Change Q/Q) severe weakness in H2 2014.

Since the slowdown has been brought about

-0.1%

by weakness overseas as well as a tightening

of credit market conditions by the Chinese

authorities going ahead we might continue

© TransGraph Consulting Pvt Ltd Slide 10

-0.6%

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

authorities, going ahead we might continue

to witness PBOC to remain market friendly.

Global Pulp and paper price trends

20

25

130

140Global recovered paper prices

100

110

1000

1050Global Pulp prices

5

10

15

110

120

70

80

90

850

900

950

0100Apr‐13 Jun‐13 Aug‐13 Oct‐13 Dec‐13 Feb‐14 Apr‐14 Jun‐14

OCC (Euro/ton) ONP (Euro/ton) ONP‐OCC (Euro/ton)Source: FOEX

60800Mar‐13 May‐13 Jul‐13 Sep‐13 Nov‐13 Jan‐14 Mar‐14 May‐14

EU NBSK (USD/ton) US NBSK (USD/ton)US‐EU diff (USD/Ton) Source: FOEX

32000

32500

33000

33500

120

125

130

135 Impact of global prices on Indian paper prices

31 000

33,000

35,000

37,000 Indian Paper Price Trends

30000

30500

31000

31500

32000

100

105

110

115

120

25,000

27,000

29,000

31,000

3 3 3 3 3 3 3 3 3 3 3 3 4 4 4 4 4 4

Source: CRISIL

© TransGraph Consulting Pvt Ltd Slide 11

30000100Apr‐13 Jun‐13 Aug‐13 Oct‐13 Dec‐13 Feb‐14 Apr‐14 Jun‐14OCC (Euro/ton) ONP (Euro/ton) Indian Kraft paper (22BF) (INR/ton)

Jan‐13

Feb‐13

Mar‐13

Apr‐13

May‐13

Jun‐13

Jul‐1

3

Aug‐13

Sep‐13

Oct‐13

Nov‐13

Dec‐13

Jan‐14

Feb‐14

Mar‐14

Apr‐14

May‐14

Jun‐14

14 BF (Kraft Paper) Duplex Board (200‐284 GSM)

Codex – input cost trend

140

150CoDex

110

120

130

80

90

100

0 0 0 0 1 1 1 1 2 2 2 2 3 3 3 3 4 4

Source: WICMA

CoDex is the cost index for the corrugated boxes include costs of paper, adhesives,

1‐Jan‐10

1‐Ap

r‐1

1‐Jul‐1

1‐Oct‐1

1‐Jan‐1

1‐Ap

r‐1

1‐Jul‐1

1‐Oct‐1

1‐Jan‐1

1‐Ap

r‐1

1‐Jul‐1

1‐Oct‐1

1‐Jan‐1

1‐Ap

r‐1

1‐Jul‐1

1‐Oct‐1

1‐Jan‐14

1‐Ap

r‐1

CoDex is the cost index for the corrugated boxes include costs of paper, adhesives,printing, stitching, energy, transport, labour, interest and establishment costs andoverheads

During the last quarter input cost fluctuations due to energy crisis has contributed to

