Oxy Permian Tour · Avg 2017 Facilites Reduction Subsurface Engineering Longer Laterals 2018 2019...

27

Oxy Permian Tour Driving Value in the Permian September 20, 2017

Transcript of Oxy Permian Tour · Avg 2017 Facilites Reduction Subsurface Engineering Longer Laterals 2018 2019...

Oxy Permian TourDriving Value in the PermianSeptember 20, 2017

2

Forward-Looking StatementsPortions of this presentation contain forward-looking statements and involve risks and uncertainties that could materially affect expected results of operations, liquidity, cash flows and business prospects. Actual results may differ from anticipated results, sometimes materially, and reported results should not be considered an indication of future performance. Factors that could cause results to differ include, but are not limited to: global commodity pricing fluctuations; supply and demand considerations for Occidental's products; higher-than-expected costs; the regulatory approval environment; reorganization or restructuring of Occidental's operations, not successfully completing, or any material delay of, field developments, expansion projects, capital expenditures, efficiency projects, acquisitions or dispositions; uncertainties about the estimated quantities of oil and natural gas reserves; lower-than-expected production from development projects or acquisitions; exploration risks; general economic slowdowns domestically or internationally; political conditions and events; liability under environmental regulations including remedial actions; litigation; disruption or interruption of production or manufacturing or facility damage due to accidents, chemical releases, labor unrest, weather, natural disasters, cyber attacks or insurgent activity; failure of risk management; changes in law or regulations; or changes in tax rates. Words such as “estimate,” “project,” “predict,” “will,” “would,” “should,” “could,” “may,” “might,” “anticipate,” “plan,” “intend,” “believe,” “expect,” “aim,” “goal,” “target,” “objective,” “likely” or similar expressions that convey the prospective nature of events or outcomes generally indicate forward-looking statements. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Occidental does not undertake any obligation to update any forward looking statements, as a result of new information, future events or otherwise. Material risks that may affect Occidental’s results of operations and financial position appear in Part I, Item 1A “Risk Factors” of the 2016 Form 10-K.

Use of non-GAAP Financial InformationThis presentation includes non-GAAP financial measures. You can find the reconciliations to comparable GAAP financial measures on the “Investors” section of our website.

