PAI Claims Manual

28

Department for Transport, Energy and Infrastructure Construction Risks Principal Arranged Insurance Material Damage and Public/Products Liability Insurance Manual Effective 31 st October 2006 August 2007 Prepared by: Aon Risk Services Australia Limited ABN 17 000 434 720 Level 10, 63 Pirie Street Adelaide 5000 Telephone 61 8 8301 1111 Facsimile 61 8 8301 1100

-

Upload

sambit-datta -

Category

Documents

-

view

219 -

download

0

Transcript of PAI Claims Manual

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 1/28

Department for Transport, Energyand Infrastructure

Construction RisksPrincipal Arranged Insurance

Material Damage and Public/Products LiabilityInsurance Manual

Effective 31st October 2006

August 2007

Prepared by:

Aon Risk Services Australia Limited ABN 17 000 434 720

Level 10, 63 Pirie Street Adelaide 5000Telephone 61 8 8301 1111

Facsimile 61 8 8301 1100

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 2/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

Confidentiality Notice

This report contains information which is confidential to [Client Name]and Aon Risk Services Australia Limited (Aon).

Accordingly, we trust you will understand this report is given to [Client] and its officers and employees in confidenceand may not be reproduced in any form or communicated to any other person, firm or company without the prior approval of Aon.

Privacy Notice

The Aon Group of companies have always valued the privacy of personal information. When Aon collect, use,disclose or handle personal information, Aon will be bound by the Privacy Act 1988 (the ‘Act’).

Aon collect personal information to offer, provide, manage and administer the many financial services and productswe and our group of companies are involved in. These include insurance broking and claims management, riskmanagement consulting, and other forms of insurance services (including underwriting of insurance products andreinsurance), employee benefits, premium financing, superannuation and investment advisory services. Aon alsocollect it to be able to develop, establish and administer alliances and arrangements with other organisations in

relation to the promotion, administration and use of our respective products and services.

Aon disclose personal information to third parties who we believe are necessary to assist us in providing the relevantservices and products to our clients. For instance, we disclose personal information to the relevant product provider and their representatives, our agents and contractors and related companies. We limit, however, the use anddisclosure of any personal information provided by us to such third parties for the specific purpose for which it wassupplied.

When you give Aon personal information about other individuals, we rely on you to have made or make them awarethat you will or may provide their personal information to us, the types of third parties we may provide it to, therelevant purposes we and the third parties we disclose it to will use it for, and how they can access it. If it is sensitiveinformation we rely on you to have obtained their consent on these matters. If you have not done either of thesethings, you must tell us before you provide the relevant information.

If you collect, use, disclose or handle personal information on our behalf, or receive it from us, you and your representatives must meet the relevant requirements of the National Privacy Principles set out in the Privacy Act1988 (Cth) and you must only use such information for the specific agreed purpose(s).

If you would like a copy of the Aon Privacy Policy, or wish to seek access to or correct the personal information wecollected or disclosed about you, please telephone or email your Aon representative or access the Aon websitewww.aon.com.au.

Complaints Dispute Resolution

If you have a concern about a service that Aon have provided, you should contact your Aon representative or your local Aon office.

If your complaint is not satisfactorily resolved, you should contact Aon’s National Complaints Manager on (02) 92537000 or put your complaint in writing to: National Complaints Manager, Aon Risk Services Australia Limited, GPO

Box 4189, Sydney NSW 2001.

If you are not satisfied with the outcome determined by the National Complaints Manager, you may contact theInsurance Brokers Dispute Limited by calling 1800 064 169.

Alternatively, if your concern is with the insurer or the calculation of a claim payment, you may contact the InsuranceEnquiries and Complaints Limited by calling 1300 780 808

© Aon Risk Services Australia Limited 2006.

This work and all documents provided by Aon to you is written and published by Aon Risk Services Australia Limited.

This work is copyright and confidential. Other than as permitted by law, no part of it may in any form or by any means

be reproduced, stored or transmitted without permission of the copyright owner, Aon Risk Services Australia Limited.

63705897.doc Page i

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 3/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

Table of Contents

Section 1 - Introduction .......................................................................... 11.1 Introduction ..................................................................................................................................21.2 Service Team ..............................................................................................................................3

Section 2 - Insurance Program ................................................................ 42.1 General........................................................................................................................................ 52.2 Construction Risks – Material Damage ........................................................................................62.3 Construction Risks –Public and Products Liability (Primary Policy) ..................................................................................112.4 Construction Risk -Public and Products Liability (Excess Policies) ................................................................................13

Section 3 - Claims Procedures ............................................................... 143.1 General...................................................................................................................................... 153.2 Construction Risks – Material Damage ......................................................................................163.3 Construction Risks - Liability ......................................................................................................17

Section 4 - Statutory and Other Notices ................................................. 184.1 Duty Of Disclosure .....................................................................................................................194.2 Waiver of Rights ........................................................................................................................204.3 Claims Made Policies ................................................................................................................204.4 Occurrence Basis Policies .........................................................................................................214.5 Interests of Other Parties ...........................................................................................................214.6 Unauthorised Foreign Insurers ..................................................................................................21