© TransGraph Consulting Pvt Ltd Slide 12

increase in Codex to 144.73 from 142.10 in the earlier quarter

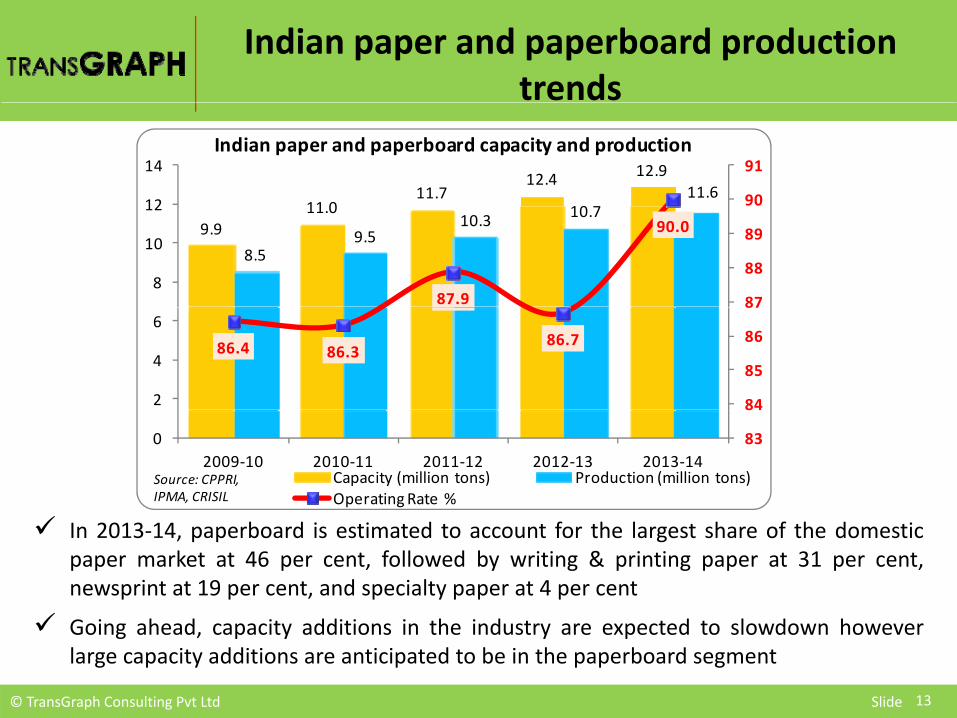

Indian paper and paperboard production trends

11 011.7

12.4 12.911.6 90

91

12

14Indian paper and paperboard capacity and production

9.911.0

8.59.5

10.3 10.7

87.9

90.0

87

88

89

90

8

10

12

86.4 86.386.7

84

85

86

87

2

4

6

83

8

02009‐10 2010‐11 2011‐12 2012‐13 2013‐14

Capacity (million tons) Production (million tons)Operating Rate %

Source: CPPRI, IPMA, CRISIL

In 2013‐14, paperboard is estimated to account for the largest share of the domesticpaper market at 46 per cent, followed by writing & printing paper at 31 per cent,newsprint at 19 per cent, and specialty paper at 4 per cent

© TransGraph Consulting Pvt Ltd Slide 13

Going ahead, capacity additions in the industry are expected to slowdown howeverlarge capacity additions are anticipated to be in the paperboard segment

Indian paper and paperboard production trends

290

300

310

housands

Month-wise Production of Kraft Paper in tons

3.1

ousand

s

Month-wise Production of Corrugated boxes in tons

240

250

260

270

280Th

2.5

2.7

2.9Tho

220

230

Jan‐12

Mar‐12

May‐12

Jul‐1

2

Sep‐12

Nov‐12

Jan‐13

Mar‐13

May‐13

Jul‐1

3

Sep‐13

Nov‐13

Jan‐14

Mar‐14

May‐14

2.1

2.3

Jan‐12

Mar‐12

May‐12

Jul‐1

2

Sep‐12

Nov‐12

Jan‐13

Mar‐13

May‐13

Jul‐1

3

Sep‐13

Nov‐13

Jan‐14

Mar‐14

May‐14

460

480

500

520

Thou

sand

s

Month-wise Production of Paper Board in tons

Since the beginning of the year, paper

production remained higher.

360

380

400

420

440

Going ahead, we expect the production

numbers are likely to decline with the on‐

© TransGraph Consulting Pvt Ltd Slide 14

340

Jan‐12

Mar‐12

May‐12

Jul‐1

2

Sep‐12

Nov‐12

Jan‐13

Mar‐13

May‐13

Jul‐1

3

Sep‐13

Nov‐13

Jan‐14

Mar‐14

May‐14 set of monsoon.

Indian waste paper imports

1.912.12

1.90

2.30 2.27

2.61

13359

1428913000

14000

15000

2.00

2.50

3.00 Indian waste paper imports

Indian waste paper imports

10187

9304

12520

1335912903

9000

10000

11000

12000

0.50

1.00

1.50

2.00

increased sharply in 2013‐14due to lower availability aswell as cheaper imports 9304

80000.002008‐09 2009‐10 2010‐11 2011‐12 2012‐13 2013‐14

Waste paper imports (million tons)

Average import price (INR per ton)Source: DGFT

compared to Indian wastepaper prices.