Cautionary Statements

3

• Introduction

• Value Based Development – Sand Dunes

• Solving Permian Problems

• Q&A

Agenda

4

Permian Resources• Introduction

• Value Based Development

• Solving Permian Problems

5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2Q17 CFFOAdjusted to

$40 WTI

Chemicals Midstream &Marketing

71 MboedPermian

ResourcesProduction

OtherImprovements

Cash FlowNeutral at $40

WTI

Increase inCash Flow at

$50 WTI

Cash FlowBreakeven with5%-8% Growth

at $50 WTI

$3.3 $3.5 $3.7

$4.3 $4.5

Current Dividend

$2.4

Sustaining Capital$2.3

$120 MM per $1 Change in WTI

Current Dividend

$2.4

Sustaining Capital$2.1

Cash Flow Breakeven at $50:Dividend + 5% – 8% Production Growth $5.7 $5.7

Ope

ratin

g Ca

sh F

low

($ B

n) Growth Capital$1.0

Cash Flow Neutral at $40:Dividend with Flat Production

Seminole-San Andres Acquisition + Chemicals

Pathway to Cash Flow Breakeven at Low Oil Prices

$4.5

6

Oxy Permian

• Position> 302,000 net acres associated with

11,325 wells in unconventional inventory

> Largest oil producer in the Permian Basin

• Scale> 10k mi2 3D seismic

> 130k mi2 2D seismic

> 24.5k gross operated wells

> 10k gross OBO wells

• NM Delaware Basin 290,000

• TX Delaware Basin** 150,000

• Midland Basin* * 210,000

Total ~650,000

NetAcres*

Resources Basin Development Areas

• Central Basin Platform 215,000

• New Mexico NW Shelf 150,000

• Emerging Unconventional 50,000

• Continuing Evaluation 335,000

Total ~750,000

NetAcres*

Other Resources Unconventional Areas

• Resources – Unconventional Areas 1.4• Enhanced Oil Recovery Areas 1.1

Oxy Permian Total ~2.5MM

NetAcres*

Business Area Acreage

Permian Resources Acreage Permian EOR Acreage

NM Delaware Basin

TX Delaware Basin

Midland Basin

Central BasinPlatform

New Mexico NW Shelf

*Includes surface and minerals.**Adjustment for transactions of 13,000 net acres announced 6/19/2017 where Oxy divested non-strategic acreage in Andrews, Martin and Pecos Counties and added incremental acreage in a new development area in Glasscock County.

2Q Permian Resources Transactions** (13,000)

Updated Resources Basin Acreage ~637,000

7

Shaping Competitive Advantage

Full Cycle Value CapabilityResources – Dynamic Development

EOR – Reservoir Management

Advantage:

• Scale + Position

• Value Based Development

• Organizational Capability

• Technology + Innovation

Reservoir Management

Operational Efficiency & Speed

Subsurface Technical Excellence

Field Development Planning + Execution

Enhanced Recovery

8

Permian Resources• Introduction

• Value Based Development

• Solving Permian Problems

9

Oxy’s Competitive Advantage in Permian Unconventional

Subsurface Characterization

3D Modular Development

Development Scenarios

Vision Well Manufacturing Blueprint

Portfolio Decisions

Hands-Free Operations

Leadership in Full Cycle Returns

Automation and Data CaptureSystem Integration

Data Analytics

Organization Designed for Integrated Development

Valu

e B

ased

Tech

nolo

gy +

Dev

elop

men

t Sys

tem

Inno

vatio

n

10

Subsurface Characterization Adds Value• Extensive subsurface

characterization & expertise> Seismic integration

> Data acquisition

> Models

• Customized desings based on unique subsurface attributes> Sweet spots

> Frac barriers

> Landing zones

• Capture resource potential at the highest value

Schematic Representation of 2nd Bone Spring Sand Well Placement

2nd Bone Spring Net Sand Thickness and Middle Carbonate Outline

Seismic Interpretation of Middle Carbonate Inside 2nd Bone Spring Sand

A

A A’

Landing + Stimulation + Spacing Optimization

A A’

A’Middle Carb. Outline

11

Production drivers

Data analytics

Implement

Surveillance

Vision Well

Design the system

Challenging the Vision Well Adds Value

• Discover recipe for play-leading wells

• Apply data analytics to identify production drivers> Subsurface

> Completion Design

> Choke and lift optimization

• Design the system to test hypothesis

• Implement and confirm results

• Continue to push expectations

*Normalized to 4,500 ft

Customized Vision Wells Increase Well Productivity

2nd Bone Spring Productivity Improvement2nd Bone Spring Landing and Frac Optimization

0

20

40

60

80

100

0 10 20 30 40 50 60

Cum

ulat

ive

Oil

Prod

uctio

n M

bo

Normalized Day

2nd BS Carbonate – Recent 7,500’

2nd BS No Carbonate – 4,500’

2nd BS Carbonate – 4,500’

13

Modular Development Adds Value• Maximize value through optimizing

pace and sequencing

• Identify Uncertainties: > Variability of production results

> Rate of improvement

• Recognize Current Limitations> Existing infrastructure capacity and water

network

> Land position

• Realize full cycle returns through modular field development plans

1

Mature land position Bench delineation Advanced BLM permitting Fewer unknowns

14

Modular Development Adds Value• Maximize value through optimizing

pace and sequencing

• Identify Uncertainties: > Variability of production results

> Rate of improvement

• Recognize Current Limitations> Existing infrastructure capacity and water

network

> Land position

• Realize full cycle returns through modular field development plans

2

Land unitization complete Appraisal wells complete Optimized well designs Infrastructure sized for plan New technologies