4.7 Utmost Good Faith .....................................................................................................................214.8 Change of Risk or Circumstances .............................................................................................214.9 Average (Co-Insurance) Clause ................................................................................................224.10 Binder Agreements ..................................................................................................................234.11 Mis-statement of Premium .......................................................................................................234.12 Essential Reading of Policy Wording .......................................................................................244.13 Terrorism Insurance Act 2003 .................................................................................................24

Appendix 1 - Claim Forms.....................................................................25

63705897.doc Page ii

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 4/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

Section 1 - Introduction

63705897.doc Page 1

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 5/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

1.1 Introduction

This Insurance & Claims Manual has been compiled by Aon Risk Services (Aon) to provide a broad outline of your Insurance Program and to offer general information and assistance in understanding the variousinsurances which have been arranged on your behalf and the steps and procedures to be followed in theevent of claims arising under the program.

Aon’s role in the claims management process, as regards above deductible claims, is as follows:

to submit, manage, regularly follow up and negotiate settlement of above deductible claims,

to assist in the resolution or conduct of difficult or contentious claims with underwriters and re-insurerswhere required,

claims administration, including collection of insurance proceeds and proactive follow-up of outstanding

claims until finalisation,

provision of status reports on above deductible claims, and

to maintain records of paid and outstanding claims for underwriting disclosure and inclusion in renewalsubmissions.

The Insurance Program section of the manual contains a brief description of individual insurances. It shouldnot however be treated as a replacement for the relevant policy documents. Each policy should be carefullyread and, in particular, note taken of the description in the policy of the coverage thereby provided as well asthe exclusions and policy conditions – these should not in any way be regarded as being fully or accuratelydescribed in the manual.

63705897.doc Page 2

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 6/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

1.2 Service Team

The Aon personnel responsible for the management of your account are:

Aon Contacts

Client RelationshipManager

Karen Brown

Telephone: 61 8 8301 1114

Facsimile: 60 8 8301 1100

E-mail: [email protected]

Account Executive Helen Auricht

Telephone: 618 8301 1176

Facsimile: 60 8 8301 1100

E-mail: [email protected]

Top Level Contact Greg Johnson

Telephone: 61 8 8301 1151

Facsimile: 60 8 8301 1100

E-mail: [email protected]

Aon Servicing Office:

Location:

Level 10, 63 Pirie StreetAdelaide, South Australia

Postal Address:

GPO Box 514Adelaide, South Australia 5001

63705897.doc Page 3

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 7/28

Department for Transport Energy and InfrstructureInsurance Manual effective 31st October 2006

Section 2 - Insurance Program

63705897.doc Page 4

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 8/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

2.1 General

The Named Insured and Business Description form part of your insurance contracts. It is thereforeimportant that you advise of any alterations that may be arise during the course of the year as these mayprejudice your insurance cover.

To eliminate unnecessary repetition, unless otherwise stated within the manual, the following informationis common to all policies:

Named Insured The Crown in the Right of the State of South Australia and theDepartment for Transport, Energy and Infrastructure

Policies also insure other parties as specified within the policy definitionof the Insured, including but not limited to:

• any principal, owner, joint venturepartner or alliance participant

• any construction manager,superintendent or project manager

• any contractor or sub-contractor of any tier

• any architect, engineer, surveyor or professional consultant

Business Description Principally but not limited to:

• government instrumentality responsible for the design, construction,manufacture, testing, commissioning and maintenance of roads,busways, bridges and other transport and infrastructure;

• plant and equipment owners, operators and hirers, lessees andlessors;

• civil contractors, designers, consultants, suppliers, project andconstruction managers, maintenance contractors;

• property owners and occupiers, lessees and lessors, but only when inconnection with the Insured Operations;

and all incidental and associated operations, trades and activities.

Insured Operations: Contracts commenced during the Period of Insurance.All Contracts of any kind or description undertaken by or on behalf

of the Named Insured and commenced during the Period of Insurance,unless subject to policy Referral conditions.

Period of Insurance From: 4.00 PM on 31st October 2006 Local Standard Time

To: as set put in each policy summary

63705897.doc Page 5

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 9/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

2.2 Construction Risks – Material Damage

Scope of Cover Material Loss or Damage Damage to the Insured Property during the Period of Insurance

Defects LiabilityDamage manifesting during the Defects Liability Period and originatingfrom:

(i) an event on the Worksite during the construction period beforethe certificate of close out is issued for the final section; or (ii) an act or omission of any of the Insured parties or some other causeoccurring in connection with an Insured party complying with therequirements of the Defects Liability Period provisions of the Contract

Insured Operations Contracts commenced during the Period of Insurance BasisAll Contracts of any kind or description undertaken by or on behalf of theNamed Insured and commenced during the Period of Insurance,however, subject to Insurer’s acceptance of Referral Contracts.

