Paper 3A: Cost Accounting Chapter 7 CA. Dharmendra · PDF file1 • Meaning & Features Of...

32

Paper 3A: Cost Accounting Chapter 7 CA. Dharmendra Gupta, FCA

Transcript of Paper 3A: Cost Accounting Chapter 7 CA. Dharmendra · PDF file1 • Meaning & Features Of...

Paper 3A: Cost Accounting Chapter 7CA. Dharmendra Gupta, FCA

11 • Meaning & Features Of Process Costing

22 • Applicability of Process Costing

33 • Costs Classification

44 • Cost Unit in Process Costing

55 • Treatment of Normal loss, Abnormal loss and Abnormal gain

66 • Costing of equivalent production units

77 • Inter-process profit

88 • Joint product and By product

Wherein Raw Material converted from one identifiable form into another

Process distinct in manufacturing or production

Useful in steel, Scrap, chemical, rubber production

Steel Production

Soap Production

Chemical Production

Rubber Production

Vegetable oil Production

paints Production

Varnish Production

Direct Material

Direct Labour

Direct Expenses

Production Overheads

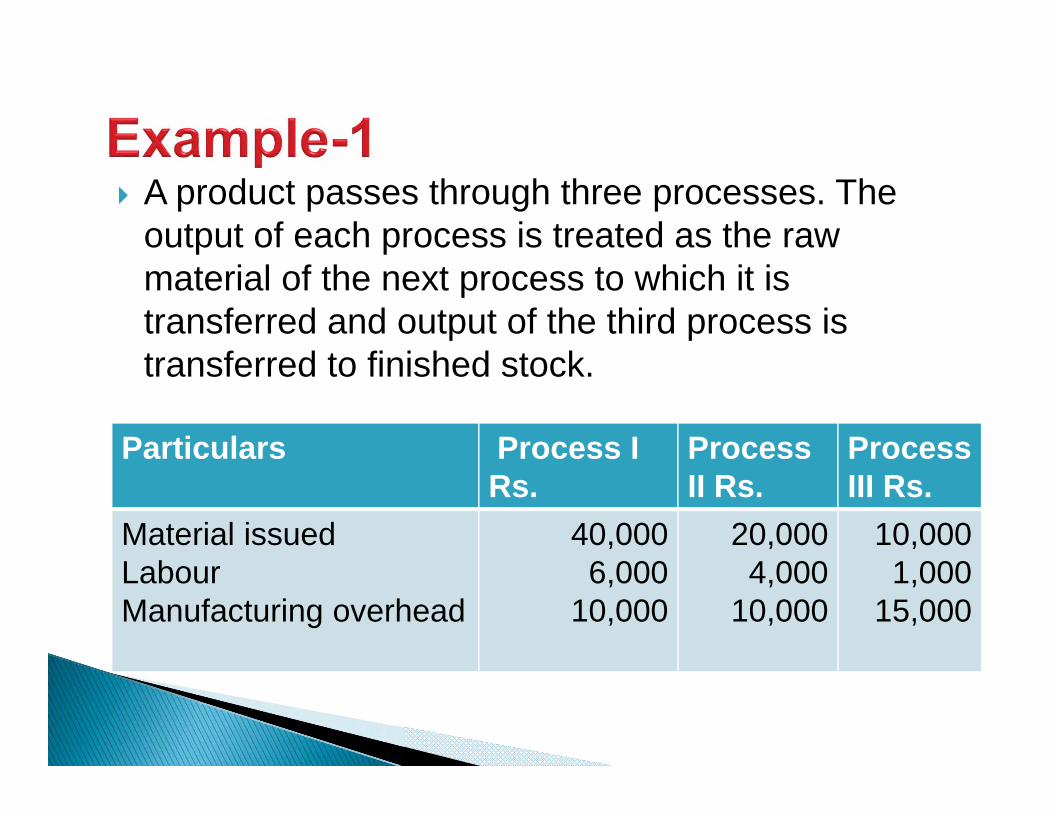

A product passes through three processes. The output of each process is treated as the raw material of the next process to which it is transferred and output of the third process is transferred to finished stock.

Particulars Process IRs.

Process II Rs.

Process III Rs.