implementable Detailed operations blueprint

15

Modular Development Adds Value• Maximize value through optimizing

pace and sequencing

• Identify Uncertainties: > Variability of production results

> Rate of improvement

• Recognize Current Limitations> Existing infrastructure capacity and water

network

> Land position

• Realize full cycle returns through modular field development plans

12

3

4

Land core-up completed Learnings from other

development units applied Vision wells maximizing value Infrastructure optimized

Optimizing Development Scenarios Adds Value

Time

Net Present Value

Vision ValueVision wells

Acreage improvements

Initial ValueAppraisal and SSC

Optimized InfrastructureBalance infrastructure capacity and pace

Modular DevelopmentPace to implement learning and technology

Optimized Well DesignProductivityWell costLift design

Hands Free OperationsHigher operabilityLower OPEX

• Scale + Position

• Value Based Development

• Organizational Capability

• Integrated Technology

Oxy’s Competitive Advantage

Optimized Pace + Sequencing =

Leadership in Full Cycle Returns

17

Permian Resources• Introduction

• Value Based Development

• Solving Permian Problems

18

Solving Permian Problems Now

• Data Analytics> Driving value @ the Bit

> Driving value @ the Reservoir

> Driving value @ the Well

> Driving value @ Field Development

• Subsurface Characterization with Data Analytics> Identify production drivers

> High-grade inventory and improve field development plans

• Oxy Drilling Dynamics with Analytics > Better wells faster

• Logistics Hubs> Integrated partnerships with service contractors

> Protect margins

20

Permian Resources Wells Continue to Improve

Top Peers is average of Peers in the Top 15 based on # of wells online in 2016 with 6 month cumulative production available.Oxy and Peer data sourced from IHS Performance Evaluator, Gas Equivalent calculated at 20:1, solid bars represent oil, grey bars represent gas

New Mexico Bone Spring

New Mexico Wolfcamp

Texas Delaware Wolfcamp

Midland Basin Wolfcamp

AVG Lat Length (ft) 4,169 4,937 5,174 ~6,000 4,849

AVG Lat Length (ft) 4,576 ~6,700 5,158 AVG Lat Length (ft) 6,700 7,457 7,467 ~8,200 7,907

AVG Lat Length (ft) 4,807 5,418 ~7,500 5,938

*Operators Include: Bopco, Bta Oil Producers, CVX, CXO, DVN, EOG, Fasken Oil And Ranch, GMT, LGCY, Mewbourne, MTDR, Regeneration Energy, WPX, XEC, XOM

*Operators Include: APA, APC, BHP, CDEV, CXO, EOG, FANG, HK, Mewbourne, MTDR, RDSA, REN, RSPP, WPX, XEC

*Operators Include: APA, CVX, CXO, ECA, EGN, END, EPE, FANG, LPI, PE, Permian Rscs, PXD, RSPP, SM, XOM

*Operators Include: Bc Opg, COP, CXO, DVN, EOG, Mewbourne, MTDR, WPX

0

50

100

150

200

2015 1H16 2H16 2017Target

Top Peers2016

0

50

100

150

200

250

2015 1H16 2H16 2017Target

Top Peers2016

0

50

100

150

2015 1H16 2H16 2017Target

Top Peers2016

020406080

100120

2015 1H16 2H16 2017Target

Top Peers2016

6 M

onth

BO

E Cu

mul

ativ

e Pr

oduc

tion

6 M

onth

BO

E Cu

mul

ativ

e Pr

oduc

tion

6 M

onth

BO

E Cu

mul

ativ

e Pr

oduc

tion

6 M

onth

BO

E Cu

mul

ativ

e Pr

oduc

tion

21

0

2

4

6

8

10

12

14

16

18

20

-

50

100

150

200

250

300

2017 2018 2019

Prod

uctio

n (M

boed

)

