Pancake House Center 2259 Pasong Tamo Extension Makati ...s3.amazonaws.com/zanran_storage/ ·...

110

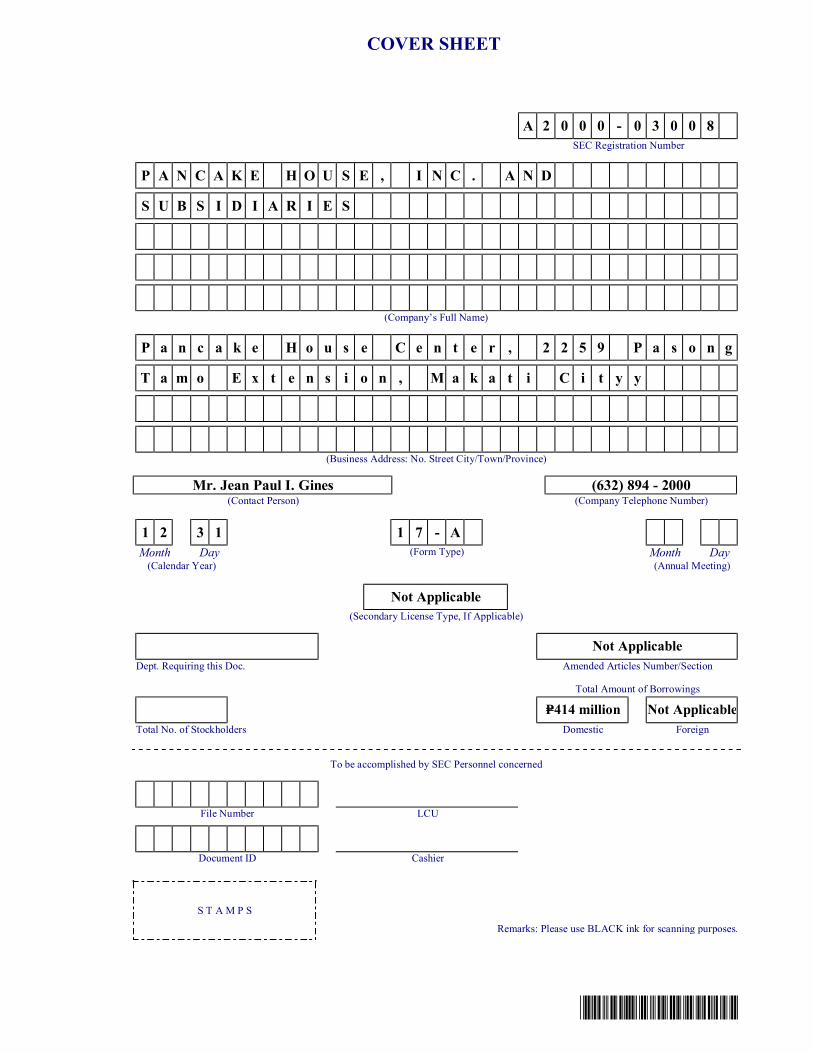

SEC Number: A2000-03008 File Number PANCAKE HOUSE, INC. _________________________________________________ (Company’s Full Name) Pancake House Center 2259 Pasong Tamo Extension Makati City ______________________________________ (Company’s Address) (632) 893-4822 ______________________________________ (Telephone Number) December 31 ______________________________________ (Calendar Year Ending) (month and day) Form 17-A Annual Report ______________________________________ Form Type ______________________________________ Amendment Designation (If applicable) December 31, 2008 ______________________________________ Period Ended Date ______________________________________ (Secondary License Type and File Number)

Transcript of Pancake House Center 2259 Pasong Tamo Extension Makati ...s3.amazonaws.com/zanran_storage/ ·...

SEC Number: A2000-03008 File Number

PANCAKE HOUSE, INC. _________________________________________________

(Company’s Full Name)

Pancake House Center 2259 Pasong Tamo Extension

Makati City ______________________________________

(Company’s Address)

(632) 893-4822 ______________________________________

(Telephone Number)

December 31 ______________________________________

(Calendar Year Ending) (month and day)

Form 17-A Annual Report ______________________________________

Form Type

______________________________________ Amendment Designation (If applicable)

December 31, 2008 ______________________________________

Period Ended Date

______________________________________ (Secondary License Type and File Number)

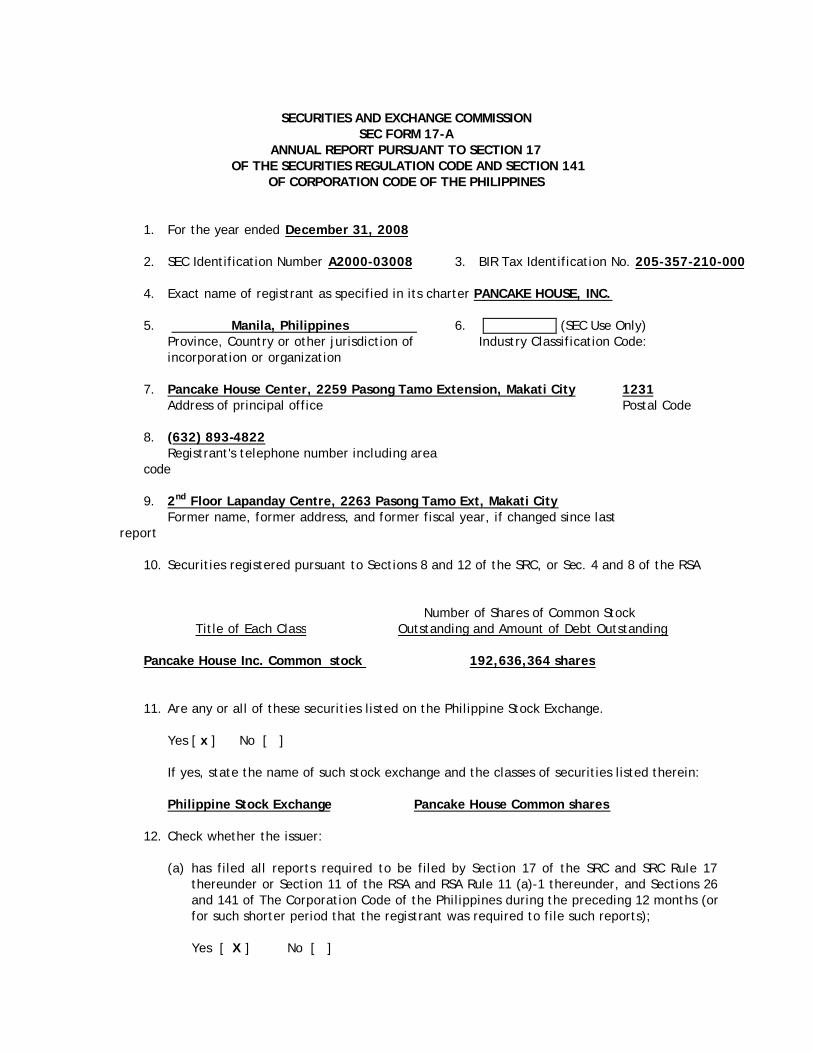

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17

OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES

1. For the year ended December 31, 2008

2. SEC Identification Number A2000-03008 3. BIR Tax Identification No. 205-357-210-000

4. Exact name of registrant as specified in its charter PANCAKE HOUSE, INC.

5. Manila, Philippines 6. (SEC Use Only) Province, Country or other jurisdiction of Industry Classification Code: incorporation or organization

7. Pancake House Center, 2259 Pasong Tamo Extension, Makati City 1231

Address of principal office Postal Code

8. (632) 893-4822 Registrant's telephone number including area

code

9. 2nd Floor Lapanday Centre, 2263 Pasong Tamo Ext, Makati City Former name, former address, and former fiscal year, if changed since last

report 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of the RSA

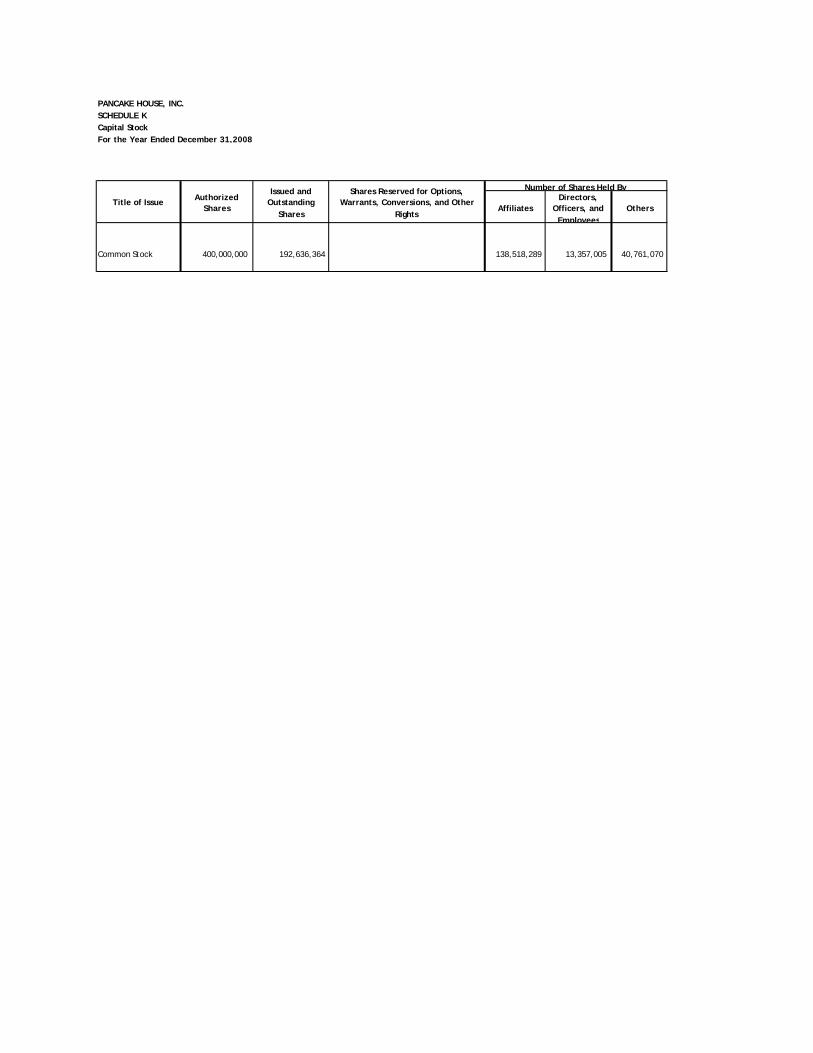

Number of Shares of Common Stock Title of Each Class Outstanding and Amount of Debt Outstanding Pancake House Inc. Common stock 192,636,364 shares

11. Are any or all of these securities listed on the Philippine Stock Exchange.

Yes [ x ] No [ ]

If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange Pancake House Common shares

12. Check whether the issuer:

(a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17

thereunder or Section 11 of the RSA and RSA Rule 11 (a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding 12 months (or for such shorter period that the registrant was required to file such reports);

Yes [ X ] No [ ]

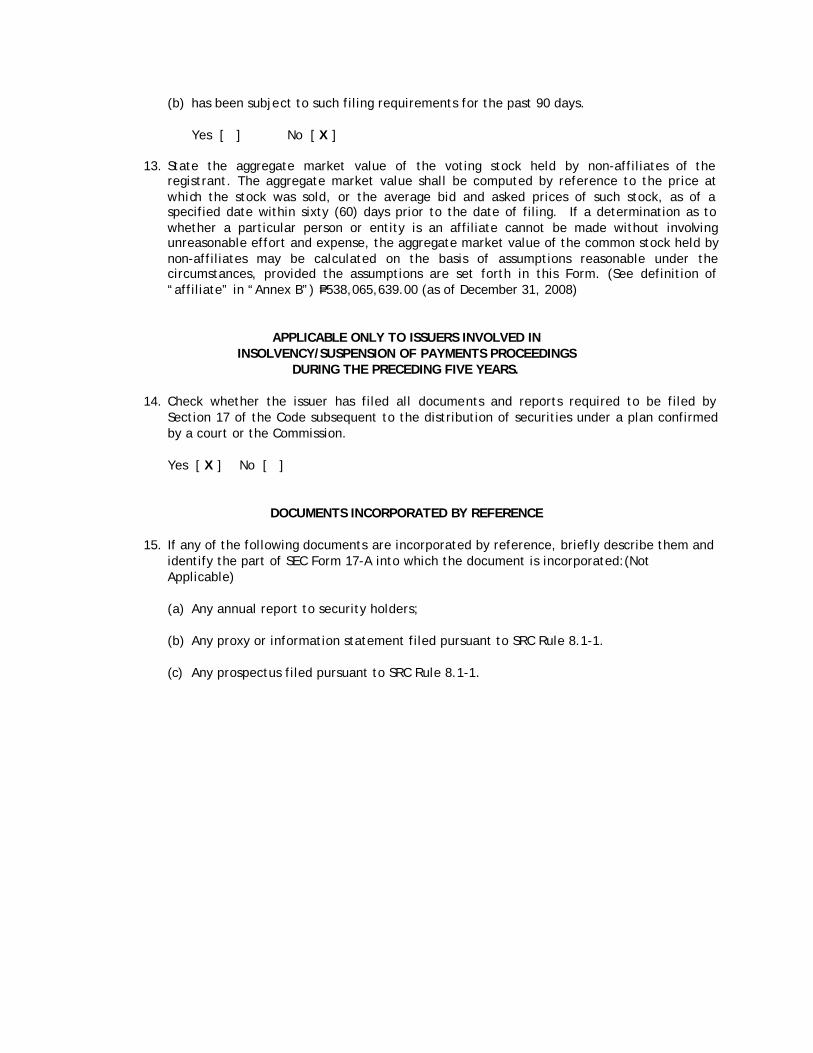

(b) has been subject to such filing requirements for the past 90 days. Yes [ ] No [ X ]

13. State the aggregate market value of the voting stock held by non-affiliates of the

registrant. The aggregate market value shall be computed by reference to the price at which the stock was sold, or the average bid and asked prices of such stock, as of a specified date within sixty (60) days prior to the date of filing. If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided the assumptions are set forth in this Form. (See definition of “affiliate” in “Annex B”) P=538,065,639.00 (as of December 31, 2008)

APPLICABLE ONLY TO ISSUERS INVOLVED IN INSOLVENCY/SUSPENSION OF PAYMENTS PROCEEDINGS

DURING THE PRECEDING FIVE YEARS.

14. Check whether the issuer has filed all documents and reports required to be filed by Section 17 of the Code subsequent to the distribution of securities under a plan confirmed by a court or the Commission. Yes [ X ] No [ ]

DOCUMENTS INCORPORATED BY REFERENCE

15. If any of the following documents are incorporated by reference, briefly describe them and identify the part of SEC Form 17-A into which the document is incorporated:(Not Applicable)

(a) Any annual report to security holders;

(b) Any proxy or information statement filed pursuant to SRC Rule 8.1-1.

(c) Any prospectus filed pursuant to SRC Rule 8.1-1.

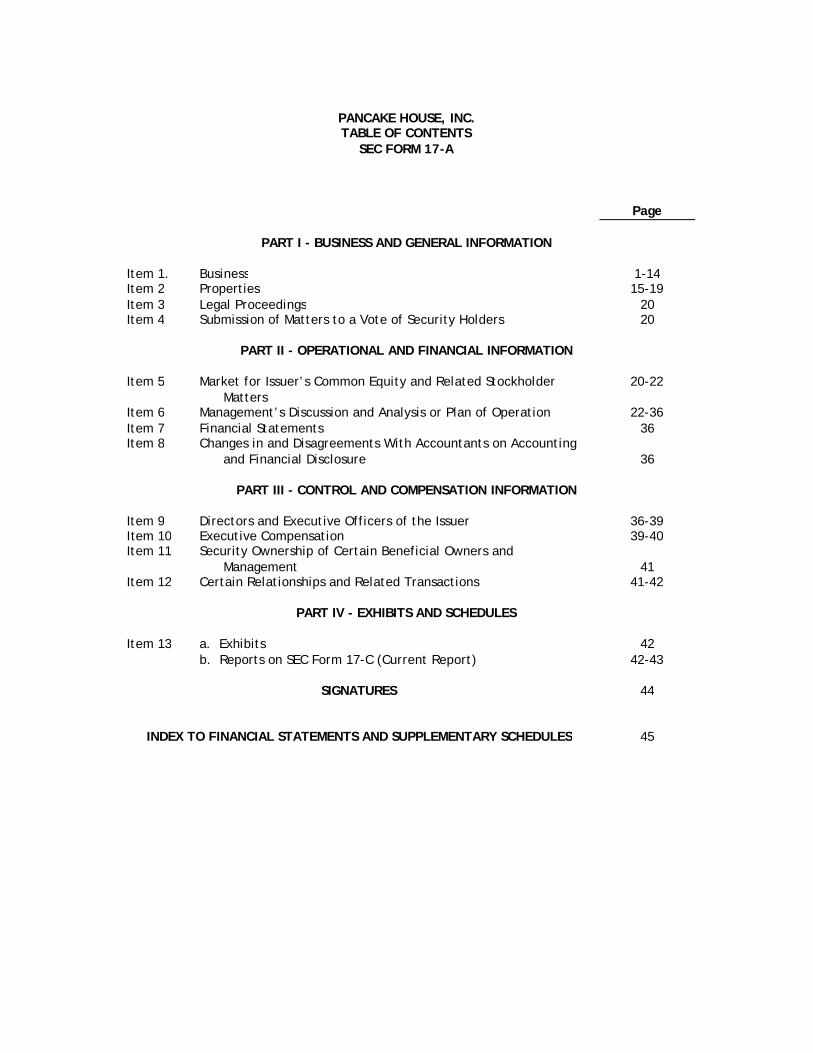

PANCAKE HOUSE, INC. TABLE OF CONTENTS

SEC FORM 17-A

Page

PART I - BUSINESS AND GENERAL INFORMATION Item 1. Business 1-14 Item 2 Properties 15-19 Item 3 Legal Proceedings 20 Item 4 Submission of Matters to a Vote of Security Holders 20

PART II - OPERATIONAL AND FINANCIAL INFORMATION Item 5 Market for Issuer’s Common Equity and Related Stockholder

Matters 20-22

Item 6 Management’s Discussion and Analysis or Plan of Operation 22-36 Item 7 Financial Statements 36 Item 8 Changes in and Disagreements With Accountants on Accounting

and Financial Disclosure

36

PART III - CONTROL AND COMPENSATION INFORMATION Item 9 Directors and Executive Officers of the Issuer 36-39 Item 10 Executive Compensation 39-40 Item 11 Security Ownership of Certain Beneficial Owners and