Referral Contracts

Contract Type

Where the originalEstimated ContractValue for the ContractType exceeds:

Bridge Contracts $20,000,000Tunnelling Contracts $2,500,000All Other Contracts $100,000,000Where the original estimated ConstructionPeriod for the Contract exceeds 24 months

All values

Period of Insurance From: 4.00 PM on 31st October 2006 Local Standard Time

To: 4.00 PM on 30th September 2008 Local Standard Time

Maximum DefectsLiability Period 24 months any one Contract in respect of the original Defects Liability

Period

Territorial Limits Anywhere in Australia, including cover for Insured Property whilst instorage and in transit.

Limits of Liability Limit of Liability any one Event at any one Worksite:

Contract Work $100,000,000Existing Property $1,000,000

Construction Plant and Equipment Not covered

63705897.doc Page 6

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 10/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

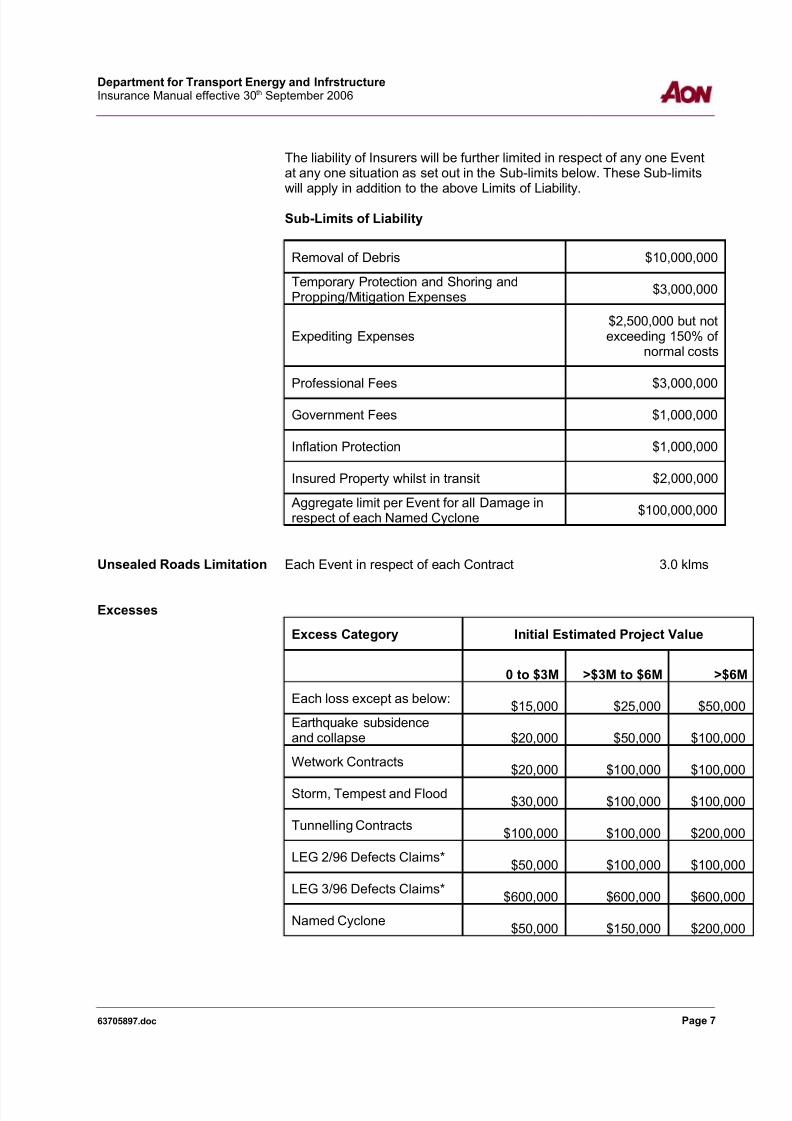

The liability of Insurers will be further limited in respect of any one Eventat any one situation as set out in the Sub-limits below. These Sub-limitswill apply in addition to the above Limits of Liability.

Sub-Limits of Liability

Removal of Debris $10,000,000

Temporary Protection and Shoring andPropping/Mitigation Expenses

$3,000,000

Expediting Expenses$2,500,000 but notexceeding 150% of

normal costs

Professional Fees $3,000,000

Government Fees $1,000,000

Inflation Protection $1,000,000

Insured Property whilst in transit $2,000,000

Aggregate limit per Event for all Damage inrespect of each Named Cyclone

$100,000,000

Unsealed Roads Limitation Each Event in respect of each Contract 3.0 klms

Excesses

Excess Category Initial Estimated Project Value

0 to $3M >$3M to $6M >$6M

Each loss except as below:$15,000 $25,000 $50,000

Earthquake subsidenceand collapse $20,000 $50,000 $100,000

Wetwork Contracts$20,000 $100,000 $100,000

Storm, Tempest and Flood$30,000 $100,000 $100,000

Tunnelling Contracts$100,000 $100,000 $200,000

LEG 2/96 Defects Claims*$50,000 $100,000 $100,000

LEG 3/96 Defects Claims*$600,000 $600,000 $600,000

Named Cyclone$50,000 $150,000 $200,000

63705897.doc Page 7

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 11/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

*Application of Excess Defects ClaimsFor the purpose of application of the Defects Claims Excesses specified itis agreed that the relevant lower LEG2/96 Defects Excess shall apply toall losses in respect of Defects Claims to all Insured Property, exceptwhere a loss occurs to a Structure and where the application of theDefects Exclusion (a) – LEG3/06 (offering broader cover) results in alarger claim being payable under this Policy, than would otherwise bepaid under application of Exclusion (b) - LEG2/96.Due to the difference in Defects Claims Excesses, the Insured may electto submit a claim only applying the Defects Exclusion (b), and in suchcircumstances, the Insurers agree to apply only the LEG 2/96 DefectsExcess.

