P FIAAS 19Mar13.pptfinity.com.au/wp-content/uploads/2013/04/34-FIAAS... · ICAAP – 2013 and...

34

FIAAS Forum 19 March 2013 Finity Consulting Pty Limited 2013 Supplied subject to the FIAAS terms of agreement and http://www.finity.com.au terms of use of the Finity client website available at: http://www.finity.com.au/Website_Terms_of_Use.pdf Queries can be directed to [email protected]

Transcript of P FIAAS 19Mar13.pptfinity.com.au/wp-content/uploads/2013/04/34-FIAAS... · ICAAP – 2013 and...

FIAAS Forum

19 March 2013

Finity Consulting Pty Limited 2013 Supplied subject to the FIAAS terms of agreement and

http://www.finity.com.au terms of use of the Finity client website available at:

http://www.finity.com.au/Website_Terms_of_Use.pdf

Queries can be directed to [email protected]

Agenda

ICAAP update

Use of broker Cat models

ICRC

� Property – horizontal requirement

� Non-property – other accumulations

Reminder of Chatham House rule:

“Participants are free to use the information received, but neither the identity nor the affiliation of the speaker(s), nor that of any other participant, may be revealed.”

Slide 2

ICAAP Update

Slide 3

ICAAP recap

ICAAP challenges

What’s next?

ICAAP annual report

ICAAP reviews

Today’s Discussion

Slide 4

ICAAP Overview

Consistency

Alignment

Risk

Appetite

Business

Planning &

Decision

MakingRisk Mgmt

& RMF

Cap Ad and

Capital Mgmt

Slide 5

Key Learnings and Outcomes

• Better understood

• Made explicit

• Clearer definition

Better risk appetite

• Range of risks understood

• Better understanding of likelihood of unfavourable outcomes

Risk analysis

• More sophisticated basis for TOR

• Understanding of why TOR chosen – Boards and management

Capitalmanagement

plan

• Increased Board engagement

• Integration of risk appetite, analysis and capital management

• Documentation – ICAAP Summary Statement

Other

Slide 6

Challenges of ICAAP development

Risk appetite statement

� Format of statement

� Staying out of the detail

� Probabilities?

Risk analysis (scenario and stress testing)

Developing scenarios

� individual classes/factors

� combinations of factors – ‘holistic’ across business/market

� how extreme?

� Technical

� estimating scenario probabilities (e.g. claims: use risk margins CV)

� 1 year vs ultimate

� Operational and other less quantifiable risks

� Explaining results and implications

� Branches – relevance of output

Slide 7

Challenges (continued)

TOR

� Bottom of range – what probability of PCR coverage reducing to 1 is

OK?

� Top of range – how much is too much?

ICAAP summary statement

� Level of detail, length

� Document ‘going round in circles’

� (Sometimes) highlighting inconsistency between risk appetite and

findings of risk analysis

Slide 8

ICAAP – 2013 and beyond

Monitoring solvency and consistency with risk tolerances

Embedding ICAAP into day-to-day business management

Refinement of framework – especially if business changes

Reporting to Board

Annual ICAAP Report

Independent review

Slide 9

APRA’s Focus

‘Low key’ collection of all Summary Statements

� Feedback?