Management

41 Item 12 Certain Relationships and Related Transactions 41-42

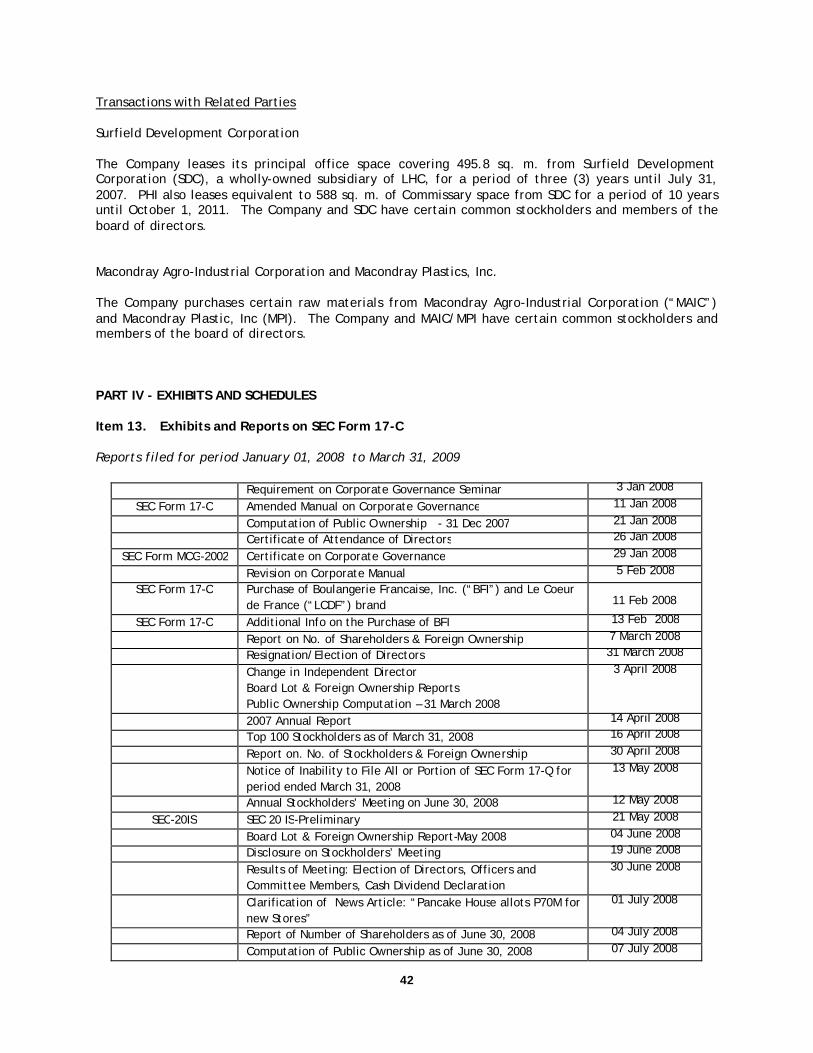

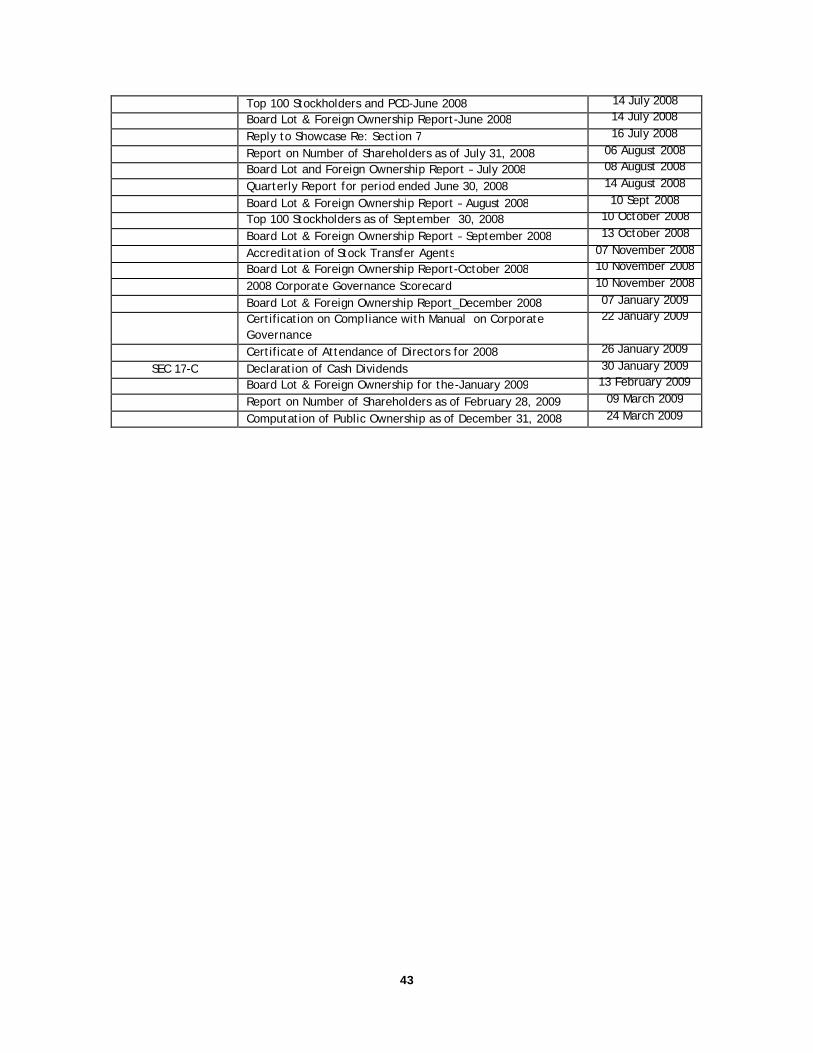

PART IV - EXHIBITS AND SCHEDULES Item 13 a. Exhibits 42 b. Reports on SEC Form 17-C (Current Report) 42-43

SIGNATURES 44

INDEX TO FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES 45

1

PART I - BUSINESS AND GENERAL INFORMATION Item 1. Business Nature of Business and Brief Historical Background The Company Pancake House, Inc. (“PHI” or the “Company”) is a publicly listed company in the Philippine Stock Exchange (“PSE”). It is a Filipino-owned corporation, principally engaged in the development, operation and franchising of a casual dining chain of restaurants under the trade name “Pancake House”. The consumer brand name has traditionally been associated with specialty pancakes and waffles and has likewise expanded to offer an array of popular international dishes such as spaghetti, tacos and chicken. The Company also owns and operates various restaurant brands directly or through its subsidiaries. These brands include “Dencio’s”, “Ka bisera”, “Teriyaki Boy”, “Singkit”, “Sizzlin’ Pepper Steak” and “Le Coeur De France” (collectively, the “Group”). Total system-wide sales of the Group (total restaurant sales from company-owned, joint venture and franchised stores) reached PHP 2.3 billion, translating to a compounded annual growth rate of 30% over a 3-year period. The Group opened 24 stores in 2008, including the group’s second outlet in Malaysia. The original Pancake House was established in 1970 by Milagros Basa, Leticia Zamora and Carmen Zaragosa. In 1974, Sta. Rosa Food Services Corporation (“SRFSC”) and in 1978, Extrovert Corporation (“Extrovert”), were incorporated to hold ownership in succeeding Pancake House outlets. It successfully opened its first franchised outlet in Greenhills, San Juan in 1978.

On February 15, 2000, a new investor group led by Mr. Martin P. Lorenzo entered into an Asset Purchase Agreement with SRFSC and Extrovert for the acquisition of the “Pancake House” trade name and purchase of all of the latter’s operating assets. Pending the final purchase, a new team of management and employees was organized to take over the company-owned outlets of SRFSC and Extrovert. On March 1, 2000, the new investor group incorporated Pancake House, Inc. as the acquisition vehicle of the investor group, finalized the purchase of the operating assets. On December 15, 2000, Pancake House, Inc. was listed in the Philippine Stock Exchange.

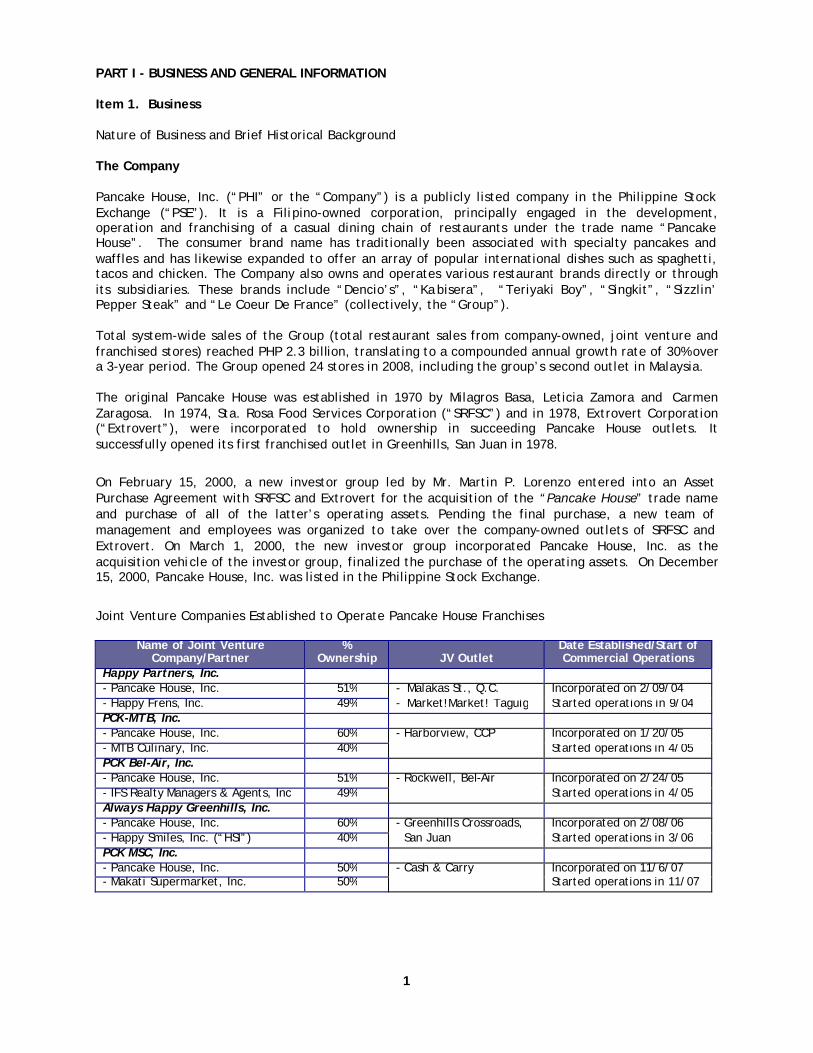

Joint Venture Companies Established to Operate Pancake House Franchises

Name of Joint Venture

Company/Partner %

Ownership

JV Outlet Date Established/Start of Commercial Operations

Happy Partners, Inc. - Pancake House, Inc. 51% - Malakas St., Q.C. Incorporated on 2/09/04 - Happy Frens, Inc. 49% - Market!Market! Taguig Started operations in 9/04 PCK-MTB, Inc. - Pancake House, Inc. 60% - Harborview, CCP Incorporated on 1/20/05 - MTB Culinary, Inc. 40% Started operations in 4/05 PCK Bel-Air, Inc. - Pancake House, Inc. 51% - Rockwell, Bel-Air Incorporated on 2/24/05 - IFS Realty Managers & Agents, Inc 49% Started operations in 4/05 Always Happy Greenhills, Inc. - Pancake House, Inc. 60% - Greenhills Crossroads, Incorporated on 2/08/06 - Happy Smiles, Inc. (“HSI”) 40% San Juan Started operations in 3/06 PCK MSC, Inc. - Pancake House, Inc. 50% - Cash & Carry Incorporated on 11/6/07 - Makati Supermarket, Inc. 50% Started operations in 11/07

2

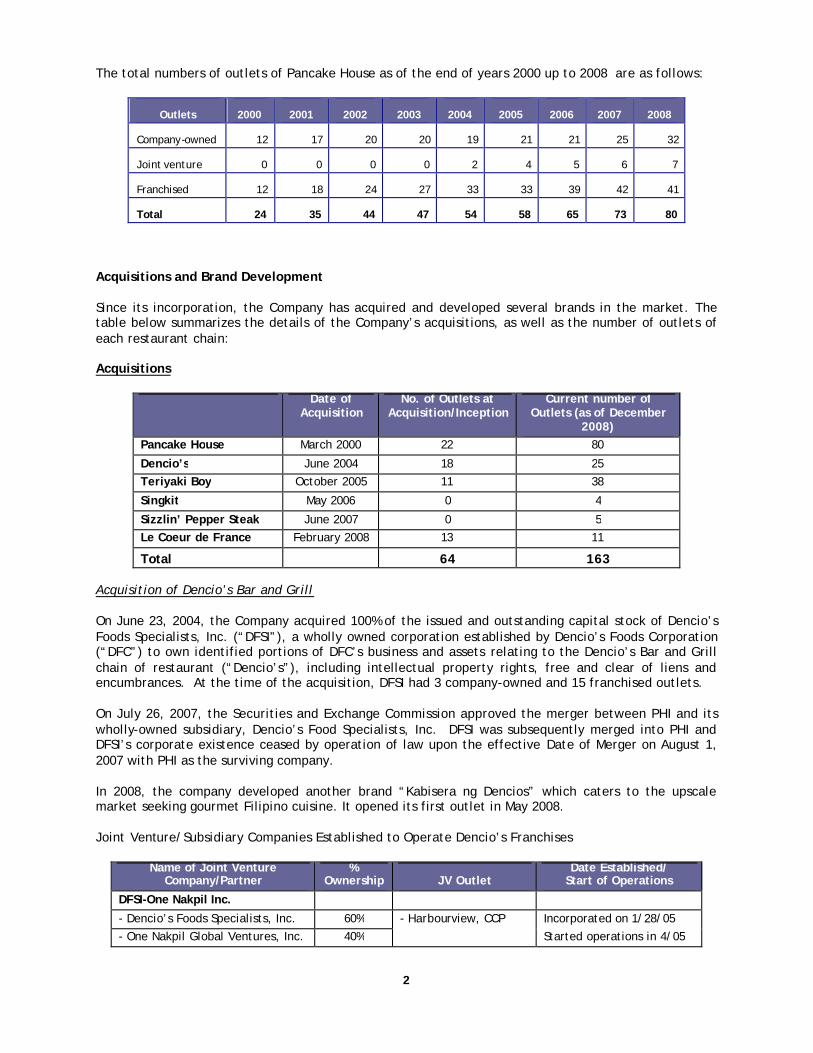

The total numbers of outlets of Pancake House as of the end of years 2000 up to 2008 are as follows:

Outlets 2000 2001 2002 2003 2004 2005 2006 2007 2008

Company-owned 12 17 20 20 19 21 21 25 32

Joint venture 0 0 0 0 2 4 5 6 7

Franchised 12 18 24 27 33 33 39 42 41

Total 24 35 44 47 54 58 65 73 80

Acquisitions and Brand Development Since its incorporation, the Company has acquired and developed several brands in the market. The table below summarizes the details of the Company’s acquisitions, as well as the number of outlets of each restaurant chain:

Acquisitions

Date of

Acquisition No. of Outlets at

Acquisition/Inception Current number of

Outlets (as of December 2008)

Pancake House March 2000 22 80

Dencio’s June 2004 18 25 Teriyaki Boy October 2005 11 38

Singkit May 2006 0 4

Sizzlin’ Pepper Steak June 2007 0 5 Le Coeur de France February 2008 13 11

Total 64 163

Acquisition of Dencio’s Bar and Grill On June 23, 2004, the Company acquired 100% of the issued and outstanding capital stock of Dencio’s Foods Specialists, Inc. (“DFSI”), a wholly owned corporation established by Dencio’s Foods Corporation (“DFC”) to own identified portions of DFC’s business and assets relating to the Dencio’s Bar and Grill chain of restaurant (“Dencio’s”), including intellectual property rights, free and clear of liens and encumbrances. At the time of the acquisition, DFSI had 3 company-owned and 15 franchised outlets. On July 26, 2007, the Securities and Exchange Commission approved the merger between PHI and its wholly-owned subsidiary, Dencio’s Food Specialists, Inc. DFSI was subsequently merged into PHI and DFSI’s corporate existence ceased by operation of law upon the effective Date of Merger on August 1, 2007 with PHI as the surviving company. In 2008, the company developed another brand “Kabisera ng Dencios” which caters to the upscale market seeking gourmet Filipino cuisine. It opened its first outlet in May 2008. Joint Venture/Subsidiary Companies Established to Operate Dencio’s Franchises

Name of Joint Venture

Company/Partner %

Ownership

JV Outlet Date Established/

Start of Operations

DFSI-One Nakpil Inc.

- Dencio’s Foods Specialists, Inc. 60% - Harbourview, CCP Incorporated on 1/28/05 - One Nakpil Global Ventures, Inc. 40% Started operations in 4/05

3

Name of Joint Venture Company/Partner

% Ownership

JV Outlet

Date Established/ Start of Operations

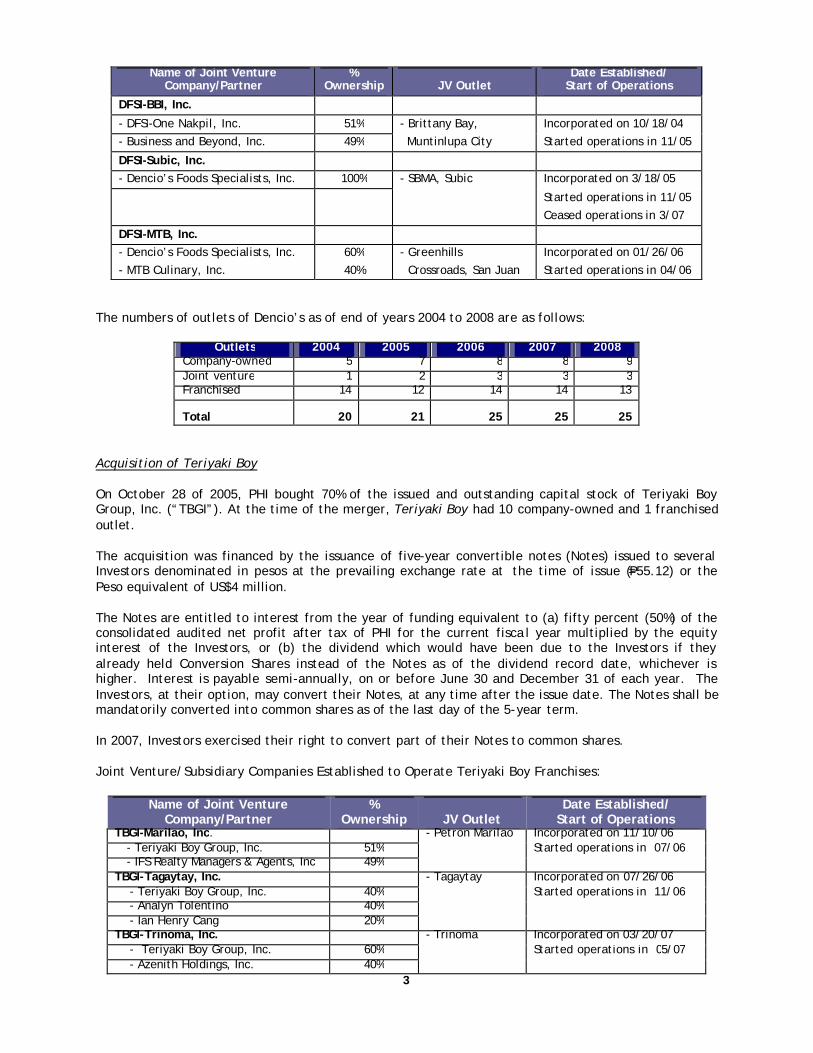

DFSI-BBI, Inc.

- DFSI-One Nakpil, Inc. 51% - Brittany Bay, Incorporated on 10/18/04 - Business and Beyond, Inc. 49% Muntinlupa City Started operations in 11/05

DFSI-Subic, Inc. - Dencio’s Foods Specialists, Inc. 100% - SBMA, Subic Incorporated on 3/18/05

Started operations in 11/05 Ceased operations in 3/07

DFSI-MTB, Inc. - Dencio’s Foods Specialists, Inc. - MTB Culinary, Inc.