Defects ExclusionThe policy does not provide indemnity:

(a) in respect of Damage to Structures (LEG 3/06):all costs rendered necessary by defects of material, workmanship,design, plan or specification, however should Damage (which for the purposes of this Exclusion (a) shall include any patentdetrimental change in the physical condition of the InsuredProperty) occur to any portion of the Insured Property containingthe said defects the cost of replacement or rectification which ishereby excluded is that cost incurred to improve the originalmaterial, workmanship, design, plan or specification.

(b) in respect of Damage to all other Insured Property (LEG 2/96):all costs rendered necessary by defects of material workmanshipdesign plan or specification, however should Damage occur to anyportion of the Insured Property containing any of the said defects

the cost of replacement or rectification which is hereby excluded isthat cost which would have been incurred if replacement or rectification of the Insured Property had been put in handimmediately prior to the said damage.

Annual Declarationof Contract Values You are required to declare within 30 days of the expiry of each period:

(a) final Contract Values by contract typecompleted during the precedingperiod

(b) projected Contract Values by

contract type commenced during thepreceding period, but not completedas at the end of the Period of Insurance.

(c) projected Contract Values bycontract type expected to commenceduring the forthcoming period

Subject to any applicable minimum premium, the Premium will beadjusted by payment to the Insurers of an additional premium or byallowance to the Insured of a return premium, as the case may be,calculated at the agreed rates on the difference between the estimatedand final or projected Contract Values.

63705897.doc Page 8

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 12/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

63705897.doc Page 9

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 13/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Underwriter Zurich London Limited 51%Great lakes UK 34%Vero Insurance Australia Limited 15%

Policy Number/s Zurich London Limited TBAGreat Lakes UK TBAVero Insurance Australia Limited TBA

63705897.doc Page 10

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 14/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

2.3 Construction Risks –Public and Products Liability (Primary Policy)

Scope of Cover Legal LiabilityLegal liability to pay damages or compensation in respect of:(a) Personal Injury;(b) Property Damage; or (c) Advertising Injury,happening :

(i) during the Construction Period or the Defects Liability Period inrespect of the Insured Operations; or (ii) during the Period of Insurance in respect of the Insured’s

Products;Defence and Other CostsIn addition to the above(a) all legal costs and other expenses incurred with the written consent of the Insurers;(b) all costs and expenses incurred by the Insured for legalrepresentation at any coroner's inquest, fatal accident inquiry or court of summary jurisdiction;(c) expenses incurred by the Insured for first aid rendered for injury toothers at the time of an Occurrence;(d) expenses incurred by the Insured for temporary repair and or shoringup of property made necessary by an Occurrence,

subject to the approval of the Insurers.

Insured Operations Contracts commenced during the Period of Insurance BasisAll Contracts of any kind or description undertaken by or on behalf of theNamed Insured and commenced during the Period of Insurance,however, subject to Insurer’s acceptance of Referral Contracts.

Referral Contracts

Contract Type

Where the originalEstimated ContractValue for the Contract

Type exceeds:Bridge Contracts $20,000,000Tunnelling Contracts $5,000,000All Other Contracts $100,000,000Where the original estimated ConstructionPeriod for the Contract exceeds 36 months

All values

63705897.doc Page 11

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 15/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Endorsed ReferralContracts The following Contracts have been referred and accepted by

Underwriters:

DescriptionEstimatedConstruction/DefectsLiability Period

South Road / Anzac Highway Underpass Mid 2007 to Mid 2009South Road / Port,Grange & Torrens RoadsUnderpass

Mid 2007 to Mid 2009

Period of Insurance From: 4.00 PM on 31st October 2006 Local Standard Time

To: 4.00 PM on 30th September 2008 Local Standard Time

Defects Liability Period 24 months any one Contract in respect of the original Defects LiabilityPeriod

Territorial Limits Anywhere in the world but excluding any operations of the Insureddomiciled in the United States of America or Canada.

Limit of Liability Limit in respect of each Occurrence $20,000,000

but limited to $20,000,000 in the aggregate for all Occurrences in respectof Products.Limit of Liability any one Event at any one Worksite.