Will be looking for evidence that management is actively considering its ICAAP

� Board, Audit Committee meetings

� Business planning, budgeting

� Key decision making

� Day-to-day risk management

Slide 10

ICAAP Annual Report

• Actual vs planned ICAAP outcomes

• Material changes to ICAAPReview

• Projected capital levels

• Planned capital usage

• Changes in risk profile or capital management

Project

• Details of scenario and stress testing

• Details of ICAAP review

• Declaration

Other

Slide 11

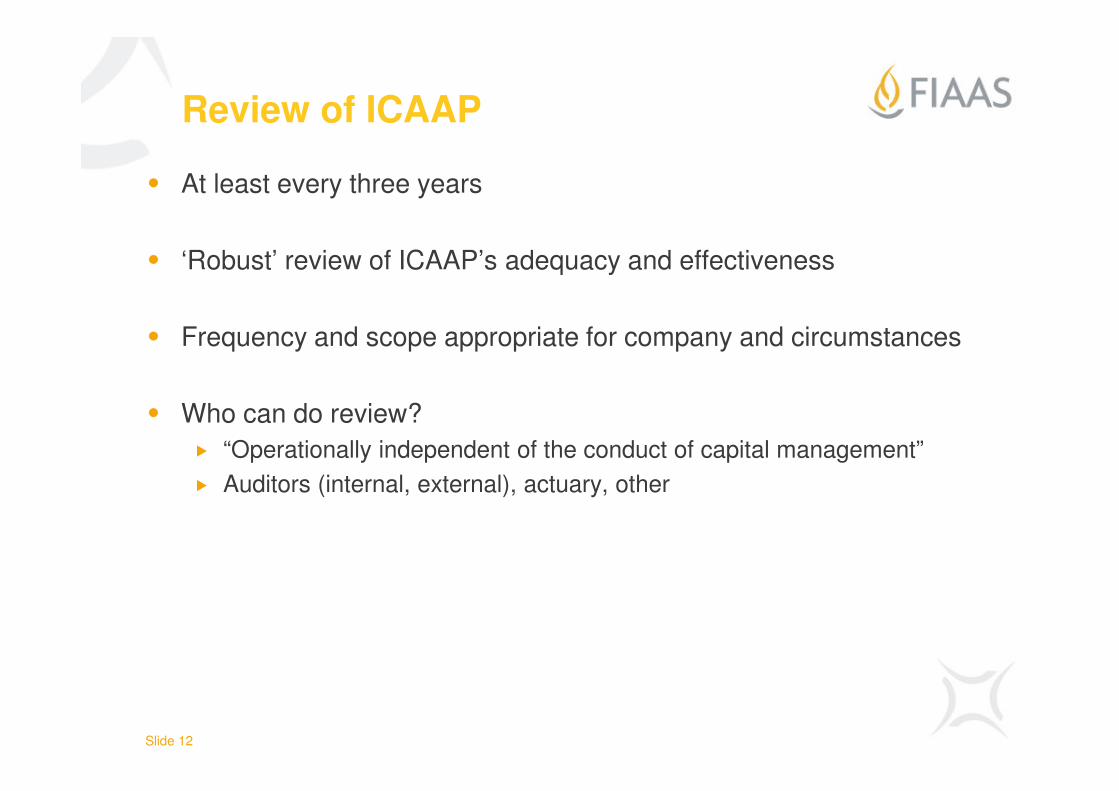

Review of ICAAP

At least every three years

‘Robust’ review of ICAAP’s adequacy and effectiveness

Frequency and scope appropriate for company and circumstances

Who can do review?

� “Operationally independent of the conduct of capital management”

� Auditors (internal, external), actuary, other

Slide 12

Use of Broker CAT Models

Slide 13

APRA requirements

The GPS 116 requirements are:

Catastrophe models

55. It is common practice for an insurer to use computer-based modelling techniques, developed either in-house or by external providers, to estimate likely losses under different catastrophe scenarios. If an insurer uses such a model, the model must be conceptually sound and capable of consistently producing realistic calculations.

An insurer must be able to demonstrate:

(a) that the model has been researched and tested

(b) that the insurer has taken measures to ensure that the data used to estimate its losses is sufficiently consistent, accurate and complete, and there is appropriate documentation of any estimates of data used; and

(c) an understanding of the model used in estimating losses, including:

(i) perils and elements that are not included in the model

(ii) assumptions and any estimates used in the modelling process

(iii) sensitivity of the model outputs as a result of the factors in (i) and (ii).

Slide 14

Much of guidance (GPG 116) appears quite onerous

APRA expects the Board and senior management of an insurer to have a sound understanding of the insurer’s approach to the use of models to manage catastrophe risks

This would include an overall understanding of the use of the models, their limitations and their weaknesses

The Board and senior management are expected to understand the uncertainty in the model outputs and the resulting impact this has on key decisions such as reinsurance purchasing and the capital held for catastrophe risk

Slide 15

• Once the insurer settles on the model(s) to be used, GPS 116 requires an insurer to be able to demonstrate that the catastrophe model(s) have been adequately researched and tested

• APRA envisages an insurer using a catastrophe model from an external provider would document:

(a) which model(s) have been chosen and the model versions

(b) a clear rationale for choosing the model(s), including, where relevant, consideration of advice on model selection from brokers or other external advisors

(c) an approach to validating the model(s), including demonstration that the model provider itself understands the environment the insurer operates in and confirms the model is suitable for its intended use

(d) an understanding of the shortcomings (such as non-modelled elements and assumptions) of the model including how it can impact the model output and how the insurer has attempted to address those shortcomings

Much of guidance (GPG 116) appears quite onerous…….