60% 40%

- Greenhills Crossroads, San Juan

Incorporated on 01/26/06 Started operations in 04/06

The numbers of outlets of Dencio’s as of end of years 2004 to 2008 are as follows:

Outlets 2004 2005 2006 2007 2008

Company-owned 5 7 8 8 9 Joint venture 1 2 3 3 3 Franchised 14 12 14 14 13

Total 20 21 25 25 25

Acquisition of Teriyaki Boy On October 28 of 2005, PHI bought 70% of the issued and outstanding capital stock of Teriyaki Boy Group, Inc. (“TBGI”). At the time of the merger, Teriyaki Boy had 10 company-owned and 1 franchised outlet. The acquisition was financed by the issuance of five-year convertible notes (Notes) issued to several Investors denominated in pesos at the prevailing exchange rate at the time of issue (P=55.12) or the Peso equivalent of US$4 million. The Notes are entitled to interest from the year of funding equivalent to (a) fifty percent (50%) of the consolidated audited net profit after tax of PHI for the current fisca l year multiplied by the equity interest of the Investors, or (b) the dividend which would have been due to the Investors if they already held Conversion Shares instead of the Notes as of the dividend record date, whichever is higher. Interest is payable semi-annually, on or before June 30 and December 31 of each year. The Investors, at their option, may convert their Notes, at any time after the issue date. The Notes shall be mandatorily converted into common shares as of the last day of the 5-year term. In 2007, Investors exercised their right to convert part of their Notes to common shares. Joint Venture/Subsidiary Companies Established to Operate Teriyaki Boy Franchises:

Name of Joint Venture

Company/Partner %

Ownership

JV Outlet Date Established/

Start of Operations TBGI-Marilao, Inc. - Petron Marilao Incorporated on 11/10/06 - Teriyaki Boy Group, Inc. 51% Started operations in 07/06 - IFS Realty Managers & Agents, Inc 49% TBGI-Tagaytay, Inc. - Tagaytay Incorporated on 07/26/06 - Teriyaki Boy Group, Inc. 40% Started operations in 11/06 - Analyn Tolentino 40% - Ian Henry Cang 20% TBGI-Trinoma, Inc. - Trinoma Incorporated on 03/20/07 - Teriyaki Boy Group, Inc. 60% Started operations in 05/07 - Azenith Holdings, Inc. 40%

4

Name of Joint Venture Company/Partner

% Ownership

JV Outlet

Date Established/ Start of Operations

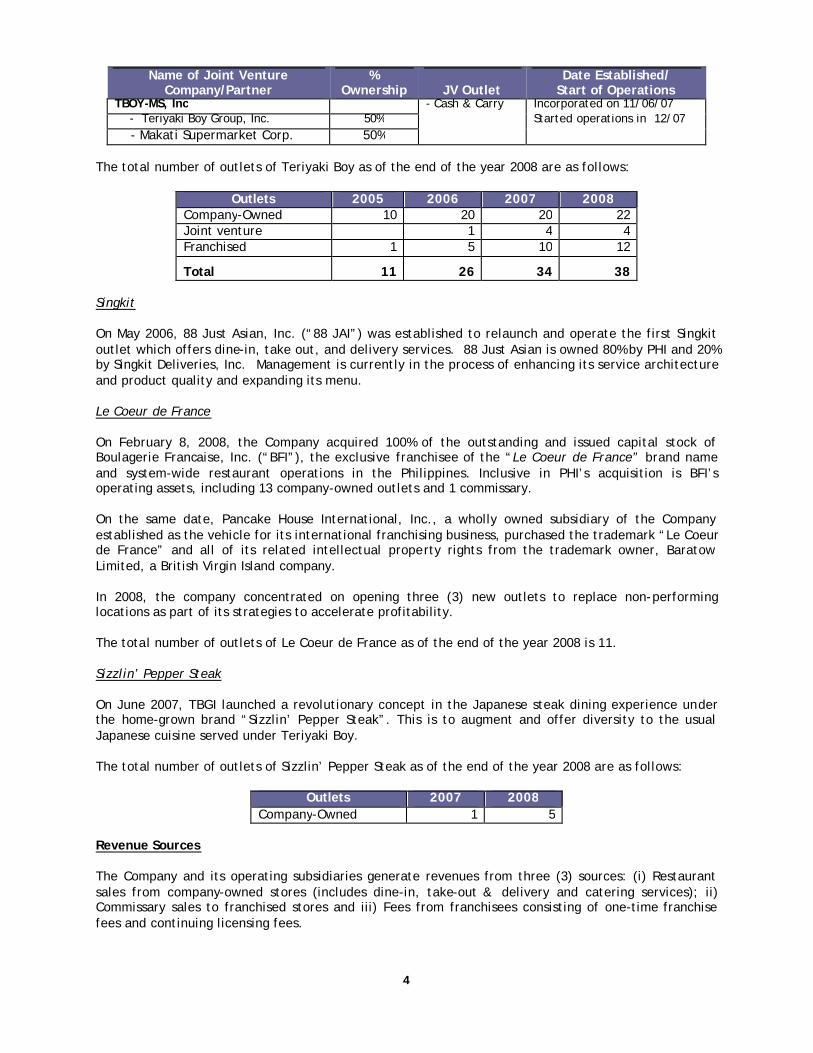

TBOY-MS, Inc - Cash & Carry Incorporated on 11/06/07 - Teriyaki Boy Group, Inc. 50% Started operations in 12/07 - Makati Supermarket Corp. 50%

The total number of outlets of Teriyaki Boy as of the end of the year 2008 are as follows:

Outlets 2005 2006 2007 2008

Company-Owned 10 20 20 22 Joint venture 1 4 4 Franchised 1 5 10 12

Total 11 26 34 38

Singkit On May 2006, 88 Just Asian, Inc. (“88 JAI”) was established to relaunch and operate the first Singkit outlet which offers dine-in, take out, and delivery services. 88 Just Asian is owned 80% by PHI and 20% by Singkit Deliveries, Inc. Management is currently in the process of enhancing its service architecture and product quality and expanding its menu.

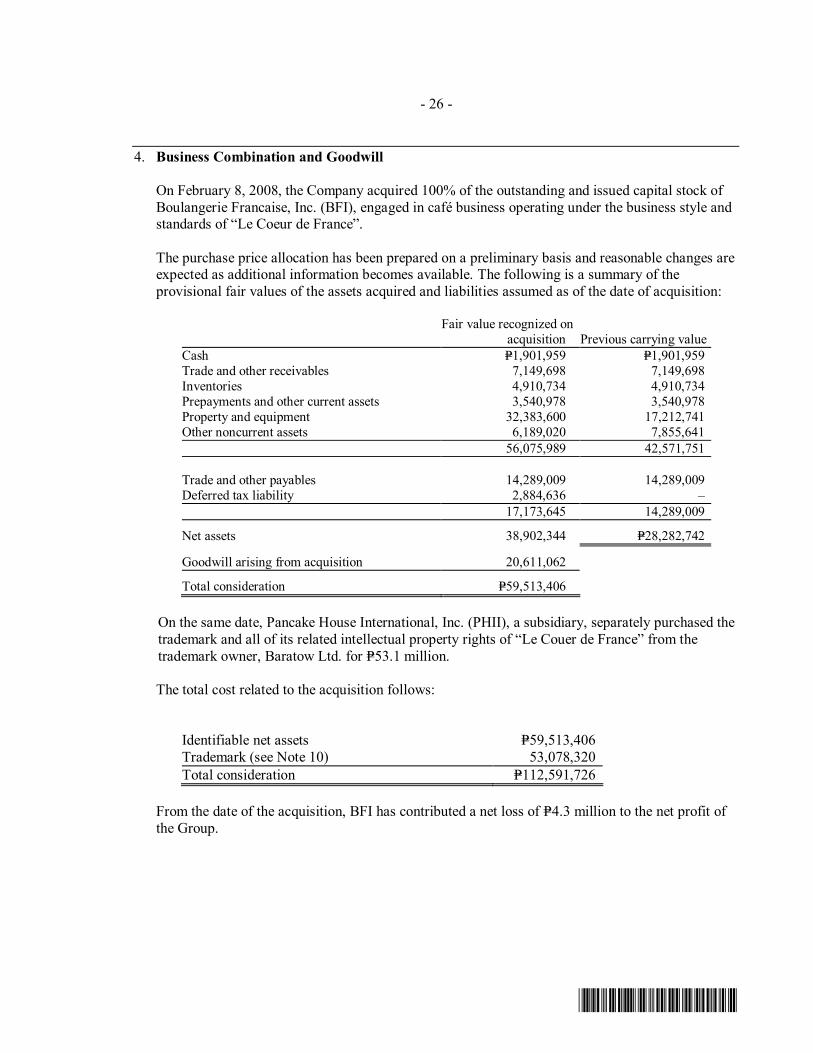

Le Coeur de France On February 8, 2008, the Company acquired 100% of the outstanding and issued capital stock of Boulagerie Francaise, Inc. (“BFI”), the exclusive franchisee of the “Le Coeur de France” brand name and system-wide restaurant operations in the Philippines. Inclusive in PHI’s acquisition is BFI’s operating assets, including 13 company-owned outlets and 1 commissary. On the same date, Pancake House International, Inc., a wholly owned subsidiary of the Company established as the vehicle for its international franchising business, purchased the trademark “Le Coeur de France” and all of its related intellectual property rights from the trademark owner, Baratow Limited, a British Virgin Island company. In 2008, the company concentrated on opening three (3) new outlets to replace non-performing locations as part of its strategies to accelerate profitability.

The total number of outlets of Le Coeur de France as of the end of the year 2008 is 11. Sizzlin’ Pepper Steak On June 2007, TBGI launched a revolutionary concept in the Japanese steak dining experience under the home-grown brand “Sizzlin’ Pepper Steak”. This is to augment and offer diversity to the usual Japanese cuisine served under Teriyaki Boy. The total number of outlets of Sizzlin’ Pepper Steak as of the end of the year 2008 are as follows:

Outlets 2007 2008

Company-Owned 1 5 Revenue Sources The Company and its operating subsidiaries generate revenues from three (3) sources: (i) Restaurant sales from company-owned stores (includes dine-in, take-out & delivery and catering services); ii) Commissary sales to franchised stores and iii) Fees from franchisees consisting of one-time franchise fees and continuing licensing fees.

5

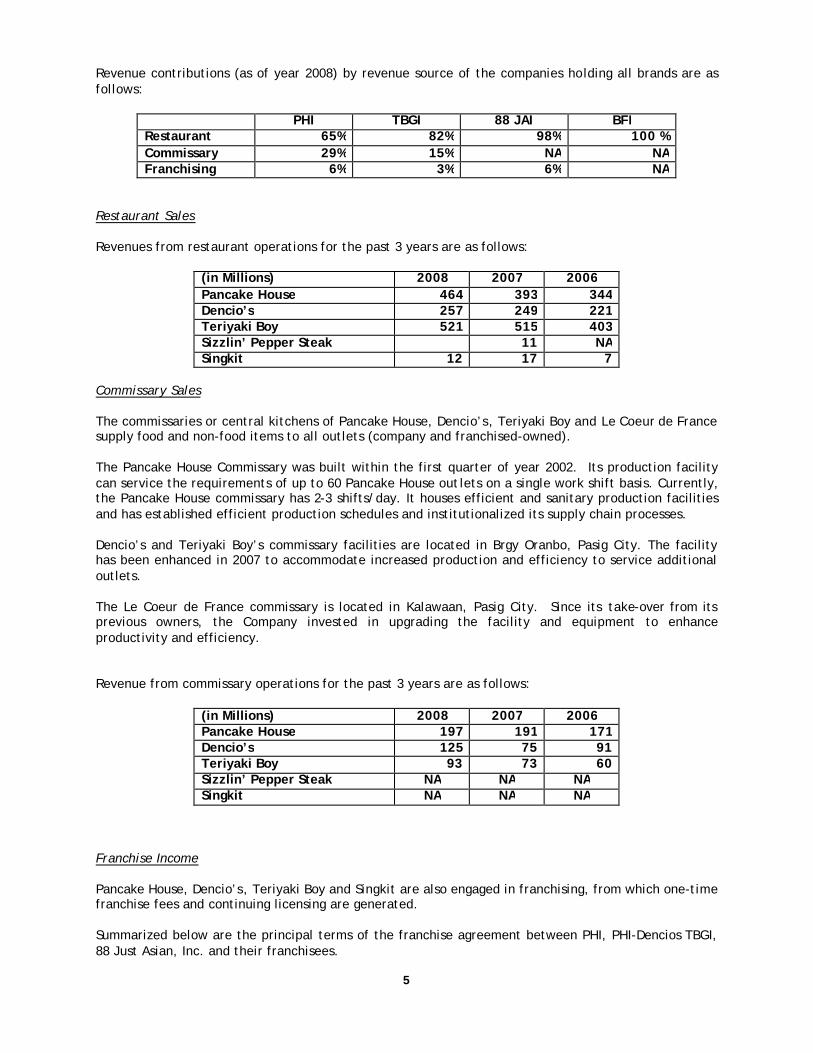

Revenue contributions (as of year 2008) by revenue source of the companies holding all brands are as follows:

PHI TBGI 88 JAI BFI Restaurant 65% 82% 98% 100 % Commissary 29% 15% NA NA Franchising 6% 3% 6% NA

Restaurant Sales Revenues from restaurant operations for the past 3 years are as follows:

(in Millions) 2008 2007 2006 Pancake House 464 393 344 Dencio’s 257 249 221 Teriyaki Boy 521 515 403 Sizzlin’ Pepper Steak 11 NA Singkit 12 17 7

Commissary Sales The commissaries or central kitchens of Pancake House, Dencio’s, Teriyaki Boy and Le Coeur de France supply food and non-food items to all outlets (company and franchised-owned). The Pancake House Commissary was built within the first quarter of year 2002. Its production facility can service the requirements of up to 60 Pancake House outlets on a single work shift basis. Currently, the Pancake House commissary has 2-3 shifts/day. It houses efficient and sanitary production facilities and has established efficient production schedules and institutionalized its supply chain processes. Dencio’s and Teriyaki Boy’s commissary facilities are located in Brgy Oranbo, Pasig City. The facility has been enhanced in 2007 to accommodate increased production and efficiency to service additional outlets. The Le Coeur de France commissary is located in Kalawaan, Pasig City. Since its take-over from its previous owners, the Company invested in upgrading the facility and equipment to enhance productivity and efficiency. Revenue from commissary operations for the past 3 years are as follows:

(in Millions) 2008 2007 2006 Pancake House 197 191 171 Dencio’s 125 75 91 Teriyaki Boy 93 73 60 Sizzlin’ Pepper Steak NA NA NA Singkit NA NA NA

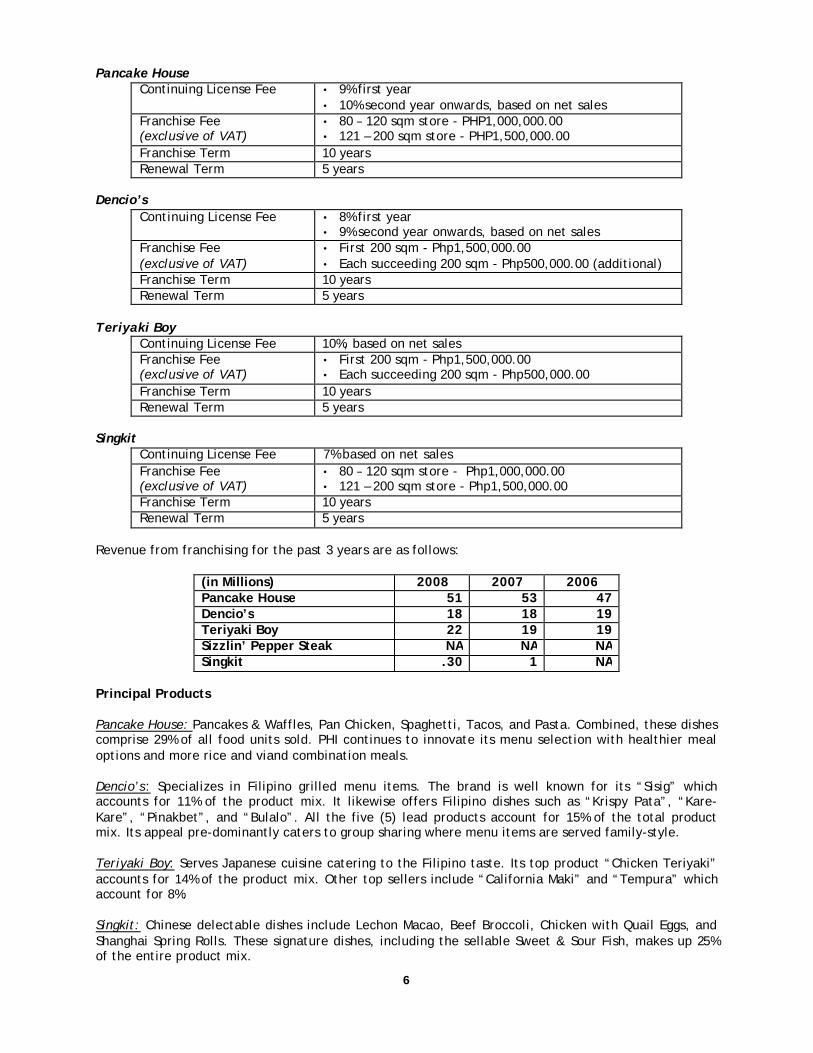

Franchise Income Pancake House, Dencio’s, Teriyaki Boy and Singkit are also engaged in franchising, from which one-time franchise fees and continuing licensing are generated. Summarized below are the principal terms of the franchise agreement between PHI, PHI-Dencios TBGI, 88 Just Asian, Inc. and their franchisees.

6

Pancake House Continuing License Fee • 9% first year

• 10% second year onwards, based on net sales Franchise Fee (exclusive of VAT)

• 80 – 120 sqm store - PHP1,000,000.00 • 121 – 200 sqm store - PHP1,500,000.00

Franchise Term 10 years Renewal Term 5 years

Dencio’s

Continuing License Fee • 8% first year • 9% second year onwards, based on net sales

Franchise Fee (exclusive of VAT)

• First 200 sqm - Php1,500,000.00 • Each succeeding 200 sqm - Php500,000.00 (additional)

Franchise Term 10 years Renewal Term 5 years

Teriyaki Boy

Continuing License Fee 10%, based on net sales Franchise Fee (exclusive of VAT)

• First 200 sqm - Php1,500,000.00 • Each succeeding 200 sqm - Php500,000.00

Franchise Term 10 years Renewal Term 5 years

Singkit

Continuing License Fee 7% based on net sales Franchise Fee (exclusive of VAT)

• 80 – 120 sqm store - Php1,000,000.00 • 121 – 200 sqm store - Php1,500,000.00

Franchise Term 10 years Renewal Term 5 years

Revenue from franchising for the past 3 years are as follows:

(in Millions) 2008 2007 2006 Pancake House 51 53 47 Dencio’s 18 18 19 Teriyaki Boy 22 19 19 Sizzlin’ Pepper Steak NA NA NA Singkit .30 1 NA

Principal Products Pancake House: Pancakes & Waffles, Pan Chicken, Spaghetti, Tacos, and Pasta. Combined, these dishes comprise 29% of all food units sold. PHI continues to innovate its menu selection with healthier meal options and more rice and viand combination meals. Dencio’s: Specializes in Filipino grilled menu items. The brand is well known for its “Sisig” which accounts for 11% of the product mix. It likewise offers Filipino dishes such as “Krispy Pata”, “Kare-Kare”, “Pinakbet”, and “Bulalo”. All the five (5) lead products account for 15% of the total product mix. Its appeal pre-dominantly caters to group sharing where menu items are served family-style. Teriyaki Boy: Serves Japanese cuisine catering to the Filipino taste. Its top product “Chicken Teriyaki” accounts for 14% of the product mix. Other top sellers include “California Maki” and “Tempura” which account for 8%. Singkit: Chinese delectable dishes include Lechon Macao, Beef Broccoli, Chicken with Quail Eggs, and Shanghai Spring Rolls. These signature dishes, including the sellable Sweet & Sour Fish, makes up 25% of the entire product mix.