Retroactive Date In respect of Product Liability:Bakewell Bridge 13th October 2006All Other Contracts 31st October 2006

Excesses

Each Occurrence in respect of Contracts where theoriginal estimated Contract value is:

$0 to $3,000,000 $25,000

$3,000,001 to $6,000,000 $50,000Greater than $6,000,000 $100,000Except for Worker to Worker LiabilityEach Occurrence in respect of all Contracts irrespective of the Contract value

$100,000

Underwriter Liberty International Underwriters 66.67%Lloyds of London (DA Constable Syndicate) 33.33%

Policy Number Liberty International Underwriters TBALloyds of London (DA Constable Syndicate) TBA

63705897.doc Page 12

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 16/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

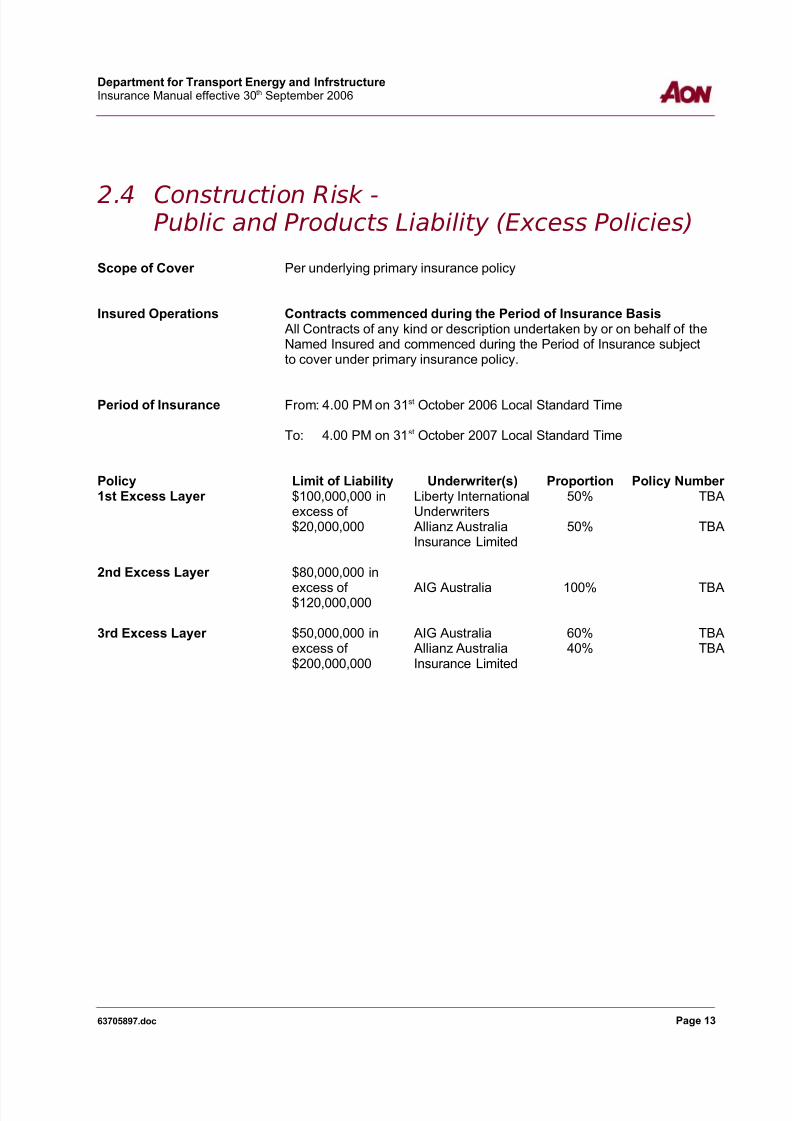

2.4 Construction Risk -Public and Products Liability (Excess Policies)

Scope of Cover Per underlying primary insurance policy

Insured Operations Contracts commenced during the Period of Insurance BasisAll Contracts of any kind or description undertaken by or on behalf of theNamed Insured and commenced during the Period of Insurance subjectto cover under primary insurance policy.

Period of Insurance From: 4.00 PM on 31st October 2006 Local Standard Time

To: 4.00 PM on 31st October 2007 Local Standard Time

Policy Limit of Liability Underwriter(s) Proportion Policy Number 1st Excess Layer $100,000,000 in

excess of $20,000,000

Liberty InternationalUnderwriters

50% TBA

Allianz AustraliaInsurance Limited

50% TBA

2nd Excess Layer $80,000,000 in

excess of $120,000,000

AIG Australia 100% TBA

3rd Excess Layer $50,000,000 inexcess of $200,000,000

AIG Australia 60% TBAAllianz AustraliaInsurance Limited

40% TBA

63705897.doc Page 13

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 17/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Section 3 - Claims Procedures

63705897.doc Page 14

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 18/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

3.1 General

This section is designed to provide assistance in procedures to be followed in the event of any incidentthat might give rise to a claim occurring under any of your insurance policies.

All claims (except where otherwise agreed and noted herein) are to be reported immediately to Aon.

To enable the processing of the claim without delay and to minimise the possible damage or injuryincurred, it is important that the following action be taken.

1. All reasonable steps should be taken following an accident or loss to protect the property or personfrom any further damage or injury.

2. Any incident which may give rise to a claim should be immediately reported to Aon to avoid anypotential for denial of liability from underwriters alleging late notification.

3. Any loss by theft and/or wilful or malicious damage should be immediately reported to the nearestPolice station.

4. Comply with the relevant claims procedure specific to the class of insurance for which the claimapplies to.

5. Complete the appropriate Aon claim form included within Appendix 1 of this Manual. The forms arealso available through the Aon website http://www.aon.com.au/.