Slide 16

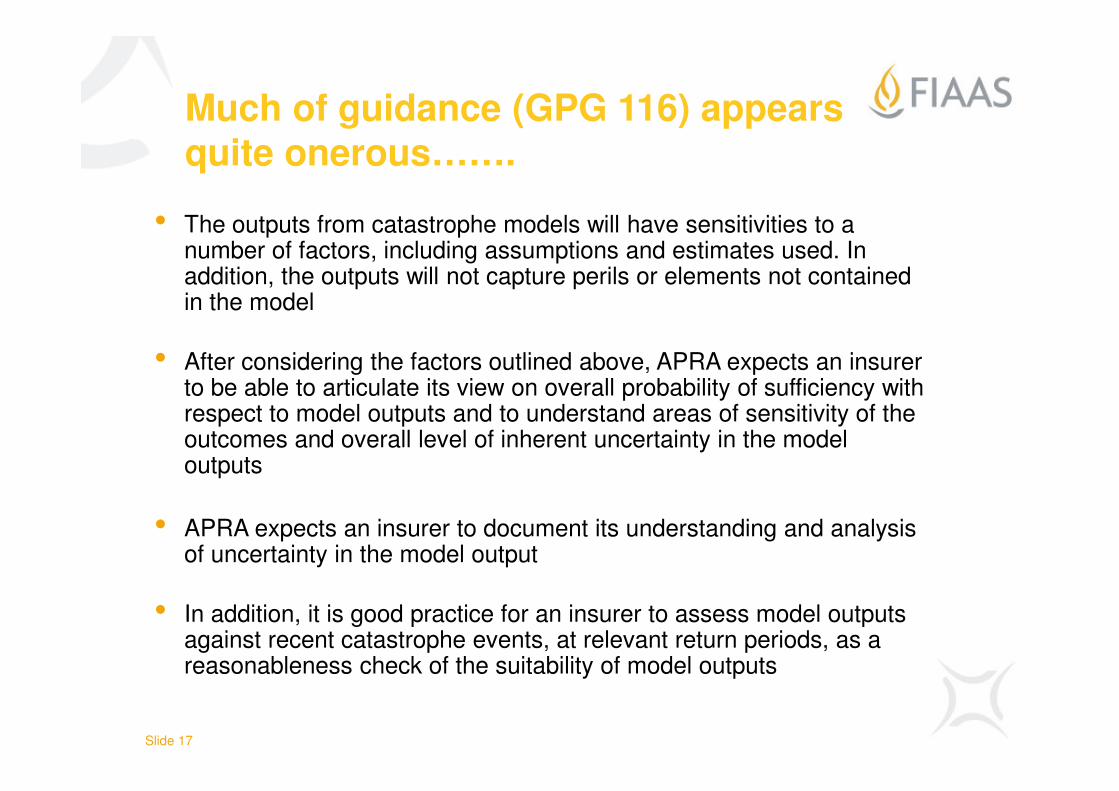

• The outputs from catastrophe models will have sensitivities to a number of factors, including assumptions and estimates used. In addition, the outputs will not capture perils or elements not contained in the model

• After considering the factors outlined above, APRA expects an insurer to be able to articulate its view on overall probability of sufficiency with respect to model outputs and to understand areas of sensitivity of the outcomes and overall level of inherent uncertainty in the model outputs

• APRA expects an insurer to document its understanding and analysis of uncertainty in the model output

• In addition, it is good practice for an insurer to assess model outputs against recent catastrophe events, at relevant return periods, as a reasonableness check of the suitability of model outputs

Much of guidance (GPG 116) appears quite onerous…….

Slide 17

Where to from here?

Most (or all) insurers do not meet the APRA requirements currently

� Probably few are close

While the requirements appear onerous, there is some value to be gained

The journey is more important than the destination (and it will be quite a

journey)

Your cat modellers can do much of this for you, if you ask the right questions

Initial areas for focus?

� Clear framework

� Greater communication with cat modellers

� Dealing with the known unknowns

� Dealing with uncertainty

� Better documentation

� Board education

Slide 18

Consider a framework which deals explicitly with known gaps in the modelling and with the uncertainty of the results.

Comparison of the final PML with realistic disaster scenarios as a means of reasonableness checking the PML.

Catastrophe Modelling Results

Adjustment for known

omissions

Dealing with uncertainty

Proposed Approach

Base PML (at least 1 in 200 PML)

Explicit allowance:

- non-modelled perils + a%

- secondary events + b%

- non modelled claim costs + c%

- uncertainty buffer + d%

= Base PML, plus explicit buffers

A framework for estimating PML

Slide 19

Adjustment for known omissions

Is it possible to estimate explicit adjustments for hazards not modelled:

� Non modelled perils

� Perils which are modelled, but aspects of the hazard are missed

Is it possible to estimate explicit adjustments for costs not modelled:

� Missing direct costs

� Missing indirect costs

� Inflation, growth

Slide 20

Estimating cat model uncertainty

Slide 21

Property ICRC – Horizontal Requirement

Slide 22

Horizontal RequirementGreater of:

a. Net cost of four 1-in-6-year (H4) events less premium liability offset, and

b. Net cost of three 1-in-10-year (H3) events less premium liability offset

Premium Liability Offset = Net cost of events that are also included in net

premium liability (with a frequency of at most 1 in 3 months)