7

Sizzlin’ Pepper Steak: Specializing in dishes cooked in hot plates, SPS most in demand dishes are their “Pepper Rice” line. These include the “Beef Pepper Rice”, “Seafood Pepper Rice”, Teriyaki Beef Pepper Rice”, and “Pork Pepper Rice” which constitute 36%. Their house specialty also includes the Tori Karaage and Ribeye. Le Coeur de France: Bakery café that offers authentic French baked goods. Among their sellable items are croissants, feuilletes (turnover), chausson, and baguettes. But not limited to French breads, one of the fast moving items is their pandesal, baked to suit the Filipino palate. Distribution Methods Ingredients, supplies, and operating equipment are kept on stock at the Commissary, and are dispatched to the stores based on their orders via delivery vans (Company-owned units and third party truckers) for outlets in Luzon and sea and/or air freight for outlets in Vizayas and Mindanao. Deliveries are done twice to thrice weekly, depending on the volume of sales and distance of the outlet from the Commissary. Operations Commissary and Purchasing The Company operates three (3) central commissaries for all the brands under its wing. It allows the consolidation of common production processes for efficiency and product consistency. Furthermore, the centralized purchasing process likewise enhances the supply chain efficiency since it utilizes economics of scale across all raw material and processed items required by all restaurants. Research & Development The Company employs the Research and Development Team under the commissary which revisits existing menus, production processes and audits quality of products against standards. These activities contribute to the improvement of food and production casts. Furthermore, it develops new product offerings to replace non-performing products that embraces profitability of both the commissary and outlets. Marketing and Advertising Programs The main objective of constantly revitalizing the brands is to increase brand awareness and trials from untapped markets. Marketing strategies include the use of lasting but more cost efficient materials such as billboard placements all over Metro Manila and selected provincial locations to allow all-year round program. Special features using print media and cable television have likewise been utilized to introduce new menu items and concepts to the market. In 2008, Pancake House featured the ‘Welcome Home” Campaign to reinforce the positioning of the brand as into the international/broad spectrum comfort food restaurant in an ambience that is designed for family and friends. It launched the new menu design, table mats and kids menu and introduced new menu items such as Salmon Fillet, Jackfruit Parfait, Stewed Lengua and Shrimp Mango Salad, to name a few. Teriyaki Boy, in the meantime, underwent major brand revitalization as part of its strategy to continuously uphold its market leadership in the Japanese casual dining segment. Most outlets are extensively being refurbished to carry the new logo and concept “A new way to look at an old favorite”. Furthermore, menu items had been enhanced offering newer varieties such as salads and desserts. Dencio’s on the other hand, implemented the “Pugad Dencio’s” campaign to further stimulate the interest of its target market. It engaged the well-known Filipino band “Sugarfree” to render the Dencio’s musical jingle which was played in radio stations and music video played in selected cable channels. The campaign’s objective was to nurture the family gatherings in a homey venue offered by Dencios outlets.

8

International Expansion The brand “Pancake House” continued to expand its international presence by opening its 2nd outlet in Malaysia. Furthermore, the Company is in the process of selling the Master Franchise to a prospective franchisee in Kuala Lumpur. It is currently processing the Company’s registration of the franchise with the Perbadanana Nasional Berhad (PNS) in Malaysia. Furthermore, the brand “Le Coeur de France” and “Teriyaki Boy” are being explored to enter the international market within a year or two. These brands will complement not only the market heritage but their reception to foreign brands as well. Trademarks The Company has pending applications for its trademarks filed with the Intellectual Property Office “(IPO”) of the Department of Trade and Industry of the Philippines, United States Patent and Trademark Office (“USPTO”) and Malaysia Intellectual Property Office (MyIPO). The Company believes that its service marks and trademarks have significant value and are important to its marketing efforts and will pursue registration of its marks whenever possible to mitigate any infringement to its marks. Key Business Strategies Consistent with its thrust to grow the business in the casual dining industry, PHI invests in brands that are equally reputable as the “Pancake House” brand. Its latest acquisition, “Le Coeur de France”, has established solid reputation in providing quality food and service to address the constantly changing demographic preferences and tastes. The Company believes that it can continue to further penetrate into its market base by offering food concept diversification. The Group now covers a wide range of food offerings, from International, Filipino, Japanese, Chinese, and now French cuisine. These brands specifically identified the products and service that cater to the target markets. The target market is defined by age demographics as illustrated in the chart below:

AB& C

2-13 years old AB& C

14-21 years old AB& C

22-35 years old AB&C

36 and Above Pancake House

Dencio’s

Kabisera

Teriyaki Boy

Singkit

Sizzlin’ Peppersteak

Le Coeur de France

Furthermore, the Company has identified these brands to be well received by the international market. These are currently being prepared for the implementation of the international expansion strategy of the Company. Pancake House Pancake House is known for serving food in a wholesome and homey environment. It continues to attract the AB and broad C markets that prefer single serve comfort food in their comfort zones. The

9

Company is active in securing locations, not only in Metro Manila where 80% of the outlets are located, but also in other key cities and provinces in the country like Bulacan, Baguio, Subic, Tagaytay, Laguna, Cagayan de Oro, Cebu and Davao. From the 80 outlets as of year-end 2008, Pancake House is committed to expand to 89 by end of 2009. Pancake House also continuously revitalizes the image of the brand by renovating existing outlets, for both kitchen and dining space. Most outlets, both Company-owned and franchised now carry the new Pancake House concept. Management evaluates each outlet’s profitability performance and relocates or right sizes these, as necessary, to optimize return on investment. Dencio’s Since its acquisition, Dencio’s has continued to evolve into a more inviting restaurant for wholesome family gatherings and place for unwinding and cool down. It offers a unique Filipino dining experience especially with the future launching of a new concept “Kabisera”, a higher-end, Filipino casual-dining concept to serve the more discriminating market. Dencio’s plans to grow the business by expanding its restaurant operations (company-owned and franchised) from the present 26 outlets to 35 within the next two years. Major locations will be owned by the Company, either 100% or as joint venture with selected partners. Teriyaki Boy Teriyaki Boy, being the current leading Japanese brand in the casual dining industry, remains very strong in the market particularly in the 13-35 year old bracket. The Company will expand its restaurant operations to bring the brand closer to its market. From 10 at the time of acquisition in late 2005, the number of outlets has increased to 38 as of end 2008 and will further increase to 42 stores by end of 2009. Competitors Several brands compete in the casual dining segment of the food industry. For Pancake House, the specific competitors include Max’s restaurant, Barrio Fiesta, Dulcinea and Heaven and Eggs. Pancake House Inc. is a publicly listed casual dining restaurant in the Philippines. It manages seven (7) brands under the group namely, Pancake House, Teriyaki Boy, Dencio’s, Kabisera, Café Le Coeur de France, Sizzlin’ Pepper Steak and Singkit. Pancake House was initially recognized as a pancake and waffle breakfast place but it has diversified its menu to include food items such as spaghetti, sandwiches, salad, and steaks among others. Max’s restaurant has been in existence for more than 60 years. It has over 100 branches all around the Philippines and in the United States. Aside from its well known fried chicken, it serves a wide variety of Filipino dishes such as kare-kare, sinigang, crispy pata, and lechon kawali. It also offers combo meals and snacks. Max’s also provides catering and function services for wedding and other occasions. La Dulcinea Restaurant was first established in 1963 in Ermita Manila. It offers Spanish food specifically targeting the AB market. The restaurant popularized the Spanish snack Churros con Chocolate. Dulcinea has now 10 outlets around Metro Manila. Heaven and Eggs started its operation in May 2005. It offers international dishes. It presently has 5 branches in Metro Manila located in Tomas Morato, Eastwood City, Fort Bonifacio Global City, and Glorietta 4, and Trinoma. E-Commerce Development The Group uses Point-of-Sale (POS) systems in all its outlets. The systems provide daily sales information that helps determine demand forecasts and aid in the timely purchases of supplies. Computerized purchasing, inventory management and delivery & billing systems for the Commissaries

10

and ordering system for the stores (both Company-owned and franchised) have also been installed and continuously reviewed for further enhancements. Sources and Availability of Raw Materials The Group sources most of its ingredients and supplies from major local suppliers including San Miguel-Purefoods Corp, Unilever, Nestle Philippines, CDO-Foodsphere Inc., Coca-Cola Bottlers Phils. Inc. and Swift Foods Inc. Restaurant & kitchen supplies and operating equipment are bought from local and foreign sources (through their authorized distributors in the Philippines). The Group maintains a number of suppliers for each type of item and is not dependent on a limited number of suppliers for its requirements. Trademarks The following are the details of pending applications for trademarks filed with the Intellectual Property Office “(IPO”) of the Department of Trade and Industry of the Philippines, United States Patent and Trademark Office (“USPTO”) and Malaysia Intellectual Property Office (“MyIPO”).

Pancake House

1. TM Pancake House & Device

Registered No.: 4-1996-114538 Registered: August 28, 2004 Status: Issuance of Certificate of Registration

2. TM Pancake House Since 1974 & Device Registered No.: 4-2000-015012 Registration: August 28, 2004 Status: Issuance of Certificate of Registration

3. TM Pancake House Since 1974 & Device Application No: 4-1998-01688 Filed: 03 October 1998 File No.: 10P601

Filed with the IPO: 14 March 2000 in favor of PHI by SRFSC (original term- 15 years) Status: No longer being used thus no Declaration of Actual Use was filed

4. TM PAN CHICKEN Application No: 4-2001-0001913 Filed: 16 March 2001, File No.: 10P-616 Filed with the IPO: 29 May 2002 Declaration of Actual Use Filed: 15 March 2004 Status: Issuance of Certificate of Registration

5. TM WE’RE MORE THAN JUST GREAT PANCAKES Application No: 4-2003-0004128 Filed: 08 May 2003 File No.: 10P-823 Declaration of Actual Use Filed: 8 May 2003 Status: Issuance of Certificate of Registration

Dencio’s

1. TM DENCIO’S BAR & GRILL & DEVICE Registered No. 4-2000-006478 Registered: 15 December 2003

11

2. TM DENCIO’S LOGO Application No: 4-2004-011829 Filed: 14 December 2004 File No.: 116-D-001 Status: Application still being examined by the IPO

3. TM DENCIO’S - US TM Application Serial/Reference No: 78/560276 Filed: 03 February 2005 File No.: 116-D-002 Status: Application closed

4. TM Kabisera ng Dencios and Logo Registration No.: 4-2008-500187 Registration Date.: 03 November 2008 Term: Ten Years (until November 03, 2018)

Teriyaki Boy

1. TM WE BRING JAPAN TO YOUR DINING EXPERIENCE

Registered No.: 4-2004-002486 Registration Date: 10 November 2005

2. TM TERIYAKI BOY AND DEVICE WITH CHINESE & JAPANESE CARACTERS

Application No.: 4-2001-006508 Application Date: 31 August 2001 Status: Published for Opposition in the IPO E-Gazette which was released on October 10, 2005

3. TM LOGO

Application No.: 4-2001-006509 Application Date: 31 August 31, 2001 Status: Published for Opposition in the IPO E-Gazette which was released on October 10, 2005

4. TM TBOY TOWN & DEVICE

Application No.: 4-2001-006510 Application Date: 31 August 2001 Status: Published for Opposition in the IPO E-Gazette which was released on October 10, 2005

5. TM TBOY TOWN & DEVICE

Application No.: 4-2006-500015 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration

6. TM JAPANESE CHARACTERS (FAT BOY)

Application No.: 4-2006-500016 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration Term: Ten (10) years (until February 26, 2017)

7. TM TERIYAKI BOY TABEMASHOU LET’S EAT (TEXT LOGO)

Application No.: 4-2006-500017 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration

8. TM TERIYAKI BOY TABEMASHOU LET’S EAT (GRAPHIC LOGO)

Application No.: 4-2006-500018 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration

12

9. TM “BRINGING JAPAN TO YOUR DINING EXPERIENCE”

Application No.: 4-2006-500019 Application Date: 16 March 2006 Status: Certificate of Registration Issued Term: Ten (10) years (until February 26, 2017)

10. TM JAPANESE CHARACTERS (TABEMASHOU LETS EAT)

Application No.: 4-2006-500020 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration

11. TM TERIYAKI BOY LOGO

Application No.: 4-2006-500021 Application Date: 16 March 2006 Status: Issuance of Certificate of Registration

12. TM TERIYAKI BOY LOGO

Application No.: 4-2006-500022 Application Date: 16 March 2006 Status: Certificate of Registration Issued Term: Ten (10) years (until February 26, 2017)

14. TM TERIYAKI BOY AND DEVICE (COLOUR) Application No.: 4-2008-008223 Application Date: 10 July 2008 Status : Published for Opposition in the IPO E-Gazette which was released on March 13, 2009 Singkit

1. TM Singkit & Device Registration No.: 56280 Date Registered: 6 October 1993 Status: Assignment of Registration of Trademark 2. TM Singkit & Device Registration No.: 4-1991-077555 Date Registered: 20 March 2005 3. TM SINGKIT MARK CLASS 29

Application No.: 4-2006-500343 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

4. TM SINGKIT MARK CLASS 43

Application No.: 4-2006-500344 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

5. TM SINGKIT DEVICE CLASS 29

Application No.: 4-2006-500345 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

6. TM SINGKIT DEVICE CLASS 43

Application No.: 4-2006-500346 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

13

7. TM THE GREAT NEW YORK TAKE-OUT CLASS 29

Application No.: 4-2006-500347 Application Date: 03 October 2006 Status: Application still being examined by the IPO

8. TM THE GREAT NEW YORK TAKE-OUT CLASS 43

Application No.: 4-2006-500348 Application Date: 03 October 2006 Status: Application still being examined by the IPO

9. TM CHINITO MARK CLASS 29

Application No.: 4-2006-500349 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

10. TM CHINITO MARK CLASS 43

Application No.: 4-2006-500350 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

11. TM CHINITO DEVICE CLASS 29

Application No.: 4-2006-500351 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

12. TM CHINITO DEVICE CLASS 43

Application No.: 4-2006-500352 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

13. TM CHINITO SIZE MARK CLASS 29

Application No.: 4-2006-500353 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

14. TM CHINITO SIZE MARK CLASS 43

Application No.: 4-2006-500354 Application Date: 03 October 2006 Status: Published for Opposition in the IPO E-Gazette which was released on October 5, 2007

Sizzlin’ Pepper Steak 1. TM BEEF PEPPER RICE

Application No.: 4-2007-500750 Application Date: 08 November 2007 Status: Application still being examined by the IPO

2. TM THE SIZZLIN’ PEPPER STEAK, STEAK & MORE AND DEVICE

Application No.: 4-2006-004060 Application Date: 18 April 2006 Status: Certificate of Registration Issued Term: Ten (10) years (until December 18, 2016)

14

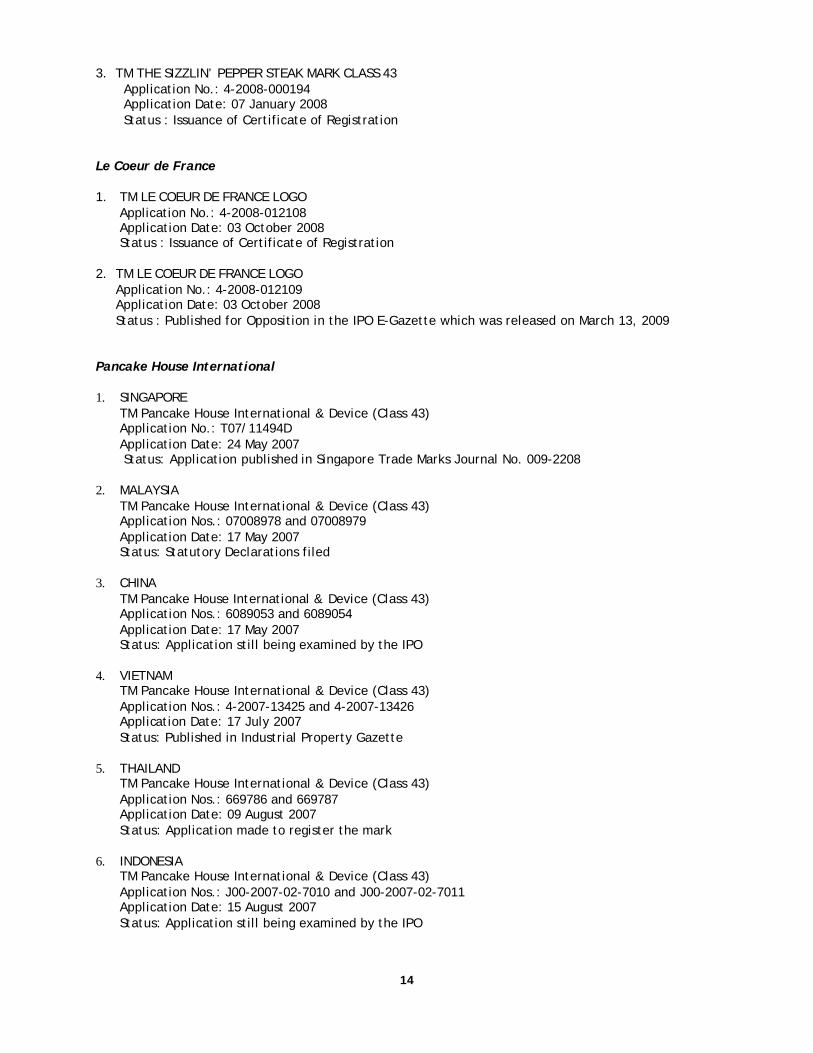

3. TM THE SIZZLIN’ PEPPER STEAK MARK CLASS 43 Application No.: 4-2008-000194 Application Date: 07 January 2008 Status : Issuance of Certificate of Registration

Le Coeur de France 1. TM LE COEUR DE FRANCE LOGO

Application No.: 4-2008-012108 Application Date: 03 October 2008 Status : Issuance of Certificate of Registration

2. TM LE COEUR DE FRANCE LOGO Application No.: 4-2008-012109 Application Date: 03 October 2008

Status : Published for Opposition in the IPO E-Gazette which was released on March 13, 2009

Pancake House International 1. SINGAPORE

TM Pancake House International & Device (Class 43) Application No.: T07/11494D Application Date: 24 May 2007

Status: Application published in Singapore Trade Marks Journal No. 009-2208 2. MALAYSIA

TM Pancake House International & Device (Class 43) Application Nos.: 07008978 and 07008979 Application Date: 17 May 2007 Status: Statutory Declarations filed

3. CHINA

TM Pancake House International & Device (Class 43) Application Nos.: 6089053 and 6089054 Application Date: 17 May 2007

Status: Application still being examined by the IPO 4. VIETNAM

TM Pancake House International & Device (Class 43) Application Nos.: 4-2007-13425 and 4-2007-13426 Application Date: 17 July 2007 Status: Published in Industrial Property Gazette

5. THAILAND

TM Pancake House International & Device (Class 43) Application Nos.: 669786 and 669787 Application Date: 09 August 2007 Status: Application made to register the mark

6. INDONESIA

TM Pancake House International & Device (Class 43) Application Nos.: J00-2007-02-7010 and J00-2007-02-7011 Application Date: 15 August 2007 Status: Application still being examined by the IPO

15

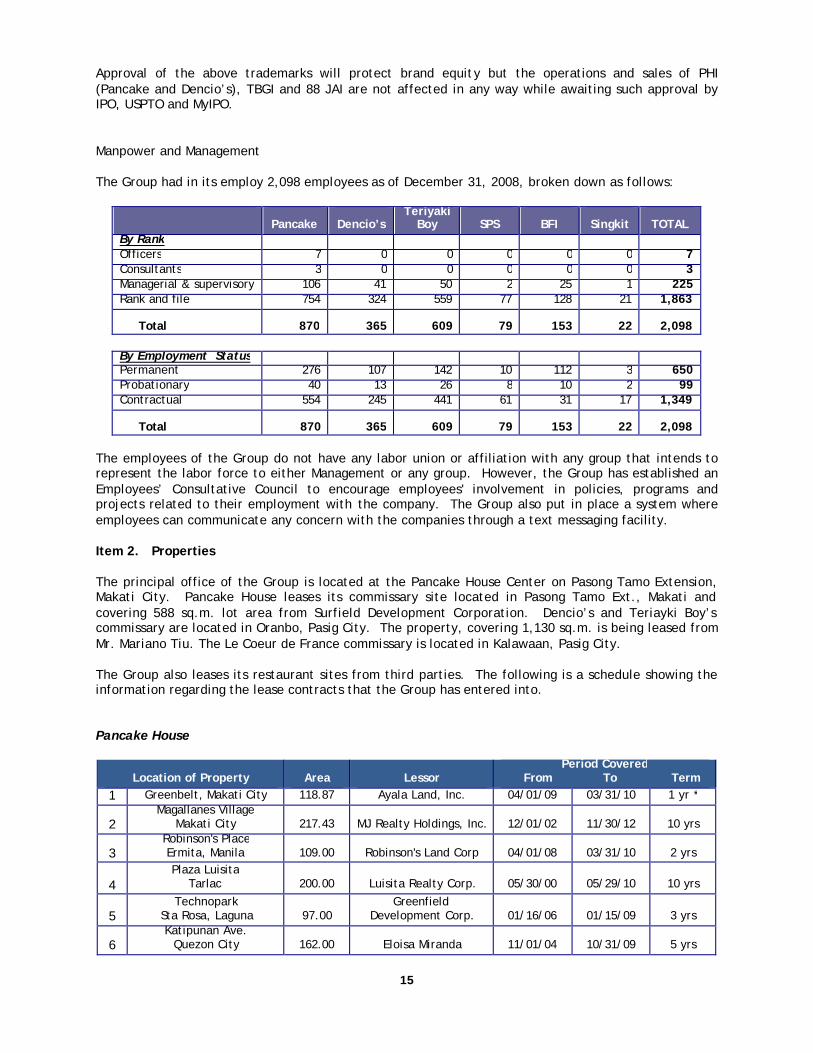

Approval of the above trademarks will protect brand equity but the operations and sales of PHI (Pancake and Dencio’s), TBGI and 88 JAI are not affected in any way while awaiting such approval by IPO, USPTO and MyIPO.