6. Forward claim documentation including any supporting papers without delay to Aon.

63705897.doc Page 15

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 19/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

3.2 Construction Risks – Material Damage

Generally, such claims relate to loss or damage to your property which may involve events such as fire,storm, explosion, flood, theft/burglary, malicious damage, etc.

Where there has been loss or damage to your property:

1. Take all reasonable steps to protect property from any further loss or damage.

2. Call the Police or other Emergency Services as required. Any loss by theft or wilful or maliciousdamage should immediately be reported to the nearest Police Station and details of the attendingPolice noted.

3. If you suspect that the loss or damage may exceed the policy deductible, notify Aon immediately of the details of the claim (e.g. description of incident, amount of loss, etc.). Aon will then provide

further instructions on how to handle the claim.4. Where required, complete a Claim Form and all claims documents as soon as possible after the

occurrence whilst memory of the incident is still fresh in the minds of all concerned.

5. Ensure full cooperation with the Loss Adjuster appointed by your underwriter.

63705897.doc Page 16

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 20/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

3.3 Construction Risks - Liability

Under No Circumstances Must Liability Be Admitted Either Verbally Or In Writing

Upon the happening of any incident likely to give rise to a claim, the following points must be noted:

1. All reasonable steps should be taken following an accident or loss to protect the person or propertyfrom any further injury.

2. Advice must be forwarded to Aon, together with originals of all correspondence received from athird party and any other supporting documentation (e.g. incident report)

3. Where an Incident Report is to be completed, bear in mind the following:

Be Discreet – Do not complete the Incident Report in front of the injured person. This may signalthat an insurance claim may be possible.

Be Specific – Remember, the report you write may be forwarded to your underwriter for assessment and evaluation purposes and may be admitted as evidence in court. Be specific andcomprehensive in your details.

Provide Full Details – Detail (no matter how trivial it may seem at the time), is the most essentialcomponent of your Report. In most instances, if the claim ever reaches a court of law, it may beseveral years down the track. Nobody will remember the specifics unless you write them down atthe time of the Report.

4. No correspondence should be entered into with a third party except acknowledgement of receipt of the claim. The acknowledgement letter should read as follows:

"Without Prejudice"

We acknowledge receipt of your correspondence concerning an incident at [Location]. This isreceiving our attention.

5. Do not give any interview or make any statement to a Loss Adjuster or other person investigatingany accident or damage unless such person is acting on behalf of your underwriter.

63705897.doc Page 17

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 21/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Section 4 - Statutory and OtherNotices

63705897.doc Page 18

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 22/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

It is essential that you carefully read and understand the following notices. If you have any queries pleaseseek advice from Aon.

4.1 Duty Of Disclosure

In accordance with the provisions of the Insurance Contracts Act 1984 (Cth), you and everyone who is aninsured under your policy and/or everyone who arranges insurance on behalf of a business entity and/or body corporate, must comply with the Duty of Disclosure. Make sure that you explain the duty to anyother insureds you apply on behalf of and/or to others involved in arranging insurance.

The duty requires you to tell an insurer certain matters which will help it decide whether to offer insuranceand, if so, on what terms.

The duty applies at the first application for a policy and on any renewal, variation, extension or replacement of the policy.

The type of duty that applies can vary according to the type of policy.

To assist Aon in protecting your interests, it is important that you tell us every matter that:

you know, or

a reasonable person in the circumstances could be expected to know,

is relevant to the insurer's decision whether to offer insurance and, if so, on what terms.

Aon will then assist you in determining what needs to be disclosed to the insurer in order to meet your duty.

Examples of matters that should be disclosed are:

any claims made in recent years for the particular type of insurance;

refusal by an insurer to renew a policy;

any unusual feature of the insured risk that may increase the likelihood of a claim.

Failure to comply with the duty may give the insurer the right to cancel the policy or reduce the amount itpays in the event of a claim. If the failure to comply with the duty is fraudulent, the insurer may treat thepolicy as if it never existed and pay nothing.

Even if Aon is handling claims for you, you must disclose these matters on your proposal. Aon cannot

complete or add to your proposal in any way.

If you are uncertain about whether or not a particular matter should be disclosed, please contact Aon. The Duty of Disclosure must be taken seriously as it may affect your right to claim.

The history of losses suffered and claims made by the party seeking insurance, or any person, firm or company closely associated with that party, is one of the principal matters to be disclosed. It is thereforeimperative that you maintain an up-to-date record of all such losses and claims.

Whilst Aon will maintain records of all losses reported to us during the term of our appointment as your Broker, we do not accept responsibility for obtaining details of prior losses or for checking in any particular instance that you have made proper and complete disclosure.

63705897.doc Page 19

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 23/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

We recommend you:

supply all management and senior staff with a copy of the Duty of Disclosure Notice;

emphasise to them that the Duty of Disclosure applies not only at inception of the insurance, but also when policies are altered or renewed;

point out to them that disclosure is most important in matters touching upon past claims,cancellation of insurance covers, premium penalties and any other matters which may influence anunderwriter’s acceptance of the risk such as criminal convictions or insolvency of previouscompanies; and

have a system in place which ensures that all relevant matters come to their attention.