Needs an event loss distribution

Slide 23

HR – The Event Loss Distribution

Event loss distribution must be appropriate for lower return periods

� Broker models: Cannot be blindly relied upon as may not fit well for lower return

periods

Slide 24

Estimating an Event Loss Curve

Incorporate a variety of data sources to produce an event loss curve for a

specific insurer

� Catastrophe modelling results

� Insurance Council Disaster Register

� Ideally split by CRESTA zone and use insurer’s market share in that zone to estimate equivalent insurers specific 45 year history

� Insurer’s last 5-10 years of experience

� Adjust for inflation and change in size/profile

Comparison to CAT models

� Test results from catastrophe models at low ARIs

� Consider reasonableness of AAL indicated by the cat model

Slide 25

Estimating an Event Loss Curve (cont)

Allowance for past events

� Recognise that the last 5 years of experience was not typical

� Allow for the high rate of claims inflation in reviewing past events

� Consider relevance of last 45 years to assessment of current cost levels

When using this curve for reinsurance modelling

� ENSO is relevant. The distribution of the number of events in the year is more

skewed than a Poisson

� This is important to pricing aggregates etc.

� One approach is to model frequency in a multi-state manner (La Nino, El Nino, Neutral)

Finity has developed such a model

Slide 26

Non-Property ICRC – “Other Accumulations”

Slide 27

APRA GuidanceGPS 116 requires an insurer to consider:

a. the nature of the insurance

b. the common dependent causes resulting accumulation of losses, whether that cause may occur either

once at a point in time or arise over an extended period.

c. the potential for multiple classes to be impacted by the same cause;

d. whether reinsurance cover purchased is sufficient to cover the PML (cannot just rely on reinsurance

retentions to determine ICRC)

A vertical test only (i.e. 1 in 200 year event)

� However AA must “comment in the FCR on the exposure of the insurer to

multiple non-property events in a year and whether that would materially

alter the determination of the ICRC” (i.e. the horizontal component)

Insurers to consider a range of possible scenarios

� Based on historical experience and plausible hypothetical scenarios

Additional considerations:

� Including allowance for reinsurance (recoveries and reinstatements) and

any premium liability offset (as calculated by the AA)

� Can also adjust for risks that have already been allowed for within other risk charges (asset or liability)

Slide 28

Estimating Costs at 1 in 200yr

Very limited loss data at the 1 in 200 year level

General Principles

� Think about underlying drivers of accumulation exposure

� Use as much historical information as possible and other

literature/media. Have you ever had a one in 200 year event? -

probably not

� Can you extrapolate from other events?

� Build expected losses under these types of 'what if' scenarios

Time horizon – one year or multi-year?

� Expected claims incurred (includes IBNR) in a year following the

discovery of loss

Slide 29

Determining Scenarios

Institute working group approach:

•Source: “Insurance Concentration Risk Charge – Other Accumulations Vertical Requirement”: Presentation to GI

Seminar 2012, Collings, Gard, Stephan, White, Yee

Slide 30

Examples of AccumulationsDifferent accumulation risks for different portfolios

What would you classify as an accumulation?

� What does ‘common dependent cause’ mean?

� Is the risk covered elsewhere in your capital?

Risk Accumulation?

Pandemic Yes for Travel, other Accident/Health

covers

Common lack of understanding in a profession

Yes for “industry” insurers

General economic downturn (e.g.

GFC)

Depends on exposures, e.g. Bank

PI&DO, LMI, Consumer Credit, Trade

Credit

Latent claims Depends on exposures, e.g. GM crops,

products using nano technology

Tort temperature Probably not

Slide 31

Case Study – Travel Pandemic

Slide 32

High Risk Areas Low Risk Areas

Asia, Africa, Eastern

EuropeFirst world countries

Number of Individuals Overseas 10,000 15,000

Assumptions

Proportion of travellers exposed to avian flu 85% 20%

Avian flu infection rates (of those exposed) 30% 30%

Mortality rate (of those contracting illness) 1.0% 0.50%

Average cost per infection 5,000 10,000

Average cost per death 30,000 30,000

Calculations

Individuals exposed to avian flu 8,500 3,000

Individuals contracting avian flu 2,550 900

Individuals dying from avian flu 26 5

Total cost of illness 12,750,000 9,000,000

Total cost of death 765,000 135,000

Total gross cost 22,650,000

Net cost needs to allow for reinsurance and policy exclusions

FIAAS 2013

Slide 33

FIAAS 2013 Agenda

Suggested dates for 2013 forums –

� 14 May

� 23 July

� 17 September

� 26 November

New grad training commences in first week of April –

� PPCI – method, mechanics and advantages / disadvantages

� Expressions of interest to [email protected]

Slide 34