Manpower and Management The Group had in its employ 2,098 employees as of December 31, 2008, broken down as follows:

Pancake

Dencio’s Teriyaki

Boy

SPS

BFI

Singkit

TOTAL By Rank Officers 7 0 0 0 0 0 7 Consultants 3 0 0 0 0 0 3 Managerial & supervisory 106 41 50 2 25 1 225 Rank and file 754 324 559 77 128 21 1,863

Total 870 365 609 79 153 22 2,098

By Employment Status Permanent 276 107 142 10 112 3 650 Probationary 40 13 26 8 10 2 99 Contractual 554 245 441 61 31 17 1,349

Total 870 365 609 79 153 22 2,098

The employees of the Group do not have any labor union or affiliation with any group that intends to represent the labor force to either Management or any group. However, the Group has established an Employees’ Consultative Council to encourage employees' involvement in policies, programs and projects related to their employment with the company. The Group also put in place a system where employees can communicate any concern with the companies through a text messaging facility.

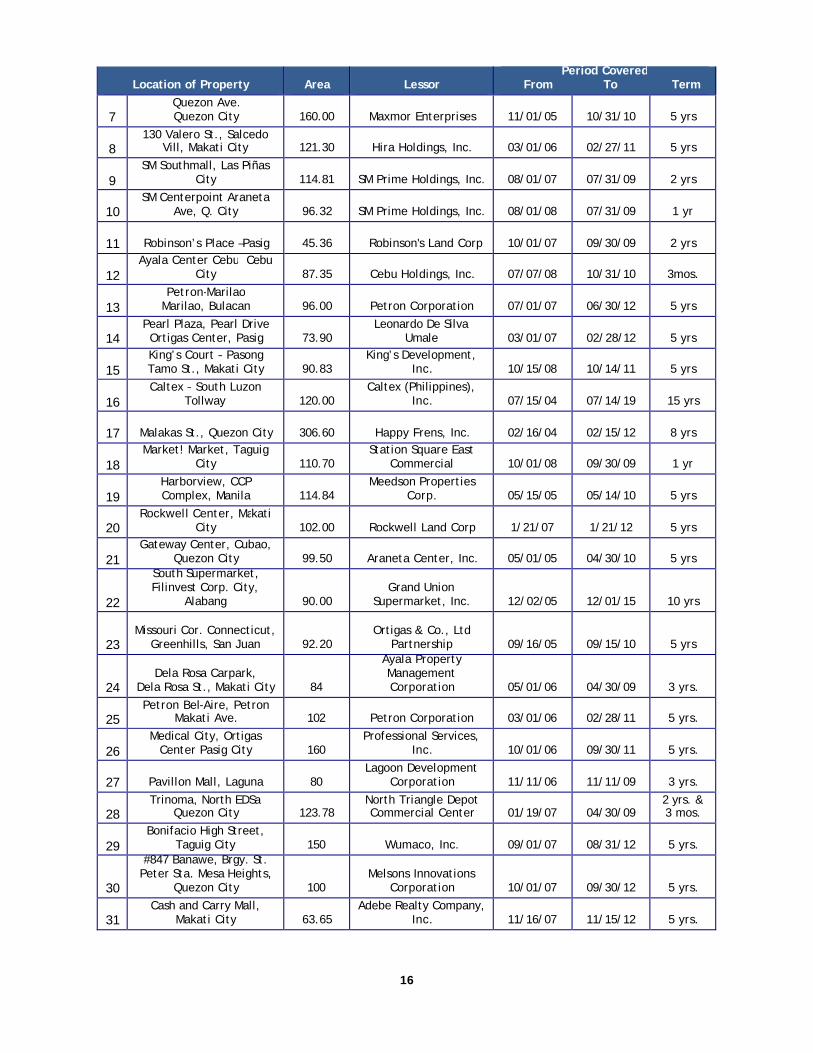

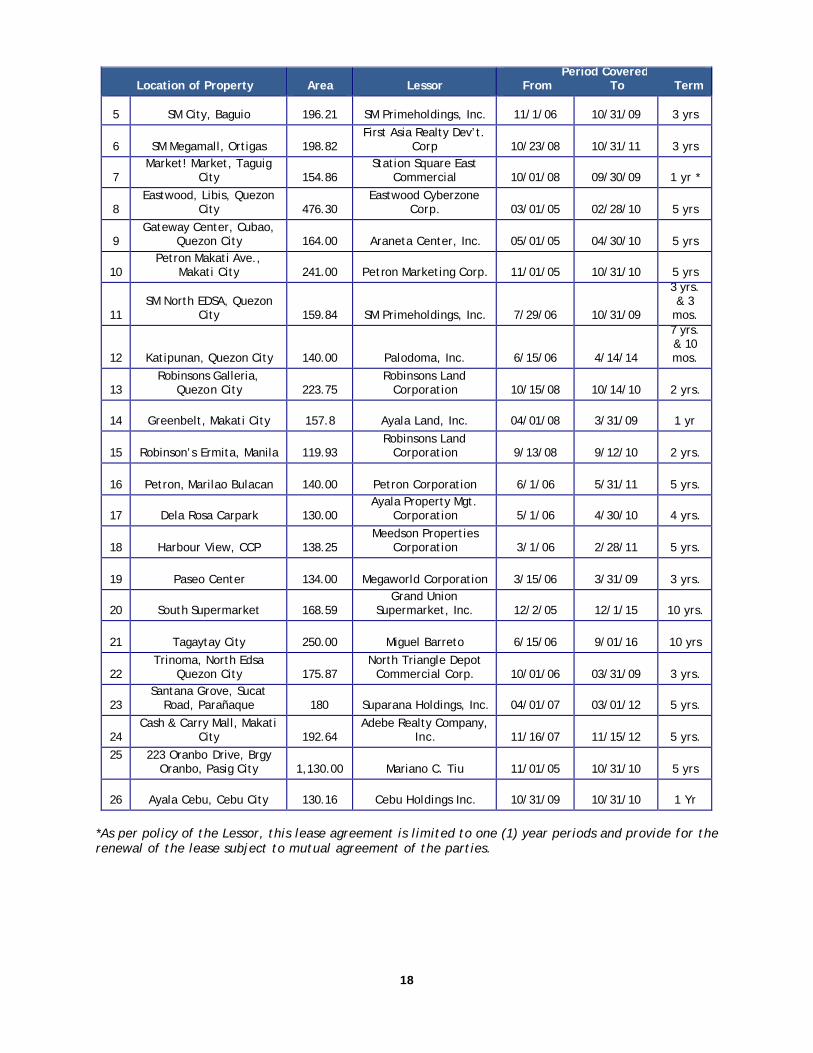

Item 2. Properties The principal office of the Group is located at the Pancake House Center on Pasong Tamo Extension, Makati City. Pancake House leases its commissary site located in Pasong Tamo Ext., Makati and covering 588 sq.m. lot area from Surfield Development Corporation. Dencio’s and Teriayki Boy’s commissary are located in Oranbo, Pasig City. The property, covering 1,130 sq.m. is being leased from Mr. Mariano Tiu. The Le Coeur de France commissary is located in Kalawaan, Pasig City. The Group also leases its restaurant sites from third parties. The following is a schedule showing the information regarding the lease contracts that the Group has entered into. Pancake House

Location of Property Area Lessor Period Covered

From To Term 1 Greenbelt, Makati City 118.87 Ayala Land, Inc. 04/01/09 03/31/10 1 yr *

2 Magallanes Village

Makati City

217.43 MJ Realty Holdings, Inc.

12/01/02

11/30/12

10 yrs

3 Robinson's Place Ermita, Manila

109.00 Robinson's Land Corp

04/01/08

03/31/10

2 yrs

4 Plaza Luisita

Tarlac

200.00

Luisita Realty Corp.

05/30/00

05/29/10

10 yrs

5 Technopark

Sta Rosa, Laguna

97.00 Greenfield

Development Corp.

01/16/06

01/15/09

3 yrs

6 Katipunan Ave.

Quezon City

162.00

Eloisa Miranda

11/01/04

10/31/09

5 yrs

16

Location of Property Area Lessor Period Covered

From To Term

7 Quezon Ave. Quezon City

160.00

Maxmor Enterprises

11/01/05

10/31/10

5 yrs

8 130 Valero St., Salcedo

Vill, Makati City

121.30

Hira Holdings, Inc.

03/01/06

02/27/11

5 yrs

9 SM Southmall, Las Piñas

City

114.81 SM Prime Holdings, Inc.

08/01/07

07/31/09

2 yrs

10 SM Centerpoint Araneta

Ave, Q. City

96.32 SM Prime Holdings, Inc.

08/01/08

07/31/09

1 yr

11

Robinson’s Place –Pasig

45.36

Robinson's Land Corp

10/01/07

09/30/09

2 yrs

12 Ayala Center Cebu Cebu

City

87.35

Cebu Holdings, Inc.

07/07/08

10/31/10

3mos.

13 Petron-Marilao

Marilao, Bulacan

96.00

Petron Corporation

07/01/07

06/30/12

5 yrs

14 Pearl Plaza, Pearl Drive Ortigas Center, Pasig

73.90

Leonardo De Silva Umale

03/01/07

02/28/12

5 yrs

15 King’s Court – Pasong Tamo St., Makati City

90.83

King’s Development, Inc.

10/15/08

10/14/11

5 yrs

16 Caltex – South Luzon

Tollway

120.00 Caltex (Philippines),

Inc.

07/15/04

07/14/19

15 yrs

17 Malakas St., Quezon City

306.60

Happy Frens, Inc.

02/16/04

02/15/12

8 yrs

18 Market! Market, Taguig

City

110.70 Station Square East

Commercial

10/01/08

09/30/09

1 yr

19 Harborview, CCP Complex, Manila

114.84

Meedson Properties Corp.

05/15/05

05/14/10

5 yrs

20 Rockwell Center, Makati

City

102.00

Rockwell Land Corp

1/21/07

1/21/12

5 yrs

21 Gateway Center, Cubao,

Quezon City

99.50

Araneta Center, Inc.

05/01/05

04/30/10

5 yrs

22

South Supermarket, Filinvest Corp. City,

Alabang

90.00

Grand Union

Supermarket, Inc.

12/02/05

12/01/15

10 yrs

23 Missouri Cor. Connecticut,

Greenhills, San Juan

92.20

Ortigas & Co., Ltd

Partnership

09/16/05

09/15/10

5 yrs

24 Dela Rosa Carpark,

Dela Rosa St., Makati City 84

Ayala Property Management Corporation 05/01/06 04/30/09 3 yrs.

25 Petron Bel-Aire, Petron

Makati Ave. 102 Petron Corporation 03/01/06 02/28/11 5 yrs.

26 Medical City, Ortigas

Center Pasig City 160 Professional Services,

Inc. 10/01/06 09/30/11 5 yrs.

27 Pavillon Mall, Laguna 80 Lagoon Development

Corporation 11/11/06 11/11/09 3 yrs.

28 Trinoma, North EDSa

Quezon City 123.78 North Triangle Depot Commercial Center 01/19/07 04/30/09

2 yrs. & 3 mos.

29 Bonifacio High Street,

Taguig City 150 Wumaco, Inc. 09/01/07 08/31/12 5 yrs.

30

#847 Banawe, Brgy. St. Peter Sta. Mesa Heights,

Quezon City 100 Melsons Innovations

Corporation 10/01/07 09/30/12 5 yrs.

31 Cash and Carry Mall,

Makati City 63.65 Adebe Realty Company,

Inc. 11/16/07 11/15/12 5 yrs.

17

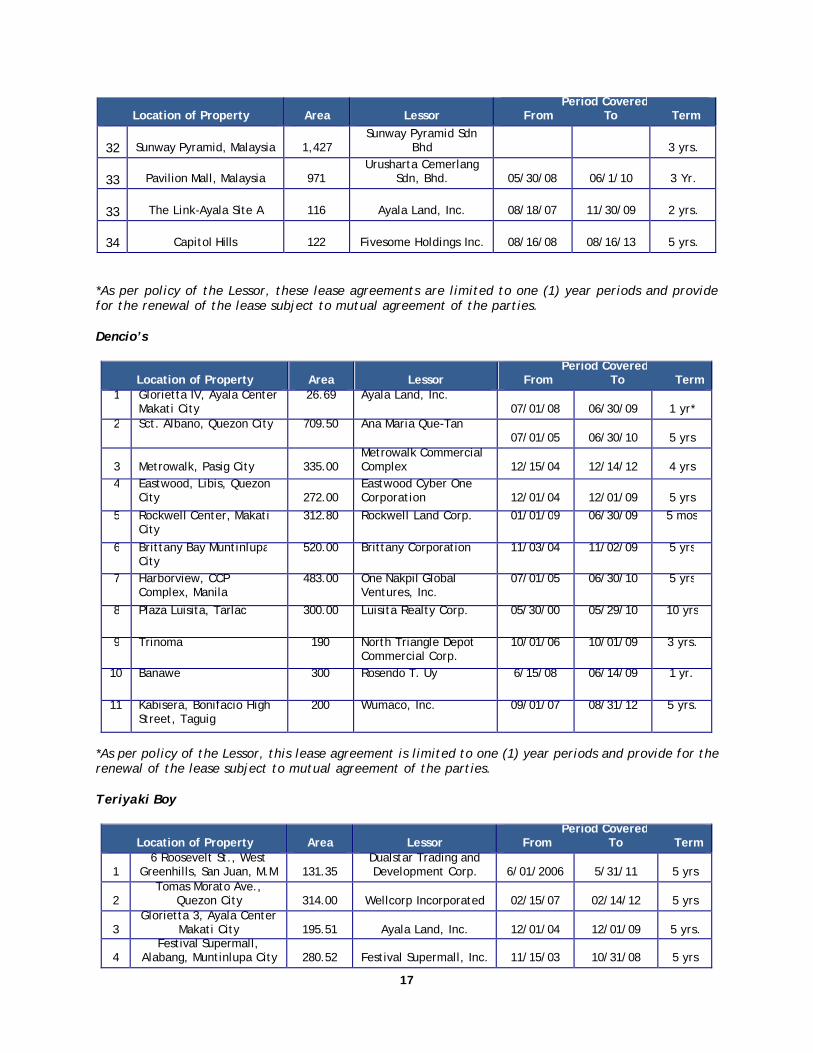

Location of Property Area Lessor Period Covered

From To Term

32 Sunway Pyramid, Malaysia 1,427 Sunway Pyramid Sdn

Bhd 3 yrs.

33 Pavilion Mall, Malaysia 971 Urusharta Cemerlang

Sdn, Bhd. 05/30/08 06/1/10 3 Yr.

33 The Link-Ayala Site A 116 Ayala Land, Inc. 08/18/07 11/30/09 2 yrs.

34 Capitol Hills 122 Fivesome Holdings Inc. 08/16/08 08/16/13 5 yrs. *As per policy of the Lessor, these lease agreements are limited to one (1) year periods and provide for the renewal of the lease subject to mutual agreement of the parties.

Dencio’s

Location of Property Area Lessor Period Covered

From To Term 1 Glorietta IV, Ayala Center

Makati City 26.69 Ayala Land, Inc.

07/01/08

06/30/09

1 yr* 2 Sct. Albano, Quezon City 709.50 Ana Maria Que-Tan

07/01/05

06/30/10

5 yrs 3

Metrowalk, Pasig City

335.00

Metrowalk Commercial Complex

12/15/04

12/14/12

4 yrs

4 Eastwood, Libis, Quezon City

272.00

Eastwood Cyber One Corporation

12/01/04

12/01/09

5 yrs

5 Rockwell Center, Makati City

312.80 Rockwell Land Corp. 01/01/09 06/30/09 5 mos

6 Brittany Bay Muntinlupa City

520.00 Brittany Corporation 11/03/04 11/02/09 5 yrs

7 Harborview, CCP Complex, Manila

483.00 One Nakpil Global Ventures, Inc.

07/01/05 06/30/10 5 yrs

8 Plaza Luisita, Tarlac 300.00 Luisita Realty Corp. 05/30/00 05/29/10 10 yrs

9 Trinoma 190 North Triangle Depot Commercial Corp.

10/01/06 10/01/09 3 yrs.

10 Banawe 300 Rosendo T. Uy 6/15/08 06/14/09 1 yr.

11 Kabisera, Bonifacio High Street, Taguig

200 Wumaco, Inc. 09/01/07 08/31/12 5 yrs.

*As per policy of the Lessor, this lease agreement is limited to one (1) year periods and provide for the renewal of the lease subject to mutual agreement of the parties.

Teriyaki Boy

Location of Property Area Lessor Period Covered

From To Term

1 6 Roosevelt St., West

Greenhills, San Juan, M.M

131.35 Dualstar Trading and Development Corp.

6/01/2006

5/31/11

5 yrs

2 Tomas Morato Ave.,

Quezon City

314.00 Wellcorp Incorporated

02/15/07

02/14/12

5 yrs

3 Glorietta 3, Ayala Center

Makati City

195.51

Ayala Land, Inc.

12/01/04

12/01/09

5 yrs.

4 Festival Supermall,

Alabang, Muntinlupa City

280.52

Festival Supermall, Inc.

11/15/03

10/31/08

5 yrs

18

Location of Property Area Lessor Period Covered

From To Term

5

SM City, Baguio

196.21 SM Primeholdings, Inc.

11/1/06

10/31/09

3 yrs

6

SM Megamall, Ortigas

198.82 First Asia Realty Dev’t.

Corp

10/23/08

10/31/11

3 yrs

7 Market! Market, Taguig

City 154.86 Station Square East

Commercial 10/01/08 09/30/09 1 yr *

8 Eastwood, Libis, Quezon

City

476.30 Eastwood Cyberzone

Corp.

03/01/05

02/28/10

5 yrs

9 Gateway Center, Cubao,

Quezon City

164.00

Araneta Center, Inc.

05/01/05

04/30/10

5 yrs

10 Petron Makati Ave.,

Makati City 241.00 Petron Marketing Corp. 11/01/05 10/31/10 5 yrs

11 SM North EDSA, Quezon

City

159.84

SM Primeholdings, Inc.

7/29/06

10/31/09

3 yrs. & 3

mos.

12 Katipunan, Quezon City

140.00

Palodoma, Inc.

6/15/06

4/14/14

7 yrs. & 10 mos.

13 Robinsons Galleria,

Quezon City

223.75 Robinsons Land

Corporation

10/15/08

10/14/10

2 yrs.

14

Greenbelt, Makati City

157.8

Ayala Land, Inc.

04/01/08

3/31/09

1 yr

15 Robinson’s Ermita, Manila

119.93 Robinsons Land

Corporation

9/13/08

9/12/10

2 yrs.

16 Petron, Marilao Bulacan 140.00 Petron Corporation 6/1/06 5/31/11 5 yrs.

17

Dela Rosa Carpark

130.00 Ayala Property Mgt.

Corporation

5/1/06

4/30/10

4 yrs.