Material issuedLabourManufacturing overhead

40,0006,000

10,000

20,0004,000

10,000

10,0001,000

15,000

10,000 units have been issued to the 1st process and after processing, the output of each process is as under :

Output Normal Loss Process No. 1 9,750 units 2% Process No. 2 9,400 units 5% Process No. 3 8,000 units 10% No stock of materials or of work-in-process was left at

the end. Calculate the cost of the finished articles.

Working Notes:-

Process cost=Direct Material + Direct Labour + Direct Expenses + Production Overheads

Process Cost = 40,000 + 6,000 + 10,000

= Rs. 56,000

Scrap Value of Normal loss units = Nil

Cost of a good unit =

(Process Cost – Scrap value of N.loss)/(Input- N.loss units)

Rs. 56000/(10000-200) = 5.714..

Cost of Abnormal Loss = 50 X 5.714 = Rs.286

Cost of Units Transferred to Next Process = 9750 X 5.714

= Rs. 55714

Process I A/C

Particular Units Rs. Particular Units Rs.

To MaterialTo LabourTo OH

10,000 40,0006,000

10,000

By Normal wastageBy Abnormal wastage (cost per unit, Rs 5.714)

200

50

--

286

By Process No, 2 (T/Fof completed units)

9,750 55,714

Total 10,000 56,000 Total 10,000 56,000

Particular Units Rs. Particular Units Rs.To Process No, 1

“ Materials“ Labour“ OH“ Abnormal gain

@ Rs. 9,686

9,750

138

55,71420,000

4,00010,000

1,337

By Normal wastage ( 5% of 9,750 )By Process No. 3 ( cost per unit Rs. 9,686)

488

9,400

-

91,051

Total 9,888 91,051 Total 9,888 91,051

Note : The cost per unit is obtained by dividing Rs. 89,714 by 9,262 units, i.e., 9,750 units less 488 units.

Units Rs. Particular Units Rs.To Process No.2To MaterialsTo LaboursTo OH

9400 9105110000

100015000

By Normal wastage

By Abnormal wastage(cost per unit Rs13836)

By Finished stock

940

460

8000

--

6364

110687Total 9400 117051 Total 9400 117051

Note : The calculation of the cost of abnormal wastage : Normal Output = 9400 units – 940 units = 8460 unitsCost per unit of normal output = 117051 / 8460 = 13.836Cost of 460 units is = 6364

Equivalent production means converting the incomplete production

units into their equivalent completed units.

Formula for computing equivalent completed

units is:

• Equivalent completed units = Actual no. units in process manufacture x %age of work completed

Process Costing• Refer to where raw materials are converted from one form to another• Standardized mass production• Output of each Process consists of similar units, in large quantities.

Job Costing• Refer to specific contract work order or arrangement, where work is

executed as per customer requirement• Specialized production based on customers specifications. • Each job is distinct from other. Output consists of one or a few items

only.

Compute equivalent production & cost per equivalent unit. Also evaluate the output.• Opening work-in-progress 1000 units ( 60% complete). Cost

Rs. 1100. Units introduced during the period 10.000 units; Cost Rs. 19300. Transferred to next process – 9.000 units.

• Closing work-in-progress- 800 units (75% complete). Normal loss is estimated at 10% of total input including units in process at the beginning. Scrap realise Rs. 1 per unit. Scrapped are 100% complete.

Computation of equivalent production & cost per equivalent unit and evaluate the output

Particulars

Input units

Particulars Output units

% work done

Equivalent

UnitsOp. WIPUnitsIntro

1.00010,000

Op. WIPCompletedNormal Loss

Closing work-in-process

1.0008.0001,100

800

40100

-

75

4008,000

-

600

Abnormal Loss( Bal. Fig.)

100 100 100

1100 11,000 9,100

• Rs.19,300Cost of the Process (for the period)

• Rs. 1,100Less: Scrap value of normal loss

• Rs. 18,200/9100 units =2Cost per equivalent unit

Particulars Equivalent cost/ Amtunits equivalent units

1. op. WIP completed 400 2.00 800Add: Cost of op. WIP - - 1,100complete cost of 1,000 units of op, WIP 1,000 1.90 1.900

2. Completed processed units 8,000 2.00 16,0003. Abnormal loss 100 2.00 2004. Closing WIP 600 2.00 1,200

Joint Product:

Two or More products from the same process or operation of relatively equal importance.