Multi-Year Permian Resources Growth

Rig

Cou

nt

20% 3-yr CAGR

30% 3-yr CAGR

Base rig count* Upside rig count*

6

8

8 8

1314

STX SaleRe-invested

13 rigs at exit

2017 Exit rig count*

Current trajectory of 30% CAGR

• Exited 2Q with 11 operated rigs> 26 wells online in 2Q17

• Exit 2017 with 11 company operated rigs, 2 net non-op rigs> Avg lateral length 7,400 in 1H17 to 7,900

in 2H17

> 2017 wells online ~130

• Shifting activity to New Mexico> 5 NM rigs in 2H 2017

> 7+ NM rigs in 2018+

> 1 net non-op rig in 2018+

Achieving Plan Through Value-based Approach

*Includes estimated net non-operated rigs

22

0

500

1,000

1,500

2,000

2,500

3,000

4Q16 <$50 BE Drilled 1H17 DemonstratedCapex

Efficiency

DemonstratedWell Performance

LandImprovement

EvaluatedNew Acreage

2Q17 <$50 BE

Added 400 Hz Locations <$50 BreakevenReached <$50 inventory additions goal since 4Q16

• + 400 locations YTD

• + 3.5 MM feet of total horizontal lateral

• Increased <$50 average length from 8,400’ to 8,600’

• Cost and well performance improvements are sustainable

• Executed 7,000 net acres of trades to enable longer laterals

• Evaluated ~15,000 net acres of new development areas

2,500

2,855

16 years of inventory <$50 breakeven with 10 rigs

Midland Basin

Texas Delaware

Basin

New Mexico

Delaware Basin

Breakeven defined as positive NPV 10

Und

evel

oped

Dril

ling

Loca

tions 45

155 45100

100

23

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Breakeven <$50

Breakeven <$60

Breakeven <$70

AdditionalInventory

2Q17 Normalizedto 7,100'

4Q16

Added ~20 Rig Years of Activity to <$50 Inventory

2,855

4,250

5,725

11,325 11,650

Permian Resources Inventory 2Q17• + 400 locations BE <$50

> ~300 in New Mexico

> Replaced inventory from divestitures

• + 3.0 MM ft of horizontal lateral footage to inventory

> Increased average lengthfrom 7,100 ft to 7,500 ft

Midland Basin

Texas Delaware

Basin

New Mexico Delaware

Basin

*2Q 2017 increased lateral length adjustment to normalize current inventory to 7,100’. **Breakeven defined as positive NPV 10

11,963*

Und

evel

oped

Dril

ling

Loca

tions

24

2015 & 2016Avg

2017 FacilitesReduction

SubsurfaceEngineering

LongerLaterals

2018 2019

*Calculated using estimated total year capex (drilling, completions, hookup, facilities, infrastructure, capital workovers, maintenance, seismic). Annual wedge represents the new production added in each year from the capital program (excludes base production)** Other capex includes seismic, science, and maintenance capex.

Permian Resources Capital Intensity Improves through 2019

All-In Capital IntensityAnnual Capex $MM / Annual Wedge Mboed*

$54MM

$33MM2018 & 2019

$27MM – $23MM

• 2017 to 2019 – Value-based Development reduces capital intensity

> Facilities, infrastructure and other** 23% to <15% of

capital budget

> New Mexico wells ~30% to ~55% of total well count

> Effective lateral length from 7,700 ft to 8,600 ft for wells

drilled

• Future intensity improvement opportunities

> Well productivity

> Additional capital efficiency

> SL2 in secondary benches

> Maintenance & logistics hub

> Water recycling

10% improvement in well productivity or capital costs reduces capital intensity by $2MM

$42MM

2H 2017 Rig Ramp

Subsurface Characterization

25

The Permian Drives Oxy’s Value Proposition

Development Cost Opex G&A Production Taxes Cash Costs

$16 - $19/BOE

Note: Estimated future project costs.

Improving top tier margins with recent operational and technical breakthroughs.

$6 - $12/BOE

Development Cost Opex G&A Production Taxes Cash Costs

$6 - $10/BOE

$18 - $25/BOE

Permian EOR provides stable, free cash flow with minimal base decline.