18

Harbour View, CCP

138.25 Meedson Properties

Corporation

3/1/06

2/28/11

5 yrs.

19

Paseo Center

134.00 Megaworld Corporation

3/15/06

3/31/09

3 yrs.

20

South Supermarket

168.59 Grand Union

Supermarket, Inc.

12/2/05

12/1/15

10 yrs.

21 Tagaytay City 250.00 Miguel Barreto 6/15/06 9/01/16 10 yrs

22 Trinoma, North Edsa

Quezon City 175.87 North Triangle Depot

Commercial Corp. 10/01/06 03/31/09 3 yrs.

23 Santana Grove, Sucat

Road, Parañaque 180 Suparana Holdings, Inc. 04/01/07 03/01/12 5 yrs.

24 Cash & Carry Mall, Makati

City 192.64 Adebe Realty Company,

Inc. 11/16/07 11/15/12 5 yrs. 25

223 Oranbo Drive, Brgy Oranbo, Pasig City

1,130.00

Mariano C. Tiu

11/01/05

10/31/10

5 yrs

26 Ayala Cebu, Cebu City 130.16 Cebu Holdings Inc. 10/31/09 10/31/10 1 Yr

*As per policy of the Lessor, this lease agreement is limited to one (1) year periods and provide for the renewal of the lease subject to mutual agreement of the parties.

19

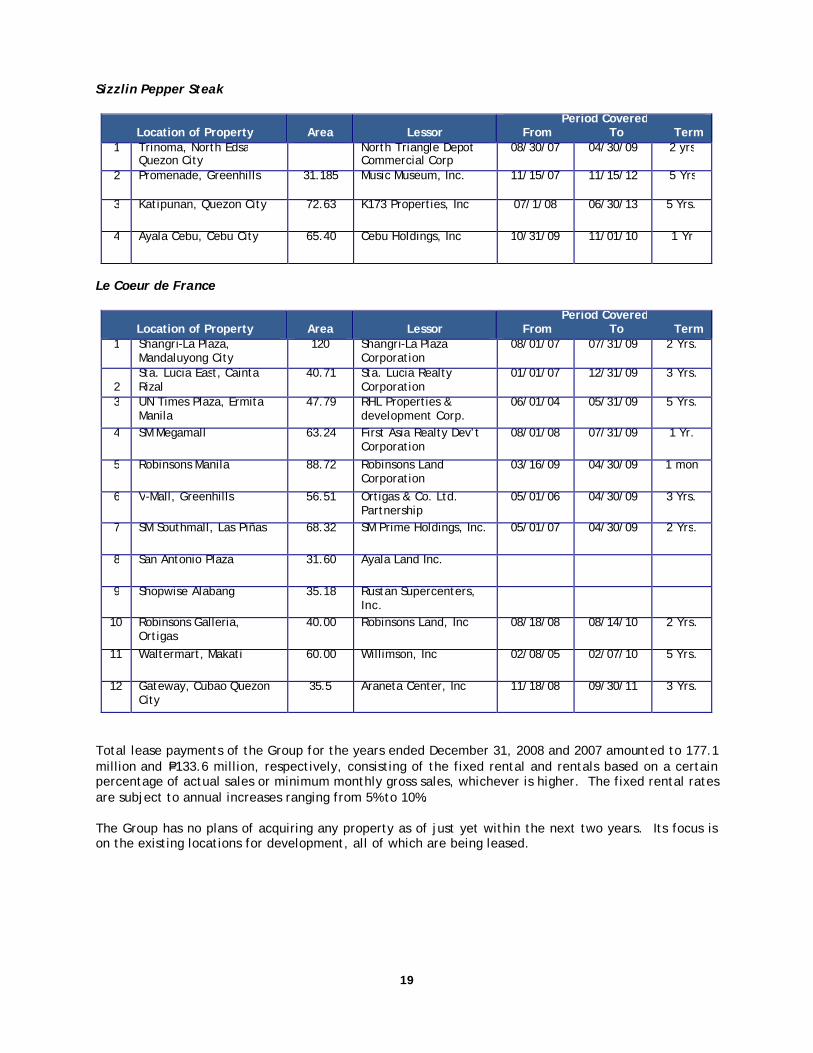

Sizzlin Pepper Steak

Location of Property Area Lessor Period Covered

From To Term 1 Trinoma, North Edsa

Quezon City North Triangle Depot

Commercial Corp 08/30/07 04/30/09 2 yrs

2

Promenade, Greenhills 31.185 Music Museum, Inc. 11/15/07 11/15/12 5 Yrs

3 Katipunan, Quezon City 72.63 K173 Properties, Inc 07/1/08 06/30/13 5 Yrs.

4 Ayala Cebu, Cebu City 65.40 Cebu Holdings, Inc 10/31/09 11/01/10 1 Yr

Le Coeur de France

Location of Property Area Lessor Period Covered

From To Term 1

Shangri-La Plaza, Mandaluyong City

120 Shangri-La Plaza Corporation

08/01/07 07/31/09 2 Yrs.

2

Sta. Lucia East, Cainta Rizal

40.71 Sta. Lucia Realty Corporation

01/01/07 12/31/09 3 Yrs.

3 UN Times Plaza, Ermita Manila

47.79 RHL Properties & development Corp.

06/01/04 05/31/09 5 Yrs.

4 SM Megamall 63.24 First Asia Realty Dev’t Corporation

08/01/08 07/31/09 1 Yr.

5 Robinsons Manila 88.72 Robinsons Land Corporation

03/16/09 04/30/09 1 mon

6 V-Mall, Greenhills 56.51 Ortigas & Co. Ltd. Partnership

05/01/06 04/30/09 3 Yrs.

7 SM Southmall, Las Piñas 68.32 SM Prime Holdings, Inc. 05/01/07 04/30/09 2 Yrs.

8 San Antonio Plaza 31.60 Ayala Land Inc.

9 Shopwise Alabang 35.18 Rustan Supercenters, Inc.

10 Robinsons Galleria, Ortigas

40.00 Robinsons Land, Inc 08/18/08 08/14/10 2 Yrs.

11 Waltermart, Makati 60.00 Willimson, Inc 02/08/05 02/07/10 5 Yrs.

12 Gateway, Cubao Quezon City

35.5 Araneta Center, Inc 11/18/08 09/30/11 3 Yrs.

Total lease payments of the Group for the years ended December 31, 2008 and 2007 amounted to 177.1 million and P=133.6 million, respectively, consisting of the fixed rental and rentals based on a certain percentage of actual sales or minimum monthly gross sales, whichever is higher. The fixed rental rates are subject to annual increases ranging from 5% to 10%. The Group has no plans of acquiring any property as of just yet within the next two years. Its focus is on the existing locations for development, all of which are being leased.

20

Item 3. Legal Proceeding

To the best of the knowledge of Management, the Company is not aware of: (a) any bankruptcy petition filed by or against any business of which they are incumbent directors or

senior officers, was a general partner or executive officer either at the time of bankruptcy or within two (2) years prior to that time;

(b) any conviction by final judgment in criminal proceeding, domestic or foreign, pending against any

of the incumbent directors or officers; (c) any order, judgment, or decree, not subsequently reversed, suspended or vacated, of any court

competent jurisdiction, domestic or foreign, permanently or temporarily enjoining, barring, suspending or otherwise limiting the involvement of any of the incumbent directors or executive officers in any type of business, securities, commodities or banking activities; and,

(d) any finding by or domestic or foreign court competent jurisdiction (in civil action), the SEC or

comparable foreign body, or domestic or foreign exchange or electronic marketplace or said regulatory organization, that any of the incumbent directors or executive officers has violated a securities or commodities law, and the judgment has not been reversed, suspended or vacated which may have a material effect in the operation and deter, bar or impede the fulfillment of his/her duties as a director or executive of the Company.

The Company, PH Ventures, Inc. (“PHVI”) and Mr. Martin P. Lorenzo, in his capacity as President of the two companies, were named defendants in a civil case filed in October 2002 by Kenmor Corporation (Kenmor) and Emmanuel B. Moran, Jr. (the joint venture partner of PHVI in Kenmor) for the collection of sum of money and damages in the aggregate amount of PHP 9,820,701.82. The plaintiffs alleged, among others, that PHVI did not put in its required capital contribution in Kenmor. The Pancake House – Libis outlet, which is owned and operated by Kenmor, closed down in June 2002 due to its lack of financial performance. On January 31, 2008, a complaint was filed by FILSCAP (Filipino Society of Composers, Authors and Publishers, Inc.) against Dencio’s Food Specialist, Inc. for failure to pay music royalties amounting to PHP485,140 for the Year 2007 and 2008. The case was turned over to PECABAR Law Offices for due process. Management and its legal counsel believe that no provision needs to be made in the accounts since the case above are projected to be ruled in favor of the Company and its materiality is not yet determinable and it is impracticable to make a reliable estimate.

Item 4. Submission of Matters to a Vote of Security Holders (not applicable)

PART II – OPERATIONAL AND FINANCIAL INFORMATION

Item 5. Market for Issuer's Common Equity and Related Stockholder Matters

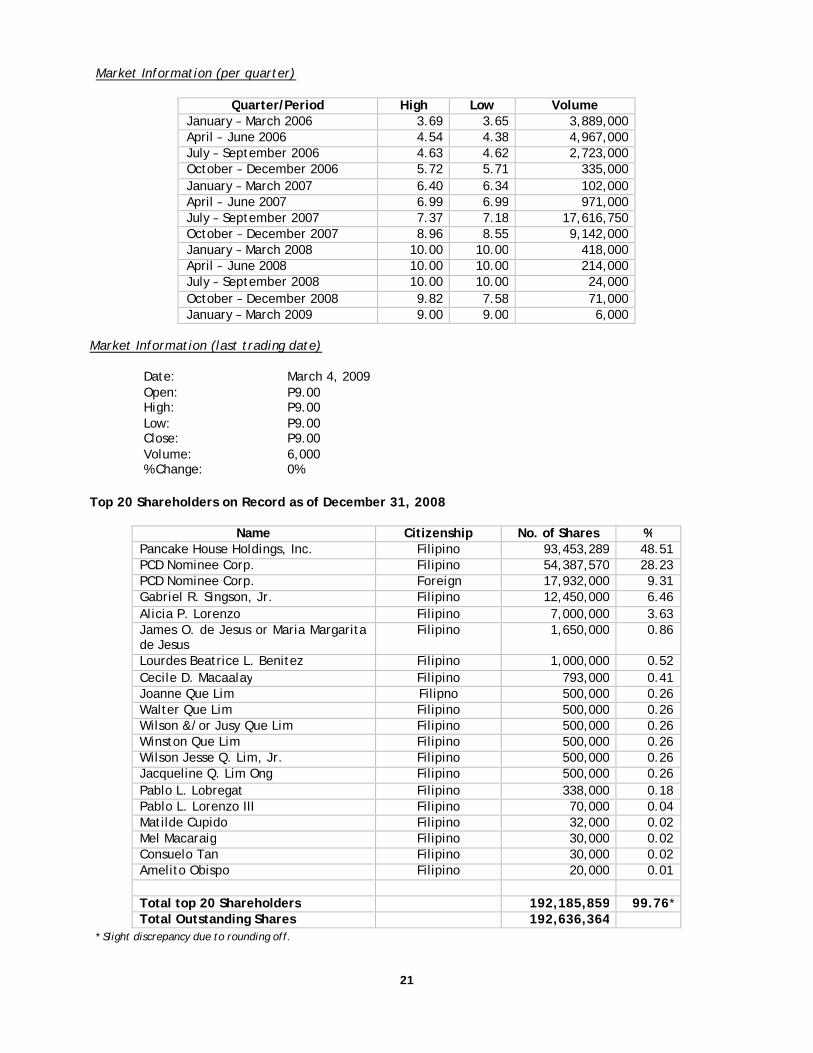

Market Information The Pancake House, Inc. Common Shares were listed in the Philippine Stock Exchange on December 15, 2000. Currently, it is being traded under the ticker “PCKH”. The trading record of the Company since it listed is as follows:

21

Market Information (per quarter)

Quarter/Period High Low Volume January – March 2006 3.69 3.65 3,889,000 April – June 2006 4.54 4.38 4,967,000 July – September 2006 4.63 4.62 2,723,000 October – December 2006 5.72 5.71 335,000 January – March 2007 6.40 6.34 102,000 April – June 2007 6.99 6.99 971,000 July – September 2007 7.37 7.18 17,616,750 October – December 2007 8.96 8.55 9,142,000 January – March 2008 10.00 10.00 418,000 April – June 2008 10.00 10.00 214,000 July – September 2008 10.00 10.00 24,000 October – December 2008 9.82 7.58 71,000 January – March 2009 9.00 9.00 6,000

Market Information (last trading date)

Date: March 4, 2009 Open: P9.00 High: P9.00 Low: P9.00 Close: P9.00 Volume: 6,000 % Change: 0%

Top 20 Shareholders on Record as of December 31, 2008

Name Citizenship No. of Shares %

Pancake House Holdings, Inc. Filipino 93,453,289 48.51 PCD Nominee Corp. Filipino 54,387,570 28.23 PCD Nominee Corp. Foreign 17,932,000 9.31 Gabriel R. Singson, Jr. Filipino 12,450,000 6.46 Alicia P. Lorenzo Filipino 7,000,000 3.63 James O. de Jesus or Maria Margarita de Jesus

Filipino 1,650,000 0.86

Lourdes Beatrice L. Benitez Filipino 1,000,000 0.52 Cecile D. Macaalay Filipino 793,000 0.41 Joanne Que Lim Filipno 500,000 0.26 Walter Que Lim Filipino 500,000 0.26 Wilson &/or Jusy Que Lim Filipino 500,000 0.26 Winston Que Lim Filipino 500,000 0.26 Wilson Jesse Q. Lim, Jr. Filipino 500,000 0.26 Jacqueline Q. Lim Ong Filipino 500,000 0.26 Pablo L. Lobregat Filipino 338,000 0.18 Pablo L. Lorenzo III Filipino 70,000 0.04 Matilde Cupido Filipino 32,000 0.02 Mel Macaraig Filipino 30,000 0.02 Consuelo Tan Filipino 30,000 0.02 Amelito Obispo Filipino 20,000 0.01 Total top 20 Shareholders 192,185,859 99.76* Total Outstanding Shares 192,636,364

* Slight discrepancy due to rounding off.

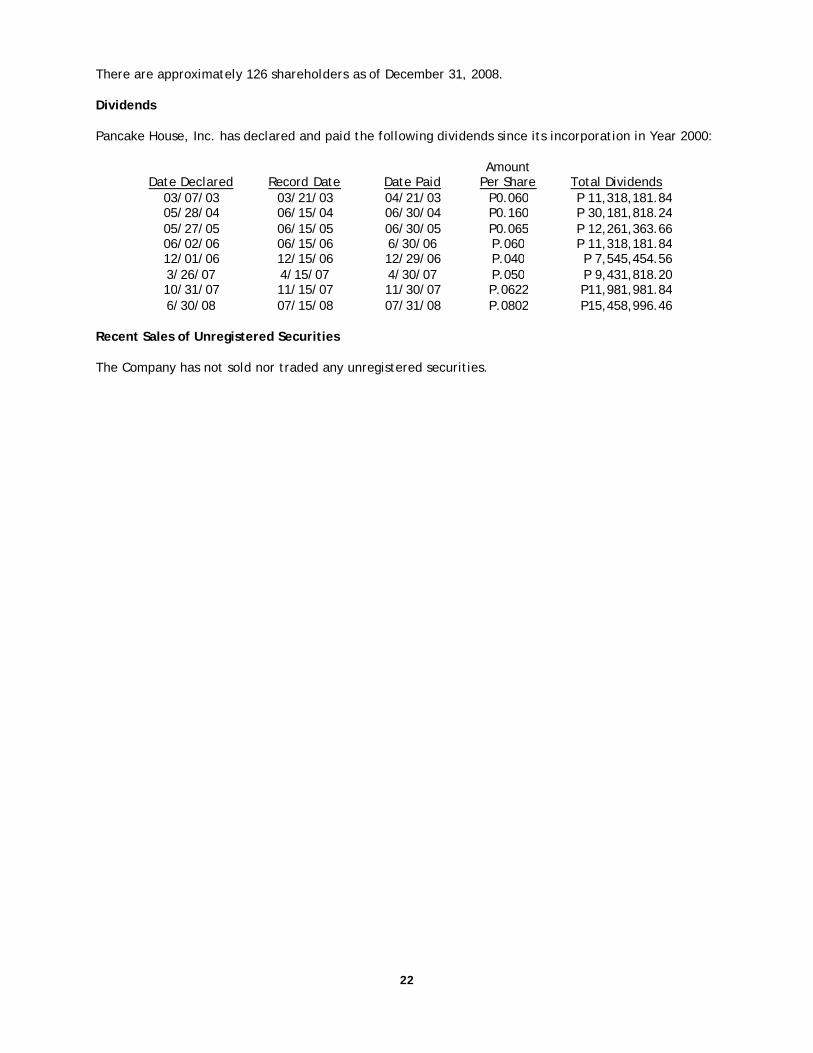

22

There are approximately 126 shareholders as of December 31, 2008.

Dividends

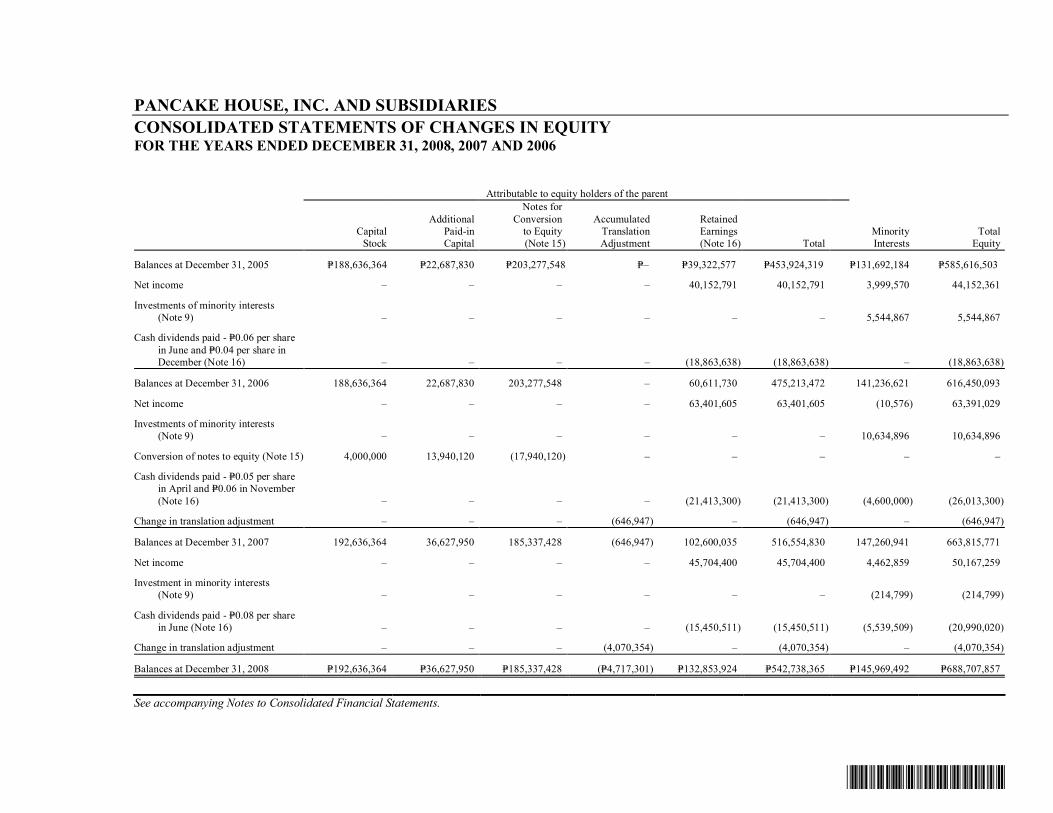

Pancake House, Inc. has declared and paid the following dividends since its incorporation in Year 2000:

Date Declared

Record Date

Date Paid

Amount Per Share

Total Dividends

03/07/03 03/21/03 04/21/03 P0.060 P 11,318,181.84 05/28/04 06/15/04 06/30/04 P0.160 P 30,181,818.24 05/27/05 06/15/05 06/30/05 P0.065 P 12,261,363.66 06/02/06 06/15/06 6/30/06 P.060 P 11,318,181.84 12/01/06 12/15/06 12/29/06 P.040 P 7,545,454.56 3/26/07 4/15/07 4/30/07 P.050 P 9,431,818.20 10/31/07 11/15/07 11/30/07 P.0622 P11,981,981.84 6/30/08 07/15/08 07/31/08 P.0802 P15,458,996.46

Recent Sales of Unregistered Securities The Company has not sold nor traded any unregistered securities.