• Example:Petoleum products

By-Products

Products recovered from material discarded from the main process

• Example: Molasses in Sugar Industry

Agriculture product

industries

Chemical process

industries

Sugar industries

Extractive industries

A coke manufacturing product company produces the following products by using 5,000 tonnes of coal @ Rs. 15 per tonne into a common process• Coke 3,500 tonnes• Tar 1,200 tonnes• Sulphate of ammonia 52 tonnes• Benzol 48 tonnes• Apportion the joint cost amongst the product on the basis of the

physical unit method.

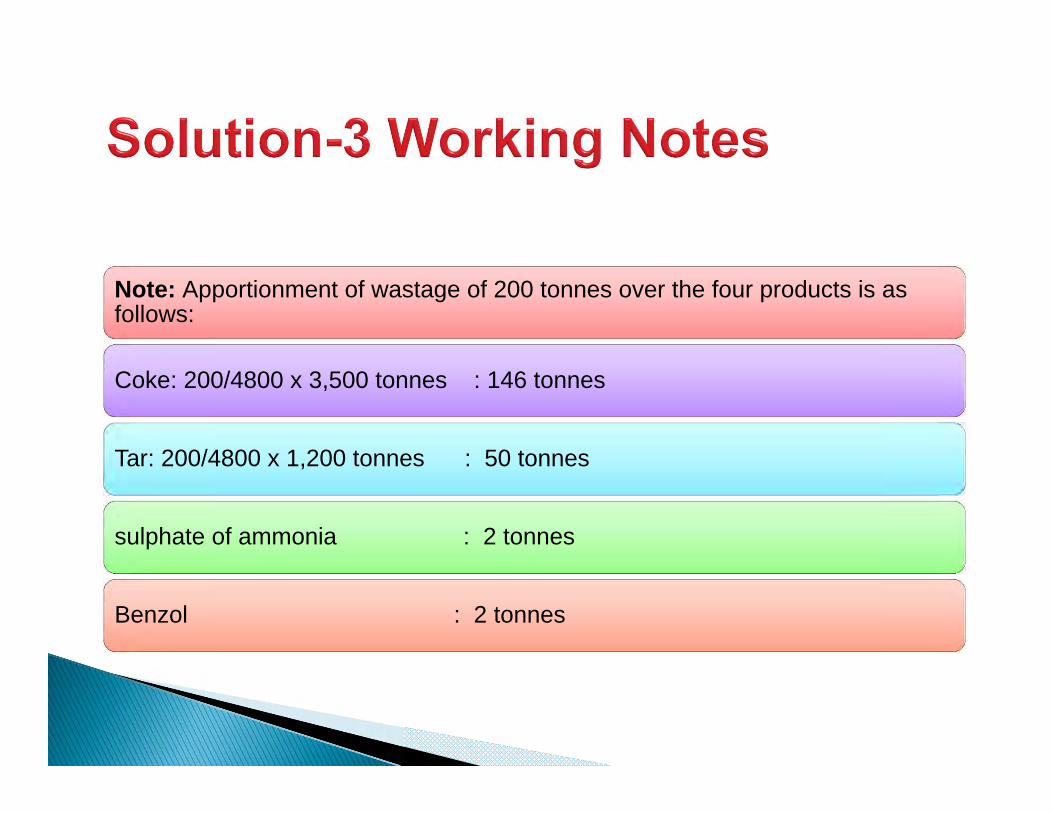

Note: Apportionment of wastage of 200 tonnes over the four products is as follows:

Coke: 200/4800 x 3,500 tonnes : 146 tonnes

Tar: 200/4800 x 1,200 tonnes : 50 tonnes

sulphate of ammonia : 2 tonnes

Benzol : 2 tonnes

ProductsCoke Tar sulphate

of Ammonia

Benzol Wasatge Total

Output(In tonnes)

3500 1200 52 48 200 5000

Wastge(In tonnes)Basis-Weight

146 50 2 2 ----- 200

Total Weights (in tonnes

3646 1250 54 50 5000

Joint Cost @Rs.15.pertonne

54690 18750 810 750 75000

The Output of One process is transferred to next process not at cost but at Market Value or Cost Plus Mark up

The Difference between cost & transfer price is known as inter-process profits

Prepare process cost accounts & finished goods a/c showing the profit element at each stage

Particulars Process I Rs.