4.2 Waiver of Rights

Some policies contain a clause that limits or excludes claims where the insured has limited its rights torecover a loss from another party in circumstances where that other party is responsible for the loss. For example, this may happen where the insured has entered into a contract limiting the liability that the other contracting party would have been under in the absence of the contract.

If you have entered into, or propose to enter into a contract which might limit rights against another contracting party, please let Aon know, so that we can advise you about how the agreement affects, or will affect, your cover.

4.3 Claims Made Policies

Directors’ and Officers’ Liability, Comprehensive Crime, Professional Indemnity and SuperannuationTrustees’ Liability policies and some other liability policies are written on a “Claims Made” basis.

This means that they cover only those claims made against you during the period of insurance. In somecases you must also notify the insurer of the claim during the period of insurance.

A Claims Made policy does not provide cover in relation to:

claims made after the expiry of the period of insurance even though the event giving rise to theclaim may have occurred during the period of insurance;

claims notified or arising out of circumstances notified under any previous policy;

claims made against you prior to the commencement of the period of insurance; claims arising out of circumstances noted on the proposal form for the current period of insurance

or on any previous proposal form; and

events that occurred prior to the retroactive date of the policy (if such a date is specified).

However, where you give notice in writing to the insurer of any facts that might give rise to a claim againstyou as soon as reasonably practicable after you become aware of those facts, but before the expiry of theperiod of insurance, the policy will, subject to it’s terms and conditions, provide cover even if that claim ismade after the expiry of the period of insurance. For this reason, you must send us written notice duringthe policy period of any facts or events that might give rise to a future claim. If you do not, you may nothave cover if a claim arises later.

Upon expiry of the policy no further claims can be made thereunder and the need to maintain insurance

63705897.doc Page 20

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 24/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

or the arrangement of run-off cover is essential.

4.4 Occurrence Basis Policies

Combined General Liability, Industrial Special Risks, Travel, Aviation, Contract Works, Marine policiesand some other policies are written on an occurrence basis.

This means when there is an incident/occurrence giving rise to a claim, the policy that responds is thepolicy that was in force at the time of the incident/occurrence.

4.5 Interests of Other Parties

Many policies exclude cover for an interest in the insured property held by someone other than thenamed insured, unless that interest is specifically noted on the policy. For example, if property is jointlyowned, or subject to finance, the interest of the joint owner or financier may be excluded if it is notspecifically noted on the policy.

Generally, the safest course is to have all interests in all property insured noted on each policy.

4.6 Unauthorised Foreign Insurers

If one or more of the insurance companies concerned with a particular policy is an unauthorised foreigninsurance company Aon will notify you of this fact. Nothing stops an unauthorised foreign insurer fromissuing insurance to you.

An unauthorised foreign insurer is an insurer that does not directly carry on insurance business inAustralia (i.e. they operate overseas only) and thus is not required to be licensed to do so under theInsurance Act 1973 (Cth). Such insurers are not subject to the Act which establishes a system of financial supervision of general insurers in Australia. You can obtain further information from Aon on theinsurer such as where it is incorporated, its paid up capital, whether it is subject to financial regulation,and the laws that will apply to any dispute.

4.7 Utmost Good FaithEvery contract of insurance is based on the principle of utmost good faith, requiring each party (whichmeans both you and the insurer) to act towards the other party in respect of any matter arising under thecontract, with the utmost good faith. If you fail to do so you may prejudice your rights under the policyand in particular, any claim.

4.8 Change of Risk or Circumstances

It is important that you advise Aon of any material alterations to your business or products or indeed of

any development which may have a bearing on the adequacy of your Insurance Program.

63705897.doc Page 21

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 25/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Your insurers have assessed and accepted your risks at an agreed premium on the basis of informationprovided during the placement and/or subsequent renewals of your insurance policies. Any variation of those details, if not advised to them, could prejudice the insurance cover.

The following list may be used as a guide to activities that should be notified to Aon when they are beingproposed or when they occur so that action can be taken to ensure your interests are adequatelyprotected. It is by no means a complete list so, when in doubt, contact Aon for guidance:

Acquisition of new companies and/or mergers and/or joint ventures (including sale or disposal of subsidiary companies).

Purchase, construction or occupancy of new premises, alteration, vacation, temporaryunoccupancy, extension or demolition of existing premises. Details of any new building or alteration work should be advised during the planning stage.

Proposed installation of significant items of plant, machinery or equipment.

Increase in value in excess of insured limits for buildings, plant and stock.

Substantial removal of stock or equipment to other locations.

Contractual liabilities (i.e. leases, hiring agreements), particularly any contracts which imposegreater than usual liabilities.

Granting of indemnities or hold harmless agreements e.g. lease agreements, contracts for supplyor maintenance of fire protection and/or burglary protection equipment.

Changes in processes, property occupancy, products or extension of business operations,including new products or processes.

Alteration, amendment to or disconnection of fire or burglary protection systems.