Going ahead, waste paperimports are expected toi f th th 1.91

2.121.90

2.30 2.272.6111% 21%

15%

5%

10%

15%

20%

25%

1 50

2.00

2.50

3.00Indian waste paper imports

increase further as themonsoon season is expectedto reduce the collectionti it

8%

‐10%

‐1%

‐15%

‐10%

‐5%

0%

5%

0.00

0.50

1.00

1.50

2008 09 2009 10 2010 11 2011 12 2012 13 2013 14

© TransGraph Consulting Pvt Ltd Slide 15

activity. 2008‐09 2009‐10 2010‐11 2011‐12 2012‐13 2013‐14

Waste paper imports (million tons)

Average import price % changeSource: DGFT

Inflation outlook amidst fears of El‐Nino

El‐Nino Years Drought % Decline in rainfall % fall in Kharif Production1972‐73 Yes 24% 6.9%

1982‐83 No ‐ ‐

1986‐87 Yes 13% 5.9%

1991‐92 No ‐ ‐

1994‐95 No ‐ ‐

1997‐98 No ‐ ‐

2002‐03 Yes 19% 19.1%

2004‐05 No ‐ ‐

2006‐07 No ‐ ‐

2009‐10 Yes 23% 12%

From the above study, we conclude that an intense El‐Nino has not always been accompanied by adrought of equal intensity.

h ( ) d h h lf f bl f d h

Source: IMD and Ministry of Agricultural

© TransGraph Consulting Pvt Ltd Slide

In the past 130 years (1880‐2010) it is witnessed that half of Ei‐Nino events are responsible for droughtconditions. Hence, incase the El‐Nino situation in 2014 leads to drought, we expect higher food pricesmight contribute to increasing inflation outlook and might limit the appreciation of the rupee.

El Nino

© TransGraph Consulting Pvt Ltd Slide 17

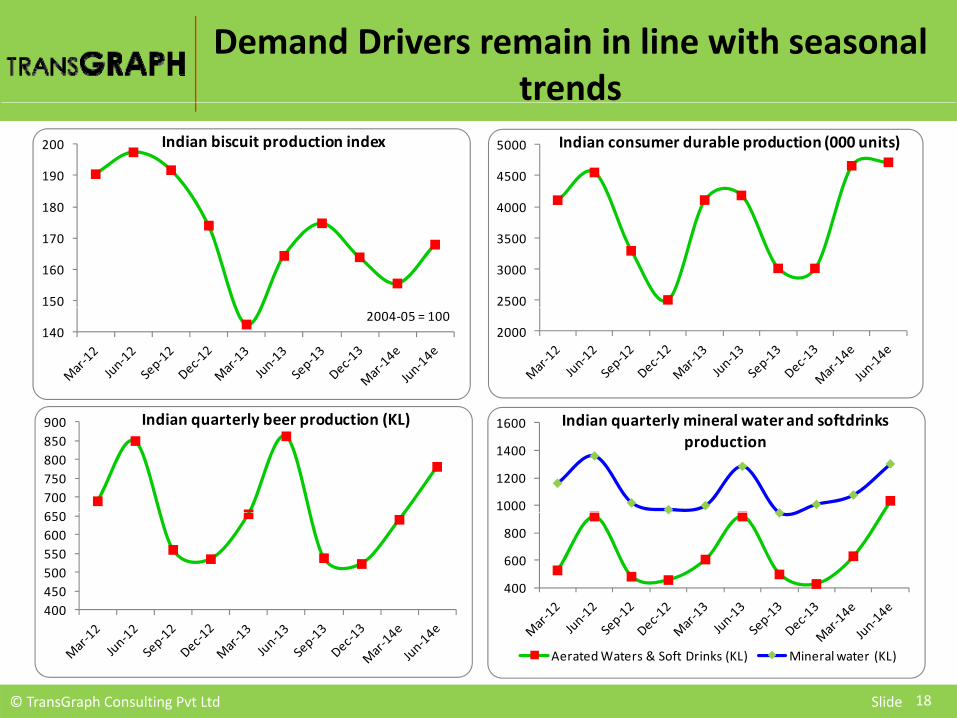

Demand Drivers remain in line with seasonal trends

180

190

200 Indian biscuit production index

4000

4500

5000 Indian consumer durable production (000 units)

150

160

170

180

2500

3000

3500

4000

1402004‐05 = 100

2000

650700750800850900 Indian quarterly beer production (KL)

1000

1200

1400

1600 Indian quarterly mineral water and softdrinks production

400450500550600650

400

600

800

© TransGraph Consulting Pvt Ltd Slide 18

Aerated Waters & Soft Drinks (KL) Mineral water (KL)