Process IIRs.

FGRs.

Op. StockDirect materialsDirect wagesFactory OHClosing stockInter-process profitIncluded in op. stock

7500150001120010500

3700

9000157501125045004500

1500

22500

11250

8250

Output of Process I is Transferred to Process II at 25% profit on the Transfer price.

Output of Process II is Transfered to finished stock at 20% profit on the Transfer price.

Stock in process is valued at prime cost.

Finished stock is valued at the price at which it is received from process II.

Sales during the period are Rs. 1,40,000.

Process I AccountTotal

Rs.Cost Rs.

Profit Rs.

TotalRs.

CostRs.

Profit Rs.

Op. stockD. MaterialsD, wages

Less: Clo. stockPrime costOHProcess costProfit 33.33% of total cost(See WN1)

7500150001120033700(3700)300001050040500

13500

7500150001120033700

( 3700)300001050040500

-

----

---

13500

Transfer to Process II

A/c

54000 40500 13500

54000 40500 13500 54000 40500 13500

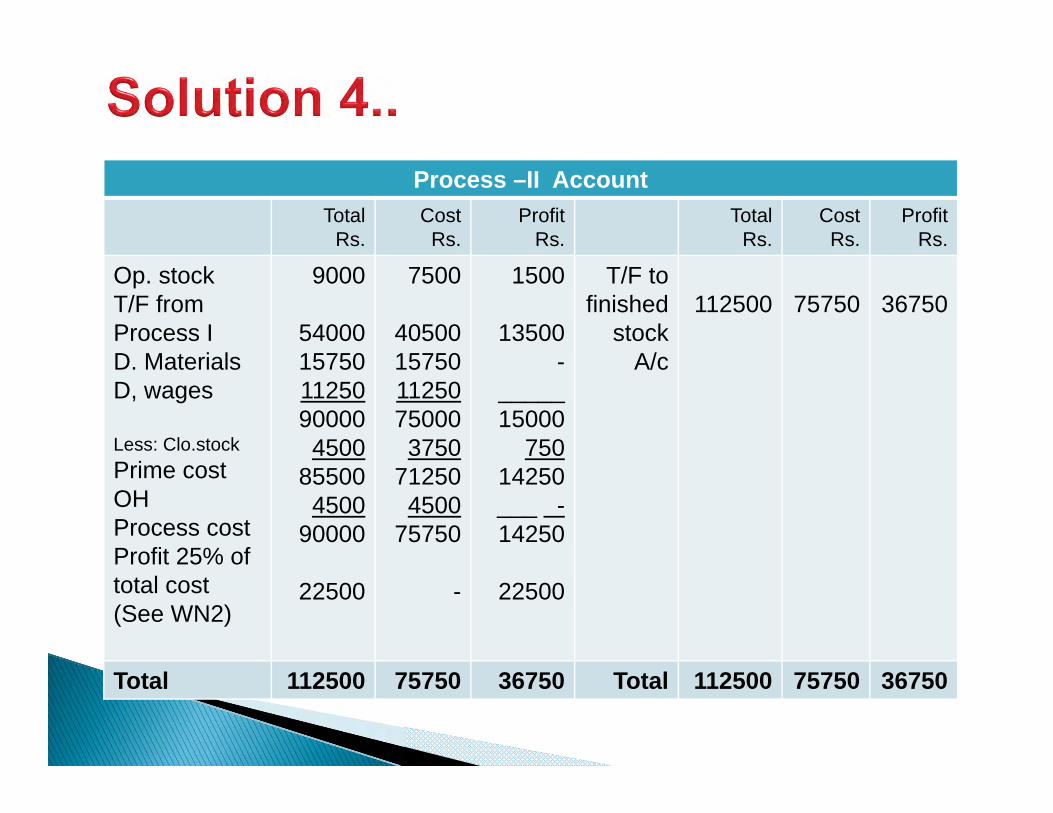

Process –II AccountTotal

Rs.Cost Rs.

Profit Rs.

Total Rs.

Cost Rs.

Profit Rs.

