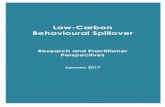

P Q CORRECTING SPILLOVER COSTS D 0 Spillover costs StSt S TAX Overallocation Corrected Q0Q0 QeQe.

11

-

Upload

trevor-gin -

Category

Documents

-

view

216 -

download

2

Transcript of P Q CORRECTING SPILLOVER COSTS D 0 Spillover costs StSt S TAX Overallocation Corrected Q0Q0 QeQe.

P

Q

CORRECTING SPILLOVER COSTS

D

0

Spillovercosts

St

S

TAX

OverallocationCorrected

Q0 Qe

P

Q

CORRECTING SPILLOVER BENFITS

0 Q0Qe

D

S

Dt

Subsidy toconsumerincreasesdemand

UnderallocationCorrected

Correcting by Subsidy to Consumers

P

Q

D

0

Subsidy toproducersincreases

supply

St

S’t

UnderallocationCorrected

Qe Q0

Correcting by Subsidy to ProducersCORRECTING SPILLOVER BENFITS

S = Supply of pollution rights

D 2012

Pric

e pe

r pol

lutio

n rig

ht

Quantity of pollution rights500 750 1000

$200

$100

D 2004

Market for Externality Rights

SOCIETY’S OPTIMAL AMOUNTOF EXTERNALITY REDUCTION

MC

MB

Socially optimumamount ofpollution

abatement

0

So

ciet

y’s

mar

gin

al b

enef

it a

nd

mar

gin

alco

st o

f p

oll

uti

on

ab

atem

ent

Amount of pollution abatement

Q1

Apportioning the Tax Burden• Benefits-received principle• Ability-to-pay principle• Types

– Progressive• Average Rate increases as income increases• Ex. Federal Income Tax

– Proportional (Flat)• Average rate remains the same regardless of income• Ex. Corporate Income Tax (35%)

– Regressive• Average rate declines as income increases• Ex. Sales Tax

Incidence and Elasticity

20 40 60 80 100

100

80

60

40

20

0

Percent of Families

Per

cen

t o

f In

com

e Perfect Equality

CompleteInequality

Lorenz Curve (actual distribution)

Area betweenthe lines shows

the degree ofincome inequality

Lorenz curveafter taxes and

transfers

THE LORENZ CURVE