23

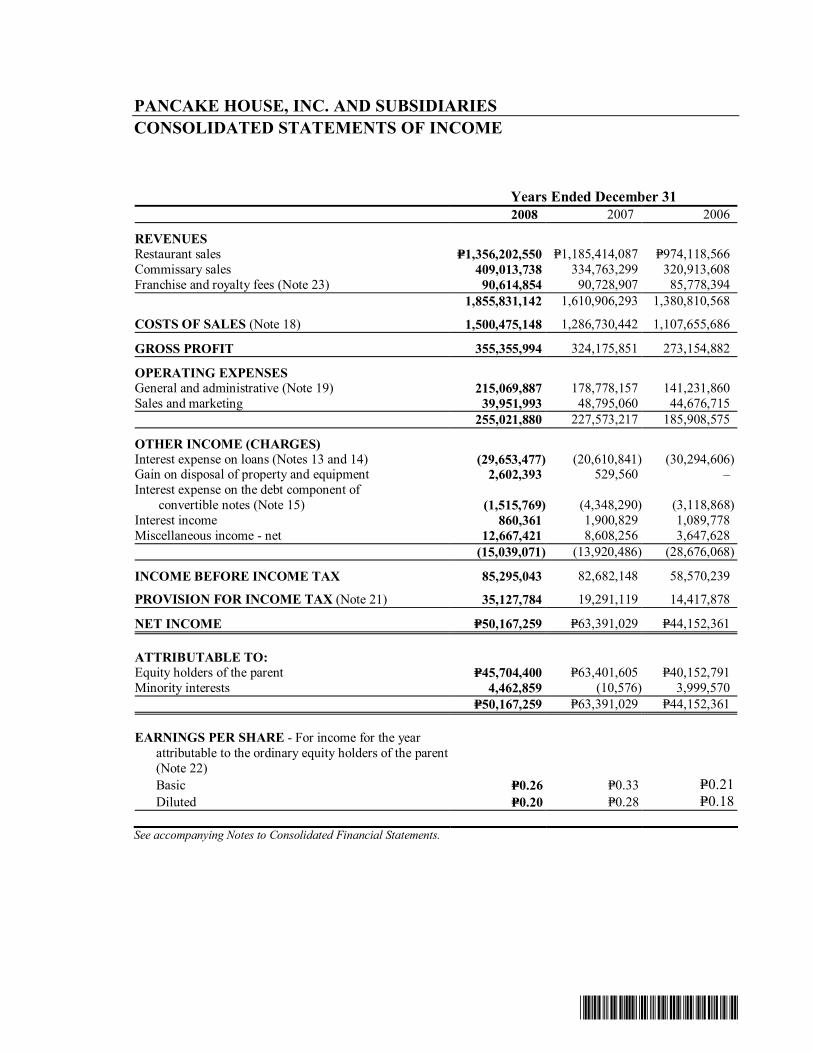

ITEM 6. MANAGEMENT'S DISCUSSION AND ANALYSIS OR PLAN OF OPERATION EXECUTIVE SUMMARY Pancake House, Inc. focuses on reliability and stability for the year 2008. With the expected decrease in consumer spending coupled with challenging business climate as a result of the current worldwide economic slowdown, the Company successfully upheld the continuous increase in EBITDA and Consolidated Revenues. Despite the contraction in business activity, PHI continued to sustain the upward trend of its EBITDA with an increase of 8.5% to P290.7 million (P252.4 million attributable to equity holders of the Parent) from P267.9 million (P234.2 million attributable to equity holders of the Parent) in 2007. Consolidated revenues increased by 15.2% to P1,855.8 million this year from P1,610.9 million last year. Restaurant sales of P1,356.2 million increased by 14.4% from last year’s P1,185.4 million. The increase in revenues was a result of the Company’s disciplined expansion program through the opening of new company-owned outlets and purchase of performing franchised–owned locations. Furthermore, the outlets from the recently acquired subsidiary Boulangerie Francaise, Inc., operating the “Le Coeur de France” brand contributed to the revenue upswing. Meanwhile, commissary sales rose by 22.2% to P409 million from P334.8 million in 2007; while franchise income remained the same at P91 million for both the years 2008 and 2007. On the other hand, while cost saving measures had been challenging in an ever rising operating cost environment, the Company managed to maintain its Cost of Sales at 40.6% this year with a slight increase of only 0.4% from last year’s 39.6% of revenues. Furthermore, Labor efficiency increased resulting to a lower Cost of Labor at 13.8% from last year’s 16.2% of revenues. The Company maintained a healthy Income from Operations which remained the same for the last 2 years at 6% of revenues. The Group’s consolidated net income for the year 2008 at P50.2 million (P45.7 million attributable to equity holders of the Parent) decreased by 20.8% from P63.39 million (P63.4 million attributable to equity holders of the Parent) due to the interest from short-term loans incurred to acquire the ‘Le Coeur de France” brand. Although the Company initially planned to raise equity or secure a long term facility to finance the acquisition, the economic condition in 2008 delayed such fund raising activity. Furthermore, the Company’s compliance with the current tax rates and laws caused the reversals of Deferred Tax Assets resulted to non-cash accounting entries which affected the bottom line financial performance.

24

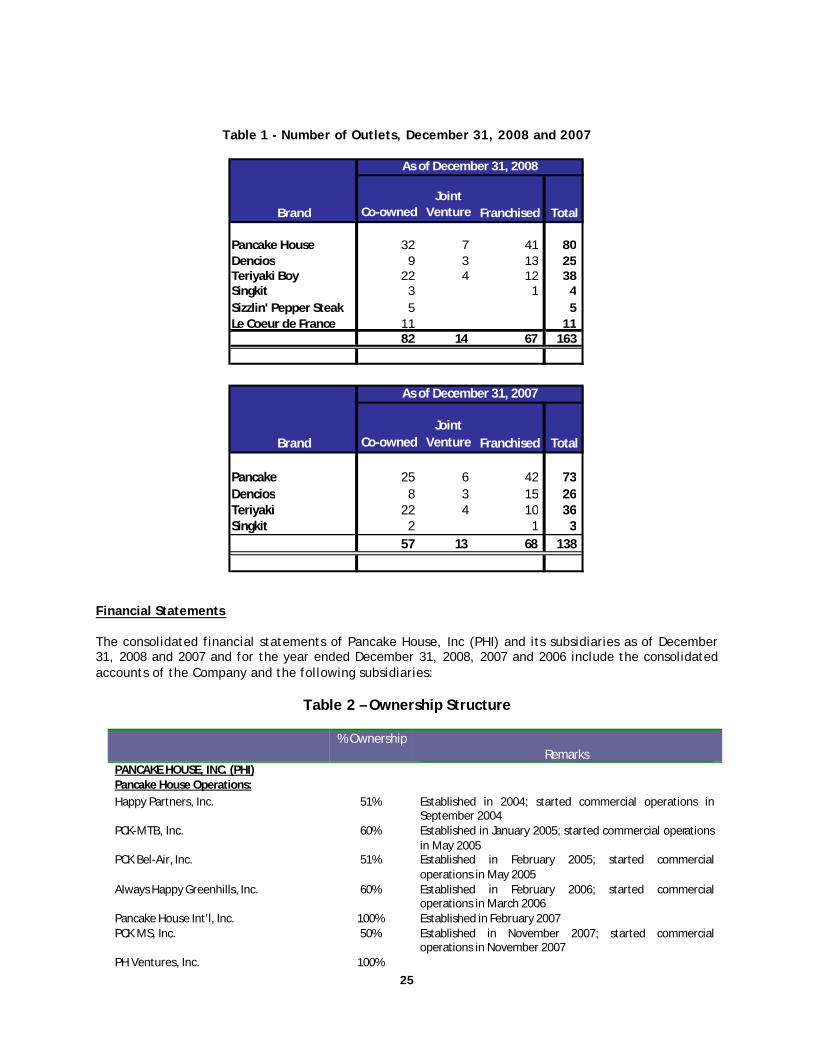

Developments in 2008 Going global. Included in the continuing strategies of the Pancake House Group is to bring its brands to the mainstream international market. The Group identified Malaysia as its gateway into the Asian consumer market to initially introduce the brand “Pancake House International”. Through its international affiliate, Pancake House, International Malaysia Sdn Bhd (a wholly-owned subsidiary of Pancake House International, Inc.), it now currently operates 2 outlets in Malaysia serving menu items that cater specifically to the Malaysian taste profile while upholding the brand’s vision of quality product and service that guarantees a distinct gratifying and delightful dining experience. Acquisition of Le Coeur de France. On February 8, 2008, the Company acquired 100% of the outstanding and issued capital stock of Boulangerie Francaise, Inc. (“BFI”), the exclusive franchisee of the Le Coeur de France brand name and system-wide restaurant operations in the Philippines. Inclusive in PHI’s acquisition is BFI’s operating assets, including 13 company-owned outlets and one commissary. On the same date, Pancake House International, Inc., a wholly owned subsidiary of the Company established as the vehicle for its international franchising business, purchased the trademark “Le Coeur de France” and all of its related intellectual property rights from the trademark owner, Baratow Limited, a British Virgin Island company. Innovation. The Pancake House Group recently developed an upscale Filipino brand “Kabisera” to address the market’s need for higher-end Filipino restaurants. This is to further complement the popular bar and grill concept under the group called “Dencio’s” as an alternative despite both brands catering to the same market segment. The restaurant features new menu items developed by popular and well established chefs and such dishes consequently carry the chef’s identities. Merger between PHI and DFSI On July 26, 2007, the Securities and Exchange Commission approved the merger between Pancake House, Inc. (PHI) and its wholly-owned subsidiary, Dencios Food Specialists, Inc. (DFSI). Under the Plan of Merger, DFSI shall be merged into PHI, and DFSI’s corporate existence shall cease by operation of law upon the effective Date of Merger which shall be August 1, 2007 with PHI as the surviving company. The merger was accounted for similar to a pooling of interests and accordingly, all financial data of PHI for the periods prior to the merger have been restated to include the results of DFSI. Also, the results of operations for the period ended September 30, 2008 are reported as though PHI and DFSI had been combined as of the beginning of the period. On March 28, 2008, the Bureau of Internal Revenue (BIR) approved the application for a “tax free merger” within the meaning of Sections 40(C)(2)(a) and (b) and 40(6)(b) of the 1997 Tax Code, as amended. Consequently, no gain or loss was recognized by DFSI, as the transferor, on the transfer of all its assets and liabilities to the Company pursuant to the Plan of Merger. Likewise, no gain or loss was recognized by PHI, as the transferee, on its receipt of the assets and liabilities of DFSI without issuing stocks in exchange therefore. Steady Growth. The Group had a total of 163 outlets as of December 31, 2008 and 138 outlets as of December 31, 2007, broken down as follows:

25

Table 1 - Number of Outlets, December 31, 2008 and 2007

Brand Co-ownedJoint

Venture Franchised Total

Pancake House 32 7 41 80 Dencios 9 3 13 25 Teriyaki Boy 22 4 12 38 Singkit 3 1 4 Sizzlin' Pepper Steak 5 5 Le Coeur de France 11 11

82 14 67 163

As of December 31, 2008

Brand Co-ownedJoint

Venture Franchised Total

Pancake 25 6 42 73 Dencios 8 3 15 26 Teriyaki 22 4 10 36 Singkit 2 1 3

57 13 68 138

As of December 31, 2007

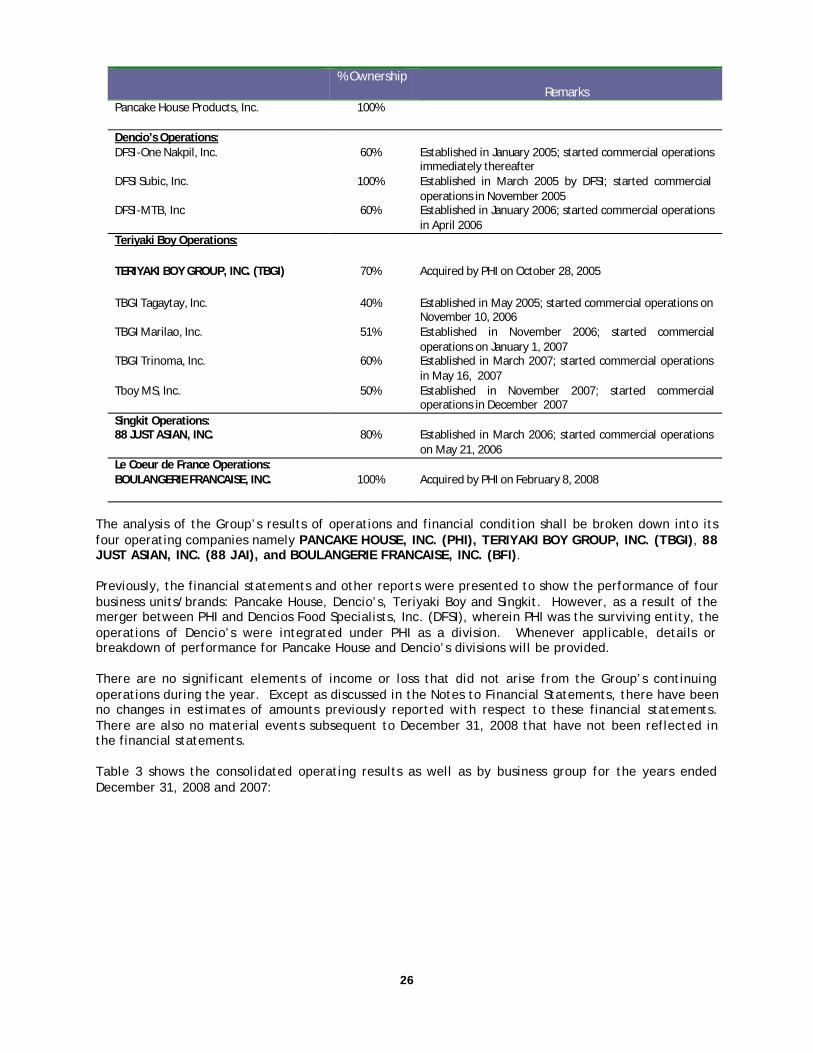

Financial Statements The consolidated financial statements of Pancake House, Inc (PHI) and its subsidiaries as of December 31, 2008 and 2007 and for the year ended December 31, 2008, 2007 and 2006 include the consolidated accounts of the Company and the following subsidiaries:

Table 2 – Ownership Structure

% Ownership

Remarks PANCAKE HOUSE, INC. (PHI) Pancake House Operations: Happy Partners, Inc. 51% Established in 2004; started commercial operations in

September 2004 PCK-MTB, Inc. 60% Established in January 2005; started commercial operations

in May 2005 PCK Bel-Air, Inc. 51% Established in February 2005; started commercial

operations in May 2005 Always Happy Greenhills, Inc. 60% Established in February 2006; started commercial

operations in March 2006 Pancake House Int’l, Inc. 100% Established in February 2007 PCK MS, Inc. 50% Established in November 2007; started commercial

operations in November 2007 PH Ventures, Inc. 100%

26

% Ownership Remarks

Pancake House Products, Inc.

100%

Dencio’s Operations: DFSI-One Nakpil, Inc. 60% Established in January 2005; started commercial operations

immediately thereafter DFSI Subic, Inc. 100% Established in March 2005 by DFSI; started commercial

operations in November 2005 DFSI-MTB, Inc 60% Established in January 2006; started commercial operations

in April 2006 Teriyaki Boy Operations:

TERIYAKI BOY GROUP, INC. (TBGI) 70% Acquired by PHI on October 28, 2005

TBGI Tagaytay, Inc. 40%

Established in May 2005; started commercial operations on November 10, 2006

TBGI Marilao, Inc. 51% Established in November 2006; started commercial operations on January 1, 2007

TBGI Trinoma, Inc. 60% Established in March 2007; started commercial operations in May 16, 2007

Tboy MS, Inc. 50% Established in November 2007; started commercial operations in December 2007

Singkit Operations: 88 JUST ASIAN, INC.

80%

Established in March 2006; started commercial operations on May 21, 2006

Le Coeur de France Operations: BOULANGERIE FRANCAISE, INC.

100%

Acquired by PHI on February 8, 2008

The analysis of the Group’s results of operations and financial condition shall be broken down into its four operating companies namely PANCAKE HOUSE, INC. (PHI), TERIYAKI BOY GROUP, INC. (TBGI), 88 JUST ASIAN, INC. (88 JAI), and BOULANGERIE FRANCAISE, INC. (BFI). Previously, the financial statements and other reports were presented to show the performance of four business units/brands: Pancake House, Dencio’s, Teriyaki Boy and Singkit. However, as a result of the merger between PHI and Dencios Food Specialists, Inc. (DFSI), wherein PHI was the surviving entity, the operations of Dencio’s were integrated under PHI as a division. Whenever applicable, details or breakdown of performance for Pancake House and Dencio’s divisions will be provided. There are no significant elements of income or loss that did not arise from the Group’s continuing operations during the year. Except as discussed in the Notes to Financial Statements, there have been no changes in estimates of amounts previously reported with respect to these financial statements. There are also no material events subsequent to December 31, 2008 that have not been reflected in the financial statements. Table 3 shows the consolidated operating results as well as by business group for the years ended December 31, 2008 and 2007:

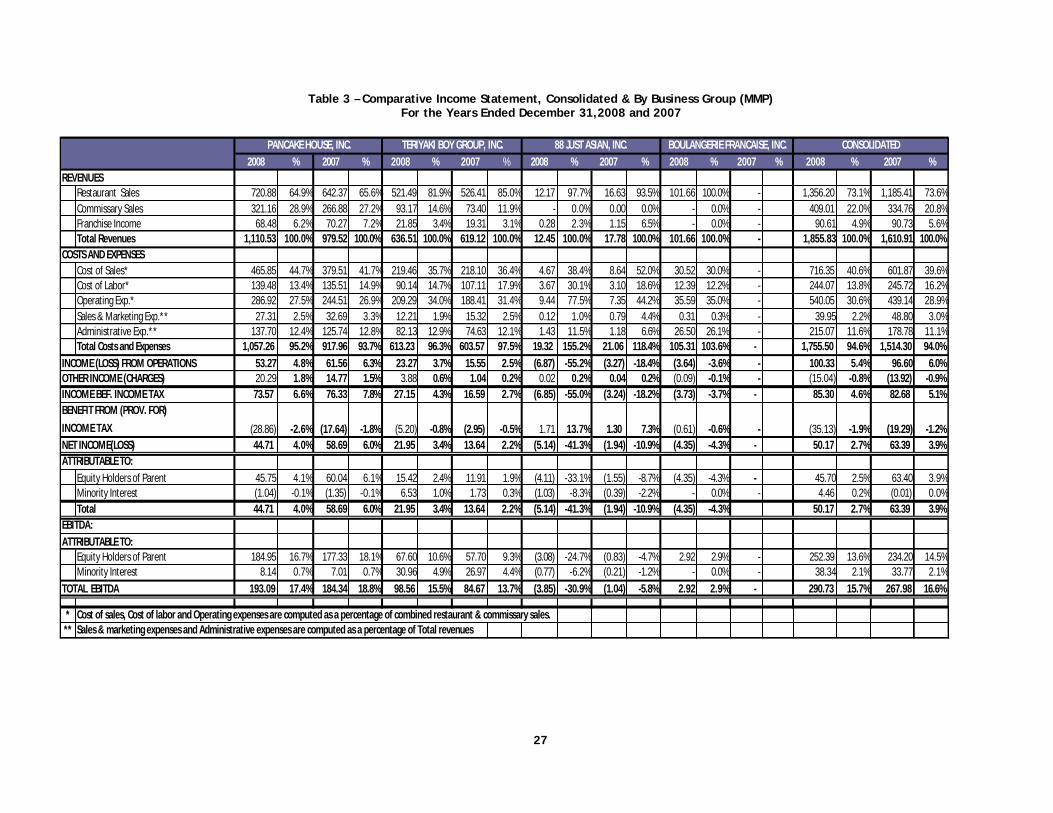

27

Table 3 – Comparative Income Statement, Consolidated & By Business Group (MMP) For the Years Ended December 31,2008 and 2007