Op. stockT/F from Process ID. MaterialsD, wages

Less: Clo.stockPrime costOHProcess costProfit 25% of total cost(See WN2)

9000

54000157501125090000

450085500

450090000

22500

7500

40500157501125075000

375071250

450075750

-

1500

13500-

_____15000

75014250___ -14250

22500

T/F to finished

stock A/c

112500 75750 36750

Total 112500 75750 36750 Total 112500 75750 36750

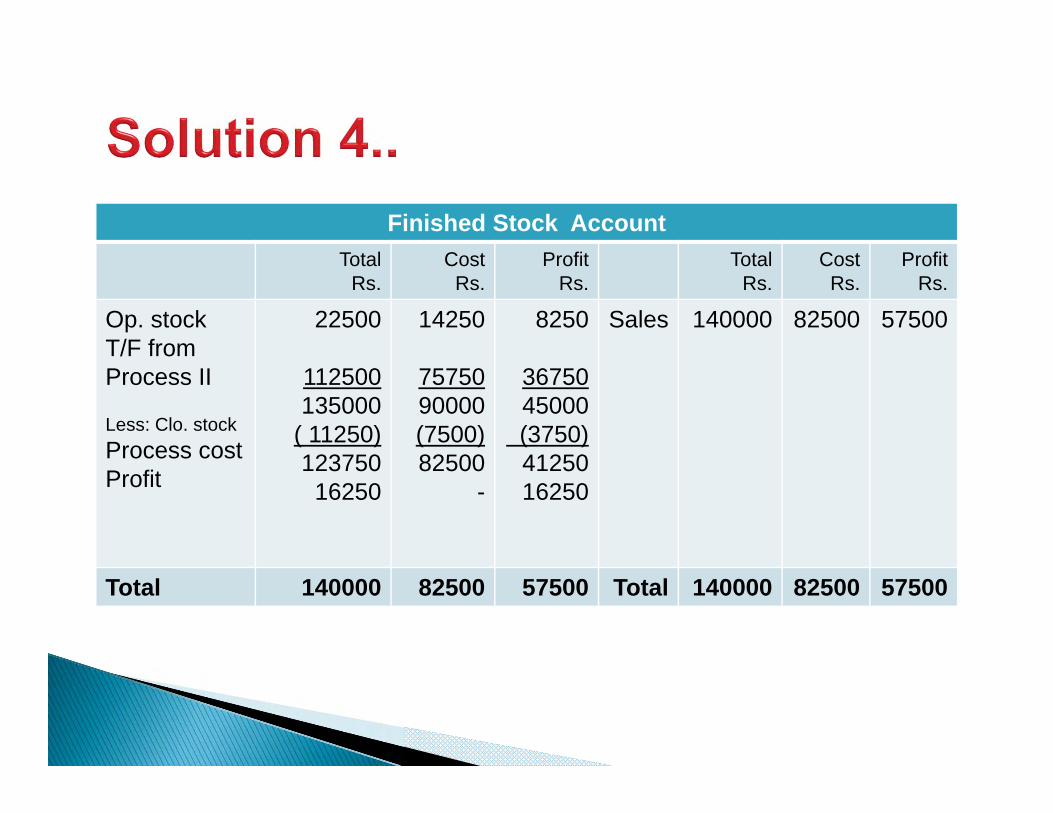

Finished Stock AccountTotal

Rs.Cost Rs.

Profit Rs.

Total Rs.

Cost Rs.

Profit Rs.

Op. stockT/F from Process II

Less: Clo. stockProcess costProfit

22500

112500135000

( 11250)123750

16250

14250

7575090000(7500)82500

-

8250

3675045000(3750)4125016250

Sales 140000 82500 57500

Total 140000 82500 57500 Total 140000 82500 57500

Working Notes :

Let the transfer price be 100 then profit is 25: i.e., cost price is 75

1.If cost is 75 then profit is 25

If cost is 40500 then profit is 25/75 x 40500 = 13500

2. If cost is 80 then profit is 20

If cost is 900000 then profit is 20/80 x 90000 = 22500

1 • Meaning & Features Of Process Costing

2 • Applicability of Process Costing

3 • Costs Classification

4] • Inter-process profit

5 • Costing of equivalent production units

6 • Difference Between Process & Job Costing

7 • Examples and Problem

1 • What do you mean by Process costing?

2 • What are features of Process costing?

3 • Differentiate Process & Job Costing

4 • How to value WIP in Process Costing?

5 • Define By – Product and Joint Products?

6 • How Inter Process Profit is treated?

7 • Name some industries where it can be use?