Charter or operation of aircraft or waterborne craft, other than ordinary commercial passenger

travel. Developments involving establishment or extension of overseas operations or export of products.

If Fidelity Guarantee (or Employee Theft) is insured, any alteration to the system of checks,supervision, audits and the like must be advised to insurers immediately.

Issuance of any shares, debentures, ADRs; issuance of a prospectus or Information Memorandum;listing on a stock exchange; issuance of public or private offerings.

Advice of other activities which could affect the nature of the risk originally accepted by insurers.

Early notification of development projects at the planning stage will enable Aon to further assist you by:

developing a sound and economical approach to construction insurance;

reviewing indemnity and insurance clauses of contracts to ensure they are drafted in your bestinterests and do not prejudice your insurance program;

mutually analysing and agreeing upon standards of fire protection and security;

introducing Aon’s experienced consultants, to advise you on important aspects of Safety and RiskManagement;

mutually analysing your exposure to financial loss if the project is delayed, to determine your needfor Advanced Business Interruption Insurance.

4.9 Average (Co-Insurance) Clause

Many policies, principally Industrial Special Risks (Material Damage and Business Interruption), Fire and

63705897.doc Page 22

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 26/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Perils, General Property, Computer and Machinery Breakdown, contain an “average” (otherwise called“co-insurance”) clause. This type of clause requires you to bear a proportion of each loss or claim if thesum insured is inadequate to cover the full potential loss. In effect, you are treated as if you self-insureda proportion of the risk because you did not insure the full value of the risk.

In order to avoid the application of average to a claim it is essential to ensure that the level of insurance isadequate whenever you arrange a new policy or renew an existing one. If insurance is on a“reinstatement and replacement” basis (i.e. “new for old”), the sum insured must be for the full cost of replacing the insured property with new property.

Aon does not calculate or approve the sums insured that you notify to us. Aon has a specialist division,which offers valuation services. If you would like to know more about this service, please contact your Aon representative.

Note: Insurance valuations typically represent reinstatement / replacement costs and estimates of related

professional fees exclusive of GST, on the assumption that most commercial property owners will beentitled to a 100% Input Tax Credit on outlays incurred in the event of a loss.

It is customary for insurers to establish an insured’s GST status upon receiving a claim and to arrangesettlement on a GST neutral basis.

Insureds who may not be entitled to a 100% Input Tax Credit are advised to ensure that their propertyinsurance valuations – and their sums insured – correctly reflect their GST status.

4.10Binder Agreements

Aon has binder agreements with some insurers under which we are authorised to commit those insurersto providing cover without reference to them. Some of the classes of insurance provided in your programmay be placed under such binder agreements.

When acting under a binder agreement we will be acting under an authority given to Aon by the insurer and will be effecting the insurance contract as agent of the insurer and not as your agent.

Nevertheless, we believe that in respect of those classes of insurance written under a binder agreement,the policy terms are very favourable and the rates are highly competitive. In addition, our binder arrangements with the insurers are such that we remain your agent in the handling of any claims thatmight arise under any of the policies written.

4.11Mis-statement of Premium

Aon makes every effort to determine the correct amount of premium and statutory charges that apply toyour insurance. In the event that Aon mis-state that amount (either because we have made anunintentional error or because a third party has mis-stated the amount), we reserve the right to correct theerror.

By instructing Aon to arrange insurance for you, you agree, where permitted by law, that you shall nothold Aon responsible for any loss that you may suffer as a result of any such mis-statement.

63705897.doc Page 23

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 27/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

4.12Essential Reading of Policy Wording

Your policy wordings have been issued or will be issued to you as soon as they are received from theinsurers. It is absolutely essential that you read these documents and advise Aon in writing of anyaspects which are not clear or where the cover does not meet with your requirements.

4.13Terrorism Insurance Act 2003

The Terrorism Insurance Act 2003 (the Act) deems terrorism cover into certain commercial insurancepolicies – eligible insurance contracts – covering eligible property in Australia.

In broad terms, the Act applies to non-residential buildings, structures, other works and their contents.Business Interruption covers which relate to the ownership or occupation of such property, and liabilitypolicies, to the extent that the liability arises from the ownership or occupation of such property, are alsoembraced by the legislation.

To qualify as an eligible insurance contract, a policy must be subject to a terrorism exclusion. Upon anevent being deemed a declared terrorism incident by the Government, the Act renders terrorismexclusions inoperative and insureds may lodge claims with their insurers for losses caused by the terroristincident. Apart from the terrorism exclusion, all other terms and conditions of policies deemed to beeligible insurance contracts remain the same.

Policies which contain an Act of Terrorism exclusion and which are designated an eligible insurancecontract in terms of the Terrorism Insurance Act, are generally identified accordingly. Subject to all other terms and conditions of policies so designated, coverage is amended to the extent provided by theTerrorism Insurance Act 2003.

63705897.doc Page 24

8/6/2019 PAI Claims Manual

http://slidepdf.com/reader/full/pai-claims-manual 28/28

Department for Transport Energy and InfrstructureInsurance Manual effective 30th September 2006

Appendix 1 - Claim Forms

63705897 doc Page 25