2008 % 2007 % 2008 % 2007 % 2008 % 2007 % 2008 % 2007 % 2008 % 2007 %

Restaurant Sales 720.88 64.9% 642.37 65.6% 521.49 81.9% 526.41 85.0% 12.17 97.7% 16.63 93.5% 101.66 100.0% - 1,356.20 73.1% 1,185.41 73.6%Commissary Sales 321.16 28.9% 266.88 27.2% 93.17 14.6% 73.40 11.9% - 0.0% 0.00 0.0% - 0.0% - 409.01 22.0% 334.76 20.8%Franchise Income 68.48 6.2% 70.27 7.2% 21.85 3.4% 19.31 3.1% 0.28 2.3% 1.15 6.5% - 0.0% - 90.61 4.9% 90.73 5.6%Total Revenues 1,110.53 100.0% 979.52 100.0% 636.51 100.0% 619.12 100.0% 12.45 100.0% 17.78 100.0% 101.66 100.0% - 1,855.83 100.0% 1,610.91 100.0%

Cost of Sales* 465.85 44.7% 379.51 41.7% 219.46 35.7% 218.10 36.4% 4.67 38.4% 8.64 52.0% 30.52 30.0% - 716.35 40.6% 601.87 39.6%Cost of Labor* 139.48 13.4% 135.51 14.9% 90.14 14.7% 107.11 17.9% 3.67 30.1% 3.10 18.6% 12.39 12.2% - 244.07 13.8% 245.72 16.2%Operating Exp.* 286.92 27.5% 244.51 26.9% 209.29 34.0% 188.41 31.4% 9.44 77.5% 7.35 44.2% 35.59 35.0% - 540.05 30.6% 439.14 28.9%Sales & Marketing Exp.** 27.31 2.5% 32.69 3.3% 12.21 1.9% 15.32 2.5% 0.12 1.0% 0.79 4.4% 0.31 0.3% - 39.95 2.2% 48.80 3.0%Administrative Exp.** 137.70 12.4% 125.74 12.8% 82.13 12.9% 74.63 12.1% 1.43 11.5% 1.18 6.6% 26.50 26.1% - 215.07 11.6% 178.78 11.1%Total Costs and Expenses 1,057.26 95.2% 917.96 93.7% 613.23 96.3% 603.57 97.5% 19.32 155.2% 21.06 118.4% 105.31 103.6% - 1,755.50 94.6% 1,514.30 94.0%

53.27 4.8% 61.56 6.3% 23.27 3.7% 15.55 2.5% (6.87) -55.2% (3.27) -18.4% (3.64) -3.6% - 100.33 5.4% 96.60 6.0% 20.29 1.8% 14.77 1.5% 3.88 0.6% 1.04 0.2% 0.02 0.2% 0.04 0.2% (0.09) -0.1% - (15.04) -0.8% (13.92) -0.9% 73.57 6.6% 76.33 7.8% 27.15 4.3% 16.59 2.7% (6.85) -55.0% (3.24) -18.2% (3.73) -3.7% - 85.30 4.6% 82.68 5.1%

(28.86) -2.6% (17.64) -1.8% (5.20) -0.8% (2.95) -0.5% 1.71 13.7% 1.30 7.3% (0.61) -0.6% - (35.13) -1.9% (19.29) -1.2% 44.71 4.0% 58.69 6.0% 21.95 3.4% 13.64 2.2% (5.14) -41.3% (1.94) -10.9% (4.35) -4.3% - 50.17 2.7% 63.39 3.9%

Equity Holders of Parent 45.75 4.1% 60.04 6.1% 15.42 2.4% 11.91 1.9% (4.11) -33.1% (1.55) -8.7% (4.35) -4.3% - 45.70 2.5% 63.40 3.9%Minority Interest (1.04) -0.1% (1.35) -0.1% 6.53 1.0% 1.73 0.3% (1.03) -8.3% (0.39) -2.2% - 0.0% - 4.46 0.2% (0.01) 0.0%Total 44.71 4.0% 58.69 6.0% 21.95 3.4% 13.64 2.2% (5.14) -41.3% (1.94) -10.9% (4.35) -4.3% 50.17 2.7% 63.39 3.9%

Equity Holders of Parent 184.95 16.7% 177.33 18.1% 67.60 10.6% 57.70 9.3% (3.08) -24.7% (0.83) -4.7% 2.92 2.9% - 252.39 13.6% 234.20 14.5%Minority Interest 8.14 0.7% 7.01 0.7% 30.96 4.9% 26.97 4.4% (0.77) -6.2% (0.21) -1.2% - 0.0% - 38.34 2.1% 33.77 2.1%

193.09 17.4% 184.34 18.8% 98.56 15.5% 84.67 13.7% (3.85) -30.9% (1.04) -5.8% 2.92 2.9% - 290.73 15.7% 267.98 16.6%

* Cost of sales, Cost of labor and Operating expenses are computed as a percentage of combined restaurant & commissary sales. ** Sales & marketing expenses and Administrative expenses are computed as a percentage of Total revenues

NET INCOME(LOSS)ATTRIBUTABLE TO:

EBITDA:ATTRIBUTABLE TO:

TOTAL EBITDA

REVENUES

COSTS AND EXPENSES

INCOME (LOSS) FROM OPERATIONSOTHER INCOME (CHARGES)INCOME BEF. INCOME TAXBENEFIT FROM (PROV. FOR) INCOME TAX

PANCAKE HOUSE, INC. TERIYAKI BOY GROUP, INC. 88 JUST ASIAN, INC. BOULANGERIE FRANCAISE, INC. CONSOLIDATED

27

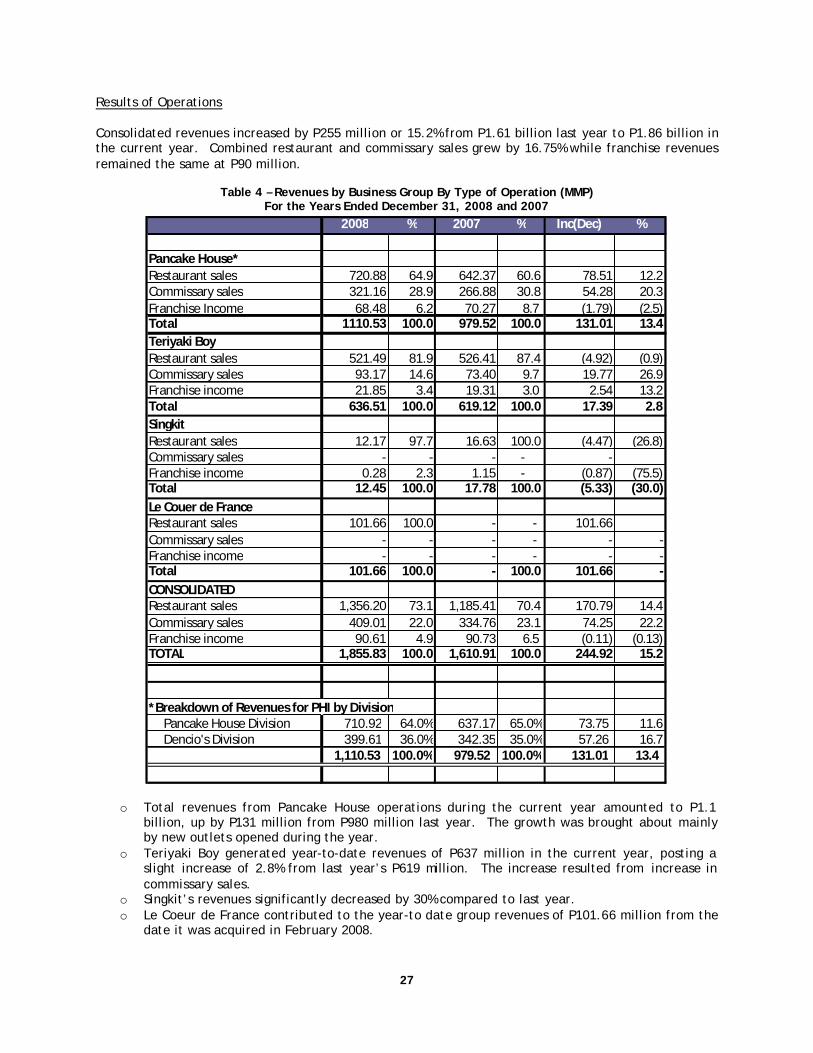

Results of Operations Consolidated revenues increased by P255 million or 15.2% from P1.61 billion last year to P1.86 billion in the current year. Combined restaurant and commissary sales grew by 16.75% while franchise revenues remained the same at P90 million.

Table 4 – Revenues by Business Group By Type of Operation (MMP) For the Years Ended December 31, 2008 and 2007

2008 % 2007 % Inc(Dec) %

Pancake House*Restaurant sales 720.88 64.9 642.37 60.6 78.51 12.2 Commissary sales 321.16 28.9 266.88 30.8 54.28 20.3 Franchise Income 68.48 6.2 70.27 8.7 (1.79) (2.5)Total 1110.53 100.0 979.52 100.0 131.01 13.4 Teriyaki BoyRestaurant sales 521.49 81.9 526.41 87.4 (4.92) (0.9)Commissary sales 93.17 14.6 73.40 9.7 19.77 26.9 Franchise income 21.85 3.4 19.31 3.0 2.54 13.2 Total 636.51 100.0 619.12 100.0 17.39 2.8 SingkitRestaurant sales 12.17 97.7 16.63 100.0 (4.47) (26.8)Commissary sales - - - - - Franchise income 0.28 2.3 1.15 - (0.87) (75.5)Total 12.45 100.0 17.78 100.0 (5.33) (30.0)Le Couer de FranceRestaurant sales 101.66 100.0 - - 101.66 Commissary sales - - - - - - Franchise income - - - - - - Total 101.66 100.0 - 100.0 101.66 - CONSOLIDATEDRestaurant sales 1,356.20 73.1 1,185.41 70.4 170.79 14.4 Commissary sales 409.01 22.0 334.76 23.1 74.25 22.2 Franchise income 90.61 4.9 90.73 6.5 (0.11) (0.13)TOTAL 1,855.83 100.0 1,610.91 100.0 244.92 15.2

*Breakdown of Revenues for PHI by Division Pancake House Division 710.92 64.0% 637.17 65.0% 73.75 11.6 Dencio's Division 399.61 36.0% 342.35 35.0% 57.26 16.7

1,110.53 100.0% 979.52 100.0% 131.01 13.4

o Total revenues from Pancake House operations during the current year amounted to P1.1 billion, up by P131 million from P980 million last year. The growth was brought about mainly by new outlets opened during the year.

o Teriyaki Boy generated year-to-date revenues of P637 million in the current year, posting a slight increase of 2.8% from last year’s P619 million. The increase resulted from increase in commissary sales.

o Singkit’s revenues significantly decreased by 30% compared to last year. o Le Coeur de France contributed to the year-to date group revenues of P101.66 million from the

date it was acquired in February 2008.

28

The Group continues to monitor closely its costs structures given the increasing costs of raw materials and supplies, rental and utility rates, and government-mandated wage hikes. Management continues to implement programs that optimize the use of the Group’s resources as well as generate savings. These include expanded synergies among the seven brands, strategic purchasing, and more efficient manning. These programs are supported by regular quality assurance and financial audits to check strict adherence to established costs and product and service quality standards.

o Combined restaurant and commissary costs of sales ratio for Pancake House operations increased to 44.7% this year from 41.7% last year, brought about by higher costs of raw materials in the current year. Meanwhile, due to better yields, the commissary’s cost of sales ratio increased only slightly despite increases in purchase costs of raw materials. Combined restaurant and commissary cost ratio of Teriyaki Boy operations slightly went down from 36.4% in 2007 to 35.7% this year. Continuous improvements in production yields have translated into lower cost ratios during the current year.

o Cost of labor slightly decreased during the year due to more efficient manning. Teriyaki Boy’s cost of labor ratio improved significantly to 14.7% this year from 17.9% last year to while Singkit’s ratio went up to 30.1% this year from 18.6% last year due to lower sales.

o Consolidated operating expenses for the year went up from P439 million to P540 million as a

result of the group’s expansion plans and opening of new outlets during the year.

o Consolidated sales and marketing expenses amounted to P40 million, 19% lower than last year’s P49 million.

o Consolidated administrative expenses for the current year were at 11.6% of gross revenues, slightly higher than the previous year’s level of 11.1%.

Consolidated other charges exceeded other income for the current year, resulting in a net Other Charges of P15 million, significantly higher than the P14 million net Other Charges recorded during the previous year. The increase is attributed to lower miscellaneous income and increase in interest expense on bank loans, net of increase in interest expense on the debt component of the convertible notes. Consolidated EBITDA (amount attributable to equity holders of the Parent) significantly improved by 8% from P234 million in 2007 to P253 million for the current year from P234 million in 2007. The Group’s performance during the year posted a net income of P45.7 million (amount attributable to equity holders of the Parent), down by 28% from last year’s P63 million.

o EBITDA improved by 4% to P185 million this year from P177 million last year. Net income for the year from combined Pancake House and Dencio’s divisions went down by 24% from P60 million last year to P46 million this year.

o Teriyaki Boy EBITDA increased by 17% to P68 million this year from P58 million last year. Meanwhile, net income is significantly higher at P15.4 million than last year’s P11.9 million.

o Singkit EBITDA went down from -P0.83 million last year to -P3.08 million this year. It incurred a net loss of P4.11 million, a significant decline compared to last year’s loss of P1.6 million.

o Le Coeur de France posted an EBITDA of P2.92 million however it incurred a net loss of P4.35 million

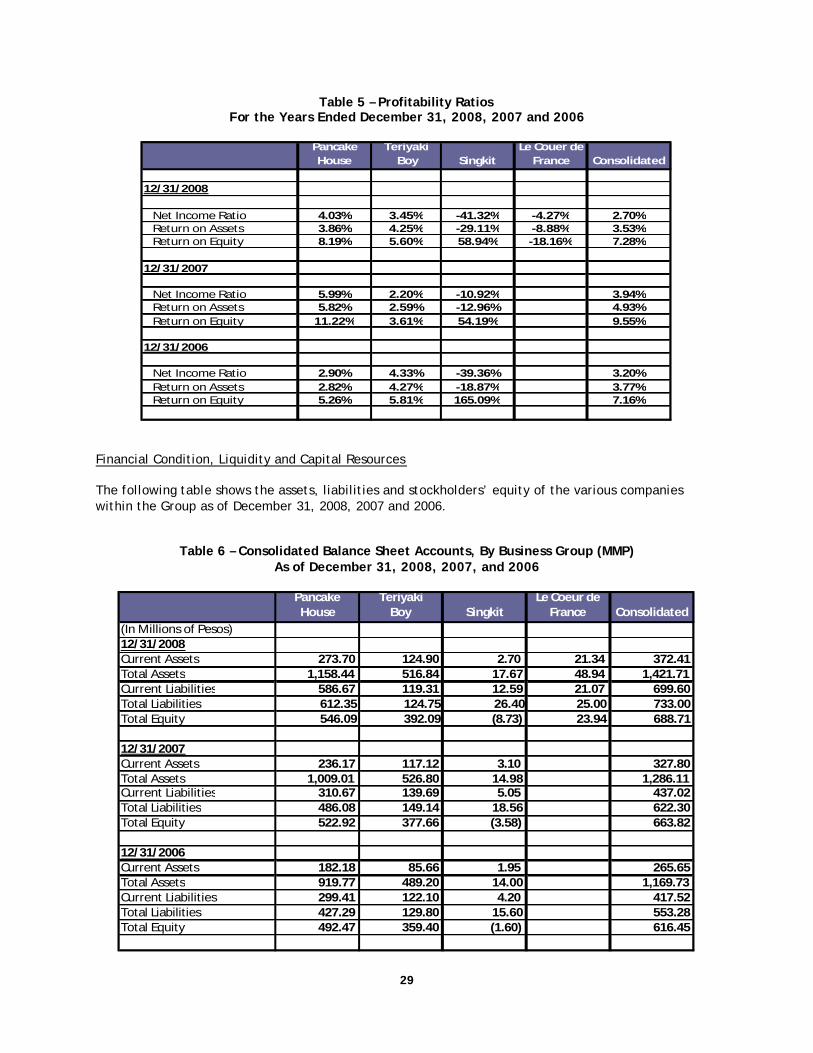

29

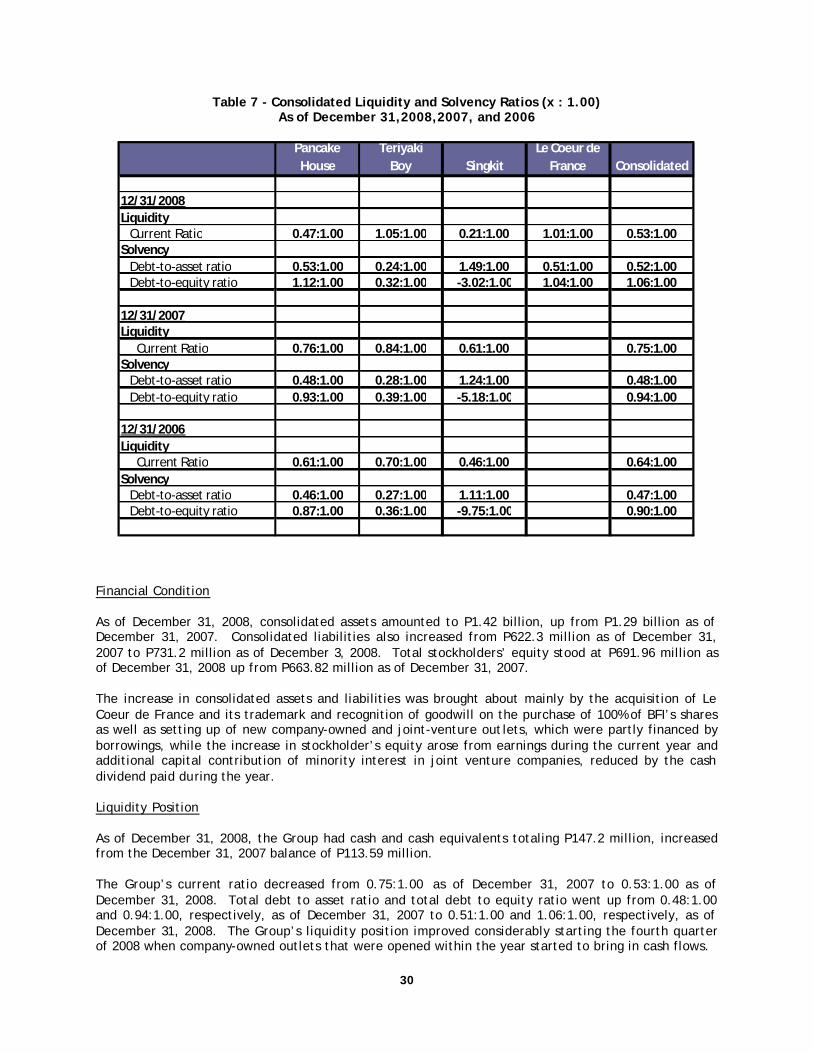

Table 5 – Profitability Ratios For the Years Ended December 31, 2008, 2007 and 2006