Indian paper demand growth vs. GDP and IP growthg

15

17

14

16IP Growth Vs. growth in Paper demand - India

9

10

14

16GDP Growth Vs. growth in Paper demand - India

7

9

11

13

6

8

10

12

5

6

7

8

6

8

10

12

-1

1

3

5

0

2

4

6

2005-06 2007-08 2009-10 2011-12 2013-14P

Consumption growth (%) IP growth (%)2

3

4

5

0

2

4

6

2003-04 2005-06 2007-08 2009-10 2011-12 2013-14P

Consumption growth (%)

GDP growth (%)

2005 06 2007 08 2009 10 2011 12 2013 14P2003 04 2005 06 2007 08 2009 10 2011 12 2013 14P

Paper consumption during past year witnessed a strong recoveryafter the slump in earlier years supported the positive growthafter the slump in earlier years supported the positive growthrate in GDPDespite the weakness in industrial sector, growth in consumer

l d hi h i i d d

© TransGraph Consulting Pvt Ltd Slide 19

sector led to higher consumption in paper demand

Indian Paper and paperboard supply and demand

Attribute 2010‐11 2011‐12 2012‐13 2013‐14

Number of mills 610 605 666 750

Capacity 10.95 11.70 12.40 12.85p y

Production 9.45 10.28 10.75 11.56

Imports 0.68 0.75 0.86 0.91

Exports 0.34 0.34 0.37 0.35

Apparent Consumption 9.79 10.69 11.24 12.12

S CPPRI IPMA CRISIL TG E ti t All it i illi t

© TransGraph Consulting Pvt Ltd Slide 20

Source: CPPRI, IPMA, CRISIL, TG Estimates, All units in million tons

Indian Kraft paper supply and demand

Attribute 2010‐11 2011‐12 2012‐13 2013‐14

Production 2605.00 2810.00 2935.75 3082.40

% Ch 6 98% 7 87% 4 48% 5 00%% Change 6.98% 7.87% 4.48% 5.00%

Imports 156.00 180.00 190.25 202.60

E t 0 00 0 00 0 00 0 00Exports 0.00 0.00 0.00 0.00

Apparent Consumption 2761.00 2990.00 3126.00 3285.00

% Ch 7 26% 8 29% 4 55% 5 09%% Change 7.26% 8.29% 4.55% 5.09%

Source: CPPRI, IPMA, CRISIL, TG Estimates, All units in thousand tons

© TransGraph Consulting Pvt Ltd Slide 21

Indian duplex board supply and demand

Attribute 2010‐11 2011‐12 2012‐13 2013‐14

Production 1819.00 1960.00 2105.00 2231.00

% Change 7.82% 7.75% 7.40% 5.99%

Imports 71.00 80.00 90.27 98.12

Exports 0.00 0.00 0.00 0.00

Apparent Consumption 1890.00 2040.00 2195.00 2330.00

% Change 8.00% 7.94% 7.60% 6.15%

Source: CPPRI, IPMA, CRISIL, TG Estimates, All units in thousand tons

© TransGraph Consulting Pvt Ltd Slide 22

Supply Demand Analysis

Region Demand Supply

Grim demand growth outlook due tod li i i d t i l ti it t Chi f t

Additional paperboard Capacities in Europed N th A i d t d li i fit bilit

Global

declining industrial activity at Chinese frontand slowdown in Euro zone economicgrowth

Revival in US industrial production after

and North America due to declining profitabilityin printing paper sector likely to keep globalsupply higher in the coming year

Muted demand along with economic growthwinter season expected to boost demand incoming months

expected to result in higher wood pulpinventories

Expectation of robust performance byIndian industrial sector to propel demand forduplex boards

Growing number of Export ‐ oriented

Obsolescence of technology and shortage ofraw material being a major hindrance at supplyside. Government ignoring industry demand forinterest subsidy under Technology Upgradation