~11,650 Undeveloped Drilling Locations ~2B Bbls Identified Undeveloped Resource

Permian Resources Permian EOR

26

Seminole-San Andres Further Strengthens Our Leading Position in EOR

*Source: 2014 Oil & Gas Journal, EOR Survey, adjusted for recent Oxy EOR acquisition

Occidental

Kinder Morgan

DenburyChevron

Exxon Anadarko

Whiting

Resolute

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 5 10 15 20 25 30 35 40

Inje

ctio

n W

ells

CO2 Projects

Gas EOR Projects*

$0

$100

$200

$300

$400

$500

$600

$700

Base Case Target Upside Case

Value of Operating Cost Synergies ($MM PV10)

$5/Boe

$7/Boe

$10/Boe

• Seminole-San Andres is now our largest operated CO2project in the Permian

> San Andres reservoir is world-class

> Oxy now operates 34 CO2 projects in the Permian Basin

• Scale in the Permian provides operating cost savings and production reliability opportunities:

> Base case savings ($5/Boe): improved well maintenance, automation, and commercial scale for supply chain and logistics

> Target savings ($7/Boe): improved plant reliability

> Upside savings ($10/Boe): asset performance at parity with our Denver Unit

• Additional opportunities: D&C cost improvement, plant expansion to accelerate growth, and re-drill and ROZ potential

Production Volumes

27

0

500

1,000

1,500

2,000

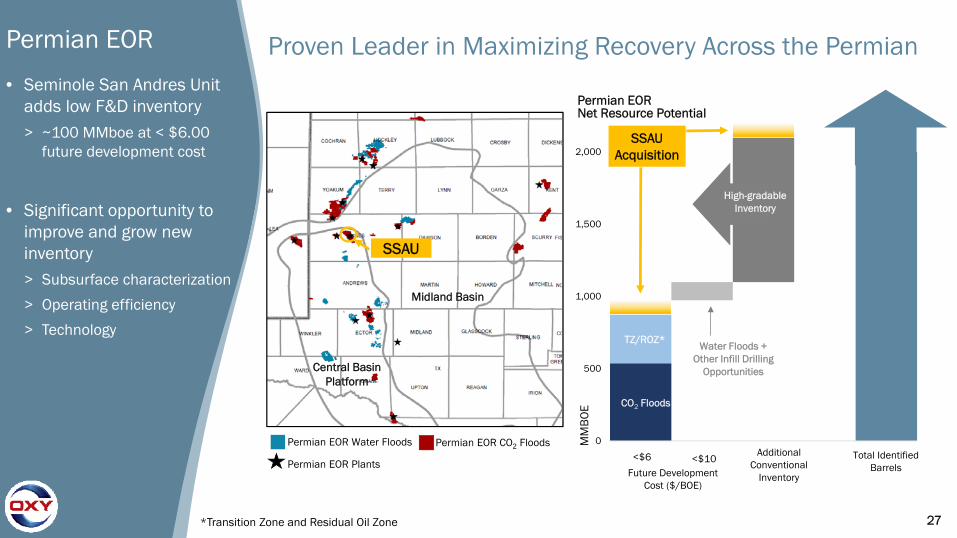

Proven Leader in Maximizing Recovery Across the Permian

<$10 <$6

Permian EOR Net Resource Potential

MM

BO

E CO2 Floods

TZ/ROZ*Water Floods +

Other Infill Drilling Opportunities

High-gradable Inventory

*Transition Zone and Residual Oil Zone

Permian EOR

• Seminole San Andres Unit adds low F&D inventory> ~100 MMboe at < $6.00

future development cost

• Significant opportunity to improve and grow new inventory> Subsurface characterization

> Operating efficiency

> Technology

Future Development Cost ($/BOE)

Permian EOR Water Floods

Midland Basin

Central BasinPlatform

Additional Conventional

Inventory

SSAU Acquisition

Permian EOR CO2 Floods

Permian EOR Plants

SSAU

Total Identified Barrels