( )India

g pindustries

Strong demographic factors likepopulation growth and increase in literacylevels

Fund (TUF) Scheme

Lack of government initiatives to providewaste land for plantation

Not much new capacity coming on stream for

© TransGraph Consulting Pvt Ltd Slide 23

levels Not much new capacity coming on‐stream forDuplex board – A long term issues yet to betackled

Price outlook summary

Region 2‐3 months More than 4 monthsKraft paper West India (Recycled paper based) +600 ‐250Kraft paper West India (Recycled paper based) +600 250Kraft paper North India (Bagasse based) +500 ‐450Duplex Board West India +300 ‐100Duplex board North India +300 ‐100pChromo paper West India +400 +100

Indian Kraft paper and Duplex board prices are expected toIndian Kraft paper and Duplex board prices are expected toremain supported by higher raw material prices in the near term.However, slowing global demand and delay in pick up of exportsd t d l d ld d d d ti tdue to delayed monsoon could dampen demand sentiments overthe medium term leading to price decline in the coming 3‐4months

© TransGraph Consulting Pvt Ltd Slide 24

Thanking you for your attention.

+91‐40‐33404040 [email protected] @t h www.transgraph.com

WWW

TransGraph Consulting Private Limited6‐3‐655 / 2 / 1 A P Civil Supplies Bhavan Lane Somajiguda

6‐3‐655 / 2 / 1, A.P. Civil Supplies Bhavan Lane, Somajiguda,Hyderabad ‐ 500 082, India.

LEGAL INFORMATION

This document is the whole property of Transgraph Consulting Private Limited, Hyderabad, India (hereafter “TransGraph”).

The following acts are strictly prohibited:Reproduction and/or forwarding for sale or any other usesReproduction and/or forwarding for sale or any other usesPosting on any communication mediumTransmittal via the Internet

Terms of usageUpon receipt of this document either directly or indirectly, it is understood that the user will and must fully comply with the other terms and conditions ofTransGraph By accepting this document the user agrees to be bound by the foregoing limitationsTransGraph. By accepting this document the user agrees to be bound by the foregoing limitations.

This publication is prepared by TransGraph and protected by copyright laws. Unless otherwise noted in the Service Agreement, the entire contents of thispublication are copyrighted by TransGraph, and may not be reproduced, stored in another retrieval system, posted on any communication medium, ortransmitted in any form or by any means without prior written consent of TransGraph. Unauthorized reproduction or distribution of this publication, or anyportion of it, may result in severe civil and criminal penalties, and will be prosecuted to the maximum extent necessary to protect the rights of TransGraph.

The information and opinions contained in this report have been obtained from sources TransGraph believed to be reliable, but no representation orwarranty, express or implied, is made that such information is accurate or complete and it should not be relied upon as such.

This report does not constitute a prospectus or other offering document or an offer or solicitation to buy or sell any assets (commodities, currencies, etc) orother investment. Information and opinions contained in the report are published for the assistance of recipients, but are not to be relied upon asauthoritative or taken in substitution for the exercise of judgment by any recipient; they are subject to change without any notice and not intended to providethe sole basis of any evaluation of the instruments discussed herein. Any views expressed reflect the current views of the analysts, which do not necessarilycorrespond to the opinions of TransGraph or its affiliates. Opinions expressed may differ from views set out in other documents, including research, publishedby TransGraph.

Any reference to past performance should not be taken as an indication of future performance. No member in the public related to TransGraph accepts anyliability whatsoever for any direct or consequential loss arising from any use of material contained in this report.

Analyst CertificationEach analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the analyst's views about anyand all of the factors and assets (commodities, currencies, etc) named in this report, and (ii) no part of the analyst's compensation is directly or indirectly,related to the execution of the specific recommendations or views expressed herein.related to the execution of the specific recommendations or views expressed herein.

Copyright © TransGraph Consulting Private Limited, Hyderabad, India.

Prepared by Consulting Team – TransGraphRegistered Office: 6‐3‐655/2/1, AP Civil Supplies Bhavan Lane, Somajiguda, Hyderabad – 500082 INDIAPhone: +91‐40‐33404040| E‐mail: services@transgraph com | Internet: www transgraph com

26